| 2023 | 2024 | ||||||

| Price: | 390.50 | EPS | 31.93 | 37.20 | |||

| Shares Out. (in M): | 148 | P/E | 12.2 | 10.5 | |||

| Market Cap (in $M): | 57,610 | P/FCF | 16.6 | 15.5 | |||

| Net Debt (in $M): | 96,430 | EBIT | 12,700 | 13,400 | |||

| TEV (in $M): | 154,040 | TEV/EBIT | 12.2 | 11.5 | |||

| Borrow Cost: | Available 0-15% cost | ||||||

Sign up for free guest access to view investment idea with a 45 days delay.

- CHARTER COMMUNICATIONS INC CHTR 07/18/2023

- CHARTER COMMUNICATIONS INC CHTR 05/11/2022

- CHARTER COMMUNICATIONS INC CHTR 08/06/2018

- CHARTER COMMUNICATIONS INC CHTR 11/02/2017

- CHARTER COMMUNICATIONS INC CHTR 12/06/2014

- CHARTER COMMUNICATIONS INC CHTR 01/28/2014

- CHARTER COMMUNICATIONS INC CHTR 07/31/2013

- CHARTER COMMUNICATIONS INC CHTR 04/05/2011

- BETA

- LIBERTY BROADBAND CORP LBRDK 05/27/2022

- Charter Financial CHFN 10/20/2001

- Genco Shipping and Trading Ltd GSTL 12/14/2005

- CAPITAL PRODUCT PARTNERS LP CPLP 08/02/2020

- Stelmar Shipping SJH 12/04/2003

- GENCO SHIPPING & TRADING GNK S 05/26/2011

Description

Charter Communications

CHTR $389.50

December 26, 2023

A Shrinking Moat and Questionable Capital Allocation Weaken the Investment Thesis for Charter

Summary

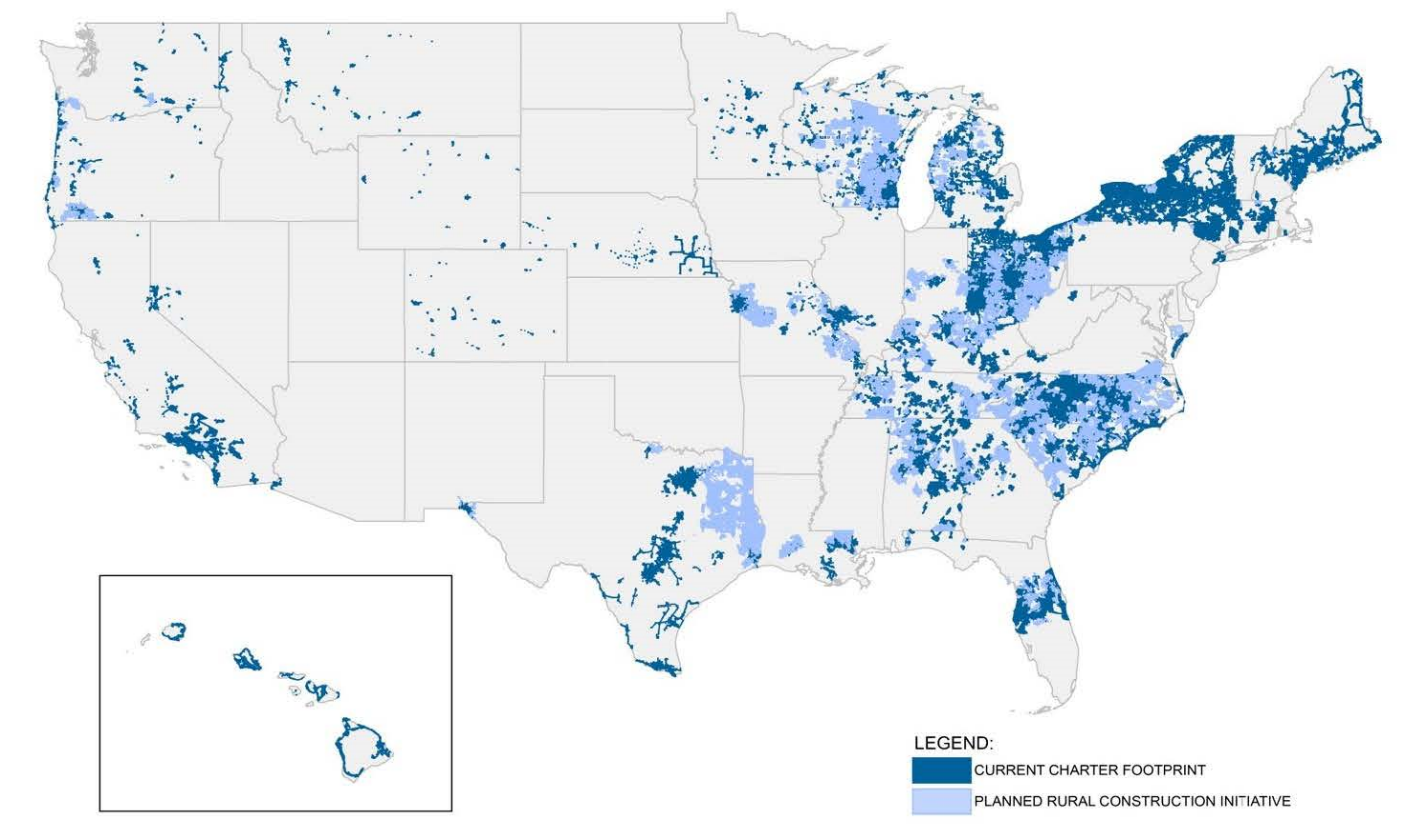

Charter Communications (CHTR) is the #2 broadband connectivity company and cable operator in America, serving more than 32 million customers in 41 states through their Spectrum brand. Their network passes over an estimated 55 million households.

The cable industry is mature and generates significant cash flow. However, the competitive moat around the business has shrunk as the industry faces true competition. Fiber overbuilders have established a position in almost half of Charter’s household passings. Fixed wireless providers are displacing DSL broadband in the rural markets that Charter is entering. This competitive dynamic has suppressed pricing power and has resulted in the need for continual capital investment to simply maintain its competitive position. These new investments are not likely to generate sufficient absolute returns, but they may be justified if their absence would cause further deterioration in the business.

Charter operates with an aggressive capital allocation strategy that is driven in part by management incentives that reward growth while ignoring the related costs. This is evidenced by Charter’s investment in low return capital projects, aggressive buybacks without regard to valuation, zero dividend policy, and a highly levered balance sheet.

The primary risks to the bullish Charter investment thesis include:

-

Rural Expansion: probable cost overruns and lower sales penetration due to fixed wireless taking DSL customers prior to Charter finishing their network buildout.

-

Low cash flow growth: increased competition impacting sales and pricing power, limited opportunities for further cost reduction, continued funding of low (and negative) return capital spending, and the difficulty of moving the needle of a large scale business constrain growth.

-

Capital markets: Charter needs favorable credit and equity market conditions to persist for highly-levered firms.

To invest in Charter today, an investor must believe that:

-

Growth will be above expectations, resulting from some combination of network expansion, pricing power, and cost savings.

-

Returns on capital spending including share repurchases will achieve acceptable levels of return.

-

Capital markets will remain favorably disposed to Charter’s leverage and management.

While it’s certainly possible that investors will continue to reward the company by focusing on artificial non-GAAP earnings, the risk profile of the business, combined with factoring in the cost of growth and buybacks as well as the agency issues, makes Charter an unattractive investment for a long-term investor at the current price.

Company Overview

Charter Communications (CHTR) is the #2 broadband connectivity company and cable operator serving more than 32 million customers in 41 states through their Spectrum brand. Their network passes over an estimated 55 million households.

Company History

Charter started as a Michigan cable company in 1980. In 1998, Microsoft co-founder Paul Allen purchased a controlling interest. Mr. Allen purchased cable assets in the late 1990s at what were then full valuations of $3000+ per subscriber. The acquired assets necessitated significant capital investment to expand the cable plant to offer broadband access to fulfill Mr. Allen’s “wired world” vision.

Mr. Allen combined his other cable properties with Charter and took the company public via an IPO in 1999. Charter completed 10 acquisitions in 1999 alone.

Capital expenses to build telecommunications networks are incurred well before revenue is received. The combination of high initial prices paid to acquire the cable assets, the significant capital expenditures necessary to upgrade the plant, combined with a slow build in consumer appetite for broadband pushed Charter into financial distress.

At the end of 2008, Charter’s debt stood at $21.7 billion while EBITDA for 2008 was only $200 million – a Debt/EBITDA of 109x – on revenues of $6.5 billion. Cash flow from operations was $400 million for the year and capital expenditures were $1.2 billion, yielding free cash flow of ($800 million).

Charter Communications declared bankruptcy in early 2009 and entered a “prearranged bankruptcy,” The company emerged from Chapter 11 bankruptcy in November 2009 after erasing $8 billion of debt and the new company was left with borrowings of $13 billion. Bondholders who exchanged $8 billion of debt ended up owning substantially all of the newly reorganized company. The public equity was wiped out although Mr. Allen remained Chairman.

In 2010, Charter stock was relisted on NASDAQ. In 2011, Mr. Allen stepped down and in 2012, Tom Rutledge, who was COO at Cablevision and previously at Time Warner Cable, became CEO.

In 2013, Liberty Media, led by John Malone – founder of TCI – purchased a 27.3% ownership in Charter largely by acquiring shares from investment funds that had participated in the restructuring. Liberty spun off the Charter holdings into Liberty Broadband (LBRDA) in 2014.

In 2014-2015, Charter prevailed in a bidding war for Time Warner Cable against Comcast. The deal closed in May 2016. This purchase made Charter the third largest pay-tv company in the US behind AT&T (DirecTV) and Comcast. Liberty Broadband invested an additional $5 billion in Charter to have a roughly 20% ownership stake in the combined company.

In 2012, Time Warner Cable and Comcast sold wireless spectrum to Verizon for $3.6 billion. The agreement had a clause that gave TWC and Comcast perpetual access to Verizon’s cellular network as a Mobile Virtual Network Operator (MVNO), essentially reselling access to Verizon’s network under their own brand. In 2017, Charter, who acquired the TWC agreement, started offering wireless services under the MVNO agreement as Spectrum Mobile, following Comcast who launched mobile service in 2016.

Verizon reportedly made a $100 billion offer to acquire Charter in 2017 that was spurned as inadequate.

Charter has aggressively bid for licenses to expand under the Rural Digital Opportunity Fund (RDOF) auctions. The RDOF, combined with state programs and the forthcoming Broadband Equity Access and Deployment (BEAD) program, is designed to expand broadband access into underserved and rural communities by offering licenses and subsidies to incent development. Charter intends to spend $6 billion from 2022-2025 for the RDOF, and likely will spend more through BEAD in 2025/6 – 2028/9.

In 2022, Tom Rutledge was succeeded as CEO by Christopher Whitney who had been COO since 2021 and CFO for a decade prior.

Business Segments

Charter reclassified its operating segments in 2023. It now reports Residential revenue, which covers Internet, Video, Voice, and Mobile; Commercial revenue which covers small and medium business (Internet, Video, and Mobile – although not broken out) and Enterprise; Advertising sales; and Other.

Video and wired Voice are in decline. Advertising sales are tied to Video and benefitted from political spending in 2022. Charter and Comcast established a joint venture, Xumo, to provide a streaming platform. Although Charter doesn’t break out profit by segment or product, Video margins are significantly lower than Internet margins due to programing and regulatory/access costs. The goal with Xumo is to provide a Video product to both create further customer stickiness as well as have a platform to capture advertising revenues as well as product sales revenues like it receives from QVC.

Leadership

Tom Rutledge was CEO from 2012 – 2022. Prior to Charter, he was at Cablevision and Time Warner Cable and joined Charter following its emergence from bankruptcy in 2009 and return to public equity markets in 2010.

Rutledge is considered a very effective operator and gets credit for the integration of the Time Warner Cable and Bright House acquisitions in 2016 which took Charter from $2b to $12b in operating cash flow.

Rutledge received some criticism in recent years for focusing more on financial engineering (Charter’s levered equity strategy) than on innovation.

In 2022, Tom Rutledge was succeeded as CEO by Christopher Whitney who had been COO since 2021 and CFO for a decade prior.

Rutledge’s exit was unexpected. Rutledge retained a position as Executive Chairman.

Rutledge attracted criticism for recent capital allocation decisions that are questionable, including repurchasing a massive number of shares at elevated prices in 2020-2021 in front of a significant increase in capital expenses. In addition, Rutledge aggressively pursued the RDOF auction, even though the reverse auction was compromised by unqualified parties bidding down required subsidies to a point that they are arguably uneconomic.

Whitney was a convenient, but not necessarily obvious choice to succeed Rutledge, if Rutledge was pushed out for his capital allocation decisions, Whitney played a supporting role. These capital allocation decisions would have been presented to the board, and Whitney seems committed to the same path, so it might be more likely that there was a personality dispute with the board rather than a strategic difference.

In December 2022, Charter – which typically doesn’t give many details to the investment community – held an investor day where they laid out in detail the projected increase in their capital expenses for the next three years while being light on the details of what the expected returns on capital might be. The stock fell -22% to $304 following the investor day.

What might have prompted Charter management to hold the investor day in December, when they could have simply disclosed their capex plans on the Q422 earnings call in late January 2023? It may not be coincidental that Charter prices its annual option grants in mid-January. In 2023, the grant date was January 17th, and the options are priced with a strike price at that day’s closing value of $388. These options have a 10-year life. The benefit to executives of a lower share price on the grant date is twofold: they get a larger number of options at a lower strike price.

In the January 2023 grant, Whitney received a $17 million options grant and Rutledge received a $15 million options grant, which seems rather generous considering he is no longer actively involved in the business. It’s hard to see this as anything other than a buy off, and likely relates to the fact that at the end of 2022, many of the executive’s options grants – including $90 million granted to Rutledge in 2020 – 2022 – were underwater.

In February 2023, Charter issued an additional and unique grant to the executive team, excluding Rutledge. Executives were granted a package of 90% options and 10% RSUs for 4x their January grants. Whitney received an additional $68 million grant at a strike price of $381. This grant is unique in that while there is a 5-year vesting period, accelerated vesting occurs at share prices between $500 - $1,000 by 2029.

A significant agency conflict exists between Charter management and shareholders. While both are rewarded for a higher stock price, Charter management is not being constrained by controlling risk. There is no return on invested capital criteria in Charter’s compensation structure. The rewards are solely tied to growth in revenues, EBITDA, expansion, and stock price. The executive incentives tied to the RDOF buildout are limited to achieving execution targets on the buildout, without regard to the capital cost or the returns achieved on said capital.

Charter management truly has been given a free call option on Charter’s stock price with virtually no restrictions on how it achieves that goal. This implicitly encourages risky capital allocation strategies that may well be contrary to the interests of shareholders who have invested capital and bear a risk of capital impairment if Charter fails to meet their stated goals.

Industry Analysis

The history of cable television dates to the 1950s. Many small operators obtained a license to deploy cable TV to a given geography. At the time, TV was primarily accessible through over-the-air antennas (satellite TV arrived in the late 1970s). While the cable provider had to spend capital upfront to build out the network, they had a captive audience as they provided a superior product to over the air (more stations, better quality) and they had an exclusive license from the municipality. As a result, penetration and growth was significant and provided the operator with a very steady income stream and high customer stickiness. As a monopolist, the operator had significant pricing power.

Three primary factors changed the competitive dynamics of the industry.

First, the networks shifted from analog to digital in the late 1990s, driving a significant increase in capital expenditures to essentially rewire the network. Cable still had a significant advantage as its broadband product was demonstrably superior to DSL over copper offered by the telcos. John Malone, an astute investor, sold the company he founded – TCI – to AT&T in 1998 for $4,100/subscriber. AT&T sold the assets to Comcast in 2001 – after investing significant capital to upgrade the cable plant – for $4,500/subscriber.

Second, inexpensive capital in the last 15 years resulted in selective overbuilding of fiber networks in the cable operators’ territories, bringing real competition for the first time as fiber is a superior product to cable in terms of both network speeds and maintenance cost. It’s estimated that Charter faces fiber competition in almost half of their 55 million passings.

Wireless providers started offering fixed wireless internet, providing additional competition at the low end and in rural markets. Fixed wireless has been successful in displacing DSL lines in rural areas (T-Mobile), muting its impact on cable net adds to date. However, this has significant adverse implications for the penetration rates and returns on Charter’s rural broadband expansion as the low-hanging-fruit of DSL customers may largely convert to fixed wireless customers before Charter can deploy broadband in those communities,

Increased competition has forced the cable operators to invest significant capital in further upgrades to remain competitive. Google’s launch of Google Fiber in 2010 was done explicitly to create the incentive for cable operators to invest in their plant to increase broadband speeds.

Charter has historically spent around $25/passing per year on network evolution to keep pace with the competition.

In December 2022, Charter announced that it would be spending an additional $100/passing ($5.5b) over 2023 – 2025 to further upgrade the cable plant to support multi-gig bidirectional speeds. No benefits were discussed relating to this capital deployment. I view this as an entirely defensive act to remain competitive with fiber that offers both higher absolute speeds, but also higher upload speeds than cable. There isn’t much current demand for multi-gig residential broadband, as most homes connect devices using wifi and neither the devices nor the wifi routers can rise above 1g speeds, and are typically able to sustain mid hundred megabyte speeds. Charter is investing today with the expectation that the demand will come, but that thesis appears risky and questionable.

Third, as television migrated towards streaming over the last decade, the cable operators lost video customers and were left offering a broadband product that, while essential to most households, is also viewed as a commodity product – and one that they increasingly have competitive offerings to choose from.

This combination of increased capital requirements, real competition, and less customer stickiness has eroded the quality of the cable business from exceptional to above average. Simply put, Charter’s competitive moat has contracted.

Industry Structure

There were 131 million households in the US in 2022. 65 million were traditional pay TV subscribers, versus 101 million in 2013. These subscribers have been declining by roughly 10% per annum and are forecast to fall to 48 million in 2027.

117 million households had broadband internet service in 2022.

A survey conducted by Leichtman Research Group in late 2022 of 1,910 adults in the US revealed the following observations:

-

90% of U.S. households get an internet service at home, compared to 84% in 2017, and 74% in 2007.

-

Broadband accounts for 99% of households with an internet service at home, and 89% of all households get a broadband internet service, compared to 82% in 2017, and 53% in 2007.

-

Individuals ages 65+ represent 34% of those that do not get internet service at home.

-

61% of those reporting speeds >100Mbps are very satisfied with their service.

-

40% of broadband households get a bundle of services from a single provider – compared to 64% in 2017, and 78% in 2012.

-

Among those that do not get an internet service at home, 58% also do not use a computer at home.

The implication of this data is straightforward: the broadband market is mature and well saturated. Most households that currently do not get internet service in areas where it is currently available are unlikely to until there is turnover at those residences.

In addition, as customers shift towards getting broadband only versus a bundle of services, their switching costs – which are limited to inconvenience rather than financial – decrease, making them more susceptible to switching providers. The counterpoint to this is that with the majority of those with high-speed broadband being very satisfied with their service, the inducement necessary for them to switch providers is increasing – and probably at least as driven by a negative experience with the incumbent as a competitor’s promotional activity.

Over the last 20 years, broadband has shifted from local monopolies to local oligopolies. In any given market, there are a few competitors selling an undifferentiated service. Each seller has a high percentage of market share and cannot afford to ignore the actions of the others. There are relatively high barriers to entry. This creates an environment where broadband providers have limited control over setting prices independently, but the high capital costs and limited number of competitors should lead to a stable, rational pricing model. Occasionally, new entrants will emerge – often at the lower end of service quality (fixed wireless) – and try and pick off the low end of the market with aggressive pricing, but these entrants often run out of capacity and capital to be more than a periodic nuisance.

Broadband has become a critical utility for most, equivalent to electricity. Yet broadband remains largely unregulated in comparison to electric utilities.

Competitive Dynamics

Charter had 32 million customers in 2022, representing 58% of the 55 million homes passed by its network. Comparing company data to country data is not apples to apples, if we use the national data as a proxy, most of the remaining homes passed in Charter’s network (and this is true for all providers) are current broadband customers of a competitor.

In the 2022 and 2023 earnings calls, Charter and Comcast have called out the current suppression in customer mobility (people moving residences) as weighing on net adds. This reveals both the stickiness of the product (people usually select an internet provider upon move in and rarely change providers) and competition (Charter needs people to move in the hope of retaining the business of homes that were previously Charter customers as well as winning business away from homes that were previously customers of a competitor.

Aside from the subsidized rural expansion, there are limited greenfield opportunities. New housing starts have been roughly 1.3 – 1.4 million per year. The vast majority of these are in new housing developments, which often have multiple broadband providers wiring the neighborhood at inception, providing competition from day 1.

The existence of competition has both raised capital intensity by the frequent need to upgrade the plant to remain competitive as well as limiting pricing power.

What are emerging trends? Threats?

Emerging trends include the convergence of wireless and broadband which presents both an opportunity and a threat.

The wireless operators own radios on leased towers connected by either leased or, increasingly, owned fiber. They have a wired broadband network, with a wireless connection to their customers. They are not well positioned to deploy fiber from the towers into homes, but they do offer a competing broadband product – particularly appealing at present to the low-tier consumer and to small businesses with modest broadband needs.

The broadband providers have a hybrid-fiber-coaxial (HFC) network with fiber to the neighborhood and coaxial cable to the home. In homes served, the cable modem/Wi-Fi router also serves as an external hotspot offering Wi-Fi to customers passing by. This has allowed for the Charter and Comcast to enter the wireless market utilizing a combination of leased wireless capacity from Verizon and offloading as much traffic as possible onto their owned Wi-Fi network where there is minimal marginal cost.

Charter and Comcast have a unique agreement with Verizon giving them access to Verizon’s mobile network. In the last few years, both have rolled out their branded mobile service as an MVNO utilizing Verizon’s network. These efforts are best viewed as a low capital cost trial. The MVNO agreement is said to be priced on a $-per-gig basis, creating a strong incentive for the cable providers to offload wireless traffic onto their networks at low marginal cost. Both operators have been successful at this and are offloading 75% - 85% of traffic onto their networks.

The near-term goal of offering mobile wireless service is to create additional customer stickiness by making it more inconvenient to change providers when multiple services are involved.

The long-term goal of offering mobile wireless is a belief that ultimately there will be a convergence of wireless and wireline broadband. Rolling out wireless under the MVNO agreement allows the cable providers to build a customer base while expanding their knowledge and capabilities. At some point, they may achieve enough customer scale to start installing their own wireless radios to move away from reselling Verizon’s network. Alternatively, in a more relaxed regulatory environment, there is the potential for a merger between a wireless operator and a cable operator.

Mobile is currently a loss leader. Customer acquisition costs including zero-interest financing on phones and 1st year teaser prices creates an upfront cost that expands as Charter accelerates growth. In 2022, mobile operating losses were $1.1b on top of $0.5b in capital expenses. Charter claims that after excluding customer acquisition costs, it is achieving Adjusted EBITDA margins of 18%, which remains well below the 40% margins for the broadband business. Mobile can drive growth in revenues and profits, while achieving a lower ROIC than the legacy business. Management states that a big reason for offering wireless is to increase customer stickiness, which has been reduced by the secular shift away from cable tv towards streaming. Offering a bundled package increases customer switching costs.

Rural expansion is the largest greenfield opportunity for broadband and supported by subsidies at the federal and state level. At the federal level, there are two main programs: The Rural Digital Opportunity Fund (RDOF) and the Broadband Equity Access and Deployment (BEAD) program. The RDOF will offer up to $20.4 billion over ten years to subsidize the construction of broadband assets into rural communities. Only $9.2 billion was allocated in phase 1 and it is unclear what will happen with the remainder. Charter is the largest winner of RDOF subsidies. The BEAD program is part of the 2021 JOBS Act and will offer up to $42.5 billion for the construction of high-speed internet in rural areas. The funds are allocated to the states to distribute to operators. Building under the BEAD program should commence in the 2025-2026 timeframe.

The attractiveness of these initiatives to the cable operators is greenfield expansion with subsidized construction costs. There also is a prevailing sense by Charter that it’s a defensive move – if they didn’t build it, a competitor would. This should result in high penetration rates. In addition, subsidies are available to low-income households that should further boost adoption. The disadvantage is that because of the lack of household density in rural markets the cost per passing is forecast at $5,000 - $6000/passing – which is why these communities have historically been underserved.

As with mobile, the challenge with rural lies both in the magnitude of the opportunity and achievable returns on capital. Charter passes 55 million households with its broadband network. Adding an additional 1.3 million passings represents only 2.4% growth and a capital investment of $6.7 billion. While the investment occurs over 3 years, the subsidies are paid out over 10 years, lowering the return on capital. Construction costs are far more likely to exceed their estimates than not. With T-Mobile aggressively offering fixed wireless to convert rural DSL customers to an acceptable broadband product for most households before Charter can build out its network, the likelihood that Charter’s penetration rates may fall below the levels necessary to earn an attractive investment are high.

Financial Summary

How does the company make money?

Charter provides telecommunications services including broadband internet, video, voice, and mobile to homes and small businesses for a monthly fee.

What are the drivers of growth? And how have they evolved over time?

The primary drivers of growth are users and pricing. User growth has slowed as broadband has become a mature market. The rapid adoption of broadband over the last twenty years has hit a 90% threshold. The remaining 10% (13 million households), is split between the unserved (which is addressed by the rural broadband initiatives) and those who choose not to purchase broadband. The latter households are likely to convert to broadband users over time with generational change.

Pricing is relatively stable due to competition in most markets. Typically, discounted prices are offered to new customers for a year. Charter does not disclose ARPU by product. Residential ARPU increased 1.9% in 2022 and SMB ARPU was flat.

In mobile, Charter is expanding rapidly by offering plans that dramatically undercut most wireless providers. Since the beginning of 2021, Charter has added 4.3 million mobile lines and had 6.4 million mobile lines as of 6/30/23. They are offering one line for free and two lines at $29 for the first year. T-Mobile has questioned Charter’s growth, suggesting that their net adds are not coming at the expense of other wireless providers. Given that the mobile market is mature with very high penetration, there is some question as to the sustainability of this growth, particularly as customers roll off their free year.

What is the runway for growth?

Broadband is a mature market, with high penetration in urban and suburban areas in the US that are often served by multiple providers due to the fiber overbuilding by telcos and independent operators like Google Fiber. Pricing power is limited, and discounts are regularly offered to new customers and to retain existing customers who call to cancel or downgrade their service.

There is a revenue headwind on video and voice services due to the secular shift towards video streaming and wireless telephony, but this has a modest impact on profitability and cash flow due to the programming and regulatory costs associated with video services.

Growth might pace GDP at 2-3% per year due to customer growth and price increases.

There are two primary growth avenues for the cable providers: mobile and rural.

The largest growth opportunity is rural expansion. Rural markets have historically been underserved with broadband access due to the low density of households making the potential return on massive capital costs unattractive. In recent years, the federal and state governments have taken action to provide incentives for rural broadband deployment.

The first large program is the RDOF which is being built out from 2022 – 2025. The BEAD program has the potential to be 2-3x larger than the RDOF with construction commencing in 2025-2026.

The challenge with rural expansion is in both the high capital cost and the scale of the legacy business. Charter expects to spend $6.7b just to pass 1.3 million households – which represents 2.4% growth on its current footprint. There is likely $600-1000 in additional costs per connection from the road to the home inclusive of customer acquisition costs, customer premise equipment, and installation. The subsidies are spread out over 10 years creating a mismatch with the capital investment required. Year 1 ROIC ranges from 1.7% to 3.9% at 40% - 60% penetration, with Year 2 ROIC expanding to 6.4% to 10.8% as the installation costs are not recurring. This equates to only a 1.4% - 2.8% increase in intrinsic value using current valuation multiples (and factoring in the expected buybacks in 2023 – 2025). The only way that Charter can achieve the mid-teens returns on capital that it is forecasting is with very high penetration rates. The incursion of fixed wireless into these communities should temper the ability of Charter to achieve penetration rates much above 60%. Going beyond 60% may well incur higher customer acquisition costs. In addition, there is a high probability that the construction costs will come in over budget, further deteriorating returns.

This reinforces my position that Charter’s rural expansion is primarily a defensive strategy to preclude other providers from securing that territory.

How does management allocate capital?

Charter has an aggressive capital allocation strategy which is likely influenced by how management is compensated.

The business is mature, and the company typically generates more cash flow than it can reinvest at attractive returns. Many other well-known and regarded companies, like Coca-Cola, are facing similar situations. What sets Charter apart is the aggressiveness of their levered equity strategy. Charter management intends to maintain their Debt-to-EBITDA at the upper end of a 4.0x – 4.5x range.

In the absence of paying a dividend, management’s investment priorities are organic investments and acquisitions at attractive returns, and share repurchases. Not only is their capital allocation strategy aggressive, but their philosophy constrains their options and is predicated on the assumption that they will always be able to access debt capital on attractive terms.

In most periods, they will have excess free cash flow after capital expenditures. They have tied their own hands to use the residual cash flow for share repurchases – regardless of the attractiveness of their stock as an investment at the prevailing valuation. They have chosen not to let cash build on the balance sheet or to pay down debt given their leverage target.

Charter does not intend to pay a dividend, presumably for two reasons: tax efficiency and management incentives. Charter’s management is compensated primarily through stock options.

There is a significant agency conflict between management and shareholders. Management is compensated through salary, cash bonus, and stock options. The cash bonus targets are for revenue and EBITDA growth, with no provisions for returns on invested capital. Stock option grants have a unique feature in that the vesting of the options is tied to stock price appreciation.

A compensation structure that rewards stock price appreciation might create the perception that management and shareholders are aligned, but a thoughtful analysis reveals a more complicated truth.

Charter’s compensation structure creates a very asymmetrical incentive for management that diverges sharply from the interests of shareholders. The key difference lies not with the reward structure, but the incentives for risk management.

Charter’s management has the incentive to be very aggressive in running the business for maximum share price appreciation and is reflected in their capital allocation strategy. Stock prices are reduced by dividends paid, so they refuse to pay a dividend. Returns on equity are amplified with leverage, so they elect to stay aggressively levered. Share repurchases increase per share earnings, so they aggressively repurchase stock – occasionally utilizing debt – regardless of the prevailing valuation.

The incentives offered to Charter’s management encourage risk taking and a shorter-term focus than a long-term owner. Paradoxically, there may also be an incentive for continually investing growth capital in the business as it masks what steady state cash flow might be, allowing management more latitude in pushing its growth narrative.

This is illustrated by comparing the capital allocation of Charter and Comcast over the last few years. Both businesses are mature and generate free cash flow that is partially utilized for share repurchases. During 2020-2021, both stocks rose sharply as pandemic-induced demand lifted earnings. Since closing the Time Warner Cable acquisition in 2016, Charter has repurchased stock in amounts greater than free cash flow in each year, borrowing to do so.

In 2019, Charter had free cash flow of $4.6b and repurchased $6.9b in stock. In 2020, free cash flow increased to $6.6b and Charter repurchased $11.2b in stock. In 2021, free cash flow increased further to $8.7b and Charter repurchased $15.4b in stock. In 2022, free cash flow fell to $6.1b and Charter repurchased $10.3b in stock. Charter’s stock at the end of 2019 was $485 and peaked at $821 in August 2021. The vast majority of the $36.9b in shares repurchased in 2020-2022 were at prices well above the current quote, while Charter’s debt increased by $18.8b.

Contrast this with Comcast, run by Brian Roberts who holds $6b in stock and his family’s legacy. Comcast has a more diversified portfolio including NBC Universal with television, movie studios, and theme parks. Comcast repurchases shares but also pays an annually increasing dividend.

Comcast’s executive compensation metrics include return on invested capital, rather than rewarding growth without regarding its cost.

In 2019, free cash flow was $13.3b, dividends paid were $3.7b and shares repurchased were $0.5b (shares repurchased were $5.3b in 2018). In 2020, free cash flow fell to $13.1b (theme parks were closed), dividends paid were $4.1b, and shares repurchased were $0.5b. In 2021, free cash flow increased sharply to $17.1b, dividends paid were $4.5b, and shares repurchased were $4.7b. In 2020 – 2021, debt was reduced by $9b. In 2022, free cash flow fell to $12.6b, dividends paid were $4.7b, and shares repurchased were $13.3b. While Comcast carries a significant debt balance of $94.8b at the end of 2022, cash flow from operations was $26.4b and free cash flow was 12.6b, debt to free cash flow is 7.5x vs 16.3x at Charter.

Charlie Munger said, “Show me the incentives and I’ll show you the outcome.” Comcast and Charter, while in the same business, are managed very differently. Charter is managed very aggressively, while Comcast is much more conservatively managed. I believe that this is driven by the different incentives in place at each firm. Comcast is managed and controlled by its founding family, who owns an exceptional amount of equity outright. The owner-operator tends to behave in a risk-adverse manner and focused on the long-term. Charter is managed by outside managers who literally hold call options on the stock. Their risk is modest if they fail, and their rewards are great if they can pump the stock price up at the right time. Charter’s capital structure and investment priorities are completely rational when viewed through the lens of incentives.

The question that matters most is whether it’s a rational investment for a long-term investor.

Risk Analysis

What are the key threats to the business?

I believe that the economic moat around Charter’s business today is smaller than it was twenty years ago. While competition is intense, it may stabilize and possibly easing in the near term.

Fiber overbuilding is exceptionally capital intensive (particularly when cables have to be buried), and further activity can be expected to be reduced as the current interest rate environment makes such projects less attractive. Fixed wireless offerings use up excess spectrum capacity without incurring marginal capital costs. As network traffic grows, further capacity additions will require additional capital, potentially slowing growth. Anecdotally, I think fixed wireless has likely had some success in urban/suburban markets with small businesses that have modest internet requirements. Charter’s business internet is essentially a high-priced version of entry level internet service, making them vulnerable to being picked off by a low-cost offering like Verizon has. Fortunately for Charter, business internet is a much smaller business than residential internet.

Verizon has focused on offering fixed wireless in urban/suburban locations while T-Mobile’s fixed wireless has been aggressively offering service in rural communities. T-Mobile’s strategy is superior because the excess network capacity in rural markets is higher and they are competing against an inferior DSL offering, whereas Verizon is competing against cable and fiber offerings. The risk to Charter is that rural broadband penetration assumptions are driven by the belief that they will be competing against DSL. To the extent that T-Mobile can capture and convert that DSL customer to fixed wireless before Charter enters the market, will reduce the penetration rates, increase the cost of customer acquisition, and ultimately reduce returns on Charter’s rural expansion initiatives.

I believe that in the absence of regulatory barriers, that the broadband and wireless industries are headed towards convergence. Wireless providers have been running fiber between their cell towers to lower their cost of using leased lines.

I think the larger threats to Charter are driven by their own strategy. They manage the business and their capital structure very aggressively. Like a race car, they built it to go fast, but race cars going fast tend to break far more often than the family sedan.

Charter’s debt at the end of 2022 was $98b, compared to cash flow from operations of $15b and free cash flow of $6b. Charter has outspent free cash flow on share repurchases using borrowed capital. Capital markets have accommodated Charter carrying a debt load of 4.5x Adjusted EBITDA when capital was readily available at low cost. Any adverse change in capital market conditions that would impair Charter’s access to the credit markets would be a significant problem. Currently, Charter’s debt is yielding about 200bps higher than the coupon rate across the yield curve. Charter’s year end 2022 debt stood at $98b. To refinance this debt at current yields – ignoring the possibility of further interest rate movements – would cost $2b pretax and $1.6b after tax, reducing 2022 cash flow from operations by 11% and free cash flow by 26%.

Charter’s high debt load is predicated on the presumption that it will grow free cash flow rapidly, however, that is far from guaranteed. While high speed internet has become as essential to most households as power or water, it’s unclear how much pricing power exists in a competitive environment, where the established practice is to attract and retain customers by offering discounts.

It's clear that household data consumption will continue to rise. For example, NFL Sunday Night Ticket is moving from DirecTV to YouTube TV this fall, which should massively increase streaming data consumption. What’s unclear is whether the cable providers can increase prices to reflect the increased value provided.

The returns on investment capital for the rural broadband initiatives might be disappointing. The RDOF was a reverse auction where bidders competed against each other for the lowest subsidy amount required for a given area at a time when capital markets were flush with cheap capital. Subsequently, many auction winners have defaulted on their ability to actually construct the network in part because of the sharp increase in construction costs over the last few years.

Charter was one of the most active participants in the RDOF auction process. Comcast, passed on the RDOF auction, but is participating in the state programs and the BEAD program. Comcast President Mike Cavanagh discussed their position at the Morgan Stanley Technology, Media & Telecom Conference in March 2023:

"We looked at it as a frothy capital market, lots of bidders driving prices to levels that I would say were not necessarily natural," he explained. "That doesn't mean players that got what they got won't do well, but that was a dynamic on our minds… We wanted to see a little more maturity in the bidding process."

Charter’s CEO, Christopher Winfrey offered his views on how the market should view Charter’s capital allocation at the MoffettNathanson conference in May 2023:

“…the payback is long. But if you think about it in typical what we could call John Malone math, after four years or so, if you think about it in terms of corporate finance valuation payback, your EBITDA multiple, it’s a four-year payback…If you have a higher multiple, you get there faster.”

He is effectively saying: “If I invest your capital and generate growth (regardless of whether the ROI is attractive), and you value that growth at a high multiple, you should be pleased with my efforts on your behalf.” Let’s say you invest $10b and generate $1b in sustainable cash flow in return. The ROI is 10% which is below my cost of capital, making this a negative NPV project. However, if you value my cashflow at 10x, then my enterprise value is unchanged, and you should be content with that result. That pretzel logic should be discomforting to both equity and credit investors.

The customer penetration rate required for the rural initiatives to generate acceptable returns is increasingly under threat given the expansion of fixed wireless broadband offerings into rural markets by T-Mobile. Guidance has been to 40% penetration, but I would guess that Charter was internally forecasting 80%+ penetration rates, given the competitive landscape and the fact that governmental subsidies of $30/month make the entry level option free to the low-income household. However, those forecasts and the RDOF bidding occurred prior to T-Mobile’s fixed wireless entry. Given the high capital costs, the risk that take rates fall short, that competitive providers enter select rural markets eroding penetration and pricing power, or increased investment costs hinder the ability to earn an attractive return on investment is a real threat.

It should be no surprise that Comcast factors return on invested capital into executive compensation while Charter does not.

Whenever the cable providers ramp up capital spending, they often say that in a few years, the plant will need much reduced capital spending. In practice, the industry is characterized by wave after wave of capital spending. Cable providers were some of the first managements to steer investors towards alternate “profit” metrics that made their investment case appear stronger. Investors who focus on earnings before costs do so at their own peril. The RDOF program should be completed by 2025. The BEAD program which could be 2-3x the size of the RDOF should commence shortly thereafter, continuing the capital investment cycle.

There is a remote possibility of regulatory risk. The cable tv/broadband and wireless industries grew without the regulatory framework of power and telecommunications industries. However, with broadband and wireless now as integral to the lives of most Americans as electricity, and with the broadband providers now taking construction subsidies from the government, there is always the possibility that the political and regulatory climate evolves to a point where these businesses become subject to rate regulation.

How might these risks be mitigated?

I think the biggest threat is the aggressive management of the capital structure and the pursuit of low return capital projects and this can be expected to remain intact unless and until circumstances force them to change.

I believe that Charter would be rewarded by the markets for lowering its risk profile by tying share repurchases to valuation, paying an increasing dividend, and linking management incentives to returns on invested capital. I do not foresee any of these actions being implemented.

Valuation

How do you value this business today?

The cable industry has always been challenging to value for several reasons. The business requires significant capital investment in advance of revenue and cash flow. The story that is sold to the equity and credit markets stresses the stability of the cash flow and the expected growth in that cash flow over time. While the growth story has played out, it has always been accompanied by increasing capital spending and the resulting expansion of debt.

There is some cyclicality in the underlying business, but there is far more cyclicality in the capital investment cycle and investor perceptions.

In the late 1990s – early 2000s, cable companies were operating with much higher leverage 9x+ for charter and 6x+ for Comcast and trading at valuations of EV/CFO over 40x (there was no free cash flow). Investors were sold on the growth story, particularly relating to broadband.

The industry has always been at the forefront of pushing investors to look at non-GAAP financial metrics like enterprise value/customer and Adjusted EBITDA, to achieve and sustain a higher valuation, which would allow them to access greater leverage to fund further expansion and upgrades.

The industry has had relatively few years of declines in operating cash flow, although free cash flow is more variable due to capital investment cycles.

Instead of utilizing non-GAAP metrics for valuation, I prefer using GAAP cash flow metrics. Ideally, free cash flow is utilized although this is compromised by the volatility in free cash flow. Operating cash flow is much more stable and can be estimated as a margin on revenue.

This table illustrates the relative stability of CFO as a percentage of revenue. Charter has outperformed Comcast in this regard, likely because of their less diversified business portfolio. Conversely, the stability of Comcast’s diversified portfolio combined with lower leverage, is reflected in the higher multiple investors have afforded it.

One challenge in valuing Charter is determining what an appropriate valuation metric is in future years. While investors were willing to accept lower earnings yields during a period where interest rates were low, it is rational for investors to demand higher earnings yields during periods where interest rates are relatively higher – and this impact is likely to be exacerbated for leveraged enterprises.

Charter’s long-term debt yields over 7.25%. An equity holder should demand a higher earnings yield baseline, excluding growth. A free cash flow yield of 10% - 15% absent growth options seems warranted, particularly given the leverage risk. To estimate free cash flow absent the impact of growth initiatives, I add back both the cash flow and capital expenditures relating to both mobile and line extensions. This takes free cash flow from $5.5b as reported in 2022 to $10.0b. FCF yields of 10% - 15% imply an intrinsic value of $446 - $669 per share.

At 15% FCF yield, the intrinsic value is 16% above the current quote, creating the appearance that Charter is being priced by the market as if it isn’t growing. This argument has been advanced by Charter’s management in favor of the stock given their growth forecast. Growth is not free, so let’s examine how the valuation might change when factoring in the cost of growth.

For a perpetuity, an investor’s required yield will be reduced by the rate of growth. A 15% steady state FCF yield required should fall to 13% if there is an expectation for 2% growth in perpetuity. It is likely that Charter can grow its steady state free cash flow by 2% - 4% per year, but only with continued capital investment.

But for the sake of argument, let’s assume that Charter can grow by 2% in perpetuity, lowering the required FCF yield to 13%, and let’s factor the cost of said growth in the equation. Total growth capex from 2023 – 2025 is $15.1b.

I am utilizing consensus revenue estimates for 2023 – 2025 and estimating CFO at 28% of revenues. Note that free cash flow not only drops significantly in 2023, which is well understood, but it drops sharply again in 2024, which is perhaps less well understood, before rebounding in 2025. It makes sense for Charter to curtail capital expenditures in 2025 – 2026 given their stock option incentives. Investor’s perception of the BEAD program will be influenced by success of the RDOF program, but the resulting revenues and cash flows are likely to be slow to build. This creates further incentive for Charter to pull back on capital expenditures in 2025 to show a sharp increase in free cash flow, allowing management to exercise their options before ramping capex back up.

I estimate Adj. EBITDA as a generous 40% of revenues, which gives Charter the technical ability of Charter to increase its debt load by $4.3b by 2025. I assume that Charter fully accesses this additional debt and its free cash flow for share repurchases less a 10% buffer. This would reduce the share count -14% from 148mm shares today to 127mm at the end of 2025.

Ignoring the cost of growth, a free cash flow growth rate of 2% - 3% for an investor who would demand a 15% steady state FCF yield, the intrinsic value in 2026 is $515 - $558 from $391 today at zero growth shown above – an increase of 15% - 25%. Factoring in the estimated -18% reduction in share count takes intrinsic value to $626 - $679 – an increase of 40% to 52%. This is what Charter wants investors to consider – growth absent the cost of growth.

Factoring in the cost of growth, Charter looks less appealing. Charter should spend $15.1b in capital to generate growth. Subtracting that amount from the implied future value reduces intrinsic value in 2026 to $488 - $538. The present value is $321 - $354 (below the current quote of $391) and purchasing at a 20% discount to IV would result in a price range to establish a position of $257 - $283.

Share repurchases and stock options are typically viewed favorably by investors because the true cost is often masked. Yet stock compensation is a real compensation expense and share repurchases represent a use of capital that could have been used for other purposes. If we view share repurchases as comparable to growth capital expenditures, it would be appropriate to recognize their cost in our calculations. Charter’s shareholders can view the $36.8b spent on share repurchases in 2020 – 2022 at prices well above the current quote as a negative return capital investment. Since share repurchases are not reflected in the calculation of free cash flow, their cost is typically ignored by most investors. Therefore, making the argument to adjust for the capital cost of share repurchases is technically appropriate – particularly for an ultra-long-term shareholder – it is perhaps unrealistic to expect prices to reflect this capital expense in a normal environment.

Subtracting both growth capex and share repurchases from my implied future market capitalization reduces intrinsic value further to $343 - $394 with a present value of $225 - $259. Purchasing at a 20% discount to IV would be in the range of $180 - $207, well below the current quote.

My calculations are far more conservative than Wall Street, which tends to focus on the benefits of growth absent consideration of its cost. And it’s entirely plausible that investors will pay up for a 4.5x levered cable company facing increasing competition based on its ability to grow revenues by 2% - 3% per annum with a resulting growth of 4% in “Adjusted EBITDA” and apply a high multiple on a bogus earnings calculation.

How might your perception of fair value change over time?

It is particularly interesting that Charter’s steady state free cash flow isn’t expected to increase by 2025. 2025E FCF is $4.2b and 2025 growth capex is estimated at $4.1b, resulting in steady state FCF of $8.3b in 2025 vs $10.0b in 2022. Either consensus revenue estimates are understated or Charter’s underlying FCF is not going to change that much inclusive of the significant capital expenditures. This could be both because the ramp of the rural revenues will be protracted and because Charter is playing defense as its competitive moat shrinks and these capital expenditures are required not so much for growth as to offset continued erosion in the underlying business.

We currently know the estimated growth capital expenses through 2025. 2026 is an important year for Charter’s management because the 2016 options granted in conjunction with the Time Warner merger expire in June 2026. Charter’s management has a massive incentive to boost the price of the stock before expiry. We also know that the BEAD program for rural broadband will start deployments in the 2025 – 2026 timeframe. $9.2b RDOF subsidies were awarded in phase 1 out of $16b available, roughly 60%. Charter won $1.2b in subsidies in the auction, or 13% of total awards. Using similar statistics to estimate the magnitude of the BEAD program for Charter, $42.5b in total subsidies exist. Assuming 60% are awarded arrives at $25.5b in subsidies. Assuming Charter wins 13% of awards, yields $3.3b in subsidies. The RDOF subsidies are $1,200/passing, while the state subsidies have been more generous. This is largely due to the aggressive bidding in the RDOF reverse auction that lowered the subsidy amounts. Generously assuming the BEAD subsidies come in at $2,000/passing, $3.3b would equate to 1.7 million passings. Charter estimates the RDOF cost at $5,000/passing. I suspect that the actual cost will come in higher than expected and given that the BEAD program is a few years out, it seems reasonable to use a 20% higher cost of $6,000/passing, which would equate to a gross construction cost of $10.2b to be spread out over 3-4 years.

Charter, as a pure play cable/broadband company has greater exposure to competition than a diversified company like Comcast. The cable business has always required significant periodic capital investments to upgrade its plant. The size and frequency of these investments intensified with the shift from analog to digital in the late 90s and have continued to intensify more recently due to increased competition from fiber and fixed wireless. As the RDOF program concludes, the BEAD deployment will commence.

This mature business does generate significant cash flow, but those flows are largely consumed by the need to continue investing capital in the business. Charter’s strategy of running at 4.5x leverage and repurchasing shares regardless of valuation adds additional risk. Given that this strategy is encouraged by management incentives which diverge from the interest of a conservative long-term shareholder adds agency risk.

Recommendation

My recommendation is that Charter is not a compelling long investment at the current quote. I believe that it becomes appealing in the mid $200s and becomes compelling below $200, where it qualifies only as a mid-size position given the inherent risks pertaining to competition and leverage. As a highly levered, low growth company, it deserves a below average valuation multiple.

I make this recommendation from the perspective of a hypothetical, conservative, long-term holder who intends to purchase shares and hold for 5-10+ years without selling. For that investor, I do not believe Charter is an attractive investment in part because of its risk profile due to lack of diversification, leverage, and agency conflicts.

The attractiveness of a long-term investment perspective combined with a permanent capital base is the ability to focus solely on long-term value creation. The primary objective switches from the probability of short term returns to the probability of a permanent capital impairment. Such an investor should focus first on risk and second on reward. Buffett’s metaphor of having a punch card for investments is an appropriate framework. The construct is that you only have a certain number of punches on a card, say 20, and for each investment you make one punch. Once you’ve hit 20, you can make no further investments. This would change your thinking drastically compared to a world where there is ample liquidity and low transaction costs that encourage short-term thinking and investment. In the punch card metaphor, you would focus on an ultra-long-term timeframe and your considerations shift to will this business be around in 10-20 years and will it be significantly larger than it is today. With this strict framework, I’m not sure that Charter makes the cut. It is a fine business with stable and significant cash flows, but there is significant risk in its leverage, the continued capital requirements, and the agency conflicts with management.

I would suggest that a company that does meet those requirements is Comcast. It has the same positive attributes as Charter, a more diversified set of businesses, owner-operator management, and far more prudent capital allocation. While it trades at a slightly higher valuation than Charter, that premium is warranted by the above factors.

For a more active investor/trader, I would suggest avoiding Charter at present, but pay particular attention to Charter in 2024 when capital expenses are peaking, and free cash flow falls sharply. Given their leverage, the possibility of a continued rise in interest rates, and the possibility of recession, it is not hard to envision a situation where highly levered stocks with deteriorating cash flows get punished by the market – as they did in 2022.

Also, while not considered in this report, a potential investor in Charter should consider investing through Liberty Broadband (LBRDA) as its main holdings are Charter stock and other cable investments and can often trade at a discount to the underlying assets.

If these events do occur, then Charter becomes an interesting opportunity at prices in the $200s because of the management incentives on the 2016 options that expire in June 2026. In addition, the 2023 options have vesting triggered by the achievement of share price objectives, which presents a huge agency conflict. Given the magnitude of these incentives, combined with management’s ability to change how they allocate capital, could make for an attractive investment over a 1.5 – 2-year horizon, but that is a very different strategy than investing in long-term compounders.

What return can we generate over a 5+ year time horizon?

I believe the only way a 10%-12% return is possible in Charter over a 5+ time horizon is if investors continue to embrace, or at least tolerate the risk profile of the company, the agency conflicts, and the capital allocation. This is assuming a 2% growth rate of free cash flow, expected share repurchases, maintaining the 4.5x leverage, and paying no dividends.

I would hesitate to recommend Charter as a short position, particularly in 2025 – 2026 given the strong management incentives tied to stock options expiring in mid-2026.

Appendix

Supporting information

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

The primary catalyst is time. The franchise value is eroding from increasing competition and questionable capital allocation. The fundamentals of the business have weakened significantly this year which will be fully reflected in the stock price over time.

| show sort by |