| 2020 | 2021 | ||||||

| Price: | 72,500.00 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 73 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 4,380 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 607 | EBIT | 0 | 0 | |||

| TEV (in $M): | 4,987 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

Description

Situation Summary

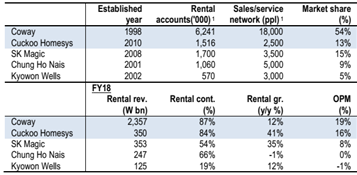

Coway (021240 KR) is the heavyweight of health appliance rental market with 7.4m customer accounts and 50% market share in the domestic Korean market. 80% of revenue comes from high margin, monthly contracts. The remaining 20% includes direct sales to export markets where renting is not the norm, including the US and China. Despite the entrance of numerous copy-cat competitors, Coway has defended its position at the high end of the appliance market, and continues to grow customer accounts organically each year.

On February 14th 2020, Netmarble acquired a 25% equity stake in the company from Woongjin Thinkbig in a distress sale. When new management announced a 3-term plan to de-lever the balance sheet and focus on product development while reducing Coway’s dividend payout, dividend funds liquidated their positions and the share price fell 18% in a single day. Coway currently trades 19.8% below the pre-announcement price, and 39.7% below Netmarble’s purchase price.

Despite the overwhelmingly negative price reaction, the same operating team remains in place, and Coway’s operations have remained stable throughout Covid. In reality, the company’s condition seems likely to improve under Netmarble. The prior owner, Woongjin Group, had saddled Coway with acquisition leverage, questionable royalty obligations, and inflated related party purchases. Meanwhile, Netmarble already enjoys a net cash position and has demonstrated via the dividend cut that it has long-term goals beyond milking Coway for cash. Further, Netmarble’s strengths in IT, CRM, and data-driven cross-selling appear to complement Coway’s weaknesses as a traditional door to door service company.

Brief History and Business Model

Coway was the first successful player in Korea’s the appliance rental market after entering the market in 1999. Over the years, the company diversified from water filters to air purifiers, bidets, mattresses, and clothing purifiers while maintaining its reputation for top quality.

Korea’s home appliance rental market is a unique industry that deserves an introduction. In recent years, wage stagnation coupled with growing concerns about environmental pollution (see fine dust warnings, red tap water in Incheon) have propelled the health appliance rental business into the mainstream. Coway alone has 17% penetration into Korean households. At the same time, the total market size has actually increased with the rapid formation of single households, whose members spend an average of 40% more per capita than those living with family members.

Coway’s rental customers pay roughly $20/ month to rent reverse-osmosis water filters, industrial-grade air filters, bidets, and other appliances that otherwise retail for $500 to >$1,000. Membership includes professional cleaning, filter replacements, and repair services by a professional Coway service provider (“CODY”). Although the services concept probably seems odd here in the DIY-loving U.S., most Korean households value the convenience and peace of mind that comes with professional maintenance, and even pay for this service on some of their fully-owned products.

At the end of a 3-5 year rental contract, ownership of the appliance transfers to customer. However, only 23% of retiring accounts actually retire; 45% start a fresh rental contract with a new product, and another 32% continue to subscribe for maintenance services.

Cancellations have been stable at 1% a month, in part because of cancellation penalties that occur early in the contract. Secondly, while the effect is hard to quantify, customers build up a level of trust with their assigned CODY over years of repeated home visits, and this social contact also reduces cancellations. Meanwhile, average products per account is 1.77x and has increased each year since at least 2012.

Source: company disclosures

Competitive Advantages

1. Large service force of CODYs

Through its 22 years of continuous operation, Coway has built up a team of some >15K sales people who work on commission to provide appliance-related sales and services.

The scale of this group lends itself to natural operating efficiencies, as each CODY can handle 300-400 accounts without going beyond 1 km^2. Thus sales contractors with Coway enjoy a level of account efficiency that cannot be replicated at the smaller competitors.

Without the advantage of a large enough salesforce, many competitors have leaned on competing sales channels such as home-shopping, retail sales, and online -- that also happen to be effective for gaining share at the lower end of the market.

2. Reputation as most trusted health appliance brand

Coway manufactures key products in-house and has a reputation for differentiated quality, for instance, leading in water purifier brand surveys for 20 consecutive years. Among its flagship products are a tankless reverse osmosis water purifier.

In contrast, appliance rental newcomers have grown their account base quickly by targeting the low-end market with basic, lower-cost water and air filters. In each category, Coway is able to charge 20-30% more than its competition.

source: Korea Brand Power Index, KMAC.

3. Capital Efficiency

ROIC (NOPLAT / Invested Capital) averaged 37% between 2017 and 2019, suggesting that this is a highly capital-efficient business.

Intuitively, we can understand that manufacturing air and water purifiers is not too land or capital intensive. Roughly 75% of Coway’s fixed assets comprise their fleet of rental appliances that are deployed in customers’ homes. Finally, the majority of the workforce is effectively work from their own homes and neighborhoods, saving on the need for a large office facilities.

4. Operating Leverage

Because expenses related to commission and production are typically recognized upfront, customer accounts typically do not reach break even until the second or third year. Thus, Coway’s large base of paying accounts allows the company to stay cash flow positive as it invests through the growth phase of new accounts, while opening up possibilities from organic cross-selling.

Consensus view

Before February 2020’s change of control, the conventional view of Coway was as a blue chip stock operating in a saturated and mature market, with few growth opportunities to look forward to. After February, the sell-side abruptly soured on the stock, with about half of buy ratings flipping to sell or hold. A top tier prominent research house recommended a 33% price target cut, noting that Coway’s potential is "capped due to a lack of positive catalysts".

Exhibit: Broker Recommendations (source: FactSet)

Variant View:

Prior to COVID, between 2017 and 2019, Coway’s top line grew 5.9%, 7.6%, and 11.9%[1], which can be attributed to two growth drivers

1) Organic account growth in Korea is growing at ~4% per annum, helped by cross selling and new product categories.

2) Overseas markets.

o Malaysia is Coway’s most successful overseas market to date. Coway entered in 2006, and steadily built up a local salesforce and brand awareness by educating consumers on the benefits of water filtration. Coway’s operations finally achieved profitability and scale in the last few years; MA sales grew 45%, 70%, and 49% in the last 3 years.

o Coway also has operations in several nascent markets including Thailand, Indonesia, and China.

Impact of COVID

The high proportion of recurring contracts has kept revenues stable through COVID (Q1 sales reached a record high, growing 8.4% year over year). There has been no effect in S Korea beyond a brief service visit suspension in Daegu and Gyeongbuk. However, Malaysia’s government implemented a lock-down mid-March that forced Coway to suspend face-to-face sales and service visits. The full impact on Coway in terms of cancellations or sales interruptions can only be known after the Q2 earnings results, but the uncertainty has created another source of overhang on the stock and has already led to earnings downgrades.

Financial Projections and Valuation

Our model makes the assumption that 2Q and the remainder of the year may yet still see a slow-down from COVID containment policies; it assumes 0-growth in 2020, ramping to 5.4% in 2021, and returning to 7.6% in 2022.

Coway’s operating margins have historically ranged in the high-teens. Our projections assume that the conversion of Coway’s 1500 repair contractors in 2020 creates an incremental opex burden in 2020, which causes operating margin to remain below margin levels seen in 2017 and 2018[2].

Approach 1: Fair EV/ NOPLAT multiple

- Based on historic ROIC’s (ROIC averaged 34% over 10 years), we calculate a fair EV/ NOPLAT multiple of 20x. This assumes long-term growth of 6% (derived from 20% ROE x 30% long-term reinvestment); 30% ROIC; and 10% WACC.

- As a sanity check, this multiple approximates Coway’s 10-year average EV/ NOPLAT multiples of 21.6x.

- Multiplying this by projected 2021 NOPLAT yields KRW 8,455bn, 41% above current value enterprise value.

Approach 2: Discounted Cash flows

- Coway’s operations are capable of generating 11%+ free cash flow margins in years without capacity additions. We forecast that the company can comfortably reach a net cash balance by 2022. The DCF model assumes 7 years of economic value added operations, during which returns on capital exceed the company’s cost of capital. Assuming a 10% discount rate and 2% perpetuity growth, this yields an equity value of K6,974Bn, 32.7% above the current capitalization.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

· Increased clarity regarding Netmarble’s plan. The Q2 earnings call in August may be a chance for Coway’s new CFO to discuss Netmarble’s capital allocation strategy in more detail.

· Visibility on future plans for the dividend payout.

· Evidence of efficiency improvements in cross-selling and customer retention y.

· Exit of sub-scale entrants competitors. As recent entrants approach their fifth year of operations and account churn data becomes normalized, investors can have a more realistic sense of the competitive environment.

| show sort by |