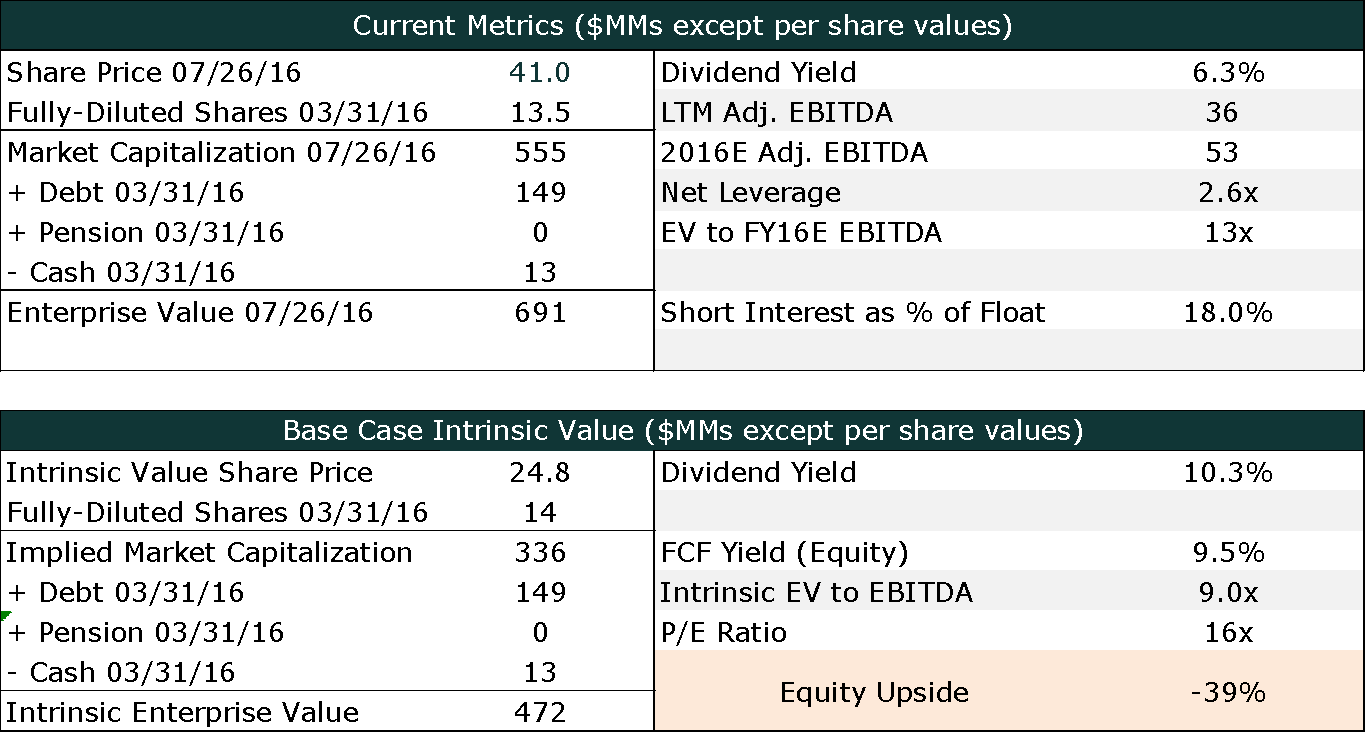

| 2016 | 2017 | ||||||

| Price: | 41.00 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 14 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 555 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 136 | EBIT | 0 | 0 | |||

| TEV (in $M): | 691 | TEV/EBIT | 0 | 0 | |||

| Borrow Cost: | Available 0-15% cost | ||||||

Sign up for free guest access to view investment idea with a 45 days delay.

- Healthcare

- IT Consulting

- Poor management

Description

Recommendation: Initiate a short position in Computer Programs & Systems, Inc. (“CPSI” or the “Company”) with a ~12 month price target of ~$25 per share representing a ~40% return in the base case.

Business Description

Founded in 1979 in Mobile Alabama, CPSI is a provider of healthcare IT for rural and community hospitals with 650 client hospitals. CPSI offers an integrated clinical and financial system for its clients as well as business management, consulting and managed IT services through its TruBridge subsidiary. CPSI client base is predominately comprised of hospitals with 100 or fewer acute care beds. As of 12/31/2015, CPSI generated $182MM of revenue and $30MM of Adj. EBITDA.

Transaction Overview

On November 10th, CPSI announced the acquisition of healthcare IT provider Healthland Holdings Inc. (“Healthland”) from private equity firm Francisco Partners (purchased in FY07) for $252MM consisting of ~$165MM in cash and ~$87MM in stock.

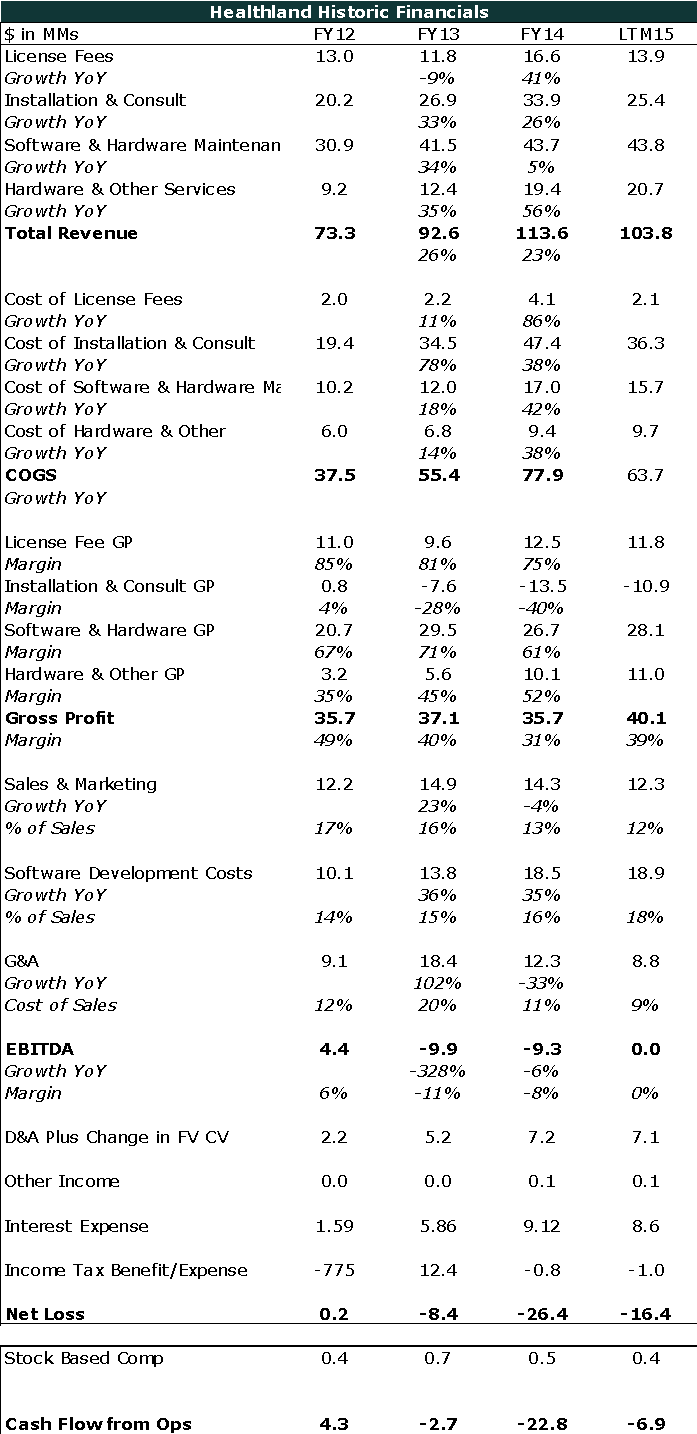

Healthland provides healthcare information solutions for community hospitals and post-acute providers through three business segments: The legacy Healthland business is a longstanding competitor to CPSI’s core business, as it provides EHR and patient accounting solutions to 350 small hospital customers under the Centriq (250 customers) and Classic (100 customer) products. Further, the company’s American HealthTech segment (acquired by Healthland in May 2013) provides clinical and financial solutions to over 3,300 skilled nursing facilities. Lastly, the Rycan segment (acquired by Healthland in April 2015) offers SaaS-based revenue cycle management (RCM) workflow and automation software to nearly 300 hospitals. As of 9/30/15, Healthland generated $103.8mm in revenues and was Adj. EBITDA breakeven.

Thesis

Despite reporting a horrendous 4th quarter and its 8th consecutive miss, CPSI equity experienced significant price appreciation due to the announced acquisition of competitor Healthland Inc. The market and sell side are overlooking Management’s poor track record as the consensus is simply taking the Company’s EBITDA guidance at face value. Notably this assumes the core business doubles EBITDA from FY15 to FY16 while the acquired segment is expected to more than triple EBITDA despite stagnant revenue growth. CPSI’s horrendous first quarter results confirmed our view as CPSI once again missed revenue and profitability estimates, this time as a combined entity. Despite the major whiff, Management is holding onto its unachievable guidance which is purely reliant on dubious add-backs (such as NOL cash taxes added back to EBITDA), expected cost and cross-sale synergies and a recovery in the back half of the year.

Spearheaded by a Management team which has never operated with financial leverage nor completed an acquisition in its 35 year history, CPSI was forced into a horrible acquisition driven by its significant revenue headlines ultimately purchasing a distressed business which is bleeding clients and cash. The merger offers little in the way of real cost synergies as the combined entity will be forced to support and increase investment in two ill-equipped software platforms (Centriq and Thrive) effectively running two separate software platforms which compete against one another. Furthermore, sales synergies won’t be realized and the combined top-line will continue to erode due to heightened competition from larger competitors with better offerings such as Epic, Meditech and Cerner, saturated end markets as well as various spending headwinds related to shrinking community hospital budgets. Shorts not only have continued earnings misses as a means to get paid, but also a dividend cut as well as potential issues pertaining to financial leverage.

-

Saturated Market & Declining Customer Spend: The EHR industry experienced a brief increase in revenues from FY11 to FY13 driven by mandated Meaningful Use 2 upgrades, however that has since dissipated leaving a market that is fully penetrated. Moreover, healthcare IT spend particularly for community hospitals continues to face significant headwinds. Commentary suggests hospitals are moving away from expensive infrastructure products in favor or lower initial ticket SaaS offerings. These headwinds are clearly evident not only in CPSI and Healthland’s financial results but also for pure-play Meditech. While CPSI has tried to stymie flat/declining revenues with ancillary offerings such as TruBridge and other RCM products, those markets garnish significant competition and pressure on pricing.

-

Recall Healthland has remained EBITDA negative even when experiencing significant growth driven by Meaningful Use 2. Hence with the top-line for Centriq/Classic shrinking, it is likely EBITDA will remain break-even or slim at best.

-

The shrinking opportunity/lack of evergreen contracts can be viewed by the decline of non-recurring backlog and deferred revenues which shrunk by over 50% YoY for Healthland as well as recent call commentary:

-

“First, as we have discussed on the last several investor conference calls, the post MU EHR market is essentially fully penetrated and CPSI's ability to survive and thrive as an EHR vendor in the future has shifted from winning greenfield EHR opportunities to instead being largely dependent on several previously stated factors: competitive EHR vendor replacements, add-on software sales to existing customers, leadership in new product development such as data analytics and population health, expansion into new markets such as ambulatory surgery centers, LTACs and postacute care facilities, and perhaps most importantly, the continued ability to sell and implement TruBridge services to the community hospital marketplace.”

-

The following commentary also supports the view that spending will be challenged: “Small Hospital Troubles. We believe a key issue throughout FY15 revolved around the limited finances and resources associated with small hospitals. Several smaller vendors faced purchasing disruption because of less purchasing activities across this portion of the market. Based on our research, we believe that most small hospitals limited their investment in the ICD-10 transition and were likely unprepared, and these entities provided limited training around the transition, as well. We believe that recent performance at CPSI and IMPR suggest that spending will remain challenged in 4Q15 and into FY16. In our view, the biggest indicator of spending challenges lingering into FY16 revolves around the merger of CPSi and Healthland. In our view, the merger brings together two technologically challenged platforms looking to extend the runway of their challenged businesses.”

-

Growth Multiple for an “Old Tech” Business: CPSI is currently priced at 13x FY16E Adj. EBITDA, a rich multiple for an obsolete old tech business with eroding top-line and increasing competition. As earnings disappoint, CPSI will re-rate to ~8x to 9x EBITDA in-line with other declining no growth tech companies, representing 30% - 50% upside to the short thesis.

-

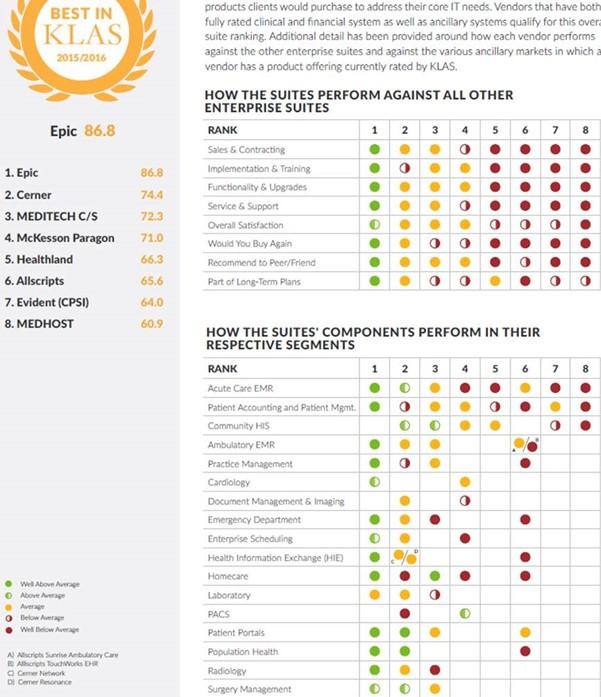

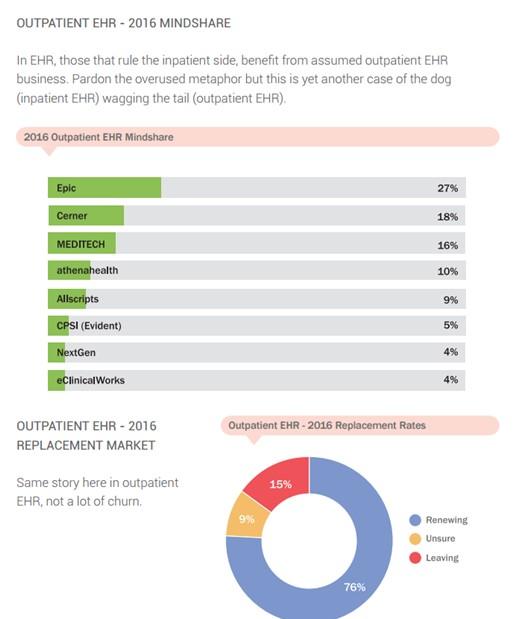

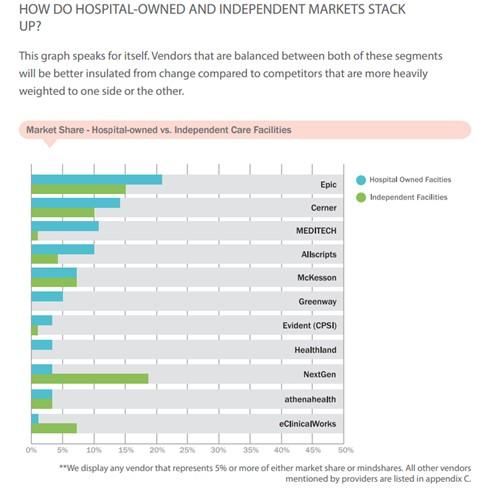

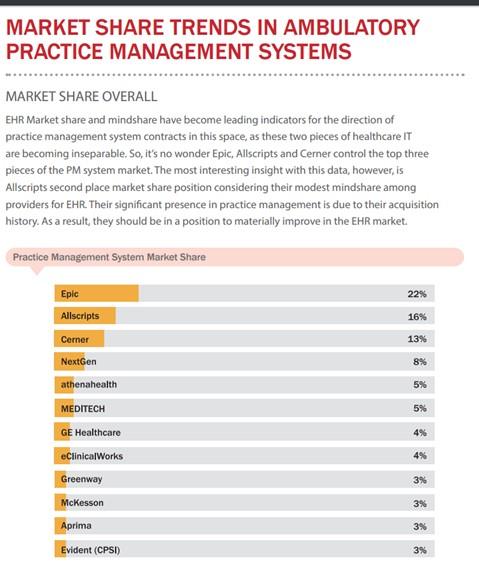

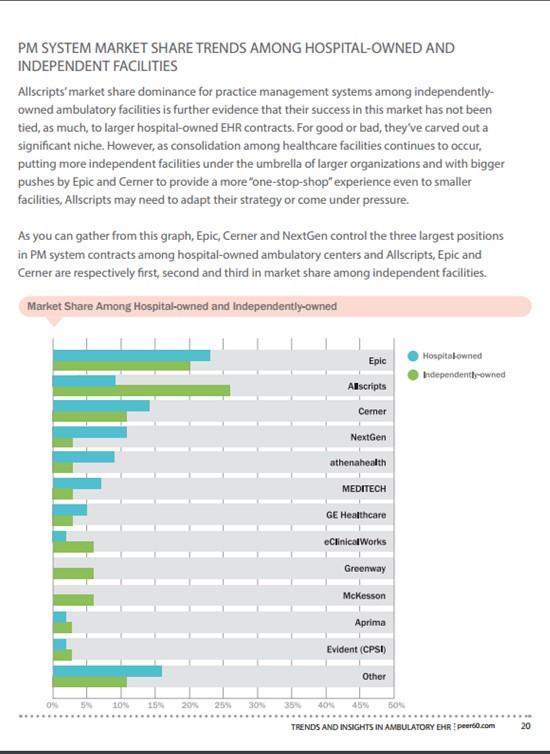

Competition and Inferior Product Quality will lead to Further Sales Declines: CPSI and Healthland face increasing competition from large EHR participants such as Epic, Cerner, Meditech and McKesson who are going downstream into the community hospital channel to capture market share. Despite Healthland and CPSI being predominantly focused pure-play community health EHR providers, the space is dominated by Meditech (~28%), McKesson (12%) and Cerner (12%). With 20% of community hospitals looking to switch potentially switch providers, the top participants with the largest mind share (i.e. indicative of which vendor a hospital is going to switch too) has been Epic (the largest EHR provider), Cerner and Meditech.

-

Per the KLAS ranking charts below, CPSI and Healthland are at the bottom of their respective peer groups for overall quality, behind stalwarts such as Epic, McKesson, and Meditech. Importantly, both software platforms have below average to well below average rankings. Recall, CPSI will need to increase investment in two low quality software platforms however this is unlikely due to the current abysmal R&D spend hence it is highly likely the consolidated CPSI entity will continue to lose share. For a pure-play community health EHR/HCIT provider, these low rankings are an embarrassment at best.

-

R&D spend is de-minimus for the core CPSI business, totaling under $4MM per annum or less than 2% of revenues over the past four years. Not only is this very low for a software/tech business, its own competitors historically have spent over 10% of revenues on R&D. Hence it’s no surprise why customers are leaving CPSI for the peers noted above.

-

Management has noted attrition remains high and that can be seen in Healthland clients which declined from 500 in 2013 to 350 as of the acquisition close. Recall 100 Healthland clients are classic customers which is losing support over the next two years. Likely 70 of those clients will churn to other platforms, with the total opportunity for CPSI being the remaining 25.

-

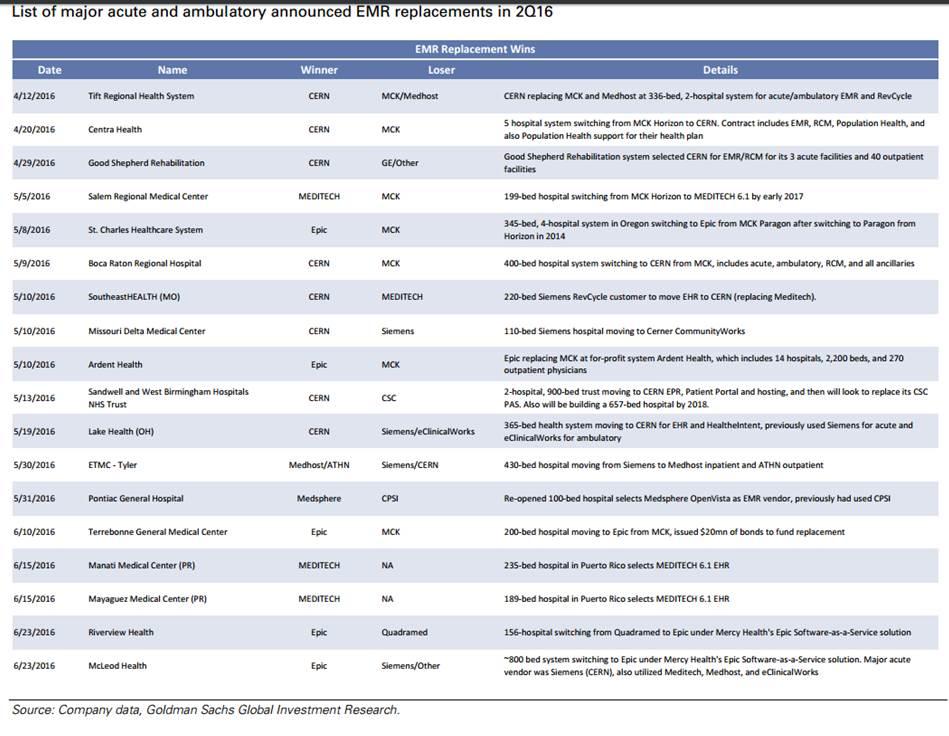

Competition and lack of execution partially due to the mergers have caused sinigifcant issues. As of July 19th 2016, it appears CPSI has not won any major EMR deals, instead it has lost one key contract to Medsphere.

-

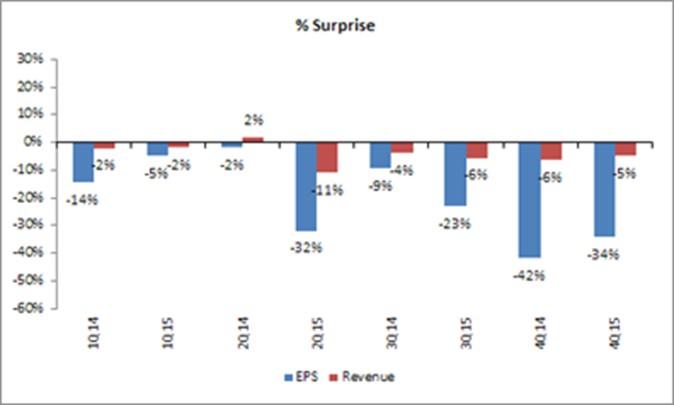

Minimal Insider Ownership & History of Missing Estimates and Guidance: Management have been recent sellers as of recent, while Francisco Partners has filed the S-3 registering their shares (~15%) for a sale at expiration in July. Moreover, CPSI has a strong reputation of missing revenue and EPS estimates per the chart below:

-

Questionable Accounting and One-Time Items Inflate Adj. EBITDA: The following accounting red flags exists at CPSI:

-

On the 4Q15 call, CPSI announced it will be eliminating its backlog metric. Recall non-recurring backlog has continually declined YoY as well as deferred revenues at Healthland.

-

Management noted at the close of the acquisition they were “in process of determining backlog at Healthland”. This signals they have poor visibility on the actual revenues.

-

While not sizable, delinquent A/R spiked from ~$0.5MM to $2.2MM from 12/31/15 to 3/31/16. Likely partially attributable to Healthland.

-

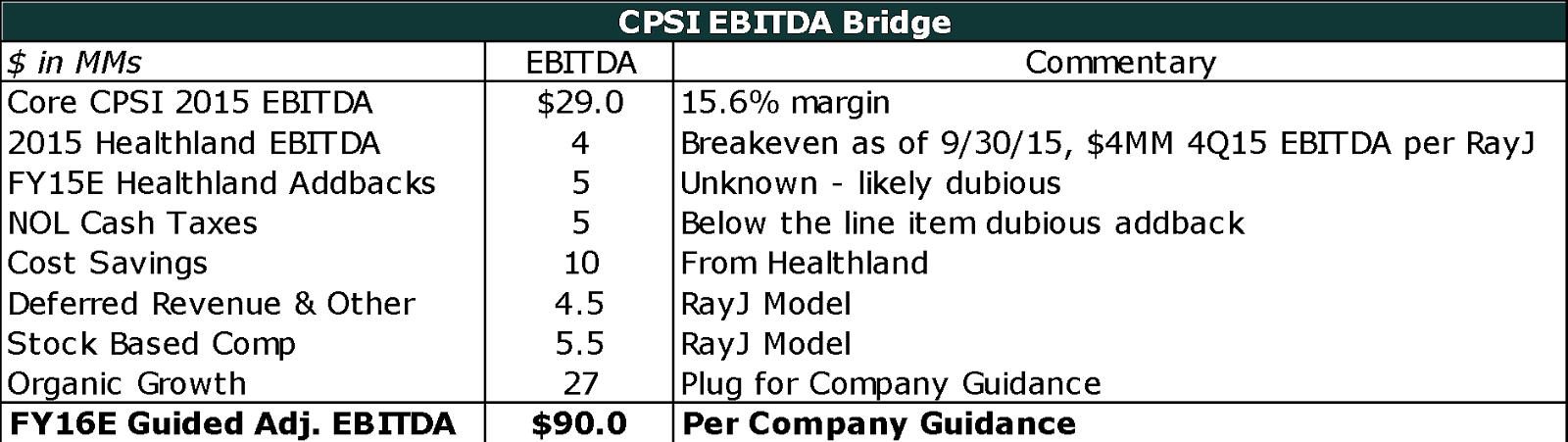

Note adjustments to FY16E EBITDA include many dubious addbacks noted below such as deferred revenue, NOL cash taxes and SBC. Furthermore, the bridge assumes ~$27MM of EBITDA from organic growth implying incremental margins near 100%, something which these businesses have never achieved in the past. Consolidated EBITDA will likely amount to ~$50MM to $55MM at the high end for FY16E.

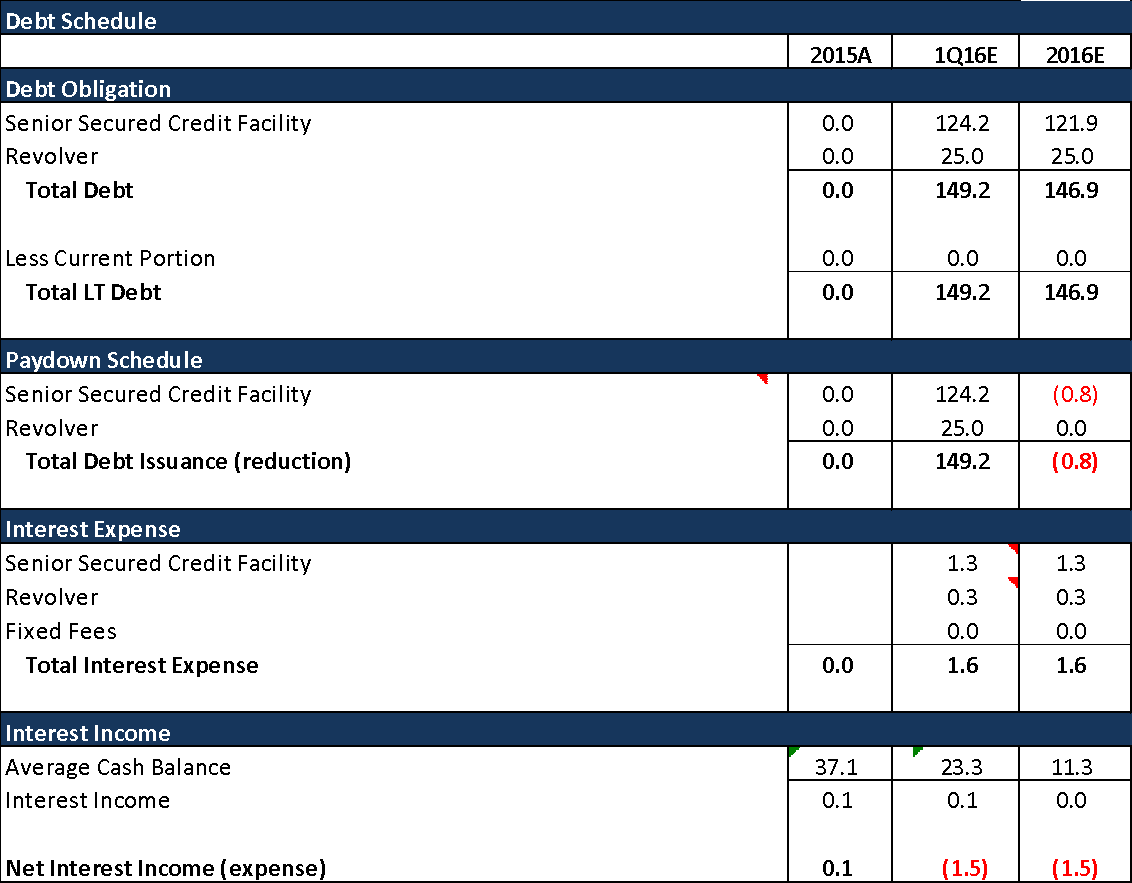

Purchase of a Low Quality Asset has Left CPSI in a Precarious Financial Position: Due to its stagnant/declining business, CPSI’s management team believed it to be a good idea to purchase a competitor in the exact same segment with similar, intensifying headwinds for 28x EBITDA. Furthermore, Healthland has been bleeding clients (declining from 500 in FY13 to 350), and is expected to lose 70 additional clients which will be a significant revenue headwind going forward. Moreover the management team has never consummated a large acquisition over its 35 year old history nor has it managed leverage. The Company has levered up over 3x debt to EBITDA while paying out over 100% of FCF as dividends. Given that the acquired entity is free cash flow negative, it is highly likely that the dividend will be eliminated or reduced over the next year.

Furthermore if cost synergies are not realized, the Company could enter into financial distress given the combination of financial leverage, top-line headwinds and operating leverage.

-

Note Healthland had multiple covenant violations and was in distress.

Why Does This Opportunity Exist & Variant View

-

Flawless Integration & Estimates Achievable:

Rebuttal: The current price and consensus estimates assumes integration is consummated without issues. If larger competitors such as Cerner had issues integrating acquisitions (Siemens), a management team which has never completed an acquisition, particularly a new CFO who could not recall EBITDA for the quarter, will definitely run into issues.

Furthermore, estimates are not achievable given the lofty growth assumptions assumed in a bleak, shrinking environment, aggressive cost cuts and dubious addbacks. Recall CPSI significantly missed Adj. EBITDA estimates for 1Q16, coming in at $13.2MM vs ~$19MM. Despite taking down FY16E revenue estimates, Management maintained their dubious FY16E Adj. EBITDA estimate of ~$86MM to $91MM while the street is at ~$78MM.

Given commentary from competitors, we think CPSI achieving its back-half loaded EBITDA estimates is a pipe-dream. We likely see a scenario in which EBITDA estimates come closer to our ~$54MM target if not materially lower.

-

Consistent & High Dividend Yield Support by FCF

Rebuttal: Historically the market has placed a floor on CPSI due to its policy of paying roughly ~100% of free cash flow out as a dividend. With a new levered capital structure and increasing costs, the dividend is at risk of being cut.

-

Significant Synergies & Cost Savings from the Healthland Acquisition

Rebuttal: Unlike other acquisition models for which products are integrated and sold through the same channel, CPSI will be running two separate/competing software platforms. Due to a long life cycle of 7 to 10 years, it will be difficult for CPSI to eliminate costs particularly when CPSI/Centriq are Moreover, much of the addbacks proposed are dubious in nature such as cash tax NOL savings.

“so our message has been to them that we get that and that we are going to continue to not just support, but to invest heavily in the improvement of the Centriq platform for the next 7 years.”

-

Significant Cross-Sale Opportunities

Rebuttal: It’s unlikely that CPSI generates additional revenues from its core or Healthland customer base given that they sell into cash-strapped community hospitals with shrinking budgets, including many whom just spent significant capital on upgrading their EHR systems to comply with Meaningful Use 2 requirements. Finally, with a 7 – 10 year product life future upgrades in the near-term are unlikely. Moreover, the market is mature and saturated with virtually zero evergreen opportunities. Hence the top-line will continue to shrink for CPSI and other peers such as Meditech. Finally, we are skeptical on Management’s ability to cross-sell given that they have never consummated an acquisition and have shown skill at missing estimates.

“Q4 call: I think the most exciting thing that we've been able to talk to them about obviously is TruBridge, which we talked a great deal about already. But then also we're going to be able to provide them with some tools, namely data analytics and interoperability that they would have -- they're both going to be able to provide that much more quickly than they were going to get otherwise as Healthland stand alone, and they understand that. I think the other thing that's been crucial for them to hear from the combined management team now was obviously there's been a lot of misinformation that's been spread about the competition. I mean, we understand that everybody that is on Centriq has spent hundreds of thousands of dollars or up to $1 million on that product within the last 2 to 4 years, and they have no interest in buying a new product any time in the near future.

Catalysts to Getting Paid

-

Earnings miss as EBITDA and EPS estimates are too high.

-

Dividend cut due to leverage and increased integration costs.

-

Francisco Partners sells their stake on July 2016. Note Francisco Partners filed to register their shares in February 2016.

-

Write off or impairment of the Healthland acquisition (2016 10K event).

-

Continued market share loss.

Short Thesis Risks

-

Management meets costs guidance through changes in revenue and expense recognition at Healthland.

-

Dividend is increased.

-

The Company successfully cross-sells Rycan/Trubridge; – we believe this is less likely given management’s inexperience with acquisitions, and commentary from the call regarding costs and cross selling.

-

Mis-modeling of the acquisition and contribution for Q1. Per the RJ model, revenues look to include the full quarter of Healthland revenues although they have been applied evenly across the four quarters.

-

Operating leverage with system sales – noted 13 Thrive installations set for 2016, roughly in-line with FY15.

-

Vista/Thoma Bravo Put aka CPSI is acquired – a lower probability risk given the recent acquisition. Moreover, it was rumored CPSI missed its chance to sell itself and hence has had to play defense by purchasing Healthland. Nonetheless, who would want to purchase a company undergoing significant upheaval transition at a fat multiple?

-

Business is somewhat sticky with recurring revenue however CPSI and Healthland’s rankings are low hence people are looking more and more to switch providers.

-

As noted above, CPSI has underspent on R&D, totaling less than $4MM per annum. Healthland currently spends ~14% - 18% of revenues or ~$16MM per annum on software development costs. CPSI may attempt to eliminate or capitalize R&D costs at Healthland in order to meet its aggressive targets. Note if cut, Healthland’s churn will increase and product position will likely decrease.

Trading Considerations

-

Daily liqudity of $9.9MM.

-

Short interest of 18%

-

52 week high of $59 per share, 52 week low of $36.

-

Sell-side coverage is broad consisting of multiple banks ranging from RJ, Oppenheimer, DB, Citi, PJ, Suntrust, Baird, William Blair and Wells Fargo.

-

Expectations are high – with adj. EBITDA and EPS estimates elevated ranging from $78MM to Mgmt at ~$86MM.

-

Shareholder base is predominatly GARP and growth managers per CapIQ.

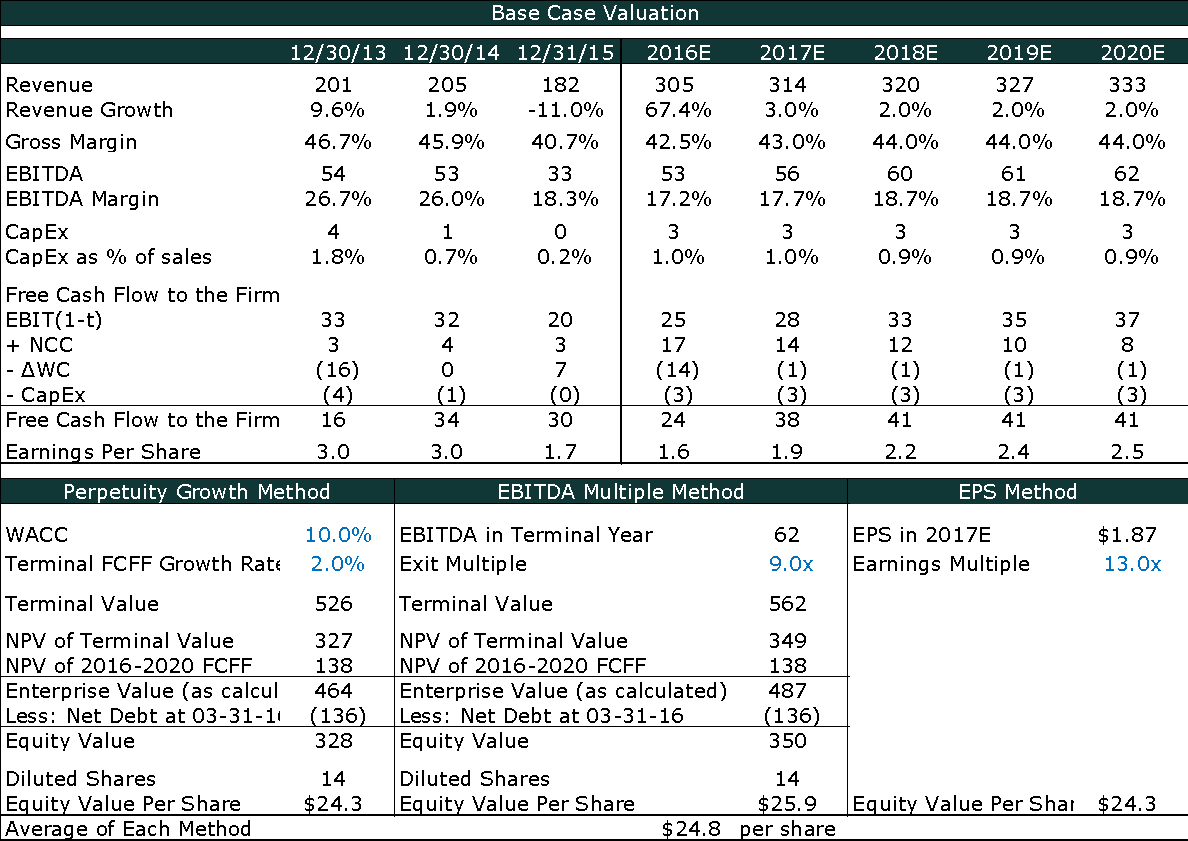

Base Case

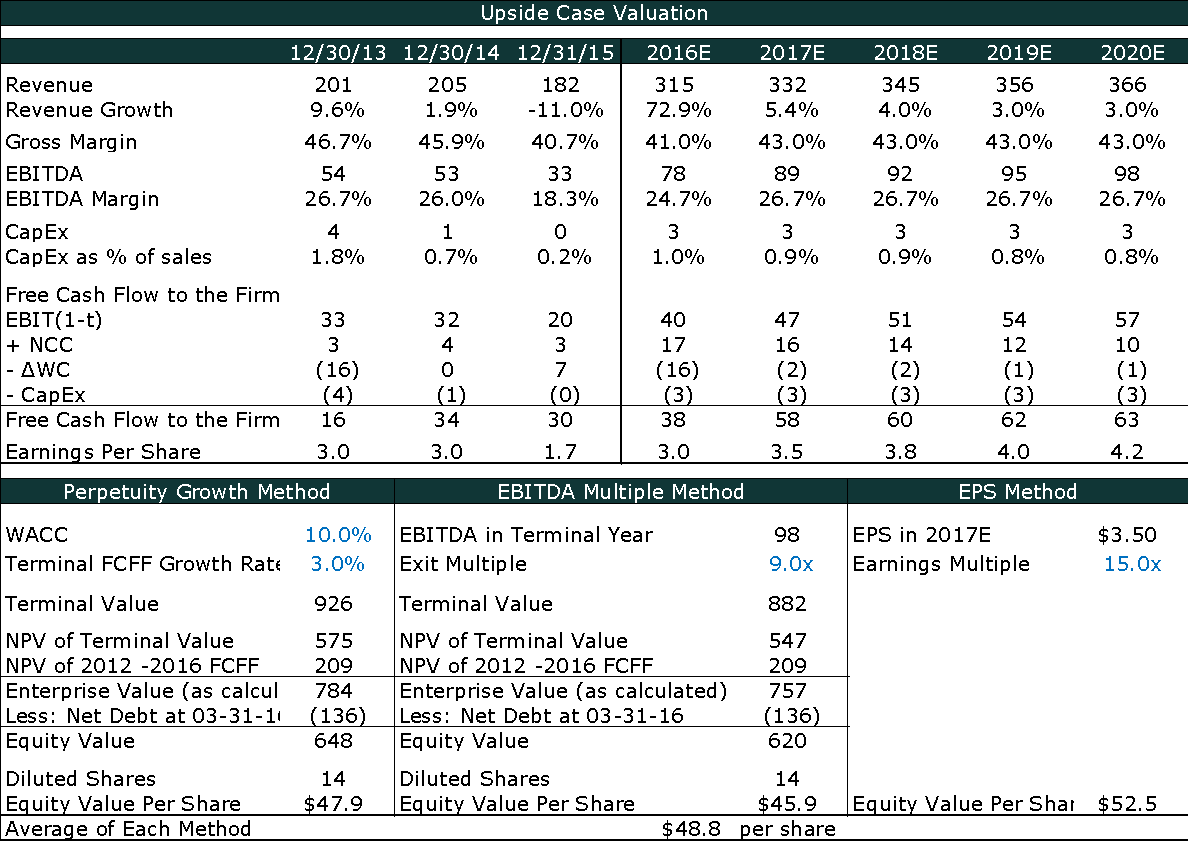

Upside Risk Case

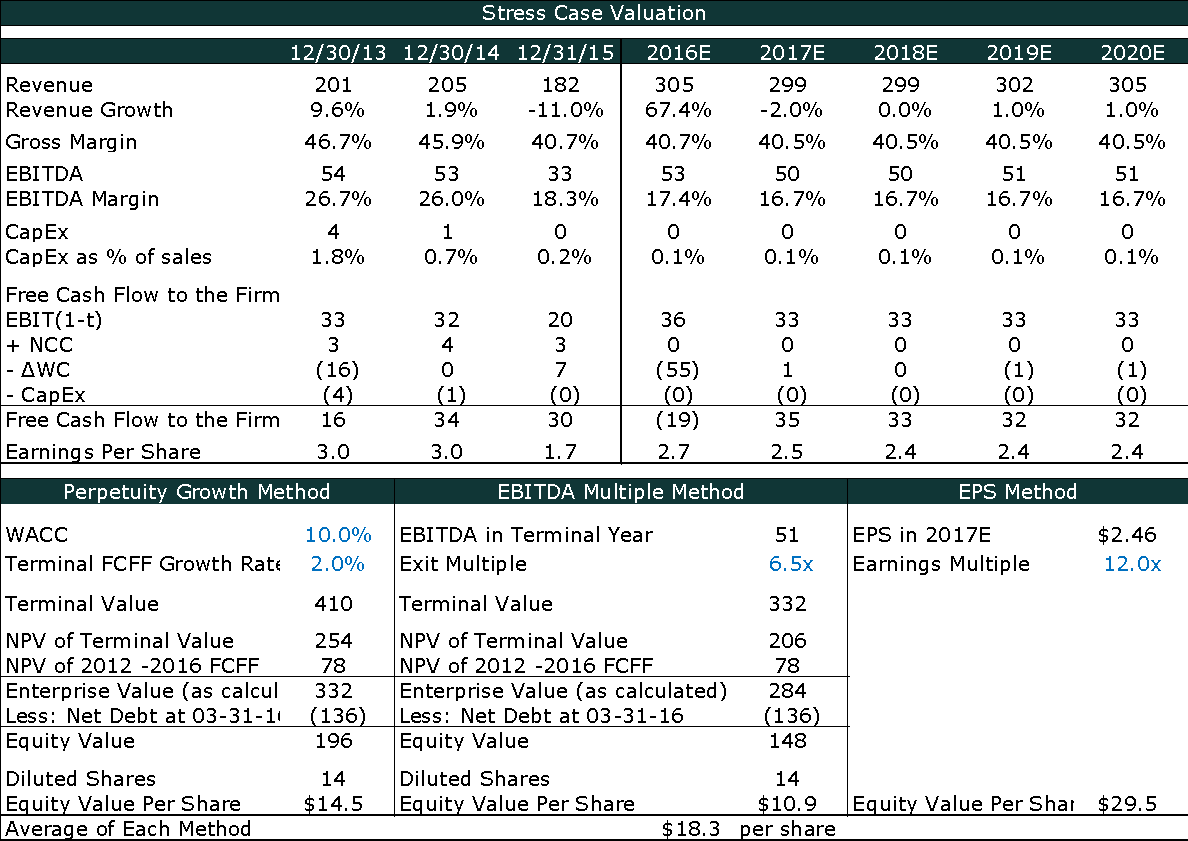

Stress Case

Appendix 1 – Charts / Additional Figures or Exhibits

Stifel Commentary

Will Healthcare Technology Spending Rebound in FY16? We remain of the opinion that the spending lull that took hold in FY15 will continue in FY16. We see several exogenous factors driving this continuation. First, “IT overload” will keep people on the sidelines unless the product or service meets specific needs and provides real value. Secondly, the continued evolution toward outcomes-based reimbursement suggests that purchasers of healthcare technology need to reallocate their investment dollars away from what are commodity products (infrastructure) towards performance-based investment (population health, et al.).

Things to know about EHRs in community hospitals

Written by Carrie Pallardy | July 29, 2015

Community hospitals may not have the resources of larger health systems, but these providers are still subject to the pressures of meaningful use.

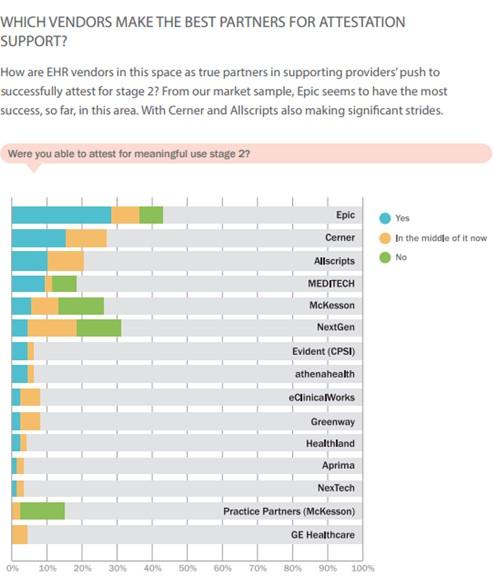

Community hospitals are actively acquiring and implementing EHRs, but already nearly 20 percent are seeking to switch vendors, according to the peer60 Community Hospital EHR Quick Report 2015. The report includes input from 277 community hospital providers. Here are five things to know about EHRs in community hospitals.

1. Of the hospitals included in the report, 53 percent have attested to MU Stage 2. Just more than a third (36 percent) are in the process of attesting, while 11 percent have not attested.

2. The biggest EHR challenge reported by community hospitals (56 percent) was system usability.

3. Community hospitals reported other challenges including:

• Missing functionality: 53 percent

• Support for strategic initiatives: 28 percent

• Service: 26 percent

• Reliability/uptime: 5 percent

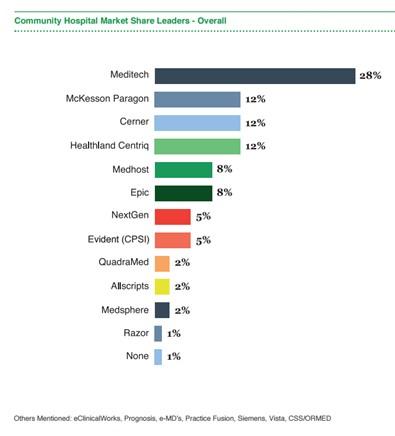

4. Meditech holds the largest market share amongst community hospitals at 28 percent. Other top vendors include:

• McKesson Paragon: 12 percent

• Cerner: 12 percent

• Healthland Centriq: 12 percent

• Medhost: 8 percent

• Epic: 8 percent

• NextGen: 5 percent

• CPSI: 5 percent

• QuandraMed: 2 percent

• Allscripts: 2 percent

• Medsphere: 2 percent

• Razor: 1 percent

• None: 1 percent

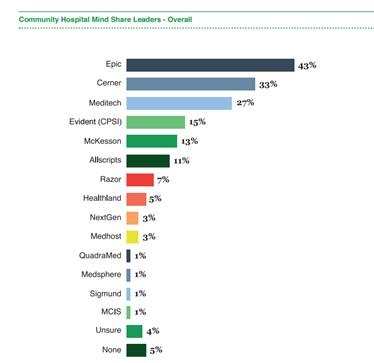

5. Though Meditech holds the largest market share, it falls to third when it comes to vendors community hospital leaders think about. Here are the top EHR vendors by mind share:

• Epic: 43 percent

• Cerner: 33 percent

• Meditech: 27 percent

• CPSI: 15 percent

• McKesson: 13 percent

• Allscripts: 11 percent

• Razor: 7 percent

• Healthland: 5 percent

• NextGen: 3 percent

• Medhost: 3 percent

• QuadraMed: 1 percent

• Medsphere: 1 percent

• Sigmund: 1 percent

• MCIS: 1 percent

• Unsure: 4 percent

• None: 5 percent

“So which vendors are top of mind to meet providers’ needs? The current community hospital EHR market is fragmented with a larger number of vendors holding relatively small, individual shares of the market. Mind share is much more consolidated toward Epic, Cerner, and Meditech. The following section shares some key findings on the current state of the community hospital EHR market.”

Overall Meditech is clearly the market share leader. Others with solid market share include Healthland, McKesson, and Cerner. Epic tops the list in mind share, which is not surprising considering their dominance in the large hospital EHR market. Cerner and Meditech were also leaders in mind share.

Peer 360 Report

Call items

Jeffrey Garro

Congratulations on the transaction. First, I wanted to ask if you could just give us a little detail on the mix of the Healthland customer base between the Centriq and Classic platform. And also how attrition and renewal rates have been trending for both those businesses recently.

David A. Dye

The first part of your question, it's about -- we had is in the call, it's about 250, I mean, on the Centriq and 100 on Classic approximately. And I didn't catch the second part of your question, Jeff.

Jeffrey Garro

It was how the renewal rates or attrition have been trending for both of those platforms recently.

David A. Dye

The attrition rate has been very high. I think everybody in the community hospital marketplace hasn't been doing a lot of -- selling new systems recently and that's certainly consistent with Healthland and us, although they certainly have some new deals. And they've had a lot of migrations from Classic to Centriq as well in the last couple of years, which Boyd alluded to in his answer to his question earlier.

J. Boyd Douglas

And then, David, I'd say the attrition rate has been low for them because of the -- there's not a lot of change going on now that people have met Meaningful Use. There's not a lot of appetite as we've discussed in several of our conference calls out there, so there's just not a lot of people looking. So our attrition rates are relatively the same between us and Healthland over the last 12 months if for no other reason because of the, like we said over and over again, the hangover effect from Meaningful Use, nobody's out there looking for any reason at this point.

Two weeks ago, the Healthland, TruBridge and Evident sales leadership teams met to begin the collaboration efforts around the sales opportunities within our combined acute care customer base. Those conversations focused on 3 primary objectives: First, upgrading the existing Healthland acute care Classic customers to either Centriq or Thrive. Although the Classic product is still supported and will be for a minimum of 2 years from any potential sunset announcement, Classic will not be Stage 3 certified. And as such, the approximately 25 Healthland Classic acute care hospital customers that wish to continue to participate in the MU program will need to upgrade to either the Centriq or Thrive solutions.

Second, as Chris discussed earlier, we believe there is significant opportunity to sell Rycan's best-of-breed claims management solutions to TruBridge's 600-plus acute care hospital customers, particularly in the area of liability estimates and denial [ph] management. And third is the substantial potential to penetrate the Healthland Classic and Centriq EHR customer base with the TruBridge's suite of revenue cycle management, consulting and IT managed services solutions.

Glassdoor Reviews

May 20, 2016

Helpful (9)

"Be Warned"

StarStarStarStarStar

Former Employee - Integration Analyst in Mobile, AL

Doesn't Recommend

Neutral Outlook

I worked at Cpsi (More than 5 years)

Pros

-You can meet a lot of really smart and talented people.

-You can get introduced to a variety of CPSI applications.

-You can travel and possibly see things you wouldn't normally see otherwise.

Cons

-All those smart and talented people are wasting all their potential at CPSI because usually, actually more than likely, they get overlooked. If they don't get overlooked, they get overused and under rewarded.

-While learning a lot of CPSI applications helps you at CPSI, it does not help you for anything else outside of CPSI. It makes the job a waste of time if you don't plan on staying until you retire. And I guarantee that unless you're a masochist, you'll want to run like the wind once you realize what CPSI is really all about.

-You're travelling to really po-dunk cities. You might fly into a big city, but then you'll probably drive a few hours to your small city to train at your small, po-dunk hospital where the janitor is also the business office manager. You'll also probably travel way more than you ever want to because CPSI likes to either keep the place short-staffed and/or book all their installs at the same time. From what I hear, it's just not worth it.

-CPSI as a whole is a lot like a psychopath. You are a number, a means to an end and you are replaceable. You can work there for years and years and if you try to make a request, like to get off the road or to work from home, etc, you'll be told this is your job or shown the door. They simply do not care.

-I worked there for almost 10 years and only saw the top dog guy for the first time in that almost 10 years earlier this year. I had no idea who he was.

-Management is lacking greatly in knowledge of the products they're managing. This is one of the main reasons I finally left. My manager had worked in my department for around 15 years and yet I was teaching/showing them things after being there for 4.

-The company hired another company to teach our management how to boost morale and so we adopted this bs philosophy to try to foster a better work environment. It doesn't work.

-Some departments have pay raise caps. So once you work there a certain number of years, you cannot make any more.

-Overtime is a joke. It is not time and a half. I think it might be maybe a dollar or two for every hour worked over your allotted hours. Absolutely not worth staying passed your 40 hours.

-Our programmers are OLD SCHOOL. COBOL old school. I think we are just starting to incorporate some SQL into the jerry-rigged product. What this means overall is that the programmers we have have been there since God was born.

-Communication between departments is not encouraged and often times it's a blame game between the departments. You would think knowing that we all work for the same company and that our end goals are all the same that we'd want to work together, but that is just not the case. It's a dog eat dog world at CPSI.

-I know of co-workers that would keep a copy of every piece of communication with any other co-worker in an effort to cover their butt should anything go down.

-Their in-house system is called Big Brother. I'm not kidding.

-You will get paid crap because this is Mobile and they can get away with it. There are no other real competitors out there in this area, so a lot of people settle for the crappy pay. And by crappy I mean probably about half of what the average is for the job title. Before you go there, google your job title and see what you should be making.

-The product they offer is quite honestly really crappy. I feel so bad for the poor small hospitals that can't afford a better EHR and have to get our crappy system. Our products never work. We roll things out without being sure they work so the customer gets a half-built, duct taped product and then we have to constantly fix fix fix. Our programmers and QA team don't have to work with the customers directly, but you will. So you'll hear the complaints from the customers and you won't be able to do anything about it. Because you can't communicate directly with QA or programming. You have to tell your manager and then your manager has to follow a protocol to talk to QA and programming. It's jacked up.

-You will cry. Probably a lot.

-You will feel stuck. Probably a lot.

-You will start to question your own self-worth because no one ever tells you you're doing a good job.

-You will daydream about the apocalypse or the end of the world in some capacity because even that would be better than working at CPSI.Show Less

Advice to Management

-Be human.

-Treat your staff like humans.

-Learn the product you're managing.

Healthland, Inc.

Healthland operates three main assets, its HCIT system Centriq/Classic which has a total of ~350 clients, American HealthTech (“AHT”), an EHR Healthland was a distressed asset with significant cash burn and covenant violations (Fortress/WF lenders) despite benefitting from the Meaningful Use 2 upgrade cycle.

Capital Structure

Source: RayJ

I and/or others I advise do not hold a material investment in the issuer's securities.

Catalyst

- Estimates come down/miss.

- Dividend cut

- competition/churn.

| 4 show sort by |