| 2021 | 2022 | ||||||

| Price: | 142.00 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 84 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 11,928 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | -445 | EBIT | 442 | 0 | |||

| TEV (in $M): | 11,483 | TEV/EBIT | 26 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

Description

The transition to SaaS and the cloud shifts business CapEx to OpEx and simplifies the hardware maintenance, integration, and troubleshooting tasks of IT departments, but it brings a new set of complexities in managing licenses and multi-cloud environments. Crayon Group is a VAR that resells software and the services and consulting around it. Crayon helps companies save money as they manage byzantine software licensing agreements and multi-cloud environments. As such, they have grown faster than an already rapidly growing industry. And, despite strong stock performance, I believe the market is underpricing the opportunity ahead.

Crayon Group is a NOK11.5b EV (1.3b US) company listed on the Oslo Børs trading at 22x 2021 EBITDA, .47x Sales, and 4x Gross Profit. Crayon has grown gross profit at a 25% CAGR from 2018 through 1Q2021 (19% since 2012) and is expected to grow at 20-25% this year and 15-20% in the medium-term. Crayon is cheap and underfollowed due to its size and domicile, limited coverage, and EBITDA margins at around half of their long-term potential. If you simplistically applied Nordic region margins to the entire company, Crayon would be trading at under 20x 2021 taxed EBIT. Of note, unlike hardware VARs and distributors which are working capital intensive, Crayon runs negative working capital balances of -20% of gross profits. Thus at past and projected growth, EBITDA converts about 100% to free cash flow.

Crayon has reached an inflection where ~50% of gross profit is now international and where we have evidence that international margins can converge on those in the Nordic region (note that whenever I discuss EBITDA margins in this write-up, they refer to EBITDA vs. Gross Profit given the pass-through nature of software licenses).

There aren’t any crucial structural or competitive differences between regions, and I believe that margins globally will converge on the Nordics over time. We have some evidence to that effect: margins in Germany and India have already grown to Nordic levels, and incremental margins in other regions like APAC & MEA have run above 30%. Additionally, management has reiterated over many calls that they are investing in growth but that EBITDA margins should converge over time. You can dig further and make assumptions about how many recent employee hires are unprofitable and arrive at similar conclusions. If you look at 1Q 2021 average employees of 1,951 vs. 4Q 2020 of 1,727 and compare that to NOK491mm employee costs in Q1, or just compare employee costs in Q1 vs. a few quarters ago, you arrive at anywhere between NOK160 and 220mm of employee costs for new/unproductive employees (or 40-50% of 2020 EBITDA). Growth and share gains in newer regions can also be driven through price and a more speculative or "show-me" type of engagement where Crayon proves their worth to new clients at initially lower profits.

In the medium-term, management guides for “double-digit” EBITDA margins. I’d like them to push growth for as long as possible, so I'm hoping margins stay there longer. Not many businesses could grow at the rates Crayon does internationally while keeping margins close to flat (and now positive) and running negative working capital balances. Fewer still trade at this valuation.

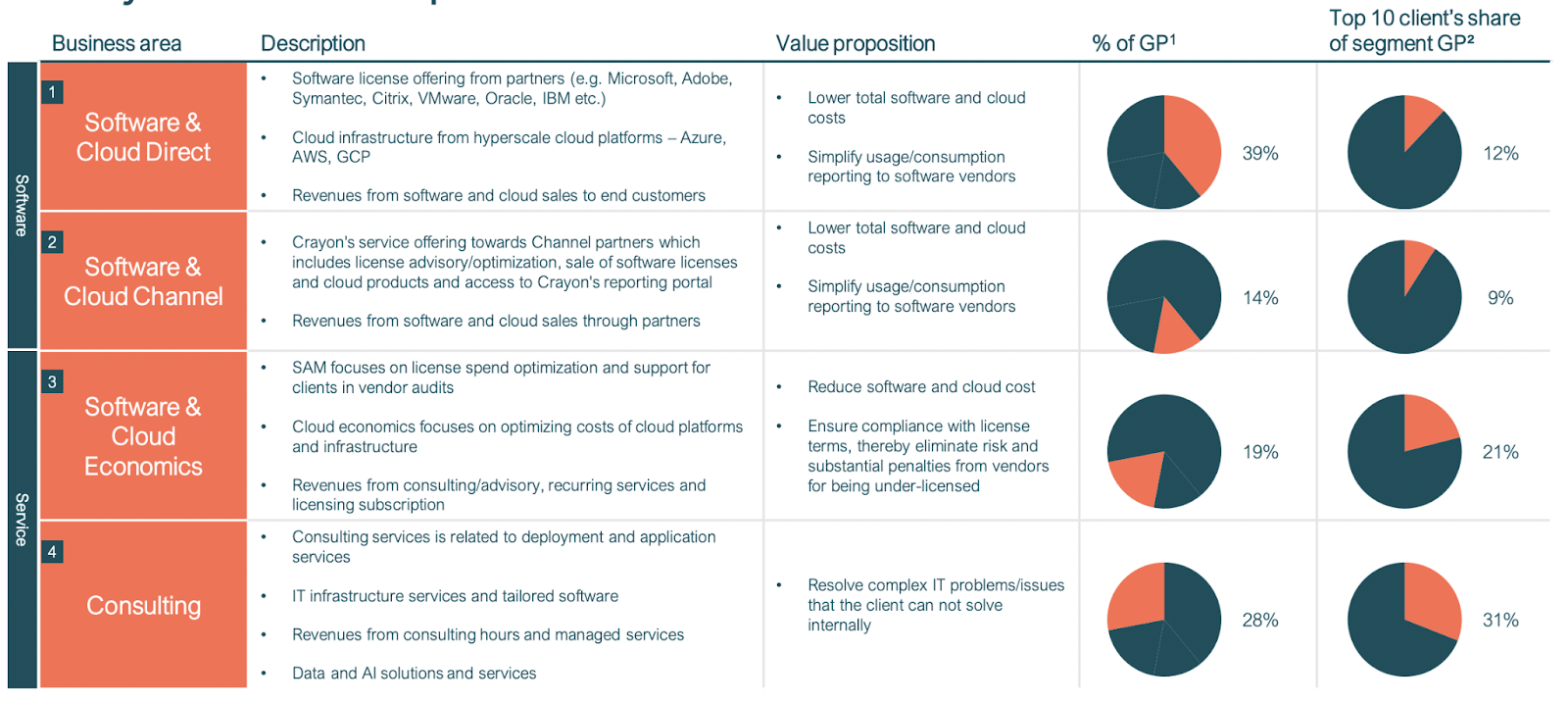

Let’s take a step back and go through Crayon’s business model for context around my hypotheses of margin expansion and value-added growth. Below I’ve included Crayon’s segment breakdown and description, but I’ll try to simplify it further. Essentially VARs act as the outsourced sales and distribution arm of software (and hardware) providers. VARs provide software licenses to companies and provide varying levels of handholding around that.

In Crayon’s case, the handholding they add - through both their Consulting and Software & Cloud Economics (fka Software Asset Management) businesses - is on saving clients money on licensing, preventing costly audits, and assisting transitions to cloud (and often multi-cloud) environments. Crayon typically leads with these services, i.e. they go to a company and tell them that they can save money if they let Crayon analyze their licensing agreements. In return they can pay Crayon directly and let Crayon manage their licenses going forward.

The need for VARs makes more intuitive sense when you think of hardware sales (again, Crayon only sells software, but I’m using hardware VARs to illustrate a point). A hardware VAR acts as a distributor, educating small businesses on the suitability of hardware options and making the (working capital) investments necessary to sell that hardware. But with software, especially SaaS software, the need for a VAR isn’t as obvious. You would think you could just go to their website and sign up. This seems especially true when public cloud providers like AWS have marketplaces where vendors can sell software to customers through a portal. But it turns out that everyone in the ecosystem, from hyperscale cloud providers to software vendors and customers, prefers to work with a VAR. Why is that?

Volume based discounting is part of the answer. Any single software vendor might be able to offer a customer more attractive economics versus what their VAR provides, but volume through the VAR matters and so the overall economics are better if you go through the VAR.

Software vendor access to markets is another part of the answer. Smaller vendors find that being part of a VAR channel means that in return for the VAR taking a small cut, the vendor has access to more customers.

Complexity is also a factor. It turns out that usage based models run in the cloud, or perhaps in a few clouds, are at least as complex to manage as traditional on-premise software licenses. Though companies enjoy outsourcing the hardware and maintenance requirements associated with on-prem software, they find that managing the licensing is actually more complex. Many Crayon engagements start when a company faces an audit from a software vendor. Audits happen every few years with some vendors, and non-compliance might mean a company owes years of back payments at 100% retail margins. Crayon is often recommended by the software vendors themselves to help with the process. Often, Crayon takes over the management of that vendor’s relationship with the company and eventually other vendor relationships as well. If Crayon gets a foot in the door they often find that they can save companies 30% on their software license costs initially.

I still find it hard to wrap my head around the idea that a company like Crayon acting to save customers money can endear itself to software vendors. Crayon sums it up with this graphic:

The idea is that you start by saving a company money but by having Crayon manage the relationship it will eventually lead to higher total spend with the vendor as more value is added to the business over time with additional software.

More compelling to me is the simple fact that 94% of Microsoft’s commercial revenue flows through its partner network. Clearly they see a need for resellers. And Crayon, with its Software Asset Management led model, is taking share. Crayon has also expanded its relationships with cloud providers like AWS who have also seen the need for partners to help onboard and manage customers. The below graphic is a ranking by region of Microsoft’s license sales through partners. If Crayon were annoying software vendors like Microsoft by saving clients money, they wouldn’t be allowed to grow in importance to those vendors over time. This is a crucial point to note because to some extent the importance of VARs is dictated by the level of importance/relationship (e.g. “platinum” tier) they have with vendors.

Crayon is a leader in what they do. Crayon claims to have the highest number of independent (i.e. not working for a software vendor) Software Asset Management (“SAM”) consultants, at 340, in the world. And they have been recognized by Gartner as being a leader in this service. Other parts of the business are also market leading. Crayon has 94% repeat buyers in the Software & Cloud Direct Segment.

Valuation

(Note that Crayon recently announced the acquisition of Rhipe Limited. To keep it simple, I’m not including that acquisition or its financing in this valuation)

My valuation is predicated on margin expansion and value-added growth. I’m much more confident in the ability of Crayon to achieve scale margins because we have plenty of evidence today that it’s possible as I hopefully demonstrated above. I’m less confident in any growth projection and therefore less willing to use it in my valuation. My solution here is to assume declining growth until 2025, after which I apply a market multiple after assuming scale margins. I assume gross profit grows at ~18% (higher now, lower by ‘25) to 2025 and EBITDA/GP gets to almost 20%. Clearly if Crayon continues to grow beyond that point, margins will be lower, but terminal value would be higher than what a market multiple on scale margins would imply.

At 18x 2025 taxed EBIT, Crayon would be worth about NOK300/share, which is about a 20% CAGR from today. Because working capital is a source of cash, my cash builds at just about cumulative EBITDA over that time. Another way to look at it, as stated in my introduction, is that we’re at about 20x taxed 2021 EBIT assuming scale margins, and 22x 2021 EBITDA and FCF (which approximates EBITDA given working capital as a source of cash) as long as we grow at these rates.

Crayon also stands out when comparing 2021 EV/EBITDA versus growth (which I show as three years through 2022E to eliminate any COVID distortions) to peers. I hate buying anything that has a stock chart like this, but as with any better business that grows over long periods, value is almost never recognized all at once.

I’ll conclude with a brief discussion on management. The founders are still involved at the board level and we have a new CEO. Insiders own some stock, but this isn’t by any means founder-run and controlled. Founder shares show up on the holders list as Karbon Invest AS.

Risks

- Microsoft is a large vendor for this business. Changed incentives offered by Microsoft, strategic priorities, or any deterioration in the relationship would be a clear negative

- new CEO. The founders are still involved, but now only on a board and ownership level.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

Growth, op leverage.

| show sort by |