| 2017 | 2018 | ||||||

| Price: | 33.00 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 32 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 838 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 487 | EBIT | 0 | 0 | |||

| TEV (in $M): | 1,325 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- Convertible Bond

- Family Controlled

- DOREL INDUSTRIES INC DII.B 01/19/2023

- DOREL INDUSTRIES INC DII.B 11/01/2020

- BETA

- SLEEP NUMBER CORPORATION SNBR 08/21/2018

- Universal Stainless USAP 02/23/2023

- Office Properties Incom Trust OPI 4.5 2025 03/21/2024

- Shimano Inc 7309 S 01/29/2023

- STAGE STORES INC SSI 11/21/2019

- HARLEY-DAVIDSON INC HOG 09/18/2020

- IES HOLDINGS INC IESC 08/15/2022

- SUPERIOR INDUSTRIES INTL (SUP) SUP 02/15/2024

Description

NOTE: THIS IS A LOW-YIELDING, SHORT-DURATION CREDIT IDEA THAT PROBABLY IS NOT WORTH READING UNLESS YOU HAVE SIGNIFICANT EXCESS CASH OR A NARROWLY-FOCUSED MANDATE.

Investment Thesis

Dorel Industries is a Canadian mini-conglomerate that owns three consumer products wholesaling businesses. The company owns well-known brand names in each segment, including Safety 1st and Maxi-Cosi in the kids business, Cannondale and Schwinn in the bike business, and Cosco in the home and office business. The former two businesses have struggled over the last several years, and we believe they are underearning. In contrast, home and office is hitting the ball out of the park and may not be getting the credit it deserves for its e-commerce growth.

Dorel is family-controlled and run by the Schwartz Brothers and their brother-in-law. CEO Martin Schwartz and his brother-in-law founded part of Dorel’s furniture business way back in 1969 and have not worked anywhere since. Martin has been the CEO since 1992. He is 68 years, and the others are 66, 65, and 54. The four executives have a combined 16% economic interest in the company and 47% of the voting control. The Schwartz’s mother Laura (wife of the late founder) owned another 9.5% of the votes, giving control to the family. She passed away in April. Her death could be the impetus that causes the brothers to sell after a lifetime of service to the company. They would each get a CAD 42 million payday at today’s prices.

Dorel will be sold in pieces at some point, but we don’t have confidence in the timing. If a sale were to occur today, we believe it would be for significantly more than current trading levels. On a standalone basis, the stock is probably not trading at a material discount. However, the company has a small convertible issue that we believe is attractive considering the dearth of non-distressed credit opportunities. The 5.5% converts mature on November 30, 2019, but must be redeemed before May 30, 2019. They are currently trading around 102 for a 4%+ yield to May 2019. The bonds are USD denominated. They are traded on the Toronto exchange and are available to Canadian retail investors, but are considered 144A securities for U.S. buyers.

Company Analysis

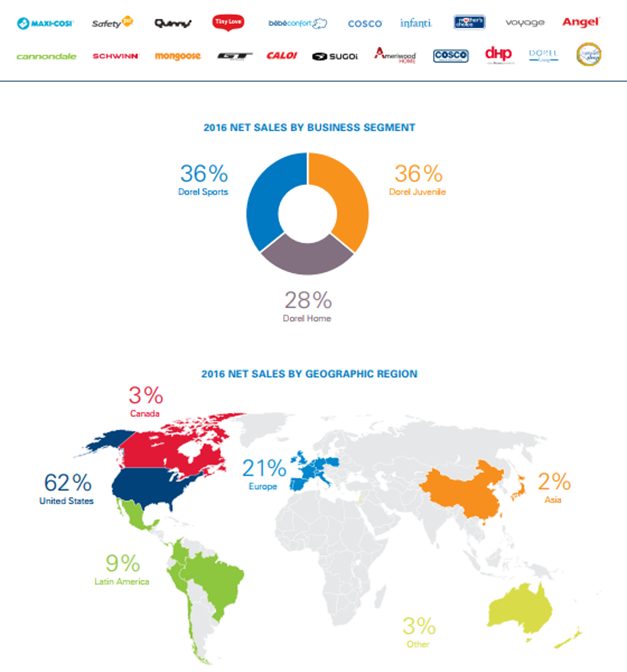

Dorel Industries was started by Leo Schwartz (the brothers’ father) in 1962 as a manufacturer of cribs. It was merged with Martin Schwartz’s furniture business in the late 1980s, after which it completed an IPO in Canada. The firm has grown by acquisition. The kids business grew materially in 2000 with the purchase of Safety 1st. Dorel entered the bike business in 2004 with the purchase of Schwinn’s parent, then it bought Cannondale in 2008. The three businesses each make up about a third of total sales. By region, more than half of sales are concentrated in the U.S. This is because Dorel’s largest customer is Wal-Mart. Across the three business, Wal-Mart accounted for 28% of Dorel’s sales last year, with 24% in the U.S. Sales to Wal-Mart are mostly concentrated in furniture and bicycles.

Dorel Juvenile

The Dorel Juvenile segment produces and sells child products in over 115 countries. The business accounted for 36% of Dorel’s total sales in 2016, down considerably from 45% in 2010 due to weak results and growth in other segments. Juvenile product lines are primarily composed of car seats, strollers, high chairs, swings, toys, and safety products. The segment owns kid brands that are well-known in their respective markets. The segment’s global brands are Safety 1st, Quinny, Maxi-Cosi, and Tiny Love. Regional brands include Cosco, Bebe Comfort, Infanti, Voyage, Angel, and Mother’s Choice.

Dorel’s market position and strategy vary by geography. In North America, the company primarily sells opening price point merchandise to mass merchants. Cosco car seats and strollers are some of the cheapest you can buy. Cosco car seat prices are generally not much more than $50, and umbrella strollers sell for less than 20 bucks. They are available at standard mass retailers like Wal-Mart, Target, Kmart, Toys “R” Us, Bed Bath and Beyond, etc., as well as well-known online retailers like Jet and Overstock.

The North American juvenile market is one of Dorel’s toughest for a few reasons: 1) the majority of Juvenile’s sales are in opening price points where the offerings are highly commoditized, 2) these sales are concentrated with powerful mass merchants, and 3) Dorel has strong competition from sizeable peers that have moderate brand awareness. These peers include Graco (owned by Newell Brands), Evenflo (Goodbaby International), and Britax (PE firm Nordic Capital). Britax is higher-end, but Graco and Evenflo are very well represented at mass retailers, with Evenflo car seats dominating Wal-Mart’s online offerings. While no financial data is disclosed, management has made it clear that U.S. margins are lower than Europe and are unlikely to ever get as high due to the concentration of customers.

In Europe, Dorel mostly sells mid-tier and high-end price point products to juvenile product chains, specialty stores, and independent shops. In the 2010 Annual Report, the company claimed, “in Europe, no other juvenile manufacturer has the presence we do in the ranking of leading juvenile brands.” Dorel now describes its European business as “one of the leading juvenile products companies in Europe.” The segment’s primary brands in the region are Maxi-Cosi, Quinny, Safety 1st and Bebe Comfort.

Dorel entered Brazil in 2009 with a local partner. It began manufacturing car seats in the country in the same year. It expanded its Latin American presence in 2011 via the 70% acquisition of Infanti, which it claims is one of the most popular brands in Latin America. Along with the purchase came 52 retail stores operated under the Baby Infanti banner. The store base was expanded over the following years and now stands at 100 stores in Chile and Peru. The company does not provide a regional or product line breakdown on the segment level, but we do know Latin American sales are material. In early 2012, management disclosed that revenue outside of North America and Europe was 15% of Juvenile sales. Brazilian revenue was a low single-digit-percentage of segment sales. This equates to $156 million of Juvenile’s $1.04 billion in sales in 2012.

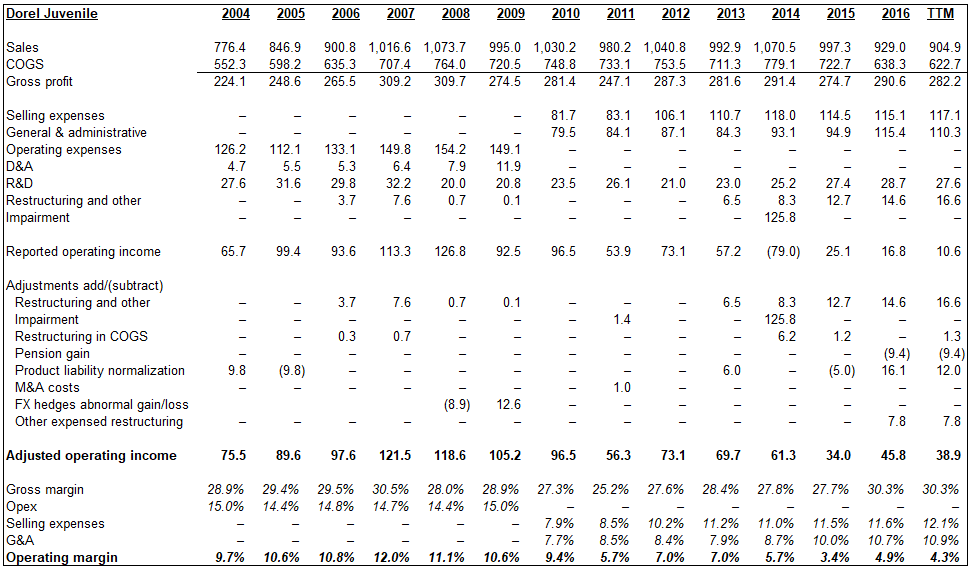

The Juvenile business appears to be moderately recession resistant due to the non-discretionary nature of the products, particularly in the lower and mid-priced products. The Juvenile segment performed reasonably well throughout the credit crisis, as one might expect, with organic sales declining only 4% in 2009. Newell’s Baby & Parenting business reported a mid-single-digit decline in sales in 2009 as well. Dorel’s U.S. sales were down less than 2%. European products struggled due to higher price points, but the organic sales change was still relatively muted at -12%, -9% and -6% in Q109, Q209 and Q309. However, the segment has struggled mightily over the last several years. There have been several minor reclassifications related to shifting products between segments (ex. moving cribs from Juvenile to Home in 2016), so we can’t know exactly how far revenues and income have declined over the last decade, but a rough estimate makes the point. Trailing-twelve-month sales of $905 million are roughly 15% below 2008 levels, and reported operating earnings have been completely decimated, falling from $127 million in 2008 to just $11 million in the TTM period. While we do not believe the segment will ever recover to historical levels, we do think it is underearning and has the opportunity to materially improve operations in the near future.

In 2014, a publicly-traded Hong Kong baby product manufacturer named Goodbaby International (ticker: 1086 HK) acquired Evenflo, one of Dorel’s primary U.S. competitors. Goodbaby was a significant supplier of products to Dorel. The relationship dates back to 1994, and Dorel had accounted for over 80% of Goodbaby’s U.S. sales in past years. Goodbaby had very little pricing power and only generated 2-3% margins, according to an old sellside report. The possibility of losing control of the supply chain caused Dorel’s management to purchase its own manufacturing facilities in China and Taiwan. Dorel bought the juvenile division of Lerado Financial Group (ticker: 1225 HK) in October 2014 for $120 million. The convertible bonds were issued to finance the purchase. In the 2014 annual report management commented, “for decades, a key strength of our juvenile business was a significant mass merchant presence in North America in the opening to mid-price point categories. We had a comfortable position in that segment but it has been contracting as we found ourselves in competition with Chinese factories. This remains a great category for us and this acquisition will put us solidly back in the game.” So far, the Lerado purchase does not appear to be a success. Several management changes have been made, smaller parcels of the main manufacturing campus have been sold off, and full production of Dorel’s own products has yet to ramp completely. However, it is difficult to evaluate due to pressures in other parts of the business, such as the volatility of foreign exchange rates and pricing pressures at U.S. mass merchants. We suspect gross margins would be lower than reported if the acquisition had not taken place, but operating expenses would likely be lower as well.

The last three years have been very tough for Juvenile. While the top line has mostly been flat (ignoring product line shifts), adjusted margins have cratered from 7% in 2012 and 2013 to just 3.4% in 2015. Foreign currency negatively impacted 2015 EBIT by $20 million. This was partially due the depreciation of the Euro, as European products are sourced from the Far East in U.S. Dollars. The Brazilian Real also had a significant impact. Management claimed the U.S. business actually showed improvement during this period as it exited super-low margin product lines. While it has yet to be reflected in the financials, management believes the juvenile market’s outlook is more favorable than it has been in several years. Dorel has multiple new product introductions that are expected to benefit the second half of this year. Additionally, point-of-sale data at the largest customer in the U.S. has been solidly positive, so some recent inventory destocking should reverse.

Barring wild swings in FX, we think Dorel Juvenile should be able to grow the top line slowly from here. We start with a $925 million sales estimate. While trailing-twelve-month adjusted operating margins are just 4.3%, the segment should be able to achieve at least 5%, which it hit in 2016. Goodbaby is probably the best comp as it has continued to buy brands and reduce its reliance on contract manufacturing. The firm recently announced another deal. The Street expects Goodbaby’s margins to rise to 6.2% for the year ended 12/31/2017 and 7.1% in 2018. Newell’s Baby & Parenting margins are much higher than both Dorel’s and Goodbaby’s at over 12%. Newell’s products occupy higher priced points and therefore may be less commoditized. Additionally, Newell sources from a single supplier and therefore probably has significant control over pricing. Hence, we believe 5% will prove conservative. Margin upside is more likely than not, particularly under new ownership. $925 million in sales at a 5% margin equals $46.25 million in segment operating income.

Goodbaby trades at 16x 2018 EBIT and 0.9x 2018 sales. Applying the same multiples to Dorel Juvenile yields $740 million and $833 million. The sellside is anticipating faster growth for some of Goodbaby’s business lines, so the Evenflo acquisition is probably a better comp. The Evenflo purchase was completed for $143 million in 2014. Evenflo was struggling at the time, and turnaround risk was a concern of the sellside. More than half of the company’s sales at the time were car seats. Evenflo generated $208 million in sales and $8.9 million in EBITDA in 2013. Jefferies put the EBITDA and P/S multiples at 13.8x and 0.7x. Goodbaby was probably willing to pay up despite the poor profitability as it would further allow the company to shift business away from Dorel. The brief acquisition document included a paragraph on potential synergies as well, but no estimates were provided. Goodbaby’s management must have believed they could achieve margins similar to Dorel Juvenile’s at 6-7%. At 7%, the buyout multiple would have been 9.5x EBIT.

We think 9.5x is fair for the North American business, which is most like Evenflo. It’s worth noting that the company used a 9.4x multiple to value Juvenile North America’s goodwill in 2016. The company discloses a lower pre-tax cap rate used to value Juvenile Europe, which makes sense as we believe the European business is stronger. 9.5x should be a comfortable floor. This puts the Juvenile valuation $440 million. We believe it’s fair to assign a premium to the European business, which probably accounts for about one-third of Juvenile’s revenue. Our calculations suggest a $40 million premium is reasonable ($480 million), or 10.8x normalized EBIT.

Dorel Sports

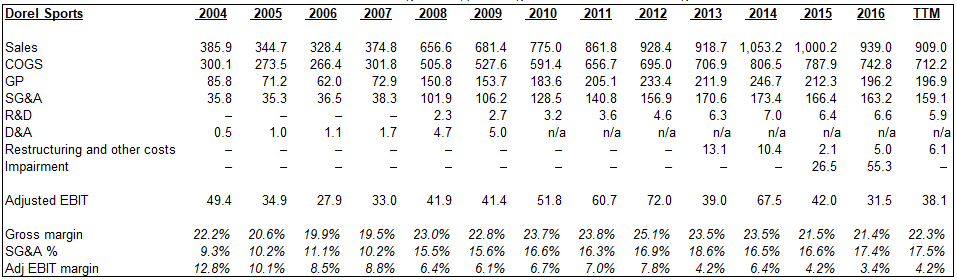

Dorel entered the bicycle industry through its 2004 acquisition of Pacific Cycles, which included highly recognizable brands such as Schwinn, Mongoose, and GT. At the time, Dorel claimed it was the number one supplier of bicycles in the U.S., with a 27% market share and 44% of mass sales. In the following years, Dorel expanded its bicycle business with several more purchases, including Cannondale, Iron Horse, and most recently Caloi, which is South America’s most popular bike brand. The segment also sells jogging strollers and bike accessories. It is also a top manufacturer of electric ride-along toys under the Kid Trax brand. Dorel Sports accounted for 36% of total revenue in 2016.

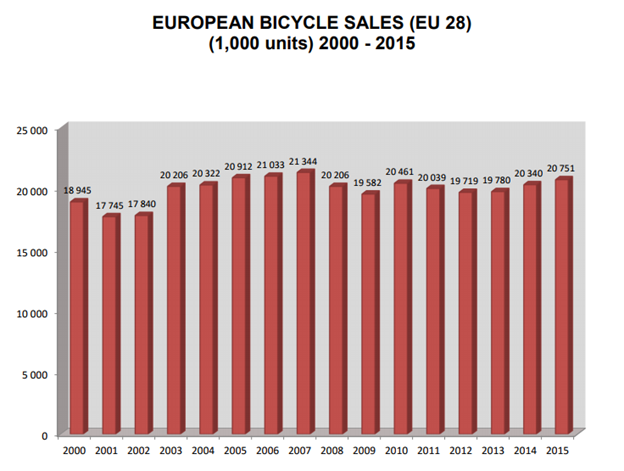

The National Bicycle Dealers Association produces extensive industry research and provides decent summary statistics for free. The statistics that follow were sourced from its most recent 2015 summary or Dorel’s annual reports. In the U.S., 74% of bicycles are sold through mass merchants, where the highest prices are in the $200-$300 range. The average selling price was $89 in 2015. The percentage of bikes sold in mass has been mostly stable over the last decade or longer. Wal-Mart is of course the course the largest bicycle retailer in the country. Approximately 25% of Dorel Sports’ sales in 2016 ($230mm of $940mm) were made to Wal-Mart in the U.S. Segment sales to Wal-Mart outside of the U.S. were minimal. The company’s most important mass brands are Schwinn and Mongoose. Mass merchants sell a few other brands, but Schwinn and Huffy are the largest. Huffy went bankrupt in 2004 due to pressure from Wal-Mart to compete on price with low-cost imports.

The firm’s premium Cannondale and GT bikes make up the Cycling Sports Group (CSG). These brands are almost exclusively sold to independent bicycle dealers (IBD). There are roughly 3,800 shops in the U.S. that capture 13% of units but nearly half of dollar share. The number of independent bike shops has declined dramatically over the last 15 years or so as shops have struggled to remain afloat. However, independents total share has been steady because larger stores are doing more business. Retail prices at IBD can reach $10,000 per bike or more, and the average price was $753. Customers are obviously enthusiasts that pay premium prices for quality. Brand names are likely to be valuable intangibles in this subset of the market. Cannondale and GT are both respected brands, but Trek, Giant, and Specialized are far larger. A 2012 market share study[1] showed “Brand Representation in Bike Shops” to be dominated by Trek with 23%. Trek owns a number of well-known smaller brands as well. Giant held 11% and Specialized was at 9%. Cannondale on the other hand was just 3%, but this was enough share to place the brand at #8, although an analyst on the Q216 conference call claimed Cannondale was #4. GT is smaller but is still well represented in lists of top bicycle brands, particularly in mountain and BMX bikes.

Trek generates about $1 billion in sales, while Specialized is estimated to be about $500 million. Giant is publicly-traded in Taiwan (ticker: 9921 TT) and produced $1.8 billion in sales last year, but this includes a significant contract manufacturing business. Additionally, only about 50% of sales are generated in the U.S. and Europe. The largest European makers, Accell Group (ticker: ACCEL EU) and privately-held Pon Holdings (bike division), which nearly merged a few months ago, produce $1.1 billion and an estimated $800 million in sales.

While Dorel hardly sells any mass bicycle products outside of North America, the CSG business has a much larger international presence. Back in 2007, 40% of Cannondale’s sales were from Europe. More recently, the firm disclosed in 2011 over 50% of CSG sales were to North American customers. The Cannondale brand is very popular in Europe, but the market is much more fragmented, with numerous small regional competitors that, in some cases, enjoy high market share in their respective geographies.

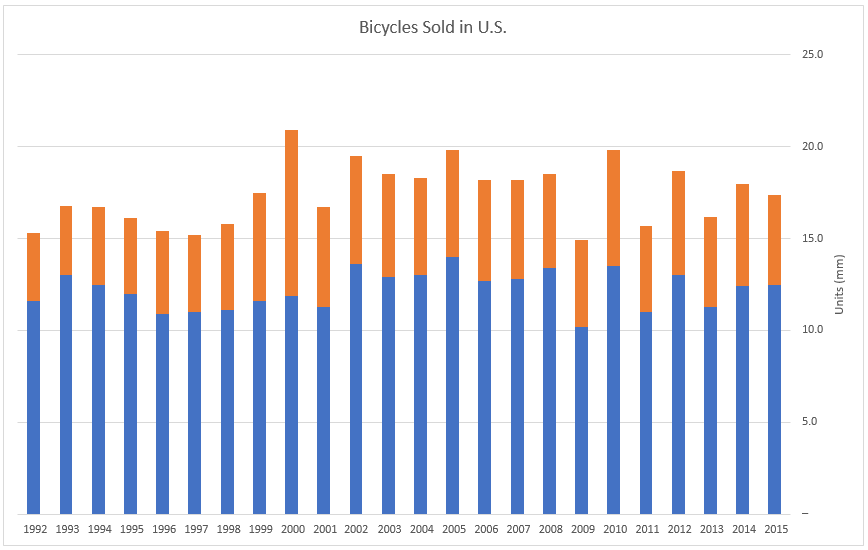

Bicycle sales are impacted by the economic cycle and, potentially even more so, adverse weather conditions. The chart below depicts the volatility in the U.S. The blue signifies bicycle sizes of 20 inches or greater (adult-size), and the orange is less than 20 inches. Units were down significantly in 2001 and 2009 due to recession, and again in 2013 due to poor weather. It should be noted that the data does not reflect actual sell-through as this data would be nearly impossible to compile. Instead, it measures bicycle imports and domestic production. Nearly all bikes sold in the U.S. are manufactured outside of the country.

While units have been relatively stable, the U.S. population has grown from 255 million to 320 million people over this period. According to the National Sporting Goods Association, peak participation in bicycle riding was in 1995 when 56.3 million people aged 7 or older claimed to have ridden a bike six or more times that year. In 2015 only 36 million people claimed to have ridden six or more times. Gluskin Townley analyzed the NSGA data from 2000 to 2010 and offered the following conclusions.

-

Participation among children (ages 7-17) declined dramatically (-21%) over the period. This trend likely has continued unabated as kids have become increasingly glued to other forms of entertainment (phones). However, we believe this pressure is likely to subside with the penetration of smartphones among teens nearing peak levels. In fact, it’s possible there could be some pent up demand for bicycles used for exercise since our young people are much fatter than they were 20-30 years ago.

-

Adult bike riders offset this to a degree, rising 2%.

-

Of adults, women ridership declined and was more than offset by men.

-

Enthusiasts have increased substantially over the decade (+12%). This is a positive for manufacturers as enthusiasts spend significantly more than the casual rider.

Bicycle sales in Europe appear more stable, although clearly are still subject to economic conditions.

Despite the cyclicality of the industry, Dorel Sports performed very well over the last decade, until recently that is. In 2009, sales declined just 3.4% organically. Sales declined just 2% organically in 2013 during tough weather, and rose double-digits in the early 2010s and in 2014 before moderating in 2015. Reported sales fell 5% in 2015, primarily due to the massive depreciation of the Brazilian Real. In 2013, Dorel acquired Caloi, South America’s largest bike manufacturer. The deal seemed to make sense at the time. Dorel had experience operating in many South American countries with its Juvenile business, and of course was very familiar with the bicycle industry. Unfortunately, the timing was terrible. Brazil’s economy fell off a cliff after oil prices crashed in late 2014, and the Real depreciated along with it. Caloi’s sales, which are required by Brazilian regulations to be disclosed separately, declined 26% to $91 million in 2015. But, using average FX rates disclosed in the annual report, local currency revenue actually increased.

In contrast, Ex-Caloi sales declined 2% in 2015, but margins fell precipitously, down 250 basis points to 4%. This is partially due to the depreciation of the Euro. The average Euro in 2015 was over 17% lower than 2014. However, manufacturing costs in the Far East are almost entirely in USD. Dorel would have had to push through materially pricing actions in short order. Sports’ sales declined 8.4% organically in 2016 and in the first two quarters of 2017 are down 9.9% and 13.4%, respectively. This has translated into a significant decline in margins.

The weakness experienced in 2016 was surprising to the management team. Dorel claimed the North American IBD industry was massively oversupplied going into the 2016 selling season, which unsurprisingly led to heavy discounting. Management cited BPSA data that showed suppliers had 40% more inventory in January than in the prior year. Management noted on the Q216 call that it had no idea why this happened, and added that Dorel did not order nearly as much inventory as competitors did. We analyzed Shimano, the top supplier of bicycle components like gears and derailleurs. Shimano’s financials appear to confirm the oversupplied thesis. From Q314 through Q215, the period when manufacturers would likely be buying, Shimano’s bike part sales were up anywhere from 25-35%. They have since tumbled (down double-digits through 2016), but the decline has stabilized to low single digits so far in 2017. This is hopefully indicative of low industry-wide inventories. In Q316, Dorel’s management claimed that supplier inventories were down 20% compared to the prior year.

Management believes the early season discounting caused by the oversupply situation caused IBDs to change their buying habits. Historically, manufacturers would ship about half of a retailer’s commitment in the third and fourth quarters for the following year’s selling season. This pre-buying occurred at the end of 2015, but clearing the supply situation did not result in the same pre-buys in late 2016. Instead, retailers are taking a wait and see approach, which seems to make sense given the weather-driven nature of the business and propensity of suppliers to discount to clear inventory if required.

The supposed shift in buying habits did not translate to improved sales in the first half of 2017. Adjusted organic sales were down 10% in the first quarter, which management blamed on poor weather in March and a later Easter that impacted both CSG and mass sales. The company added that retailers are still reducing inventory. In North America, the retail store base continues to shrink. Management noted that comps at brick and mortar store were down, but online sales are growing. On a positive note, gross margins improved significantly due to fewer discounts. Gross margin, after adjusting for an accounting change to make the comparison apples to apples, was 24.6% in the first quarter, which is in line with historical peak levels experienced in the early 2010s.

At the end of the first quarter, the inventory setup seemed somewhat favorable for the remainder of the year. However, the second quarter surprised to the downside again. Adjusted comps were even worse at -13.4%. While profitability improved year over year, it was still well below the first quarter. Management blamed the weather again, adding that mass was impacted as well. In fact, the company noted that the weakness has continued into the third quarter, especially at mass. Mass is not likely to recover as purchases this late in the season might just be deferred. While management was downbeat on Q3, it expects a rebound in Q4 and a strong performance in 2018.

We believe management’s reasons for recent weakness are legitimate and also expect a rebound next year. Management believes the 2016 NBDA data will show a significant drop in bike sales. Historically, strong years have followed weak ones. Furthermore, Cannondale has introduced an updated version of its most popular road bike for 2018 that has gotten rave reviews like this from road.cc: “Cannondale Synapse 2018 First Ride - has Cannondale made the best endurance bike yet?” Numerous cycling websites are singing its praises. The 2016 annual report stated that CSG was the only Sports group reporting a decline in earnings in the fiscal year. Based on the ex-Caloi financials, Cannondales’s performance must have been quite poor. We see no reason why the group cannot return to historical profitability, which is in line with what European competitor Accell is currently reporting. Furthermore, the company has instituted price increases in Europe to offset the currency pressure, and the Euro is moving in a favorable direction, which should help margins improve to historical levels. The Real is also slowly moving in the right direction.

In the trailing-twelve-month period, Dorel Sports generated $909 million in sales and $38 million in adjusted operating income with a 4.2% margin. Profitability has improved solidly from 2016. We believe the firm is set up well to realize a material increase in sales and earnings. Sales will likely recover to $950 million. Prior to the recent downturn, historical gross margins ranged from 23 to 25%. The acquisition of Caloi would have boosted gross margins, all else equal, because the firm owns its own manufacturing facilities in Brazil. The high-end of the range should be close to normalized levels, but we need to subtract about 1% due to a change in accounting that occurred in Q316. So far this year, Sports posted 23% or higher gross margins in both quarters, despite the sales slowdown and accounting change. Management noted on the first quarter call that gross margins would have been 24.6% using the old accounting. A 24% normalized assumption seems reasonable. SG&A+R&D should get some positive leverage on higher sales. It’s at 18.1% now, and we assume it returns to 17.5%. The implied dollar amount is not lower than the TTM period, and is similar to 2016 levels. The resulting EBIT is $62 million. This is less than 2012 (before buying Caloi) and 2014 (after Caloi).

There are a number of solid data points with which to value the Sports segment, starting with the recent takeover attempt of Accell Group (ticker: ACCEL EU) by private competitor Pon Holdings. Both companies own lesser known, but mostly-higher end, brands that articles claim are very popular with enthusiasts. Pon owns Cervelo and Santa Cruz, for example, while Accell owns Diamondback and Raleigh. Accell generated EUR1.05 billion in revenues last year. A Fortune article states combined sales would be about $2 billion, which implies Pon’s bike sales are about $750-800 million. In April 2017, Accell announced it had received a takeover offer from Pon for EUR32.72 per share, a 20% premium to the prior days share price and around a 40% premium to the stock’s trading range over the prior six or so months. Bloomberg pegged the deal price at just over EUR1 billion including EUR154 million in net debt. Revenue, EBIT, and EBITDA multiples were calculated to be 1x, 16x, and 14x, respectively. Using the adjusted EBIT provided by Accell’s management brings the multiple down to 15.3x.

Applying 1x sales and 15.3x EBIT to our normalized Dorel Sports sales and EBIT estimates gives values of $950 million and $945 million, respectively. Accell rejected Pon’s improved offer, stating it had insufficient support from shareholders. The shares are have traded back down to the pre-announcement price. Accell’s EV/2017E EBIT is 13x, according to Bloomberg. Dorel paid roughly 1x sales and 11x EBIT for both Pacific Cycles and Cannondale (after adjustments). We think 11x EBIT should be the absolute floor, but 12-13x is more realistic. This pegs the valuation range at $680-$800 million. If Dorel were broken up, we think the Cannondale business could be tucked into a larger competitor at at least 15x EBIT.

Dorel Home

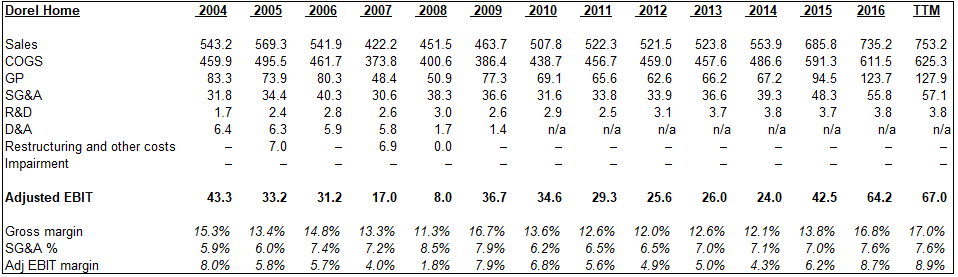

Dorel Home operates in the North American furniture industry. It is one of the top ten largest suppliers. Martin Schwartz and his brother-in-law Jeff Segel founded the genesis of the Home business in 1969 and eventually merged this business with Leo Schwartz’s Dorel. Like Juvenile and Sports, the business has engaged in M&A, but much of the segment’s growth has been organic. The business generated $735 million in revenue in 2016 (28% of total) and has higher than average operating margins.

Home manufactures baby mattresses and futons, and also sources wood and upholstered furniture from Asia, including sofas, dining room furniture, bedroom furniture, and baby cribs. Products are sold by most major retailers including Amazon, buybuy BABY, Overstock, Sam’s, Target, Wal-Mart, and Wayfair. The Cosco brand is well-recognized for step stools, ladders, and hand trucks, but the business also makes indoor furniture such as folding chairs and tables, and outdoor furniture, including full patio sets. Cosco products are sold at some of the retailers stated above, in addition to hardware stores. Lastly, the Ameriwood division manufactures ready-to-assemble (RTA) furniture. A standard RTA piece is a simple bookshelf that is packaged in a flat box and is assembled by the purchaser at home. Dorel is the second largest maker of RTA furniture in North America. Last year, 47% of the segment’s sales were to a “major customer,” (i.e. WMT). This is down substantially from five years ago as the business has grown through e-commerce.

While Dorel Home’s business lines appear mostly homogenous, the demand drivers can be very different. Demand for outdoor living furniture is probably very correlated with new and existing home sales and general economic activity/consumer confidence. On the other hand, ready-to-assemble furniture is typically the cheapest you can get and costs a fraction of its fully assembled counterpart. RTA is less economically sensitive due its needs-based nature and potential for higher income customers to shift to value-priced goods during economic contractions. The company no longer discloses revenues by product line, but we believe RTA could contribute about half of the segment’s revenue.

The RTA industry came under extreme pressure in the mid-2000s that lasted for several years. Multiple factors contributed to the weakness. Particle board prices rose significantly due to supplier issues, including a fire in 2006 at one of the industry’s largest suppliers. RTA manufacturers had trouble maintaining inventory levels sufficient enough to fulfill customer orders. Additionally, competition from the Far East heated up. Producing wood RTA furniture in Asia is not cost effective due to the low value and high weight of the finished product. Labor is a smaller component of COGS than it is for other furniture. This is a competitive advantage for domestic manufacturers. However, Asian competitors were able to take share by producing cheap alternatives with glass and metal instead, making them cost competitive with wood RTA furniture. Dorel’s RTA sales were down 17% and 15% in 2005 and 2006, and were down further in 2007 by an undisclosed amount. Two of the four large RTA players, Bush and O’Sullivan, exited the business during this time. O’Sullivan went bankrupt in 2005, and its intangibles were purchased by industry leader Sauder. An article claimed Sauder had $550 million in sales at the time. O’Sullivan had $250 million in sales in the twelve months ended June 30, 2005, according to the bankruptcy disclosure statement. O’Sullivan’s bankruptcy filings included the following passages.

“In recent years, sales of imported RTA furniture have been increasing in the U.S., a trend that the Debtors anticipate will continue.”

“Several manufacturers, including the Debtors, have excess manufacturing capacity due to the current decline in sales in the RTA furniture market and increasing imports. This excess capacity has caused increased price competition.”

“The Debtors have been and continue to be negatively impacted by increased competition within their industry, including foreign competition. In addition, consumer demand for RTA furniture has waned in recent years. Furthermore, as described above, the costs of particleboard and fiberboard, the primary raw materials used in the Debtors’ products, increased significantly in 2004 and have not fallen materially since.”

Total segment sales actually not as bad as one might expect, with revenues up 5% in 2005, and down 5% and 12% in 2006 and 2007, but it’s tough to compare because around $50 million in sales were shifted from Home to Juvenile in 2009. The top line rose 2.1% and 2.7% in 2008 and 2009, although the results were admittedly off a low base. Profitability improved substantially before waning and leveling off from 2011 to 2014. Gross margins were historically low during this period. This is partially due to historically strong CAD exchange rates, which broke parity for most of 2011. Dorel Home has manufacturing facilities in Canada. Revenue and operating margins were basically flat from 2011 through 2014.

Home has been killing it over the last 10 quarters or so, and the sellside seems to be giving them little credit for the improvement. All of the focus seems to be on Sports and Juvenile. The primary contributor to the improvement is significant growth of the e-commerce business. In 2013, the firm disclosed that online sales had grown to 20% of segment sales. In 2016, 45% of sales were from online orders. This is more than a tripling in online sales, from about $100 million to $330 million. Dorel shipped two million orders directly to customers last year. This growth has more than offset brick and mortar weakness. The top line rose 6%, 16%, and 7% in the last three years. The growth has reduced Home’s percentage of sales to Wal-Mart.

The segment has enjoyed significant margin expansion as sales have grown. One result of the opening of the online channel is that brick and mortar shelf space is no longer a limiting factor. E-commerce has allowed Dorel to expand its offerings to higher-price point products that might have smaller production runs, and therefore would not have been carried by a retailer. Additionally, the steady weakening of the Canadian Dollar has translated into improved profitability. Gross margins have risen from 12.3% on average from 2011 to 2014, to 16.8% in 2016 and 17.8% in the first half of 2017. G&A has increased faster than revenues due to the higher opex requirements in fulfilling online orders, but operating margins have still risen dramatically. Home is sporting the highest operating margins since before the particle board shortages and foreign competition of the mid-2000s.

The industry has obviously been through some difficult periods. We are somewhat comforted by the fact that the Schwartz brothers have worked in this business for nearly their entire adult lives, but that doesn’t make valuing it any easier. The segment is clearly cyclical, although as stated earlier is probably less so than a higher-priced furniture business. Sales were down much less than one would have expected during the bursting of the housing bubble, and this was one top of the industry-specific issues the RTA business was experiencing. Dorel deserves some credit for the e-commerce expansion, but how much? CEO Schwartz had this to say on the last conference call.

A - Martin Schwartz>: It's almost the hardest one to - even though the numbers are so consistent, it's almost for me the hardest one to project because it's a bit of blue sky. We're riding this Internet wave of customers that are selling more and more home furnishing goods and we are clearly one of the top suppliers to that channel. So, it's hard to judge how much our customers are going to grow. It's all double-digits for them and we're trying to keep up on that part. You don't see it as much in our top-line because we are losing as the market is losing share of bricks and mortar. So, when we increase, we're increasing double-digits our business to our e-commerce customers, but the bricks and mortars are shrinking and so are we. So, you end up with probably a high single-digit growth rate for Dorel, but the growing probably a high single-digit. Growth rate for Dorel, but the growing segment is growing really fast. So it's really difficult, we do have a little bit of higher cost here and there, but that gets eliminated by just the leverage that we have in our business and we continue to be more efficient in our expediting the products and investing in technology to help us get it to our customers faster. So it's just difficult, because I don't know where all this is going other than we know it's going up.

Q - Stephen MacLeod>: Yeah. Okay. But you - with that mix of business, you would expect margins to continue to tick higher incrementally I would expect?

<A - Martin Schwartz>: Yeah. I mean, what's going to stop it, if there is a significant rise in commodities, and again that whole idea - and even this time to be honest with you, we've had a historical timeline of what happens when prices - costs go up and how long does it take in brick-and-mortar to get the increase back to us, but we haven't really seen that online. So I can't tell you how long the lull is between us receiving cost increases and us implementing them online. So again it's new area for us, it's difficult to answer that.

<Q - Stephen MacLeod>: Yeah.

<A - Martin Schwartz>: But if there is no major increases, there is always ups and downs, yeah, I do see margins picking up.

Even though the trajectory is still higher, the risk at this point in the cycle is applying too much credit to recent performance. Let’s assume we are at the top right now. With trailing-twelve-month sales at $750 million, we model a peak-to-trough decline of 30%, which is considerably larger than the 2005-2007 decline of 17% due to more exposure to higher price point (and perhaps more discretionary) products. The mid-point normalized sales level would be $640 million. TTM margins are 9% and are expected to continue rising. We give credit for some of the structural shift in the business to online. Perhaps the normalized margin was 5% through the last cycle (this is the average of the relatively “normal” years of 2011-2014). An incremental 100 basis points on the full-cycle margin appears realistic, particularly when comparing the current margin to past peaks. This equates to $38 million in full-cycle average operating earnings.

Despite the exceptional performance of late, Dorel Home deserves a lower multiple than the other businesses. While it is the second largest RTA manufacturer on the continent, this is still a highly commoditized business. Further, Home does nearly all of its sales in the U.S. where the corporate tax rate is higher than most foreign jurisdictions. We feel 9x EBIT is a conservative full-cycle valuation. The closest peer is probably La-Z-Boy (ticker: LZB), which is currently trading at 8.5x all-time high operating income. The stock has traded at a lower multiple since 2015 even as earnings continued to ramp. During the period we claim was somewhat normalized for Dorel (2011-2014), LZB traded in a range around 12x EBIT. Valuing Home’s normalized EBIT at 9x equates to $342 million. Note that the segment should require less working capital at mid-cycle, and the difference should be added to the valuation, but it would not be very meaningful.

Financials

Dorel has grown significantly over the past two decades due to its M&A strategy. Sales have grown from $426 million in 1996 to over $2.6 billion last year. There have been several accounting reclassifications over the years. These reclassifications include:

-

Reallocation of about 40% of depreciation from single line item to COGS in 2009.

-

Changed from Canadian GAAP to IFRS in 2011: While the bottom line impact was minimal, this resulted in a reallocation of expenses among line items, primarily the treatment of R&D. The D&A line item was removed from the income statement, and some of amortization of internally developed intangibles was moved into R&D. Additionally, SG&A was split into G&A and selling. COGS was also impacted slightly. Full details of the IFRS impact is found in footnote 29 in the 2011 annual report.

-

Changed accounting for remeasurement of forward purchase agreements in 2014. Dorel has acquired majority stakes in businesses and agreed to repurchase the remaining stakes at later dates based on certain criteria. Changes in the inputs for these liabilities had been run through G&A. The impact to operating income has been large at times (ex. $12 million boost in 2011). Going forward, reported operating income will be cleaner, but finance expense may not represent cash interest expense at all.

A few things about Dorel’s financials are immediately obvious. First, the business was pretty damn stable and quite profitable through 2010. Excluding the Pacific Cycle purchase, which was done nearly at the beginning of 2004, this period was devoid of M&A until early 2008 when Cannondale was purchased. The wheels started to fall off in 2011. The firm has taken extensive restructuring and impairment charges over the last three years. While waning sales and materially lower profitability are certainly unwelcome, operating income has been mostly stable after the step-down that occurred in 2013. It is important to be aware that Dorel has spent roughly $295 million in cash on M&A since 2011, and even more if you consider the “real” purchase price of Caloi including the forward purchase agreement and debt.

Cash Flow

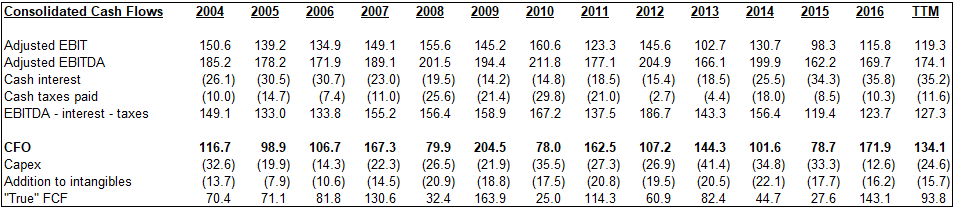

Dorel has generated significant cash flow over the years. EBITDA less cash taxes and interest has been fairly close to CFO before changes in working capital. Cash taxes have been lower than the Canadian corporate rate due to business done in lower tax rate foreign jurisdictions and net operating loss carryforwards. However, changes in working capital, in particular swings in inventories, have caused Dorel’s cash flow production to be very volatile. The volatility is not overly concerning. Dorel has historically been able to whittle down inventories after tough periods, such as what Sports has experienced over the last few years. In fact, Dorel generated its highest CFO in seven years in 2016. The only higher year in our study period was during the credit crisis in 2009 when the company produced $205 million in CFO.

Despite the variable working capital needs of the business, Dorel has not experienced a negative free cash flow year since 2004. Over the period, “true” free cash flow has totaled $1.05 billion at an average of $81 million per year, but the range is wide, from $25 million up to $164 million. Again, this is mostly explained by working capital needs. We show “true” FCF in the table above because the standard definition of FCF differs from what the company reports in the annual reports. The company includes dividend spending and stock buybacks, so the reported FCF has been negative on a few occasions. We also include spending on intangibles in the free cash flow calculation, as does the company. Under IFRS, some R&D can be capitalized when it qualifies as development spending instead of research spending. The addition to intangibles line item is mostly made up of internally-developed intangibles. These intangibles are amortized over a 2-5 year period. The company stopped disclosing what portion of R&D expense is cash each period, but one can back into rough figures using disclosed amortization. Total cash spending on R&D has consistently been 1.3-1.7% of revenues. Some $360 million has been spent in the last ten years. Capital spending has also been mostly consistent, averaging 1.2% per year, although capex last year appears abnormally light at just 50 bps. Spending has picked up to more normalized levels in 2017.

Debt

Dorel has operated with debt for most of its existence. The company has funded most of its large acquisitions with debt financing, beginning in 2000 with the purchase of Safety 1st. It has occasionally used equity. The capital structure was cleaned up in March of this year. Dorel secured a new $200 million term loan that it used to retire high-cost Brazilian debt and two series of guaranteed notes. Additionally, the revolver was amended and extended. The availability was reduced from $435 million to $350 million. Most of the reduced availability was shifted to the accordion feature. The company only provides a detailed breakdown of the debt in the annual report, so the table below is an estimate of what the debt structure looks like as of June 30, 2017.

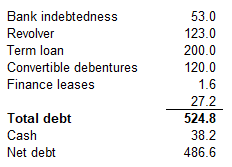

The revolver and term loan mature on July 1, 2020, but the maturity date springs forward to May 30, 2019 if the convertible notes have not been refinanced by this date, which is six months prior to the notes’ maturity. This would allow the bank lenders to control any restructuring, if necessary. The new term loan requires quarterly principal payments of $2.5 million, increasing to $3.75 million in July 2018 and $5 million beginning in July 2019 if the maturity has been extended to 2020. Additionally, 50% of excess cash flow must be used to repay loan principal if the leverage ratio is above 2.5x. The calculation of debt in the leverage ratio excludes the convertible bonds, presumably because they are payable with stock. However, it includes forward purchase agreements to buy remaining stakes in several businesses (primarily about $23 million for Silfa Group due in 2020), and also includes guarantees that are primarily letters of credit.

Using the face value of the converts, trailing-twelve-month net leverage is 2.8x. Cash interest coverage is 3.4x. This should improve due to the refinancing, which management believes will reduce interest expense by $4 million annually. While the ratios are on the worse end historically, we have confidence in the management team’s willingness and ability to maintain a responsible capital structure. The management team has proven that it is willing to delever after using debt financing for acquisitions. It did so after Pacific in 2004, Cannondale in 2008, and now Caloi/Lerado in 2013 and 2014. Furthermore, Dorel has not used debt to repurchase stock or pay a special dividend. It is also important to keep in mind that both the Juvenile and Sports segments have struggled recently. We expect this to change, particularly in Sports, which will reduce leverage. You wouldn’t know it by just looking at the leverage ratios over the past few years, but management has reduced debt by over $100 million since the end of 2014, while continuing to invest in the company and pay a sizeable dividend. The management team members’ tenures and ages also make it unlikely they would put the company in a precarious financial situation (see management section below). Management’s primary use of cash, after funding the dividend, is to pay down debt. It expects to be below 2x levered by the end of the year, using the credit facility definition of debt, which excludes the converts.

The 5.5% convertible notes were issued in late 2014 to finance the purchase of Lerado. The issue size was originally to be $105 million, but it was upsized to $120 million shortly after issuance. The notes are unsecured and subordinated. They are callable at par on November 30, 2018. Like most converts, there are few covenants, but there are several key features worth noting.

Convertible option: The bonds are convertible into 21.3904 Class B shares (1/10 of the voting control of Class A), which is a conversion price of $46.75 per share. The shares have not traded above $40 per share since the deal was launched. The conversion price will be adjusted for equity issuances and dividends greater than 30 cents per quarter. Dorel has paid the maximum dividend allowable since mid-2013.

Coupons and principal payments: If no default has occurred, the company has the option to issue shares to pay the coupon. The shares will be issued to the Trustee, which will sell the shares into the market and deliver cash to bondholders equal to the interest owed. Additionally, assuming no default, the company can issue shares to repay principal at a 5% discount to the share price.

Change of control: The company must make a par offer to repurchase the notes if a change of control occurs, except a management buyout by the Schwartz family (and brother-in-law) are excluded from this requirement. In certain circumstances, the bond conversion rate is increased to compensate holders for lost time value.

Management

Dorel was founded in 1962 by CEO Schwartz’s father, Leo Schwartz. In 1969, Martin Schwartz founded ready-to-assemble furniture manufacturer Ridgewood Industries with his brother Alan Schwartz and brother-in-law Jeff Segel. The two companies merged in the 1980s and completed an IPO in 1987. Jeffrey Schwartz joined the firm in 1989. Leo is deceased, but the three brothers and Jeff Segel hold four of Dorel’s nine board seats.

The Schwartz brothers and Jeff Segel each own a little more than 18% of the Class A shares, which have 10x the votes of the Class B shares. Leo’s wife Laura, who died in April, owned 16% of the Class A shares, leaving 11% owned by others. The Schwartz’s Class A stake (including Segel and Laura) holds about 55% of the voting control. It is unclear who Laura’s stake is now held by. Without Laura’s Class A shares, the four executives would lose voting control. The family also owns over 2 million Class B shares out of a total share count of 28.2 million. The Schwartz’s are getting up there in age, have worked at Dorel for essentially their entire adult lives, and have significant financial stakes in the company.

We believe there is an above-average chance of a breakup or sale, especially now that the patriarch’s wife has passed away. Martin entertained the idea several years ago in an interview with the Globe and Mail, saying, “If someone comes with the right deal, we'd definitely look,”… “For me to say, 'No, we'd never sell,' I'd be lying to you.” He added later in the article, “I haven't put a date to anything.” It’s also worth noting that four of the five independent directors have stakes valued more than CAD 1 million each, and one owns 5mm of the convert.

Equity and Convertible Bond

The 5.5% convertible bonds are unrated, convertible, issued in Canada, and have only $120 million outstanding. They are invisible to most investors. The bonds trade in small size regularly on the Toronto exchange, and a few blocks have printed on TRACE over the last couple of months. The notes are available to purchase for all Canadian investors, but U.S. investors must be Qualified Institutional Buyers. The next par call is in November 2018, to which the yield is 3.6%. The yield-to-maturity in November 2019 is 4.5%. The ML 1-5 year B-BB index yields 4.1% to worst and 4.7% to maturity, and this index is filled with distressed retailers, energy and telecom companies. We believe the Dorel bonds are quite attractive relative to the average index member, even if the convertible option is worth little to nothing.

To conclude the equity valuation, we deduct $200 million from the valuation to account for corporate overheard (CAD 30/year, 26% tax rate, 9% discount rate, 1.238 CAD/USD) and $26 million for the after-tax value of underfunded retirement liabilities. We think the shares are fairly-priced using conservative assumptions. The company would be worth significantly more if broken up and sold. Not only would each segment likely receive a higher multiple than we are assigning, but strategic acquirers could easily cut most if not all of the corporate overhead. Removing the overhead alone bumps up the valuation by 25%. An extra turn on each segment’s multiple would add another $4.5 per share. It’s not a question of if Dorel is broken up, but when. In the 2012 Globe and Mail article, CEO Schwartz declared, “there’s no family succession” plan. He added, “We manage the company as a group, the four of us, the family. We're in together, we're out together.”

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

Family relinquishes control and/or decides to sell the company

Sports business improves as weather normalizes

Operational improvement at Chinese manufacturing facilities pushes Juvenile margins in line with peers

| show sort by |