| 2019 | 2020 | ||||||

| Price: | 189.00 | EPS | 6.6 | 7.6 | |||

| Shares Out. (in M): | 340 | P/E | 26.5 | 25 | |||

| Market Cap (in $M): | 835 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 20 | EBIT | 0 | 0 | |||

| TEV (in $M): | 800 | TEV/EBIT | 18.6 | 17.9 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

Description

Aegis logistics is one of key beneficiaries of increasing LPG penetration in India – a key initiative by the government to promote clean fuel usage. The stock has underperformed last year along with the broader mid-cap market in India, while the larger gas distributors have had a great run of the back of number of government initiatives promoting natural gas and LPG fuel. The company is in the middle of massive capacity expansion and sorting out logistics issues, which will set it up for 20%+ volume growth for next few years. Management has historically scored very well in capital allocation and operational efficiencies, which affords comfort that the company will be able to increase utilization of new capacity at generate historical high returns on investments.

Brief company overview:

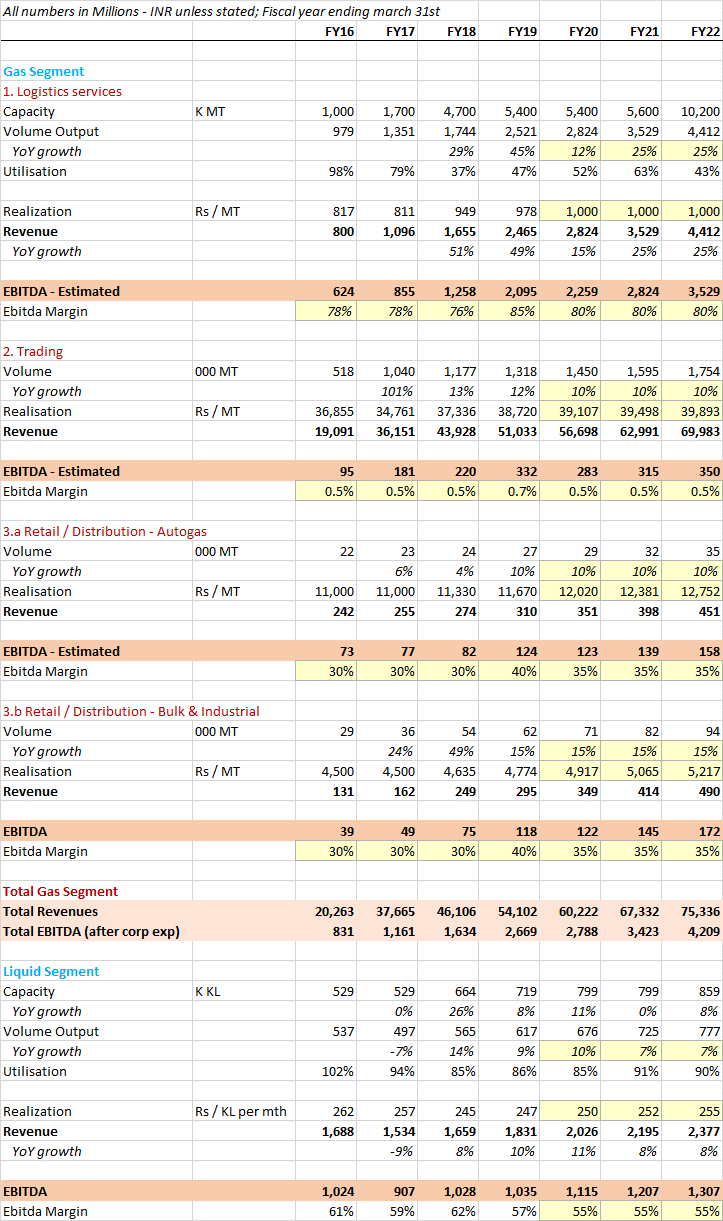

Company mainly deals with terminalling of LPG, oil products and chemical imports to the country. Business is divided into two segments, i) Gas (LPG), where it does sourcing, terminallng and distribution and generates about 75% of total EBITDA, and ii) Liquids. The earnings contribution mix has changed over the last decade and has shifted towards Gas, where the opportunity size is much larger.

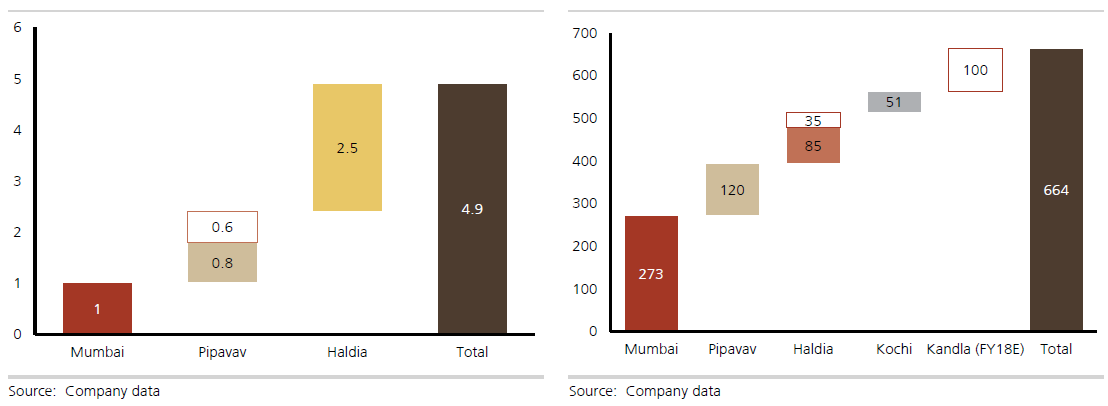

Within the Gas segment, Terminalling contributes to about 75-80% of EBITDA, while Sourcing contributes to about 10-15% (company does not provide breakup). The company has 3 LPG terminals with total throughput capacity of 5m mtpa (was about 1.35m mtpa about 2 years ago). On the Liquid terminalling side, it has terminals in 5 locations with total capacity of 664k KL.

Gas Terminalling:

Current terminalling capacity is 5m mtpa and the segment is the cash cow of the company. The company had last added 2.5m mtpa capacity in Haldia in Dec 2018 (with HPCL as anchor customer with 20 year MOU). Company is expanding its terminalling capacity by another 4m mtpa by adding a new facility in Kandla port (open contracting). Post the Kandla facility commencing in FY21, company will have total throughput capacity of 9.2mn mtpa (from its capacity of 0.75mt in FY16; 12x increase over span of 5 years).

Company is extremely efficient operator and has demonstrated ability to 80+ turns per year (90-120% utilisation), versus average of 25-30x for the industry, which affords it with extremely high ROIC on its investments. Historical investment has been about Rs 1000 per ton of capacity. On this, the company generates roughly about Rs 1000 per ton of revenue and EBITDA margins is high as 80-90% at maximum utilisation, which implies ROICs of over 75%.

Gas Sourcing:

Aegis provides LPG sourcing facility for domestic OMC customers. Company entered a JV (40% stake) in 2014 with Itochu of Japan to improve its LPG sourcing capabilities. On average, Aegis makes an EBITDA of US$4.00/mt from its sourcing business. EBITDA CAGR has been over 20% for last 4 years, and is expected to continue this momentum. Company does not take any commodity price risk in sourcing LPG.

Gas Retail/Distribution:

The company has 107 automobile gas stations in seven states and the commercial distribution of LPG is via 100 commercial distributors across 45 cities in eight states.

Liquids:

Company has Liquid terminals in 5 ports (Mumbai, Pipavav, Kochi, Haldia and Mangalore). Current EBITDA contribution from this segment is about 25% of total EBITDA and has fallen sharply over the years due to the rapid growth of the Gas terminalling business. Current capacity is about 664k KL and is expected to increase to 811k KL over the next 12 months. ROIC for this segment is about 20-25%; capex required is about 100crs for 100k KL of capacity, which can generate about 30-35crs of revenue and about 20crs of EBITDA.

Investment thesis:

-

Beneficiary of structural growth for LPG demand in India. India’s current LPG demand is about 25mn mt; about 50% of this is met via imported LPG. Demand is expected to grow at 7-8% CAGR for the foreseeable future (ahead of GDP growth). Based on current domestic refining capacity, domestics LPG production will grow at 2-3% CAGR, implying imports is expected to grow much faster than the actual demand growth. Households are the major consumer of LPG (over 90%). Currently the penetration (on paper) has reached close to about 100% of the households, due to the different government schemes to promote the usage of LPG over kerosene, wood, etc as the primary mode for cooking. But though the LPG household penetration is high, the actual consumption per capita is still very low even compared to other developing markets. Government continues to strongly promote LPG as the source of clean fuel which will help increase volumes.

-

Capacity ramp up for LPG and liquid facilities will result in multi-year growth opportunity: Last fiscal year, the LPG terminalling business did a throughput of 2.5mt or about 50% utilisation (20% of imported LPG volumes).

-

Mumbai facility: The company’s 1.1mt facility at Mumbai is operating at 80% utilisation post its brownfield expansion and is extremely profitable. Recently, HPCL’s (one of the biggest OMC in India), has completed its pipeline connecting Uran-Chakan (after about 3 years of delay) and this is expected to boost the volumes for Aegis by another 0.3-0.5mt from its Mumbai terminal.

-

Pipavav facility: The other older 1.4 mt facility at Pipava is operating at sub 40% utilisation. This facility has historically operated at low utilisation due to end connection issues. After years of struggle, the company has been able to reach an agreement with the Pipavav port to construct railway gantry. Construction for the railway gantry is about to commence and is expected to get completed in the next 6-9months. Post this, the company should be able to ramp up volumes by 0.3-0.4mtpa at this facility.

-

Haldia Facility: The company has recently announced small capacity expansion in anticipation of the bottlenecks being resolved. The more recent 2.5mt facility at Haldia was running at about 30% capacity last year and is expected to ramp up to 70-80% capacity over next 3 years. Based on company’s current expansion plans, volumes can grow at 20%+ for next 5-6 years with utilisation still staying around 80%.

-

Kandla facility: this will be the company’s and India’s biggest facility. This is expected to commence in about 1.5 years. The project is on the grid of JamnagarLoni Pipeline (JLPL) and the proposed KGPL pipeline. Company’s expects investment of about 350crs and this facility should generated EBITDA of the same level at full utilisation.

-

Liquids terminalling: capacity is expected to increase by 11% over the next year from 730k KL to 811k KL.

-

Management is highly operational focused and has skin in the game. Historical track record shows that the management has been extremely prudent in terms of capital allocation. If we look at last 10 year track record of the management, earnings have grown at 23% cagr, with zero equity dilution and incremental return on last 10 year invested capital has been over 50%. While growing earnings handsomely, the management has distributed 25% of its profits in dividends. In its Gas terminalling business, company has demonstrated that it can do turns of 80x over its static capacity (versus industry standard of 25-30x. The company has recently given out ESOPs worth 5% of outstanding shares to its top management in order to retain top management. On top of this, current valuation is attractive. Stock currently trades at about 25x this year’s earnings. But given volumes are mostly likely to grow 2x in next 3-4 years, I believe the stock is underestimating the earnings upside. Most of growth capex is will be completed in 1 year and so the company will require limited capital to grow.

I and/or others I advise do not hold a material investment in the issuer's securities.

Catalyst

volume pick in gas and liquids; resolution of logistics issues at Mumbai and Pipavav

| show sort by |