| 2016 | 2017 | ||||||

| Price: | 17.20 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 50 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 861 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 295 | EBIT | 0 | 0 | |||

| TEV (in $M): | 1,156 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

Description

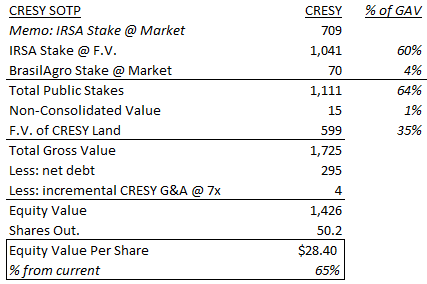

CRESUD (CRESY US EQUITY), the parent company of IRSA (IRS US EQUITY), has 65% upside and currently creates IRSA cheaper than IRSA's public stock price. Investing in CRESUD now makes sense because:

1) IRSA has significant upside from current price given positive developments in Argentina and given that it has de-risked its Israel investment through asset sales

2) CRESUD’s agricultural land holdings will benefit most from Macri’s new tariff and currency policies, which will lead to increased earnings from farming, increased farmland value, and increased profitability of land development

3) CRESY is the most attractive way to invest in the structure because you own alongside and are aligned with the controlling Elzstain family, who own ~31% of CRESUD, and you will probably benefit when the Elzstains simplify the corporate structure (three listed companies) as they’ve indicated they plan to do.

1. IRSA Stake (Update)

A past write-up of IRSA is available here which provides a full description of IRSA’s assets. Since that write-up (posted 9/10/2015 at price of $14.60) IRSA fell to a low of $8.60 on 1/19/16 and has since recovered to $19.25 as of 9/6/2016. The low price was driven by investor concern about IRSA funding debt maturities at its Israeli investment IDB and the short report published by Spruce Point in November 2015. IRSA will not need to fund future IDB debt maturities, due to recent, significant positive developments that will give the company more liquidity: primarily the sale of the Adama stake to ChemChina, and secondarily a secured bond raise and continued progress in the sale of the Clal Insurance stake.

On July 17 2016 IDB announced that it sold its remaining 40% stake in Adama to ChemChina, valuing Adama total equity at $3.2B, vs. the 2.4B contemplated in the pulled 2014 IPO, a valuation which would have put IDB’s stake at 0 net of a margin loan on the shares from ChemChina. The valuation of the sale (at ~10x LTM 1Q16 EBITDA) was a surprise to the market – IDB’s bonds rallied 10 points – and the cash inflow of $230M is more than enough to cover next year’s debt maturities of $211M by itself, before any additional asset sales or dividends of free cash flow from the operating subsidiaries. Additionally, the company indicated that the sale would satisfy debt covenants that had prevented upstreaming cash from the operating subsidiaries to IDB to satisfy debt payments. IDB also announced an offering of bonds secured by their ownership stake in Clal. Though IDB’s ability to receive the proceeds of this offering depend on regulatory approval, the $80M if received would further increase the liquidity position of IDB. Finally, recent press reports indicate the company is committed to the sales process for Clal and an offer was received from a US real estate developer for 66% of book value or 100% of tangible book value, well below the 100% of book value Chinese offer which was blocked by regulators. Though the company deemed that recent offer too low, selling Clal, especially at a premium to its current public valuation of 57% of book value, would create additional liquidity for IDB to satisfy debt maturities and be a material positive for IRSA. I believe this will be the next positive catalyst for IRSA/CRESUD.

I wrote a response to the Spruce Point short report in the messages of the IRSA write up and for reference I included it in Appendix 2 below. In summary, the report was misleading in particular in alleging that IDB’s debt was recourse to IRSA’s assets or that accounting consolidation of the entities would lead to the debt becoming recourse, which is not true; additionally, it argued that IDB would be forced to de-list its ADR because of delinquent translation of 2014 financials into US GAAS, which ended up being wrong; and that a warrant transfer was done below market price to benefit the controlling shareholder, which was not true adjusting for the time value of the embedded option and which resulted in an immaterial gain.

2. CRESUD Agricultural Land Value

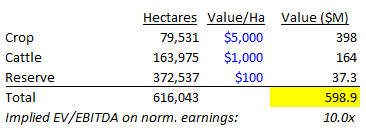

CRESUD is primarily a land developer, buying raw land to develop into cattle land, cropland, or even real estate for residential development, a business in which they have successfully realized USD IRRs averaging 18%. CRESUD’s productive cropland, grazing and cattle land, and marginal reserve land is being created cheaply at current market prices. Conservatively assigning just $100 per hectare value to the reserve land and giving $1,000 per hectare to the cattle land and $5,000 per hectare for the cropland – toward the low end of the valuation range for farmland in conversations with public and private agricultural management teams (including AdecoAgro, SLC Agricola, Vanguarda, and MSU) – gives 600M value to CRESUD’s land, significantly higher than the implied for the land at today’s market prices. The per hectare valuations I assign are very likely lower than CRESUD will actually realize in the coming years: in 2014, well before the benefits of the new president, IRSA sold 2k hectares of the San Cayetano and Araucaria farms for $7k/ha at the blue dollar FX or $10k/ha at the official FX. Additionally, some transactions in the market show that some sales of prime corn-belt farmland occur at >$20k/ha.

Another way to look at CRESUD’s stub value is on a multiple of normalized EBITDA. Agricultural production in Argentina under Kirchner was significantly distorted by three policies: high tariffs, export restrictions, and FX convertibility. Macri has quickly adopted policies which benefit the agriculture sector: he eliminated the parallel exchange rate by floating the peso and eliminated export tariffs on wheat, corn, and beef and reduced the tariff on soy from 35% to 30%. Adjusting for these distortions CRESUD should earn 50-70M USD EBITDA, meaning its stub at current market valuation is 4-5x normalized EBITDA.

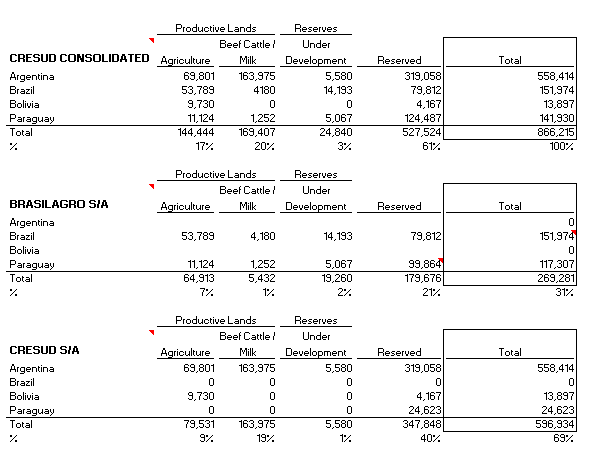

CRESUD's farmland is mapped here and laid out in appendix 3.

3. Argentina Macro

Macri was elected in the best possible outcome for IRSA, and CRESUD. Normalization has proceeded rapidly, with Macri in his first months in office since being elected in December pursuing almost all desired reforms: he has freely floated the Peso, lifted capital controls, eliminated export tariffs on wheat, corn, and beef and reduced the tariff on soy, settled with the holdout creditors, and reduced or eliminated subsidies including electrical subsidies. All these reforms have already stimulated foreign direct investment and optimism among management teams is high. As expected, the floated Peso moved to the "blue dollar rate" of ~15, similar to the FX rate I underwrote previously of 14.5. Central Bank Reserves have increased slightly since bottoming in December 2015. 2016E inflation is still very high at 30%+ though the administration announced they are targeting 5% by 2019. An additional significant upside from normalization for equities is Argentina's re-entry to the MSCI Emerging Market index and the associated capital inflows. After being downgraded to a Frontier Market following Kirchner's capital controls in 2009, Argentina should re-join the Emerging Market index now that capital controls have been lifted by Macri. As expected the MSCI put Argentina under "review" to re-join the Emerging Market index in June 2016. It will be included in 2017 annual market review. In addition to meeting requirements for openness of foreign ownership, ease of capital inflows/outflows, and stability of institutional framework, Argentina meets the minimal market size/liquidity thresholds with its largest public companies. I believe that Emerging Market index inclusion will be a major positive catalyst for re-rating Argentine stocks, given that Emerging Market tracking funds invest so much more capital than Frontier Market tracking funds (according to one source, on the order of 65x more).

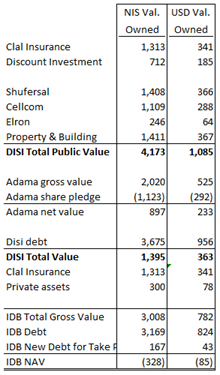

Appendix 1: IDB

I believe from speaking with holders, the company, research analysts, brokers, etc. that uncertainty about future IDB investment is the most significant factor in IRSA and CRESUD trading below fair value. IDB at cost is still a relatively small percentage of total asset value at IRSA: 350M USD investment, relative to 1.4B EV and 925M market capitalization of IRSA. The company has reiterated many times that they do not plan to make international assets larger than 20% short term or 10% long-term of the asset portfolio at IRSA (note they view current public valuation as materially below the true value of the assets), implying they do not plan to increase the current investment in IDB. Before the Adama sale, the market valuation of IRSA was clearly assuming that IRSA would fund the USD -320M NAV at IDB and more. Now that negative NAV hole has closed significantly by the 230M contribution from Adama sale at a value higher than I expected, IRSA is arguably even farther from fair value. Additionally, management has many levers they can pull including asset sales and dividends from operating companies such that more funding from IRSA is highly unlikely. I am confident from conversations with the company that they do not intend to inject more capital into IDB. Rather, they intend to make IDB [l1] self-funding through operating cash flow from the Discount Investment subsidiaries Shufersal, Cellcom, and PBC and IDBD subsidiary Clal Insurance and potential asset sales.

The company bought out minority holders in February 2016 with a deal I and they considered favorable given the alternatives. Dolphin, IRSA's investment vehicle for IDBD, had an above-market tender obligation agreed to at the time of original investment at a much higher price than current (NIS ~8/share vs. ~1.5 at market). Rather than fund the NIS 512M / USD 135M tender obligation to the minority holders, Dolphin bought them out and took the remaining IDBD equity private for 1) cash consideration of NIS 160M / USD 42M, 2) new IDBD bonds of NIS 167M / USD 44M, and 3) additional cash consideration of NIS 156M / USD 41M contingent upon Dolphin getting an operating permit for Clal, the largest subsidiary which they have failed so far to convince the insurance regulator to allow them to operate, or selling the Clal stake for >75% of Book value (>NIS 62/share vs. current price of 46), and 4) injection of NIS 350/ USD 92M cash into the company, to be used to satisfy ~70% of remaining 2016 debt maturities. The value of the new deal's guaranteed payments (cash + bonds) equaled 64% of the prior tender obligation and the value of potential payments (cash + bonds + Clal contingent consideration) equaled 94% of the value of the tender, and the cash injected into the company will likely be value to the creditors.

IDBD is a holding company that owns assets and has issued debt in Israel. The assets are mostly Israeli-listed public companies in which IDBD owns between 42-76% of the outstanding shares. These companies include Clal Insurance (61% of IDB gross value), a multi-line insurer which is 2nd largest in Israel, Shufersal (9%), a supermarket chain that owns real estate, Cellcom (6%), a wireless carrier, Property & Building (8%), a real estate owner/developer with primarily class A office assets, and Elron (2%), a collection of technology and biotechnology ventures. Additionally, IDBD owns private assets (13%) including a small tourism business, a share of a real estate development project in Las Vegas, Nevada called Trivoli. Finally, IDBD owns 40% of a large agro-chemical business called Adama but pledged their shares as part of an investment by ChemChina.

- Clal

Clal is currently earning a return on equity of ~4%, vs. 5 year average 6.9%, potentially lagging industry average return due to parent company complexity and legacy management. There is a significant difference between price-to-book ratio and price-to-tangible-book ratio, due to goodwill and capitalized/purchased software. This gap makes Clal look attractive on price-to-book but fairly valued on price-to-tangible-book. Clal's long term return on equity is 5.9% and return on tangible equity is 8.7%. Based on global comp trading averages, Clal's 8.7% RoTE should command a 1.1x P/TBV or ~NIS 60/share (vs ~45 current and BVPS of ~80).

- Cellcom

Cellular ARPU in Israel has declined significantly over last 4 years due to new entrants and a highly competitive pricing environment. The decline of average ARPU from NIS 170 to 70 has been a severe headwind for Cellcom, which has undergone several rounds of restructuring to reduce overhead and try to maintain margins. Cellcom currently earns 65% of the revenue and 35% of the EBITDA that it did in 2010. Even after aggressive headcount and operating expense reductions, Cellcom's EBITDA margins have declined from 40% to 20-22%. The industry believes that new entrants Golan and HOT are burning money in a "race to the bottom" to buy market share. Israeli ARPU is so low relative to comparable countries (at USD $18 per month for cellphone service with 3+ GB data plan) that the regulator has acknowledged the need for higher profitability to maintain infrastructure capex. At current run-rate EBITDA without any ARPU benefit, Cellcom is valued at 10.2x EBITDA-Capex, slightly cheap to global average 13.7x. Giving credit for ARPU +NIS 10-15 over 3 years, the stock would have 100-200% upside at unchanged multiple.

- Shufersal

Shufersal has operated in a difficult environment facing regulatory pressure on grocery price shopping. Topline has been ~ flat (0.7% 5 year CAGR) while EBITDA has fallen 30% (-6% 5 year CAGR). The 2011 "Food Law" passed in response to cost-of-living demonstrations pressured the grocery industry including restricting geographic expansion and mandatory pricing transparency. Additionally, concentrated suppliers (top 10 = 55% share) exert pressure on retailers and cost cutting is difficult given unionized labor and headwind of increase in minimum wage in 2017-2018. Opportunities include the bankruptcy of major competitor Mega/Blue Square which is a potentially temporary benefit; private label expansion from 5-10% historically vs. 25-35% global average, now to 17%; and a (currently small) fast-growing online channel. Shufersal also owns significant RE assets including 67 owned stores plus 20 multi-use properties plus NIS 700-800M of logistics properties. The ability to potentially spin owned RE assets helps alleviate pressure of 5.6x EBITDA gross / 3.5x EBITDA net debt. The stock looks fairly valued on its unlevered multiple of 8.1x EV/EBITDA.

- Property & Building

Property & Building owns, operates, and develops properties in Israel (80%), USA, India, and UK. Leverage is high at 94% gross debt / EV or 73% net debt / EV. Cash balance of NIS 2.3B covers ~2.5 years of maturities. The company believes it can refinance and extend other maturities as necessary (rating is BB+). US properties include the HSBC Tower on 5th Avenue and 40th St, where the IFRS value = USD 850M at a 4.5% cap. rate and the property has a 400M loan. Additionally there is a Las Vegas multi-use development called Tivoli which is owned both at PBC and IDBD directly and is worth USD 100-200M. Currently the stock trades at 80% of est. NAV but should trade to 90% or 100% of est. NAV (306-340 vs. 270 current).

Appendix 2: Short Report

I found the short report weak and misleading. It put forward many different arguments, some of which were petty and irrelevant (i.e. PWC's audit deficiency citations) but the claims that matter were:

1. Consolidation/recourse/covenants

Accounting consolidation and recourse from IDB's debt (through Dolphin ownership) to IRSA's assets are different. IRSA believed they didn't have to consolidate IDB into their financials because they owned 49% and the rest was held by IFISA, the private parent company. Now they are consolidating for accounting purposes but the report is arguably misleading in conflating consolidation and recourse ... the company is very clear that the debt is non-recourse (http://www.irsa.com.ar/archivos/IDBD-Consolidation-on-IRSA-Main-Effects.pdf) and additionally I've asked people familiar with IDB in Israel and found no evidence or rumor that any debt is recourse. It was clear from my conversations with the company that they will not consider pledging IDB assets to secure IDB debt. Consolidation adds some complication to the structure optically but I'm not worried there is a NAV impact. Additionally, Spruce Point argues that consolidation would trip IRSA's bond covenants. Per the indenture Consolidated Interest Expense and Consolidated EBITDA are defined as cumulative interest expense or EBITDA among all subsidiaries, a subsidiary being defined as a company owned >49% (regardless of financial statement consolidation or IFISA co-control). Therefore the consolidation will not impact the covenant test. Even if IRSA were in the future to go over 49% ownership of IDB they would have low-cost remedies by negotiating a waiver or amendment redefining Consolidated Interest Expense/EBITDA, carving out an exception for subsidiary consolidation, or waiving the incurrence covenant for interest expense coverage; or prepaying some or all of the bonds and issuing new debt with revised covenants.

2. De-listing

The short report also argued that IRSA’s having not filed IDB’s audited 2014 financials in US GAAS put at risk its ability to maintain the New York listed ADR. IRSA believed translating past IDB financials from Israeli to US GAAS was an undue burden and applied for waivers, but the company has made very clear they can and will have the financials translated as required and will definitely not risk the ADR registration over this issue.

3. IRSA-IFISA warrant transfer

The report also says there was an inappropriate below-market transfer of IDB warrants from IRSA to IFISA. On May 31 2014 IRSA sold 46M Series 4 IDBD Warrants (IDBDW4 on Bloomberg) to IFISA for 0.01/warrant, “on condition that IFISA agrees to exercise all of them when so required by IDBD to Dolphin.” The market price of the warrants at the time in question was NIS 0.46. On May 27 IDB stock was NIS 1.6/share vs. the warrants striking at 1.88, but then went up to 2.1 by May 31 on news that Elzstain was going to inject money into the company through these warrants. The warrants were out-of-the-money and since IRSA knew they were going to force IFISA to exercise the warrants in one week the fair value of the instrument with one week of time value would be ~0. While disclosure regarding this transaction could have been clearer, the company’s rationale makes sense, the short report ignored IRSA’s option to force the warrants’ exercise, and it’s a very small amount of money regardless.

Overall I thought the short report was misleading and I believe the difference between the stock price and intrinsic value is larger now than when I wrote up the idea. The investment in IDB has created confusion but is small relative to the size of the Argentine assets.

Appendix 3: CRESUD Detail

Disclaimer:

The author is presenting the views of an investment firm that has a material long position in the securities of the company discussed herein. The author is not otherwise affiliated with such company, including as an employee, director or consultant. The views expressed herein are provided solely for informational purposes and do not constitute an offer to sell, or the solicitation of an offer to buy, any security. The information provided herein is not intended to be, and should not be, relied upon as an investment recommendation in connection with any investment decision. The contents of this message should not be construed as legal, tax, accounting, investment or other advice. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained herein by the author or its affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions. The information and opinions contained herein are provided as of the date this message is originally posted. The author has not independently verified all information contained herein and has no obligation to update any of the information provided. The views expressed herein are subject to change without notice at any time and the author and its affiliates may trade in any manner in the company’s securities, whether consistent or inconsistent with the information provided herein, as they deem appropriate. Past performance of a security is neither indicative nor a guarantee of future results of such security. There can be no assurance that an investment in the company will be profitable or that the assumptions regarding future events and situations will materialize or prove correct.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

- IRSA's investment in IDB becomes self-funding

- Increased CRESUD agricultural earnings from currency and tariff policies

- Structural reorganization/simplification

- Argentina's upcoming EM index inclusion

| show sort by |