| 2018 | 2019 | ||||||

| Price: | 9.39 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 12 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 112 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | -136 | EBIT | 0 | 0 | |||

| TEV (in $M): | -24 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- None found

- BETA

- IMMUNOPRECISE ANTIBODIES LTD IPA 02/28/2022

Description

Summary

Catalyst Biosciences (CBIO) is a biotech currently developing therapies for hemophilia. It currently trades at a ~$112M market cap, with $136M of cash on the balance sheet as of the most recent quarter, and no debt. The enterprise value is currently -$24M. Like all negative-EV situations, this is a bit messy and complex but I will try to lay it out in as concise and straightforward a way as possible.

Simply put, the stock trades as if its drugs are dead. After disastrous news in June, investors are not willing to look at CBIO until we get a little more clarity on the situation. The stock has been entirely tossed out and subsequent news has been broadly ignored. But, trading below cash, there is little room for the stock to go down. Owning this stock, you basically only lose as the company burns all their cash. You will win if the company can show that they have at least one legitimate drug candidate – it’s a race against the clock. Currently burning <$30M per year (T12M FCF was -$24M), CBIO should have over 4 years of cash; that is, the company should have at least a few years to do something compelling. I see three clear things ways that it might not take very long at all. If any of these scenarios play out, upside could be considerable:

- MarzAA continues to look like a legitimate drug and shows no cases of anti-drug antibodies.

- DalcA (aka CB-2679d) enrolls a Ph2b trial after the company concludes that the neutralizing antibodies are not as big an issue as they initially may have seemed.

- CBIO uses their cash to in-license something new and exciting.

The incredibly asymmetric risk/reward makes this stock attractive even if you think none of these scenarios are particularly likely. However, I think both of the first two scenarios are quite possible, and there are certainly other possible scenarios that could produce upside (such as a promising partnership or something from the dry AMD program, etc). The massive optionality that remains in the stock makes this a compelling value opportunity today.

A brief description of the company

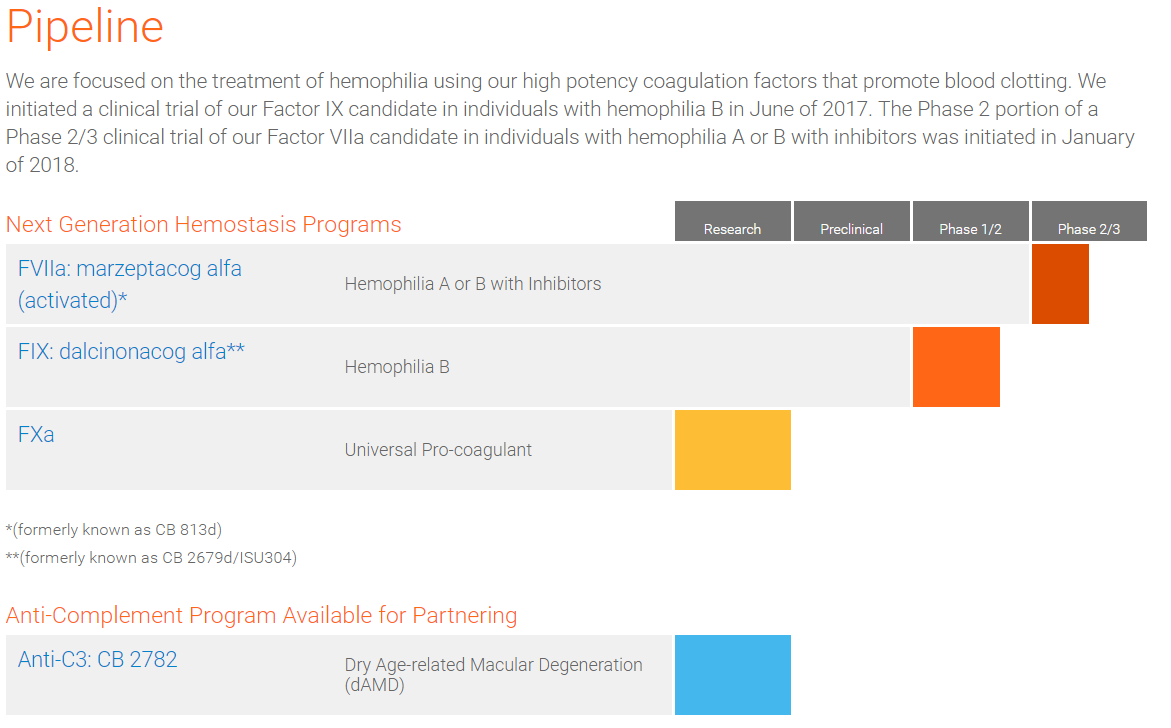

CBIO has two clinical-stage assets focused on the treatment of Hemophilia. Hemophilia is a rare genetic disease in which a patient’s blood does not clot because it lacks the necessary proteins called clotting factors. Hemophilia A patients lack clotting Factor VIII (FVIII), and Hemophilia B patients lack Factor IX (FIX).

The standard treatment for the Hemophilia is an intravenous infusion of the missing factor. This prophylactic treatment can prevent spontaneous bleeds as long as the relevant clotting factor circulates within the patient’s body at a high enough concentration. However, in some patients, because these clotting factors are not native to the patient’s body, the immune system produces antibodies that attack and neutralize the foreign clotting factor – these antibodies are called “inhibitors”. In hemophilia patients with inhibitors, Factor VIIa is an alternative clotting factor that can be administered to prevent bleeding.

CBIO is developing FIX and FVIIa products that can be administered by a subcutaneous injection (i.e. an injection with a small needle instead of an intravenous infusion directly into a vein). The factors are designed to have much higher potency than traditional factor injections which allows them to be injected subcutaneously; and they are formulated to provide different pharmacokinetics so that they last longer and produce a more constant exposure over time.

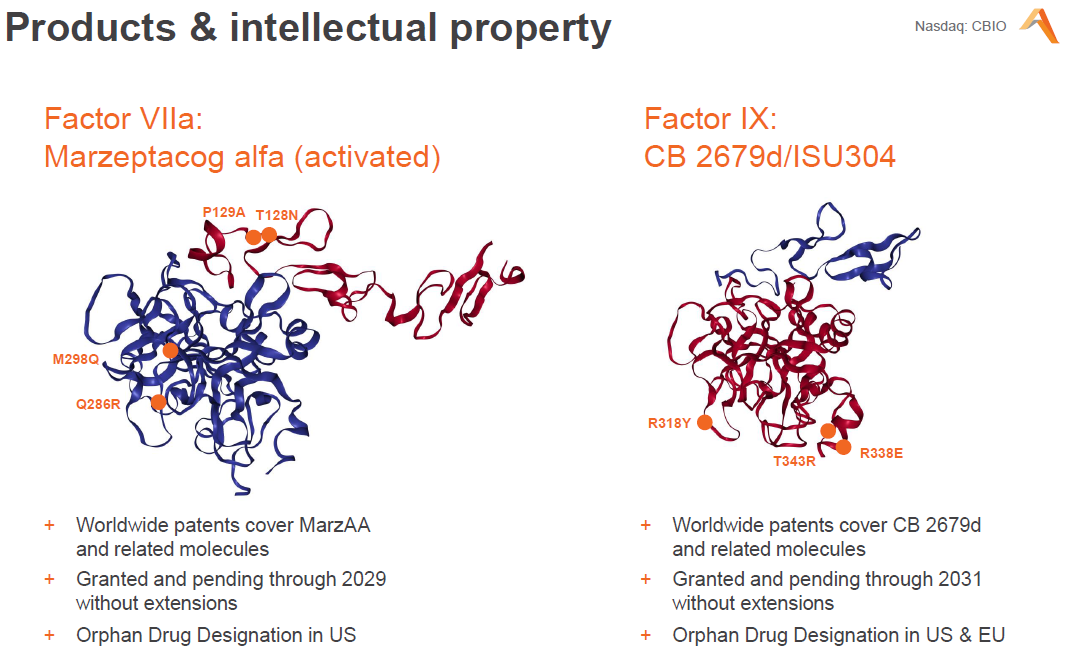

Marzeptacog Alfa Activated (aka MarzAA) is CBIO’s FVIIa product for use in Hemophilia patients with inhibitors. CB-2679d (recently named dalcinonacog alfa, aka DalcA) is the FIX product for use in Hemophilia B patients. These two product candidates currently form the basis for an investment in CBIO.

Clever amino acid substitutions in the factor proteins give the CBIO drugs their clinical utility. Compared with their respective natural proteins, MarzAA has 9x potency and DalcA has 22x potency. As such, only small amounts of protein need be delivered to achieve efficacy. The subcutaneous injection works by creating a depot (a small localized deposit) so that the drug is slowly released into the body, extending its half-life. Compared with intravenous injection, subcutaneous injection is much easier (it can quickly be administered by the patient or a parent) as compared to IV injection that requires a skilled insertion directly into a vein. It is also less painful and has the potential to produce a steadier level of drug exposure over time.

How did we get where we are today?

A year ago, CBIO shares traded near cash. As the company presented data from its phase 1/2 trial of DalcA/CB-2679d, the stock ran all the way up to the $30’s. The therapy looked to be maintaining therapeutic levels of FIX when delivered by either IV or SubQ injection. Intelligently, CBIO management used this run-up to issue equity, leaving them holding a large amount of cash. However, in June the company disclosed that moving to up to a higher dosage had caused two patients to develop neutralizing antibodies (nAb). This disclosure caused the stock to drop back to cash.

What does upside look like from here?

If either MarzAA or DalcA become an approvable product, CBIO’s fundamental value is much higher than here. Hemophilia has been a blockbuster orphan market for many years. Most hemophilia products are currently marketed by big pharma companies. Per the CBIO 10-K, worldwide sales of FIX products were at least $1.2B. And the sales of products for Hemophilia A/B patients with inhibitors were $2.2B in 2017.

As such, across their two pipeline candidates, CBIO addresses a multi-billion dollar TAM. CBIO’s more convenient injection and favorable pharmacokinetics should be enough to gain a modest chunk of their target markets. While there will continue to be competition, one would think that either product could do a few hundred million in peak sales in peak sales. At current valuation, it is very clear that CBIO gets no credit for either program. Let us just say that MarzAA and DalcA could each be a $200M/year drug.

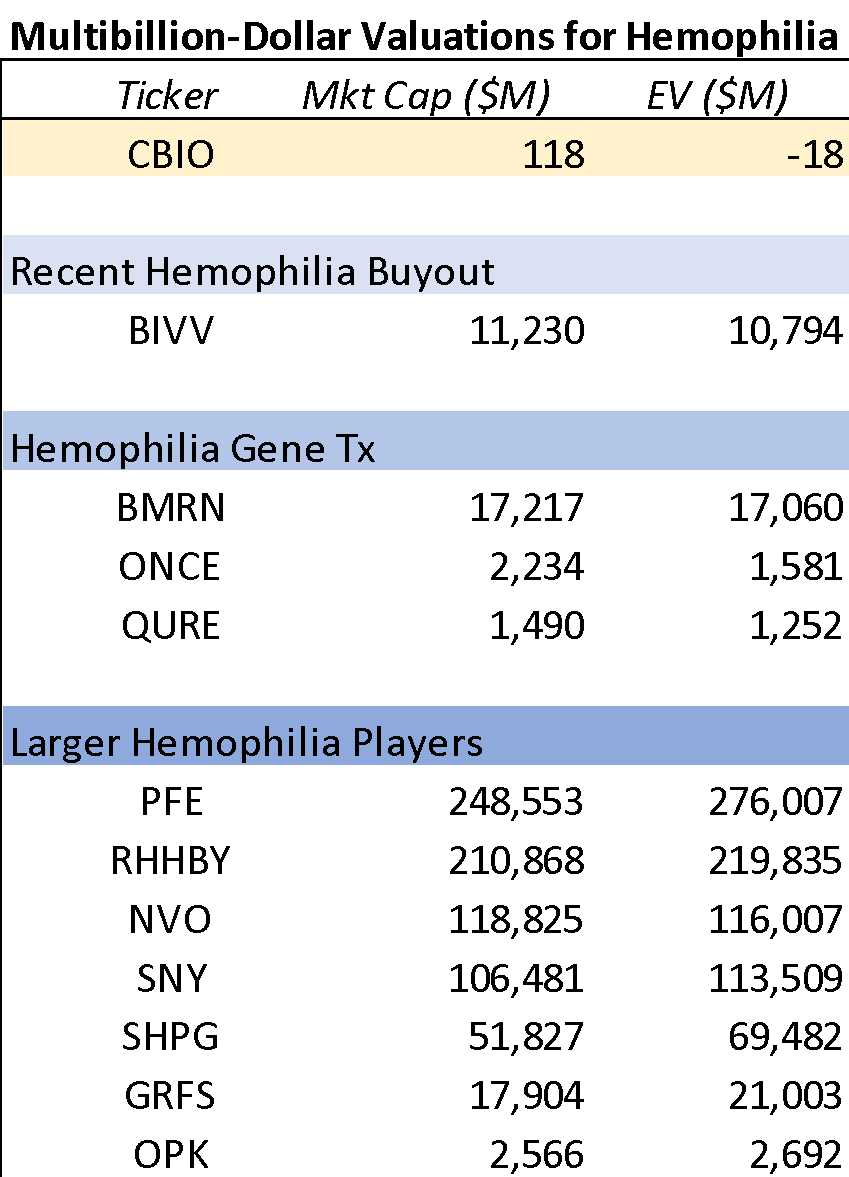

Orphan drug manufacturers often receive premium valuations. Look no further than the recent Sanofi acquisition of Bioverativ (the spinout of Biogen’s hemophilia assets). The $11B acquisition represented about 9.5x trailing revs – a clear premium multiple.

Some rough math on upside potential is as follows: a comparatively modest 5x sales would support up to a billion dollar valuation for either of CBIO’s two potential assets. Of course, you have to risk-adjust and discount back to present value: 10 years at a 10% discount rate is approximately a 60% discount, giving you $400m in un-risk adjusted PV. So, that is to say, if CBIO can convince investors that one drug has a 25% chance of hitting the market, then the equity should gain +$100M (~doubling in value).

But, neutralizing antibodies are a huge issue

The stock trades at cash for a reason. Anti-drug antibodies (ADAs) are a serious issue and can render a therapy totally inert. Even worse, the immune response could be potentially dangerous. In hemophilia patients, neutralizing antibodies can stick around and prevent the relevant factor infusion from working ever again. This can be a serious issue as, without their factor infusions, patients are once again susceptible to spontaneous bleeds that can damage organs and cause death. It is therefore potentially disastrous to induce neutralizing antibodies.

While other hemophilia factor injections do cause neutralizing antibodies (the so-called “inhibitors” mentioned previously), they must occur at an acceptably low rate for the drug to be viable. With only a handful of patients dosed so far with DalcA, it is hard to say exactly what the frequency of nAbs will be – especially because the therapeutic dosing regimen has not yet been fully fleshed out.

I do not think that the DalcA nAb issue is “no big deal.” However, I think the stock trades as if the observed ADAs are enough to kill both of CBIO’s two programs. Based on the fact set we have, I do not think DalcA is dead just yet, and MarzA certainly should not be dead. Specifically, I think that in the near term, if CBIO provides sufficient clarity on the nAb issue and starts a phase 2b trial of DalcA, the stock should appreciate meaningfully as the two assets both receive some sort of valuation.

What do we know about the FIX ADAs so far?

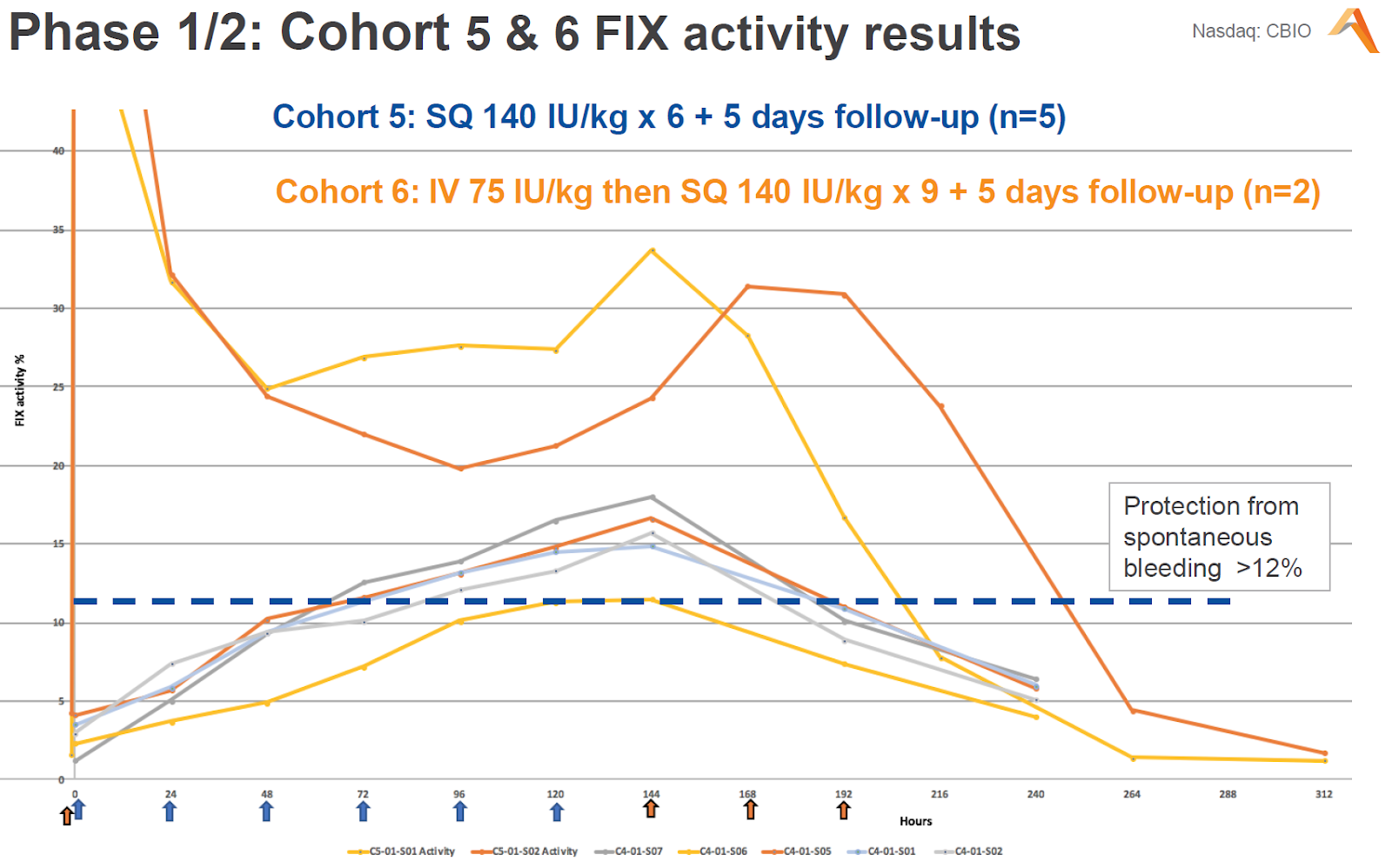

This is the most important set of efficacy data we have seen from CBIO’s CB-2679d FIX program. From this chart we can see that each patient in cohort 5 and 6 did achieve the therapeutically active level of FIX (12%). The cohort 6 patients were loaded with an initial IV dose that boosted their factor levels quite high. Daily injections for the next 9 days kept factor levels in the 20-30% range – a good outcome. However, the factor levels in both of these patients dropped as they developed anti-drug neutralizing antibodies – a very bad outcome. Furthermore, it was later disclosed that two other patients in other cohorts had developed ADAs that were not neutralizing. Here are the most important things we know about the patients and their ADAs:

- The nAbs appeared after the 8th or 9th injection in both patients of cohort 6.

The speed and consistency of the ADAs was initially very worrying. The fact that they occurred in two out of two patients treated with a higher dosing regimen means that the ADAs were almost certainly induced by exposure to higher concentration the drug.

- The cohort 6 patients were two Korean cousins who had also been part of cohort 5.

The fact that the patients had already been exposed to a lower dose of the drug and had not previously developed ADAs again indicates that the higher dose caused the problem. Or it could be that repeated exposure may have primed their immune system to respond to the higher cohort 6 dosing.

- One patient only had transient nAbs.

A modest positive point is that the first subject’s nAbs were below a quantifiable level at a follow up visit, while the second patient’s nAb levels dropped below 1 BU at a follow up visit (i.e. corresponding to only a <50% reduction in FIX activity). That is to say that the immune response was not incredibly strong, but certainly not to say that nAbs are a nonissue.

- The ADAs did not cross-react with wildtype FIX.

This is incredibly important. It is known that the FIX protein itself has fairly low immunogenicity – according to the CBIO 10-K, while up to 30% of hemophilia A patients develop inhibitors, only up to 5% of hemophilia B patients do so. As such, if the DalcA nAbs were traditional FIX inhibitors, then that would be incredibly worrying. If that were the case, then using DalcA would be putting patients at risk of being meaningfully worse off than if they had just gone with traditional FIX therapy. However, CBIO has stated that the antibodies that they found bind only to DalcA and to Furin (apparently a manufacturing component of DalcA), ignoring wildtype FIX. As such, the patients were able to discontinue DalcA and restart traditional FIX infusions with continued efficacy. Instances of anti-Furin antibodies are somewhat inconsequential and had already been reported in cohorts 1-4.

- It seems the Korean cousins were only identified as cousins during the company’s HLA typing and genotyping work.

Human leukocyte antigen (HLA) typing could be key, and based on management comments, it sounds as if the cousins had similar HLA typing. HLA is significant in mediating immune response and certain HLA types are often associated with autoimmune disorders. If it is confirmed that the cousins had similar HLA typing, it is likely that this contributed to them both developing nAbs to DalcA. If this is the case, then patients with different HLA characteristics might yet be viable subjects for a phase 2b.

- MarzAA has not caused any ADA’s yet.

Given the frequency with which DalcA seems to produce ADAs, it is somewhat comforting that MarzAA has not shown any. MarzAA has its own issues (one patient died during the trial), but given that the current phase 2/3 trial has shown 3 patients out past 44 days, if the ADAs were a platform issue, there’s a decent chance that we would have seen something there. At the very least, it seems that MarzAA can be administered at a therapeutic dose (even if DalcA can’t be) without causing nAbs: all MarzAA patients appear to have experienced a clinically significant decrease in bleeding rate.

- ISU Abixis was manufacturing the drug in Korea.

This ph1/2 DalcA trial was run by partner ISU Abixis in Korea, using product manufactured at their Korean facility. In contrast, MarzAA has recently been produced in Seattle by AGC Biologics. There is the potential that something about the manufacturing process is inducing the ADAs, and moving the manufacturing to a different facility could correct that issue. Some people have pointed out that the doses administered in this trial had been sitting around for over two years (in order to save cash). Furthermore, these older DalcA doses were manufactured by a slightly different process that has since been improved upon; in filings, management says they continue to optimize the manufacturing process for both drug candidates.

- The company is thoroughly investigating the ADAs and will update investors in October/November.

The company is not ready to throw in the towel, even though investors have. Of course, that is often the case in a biotech blowup and is not enough to conclude that we will get good news. However, it does mean that we will get some form of update in the imminent future.

Based on these facts, what can we conjecture?

It is entirely possible that there will be no fully clean explanation for the DalcA nAbs. However, before knowing anything further, we can make some broad guesses at potential factors that could be causing or contributing to the formation of nAbs. In order from best-case scenario to worst, a few possibilities are as follow:

- (1) The ADAs could be induced by manufacturing/product quality issues.

Both DalcA and MarzAA would be alive.

Given the known potential for manufacturing issues, this could be an issue that will be quickly resolved. In fact, the issue would likely have been fixed already by switching the DalcA manufacturing over to the Seattle facility and implementing an optimized manufacturing process. If this determination is made, the DalcA ph2b study could begin quite soon and the MarzAA phase 2/3 study would continue as planned. With two viable drug candidates, the stock has tons of room to appreciate.

- (2) The ADAs could be a product of immune response that is unique to patients with a certain set of genetic/immune characteristics (i.e. HLA).

Both DalcA and MarzAA would be alive, but potentially in a smaller population.

Because the ph1/2 study was run in a fairly genetically sequestered population, and the patients with nAbs happen to be cousins (seemingly with similar HLA), it is quite likely that the immune idiosyncrasies of the patients involved caused the high rate of ADA. This issue could be partly resolved already as the DalcA ph2b trial plans to enroll no Korean subjects. More work would likely be required to fully characterize the immune interaction, but hopefully the company could run the ph2b safely in a population with different HLA characteristics.

- (3) The ADAs could be caused by something unique to the structure of DalcA, (i.e. DalcA’s specific amino-acid substitutions versus wildtype FIX).

DalcA might be dead, but MarzAA would be alive.

Given that the observed nAbs target DalcA and not wildtype FIX, it is likely that the structural target of the nAb is one of the altered regions of the FIX protein. This could be a region that is unique to DalcA and therefore the immunogenicity would be unique to this product. MarzAA, with a different set of alterations, may not be plagued by the same issues. DalcA might need to be scrapped, but MarzAA could continue along its current development path. Clarity about this should allow investors to value MarzAA on its own merits.

- (4) The ADAs could be a systemic product of the CBIO platform.

Both DalcA and MarzAA would be dead, as would all other drug candidates.

For example, subcutaneous administration itself might just be too immunogenic for blood clotting factors to be administered in this way. Yes, the pipeline is worthless, but given that the equity currently trades for less than the company’s cash, how much further should the stock go down?

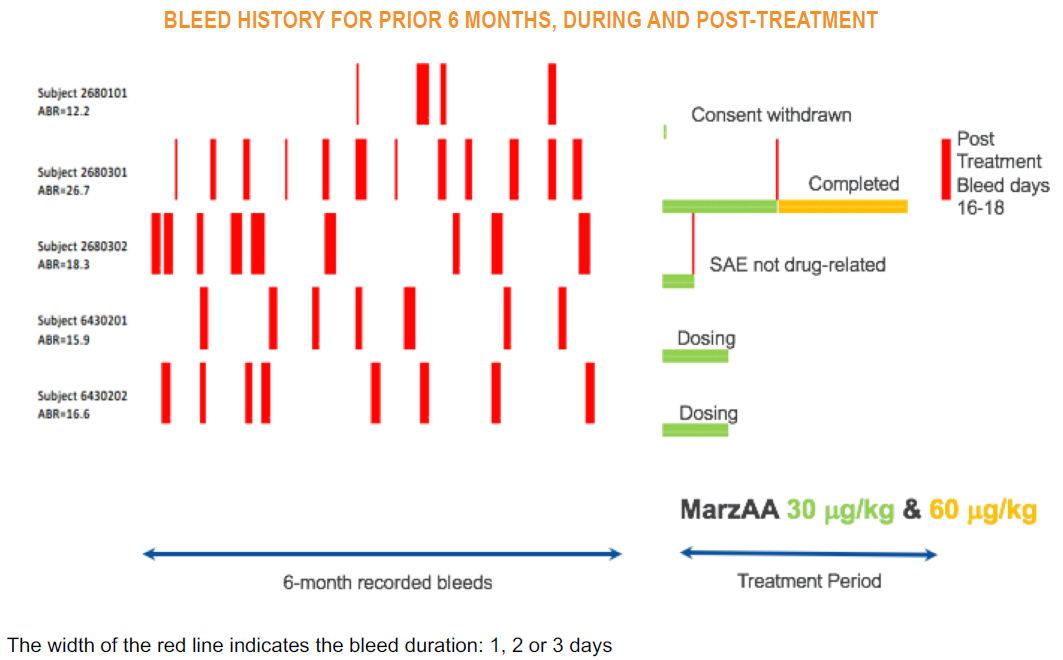

One last point: MarzAA currently looks like a drug

The current phase 2 part of the MarzAA study enrolls patients with a high annualized bleed rate (ABR), and then aims to find a dose of MarzAA that allows patients to go 50 days bleed-free.

The first patient to complete the study had a baseline ABR of 26.7 (i.e. a bleed every 13.7 days). This patient went 46 days without a bleed on the 30μg/kg dose. On day 46 the patient had a bleed and was then moved to the 60μg/kg dose; they then went the full 50 days with no bleeds. About two weeks after discontinuing the MarzAA treatment, the patient had a multi-day spontaneous bleed. This patient provides the clearest evidence of MarzAA’s strong clinical activity. They had only one bleed during the 96 days they were on drug (as compared to the ~7 that would have been expected in that timeframe) and resumed a normal bleeding rate once they were no longer being treated. Importantly the patient produced no ADAs despite 96 days of continuous dosing – including 50 days at a higher dose.

Two other patients are currently being dosed and have not yet experienced a spontaneous bleed at the 30μg/kg dose. Neither patient has shown ADAs. The trial is slated to enroll an additional 3 patients to show efficacy, and data should be presented at the ASH meeting in December.

The one questionable thing shown so far in this study is the patient who experienced a fatal adverse event while on drug. Specifically, this patient died of a hemorrhagic stroke on day 11 of treatment. The patient had a history of hypertension and had not been taking his blood pressure medication during the study. On the day of the stroke, he had not yet taken his daily dose of MarzAA. It is an unfortunate fact that a hemophilia patient with dangerously high blood pressure (recorded as 190/95) is at exquisite risk for this type of event. And mechanistically it is really the opposite adverse event (i.e. thrombosis) that one might worry an overdose of MarzAA would cause. Given that study investigator, physician and external safety review officer all concluded that the event was not related to MarzAA, I think it is safe for us to assume the same. As long as there are no further deaths in the trial, this unfortunate event should not preclude investors from seeing MarzAA as a viable drug candidate.

Investment Thesis

This is admittedly an ugly situation with little clarity. No, I do not know for sure whether the ADAs will spell the company’s demise. But the most important thing here is that investors are likely to be well compensated for taking on this uncertainty. I think that a path back to a $100-200M enterprise value is quite doable. At a fully diluted sharecount of 13.0M, and year-end cash of ~$120M, shares would trade between $17 and $25. I think CBIO stock currently prices in only a worst-case scenario (i.e. the aforementioned scenario #4). If the stock’s downside is a year of cash burn (<$3.5/sh), then $10+/sh of potential upside makes the stock an excellent risk/reward.

Based on the fact set we have, there is a very good chance that MarzAA will not be affected by the nAb issue; and current efficacy data makes it look like a legitimate product candidate. Because we have seen multiple MarzAA patients have no ADAs after being dosed for an extended period of time, and there are various clear explanations that point to a nAb issue that is unique to DalcA (or maybe even unique to that specific Korean ph1/2 trial of DalcA), I have reason to believe that that MarzAA will come out of this debacle relatively unscathed. This drug simply should not be valued at zero.

As for DalcA, near term clarity could swiftly give investors reason to believe again. While today I cannot pretend to know the root cause of the observed nAbs, I think that there are hints that the company will be able to identify a (somewhat) correctable cause of nAbs and enroll a new trial. At the very least, I think the probability of one of those scenarios is somewhat higher than 0%. If it is officially confirmed that the cohort 6 cousins share key HLA characteristics, I think it quickly becomes likely that company will be able to move towards an early 2019 phase 2b trial.

And even if both DalcA and MarzAA need to be scrapped, remember that the company is still sitting on a sizable chunk of cash and is therefore in an ideal situation to participate in an interesting reverse merger or in-licensing agreement. Specifically, the idea of a gene-therapy program would be extremely attractive in the current market environment. For example, look at the stock reactions of AXON and PTCT (+160%/$300M and +9%/$180M, for $30M and $50M acquisitions respectively) when they recently acquired gene therapy programs. If CBIO scrapped their existing programs and put their cash to use towards gene therapy, I would expect the market to reward them accordingly.

Furthermore, looking at the stock today, there is a near-term free embedded call option. If the company can provide clarity on the ADAs, then they will – the stock may respond quite positively. If they cannot do so, then then the stock will just continue to trade near cash. Either way, the stock’s current valuation affords plenty of room for everything to keep going wrong. If and when things start going right for the company, shareholders will be rewarded.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

ADA updates in October and November

MarzAA data at ASH in December

DalcA ph2b trial initiation??

| show sort by |