| 2019 | 2020 | ||||||

| Price: | 6.32 | EPS | .50 | .67 | |||

| Shares Out. (in M): | 181 | P/E | 12 | 10 | |||

| Market Cap (in $M): | 1,142 | P/FCF | 20 | 15 | |||

| Net Debt (in $M): | 211 | EBIT | 400 | 800 | |||

| TEV (in $M): | 1,353 | TEV/EBIT | 12 | 6 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

Description

Disclaimer:

This idea is better suited for investors who are comfortable investing in an illiquid security in an economically volatile country like Argentina whose asset size allows them to consider a $5 million investment.

Cablevision Holdings Capitalization

Because the stock I am recommending is a holdco with a 39% in the underlying company, the VIC headline format does not adequately capture the capitalization of the company.

Please see below the capitalization of Cablevision Holdings (CVH AR) today and proforma for the mandatory tender of minorities in Telecom Argentina (TEO). Cablevision, as per its shareholder agreement with Fintech, the other major shareholder of TEO, would need tender for 4.5% of the shares of Telecom Argentina (TEO). The price is being negotiated, but I assumed $20 per TEO share.

|

CABLEVISION HOLDINGS (CVH AR) |

Pro Forma |

|

|

Market Capitalization |

Current |

Tender |

|

As of July 13, 2019 |

||

|

Price per share, ARS |

263.00 |

263.00 |

|

ARS/USD |

41.59 |

41.59 |

|

Price per share, USD |

6.32 |

6.32 |

|

Shares outstanding, millions |

181 |

181 |

|

Market capitalization, USD millions |

1,142 |

1,142 |

|

Net debt as of 3/31/19, USD millions |

211 |

598 |

|

Enterprise value, USD millions |

1,353 |

1,740 |

|

Ownership Structure |

||

|

Control Group |

77.5% |

|

|

Direct holdings by members of Control Group |

2.5% |

|

|

ANSES (Argentine social security system) |

9.0% |

|

|

Free float |

11.0% |

|

|

Total |

100.0% |

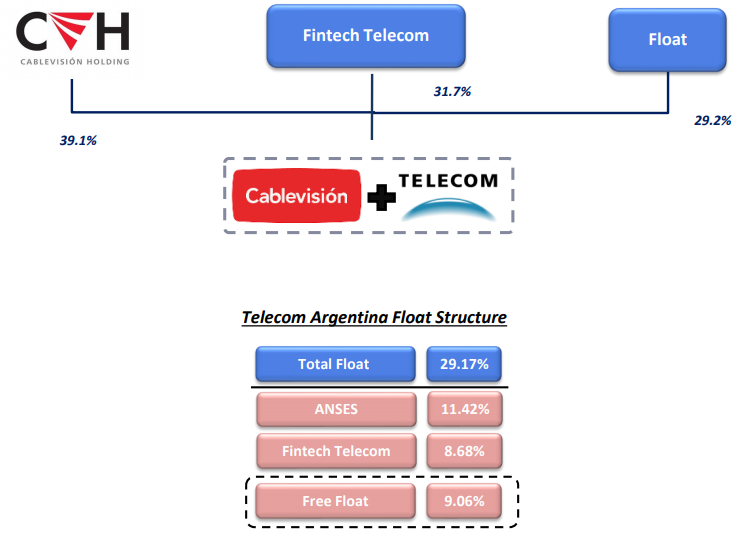

Telecom Argentina (TEO) Capitalization

|

Market capitalization |

||

|

As of July 13, 2019 |

||

|

Price per share, USD |

18.00 |

|

|

Shares outsanding, ADR equivalent in millions |

431 |

|

|

Market capitalization, USD millions |

7,753 |

|

|

Net Debt as of March 31, 2019, USD millions |

1,704 |

|

|

Enterprise value, USD millions |

9,457 |

|

|

|

||

|

Ownership Structure |

Pre Tender |

Post Tender |

|

Cablevision Holdings (CVH AR) |

39.10% |

43.60% |

|

Fintech Telecom LLC |

40.38% |

44.88% |

|

Anses (Argentina Public Pension System) |

11.42% |

11.42% |

|

Free float |

9.06% |

0% |

|

100% |

100% |

Type of Situation

Complex corporate structure. Overreaction to a temporary setback resulting from a macro crisis.

Thesis

-

By buying shares of Cablevision Holdings (CVH AR), one is investing in a holding company that has voting control and 39.1% economic interest in the leading cable TV/telecom service provider in Argentina (Telecom Argentina (TEO)) for 4x depressed (2018) EBITDA and 3x normalized EBITDA.

-

In 2018 Argentina suffered a deep recession and a 50% devaluation of its currency. Revenues of Telecom Argentina (TEO), Cablevision’s underlying operating company, declined 30% in USD terms, from $6.3 billion to $4.5 billion. EBITDA declined 25% in US$ terms, from $2 billion to $1.5 billion.

-

Based on historical precedent, profitability should recover to prior (2017) levels in US dollars in the next two to three years. I believe this is a conservative assumption.

-

EBITDA recovery will additionally benefit from merger synergies and cost rationalization measures under new management. Telecom Argentina was not efficiently run for decades as a subsidiary of Telecom Italia. In 2018, due to a merger and change of control, the company is now managed by owner operators with a record of value creation. New management is targeting $2.2 billion in NPV of synergies. Cablevision’s share of those synergies (39%) is equivalent to 90% of its current market capitalization.

-

Latin American telecom companies trade at 5x EBITDA. Cable companies trade at 8x EBITDA. Cablevision Holdings business mix is roughly half broadband/cable and half mobile.

-

Applying a blended multiple of 6x to normalized EBITDA ($2 billion in two to three years) would result in a tripling of Cablevision Holdings’ market capitalization.

-

Cablevision Holdings (CVH AR) is a holding company trading at a 50% discount to the current market capitalization of the underlying operating company, Telecom Argentina (TEO). The true free float of Telecom Argentina (TEO) when adjusting for strategic investors that form part of the control group with Cablevision (Fintech, Anses) is 9%. Cablevision Holdings is currently negotiating with the CVM (local SEC) the terms of a mandatory tender offer for the minorities. Based on its agreement with partner Fintech, it must tender for half of that float or 4.5% of TEO shares. I believe that in the next two years TEO could possibly be delisted, making Cablevision Holdings (CVH AR), the only publicly traded vehicle to own the underlying entity thus eliminating any holdco discount.

-

The downside risk is low in my opinion because the valuation is depressed, the earnings are depressed, and the balance sheet is well capitalized. Telecom Argentina has 1.2 turns of net debt to depressed EBITDA. Cablevision Holdings has $210 million of net holdco debt which adds 0.15x of EBITDA to the leverage. Cablevision will likely finance the tender of the minorities, adding another 0.10x turn of leverage to the structure.

-

Profitability is unlikely to deteriorate further even an under adverse political/macro scenario because Argentina already suffered a sharp devaluation and is already coming out of a deep recession in 2018.

-

In the unlikely event that there is an adverse outcome to the October 2019 presidential elections, I believe that this business will not be materially affected because the underlying demand for broadband is strong and the competition to Telecom cannot deliver the same quality of service in either broadband or mobile. ARPU’s are depressed in USD terms.

Background

In August 2016, Grupo Clarin, Argentina’s largest media group, announced its intention to contribute its cable, broadband, and data transmission assets, into a new company called Cablevision Holdings and spin it off to shareholders through a distribution in kind. In July 2017, prior to completing the spin off, Grupo Clarin decided to merge the assets of Cablevision Holdings with Telecom Argentina (TE0), a leading telecom operator, in exchange for a 39% stake and controlling position in the surviving entity. The merger created the only “quadruple play” cable/telecom service provider in Argentina. In August 2017 Cablevision Holdings (CVH AR), now a pure holding company with a 39.1% stake in the newly merged entity, was finally spun out to Grupo Clarin shareholders. The shares were well received, reaching a peak price of US$28.64 per share and peak market capitalization of $5.2 billion in January 2018 (versus $1.1 billion today).

Argentina’s economy has been in relative decline since the Great Depression due to populist policies and corruption. The 1990’s were a period of hope under the orthodox policies of finance minister, Domingo Cavallo, but he was ultimately unable to curb Peronist political interests and rein in fiscal spending. By the end of the decade, Argentina lost access to capital markets. In 2002 the country defaulted on its debt and abandoned its currency peg. This period was followed by twelve years of populist, incompetent, and corrupt government under Nestor Kirchner and his wife, Cristina Fernandez de Kirchner.

Hope and foreign capital returned in 2015 with the election Mauricio Macri, a reformist committed to orthodox economic policies. The stock market doubled in US Dollar terms. Accommodative credit markets enabled the country to issue a 100-year bond. However, President Macri inherited a difficult situation: a 5% current account deficit, a 5% primary fiscal deficit, high inflation, and an overvalued currency. In 2018, capital markets saw through these imbalances, and a currency run ensued. The Argentine Peso suffered a 50% devaluation, leading to skyrocketing local currency interest rates (60%+) and a deep recession.

The Merval Index dropped 65% peak to trough in USD terms, to levels not seen since 2013. Telecom Argentina (TEO) dropped from a peak price of $40/ADR in January 2018 to a low of $13/ADR in April of 2019, a 68% decline. It has since recovered to $18/ADR. Cablevision Holdings (CVH AR, CVHSY) dropped from a peak price of $28.65/share to a low of $3.80/share, an 87% decline in USD. It has since recovered to $6.31/share.

Reasons why the opportunity exists

Fear around the October 2019 presidential elections

After having been burned, investors now fear that President Macri will not be reelected in the upcoming October 2019 election and that Argentina will revert to a Kirschner led populist government. They are taking a wait and see approach. I believe it is unlikely that Cristina Kirschner can win due to the high rejection levels in the polls. However, if she were to win, I think the operations of the business would not be greatly affected. This is a long conversation, but I’m happy to elaborate in Q&A if anyone is interested.

Large macro crisis and devaluation which impacted corporate profits greatly

Profitability in USD of all domestically exposed Argentine companies has declined significantly. In emerging markets, currencies overshoot during an economic crisis. Periods of over shooting are usually followed by an appreciation or stabilization of real effective exchange rates. See a chart of Argentina’s real effective exchange rate since 1998 below. Based on historical precedents, I expect a real appreciation of the currency or at least stabilization which would provide a tailwind to companies such as Cablevision which have local currency revenues and dollar denominated debt. The market is looking backwards.

Cablevision Holdings (CVH AR) is not in the Merval Index and is not widely followed

The stock is actively covered by a small brokerage house called Allaria Ledesma y Cia.

Trading liquidity of the shares has completely dried up

Lack of liquidity is a legitimate reason for undervaluation, but in all markets liquidity is procyclical. The free float of Cablevision Holdings is 22%. However, if one excludes other long-term holders outside of the control group, free float is only 11%. The real free float at current market prices is $114 million. At its peak, the stock had a $5.2 billion market capitalization and a real free float of $572 millon). It traded at least $1 million daily and occasionally traded $6 million a day. Today the stock barely trades. I believe that it is possible to find blocks of stock and accumulate a $5 million position in the company. I also believe that once the tender for Telecom Argentina (TEO) shares is completed, Cablevision Holdings (CVH AR) will become the only vehicle to invest in these assets.

Cablevision Holdings Shareholder Structure

The controlling shareholders of Cablevision Holdings are the Noble Herrera family, Hector H. Magnetto, Jose Antonio Aranda, and Lucio Rafael Plagiaro. They started this cable business forty years ago and have grown it through organic build out and acquisitions.

The table below summarizes the shareholder structure of Cablevision Holdings (CVH AR):

The Telecom Argentina-Cablevision Merger

Between 2013 and 2016, through a series of transactions, Fintech, a financial buyer controlled by seasoned distressed investor, David Martinez, acquired Telcom Italia’s controlling stake in Telecom Argentina. In July 2017, Fintech and the Clarin Group negotiated a merger between Telecom Argentina and Cablevision Holdings’ cable, broadband, and data transmission assets. The merger was approved by the regulator, Enacom on December 2017 and by the anti-trust authority, CNDC, in June 2018.

The chart below summarizes the ownership of Telecom Argentina post-merger:

Business Description

Since the Cablevision Holdings (CVH AR) is a pure holding company, this summary is entirely focused on the business of Telecom Argentina.

Integrated telecom service providers are generally mediocre businesses in terms of return on capital. They operate in a high fixed cost, low variable cost, capital-intensive industry and offer a somewhat undifferentiated service with relatively low switching costs. However, telecom service providers globally exhibit a wide range of profitability depending on factors such as: regulatory environment, business mix, and market structure. For example, several incumbents in Continental Europe, have suffered dramatically in the last decade due to a tough regulatory and competitive environment. The United States telecom service providers, on the other hand, have benefited from a relatively benign competitive environment. Argentina, despite all its macro issues or perhaps because of them, falls into the benign category. This is reflected in Telecom Argentina’s margins. Note that margins are up in 2018 despite a 50% decline in the currency and 6% GDP contraction due to the early benefits of the merger:

|

Comparable EBITDA Margins |

2017 |

2018 |

|

Latam Telcos |

29.2% |

31.6% |

|

Global Telcos |

32.0% |

32.9% |

|

Global Cable TV and Pay TV |

36.1% |

34.8% |

|

Telecom Argentina (TEO) |

31.7% |

33.5% |

Within telecommunications services, different businesses exhibit different levels of profitability. Fixed line is a declining business. Mobile is a competitive business with a somewhat undifferentiated product, high churn, promotional pricing, and continuous capital deployment needs. Cable tends to be a much better business due to the upgradability of hybrid fiber coaxial architecture; its dominance of the “last mile;” and its unmatched ability to deliver high speed broadband connectivity to the home. Telecom Argentina’s business mix is roughly 40% mobile, 50% cable/broadband/pay-tv, and 10% fixed line.

The mobile business in Argentina is a stable three player market dominated by Telecom Argentina (TEO), Claro, a subsidiary of Carlos Slim controlled America Movil (AMX), and Telefonica Argentina, a subsidiary of Telefonica de Espana (TEF SM). Telefonica and Claro have not been as focused on developing their networks as Telecom. Telefonica’s parent has been in a deleveraging mode, and Claro has been focused on Brazil. Telecom Argentina’s focus on expanding 4G coverage and delivering superior service quality have enabled it to capture a greater share of stable, higher quality postpaid customers with greater data usage and lower churn. As a result, Telecom has a 32% market share of mobile revenues but a far greater 48% share of mobile EBITDA.

In cable and broadband Telecom Argentina is the undisputed market leader following the merger with a 56% market share of revenues. It is difficult to discern the exact share of profits because there are many smaller niche players in pay TV and broadband that do not provide profitability data. But, it is probably fair to guess that it is the most profitable given its far superior network in terms of broadband speeds. The second biggest competitor in Pay TV is Direct TV, which delivers its signal through satellite and therefore has limited capabilities in providing two-way internet broadband connectivity. The second largest competitor in broadband is Telefonica with less than half the scale of Telecom and relies mainly on an outdated ADSL network.

Telecom’s dominance is reflected in its EBITDA margins which, notwithstanding the macroeconomic shock, achieved a level of 33.5% in fiscal year 2018, superior to Comcast, Verizon, ATT, and most incumbent cable and telecom players globally. Furthermore, the merger synergies from combining functions such as CRM, IT, purchasing, which management assigns an NPV of $2.2 billion have not been fully realized because antitrust approval was not granted until July of 2018, delaying the implementation of certain measures.

Capital expenditures in 2018 were elevated at 25% of revenues. This was driven by an unprecedented push to deploy 4G sites and expand the Hybrid Fiber Coaxial network in order to gain coverage in areas where the two companies’ footprints did not overlap. Longer term, the plan is to maintain capex closer to mid to high teens of revenues in line with historical levels.

|

Comparable Capex/Sales |

2017 |

2018 |

|

Latam Telcos |

17.2% |

25.3% |

|

Global Telcos |

18.5% |

17.4% |

|

Global Cable TV and Pay TV |

14.7% |

13.9% |

|

Telecom Argentina (TEO) |

23.2% |

25.3% |

In summary, Telecom is a dominant mobile/cable/broadband service provider with a modern network, high margins, and a history of cash generation and dividend distributions operating in a relatively benign competitive and regulatory environment.

Balance Sheet

The company is conservatively capitalized. Telecom Argentina’s (TEO) net debt/trailing EBITDA is 1.2x. This is based on very depressed EBITDA. Cablevision Holdings’ net debt/trailing EBITDA when consolidating TEO and holdco debt is 1.35x again based on depressed EBITDA. If one adjusts the debt proforma for the acquisition of the minorities, it increases to 1.45x. Telecom Argentina (TEO) paid $988 million in dividends in 2018. This was an unusually high dividend. This year, it has paid $140 million thus far. Dividends payment this year will be lower due to the desire to maintain financial flexibility. Thirty nine percent of these dividends flow to Cablevision Holdings.

Valuation

The way I think of valuation is the following way. Historically, it has taken one to two years to recover pricing in US$ for telecom service providers in Argentina following a devaluation. Therefore, I think it is reasonable that in two to three years, the Company’s revenues will revert to US$6 billion and EBITDA will revert to $2 billion, the level attained in 2017. This is conservative because it does not account for any of the merger synergies. Management guided to a $2.2 billion NPV of merger synergies and this management has a four decades long history of successful acquisitions.

Applying an EBITDA multiple of 6x and use $2 billion of EBITDA (35% EBITDA margin), I arrive at an enterprise value of $12 billion which would result in a tripling of Cablevision Holdings stock. In the table below, the enterprise value of Cablevision has been adjusted to include the added debt associated with the mandatory tender of the Telecom Argentina (TEO) minorities. The tender is dilutive to Cablevision Holdings’ valuation given the 50% holdco discount.

|

Cablevision Holdings Price Targets (adjusted for mandatory tender of TEO minorities at $20/share) |

||

|

EBITDA |

Price |

|

|

Multiple |

Target |

Upside |

|

3 |

$5.95 |

0.9 |

|

4 |

$10.26 |

1.6 |

|

5 |

$14.57 |

2.3 |

|

6 |

$18.88 |

3.0 |

|

Note: Based on 2017 EBITDA of $2 billion |

||

If one looks at it in terms of EBITDA- Capex one arrives at a similar result. Comparable companies in the region trade at 12x EBITDA-Capex. Capex at Telecom Argentina is currently elevated at 25% of revenues due to the aggressive rollout of 4G and upgrading of the legacy Telecom network. I think a 15% EBITDA-capex margin is conservative based on history. Cablevision standalone historically operated at closer to 20%. If one applies the 15% EBITDA- Capex margin to 2017 revenues of $6 billion it generates $900 million. Comps in the region trade at roughly 12 that number. That would yield an enterprise value for $11 billion or a $23/share price target for Cablevision versus the current $6.32/share.

Conclusion

Having invested in Latin America for the past twenty five years, I have experienced wide and recurrent swings in sentiment and valuation. Consider the foreign debt of Argentina. The country defaulted on its dollar debt in 2002 paying only 37 cents on the dollar. In 2017 the country issued a 100 year maturity bond bond traded as high as 104 for a YTW of 6.85%. Today that “100 year bond” is trading at 77 cents on the dollar. I am not recommending Argentine sovereign debt because I think the probability of another default is not immaterial.

However, I believe Argentines, who are amongst the highest consumers of social media in the world in terms of hours spent online per capita according to a study by We Are Social, will continue to spend time online. As Cablevision Holdings improves the legacy Telecom networks, speeds will improve and usage will increase. The performance gap between the Cablevision/Telecom network and its major competitors will widen further. Cablevision will continue to capture the majority of higher quality premium customers leading to higher ARPU and lower churn than competitors. The economy will recover from current levels. Merger synergies will continue to flow through leading to a further expansion in EBITDA margin. Given the quality of the company and the quality of the management, once worries about Argetinian macro and politics have dissipated. the stock will trade at 6x EBITDA multiple at some point (versus the 8x multiple awarded by the market in 2017). This will result in a tripling of the shares sometime in the next 2-4 years.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

a) earnings recovery from trough levels

b) normalization of capex as a % of revenues

b) positive outcome in Argentine elections

c) economic recovery in Argentina

| show sort by |