| 2021 | 2022 | ||||||

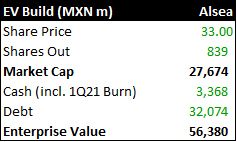

| Price: | 33.00 | EPS | 0.03 | 0.06 | |||

| Shares Out. (in M): | 839 | P/E | 47 | 29 | |||

| Market Cap (in $M): | 1,373 | P/FCF | 34 | 12 | |||

| Net Debt (in $M): | 1,424 | EBIT | 166 | 230 | |||

| TEV (in $M): | 2,798 | TEV/EBIT | 17 | 12 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- None found

- BETA

- MEXICO FUND INC MXF 06/21/2021

Description

Subject: Alsea S.A.B. de C.V. (ticker: ALSEA* MM)

Recommendation: Long

Base Case Price Target: MXN 62.86 (90% Upside)

Base Case 5 Year IRR: 30%

Recommend initiating a long-term position in Alsea with a 1-year PT of MXN 63. While exposure to Mexico and Spain has caused Alsea's performance to lag QSR peers SSS, AUV, and profit recoveries, this is more than reflected in Alsea's valuation and share price underperformance vs. peers. COVID provides a unique opportunity to own an asset with a robust organic unit growth, and EBITDA growth profile and with robust unit-level economics.

Current share price of MXN 33 implies 90% upside to 1-year PT of EUR 63 and a 30% 5-year IRR assuming a beginning of 2026 exit. The IRR Increases to 40% assuming a beginning of 2024 exit.

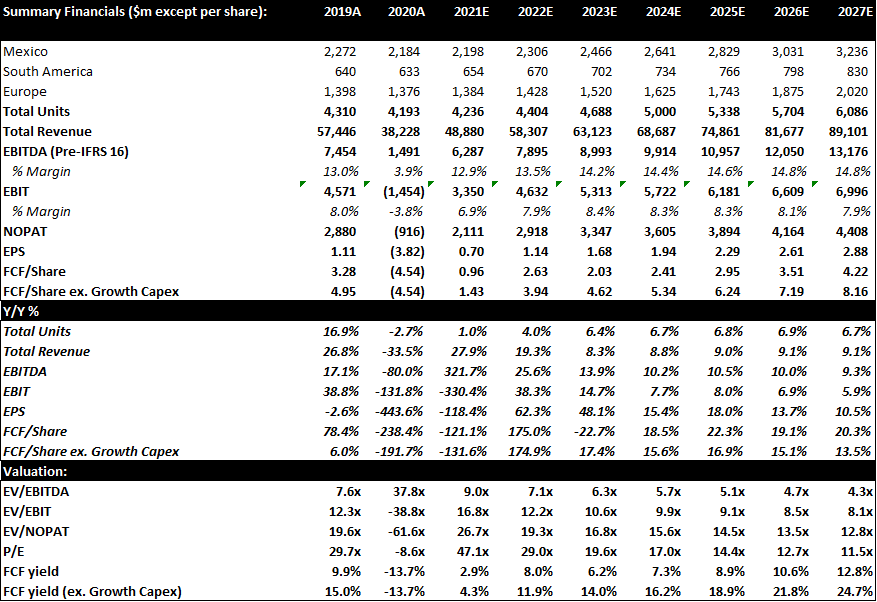

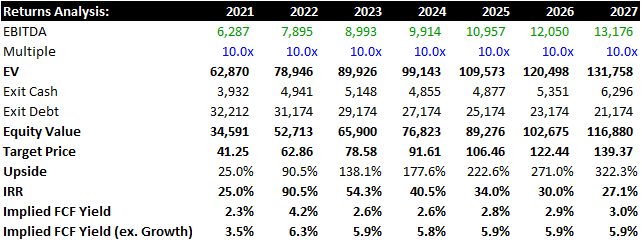

Financial Summary and Estimates

Note: Our EBITDA Estimates are on a pre-IFRS 16 Basis and Subtract out Estimated Lease Expenses

Business Overview

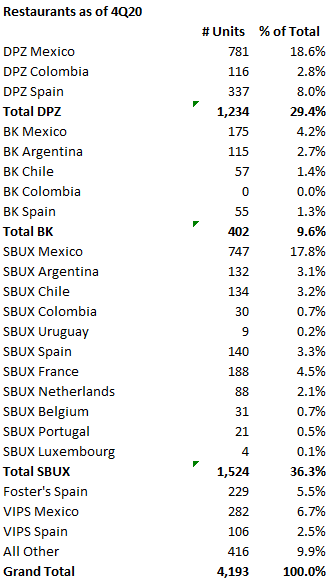

Alsea S.A.B. de C.V. (ALSEA* MM), headquartered in Mexico City, Mexico, is a franchisee as well as master franchisor of well-known American QSR brands such as Domino's, Starbucks, and Burger King primarily in Mexico, Spain, and South America. The company also owns and operates its own casual dining brand 'VIPS' and a handful of other smaller propietary brands though these are relatively insignificant from a consolidated perspective. In many of its markets, AmRest also acts as a franchisor of Domino's, Starbucks, and the company's propietary brands, collecting royalties from franchisees/sub-franchisees who own and operate the restaurants. As of their 4Q20 earnings report, Alsea owned and operated 3,284 restaurants with an additional 909 franchisee-owned restaurants. - Key competitors include: McDonald's (specifically ARCOS, the company's key Franchisee in Latin America), AmRest, KFC/Pizza Hut (and the brands local franchisees) and a plethora of local chain and mom n' pop competitors across various segments of the restaurant industry.

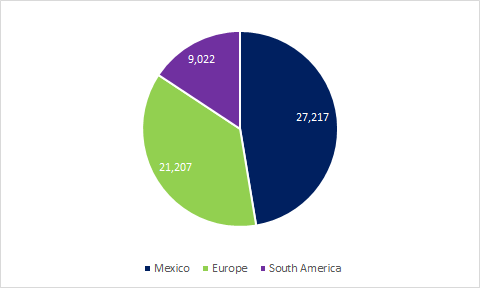

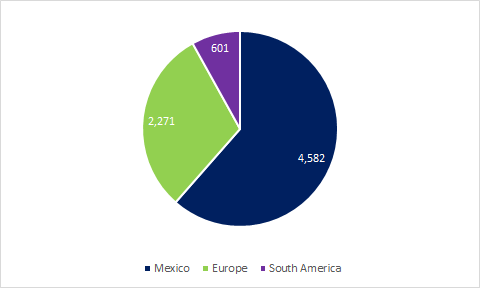

2019 Revenue Breakdown by Region (MXN m)

2019 EBITDA Breakdown by Region (MXN m)

Business Quality and Benchmarking

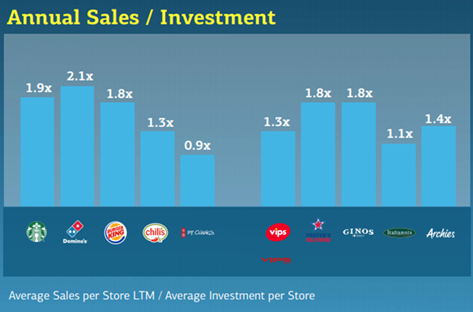

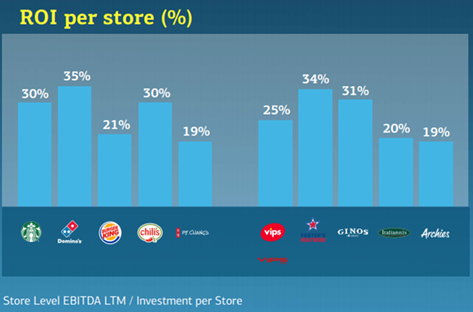

Robust Unit Economics and ROIC Profile: Prior to the company's acquisition of Starbucks European Assets as well as Grupo VIPS in late 2018 (for which the company had not yet realized synergies prior to COVID), Alsea had a strong track record of deploying incremental capital at high rates of return which led to ROIC steadily increasing from ~7% in 2014 to ~14% in 2017. Our analysis of Alsea's new-build disclosures combined with primary diligence suggests a 20%+ cash on cash return profile (~5 year payback period) for Alsea's new-builds across most brands and markets.

Alsea Pre-Tax Return on Capital

Alsea Pre-Tax Return on Incremental Invested Capital

Alsea's Disclosures Suggest a Robust Unit-Level Return Profile

Source: Alsea 2019 Analyst Day Deck

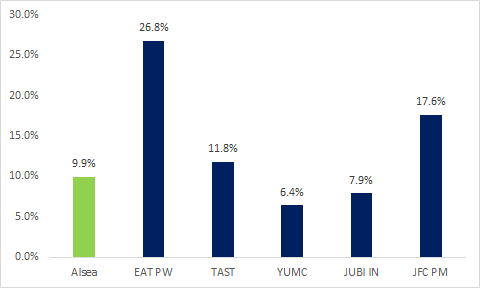

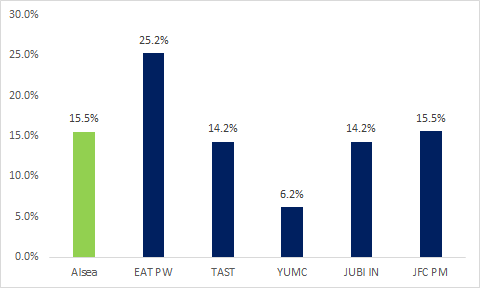

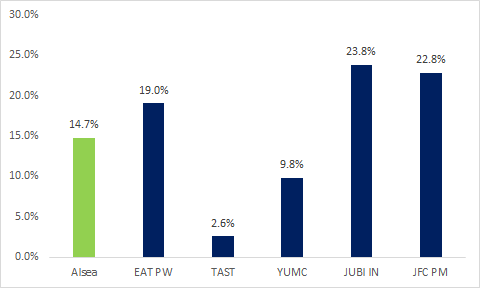

Alsea's Unit, Revenue, and EBITDA Growth are all the High End of Peers

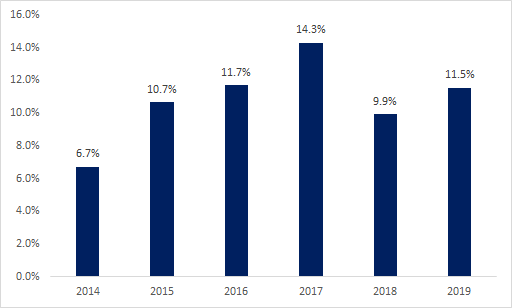

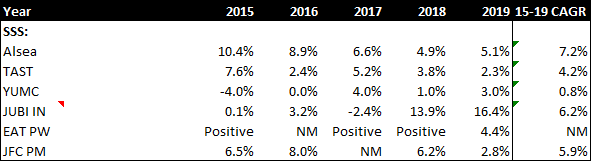

Alsea has historically had strong 15%+ top line growth and ~15% EBITDA growth (2015-2019 CAGR). Alsea's Revenue and EBITDA growth profile is near best-in-class peers whil unit growth is closer to middle of the pack. Alsea has historically also grown consolidated SSS at a ~7% rate; while this figure is somewhat inflated by the companies South America segment which includes results for the hyperinflationary Argentina market, Alsea's core geography of Mexico has also consistently had positive SSS averaging 3.3% from 2015-2019. While disclosures are somewhat limited, Alsea has historically grown organic units, revenue and EBITDA at healthy DD%+ rates for the last several years as well though this excludes 2019 where the company faced 1) a significant devaluation of the Argentine Peso, and 2) significant macroeconomic/consumer sentiment weakness in Mexico as President Trump and Mexico engaged in a tit for tat tariff exchange. As will be explored in the next section, Alsea has significant whitespace which should enable it to maintain its historic pace of rapid growth.

2015-2019 Unit Growth CAGR

2015-2019 Revenue Growth CAGR

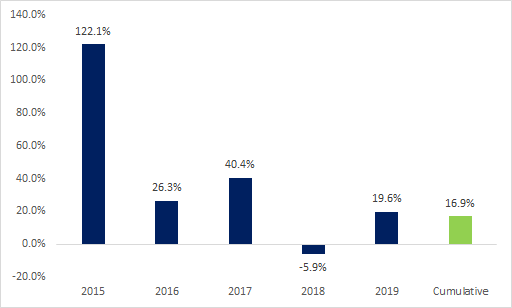

2015-2019 EBITDA CAGR

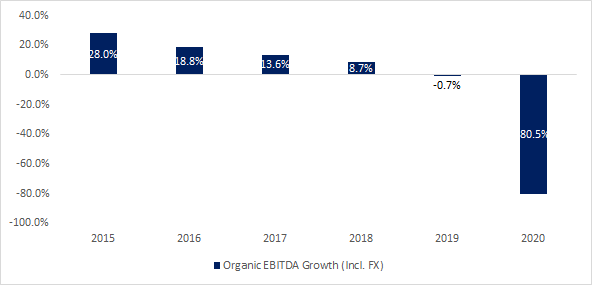

Alsea Organic EBITDA Growth was Robust Prior to 2019

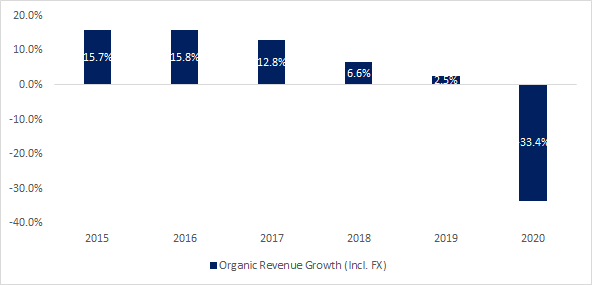

Organic Revenue Growth was Also Strong Prior to 2019

Driven by MSD-HSD% Organic Unit Growth

And MSD-HSD% SSS Growth

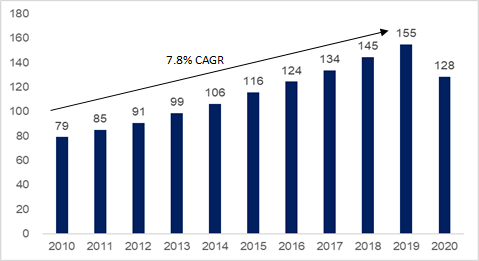

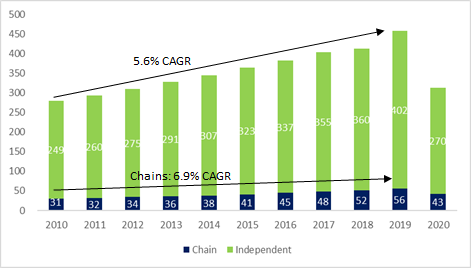

Foodservice in Alsea's core Mexican market is a strong growth industry with the opportunity for chains to continue taking share from independents in many of the segments Alsea competes in. Chains have significantly outgrown independents since 2010 (7.8% CAGR for chain consumer foodservice vs. 4.9% CAGR for total Consumer Foodservice) and yet still only comprised 16% of the total market in 2019. There is also a significant opportunity for Alsea to take share from independents in the full-service and Limited Service Pizza segments in particular. While already dominated by chains, the Specialist Coffee and Tea Shop segment has hisotrically experienced an attractive DD% growth CAGR.

Mexico Consumer Foodservice Revenue (MXN bn)

Source: Euromonitor

Mexico Chain Consumer Foodservice Revenue (MXN bn)

Source: Euromonitor

Mexico Full Service Restaurant Sales (MXN bn)

Source: Euromonitor

Mexico Limited Service Pizza Sales (MXN bn)

Source: Euromonitor

Mexico Specialst Coffee and Tea Shop Sales (MXN bn)

Source: Euromonitor

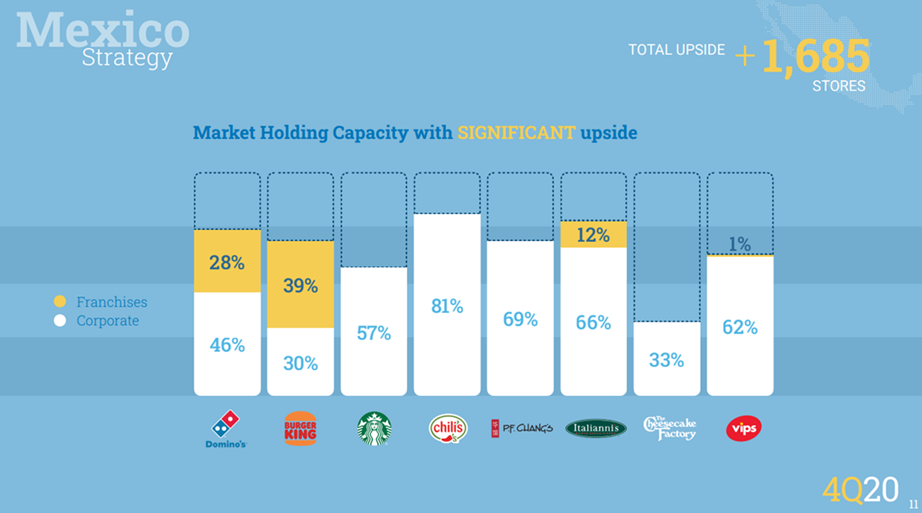

Alsea's disclosures suggest there is 'Market Holding Capacity' for another ~1,700 stores in Mexico which is equivalent to roughly 80% of the company's current footprint.

Source: Alsea 4Q20 Earnings Deck

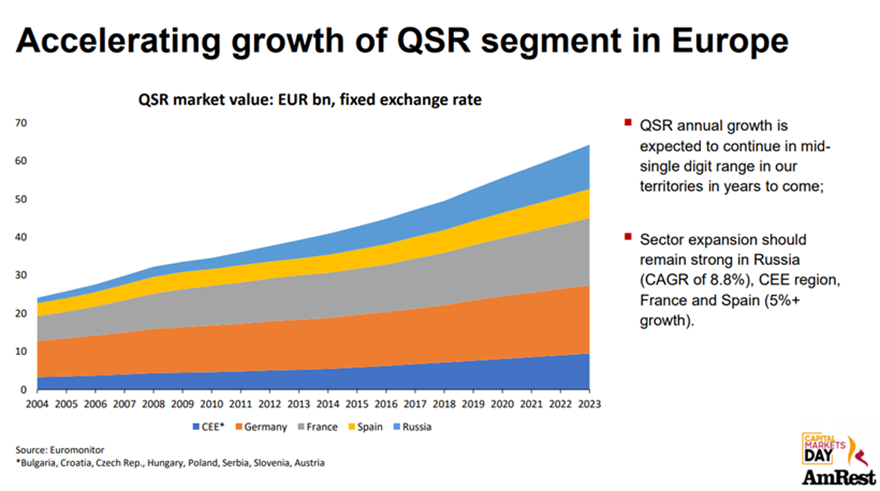

QSR in Europe is Also Significantly Underpenetrated and Alsea Enjoys an Expansive TAM Runway: Within Food-Away-From-Home, the penetration of Limited Service Restaurants significantly lags US levels further showing the opportunity for QSRs to take share.

QSR Sales in Europe are Expected to Continue at an MSD% Clip for the Foreseeable Future

Source: AmRest 2019 CMD Deck

Driven by Massive Wallet Share Opportunity for Limited Service Restaurants in Europe

Source: Aaron Allen Consultants

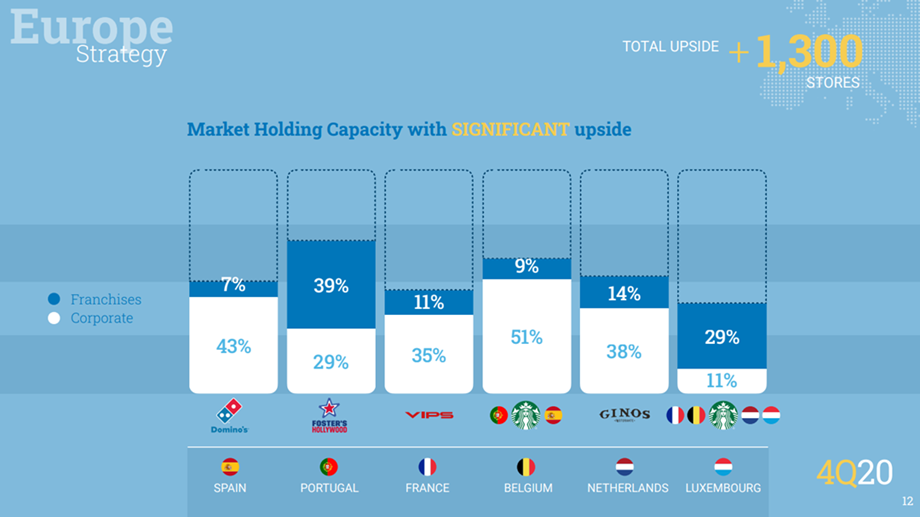

Company Disclosures suggest there is room to add another 1,300+ restuarants in Europe which is equivalent to Alsea's current European Footprint

Source: Alsea 4Q20 Earnings Deck

COVID Crisis and Opportunity

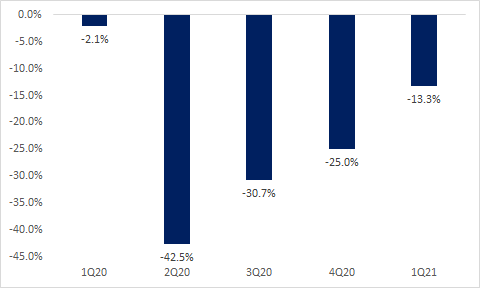

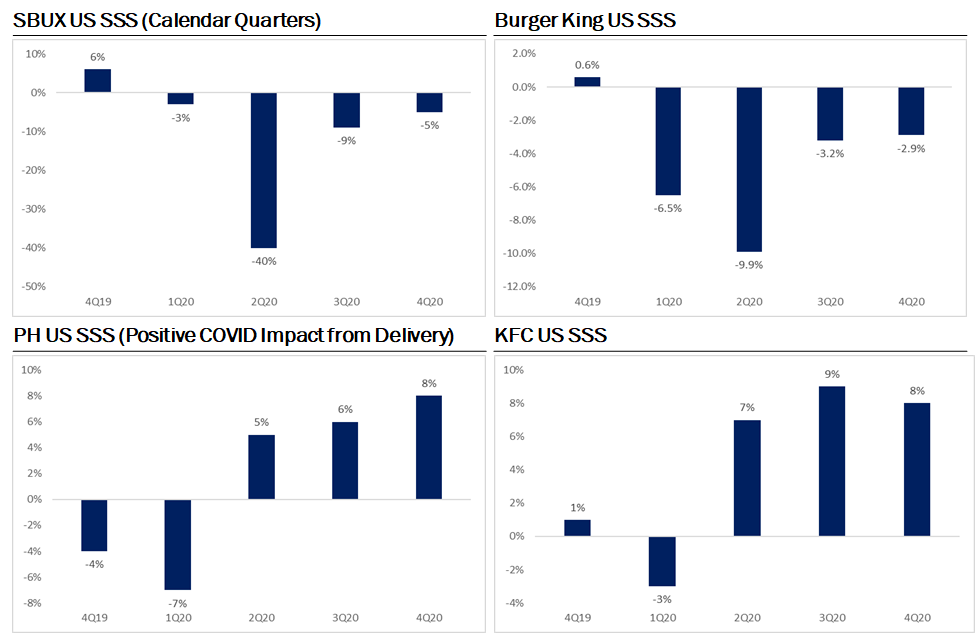

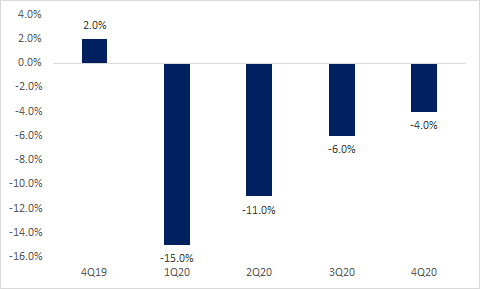

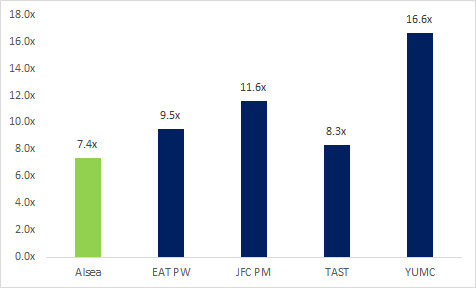

Despite robust asset quality and unit economics, Alsea has lagged peers recovery from COVID due to its exposure to Europe and Mexico which have been slower to reopen than the US and Chinese markets.The recovery in QSR Industry SSS in the US and China provide reason for optimism that once COVID restrictions are relaxed, and vaccines are distributed, the Mexican and European consumer will return to Alsea's restaurants. The relative delay in recovery is more than reflected in Alsea's valuation, which clearly assumes a multi-year recovery period to return to 2019 EBITDA. Alsea currently trades at ~7.5x EV/2019 EBITDA which is a discount to the company's historic NTM EBITDA multiple of 10x. Alsea was close to cash flow breakeven in 1Q21 (slightly positive operating cash flow with negative FCF of 275m MXN or 1% of Alsea market cap) and with the lifting of strict COVID restrictions in Europe in May, Alsea should return to positive FCF for the remainder of 2021.

Alsea SSS Recovery has Lagged Peers

US QSR Peers' SSS Have Significantly Outperformed Alsea Due to Laxer COVID Restrictions

YUMC's SSS Growth has also Outperformed Alsea

Alsea's Lagging Recovery is More Than Reflected in its Valuation Discount to Peers

Source: Company Filings and Bloomberg

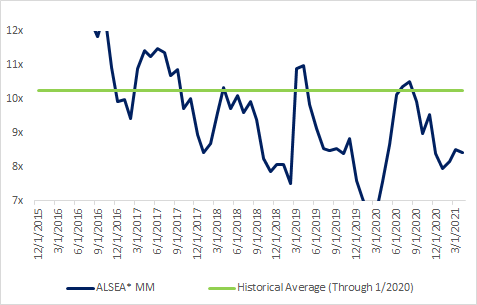

Alsea's 7.4x EV/2019 EBTIDA Multiple Compares Favorably to its Historical Average Multiple of 10x EV/NTM EBITDA

Source: Bloomberg

Despite the obvious headwind to COVID 19 on sales, the crisis has provided restaurants with a once in a generation opportunity to re-examine their cost structures and eliminate non-value-added operating expenses. This was evident in Alsea's own 1Q21 results when consolidated EBITDA margins only decreased 60 bps despite having SSS that were -13.3%. Management has closed underperforming and cash flow negative stores that will cumulatively total ~3.5% of the system in 2020-2021 and commented that they have realized permanent cost savings during COVID that should result in a higher margin profile going forward:

“So we took advantage of this by cleaning up the portfolio and closing some negative performing stores, which will translate into improved margins going on forward…And the biggest gains are going to be in Mexico, where obviously, because labor is cheaper, we were less efficient in how we structure our labor at store levels…(we) decided to close 185 corporate units…” – 4Q20 EC

Valuation

We estimate that 2022 AUVs will roughly return to 2019 levels, that 2022 EBITDA margins will also be essentially in-line with 2019 levels, and that Alsea will build ~170 net units (incl. franchised) in 2022. This leads to 2022 EBITDA of MXN 7,900m which is ~6% above 2019's MXN 7,454m (adjusted for 1x gain on sale).

A future share price analysis results in a 30% Base Case 5-Year IRR assuming the Alsea investment is exited at 10x EV/NTM EBITDA in the beginning of 2026 or a 90% IRR/total return assuming a beginning of 2022 exit at 10x 2022 EBITDA. IRR math assumes the investment is entered into at the beginning of 2021.

Alsea Historically Traded at an Average Multiple of 10x NTM EBITDA

Source: Bloomberg

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

As the current vaccination campaigns in Europe and Mexico continue, we expect an easing of restrictions and improvement in consumer sentiment this summer which should lead to improved sales and cash flow for Alsea and a re-rating in the share price. While Mexico has had some issues securing supplies of vaccines, press reports suggest that the US will prioritize Mexico and Canada for shipment of it's excess vaccine supplies.

| show sort by |