| 2021 | 2022 | ||||||

| Price: | 15.19 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 40 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 624 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | -33 | EBIT | 0 | 0 | |||

| TEV (in $M): | 591 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- deSPAC

Description

Aersale

Summary: AerSale is a company in the aviation aftermarket space taken public via SPAC. The company’s cofounders are calling the current aviation aftermarket environment “sale of a lifetime.” By investing in AerSale, public shareholders are essentially investing in the distressed aviation aftermarket through a proxy of industry veterans with a established track record. The company’s balance sheet is in pristine condition and has ample liquidity to take advantage of the current market condition. The stock is currently reasonably valued and has several catalysts that can push the company’s earnings higher. However, this small-cap company has a thin float so getting a big block of shares is difficult.

AerSale Brief history

From 1997 to 2008, Nicolas Finazzo and Robert Nichols served respectively as the CEO and COO of AeroTurbine, a supplier of aircraft and engine products and MRO service provider. The duo sold the company to AerCap in 2006 and cofounded AerSale in 2008. In Aersale, Finazzo takes the roles of Chairman,CEO, and Division President of TechOps while Nicolas serves as Executive Vice Chairman and the Division President of Asset Management Solutions. They filled the management team with veterans from the industry. With an average of 25 years of experience, the executive leadership team has been through 3 industry cycles and wide-ranging business conditions.

SPAC Merger

Monocle Acquisition Corporation completed its IPO on February 11, 2019 for $172.5 million along with a private placement raise of $7.2 million at $10.00 per unit. The SPAC looked for a growth company with proven management team and a high barrier to entry in the aerospace & defense industries. An initial business combination agreement was reached in 2019 but COVID delayed the closing. Monocle revised the combination agreement with AerSale on Sep 8,2020 and asked for shareholders’ merger approval. However, Monocle postponed the approval meeting. Later company filings showed that Monocle redeemed most of its shares at 10.26 and issued new shares in a private transaction at price below 10/share. The combination was then approved on Dec, 2020 - AerSale finally became a publicly listed company.

Business Overview

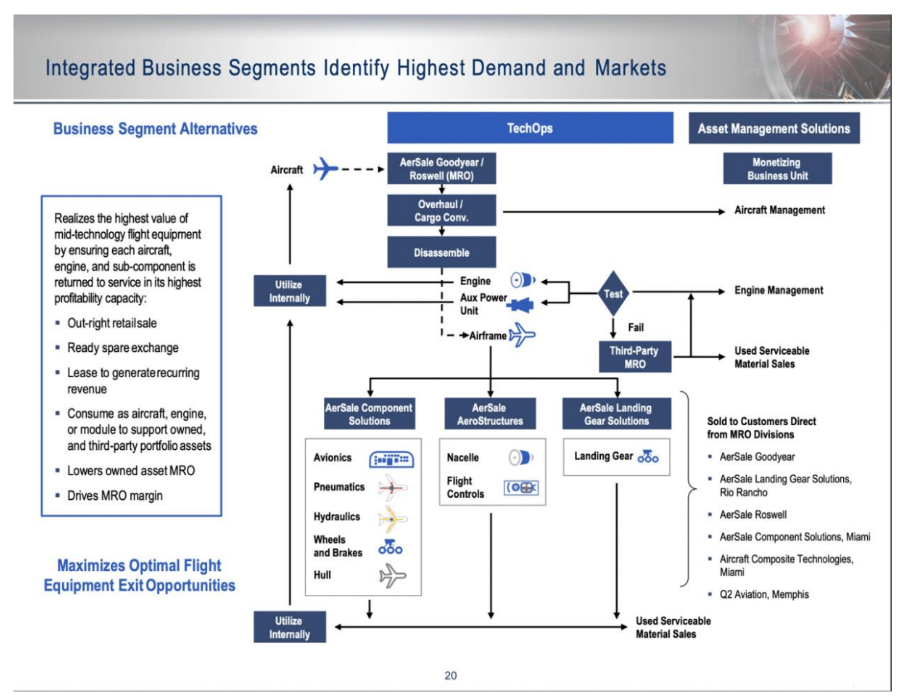

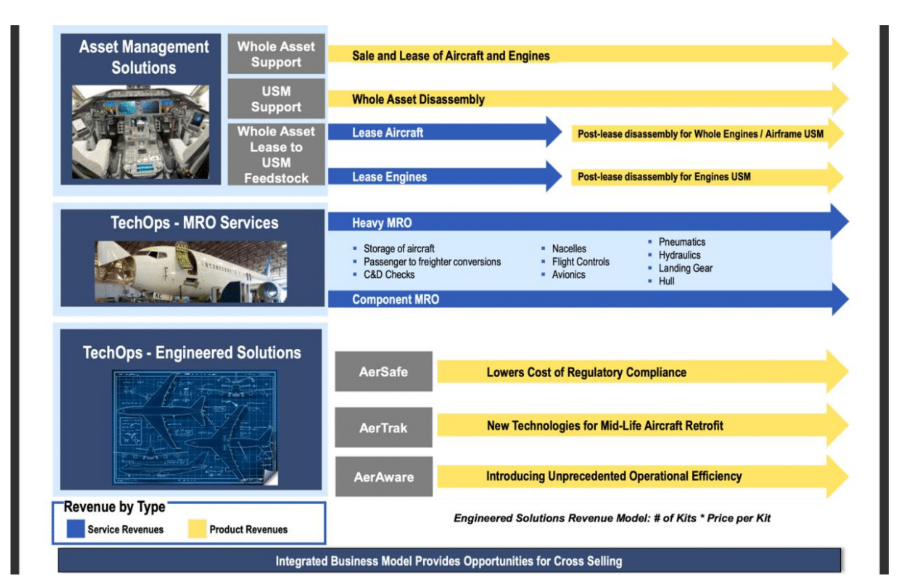

AerSale participates in the commercial aviation aftermarket. The Asset Management Solutions division purchases whole aircrafts and engines at prices that meet the company’s IRR hurdle rate in the aftermarket. It monetizes these assets by offering either hybrid power-by-the-hour highly customized leases of aircraft that garner above-market lease rates or outright sales. At the end of their leases, these aircraft will become the feedstock for the USM(Used Serviceable Materials) parts business, providing the final revenue stream in the company’s value-extraction methodology. The TechOps group consists of MRO(maintenance, repair, and overhaul) services and Engineered Solutions. It performs heavy maintenance and passenger-to-cargo conversions on aircraft at AerSale’s two MRO facilities in Goodyear, AZ and Roswell, NM. In addition, the company overhaul landing gear, components and aero structures at our facilities in Rio Rancho, NM, Memphis, TN and Miami, FL. Besides repairing flight equipment, this group also develop highly specialized products at that comply with regulatory mandates and/or enhance the safety of commercial aircraft.

Core customers and the value AerSale provides

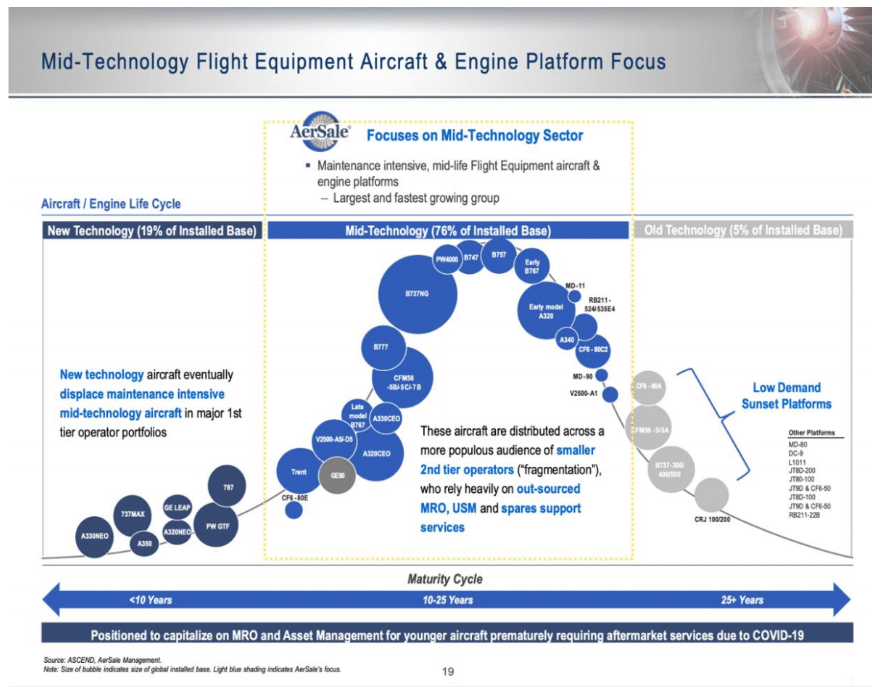

AerSale’s core customers are 2nd tier operators who rely heavily on out-sourced MRO, USM and spares support services. USM parts typically cost 30% less than new OEM parts. These customers operate mid-technology planes that are 10-25 years old in need of intensive maintenance. Airplanes in this age group make up the largest and fastest growing segment among all airplanes. To these customers, AerSale is an one-stop shop that offers an integrated solution including lease, MRO,USM services, and asset management/disposal. Once AerSale acquires a new customer that initially only employs one of its services, the company cross-sells to the customer its other offerings, enabling AerSale to achieve higher margins than its competitors, and provide enhanced value to its customers.

Why invests in AerSale now?

1). “Sale of a lifetime”

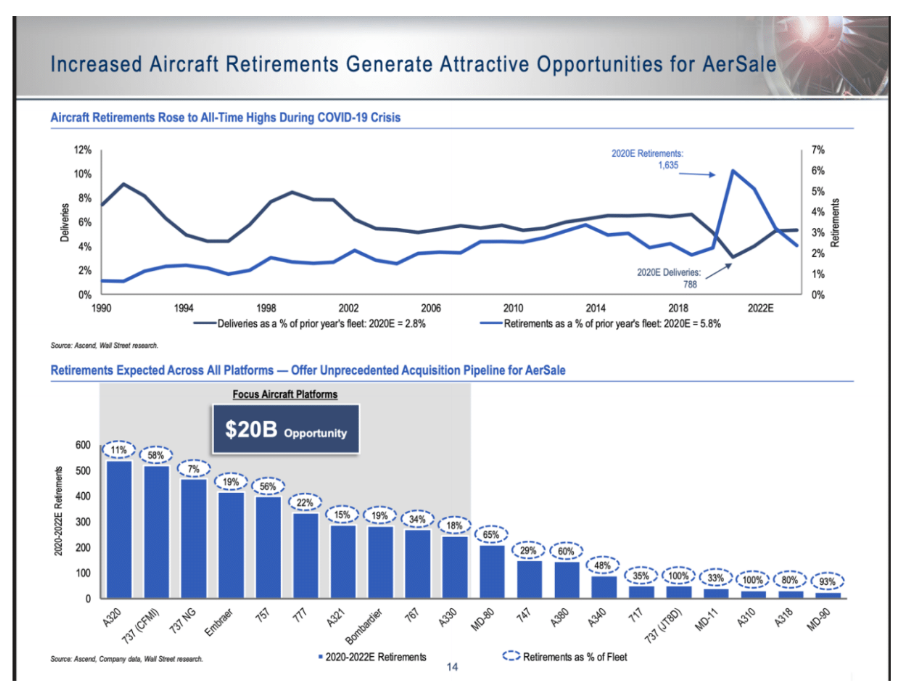

Aviation industry was one of the sectors impacted the most by the COVID pandemic. Airlines are bleeding cash and looking at all options to cut cost and stem cash outflow. Planes are either stored away or sold at depressed valuation. For companies like AerSale that operate in the aftermarket this is an excellent opportunity to acquire assets at very attractive prices. AerSale cofounders have called the current market condition “sale of a lifetime.” As CEO Finazzo explained on a Zoom presentation with investors, similar to many other markets, deep troughs follow high market peaks in the aviation aftermarket. While the average aviation cycle usually lasts about 7 years, the last super cycle before COVID lasted 11 year, pushing asset prices to record high. What followed the highest high is the lowest low as a result of COVID. Aircraft retirements is forecasted to grow from an average of approximately 600 retirements annually, to approximately 2,000 aircraft forecasted for 2020. In total, an estimated 4,000 are now expected to be retired between 2020 and 2024. This is the first time after a long while that aircraft retirement will outnumber aircraft acquisition.

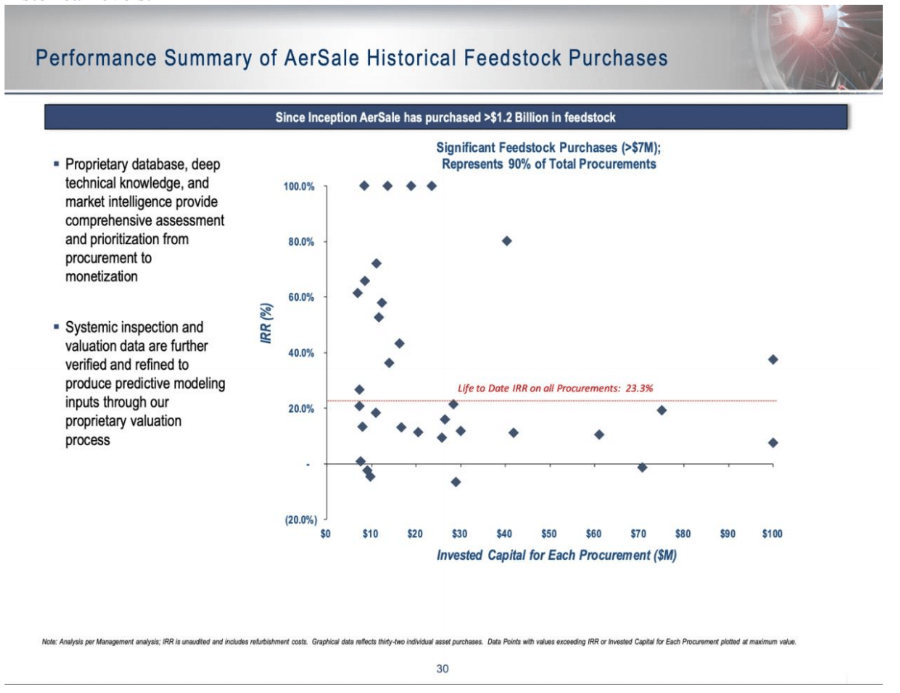

AerSale has been a very displined and return-focused company. It went on an aircraft buying spree after the 2008 financial crisis at very attractive prices. As the cycle turned and asset prices rose, the company curtailed asset purchases and had been patiently waiting for the next opportunity. Historical data show that the average return on AerSale’s purchase is 23% IRR with a bidding success rate of 12%. During the current trough, the company has already identified $20B worth of aircraft asset to bid on. To hit the company’s 2024 earnings target, the company only need to win 2% of the bids or 1/6 of the historical success rate. I think the company’s 2024 guidance is extremely conservative as it has a lot more firepower than the earmarked 400m and IRR could be considerably higher as the prices are much lower than normalized historical levels.

AerSale also has a big edge on bidding because it has much better access to information on the assets than many other potential bidders. Many sellers of assets are AerSale’s customers who currently store these assets on AerSale’s facilities, giving AerSale “first-dip” aircraft buying opportunities. AerSale is deeply knowledgeable about the conditions of the aircrafts it services while other bidders have to travel to AerSale’s site and make hasty inspections before the bidding starts. Furthermore, buying aircraft on-site provides a significant logistical savings advantage.

2). Further expansion into the cargo market

E-commerce volume spiked worldwide in 2020 and the shift to online purchase is expected to continue post COVID. This recent New York Times article (https://www.nytimes.com/2021/01/12/business/air-cargo-airports-amazon.html) illustrated the rapid growth of air cargo business. Cargo volume was up 30% for both Amazon and UPS in 2020. From the current air cargo volume of 12 million tons, "Federal analysts project that air cargo will reach 45 million tons annually by midcentury. But executives at big air shippers, airports and airplane manufacturers say that the pandemic altered online commerce so substantially that the industry will hit that mark a decade sooner."

AerSale’s CEO talked about the sustained strong demand in cargo planes from Chinese cargo carriers and DHL. Cargo planes are the same passenger planes except that they have no seats. AerSale’s TechOps division saw a big demand increase in converting passenger airplanes to cargo airplanes. One example on the company’s presentation deck showed how AerSale’s unique integrated business model capitalized on this new opportunity. Taking advantage of the aforementioned aftermarket condition, the company acquired 24 Boeing 757-200 with Rolls-Royce RB 211-535 engines, and 16 spare engines in Sep 2020. During the call with investors, the CEO revealed that the seller sold these assets at between 30-40% of the price pre-COVID. These assets were stored in AerSale’s Roswell, NM. based aircraft MRO facility. AerSale quickly performed an on-site inspection and negotiated the purchase price with the customer. Since the planes were parked on-site, not only did AerSale save logistics expense estimated at $100K+ per aircraft, it also was able to immediately start refurbishing the plane and start sales presentation to potential customers. The potential customers were not other airlines companies but air cargo operators. It turns out that these Rolls-Royce powered Boeing 757s rank among the most preferred cargo conversion aircraft due to its low capital cost, large payload, and long range. AerSale quickly received strong interest from large-scale cargo operators to purchase up to all aircraft for conversion to freighter service. The spare engines can be purchased or leased by cargo operators to avoid costly and time-consuming engine repair. As a result of AerSale’s nimble actions, the investment will pay back in less than a year.

3). Engineering Products sale could see a breakthrough

Although sales from engineering products in the TechOps division is still insignificant, AerSale management sounded very bullish on this nascent business’ prospect. It has already developed AerSafe, a system that prevents the ignition of fuel vapors in aircraft fuel tanks. There is only one competitor for AerSafe. Similarly, AerTrak has been developed to meet the needs of air traffic control to follow aircraft equipped with a GPS tracking device, rather than using radar. Transitioning aircraft will also require these devices.

Management believes the greatest opportunity lies with AerAware, a wearable heads-up display that enables a pilot to see through adverse weather while viewing necessary flight instrumentation in his visor. This system is developed for multiple aircraft platforms. At present AerAware has only one competitor, and management believe AerAware is superior and significantly less expensive. The total addressable market is over 16,000 aircraft, on multiple platforms, and the market opportunity for these three engineered solutions exceeds $10 billion dollars. AerSale has received initial interest from a potential launch customer, a major domestic airline, that could potentially install AerAware on 250 of its 737NGs.

R&D on these products are already finished so only COGS will be expensed on sales. Margin on AerAware could exceed 50%. Management said they have put a very conservative sales estimate for the company’s engineering products - only sales of18 AerAware kits are included in 21’s guidance despite the fact that AerSale is already talking to multiple customers and one potential customer can buy multiples of the 18 kits. The first Company-owned aircraft fitted with AerAware, a 737NG, has just begun flight testing.

4). M&A

The company was able to scoop up small acquisitions at very attractive valuations. It paid for two companies at 4.6X and 5X EBITDA pre-synergy and was able to improve these two businesses and integrate them into AerSale effectively. AerSale’s growth projection between ‘21-24 does not assume any contribution from M&A. It’s likely that AerSale can find attractive M&A targets in this environment and further boosts its growth.

Ownership

The co-founders retained all their shares in the SPAC conversion and owns about 10% of the company. AerSale’s early backer private equity Green Equity Investors is the biggest shareholders of the company with an ownership of 63.5%. Public shareholders owns 9.6m or 23.6% of the company.

Company growth forecast/EBITDA/Assumption

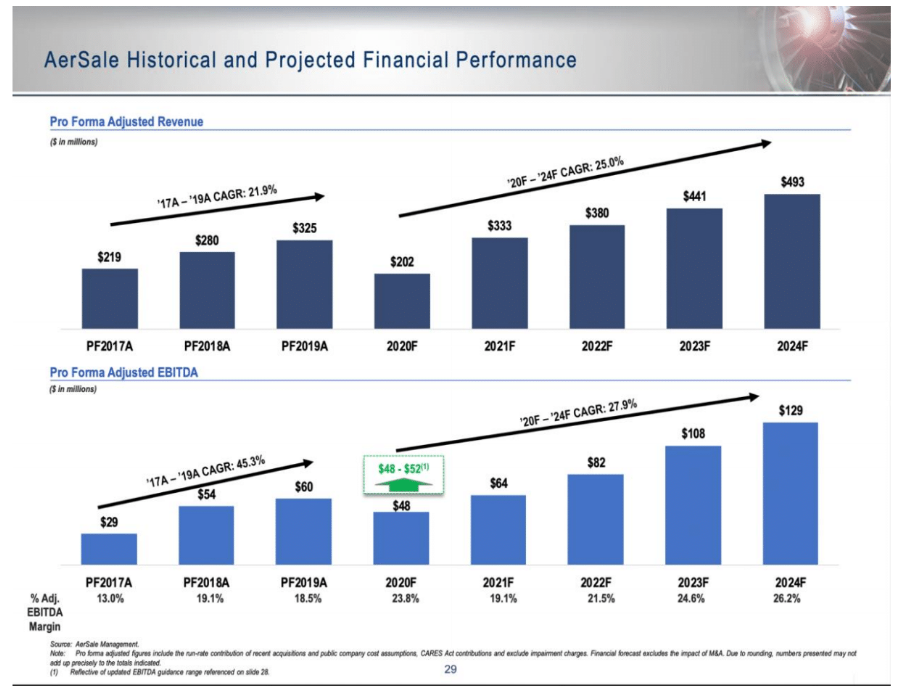

Management expects the company to grow Revenue by a 30% CAGR and Adjusted EBITDA by a 34% CAGR from 20-24. The forecast assumes that demand for passenger air travel will not reach 2019 levels until 2023. However, the company forecasts its own numbers to exceed the level of 2019 this year, 2 years earlier before the general aviation market recovers. This outperformance indicates AerSale’s superior business model and execution.

Valuation:

Comp Analysis:

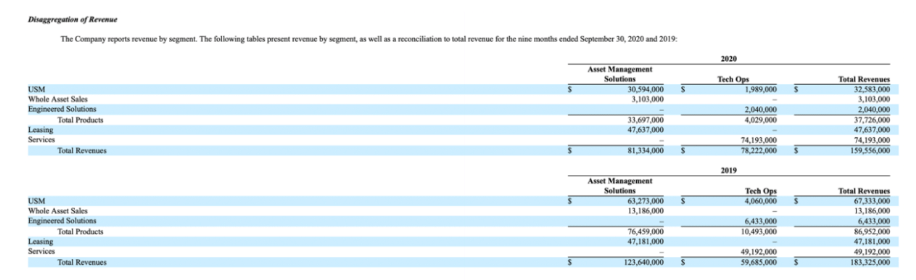

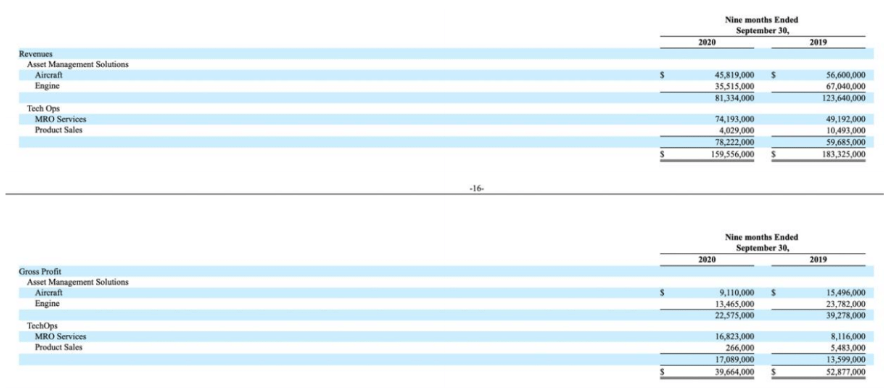

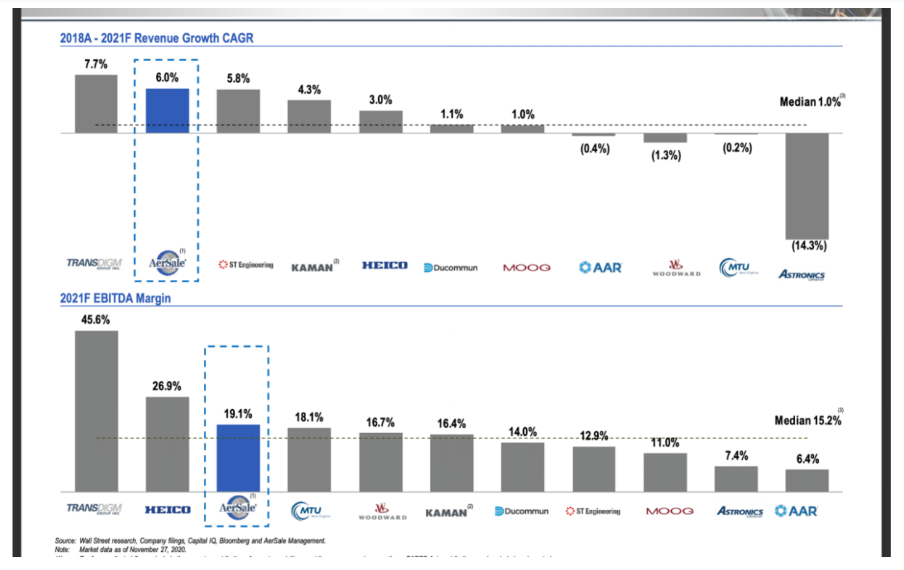

There’s really no true comp to AerSale in the public market. In the company’s investor presentation, many so-called comps are aviation equipment manufactures but AerSale is still mainly an aircraft management/service company at this point. However, it is also a different beast from pure MRO service company such as AAR: MRO related revenues from TechOps historically make up about 30% of the total revenues while the revenues from aircraft management make up the rest. It is not a pure aircraft leasing company either because the leasing revenues is only about 30% of its total revenue.

The market is very likely to misprice AerSale as a peer of AAR. During the investor meeting, the management mentioned that a very frequent question that came up from investors is whether AerSale is a similar to AAR. From the growth and margin profiles we can see AerSale has superior margin and growth compared to lots of other companies in this space including AAR. Because of the integrated leasing + servicing model, AerSale’s asset management division commands a 30% gross profit margin while AAR’s margins are in the high teens. AAR’s historical adjusted EBTIDA margin is around 7-8% and the ’21 estimate is at 6.4% vs AerSale’s 19%. Monocle founders explained the delta between AAR and AerSale’s margins is due to 1). AAR does a lot of commoditized service with high labor cost, an area that AerSale avoids; 2).AAR is a reseller that redistributes a lot of products sourced from dissemblers like AerSale 3). AAR’s acquisition strategy is less focused compared to AerSale, resulting in conglomerate inefficiencies . I believe the market will eventually rewards AerSale a higher multiple based on its profitability. If the company’s proprietary engineered solutions could really take off, we could see a re-pricing of the company that will push AerSale towards the higher multiples given to aviation equipment companies.

AerSale

AAR

Valuation:

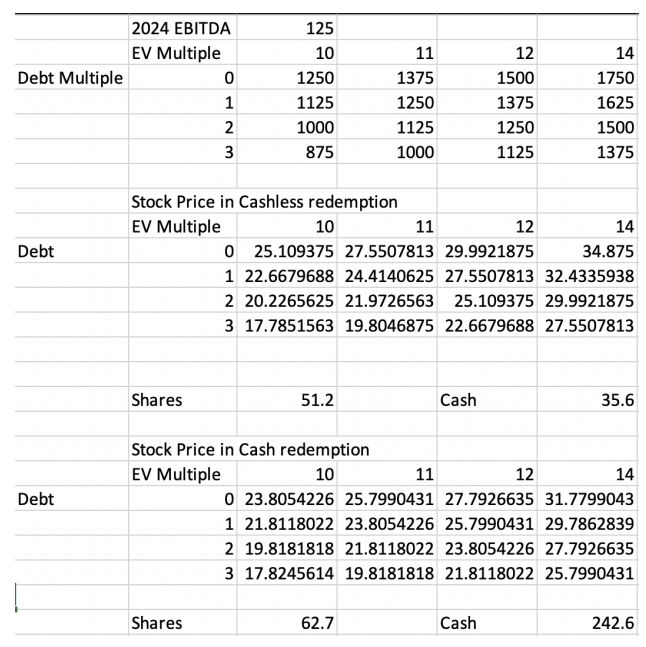

Total shares count: base count + earnout shares + warrant dilution

At closing, the company had 40.3m shares outstanding excluding 17.25m public warrants and 0.718m private warrants exercisable at the price of 11.50. There are also 3.7m AerSale founders' earnout shares and 0.7m Monocle founder earnout shares with half of the earnout shares vesting at 13.50 and the rest at 15.00. Management can force the public warrant holders to exercise their warrants once the stock price goes over 18/share for 30 consecutive trading days via either a cashless conversion or a regular redemption.

|

|

EV in a full cashless redemption scenario |

EV in a full cash redemption scenario |

|

Shares |

51.2m |

62.7m |

|

Cash |

35.6m |

242.6m |

Stock Valuation Chart

AerSale share price range in 3 yrs

The above chart shows a range of AerSale’s possible share prices in 3 years based on different EV and debt multiple assumptions. ’24 EBITDA of 125m is management’s current projection and it appears very conservative to me after attending the company’s two virtual meetings.

AerSale’s warrants are probably the best leveraged way to play this name but warrants are also very thinly traded.

Why is this cheap?

There are simply too many SPACs in the market and most investors are chasing after the hot tech SPACS over a “boring” aviation SPAC. After Monocle failed to gain approval for merger on its first try, it shrank its public shareholder base even further by redeeming most of its public shares. AerSale/Monocle is possibly forgotten,ignored, or abandoned by most investors.

Cashflow

AerSale only needs a flat minimal maintenance capital of 2m to run the business excluding feedstock acquisition. By the end of ’24, AerSale estimates it will have a total cash flow of 592m, of which 300m is ear-marked for feedstock purchase on a net basis and the rest could be used either for acquisition or possibly buybacks. Based on AerSale’s past prudent capital management history and the fact that the founders are still fully invested in the company with a sizeable 10% ownership, management is likely to be a good steward of the company’s cashflow.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

Sale of AerAware takes off

Increase conservative guidance

Attractive margin and consistent YOY grow that will eventually show up on potential investors’ radar

General aviation industry rebound

| 1 show sort by |