| 2016 | 2017 | ||||||

| Price: | 24.00 | EPS | 1.14 | 1.05 | |||

| Shares Out. (in M): | 37 | P/E | 21 | 23 | |||

| Market Cap (in $M): | 890 | P/FCF | 24 | 23 | |||

| Net Debt (in $M): | 94 | EBIT | 62 | 57 | |||

| TEV (in $M): | 983 | TEV/EBIT | 14 | 14.5 | |||

| Borrow Cost: | Available 0-15% cost | ||||||

Sign up for free guest access to view investment idea with a 45 days delay.

- Industrial Equipment

- Oil Price Exposure

- Oil Services

- Accounting

Description

For a pdf version of the writeup please go to the following link:

https://www.dropbox.com/s/l866dy613xityrt/Badger_Writeup.pdf?dl=0

|

Ticker: BAD.CN |

Company: Badger Daylighting |

Recommendation: Short |

|

Price: $23.08 as of 12/14/2015 |

2016 year-end target price: $14 |

1 year downside: 41% |

Investment Thesis Summary

I believe shorting Badger Daylighting Ltd. (“BAD” or “Badger”) offers an attractive risk-reward tradeoff at the current price. I believe Badger is a low quality business with no barriers to entry and deteriorating industry fundamentals. Additionally, I believe Badger provides inconsistent and misleading accounting disclosures and deploys questionable business practices. Historically, Badger experienced a 10 year sales CAGR of 18% from 2004 to 2014. This growth had two stages: 10% sales CAGR from 2004 to 2010 and 32% sales CAGR from 2010 to 2014. Growth in the last 10 years was driven by Badger having a first mover advantage in the use of hydro excavation technology. The stronger than average growth in the last 4 years was driven by exposure to the petroleum sector (roughly 50% exposure) during the shale boom. Going forward, however, Badger’s first mover advantage is rapidly eroding. Badger’s knowhow of hydro excavation technology is no longer proprietary and new competition is popping up all across North America. As a result, I believe both utilization and pricing are under pressure and Badger’s long runway of uncontested growth is quickly dissipating. Additionally, I believe the steep growth trajectory during the shale boom is unlikely to be repeated, even if oil prices rebound, given the large amount of idle hydrovac equipment in the market.

My short thesis is based around the following key issues:

-

The industry is getting commoditized by new entrants, thus reducing the runway for growth for Badger

-

The current PE multiple implies market is assuming long term growth rates to be much higher than what will be realized

-

Badger may be exaggerating the number of local offices it operates, thereby overstating the size of the company

-

Questionable treatment of franchisees may hurt them sooner rather than later

-

Inconsistent and misleading accounting disclosures, coupled with management and auditor turnover, raise red flags

The market is assigning a 16x multiple on its 2016 consensus EPS estimate of $1.49. Such a high multiple for a commodity business leads us to believe that investors may be expecting Badger to grow earnings in the low-teens to high teens over the next few years. I believe these expectations are too high and the bulls will be disappointed. I expect Badger to shrink EPS in the high-single digits over the next two years. In my base case, I expect 2016 EPS to be $1.14, 24% lower than consensus at $1.49. Based on a PE multiple of 13 and 2017 EPS of $1.04, I believe Badger is worth $14 a share by the end of 2016, or a downside of 41% on the stock. In my bull case, the stock is worth $28 (using 16x 2017 EPS of $1.75), an upside of 21%. In my bear case, the stock is worth $7 (using 11x 2017 EPS of $0.66), or 68% downside.

Additionally, there is a free option if Badger gets into legal trouble due to questionable business practices, pending and future lawsuits, and inaccurate financial disclosures. However, given the uncertainty around the timing of such events I do not model any of these events in any of my scenarios.

I encourage other investors to conduct their own due-diligence and come to independent conclusions on the issues I have cited in my short thesis on Badger.

Business Description

Badger Daylighting Ltd. is North America’s leading provider of non-destructive hydrovac excavation services. Badger’s primary revenue-generating asset is its fleet of over 1000 hydrovac trucks, which Badger rents to petroleum, industrial and municipal clients. Contracts are primarily short-term, work-based, and are paid on an hourly basis. The truck rental comes with one to two crew operators that are Badger employees.

23% of Badger’s fleet is operated by franchisee owned locations and 77% by company owned locations. 66% of Badger’s revenue comes from United States and 33% from Canada; and 51% from the petroleum industry (such as pipeline operators, oil/gas drilling, oil refineries) and 49% from utility and construction clients (such as municipalities, utilities and general contractors who operate in areas with a high concentration of underground power, communication, water, gas, and sewer lines, particularly in large urban centers where safety risks are high). Demand from the petroleum industry is driven mainly by the turnaround cycle for refineries, maintenance of pipelines, drilling activity for oil and gas wells, and construction activity for new pipelines. Demand from municipalities is fairly stable while demand from construction contractors is driven by the business cycle.

Hydrovac trucks help dig soil without damaging utility lines, such as gas or water pipelines, which are buried in the ground. Hydrovac trucks have two components that work simultaneously: (1) a pressure washer that uses water and (2) a vacuum system. The pressure washer breaks the soil while excavating and the vacuum system sucks up the slurry and deposits into a storage tank housed on the truck. The truck disposes the slurry at a safe location onsite or offsite. This method of digging has a lower probability of damaging underground utility lines than manual digging or digging using heavy equipment such as backhoes. Therefore, hydrovac excavating is slowly becoming the preferred way of digging in congested areas.

Badger is based in Canada and reports financials in Canadian dollars. Badger maintains a manufacturing facility in Canada, where it assembles its own equipment on truck chassis that it buys from truck manufacturers. The all-in manufacturing cost for Badger is roughly $350,000 per truck. Badger’s competitors buy pre-built hydrovac trucks from manufactures such as Caterpillar, WesTech, Tornado, Smith Industries, AmeriVac, and Foremost. Depending on the specifications, competitors can buy a hydrovac truck for $200,000-$500,000.

The industry for hydrovac services in North America is highly fragmented with hundreds of small companies owning 1-2 trucks, along with a few large companies, namely Badger (1019 trucks), Lone Star West (~100 trucks), Clean Harbors, Big Eagle Services (~100 trucks), and Hydrodig (~60 trucks). Municipal jobs are mainly won on price bids while oil and gas jobs are won on relationships.

Exhibit 1: Picture of Badger Hydrovac trucks in action (Source: Badger’s website)

Investment Thesis

Thesis Point 1: Industry is getting commoditized by new entrants, thus reducing the runway for growth for Badger

Badger started hydrovac excavation services over 20 years ago in Canada, and was one of the first to offer such services. Over the last 20 years, Badger expanded its business across the United States as well. Being the first mover helped Badger become the most dominant player in the space with over 100 local offices and over 1000 hydrovac trucks as of Sep 30, 2015. Badger grew revenues at 18% CAGR in the last 10 years while maintaining EBITDA margins in the high 20s. During its growth phase, Badger undertook several initiatives that gave it an advantage over its competitors: developing a manufacturing facility to assemble hydrovac equipment on truck chassis; educating potential clients about the advantages of hydrovac services over mechanical digging; and training several hundred employees to use hydrovac trucks and about the safety benefits of hydrovac services.

However, most of the advantages that Badger had over competitors in the past have diminished. Fully assembled, ready to use hydrovac trucks are available from several manufacturers for $200,000 to $500,000 per truck versus Badger’s internal cost of approximately $350,000. Competitors are therefore no longer disadvantaged on cost per truck, and no longer face obstacles obtaining hydrovac trucks. Clients today tend to be more knowledgeable about the advantages of hydrovac services and are looking for the cheapest provider rather than just working with Badger out of lack of options. Several trained hydrovac equipment operating professionals are available for hire by competitors. As a result of the changed market environment, small regional competitors have popped up all over North America. Since hydrovac services are delivered locally to local clients, there is little advantage to being a national player.

In addition to the removal of barriers to entry to the hydrovac market, there is an increasing trend for clients to own their own hydrovac trucks rather than hire external service providers, such as Badger. Municipalities such as the city of Wichita, Kansas and some large construction companies have determined insourcing of hydrovac trucks to be more economical than outsourcing. Over time, I expect this trend to pick up even more.

For the above mentioned reasons, the uncontested, long runway for growth that Badger had enjoyed is fast eroding. As a result, I believe that the future growth rate for Badger is going to be much slower than what it has experienced in the past. Currently, management guides to its US business (~2/3 of total) doubling over the next 3-5 years which would imply a 15%-26% CAGR. I believe such a goal seems unrealistic given increased competition. The Canadian business (1/3 of total) is much more competitive and much more penetrated than the United States, so the runway for growth in Canada is even lower than that in the US. Nevertheless, management guides to 10-15% growth in the Canadian business over the long term, which I believe is unrealistically high.

There is no reliable industry data for market size, market share, and market growth available for hydrovac services in North America. But based on my conversations with hydrovac truck manufacturers, I estimate that the industry’s fleet size for hydrovac trucks in North America is expected to increase by 20%-30% in 2015, leading me to believe that there is a lot of new supply hitting the market.

Because of increasing competition and increasing commoditization of hydrovac services, I believe Badger’s runway for growth is quickly eroding and will continue to further deteriorate over time.

Thesis Point 2: Implied growth expectation is too high to justify valuation

At a stock price of $23 per share and consensus 2016 EPS of $1.49, Badger trades at 16x PE. Such a multiple would imply that the market is expecting low to high teens EPS growth from Badger over the next few years. I believe the probability for Badger to realize such a growth rate in the next 2 years to be low. Instead, I believe EPS will compress in the high-single digits over the next two years.

Below are the key drivers of EPS growth along with my base case expectations:

-

Growth in revenue per truck per month

-

Grew at 6% CAGR from 2010-2014. I expect it contract at ~2% annually going forward in my base case

-

Fleet growth

-

Grew at 25% CAGR from 2010-2014. I expect it grow at 8-9% annually going forward in my base case

-

USDCAD exchange rate

-

Currency move was a 10% annual tailwind on 2/3 of the revenue over the last two years. I expect low-single digit headwind annually on ~2/3 of revenue going forward in my base case

-

EBITDA margin expansion

-

EBITDA margin expanded from 26.7% in 2012 to 28.5% in 2014 providing a tailwind of 3.5% CAGR to EPS growth over those two years. I believe EBITDA margins will contract going forward in my base case, going down to 24.6%, leading to a mid-single digit headwind to EPS annually

Based on my assumptions of key growth drivers, I believe EPS will contract high-single digits over the next two years. For such a growth rate, a PE multiple of 16 seems very high. I explain my rationale for my base case assumptions below:

Revenue per Truck per Month

Note that this metric captures both pricing and utilization. I don’t believe Badger will be able to increasing pricing going forward. Recent trends suggest that most likely there will be price decreases instead. My industry channel checks suggest that hourly rates for hydrovac services are down 15-20% year-over-year in Texas, down 20-30% down in South Central United States, down 10-15% down in North Dakota, down 5% in the Midwest, and flat in California. I estimate Canadian rates to be down at least 15%. In spite of materially negative overall industry rates, Badger has resisted reducing its rates and is, therefore, losing market share and experiencing decreased utilization. I believe this is an unsustainable strategy and that Badger will eventually have to bring down its rates at the level of its competitors to sustain its business model and keep utilization at a reasonable level. Badger’s trucks and services are no longer differentiated enough to justify premium prices.

If prices start to rise, clients will have an increasing tendency to purchase their own hydrovac trucks rather than outsource to a provider. This phenomenon should keep a lid on pricing, unless the oil and gas industry rebounds aggressively. Even in this scenario, I believe price increases will stay relatively subdued due to a large amount of idle hydrovac equipment in the market.

I believe consolidated revenue per truck per month would decrease ~2% annually in my base case

Fleet Growth

Badger’s fleet grew at a CAGR of 25% from 2010 to 2014. The growth dramatically slowed to 3% in 2015. I optimistically believe Badger’s fleet will grow in the high-single digits over the next two years, much slower than the historical trend. There are several reasons behind my view.

-

I expect Badger’s current utilization of its fleet to be below 50%. Although there are trucks sitting idle, management is still building four trucks per month to, in my opinion, artificially prove to the investment community that Badger is a growing company. I feel this growth is unsustainable.

-

Badger has fired a number of its area managers, which may lead to a lower utilization going forward, as many of the relationships that those area managers built are lost, to some extent.

-

There is a lower need for trucks going forward, since Badger overbuilt its fleet in the past and forced its local area managers to accept new trucks even though incremental demand for the additional trucks was not there. The head office is therefore able to allocate the cost of a new truck to the P&L of a local office by forcing the local office to accept a new truck to its location regardless of the need for that truck. I have talked to several former Badger employees who have suggested that the head office forces local area managers to accept 1 to 2 new trucks every year at their location even if there is no incremental demand. When a truck is delivered to a local area manager’s location, Badger’s head office charges roughly $110,000 per year to the local office (5 year amortization at a cost base of roughly $550,000) for having that truck. There is an additional incentive for the head office to keep building trucks as it can transfer the cost of those trucks to the local office, which reduces the bonus that the local area manager gets on its location’s profitability. Forcing trucks on local locations has been a reason why many talented area managers leave Badger to start a competing business or to work for a competitor. I believe it will take time for Badger to work through the excess fleet before it builds more new ones.

Beyond the next two years, I estimate fleet growth to be in the low to mid-single digits.

USDCAD Exchange Rate

Badger’s reporting currency is Canadian dollars even though roughly 2/3 of its hydrovac fleet is in the United States. Since the Canadian dollar has weakened by ~20% in the last two years, Badger’s consolidated revenue had an uplift of roughly ~6.5% per year (2/3 times 20% spread over two years) from currency moves. Unless the Canadian dollar further weakens, there would be little tailwinds from such moves in the future. Inversely, if the Canadian dollar strengthens, it will be headwind for Badger.

I estimate the impact of currency moves to be a low single digit headwind in my base case.

EBITDA Margin

Historically, Badger’s EPS growth was accelerated by EBITDA margin expansion, which grew from 26.7% in 2012 to 28.5% in 2014. However, during 2015 Badger has been extremely aggressive in cutting costs and deferring a large chunk of its maintenance expense onto its fleet during the last few quarters. Additionally, the industry is and will continue to suffer from pricing pressure. As a consequence, I believe Badger will experience margin contraction of ~140bp per year going forward.

Thesis Point 3. Badger may be exaggerating the number of local offices it operates, and thereby overstating the size of the company

I think Badger may be exaggerating the number of local offices it operates in order to inflate the size of the company. After reviewing Badger’s website, performing a Google map search, and visiting a small sample of locations, I could not reconcile the total number of Badger’s locations.

Badger has a “contact us” page on its website. On this page there, is conflicting information regarding the total number of local Badger offices. (See Exhibit 2)

-

At the top of the page, it says Badger has more than 100 local offices across the United States and Canada

-

If I click on the map view on this page, it gives us a zoom-able map view of all of Badger’s local offices (Exhibit 2 shows this map). Counting the icons on the map, I count 94 local offices in the United States and 57 in Canada, for a total of 151 local offices across North America. This number seemed much higher than 100, but is still consistent with the information in item (a)

-

From the list view on the same page, I counted 81 unique phone numbers in the United States and 46 unique phone numbers in Canada, implying a total of 127 local offices. This number is still consistent with the information in item (a), but there is clearly a discrepancy with the number shown in item (b)

-

I also did a Google map search for “Badger Daylighting,” and only got 39 local offices in the US and 30 in Canada, for a total of 69 local offices across North America. This number was much lower than the “more than 100” from item (a), 151 in item (b) and 127 in item (c). In the company’s defense, it is possible that Google map’s information on Badger is incomplete, but nevertheless, there are inconsistencies.

Exhibit 2: Webpage on Badger’s website showing its local offices across North America

To get more color on Badger’s local offices, I decided to visit some of the local offices shown around the New York City area on the map view on Badger’s “contact us” page (Exhibit 3 shows these locations). There are four local offices that show up on Badger’s website near the New York City area. These locations are labeled as “Central New Jersey,” “Northern New Jersey,” “US North East Regional Office,” and “Seymour, CT”. There were no addresses shown on the map for these local offices, so I zoomed in on the map icon to find the exact location of the local office and visited each of those four locations. Here is what I found out for each:

Exhibit 3: Webpage on Badger’s website showing its local offices near New York City

-

Central New Jersey Location

I drove to the location that showed up on the map (See Exhibit 4). The google map icon was near a creek with empty land, adjacent to residential property. There was nothing around the area that looked like a business that would rent hydrovac trucks.

Exhibit 4: Map location of the Central New Jersey local office and a picture of the site

-

Northern New Jersey Location

I drove through the exact point on the map icon location (See Exhibit 5), but the site was undeveloped land. Again, there was nothing around the area that looked like a business that would rent hydrovac trucks.

Exhibit 5: Map location of the North New Jersey local office and a picture of the site

-

US Northeast Regional Office

I drove through the exact point on the map icon location (See Exhibit 6). I found only abandoned property. I even inquired in several local businesses for the location of Badger Daylighting’s office, but had no success.

Exhibit 6: Map location of the US North East Regional Office and a picture of the site

-

Seymour CT location

I drove to the exact point on the map icon location (See Exhibit 7), which turned out to be a ramp of a freeway next to a river. I couldn’t even stop my car to take a picture of this location. There was no commercial or building structure, or any business for that matter, around that map icon.

Exhibit 7: Map location of the Seymour CT local office

After going through Badger’s website, Google maps, and visiting Badger’s local office locations around the New York City area as shown on its website, I are unsure of the total number of legitimate local offices Badger has.

Could Badger be overstating the size of its operations in order to inflate its enterprise value? I encourage other investors to conduct their own due diligence on this issue and come to their own conclusion as I have only explored a small sample of Badger’s locations rather than all of Badger’s locations.

Thesis Point 4: Questionable treatment of franchisees may hurt them sooner rather than later

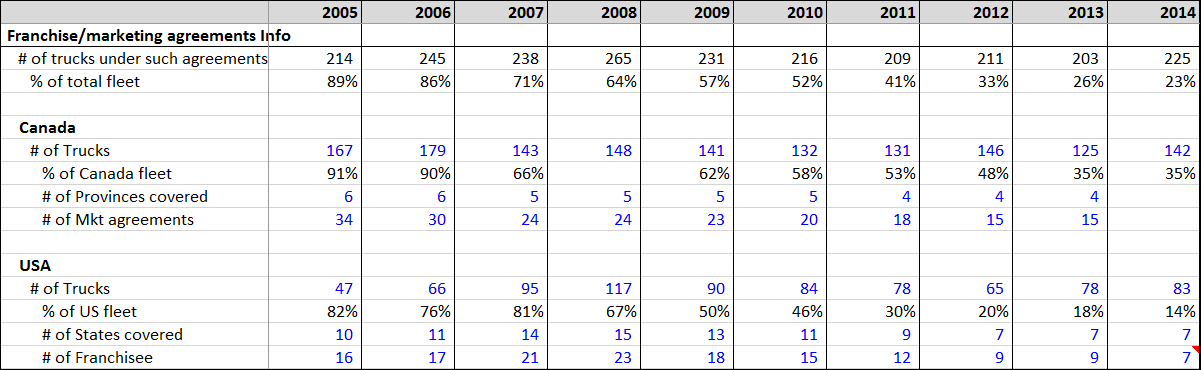

About a decade ago, Badger’s preferred growth strategy was to expand through franchisees, rather than by owning corporate locations. In 2005, roughly 90% of the fleet was under such agreements (called “franchise agreements” in the US and “marketing agreements” in Canada). Franchisees developed relationships with and solicited business from local utilities, construction contractors, and petroleum clients by educating them about the advantage of excavation using Badger hydrovac trucks over other mechanical means.

The economics of such agreements were usually structured as follows:

-

The franchisee paid 20% of the upfront capex of a truck, and in return kept 60% of the revenue from each truck

-

The franchisee paid 100% of the operating expenses

-

The franchisee also paid a recurring admin fee per month to Badger for managing accounting, invoicing, and collections.

-

Badger retained ownership of the truck.

-

Certain maintenance capital expenditures related to the trucks were to be covered by Badger.

-

The initial term of each Franchise Agreement or Marketing Agreement was 5 or 10 years, subject to renewal by the operator for an additional 5 year term.

-

The contract had minimum performance requirements for the franchisees.

Badger’s growth strategy through the franchisee model worked well, as franchisees performed all of the business development work and incurred all related expenses. Franchisees marketed Badger’s brand name, educated clients about Badger’s hydrovac trucks, passed on their clients’ contact information to Badger for billing purposes. Once a local office has been established and a client list has been developed, Badger didn’t need the franchisee as much as the franchisee needed Badger. Badger began acquiring those franchisees and converting those locations to company-owned. In fact, Badger went from 89% of its trucks under the franchisee model in 2005 to about 23% of its trucks under the franchisee model by 2014 (see Exhibit 8).

My research suggests that Badger may have been overly aggressive in acquiring back its franchisees, to the extent that it used questionable business practices in certain cases. A large number of the franchisees were taken back using non-performance clauses in the franchise agreements. I believe some of those contract violations were un-enforceable or were unfair. Recently, Badger lost a lawsuit (Case number B-CJ 2011-301 in the district court of Creek County in the State of Oklahoma) with a franchisee in Oklahoma called “Hewitt’s Badger Daylighting” (the “Plaintiff”). In June 2015, the jury entered a verdict of approximately USD$13.7 million in favor of the Plaintiff against Badger for breach of contract and other causes of action. This franchisee had 8 hydrovac trucks, so the damages came out to be $1.7 million per truck. Badger is appealing this ruling in the Supreme Court of the State of Oklahoma, but I believe the probability of the ruling getting overturned is low.

My current understanding is that, if Badger loses its appeal, Badger will have to pay additional cash for lost interest to the Plaintiff as well. That’s not the worst news for Badger, though. From my research, I believe that if the Supreme Court doesn’t overturn the district court’s ruling, there are several more disgruntled former franchisees working behind the scenes to file additional lawsuits against Badger using this case as a reference. I estimate Badger took back roughly 65 franchises in the United States over the life of the company. My guess is that the total number of trucks acquired through such methods would most likely be significantly above 100. If all of those former disgruntled franchisees file additional lawsuits, the total damages claimed in such lawsuits can easily exceed $170 million, assuming a judgment of $1.7 million per truck and only a total of 100 trucks under dispute. I agree that the range of outcomes is wide, given the lack of reliable publicly available data, but the fact remains that the above scenarios are materially negative for Badger.

Based on my conversations with former employees, I also think there is a possibility that some franchisees who agreed to sell their franchise back to Badger for a lump sum could also file a lawsuit against Badger on the grounds that Badger made it difficult for those franchisees to operate successfully, in effect, forcing them to sell their business back to Badger. There are several ways Badger can coerce a franchisee to sell. One way would be to not perform maintenance capital expenditures on the franchisee’s trucks even though, according to the franchise agreement, it is Badger’s responsibility. If a franchisee doesn’t have well maintained trucks, then it can’t conduct its business for safety reasons. Badger could also take its trucks back, citing non-performance. If there are no trucks at the franchisee’s location, it is impossible for them to conduct business. In such situations, a franchisee would rather sell its business to Badger and get some money in return, than fight with a deep-pocketed opponent on a lawsuit in which the outcome is unpredictable.

Encouraged by the success of American franchisees in lawsuits against Badger, it’s possible that some former Canadian franchisees may also file lawsuits against Badger.

Given the large amounts of potential damages involved if more cases are filed, Badger’s questionable business practices will be severely tested in the courts. Badger was already in default of its credit agreements after the judgement of the Oklahoma lawsuit came out, and had to get a waiver from its creditors to cure the default. The creditors agreed to the waiver, perhaps thinking this judgement was an isolated event rather than a regular occurrence. However, if multiple lawsuits are filed, Badger may not have the support of its creditors and may have to raise equity to pay off its debt and legal damages.

I highly encourage other investors to conduct their own due diligence on the treatment of former franchisees, as this issue could have a significant impact on Badger’s valuation and business model sustainability.

Exhibit 8: Table showing trucks under franchise or marketing agreements (Source: Sedar filings & my estimates)

Thesis Point 5: Inconsistent and misleading accounting items, along with management and auditor turnover, raise red flags

Several of Badger’s disclosures seem misleading and inconsistent. Additionally, several key employees resigned over the last two years. In May 2014, CFO Greg Kelly (who held the position since 1999) left the company, and in November 2014, Chairman of the Board, George Watson, departed. In March 2015, Director and Audit Committee member Richard Couillard decided to not stand for re-election. In April 2015, Ernst and Young stepped down as Badger’s auditor.

On the disclosure side, there are a few items I would like to highlight:

-

Dramatic growth in non-hydrovac revenue in 2014 is inconsistent with Badger’s business plan

-

The number of trucks retired seems understated

-

The revenue recognition policy excludes collectability criteria

Below I provide more color on each of the above mentioned items.

-

Dramatic growth in non hydrovac revenue in 2014 is inconsistent with Badger’s business plan

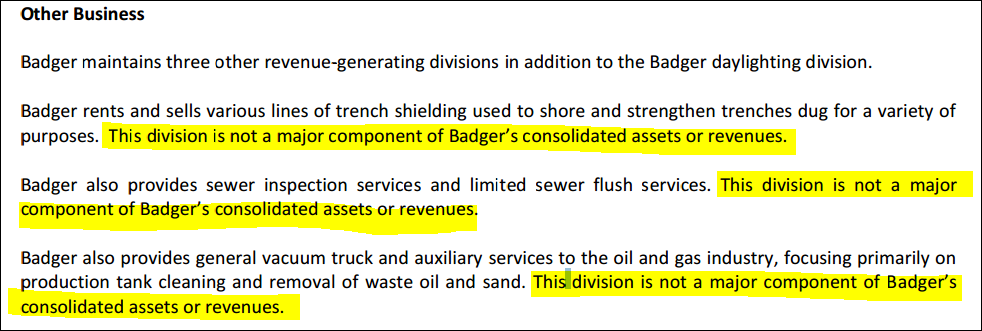

Most of Badger’s revenue comes from hydrovac services. This is the segment where management deploys almost all of its capital. However, Badger also generates revenue from four other activities, namely sewer inspection (called “Benko”), tank cleaning (called “Fieldtek”), shoring rentals (“Shoring”), and truck placement fees. The truck placement fee is a one-time payment Badger gets when it delivers a truck to a franchisee. Badger discloses truck placement fees in its earnings releases. Exhibit 9 shows the description of the other three business lines. As per the disclosure, none of those business lines are a major component of Badger’s consolidated assets or revenues. Before 2015, Badger didn’t provide any financial information on non-hydrovac revenue performance. Therefore, non-hydrovac revenue contribution needs to be estimated by piecing together information from various other line items.

Exhibit 9: Snapshot from Page 7 of 2014 AIF describing Badger’s other revenue sources

As per the company disclosures, Benko was acquired on April 1, 2007 for $4.1 million and had a revenue of $4 million in 2006. Benko came with 3 hydrovac units, 4 sewer maintenance vehicles, and 3 camera units, for a total of 10 pieces of equipment. The key point here is that Benko is a very small component of Badger’s business.

As per company disclosures, Fieldtek was acquired on November 1, 2013 for $19.2 million. Fieldtek came with 50 pieces of equipment, including semi-vacuum trucks and trailers, pressure trucks and steamer combo units. The price paid was 4 times trailing EBITDA, so trailing EBITDA was roughly $4.8 million. The key point here is that it’s a small component of Badger’s business, but is much larger than Benko. Also, just one quarter after the acquisition, management hinted in its earnings release that Fieldtek was not a good acquisition, as the company does not believe it will be able to increase Fieldtek’s margins.

There is little information about the shoring rental business in any of the company disclosures in the last several years, so my guess is that this business contributes very little in revenues. I would estimate revenues to be $1-$4 million per year.

I used all of the above disclosures, along with commentary from quarterly results made by Badger, to calculate the implied individual contribution from (1) Hydrovac services, (2) Fieldtek, and (3) Benko + Shoring combined. I estimated these three components using the following method:

-

Assume all US revenues are from hydrovac services only. Convert US revenues into USD from CAD using average exchange rate over the relevant period, and divide that converted revenue by the average US fleet size to find the implied revenue per truck per month for the US business in USD

-

Using revenue per truck per month for the US business derived from step (a), consolidated revenue per truck per month reported by the company, average fleet size in Canada, and average fleet size in the US, calculate revenue per truck per month for the Canadian hydrovac business only, using a weighted average formula

-

Multiply the Canadian revenue per truck per month from step (b) by the Canadian Average fleet to calculate Canadian hydrovac revenue contribution

-

Take the total Canadian revenue reported by the company and deduct the Canadian hydrovac revenue derived in step (c) and the “Truck Placement Revenue” reported by the company. The resulting number is the total contribution from Fieldtek and Benko+Shoring combined

-

Calculate revenue generated by Fieldtek using management commentary in the quarterly earnings releases

-

Calculate the combined revenue generated by the Benko+Shoring business lines by deducting the estimated revenues generated by Fieldtek from step (e) from the result of step (d)

I show the results of my quarterly estimates in Exhibit 10a, and yearly estimates in 10b, using the above process. There are a few interesting observations which I would like to highlight from this analysis:

-

In the first year of Benko’s purchase in 2007, Benko+Shoring combined contributed roughly $4.5 million in revenue. From company disclosures at the time of Benko’s purchase on April 1, 2007, I also know that it had generated $4.1 million in revenue in the previous year under the previous owner. So Benko’s contribution in 2007 for nine months must be close to $3.1 million, leaving Shoring to have generated ~$1.4 million. This implies Shoring is a very small component of Badger’s business.

-

The yearly growth rate of the Benko + Shoring business is very volatile from 2008 to 2014. It more than doubled in 2008, just one year after Benko’s acquisition in 2007, then shrunk by more than half in 2009, and then more than doubled again in 2010. One would expect the growth rate over the last 7 years to be relatively smooth, given such businesses have fairly steady end market demand.

-

Combined total revenue from Fieldtek, Benko and Shoring was 7% of total revenues in 2013 and 13% in 2014. This seems high given that management discloses these business as a non-significant component of Badger’s revenue or assets.

-

In 2014, revenue from Benko+Shoring of $29.7 million was larger than that of Fieldtek’s $26.1 million, even though disclosures suggests that Fieldtek is a much larger business than Benko+Shoring combined. After all, Fieldtek had 50 pieces of equipment in 2013 and generated $19.2 million in revenue whereas Benko only had 10 pieces of equipment in 2007 and generated $4.1 million in revenue, and Shoring is an insignificant contributor. None of the disclosures suggest that Badger was aggressively investing in the Benko subsidiary throughout those years. Plus, business lines such as sewer inspection and shoring rental in Canada have little to no organic growth.

-

Revenue from Benko+Shoring combined grew an astonishing 63% in 2014. From the various earnings release in 2013 and 2014, it never appeared that Badger was investing significant capital in growing these businesses. This begs the question: how did the revenues grow at a 63% rate in 2014? If the 63% growth was legitimately realized, then a prudent management would allocate a significant amount of its capital resources to further grow such business lines. But Badger didn’t.

Could Badger be using Benko/Shoring revenues as a cookie jar account to manage the market’s growth expectation in order to manipulate its stock price?

Exhibit 10a: Estimated quarterly revenues from Hydrovac Services, FieldTek, & Benko+Shoring Rental

(Source: Sedar filings and my estimates)

Exhibit 10b: Estimated yearly revenue contribution from Hydrovac Services, FieldTek, and Benko+Shoring Rental

(Source: Sedar filings and my internal estimates)

-

Retirements seem understated

In its Annual Information Form (AIF), Badger discloses that it amortizes its hydrovac trucks over 10 years for depreciation purposes. (See Exhibit 11). According to management knowledge and past experience, the economic life of hydrovac truck is 10 years. An implied conclusion would be that Badger’s fleet should turnover 100% every 10 years if Badger were to start with a brand new fleet.

Exhibit 11: Excerpt from page 12 of Badger’s 2014 AIF disclosing its amortization assumptions for its hydrovac trucks

In Exhibit 12, I show Badger’s fleet size, additions and retirement for the last 10 years. In deriving 2015 estimates, I have made some assumptions as Badger hasn’t yet reported its Q4’15 earnings. If I take Badger’s fleet size in 2005 year-end and assume that the whole fleet at the end of 2005 was brand new, I should expect all of those 2005 trucks to be retired by 2015. The fleet size at the end of 2005 was 241 trucks, but the total number of retirements between 2005 and 2015 was 154, far short of the 241 that I predicted. This is just 64% of the predicted number, even when I made the simplifying assumption that all of the trucks at the end of 2005 were brand new. This would imply an average life of a truck to be ~16 years (i.e. 10 divided by 0.64).

Now, let’s compare the above results using no simplifying assumption that Badger’s fleet at the end of 2005 was brand new. In its 2005 annual report, Badger disclosed that the average age of its fleet was 4.5 years and that the economic life of its trucks were 10 years (See exhibit 13). So the fleet at the end of 2005 would have had an average remaining life of 5.5 years (10 minus 4.5), and therefore would have all been completely retired by mid-2011. But Badger only retired 84 trucks between 2005 and mid 2011 compared to my expectation of 241. This is only 35% of the expected number. This would imply an average life of a truck to be ~29 years (10 divided by 0.35) versus management’s estimates of 10 years based on past experience.

Exhibit 12: Table showing Badger’s hydrovac fleet size, additions, and retirement

(Source: Sedar filings and my estimates)

Exhibit 13: Excerpt from page 11 of Badger’s 2005 annual report shows its fleet’s average age

Is Badger overstating the size of its fleet to inflate the size of the company in order to get a higher enterprise value from the market? An explanation in Badger’s defense could be that the company is keeping its old trucks in its parking lot and not retiring those old trucks. In that case, the true usable fleet size could be a lot lower than its Q3’15 ending fleet size of 1020 trucks; maybe just 35% of its size, which would imply only 357 usable trucks! Whatever the case may be, the most likely conclusion is that the truck retirement numbers disclosed by Badger don’t seem realistic and are inconsistent with other disclosures.

-

Revenue recognition policy excludes collectability criteria

In Exhibit 14, I can observe that Badger’s revenue recognition policy doesn’t have any collectability assurance criteria, which seems strange. This would imply that Badger can book revenues even if Badger is not sure about the counterparty paying its bills.

Exhibit 14: Excerpt from page 10 of Badger’s Q4’14 financial statements regarding its revenue recognition criteria

As expected, other Canadian peers have collectability clause in their revenue recognition policy. Exhibit 15 shows the revenue recognition policy of LoneStar West, who is Badger’s closest peer. Exhibit 16 and Exhibit 17, shows the revenue recognition policy of two other Canadian oilfield services companies, Secure Energy Services and Ensign Energy Services. All three companies clearly have a collectability clause in their revenue recognition policy.

Exhibit 15: Excerpt from page 6 of LoneStar West’s Q4’14 financial statements regarding its revenue recognition criteria

Exhibit 16: Excerpt from page 7 of Secure Energy’s Q4’14 financial statements regarding its revenue recognition criteria

Exhibit 17: Excerpt from page 58 of Ensign Energy’s 2014 annual report regarding its revenue recognition criteria

In Exhibit 18, I provide the details of Badger’s trade receivables using disclosures in its annual reports. I noticed that in 2014, the percentage of receivables that have been due for more than 90 days jumped from 13% to 23% of the total trade receivables.

Could these trade receivables never be paid? If these receivables are never paid, the reported revenue in 2014 might be inflated and therefore, the adjusted revenue could go down from $422 million to $398 million, which would imply Badger grew revenue at a 22% rate in 2014, instead of the reported 30%.

Since Badger reports trade receivables details only annually and not quarterly, I don’t know the receivable performance over 2015. However, given the economic slowdown in 2015 among Badger’s end markets, I would anticipate the receivable quality to have further deteriorated in 2015.

Based on the above, it seems that the bulls are taking unknown risk regarding the quality of Badger’s revenues, as Badger has no collectability criteria in its revenue recognition policy.

Exhibit 18: Ageing analysis of Badger’s trade receivables (Source: Sedar filings and my estimates)

Valuation and Sensitivity

In Exhibit 19 I show my estimates and assumptions for my base, bull and bear scenarios.

I believe there is a high probability that some of Badger’s accounting disclosures may be inaccurate and maybe restated in the future. However, given the uncertainty around the timing of such events, I do not model any such event in any of my scenarios. In other words, I assume all accounting disclosures to be fair and accurate as presented. Any restatements of prior financial statements would be an additional downside to the stock and is a free option for the short seller.

Base Case:

-

I expect 2016 and 2017 Rev/EBITDA/EPS growth rate to be 5%/-1%/-9% and 2%/-3%/-8%, respectively

-

I expect 2016/2017 EPS to be $1.14 / $1.04. My 2016 EPS estimate is 24% below consensus estimate at $1.49

-

I optimistically believe that such a growth rate profile for a commodity business could justify a 13x PE valuation, On my 2017 EPS of $1.04 this would imply a target price of $14 by the end of 2016, giving a downside of 41%.

-

From a replacement value standpoint, the current stock price looks expensive in my base case. The stock trades at $711,000 on EV/truck in 2017 even though it takes Badger ~$350,000 and competitors $200,000-$500,000 to build a truck. This implies that a competitor could possibly replicate the business for roughly half of the value. In my target base case price scenario, using 13x PE, the implied EV/truck is $418,000, which seems more reasonable in a rational market environment.

Bull Case

-

I expect 2016 and 2017 Rev/EBITDA/EPS growth rate to be 13%/17%/19% and 11%/13%/14%, respectively

-

I expect 2016/2017 EPS to be $1.53/$1.75

-

I believe such a growth rate for a commodity business would justify a 16x PE multiple on my 2017 EPS of $1.75. This gives us a price target of $28, or an upside of 21%

-

Implied EV/truck is $817,000, well above the replacement cost of $200,000-$500,000 for competitors

Bear Case

-

I expect 2016 and 2017 Rev/EBITDA/EPS growth rate to be -2%/-13%/-25% and -8%/-17%/-29%, respectively

-

I expect 2016/2017 EPS to be $0.94/$0.66

-

I believe such a growth rate for a commodity business would justify an 11x PE multiple on my 2017 EPS of $0.66. This gives us a target price of $7, or a downside of 68%

-

Implied EV/truck is $223,000, near the lower end of the replacement cost of $200,000-$500,000 for competitors

Asymmetric Risk Reward profile

My scenario analysis suggests that shorting Badger stock provides an attractive asymmetric risk-reward profile skewed towards the downside. (Base Case: 41% downside, Bull Case 21% upside, Bear Case 68% downside). Additionally, I believe that the probability of the bull case playing out is low. Plus, there is a free option if Badger gets into legal trouble due to questionable business practices, pending and future lawsuits, and inaccurate financial disclosures.

Exhibit 19: Model summary for my base, bull and bear case estimates (Source: Sedar filings and my estimates)

Key Risks (in order of priority from high to low)

-

Takeout Risk

-

Clean Harbors approached Badger with an offer in 2011 for $20.50 per share that was rejected by Badger’s shareholders. Given that the shale boom has busted and the industry has been commoditized over the last few years, I am not sure if Clean Harbors would still be interested in paying up for Badger.

-

Plus, it is cheaper to build Badger than buy Badger. One could replicate Badger’s fleet of 1020 trucks assuming $400k per truck, by paying a total of $408 million versus Badger’s current enterprise value at $950 million.

-

Company stays under the radar and investors don’t do detailed work on the company

-

Coverage on the name is thin. There are only 3 small sellside brokers who cover Badger: CIBC, Canaccord, and Cormark Securities.

-

Strong recovery in oil price

-

Given current oil prices, and given that both United States and Canada are just coming off of one of the biggest investment cycles in oil and gas industry history, I feel this risk is manageable, as any recovery in hydrovac truck utilization will be slow

-

Additionally, there is enough excess idle hydrovac equipment in the market that even in an oil price recovery environment, price growth for hydrovac services may not be strong

Disclaimer

The content of this document represents the views of the individual user only, does not purport to be complete, and has been provided to Value Investors Club as a means to exchange investment ideas amongst a community of professional investors. Investors are encouraged to perform their own diligence when formulating an investment view.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

Accounting Restatements

New lawsuit filings or settlements

| show sort by |