| 2019 | 2020 | ||||||

| Price: | 7.58 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 149 | P/E | 7 (5.7 normalized) | 0 | |||

| Market Cap (in $M): | 1,384 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | -290 | EBIT | 0 | 0 | |||

| TEV (in $M): | 1,094 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

Description

For those that have written / read the previous VIC write-ups on DTG, please skip to our competitive statistics work below. We hope it is as surprising to you as it was to us*. The write-up might be too much of a review, we tried to be comprehensive in sharing why we believe Dart Group is great.

*Key findings: many monopolistic routes, low overlap with Easyjet, cheapest package provider and airline on its routes.

Owner operated vertically integrated LCC/package provider with leading ROCE and at 30-50% valuation of peers (RYA, EZJ, TUI, ALGT)

As widely covered in investment circles, the internet is a game-changer for the airline industry as customers typically book airline tickets first when planning a holiday. This enables upselling of adjacent products (hotels, cars, insurance etc.) when customers are still “in the market” for these. Because of the consolidated nature of the airline industry, the Bookings.com’s have failed to break into online airline reservations. Instead, airlines themselves own the online customer touchpoint.

How can airlines convince customers to book other products and earn asset-light earning streams?

Customer purchasing habits are formed through a combination of customer satisfaction and frequency of purchase. We believe Dart Group’s airline Jet2 is well-positioned:

-

Great reputation/high customer satisfaction evidenced by a consistent place in TripAdvisor’s Top 10 Global Airlines (quite a feat for a low-cost airline, i.e. the only LCC airline in that list except for Southwest Airlines), highest Feefo customer reviews amongst peers in UK, best social media traction

-

Frequency of purchase: Many customers don’t even have a choice: Jet2’s long-standing dominance on many of its routes at smaller local Northern UK airports naturally means a higher frequency of purchase for customers wishing to go to their favourite destinations.

This is how Dart’s nascent package holiday business Jet2Holidays managed to become the UK’s second largest player in 10 years time. It also explains why Ryanair and Wizz Air have tried to start a package holiday business and failed twice. Both recently announced they would kill these initiatives.

On the other hand, legacy package operators (TUI, Thomas Cook) did not provide booking date flexibility soon enough which “always wonderfully dissatisfied customers” now demand in the age of online travel booking.

Of course, owning an LCC airline with a mix of flight-only customers helps in efficiently offering more flexible flying dates. Bundling low marginal cost delighters such as Jet2’s “free 22 kg luggage” for every package customer is another benefit of owning aircrafts. Conversely, being able to capture all the economics from marketing package holidays to airline-only customers on the plane is another efficiency. Lastly, a memorable package holiday engenders more loyalty (repeat business) than a “memorable flight” (if such a thing exists at all), closing the circular yet virtuous loop (as discussed, customer perception is important in the first place to convince an airline customer to book a package).

A package holiday business has several advantages for airlines:

-

Asset-light earning stream

-

Less volatile profits

-

profit margins on package holiday revenue are relatively fixed, unlike airline business which is a high fixed-cost business

-

more loyal, repeat passengers in the aircraft

-

Larger customer “float” (i.e. interest-free customer cash advances) vs airline tickets

-

Amount: paying a package is 660 GBP while an airline ticket is 60 GBP

-

Earlier: leisure customer books more in advance, especially package holiday customers (more risk averse)

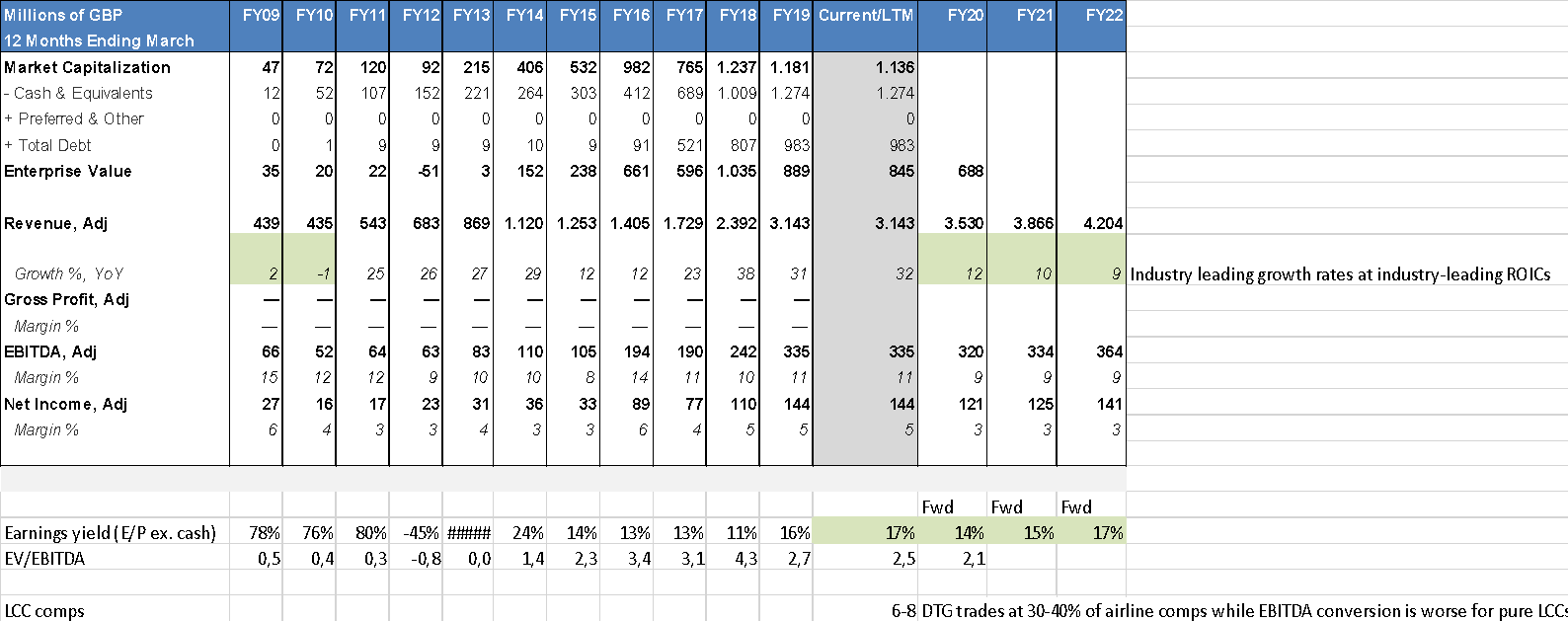

DTG is currently valued at 5,7x P/E ex. cash – roughly half of other LCC’s - while only 43% of revenue is from the airline (i.e. even counting airline tickets embedded in packages). 51% of revenue is from the package holiday segment (ex. tickets) and another 6% a legacy chilled food distribution operation.

Alternatively, 50% of Jet2’s aircraft passengers are package holiday customers, i.e. a more loyal customer base with less volatile asset light margins on top of this.

While buying a sustainable 20% net earnings yield stock should be fine without re-rating, we believe Dart deserves a multiple in line with (pure) low-cost airlines because of the attractive package holiday mix.

Business model

Jet2 is an owner-operated UK low-cost leisure airline and the UK’s second biggest package holiday provider. Like Ryanair in its infancy - and Allegiant in the US today - Jet2 has grown profitably by avoiding route competition and operating mostly older aircraft. These are bought cheaply and operated from local airport bases that on the one hand are seasonal and on the other have small catchment areas that do not support frequent service. The lower capital costs of these older aircraft more than offsets their low efficiency because of the low frequency of operation.

Shunning competition

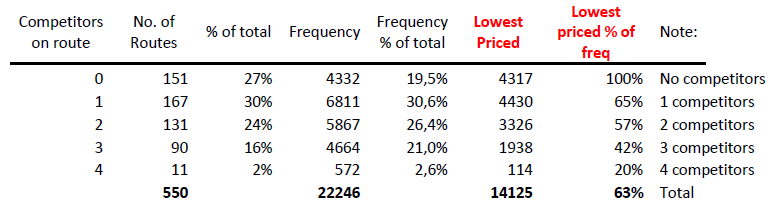

Jet2 dominates many routes that only support infrequent service. This is supported by our analysis of Civil Aviation Authority data (see figure below) which shows 27% of Jet2 routes has zero competitors. Another 30% and 24% of Jet2 routes only have 1 and 2 competitors respectively (i.e. this could be another day of the week or time of day). Weighted by Jet2 flying frequency, we found half of Jet2 routes has at most 1 competitor.

Most affordable packages and flights on its routes

Interestingly, for those that are skeptical of Jet2’s low-cost status, through Google Flights price screen scraping we found Jet2 to be the cheapest on the majority of routes it flies. Jet2 prices were compared with RYA, WIZZ, EZJ, Thomas Cook, TUI. While the below average 63% figure includes monopolistic routes, this figure remains 55% when excluding them. Note that RYA and WIZZ sell an inferior ticket without 10 kg cabin luggage. Note also that Jefferies did a similar scraping exercise for package holiday prices and came to the same conclusion of Jet2 being most affordable compared to Thomas Cook and TUI.

Figure 1 How many competitors does Jet2 have on its routes? Analysis based on Civil Aviation Authority "CAA" airport data.

Note that Dart’s business model of operating only old aircraft is not scalable: Mr. Meeson adds value by opportunistically buying aircraft (e.g. bankruptcies). This is a skill that cannot easily be scaled or transferred. In the future, Mr. Meeson will have to focus more on “market timing” large new aircraft orders, as we will discuss below.

Adapting

Jet2 successfully grew its airline and its integrated package holiday business: from the start in 2007 to ~50% of airline passengers since a few years. As Jet2’s popularity grew, this came with increased frequency on many routes. Increased airline frequency and hence flexibility for clients is a differentiator versus legacy tour operators. It also supports an investment in more efficient aircraft: in late 2015, Jet2 ordered 27 Boeing 737-800NG (later increased to 34 planes). The listing price for 34 737NG’s was a scary 3 B$ while DTG’s operating profit was only 50 M£ at the time. However, we estimate Jet2 got a 52-55% discount from Boeing. Two factors contributed to this large discount:

-

the oil price crash caused a slump in demand for BA/AIR new orders

-

the 737NG could be had at unusually high late production “end-of-line” discounts (just before the current 737 MAX went into production)

In the 2016-2018 period, when these 34 new aircrafts were to be delivered, the stock market got worried because of a scary cocktail of

-

Brexit’s associated weaker consumer confidence, and potential jeopardy of UK-EU flying rights

-

the impending debt load

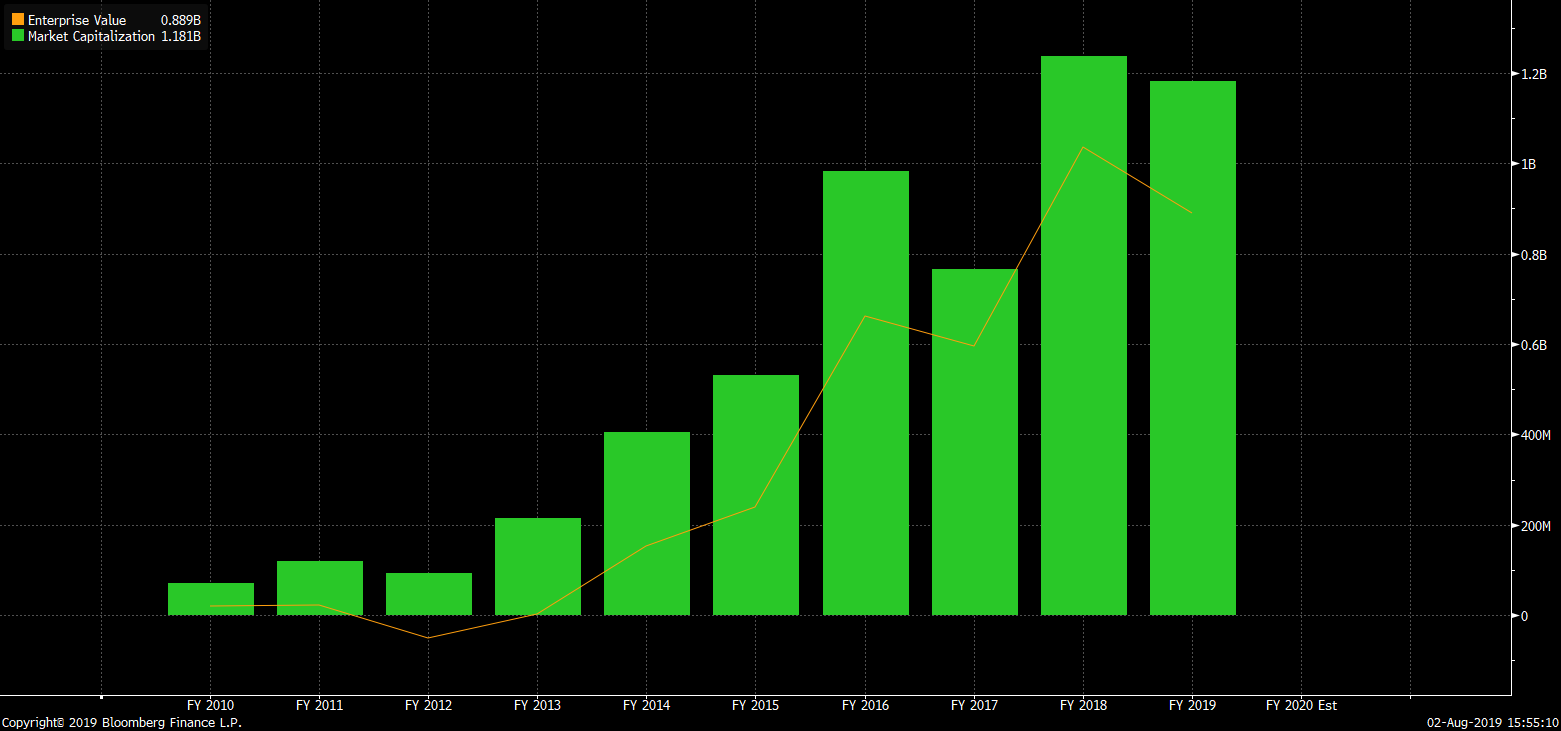

DTG’s stock bottomed at a 500M£ market cap (and a 1X EV/EBITDA valuation).

Meanwhile, Jet2 took action to grow and flatten its high seasonality and make sure aircraft utilization for the new aircraft would be high:

-

enter larger and less seasonal airports (London Stansted, Birmingham)

-

heavily market ski holidays and city trips (TV, newspapers, London tube)

Peak-to-trough month passenger capacity seasonality fell from 6-to-1 to 4-to-1 in the last 3 years. Revenue tripled while load factors and the mix of package holiday customers only increased. By the end of 2018, competitor Monarch went bankrupt, and Thomas Cook is fighting for survival today.

Note DTG receives customer advance payments “float” earlier compared to airline competition because it

-

is solely a leisure airline (these customers tend to book further in advance)

-

sells package holidays (larger, earlier)

-

is friendly with high street independent travel agents (another segment that books earlier)

In terms of business proposition to customers, Jet2’s core is family friendly and value for money. Jet2 spends a lot of time on details to improve customer experience. Examples are customer helpers at check-in and “resort flight check-in”. The latter allows customers to check-in bags for return flight at their hotel, giving them a hassle-free day without a bag. This service is available at 250+ hotels, while Thomas Cook has started replicating this at a few hotels recently.

Evidence

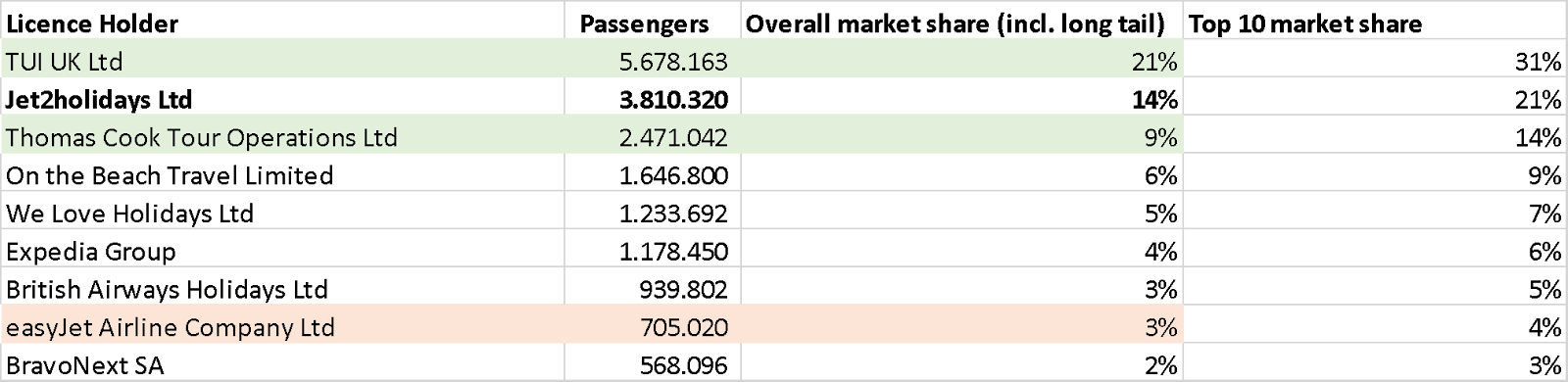

Jet2 has grown to the second biggest leisure company in 10 years. Two competitors that yielded most market share were legacy players TUI and Thomas Cook. While Jet2’s ambition is to become the largest player, Easyjet (like Ryanair and Wizz) has taken notice of this great success story and set up a competing Easyjet Holidays. While Ryanair and Wizz have failed twice and closed shop, Easyjet has tried and failed only once. Easyjet has a better chance of succeeding because of its attractive primary airport routes and overall reputation.

Figure 2 Market shares including/excluding long tail of smaller players.

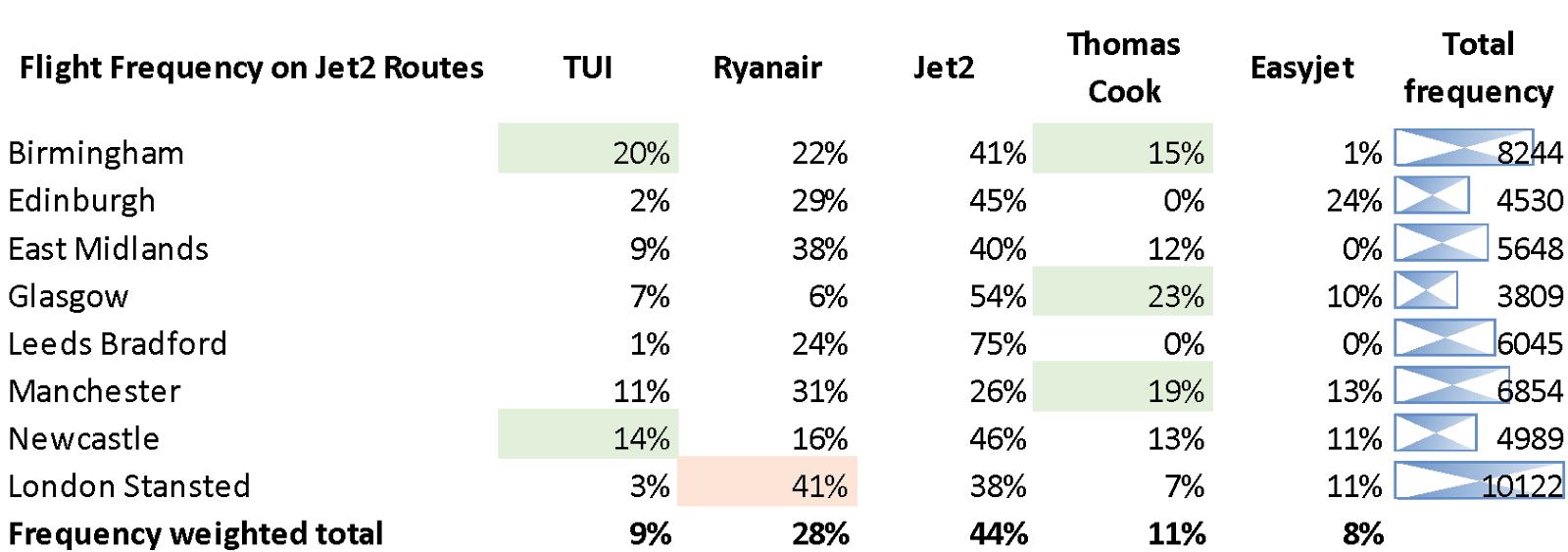

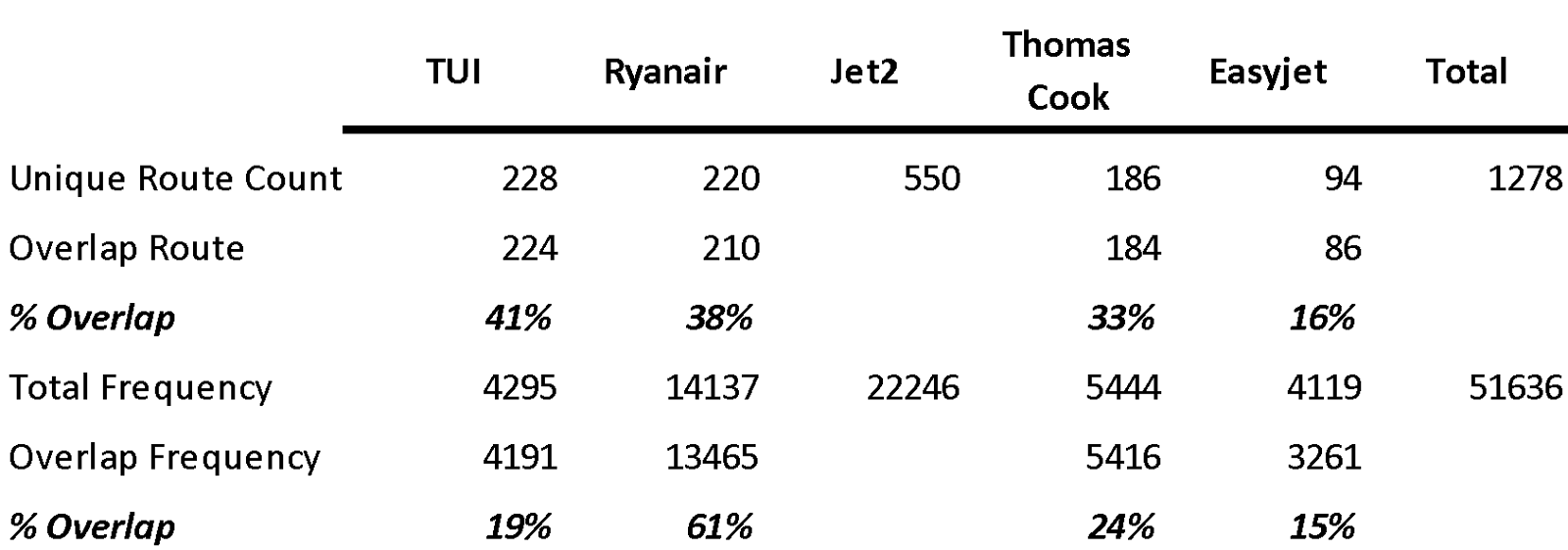

By analysing public Civil Aviation Authority filings, we found Jet2’s current overlap with competitors. We found the overlap with EasyJet is low (15%) and the overlap with competitors that are rather weaker “opportunities” is larger, i.e. Thomas Cook (24%) and TUI (19%). Manchester and Birmingham are probably attractive bases to expand for Jet2, with high legacy players shares. Jet2 only started operating in Birmingham and Stansted for 2 years as it expanded its fleet. Even if Easyjet were to succeed in rolling out package holidays in the UK (first market it will enter), Jet2 and Easyjet will probably co-exist and benefit from eating the legacy players’ lunch in the UK. Once that is finished, Easyjet has larger fish to fry as it plans to roll out packages across Europe. In addition, we believe DTG’s valuation more than offsets any Easyjet risk.

Figure 3 What is the frequency of competitor flights on Jet2 routes? Each line sums to 100%, i.e. each players frequency of operation on Jet2 routes for each Jet2 airport.

Figure 4 What is the overall frequency of competitors on Jet2 routes on a relative basis (rebased to Jet2 frequency)?

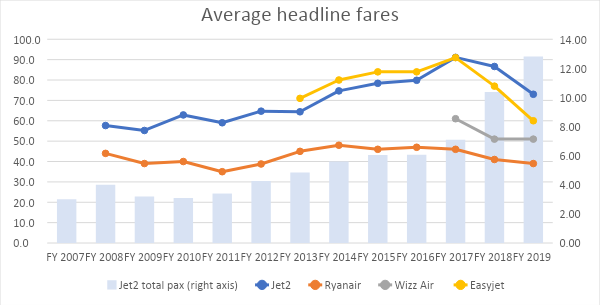

We also found evidence that package holidays insulate Jet2 somewhat from ticket-only price competition: DTG has maintained airline prices better, this was no easy trick given its

-

huge passenger growth to maintain in the last years (see figure on right axis)

-

tickets fall from a higher base (see comparable Easyjet)

-

mix of routes in this period shifted to somewhat shorter routes as (1) it opened a base in London Stansted and (2) share of ski holidays / city trips is growing

Figure 5 Jet2 prices have not come down as much as peers in recent years despite several factors suggesting otherwise.

Intelligent Fanatic: Executive Chairman Philip Meeson

An ex-RAF fighter jet pilot, Philip Meeson bought the company – then Channel Express – in 1983. In the early days, the company’s Dart Herald aircraft transported overnight mail and Jersey/Guernsey flowers to the UK mainland. On land, flowers were distributed to wholesale markets. This land business morphed into mainly chilled food logistics and distribution and is still part of DTG today, i.e. “Fowler-Welch” with ~5 MGBP in EBITDA. The company changed its name to Dart Group when it floated on the LSE in ‘91. Dart refers to the Dart Herald aircraft and the post-WWII Rolls-Royce Dart aircraft engine (Philip’s father was an RAF mechanic).

Meeson got this money originally by trading around 800 second-hand Citroen 2CV’s between Europe and London, and by founding an aerobatics team. Meeson won the British championship five times and got lucrative sponsorships from Marlboro.

People close to Meeson say he has a singular focus on running the business, checking last night’s bookings after waking up. While the low-cost airline Jet2 was only started in 2003 and Dart Group was an amalgamation of businesses, the stock has returned 90x investor’s money since 1989, compounding at 16% p.a. (excluding dividends). Management only talks to investors at the annual meeting, except for particularly large shareholders:

"To be successful in today's world you have to be really involved in a company."

We believe Meeson is smart, passionate and with relentless focus on detail. Meeson has a long track-record of meeting or exceeding expectations/guidance. Part of that is guidance conservatism.

Destination exposure

The most popular destination is Spain, accounting for about 1/3rd of travel, followed by Portugal, Greece, Turkey. Within Spain, Alicante, Mallorca and Tenerife are most popular.

Other destinations: Western Europe, Croatia, Hungary, Poland, USA (summer holiday/ ski/ city trip),.

Many of the most popular destinations top Mintel’s list of “affordable luxury” for Brits.

Valuation

As discussed, through both unwavering good execution and surely a deal of conservatism as well, management almost always meets or exceeds expectations. Note that DTG does not give conventional guidance in numbers, instead it comments whether the company will (typically) “meet” or “materially exceed” market expectations. Market expectations are based on Arden Partners, Jefferies and Canaccord Genuity. In its last update in July, management said it is confident it will meet profit expectations for the current year ending March 31st, 2020.

Because of this dynamic, and multiple industry comments that late summer bookings have since been strong, we will therefore anchor around the FY20 consensus number (FY20 = ending March ’20).

While the above explains why we think this is a conservative approach concerning the current year, the below explains why future estimates are probably on the conservative side as well.

Longer term, margins should benefit from scale and lower growth

Everything else equal, DTG’s future margin should benefit from increased scale as revenue has almost tripled (x2.7) in 4 years and DTG has borne upfront starting costs to expand to new bases (notably Stansted, Birmingham) and destinations that are now operational. The reported line “other operating charges” has ramped from 68MGBP in FY15 to 232MGBP in FY19 (x3,4). These costs are tied to new bases and a massive advertising campaign especially in London (Jet2’s has no historical presence in the South).

Part of this is expense growth was undoubtedly to support fast growth (mainly ad campaign). Without giving credit to any operational leverage, these expenses in steady state should probably not exceed revenue growth (x2.7), which implies a 40MGBP net income tailwind in the future.

Similarly, staff costs more than doubled (x2.2) showing some operational leverage. If we assume 5% of last years’ costs did not have a corresponding revenue base because of high revenue growth, this corresponds to a future margin tailwind of about 18MGBP.

Simplistically, everything else equal, margin at scale is probably around 5% (vs 4.6% last year)

Of course, everything else is not equal, as airlines and tour operators alike are experiencing increasing competitive landscape:

-

Monarch bankruptcy capacity tailwind is gone (a lot of share has been taken by DTG)

-

Fuel tailwinds in ’16 / ‘17 is finished

-

For the UK, GBP depreciation means mainland package pricing pressure on the consumer.

The consensus expects overall margins for DTG to come down to 3.3% for the next 3 years while DTG continues to take share. A bleak environment is in the estimates, while tailwinds from future knock-on bankruptcies are probably not (see growing conviction of RYA management and other comments featured in the recent RYA write-up).

DTG trades at a current year ending March ’20 consensus 7 X P/E ex. cash.

We believe in making two valuable adjustments:

-

Airlines are risky. Why? Fixed costs + price risk + volume risk. However, it would be unfair to think about current year FY20 earnings as risky though, as bookings are already secured for DTG given it is a very seasonal airline (peak-to-trough month passenger ratio is 4-to-1). Summer ’19 bookings are over, and management has guided to meet expectations in July. Moreover, many industry voices have commented in the meantime that late bookings were unusually strong this summer, so any variance with guidance should be positive.

-

we can deduct current year “normalized cash flow” from enterprise value, look instead at next year earnings multiple based on this forward EV, and discount that back to the present using a more appropriate 8% discount rate

-

“Normalized cash flow”: we conservatively use consensus accounting earnings which should at least be met given management’s history. We also add a small one-off working capital benefit detailed below

The mix shift towards packages creates a working capital cash flow tailwind because of bigger advance payments. Crucially, this cash flow tailwind happens without any growth capex requirement. In the FY13-FY19 period, package holiday passengers grew from 25% to 49,5% of the passenger mix. Because Jet2 only opened large bases in Stansted and Birmingham in FY18, this number stagnated in the last few years. We believe the mix can improve a few points towards that of the mature bases.

The mix shift cashflow tailwind is temporary, so it would be unfair to add them to “normalized earnings”. Instead, we deduct this cash tailwind from EV. For simplicity, we model a one-off 2,5 pp passenger mix shift for the next year towards 52%. There’s also a much bigger working capital tailwind for all airlines in general by simply growing revenue. As this requires growth capex (i.e. new planes), it would not be fair to include this. Instead, we isolated the mix shift effect. In DTG’s case over the past 5 years, roughly every 10£ of revenue growth have meant 2-3£ in cash flow from a growing negative working capital (i.e. customers paying in advance). We only account for cash tailwind from mix shift here.

On a base of an expected 13,8 million one-way passengers the cash flow tailwind becomes:

(pp pax shift towards packages) x (million pax / 2 return ticket) x (delta between price of package and price of return ticket-only) x (conservative estimate of fraction of pax that pay full package price amount in advance as opposed to only a non-interest bearing 60£ deposit)

= 2,5 % x (13,8 / 2) x (660 £– 60 £) x (35%) = 36 M GBP

Normalized valuation

Applying the two adjustments:

EV FY19 – consensus earnings FY19 – mix shift working capital benefit = EV FY20

= 845 – 121 – 36 = 688 M£

Normalized current year P/E ex. cash = 688 / 125 x [discount factor (8%; 7 months)] = 5,7 X

Peers

DTG has no true comparables because of the package holiday segment and distribution business.

Most comparable is Allegiant Airlines (ALGT) in the US. Like DTG, ALGT is the only ULCC in the US that dominates many local routes using older planes. There are many similarities: the makeup and absolute size of the fleet, the leisure passenger focus, owner-operated, the almost identical EBITDA.

ALGT takes Americans that live in small cities across the US on holiday to a few destinations. These are more concentrated than Jet2’s (mainly Las Vegas and Florida). Because ALGT takes millions of passengers to these two destinations, it recently started building a resort in Florida (on balance sheet!) absorbing roughly two years of net earnings. The market does not like the asset-heavy vertical integration step that management is enthusiastic about and ALGT is trading at a discount to its own historical EV/EBITDA valuation. Despite all this, and while the execution risk for DTG is past us in terms of vertical integration, ALGT trades at triple the EV/EBITDA valuation of DTG (7,5X). To be fair, ALGT did show superior ROIC versus DTG in the past (as opposed to all other peers).

On the Beach Plc (OTB) is a new UK package holiday provider (already number 4 with half the clientele of DTG, see table in “Evidence”) and acts as a digital agent. It is asset-light and its main cost is digital advertising for online user acquisition. We believe online user acquisition costs have become less attractive and OTB benefitted from being an early mover. While not very comparable, OTB trades at 20X EBITDA.

ULCC airlines Wizz and Ryanair trade at 6.5 X EBITDAR while DTG trades at 2.3X EBITDAR. As an LCC, DTG’s airline unit costs are more comparable to Easyjet, which trades at 4.3X EBITDAR. Note the use of EBITDAR to make a comparable basis with lessee Wizz.

Legacy tour operators: Thomas Cook is not comparable as the equity was wiped out. TUI is the most asset-heavy integrated operator of all, owning hotels, cruise ships and planes (despite that, net margin is similar if not inferior to DTG) and trades at 8X earnings or 5X EBITDA.

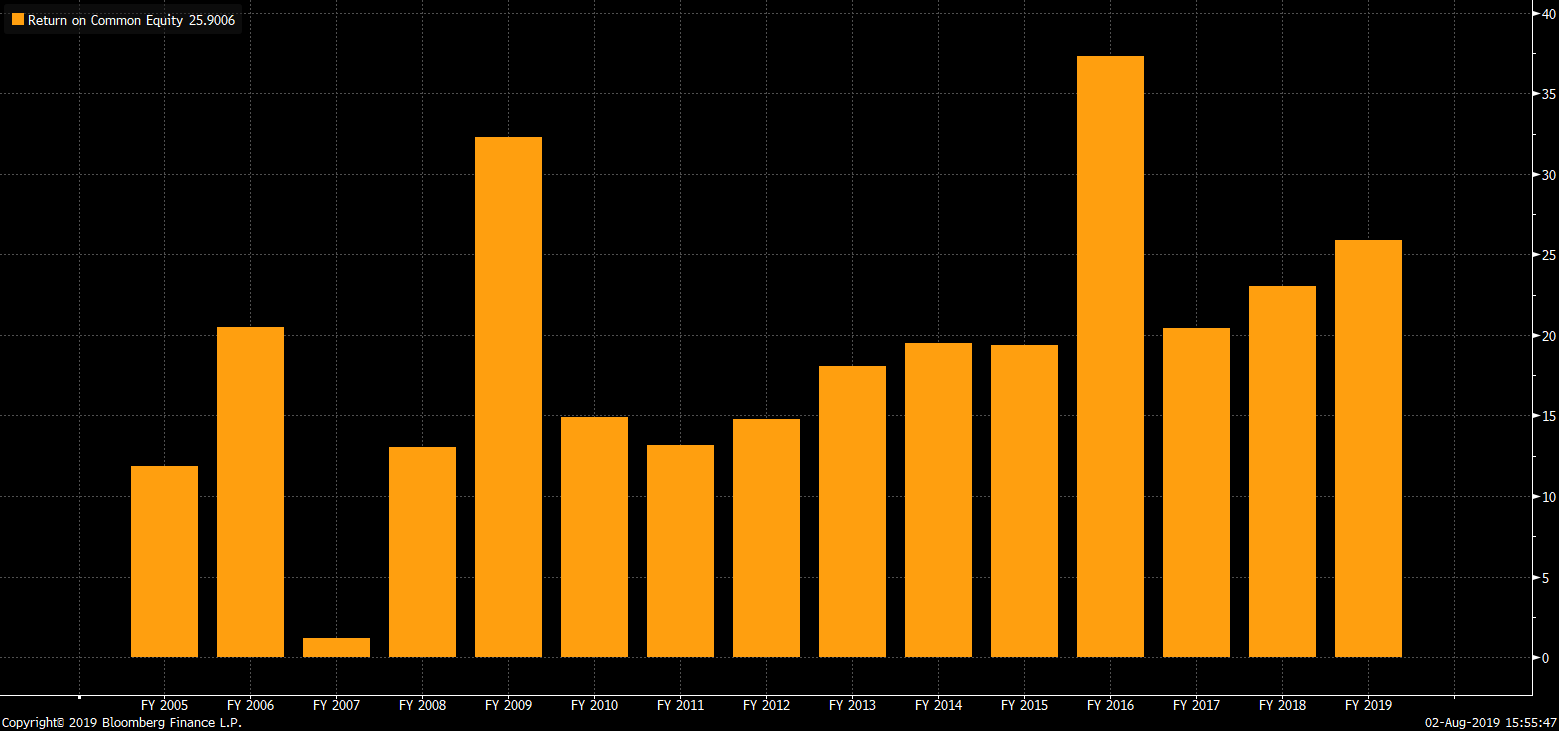

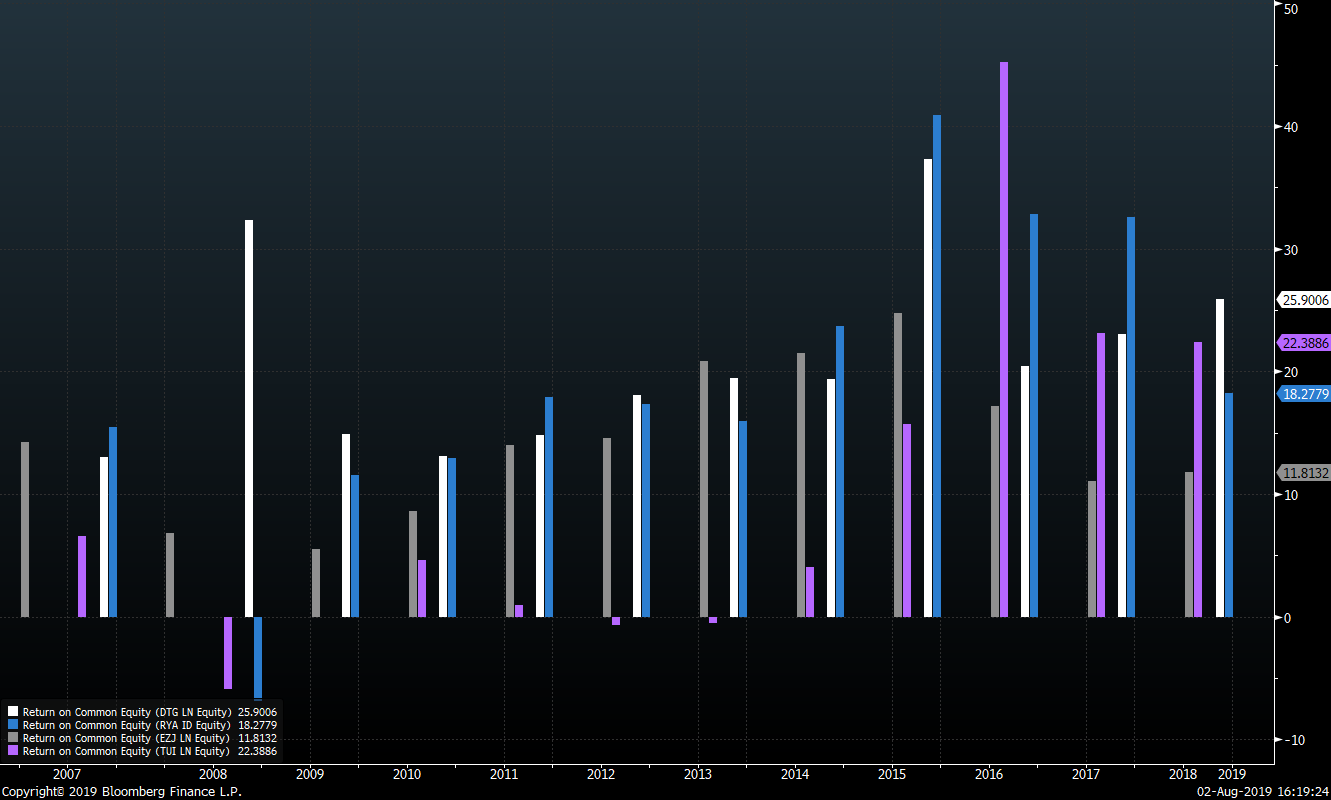

In terms of business quality versus all these peers, DTG has always had peer leading ROE as an LCC (high teens), that is growing since the shift towards packages (>20%):

Note we use ROE - and not ROIC – as Bloomberg would include non-interest-bearing customer cash in that capital (which is an intrinsic advantage to the airline business model). ROE is a good proxy of return on financial capital employed as DTG has almost never operated with a net debt position:

Although TUI’s ROE is boosted by financial leverage unlike the other peers, DTG has peer leading consistent high ROE’s (see below in white). Note ALGT (not in picture) has even higher ROE’s, trumping DTG with a few points.

Figure 7 ROE’s: DTG in white, RYA in blue, EZJ in grey, TUI in purple (boosted by financial leverage).

Risks

-

Even further GBP depreciation (price pressure on customers going on European holidays)

-

in our opinion, FX takes up most of the so-called “Brexit risk”. The remaining part being a deeper economic malaise for the UK.

-

most important risk but not knowable & FX hedging is the free lunch here for risk managers

-

Recession

-

Mitigants:

-

probably benefits from bankruptcies in medium-term as low-cost provider and with net cash

-

in ‘09, Jet2 remained profitable. Profitable in-flight revenue was boosted as richer customers trade down to flying with a low-cost carrier like Jet2

- EasyJet taking share

- limited overlap (see analysis)

- bigger fish to fry

- the big ones have a package holiday history of failure

-

Key man risk: Philip Meeson, 71 y-old

-

Mitigant: Meeson might sell to e.g. Easyjet

Why does the opportunity exist?

-

No real peer group due to idiosyncratic business mix: package holiday, low-cost airline and distribution business

-

Brexit uncertainty and related currency volatility

-

Limited research: 3 analysts Arden Partners, Canaccord, Jefferies (update: a fourth, Stifel)

-

Listed on AIM

-

DTG was listed on LSE in ‘90s, not long after migrated to the new AIM exchange. It is clear that management is listed on AIM for lower reporting requirements to focus more on the business. Both share count and Meeson’s stake have remained stable while shareholders have benefited enormously, i.e. x90 since 1989.

-

Small market cap

Review of UK Package Holiday sector

Summary of findings:

-

Brits are increasingly reluctant to give up their annual trip to the sun

-

Annual trip to the sun tops home improvements or a new car on spending priority for half of British families

-

Psychologically difficult for parents to give up annual family holiday with kids. Jet2 is oriented towards families. FT Example

-

Foreign holiday visits increasing steadily despite occasional downturns since 1980s

-

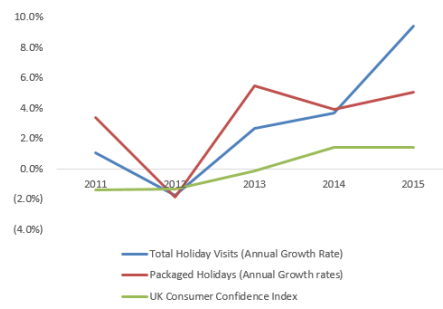

Recovery of packaged holiday post ’09 period significantly outpaced overall holiday market as consumers seek best value-for-money holidays (cutting independent travel outside EU)

-

Popularity of package holiday is inversely related to consumer confidence

-

In previous downturns, weaker operators have gone bankrupt, with surviving players emerging stronger

Before 2008, packaged holidays had undergone a multi-year decline due to rise of online travel websites, LCCs and preference for more customized holidays to more exotic destinations. This trend is well documented.

In the 1990s and 2000s, the rise of online booking website and LCCs liberated the UK holidaymakers from the restrictions of booking with brick and mortar holiday operators. The lower air fares and ease of online booking encouraged the portion of Britons who prefer independent holidays to shift away from packaged holidays. However, we argue that there are always people who prefer packaged holidays across different demographics, in particular young families.

In response to the shrinking market size, holiday operators merged in 2007 to form two large groups – Thomas Cook and Tui Group – to improve efficiency. Thomas Cook merged with MyTravel in 2007 while First Choice merged with Tui Group which operates under Thomson Holidays in the UK.

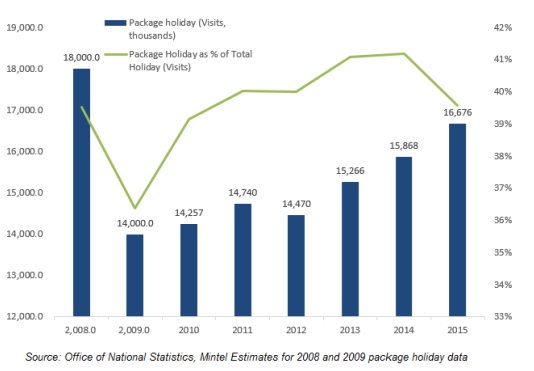

However, post-financial crisis, packaged holidays regained share as austerity led consumers to trade down to cheaper (and financially more predictable) package holidays. Between ’09 and ’15, packaged holidays gained share from 38% to 40% (Mintel.com estimate). Still, the crisis rinsed out the weaker players (e.g. Zoom, XL, Flyglobespan, Gold Trail, Flight Options, Holidays4U, see here). In the post-Brexit vote environment of weak consumer confidence, package holidays have continued to do well.

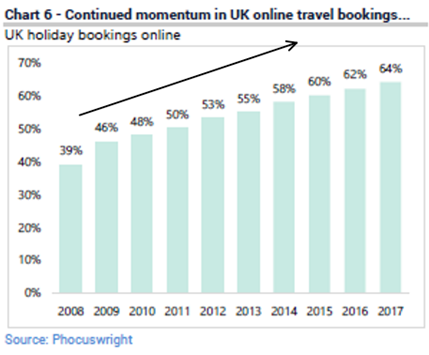

Meanwhile, UK is leading in terms of online bookings: the proportion of top 10 package holiday providers that have a retail presence halved from 90% in Summer 2010 to 2018. Jet2 sells 60% of packages online (while virtually 100% of airline tickets), and 17% through its call centres, the 23% balance is from high street holiday shops , while TUI and Thomas Cook are at 48% online sales.

Figure 8 Office of National Statistics

Figure 9 Office of National Statistics

Why do certain consumers choose packaged holiday over independent travel?

-

Want everything taken care of

-

Simply relax & unwind on beach without worrying about logistics

-

Value-for-money

-

Competitive price due to holiday operators’ scale (ability to buy hotel rooms in bulk)

-

Fixed budget beforehand: financial safety for poor budgeters

-

Convenience

-

Little research needed

-

Book at once

-

Emergency services

-

People feel safer knowing that in case of any emergency situations, their operators will repatriate them immediately

There are always people who prefer:

-

Beach holidays

-

Unwind & relax

-

Destination agnostic

-

Prefer convenience over adventure

-

Price-sensitive

-

Safety first

For example, middle income families with kids. Package holidays also became more flexible to adapt to consumer demands:

-

Greater range of hotels (all stars)

-

Larger range of nights (typically 2-14 nights)

-

More destinations

-

Expansion into ski & city-breaks

TUI & Thomas Cook - the legacy disadvantage

Jet2 is the only integrated provider of packages without owned retail presence. While 23% of its packages are still sold by independent high street agents, Jet2 should benefit from a continuing shift online while TUI and Thomas Cook struggle as they choose between further cost cuts and holding on to legacy clients (% booked offline for these players is higher as well):

But, what about a no-deal Brexit? [CAA Info; UK Govt]

The only real (and large) risks are forex and knock-on effect of specific headwind for the UK economy:

Traffic in case of no-deal

· Both EU and UK agree on continuing third & fourth freedom of the air, perhaps even seventh freedom. Third & Fourth freedom are in line with agreements of any other global bloc that EU has (so nothing special for post-Brexit UK).

· unlike LCC competitors, as Jet2 only flies between UK and EU (not within EU), it does not need seventh freedom, only up to 4th freedom.

Conclusion: Jet2 has no traffic risk exposure

Ownership & control

Each world’s bloc has 50+ year old legacy legislation requiring at least 50% domestic shareholder voting / ownership. This caused a scare after the Brexit vote in airline stocks as RYA, DTG, EZJ, etc. reminded markets in notices about their special rights to force a buyback of shares from foreign shareholders if states would ever enforce this rule.

· Reality is that this legislation is outdated and arguably in violation of WTO rules. Both UK and EU have said they would not enforce this law (in particular, not view the UK as separate from EU for purpose of this law):

· All major European airlines have adjusted domestic ownership above 50% today[1], incl. Jet2.

Conclusion: Jet2 has no ownership/control issues post-Brexit whatsoever.

[1] I understand institutional owners can simply change nationality of their holdings using UK / EU subsidiaries. Also, even if this rule would be enforced, airlines have said they plan to require the foreign owner causing the +50% limit to be exceeded to sell (LIFO rule).

References

-

Psychologically difficult for parents to give up annual family holiday with kids. Jet2 is oriented towards families. FT Example

-

Mr. Meeson’s “customers first” obsession https://www.telegraph.co.uk/travel/budgettravel/6222484/Police-called-as-airline-boss-berates-own-staff.html

-

Jet2 ad [Youtube]

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

- Bankruptcies

- Valuation

- Good execution

| show sort by |