| 2016 | 2017 | ||||||

| Price: | 25.00 | EPS | 4.48 | 5.15 | |||

| Shares Out. (in M): | 26 | P/E | 5.6 | 4.8 | |||

| Market Cap (in $M): | 640 | P/FCF | N/A | N/A | |||

| Net Debt (in $M): | 3,500 | EBIT | 330 | 360 | |||

| TEV (in $M): | 4,100 | TEV/EBIT | 12.4 | 11.4 | |||

| Borrow Cost: | Available 0-15% cost | ||||||

Sign up for free guest access to view investment idea with a 45 days delay.

- ENCORE CAPITAL GROUP INC ECPG 12/20/2023

- ENCORE CAPITAL GROUP INC ECPG 07/25/2012

- Encore Capital ECPG 06/07/2006

- BETA

- POOL CORP POOL 08/02/2023

- POOL CORP POOL 10/22/2022

- Arrow Global Group ARW.L S 12/12/2017

- Asset Acceptance Capital Corporation AACC 08/02/2011

- pool corp pool S 01/06/2023

- LATHAM GROUP INC SWIM 03/17/2023

- PRA GROUP INC PRAA 10/27/2017

- LESLIE'S INC LESL 09/15/2021

Description

Encore Capital Group, I believe has a revenue recognition problem that makes their reported earnings and EPS estimates irrelevant and even their negative tangible book value is overstated. Encore Capital Group is a debt collection company I believe is overstating revenue and balance sheet assets by using aggressive accounting assumptions to hide fundamental weaknesses. Reasonable accounting assumptions would result in at least a $250 million charge to shareholder equity, or nearly 50% of the company’s current market capitalization – from just a single pool purchased in a single geography. In this write-up I will focus mostly one this one pool, but we can assume when fraud is this evident to the public, there is likely much more fraud that we can’t see.

Valuation – I realize that the stated P/E multiples screen as extremely low. I believe that P/E is irrelevant for this company. This is a publicly traded distress debt fund, that invests in a very limited set of assets – distressed consumer loans. Valuation should be a premium or discount to NAV and ECPG’s NAV or tangible book value is currently negative and I believe overstated.

Industry Overview & Trends

Debt collection companies perform a very valuable service: getting debtors to pay their overdue bills. Every company that extends consumer credit often has customers that do not pay their bills. The lender has several options for delinquent debt: 1) write off the debt owed; 2) attempt to pursue a means to collect the debt through litigation or pestering phone calls; or, 3) sell the debt to a debt collection company (usually for a small percentage of the full amount owed). Collection companies are highly focused businesses that can usually collect more efficiently as they are less hindered by the negative publicity and goodwill that can be caused by their aggressive tactics.

The industry has recently come under scrutiny by the Office of the Comptroller of the Currency (OCC) and Consumer Finance Protection Bureau (CFPB). In July 2013, the OCC provided guidance for credit issuers about their relationship with prospective debt buyers. By doing so, the agency solidified the framework under which the issuers may sell receivables. Also in July 2013, the CFPB provided a bulletin advising of its oversight of debt collection practices. The focus of the bulletin was ensuring the availability of information to consumers about their obligations. Subsequently, on September 9th, 2015, Encore Capital Group settled with the CFPB regarding allegations relating to practices from 2011 through 2015. The company impaired its portfolio by $8.3 million to reflect the CFPB’s new rules.

Collection companies historically purchase pools of receivables through competitive auctions based upon each collection companies’ best estimate of the pool’s future collections. Historically, collection companies would pay approximately 25% of what they estimated they could collect from the pool of delinquent receivables. Therefore, collection companies would expect to collect 4x the amount they paid for any given pool. The collection company essentially becomes an investor in a pool of difficult to collect receivables. If the receivables ultimately produce collections in-line or better than they estimated, the pool would prove to be a very profitable investment. If collections are less than expected, then the collection company could lose sizable amounts of money not only from the purchase price paid, but also from the costs incurred attempting to collect the debt. One recent trend that should be noted is more collection companies are suing debtors in court to secure collections and regulatory bodies have become especially concerned with this aggressive tactic. This raises the cost to collect in the form of court costs and attorney fees, but has been very successful in producing increased collections. This is the result of few defendants appearing in court, which allows the collection companies to debit money directly from the defendant’s paychecks.

Cycle 1: Late 1990s Disaster to Early 2000s Boom

The debt collection business has a history of boom and bust. In the mid 1990s there was little competition for the purchase of these delinquent pools of debt. The industry prospered making outsized returns (6x to 10x multiples of purchase price) on the purchased pools. However, these outsized returns attracted attention and soon the competition for the pools increased. This led to price increases, ultimately driving down returns to just 2x the purchase price by 1999. Several companies paid even more in an effort to accelerate growth and ultimately went bankrupt (e.g. CrediTrust and Commercial Financial Services) when they could not recoup their initial purchase prices. This proved to be the bottom of the cycle leading to a decline in pricing and the debt collection industry was buying pools that proved to be incredibly profitable. As shown in the table below, as competition exited the market, Encore was able to purchase portfolios with very attractive returns (higher multiples are more attractive).

ECPG’s Cumulative Collections / Purchase Price

By Year of Pool Purchase, aka ‘Vintage’

1999 2000 2001 2002

2.0x 4.5x 4.9x 4.9x

Note: 1999 pricing resulted in a $21 million impairment in later years.

The expensive purchases made in the late 1990s proved to be disastrous. After its $10 / share IPO in July 1999, Encore Capital Group realized $21 million of impairments in 2000 and by the end of the year, shares were trading for less than $1 per share. However, the attractive purchases made in subsequent years (2000 to 2002), saved the company and set Encore up for attractive future results.

Cycle 2 Pre-Financial Crisis Cycle Binge Makes Pricing Too Aggressive…Again

Pre-financial crisis, competition returned to the industry, pushing pricing up and expected returns down. By 2004, purchase multiples were again down to less than 3x and by 2007 the multiples were barely above 2x. Once again, overpaying led to future impairments. Encore realized $26 million of impairments in 2008, $22 million in 2009 and $11 million in 2010.

ECPG’s Cumulative Estimated Collections / Purchase Price By Vintage

2004 2005 2006 2007

2.6x 2.5x 2.4x 2.3x

Aggressive Purchase Multiples Led to Future Impairments

2008 2009 2010

Impairments: $26M $22M $11M

Cycle 3: Post-Financial Crisis Cycle: Salad Days Return

During the financial crisis many smaller players were eliminated from the market. Public competitor Asta Funding (ASFI), was overwhelmed by its record pre-crisis purchases and never returned as a real competitor. Privately held SquareTwo struggles to survive today and have capacity to continue to purchase. While industry purchasing power was impaired, supply increased from banks selling off more and more bad debt. The result for buyers still in the market: the salad days were back, prices were down, and expected collections / purchase price exceeded 3x.

ECPG’s Cumulative Collections / Purchase Price

2009 2010

3.3x 3.1x

Cycle 4: The Industry Today

In 2011, competition returned as estimated collections / purchase price multiples once again dipped below 3x. While this is slightly concerning, what has happened in more recent years is alarming – multiples were barely above 2x by 2014 and by 2015 were below 2x for the first time in the 18 years that Encore has been required to disclose this data. What makes this data so frightening is that the industry cost to collect is approximately 50% of cash collections. Encore’s operating expenses / cash collections (before interest expense) were 47% in 2014, 50% in 2015 and 46% in 1Q16. This shows Encore is purchasing portfolios with an expectation to lose money. On a per dollar basis for 2015 and 2016 purchases, Encore spent $1.00, expects to collect $1.70 (1.7x purchase price multiple), but will spend $0.78 in operating costs to collect and incur 6% or $0.06 in financing costs. The cash flows are -$1.00 + $1.70 - $0.78 -$0.06 = -$0.14. This reminds me of an old Wall Street joke of selling a dollar for 90c, but don’t worry, the difference will be made up on volume.

ECPG’s Cumulative Collections / Purchase Price Multiples By Vintage

2011 2012 2013 2014 2015 2016

2.7x 2.5x 2.7x 2.1x 1.7x 1.7x

How Long Until Impairments Surface

2014 2015¹ 2016

Impairments $0m $8m $0m

¹2015 Impairment realized as part of new CFPB rules

Aggressive Growth Kills

Aggressive growth has proven to be the detriment of this industry. CrediTrust reported 130% portfolio growth the year before its IPO, yet filed for bankruptcy within 18-months. Commercial Financial Services reported it was hiring 40 new employees per week in 1997, yet filed for bankruptcy 12-months later. Asta Funding met its undoing when it reached for a $300 million portfolio purchase which was 10x its normal level of purchasing. To grow fast, companies must overpay for portfolio purchases and overpaying results in losses typically. Since 2013, Encore Capital has pursued an aggressive growth strategy, averaging $1.1 billion of annual purchases, or a 158% increase from the $400 million average annual purchases in the previous three years.

Typical Collection Patterns

Collection pools tend to follow a fairly predictable pattern. Collections from the pool start slowly as the collectors begin tracking down the debtors, make their initial calls, decide which debtors have the means to pay, which don’t, and which to take to court. After the initial slow start, collections progressively build over the next 12 months, but after the first 12 months of ownership, collections start to slow at fairly predictable rates. Of Encore’s 16 years of publicly disclosed collection data, spanning 108 portfolio year over year comparisons, only 1 portfolio, in 1 year (or 0.9% of observations) has experienced a year over year increase (the year 2000 pool experienced a year over year increase from 2002 to 2003).

Industry Accounting for Revenues Recognition Can Be Tricky

Revenue recognition for this industry is very confusing, based entirely upon estimates, and has less than ideal correlation to the actual cash generated by the business. FAS ASC 310-30 (formerly SOP 03-3) Accounting for Certain Loans or Debt Securities Acquired in a Transfer is the accounting standard used for revenue recognition. This standard requires that the collection company establish pools of receivables quarterly and estimates the internal rate of return (IRR) that will be earned off those pools (note the IRR calculation is for revenue and not for net income). The estimated IRR is then applied to the receivable balance to derive revenue. For example, if a debt collection company spends $100 to purchase receivables (face value of the actual receivable is irrelevant) and expects to collect $300 over the next 3 years (assume $90 in year 1, $120 in year 2, and $90 in year 3), this is an IRR of 83%. To calculate revenue in year 1, the IRR of 83% would be applied to the book value of receivables of $100 and thus revenue in year 1 would be $83. As shown below, revenue has little connection to actual cash collections. The $83 of revenue would be the same if the company collected $1 or $200, the revenue would still be $83.

What if collections are better or worse than expected based on actual experience over time? The company must do one of two things. If collections are determined to be performing better than expected, then the company must raise the IRR estimate and thus revenue recognition going forward increases. However, if the collections are determined to be performing worse than expected, then the company must recognize an impairment (sometimes referred to as an ‘allowance charge’) on the underperforming pools and this impairment will be a contra revenue item on the income statement. This will reduce the carrying amount of the receivable on the balance sheet.

Collections should always be greater than revenues recognized because the debt collection company needs to cover its initial investment in the pool. (Economically speaking, its the amount collected above the initial investment that generates returns.) Every dollar that is collected is part recovery of the initial investment and part revenue. What FAS ASC 310-30 attempts to do is precisely allocate how much of each dollar collected is allocated to revenue versus cost recovery. Going back to our example, if in year 1, $83 of revenue is recognized and the company collected $90, the excess amount ($7) is used to reduce the carrying amount of the portfolio purchase. If all estimates prove to be accurate, collections will cease at the same time the carrying amount of the portfolio reaches zero and thus revenue stops because the IRR is applied to a zero balance. A full example is shown below using our same $100 purchase price example:

Revenue Recognition Example

|

Purchase Price |

100 |

|||

|

IRR |

83% |

|||

|

Cash |

Receivable |

Portfolio |

||

|

Collections |

Pool on B/S1 |

Revenue2 |

Amortization3 |

|

|

Year 1 |

90 |

100 |

83 |

7 |

|

Year 2 |

120 |

93 |

77 |

43 |

|

Year 3 |

90 |

49 |

41 |

49 |

|

Year 3 |

|

0 |

|

|

-

Purchase price less accumulated amortization

-

IRR x Receivable on B/S

-

Collections less revenue

Higher or Lower Purchase Prices Impact Revenues, But Not Collections

What should become apparent from the preceding example is that revenues will decline when purchase prices increase even if the purchased portfolio has the exact same collections. Collections in isolation are irrelevant. What is critical is purchase price relative to collections. This is because a more expensive portfolio will need to allocate a greater portion of collections to cost recovery rather than revenue. Below I take the exact same example I used earlier with the one exception that I increased the purchase price by 50% to $150, yet the collection patterns are exactly the same.

Revenue Recognition Example with Higher Purchase Price

|

Purchase Price |

150 |

|||

|

IRR |

44% |

|||

|

Cash |

Receivable |

Portfolio |

||

|

Collections |

Pool on B/S1 |

Revenue2 |

Amortization3 |

|

|

Year 1 |

90 |

150 |

66 |

24 |

|

Year 2 |

120 |

126 |

56 |

64 |

|

Year 3 |

90 |

62 |

28 |

62 |

|

Year 3 |

|

0 |

|

|

-

Purchase price less accumulated amortization

-

IRR x Receivable on B/S

-

Collections less revenue

As shown in this example, despite the company collecting just as effectively in the second example as in the first, because the initial purchase price was 50% higher, the revenue recognized off this portfolio was $17 million lower in year 1 ($83mm-$66mm), $21 million lower in year 2, etc.

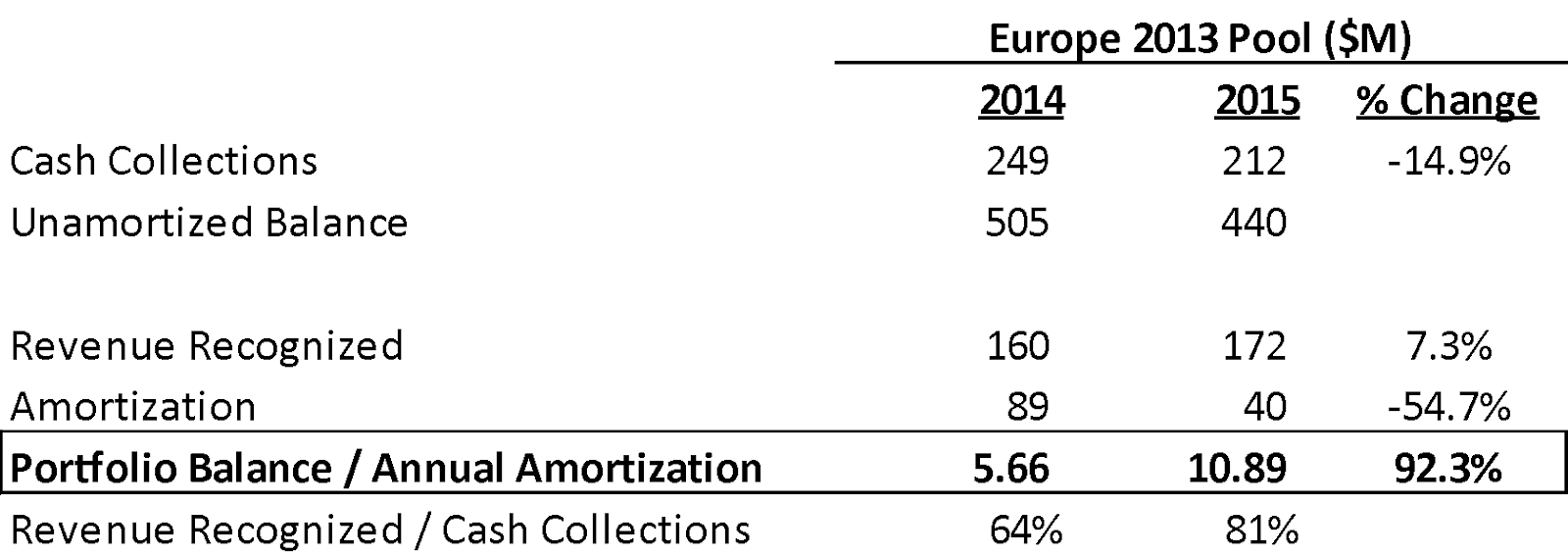

Questionable Accounting For Encore’s Europe 2013 Pool

I have the following concerns when focusing on Encore Capital Group’s 2013 Europe pool of debt receivables: 1) cash collections are declining; 2) reported revenues are increasing; 3) portfolio amortization is declining; and the result is, 4) this portfolio must collect at its current level (despite year over year cash collections declining every quarter since purchase) for 15 more years in order to avoid realizing an impairment. What is the chance that this 2013 European portfolio will continue to generate cash collection at the current rate for 15 more years (especially considering the portfolio is nearly three years old and the U.K. statute of limitations is only 6 years)?

“Zero. Zero. There is a Zero percent chance” Mark Baum in the “Big Short”.

Note: The statute of limitations for contacting consumers regarding collections in the U.K. is 6 years for standard and simple unsecured debt (starting from the date of the debtor breaching the contract with the creditor) and 12 years for secured debts according to the Limitation Act of 1980.

2013 Europe Concerns: Collections Declining + Revenue Increasing + Amortization Declining = An Unsustainably High Carrying Value

Note: Portfolio was purchased mid-2013 so annual metrics are not meaningful for 2013.

Source: Company Reports

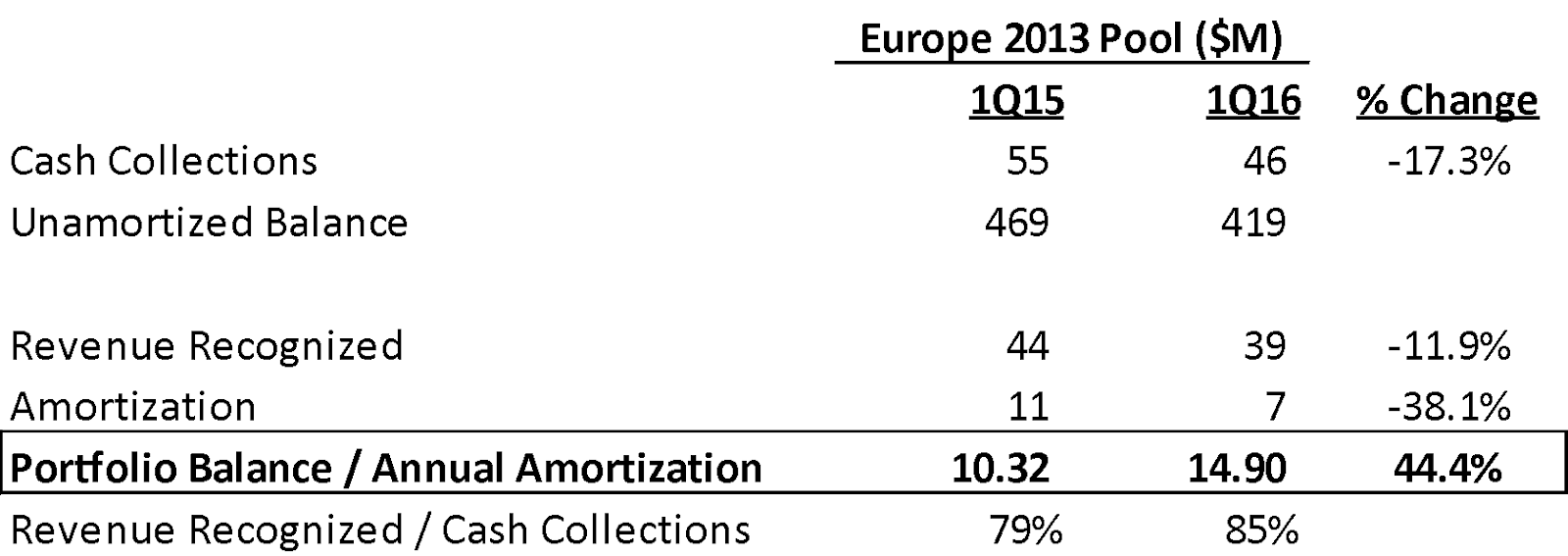

1Q16 Shows The Unsustainable Trend Continuing

Source: Company Reports

As Expected, The Europe 2013 Pool is Experiencing Declining Cash Collections

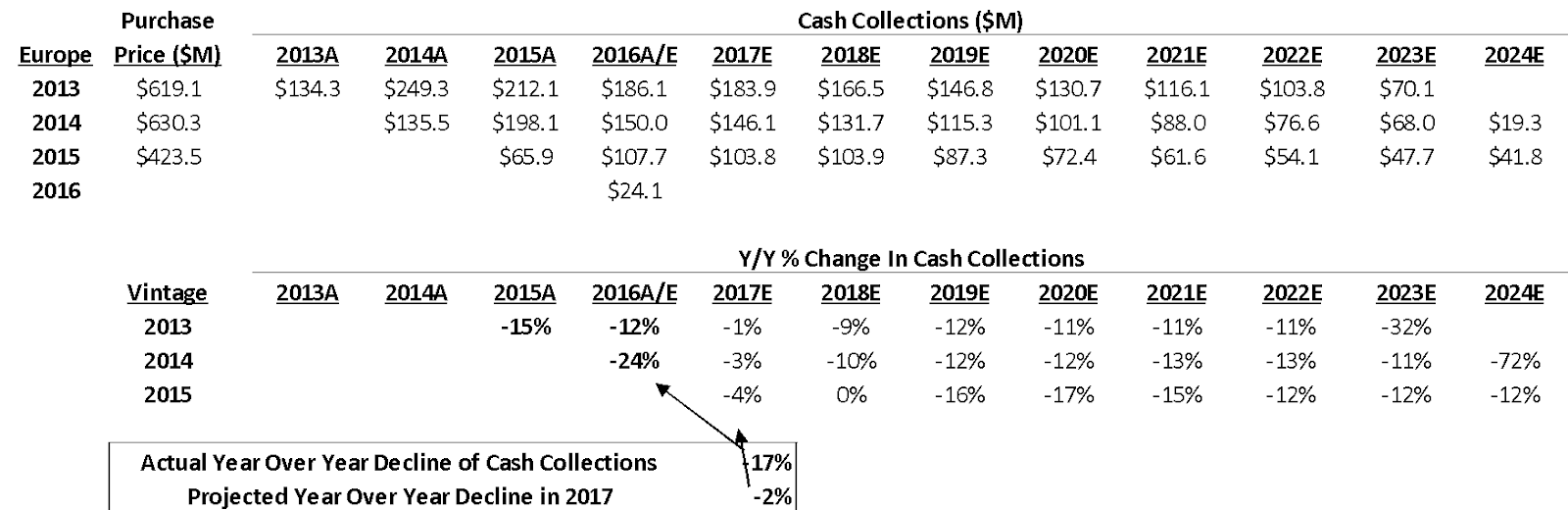

Encore Capital Group’s Europe 2013 pool (meaning debt receivables purchased in 2013 in Europe) has produced declines in cash collections in every quarter since the closing of the acquisition in 3Q13 (detailed below). This would be characteristic of a portfolio that is likely to see diminishing cash collections into the future.

The Europe 2013 Pool Shows A Persistent Decline In Collections

Source: Company Reports

Encore’s Cash Collection Accounting Assumptions Contradict Actual Experience

Cash collections from the European 2013 pool have declined as expected. As shown in the previous chart, quarterly cash collections have declined year-over-year for five consecutive quarters and on a full year basis declined 15%. Encore’s accounting assumptions incorporate a decelerating rate of decline of only 12% in 2016, much better than the actual 17% year-over year decline experienced in 1Q16. However, what is even more shocking is the de minimus -1% accounting assumption for 2017.

Encore Capital Group Is Estimating Europe 2013 Cash Collections Only Decline By 1% In 2017 Despite Actual Results of Double Digit Declines

Note: For comparable purposes, the 2016 estimated collections at 3/31/16 include cash actually collected in 1Q16

Source: Company Reports

Encore’s Accounting Assumptions for Cash Collections Contradict U.S. Experience

Encore Capital Group management is lacking experience in managing Europe pools, but they are able to rely on years of history collecting U.S. paper. This experience has shown the company that cash collections in the third year typically produce meaningful declines from the second year cash collections. The average U.S. vintage paper from 2001-2012 declined 31% in the third year and 33% in the fourth year. This history of 30%+ declines clearly contradicts the 1% decline accounting assumption for the Europe 2013 vintage.

Management Estimates Do Not Match Up With Historical Trend Seen In U.S. Paper

Note: 3rd year defined as collections the 3rd year after the purchase year (i.e. 3rd year denotes 2004 collections growth/loss rate from 2003 collections for the 2001 U.S. pool.

Source: Company Reports

Summary of US Pools Actual Experience Versus Encore Capital Group’s Accounting Assumptions for the Europe 2013 Pool

US Experience EU 2013 Accounting Assumption

Cash Collections Year 2 to Year 3 -31% -12%

Cash Collections Year 3 to Year 4 -33% -1%

Source: Company Reports

Encore Capital Group’s Accounting Assumptions Contradict Those of Public Peer Arrow Global

Arrow Global (ARW LN) is a London listed debt collection company that only purchases consumer portfolios in Europe. According to Arrow, and confirmed by their cash collection history, cash collections are expected to decline at a fairly predictable rate.

“A separate model, using an ERC forecasting methodology, then takes the 12-month estimate and uses this to form an 84-month forecast of ERCs at a portfolio level, by extrapolating the data over a decaying rate” [emphasis added].

-Arrow Global’s 2015 Annual Report

If Arrow Global, a European debt collection company with significantly more experience in Europe than Encore Capital Group expects their annual cash collections to decline, i.e. decay, annually, then what gives less experienced Encore Capital Group the confidence to assume that each of their European vintages will experience flat cash collections in 2017?

If we focus on the details within the 2013 vintage, Encore’s accounting assumptions are significantly more aggressive than those of Arrow. Encore’s European 2013 pool has collected similar to Arrow’s European 2013 pool. To-date, Arrow has collected 0.90x its purchase price while Encore has collected 0.96x or just a 7% difference. Despite the similarities in actual collections thus far, Encore’s accounting assumptions forecast the 2013 European pool to accelerate collections in the next 54 months for additional collections of 1.21x purchase price or 34% better than Arrow’s forecast of flat collections over the same period.

Encore Capital Group Is Forecasting Significantly More Aggressive Collections Than Arrow Global

Source: Company Reports

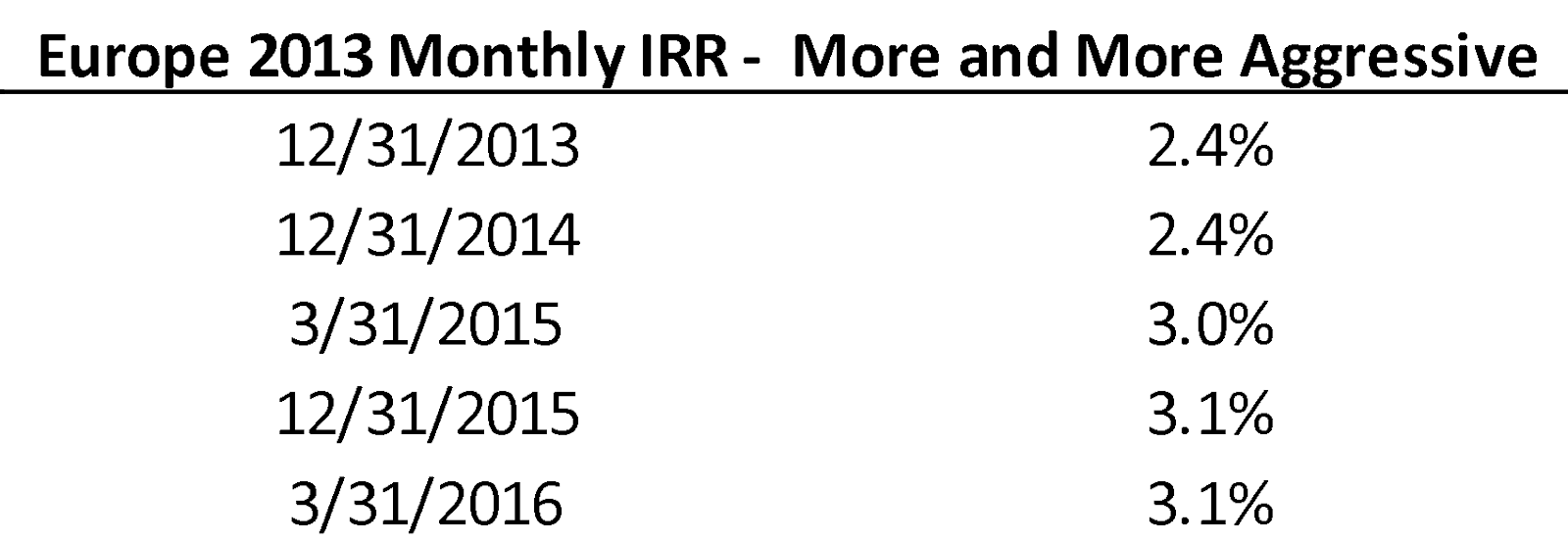

Aggressive Cash Collections Assumptions Are Increasing the Portfolio IRR And Decreasing Portfolio Amortization

The company has also taken the aggressive step of showing a consistent upward trend in the IRR estimate applied to the portfolio. This is a sign their management believes the portfolio is outperforming despite the following page showing that the company has recently reduced their estimates of future cash collections without realizing an impairment.

Encore Capital Group Has Consistently Increased The IRR Assumption On the Europe 2013 Pool

Source: Company Reports

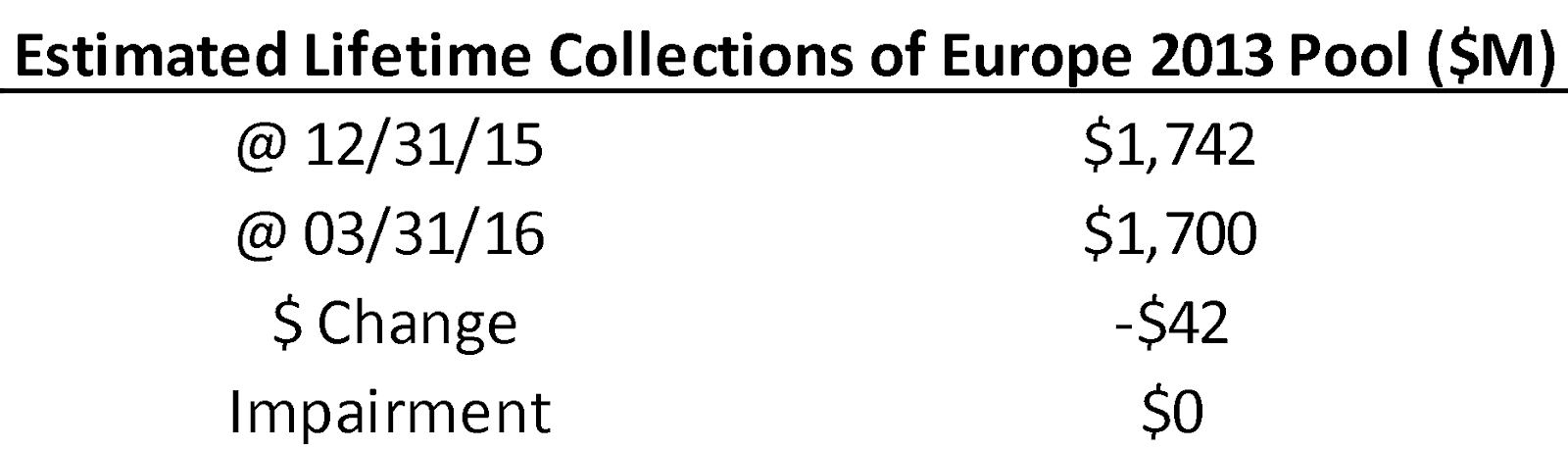

Defying Accounting, Encore Has Reduced Collection Estimates Without Taking Impairments

Despite the aggressive assumptions, management actually lowered collection estimates in 1Q16, but interestingly did not take an impairment. The estimated lifetime collections of the Europe 2013 pool declined $42 million, while management kept the IRR constant at 3.1%. From an accounting perspective, we do not see how this is possible.

Encore Capital Group Decreased Estimate Lifetime Collections For Europe 2013 Pool In 1Q16…

Source: Company Reports

…But Has Somehow Lowered Collection Forecasts Without Taking An Impairment

Source: Company Reports

If Impairment is Not Realized Immediately, Amortization Will Soon Turn Negative

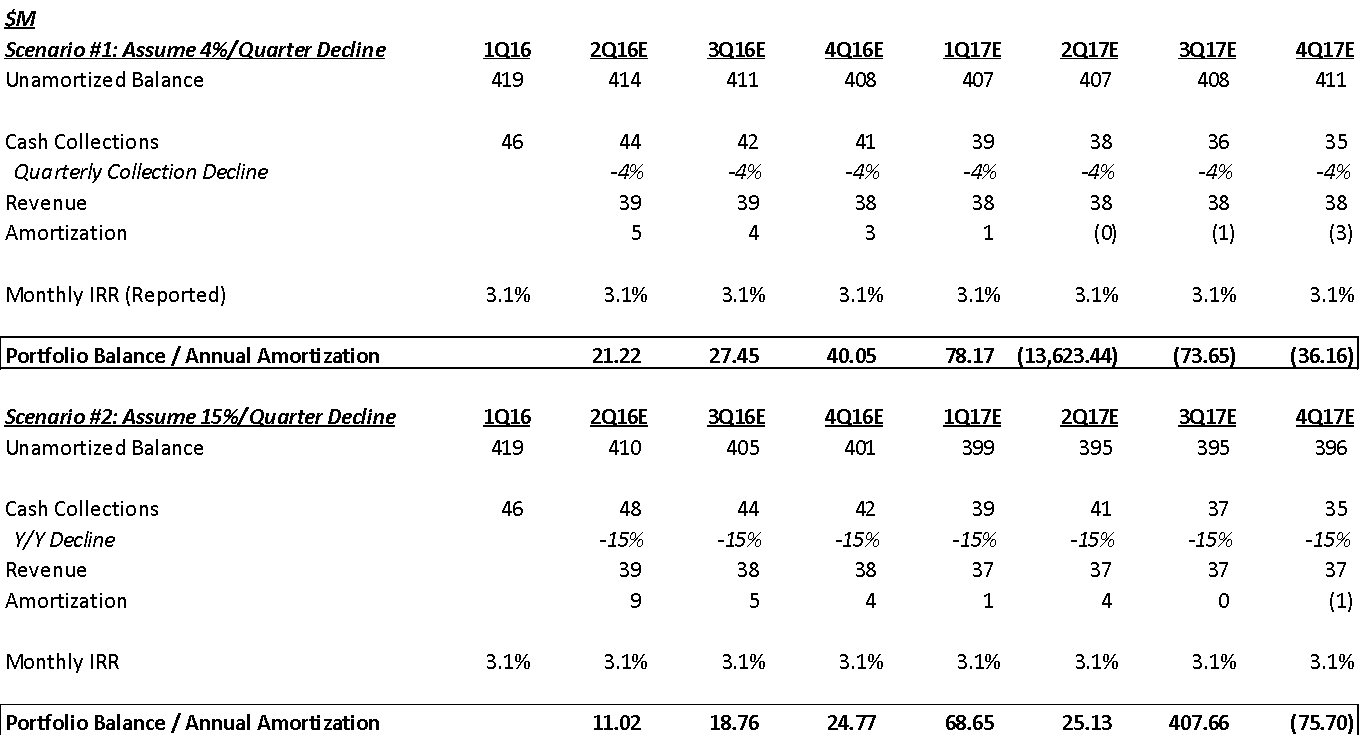

I want to provide two scenarios that I believe seem reasonable for what the portfolio may expect in terms of cash collections into the future to show the need for an impairment. Scenario #1, I assume cash collections follow the quarterly average decline since 2Q14 (first full quarter possible for sequential comparison), which has been 4%. Scenario #2, I assume cash collections follow the average year over year decline since 1Q15 (first year-over-year comparison possible), which has been 15%. If I use management’s 3.1% expected IRR for this portfolio in both scenarios, amortization will go NEGATIVE sometime in 2017.

Using Historical Collection Trends As Forecasting Tools, I See An Impairment As Imminent

Source: Company Reports

How We Quantify The Need For At Least A $250 Million Impairment

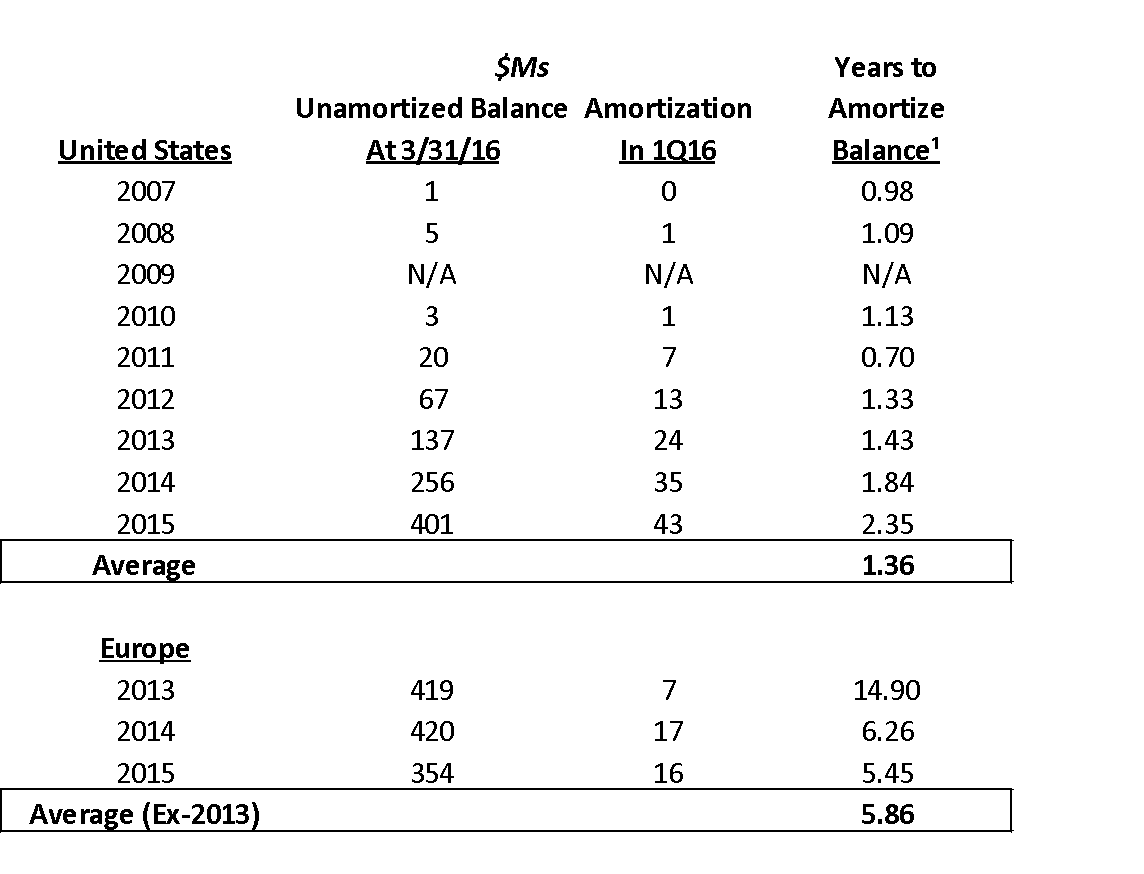

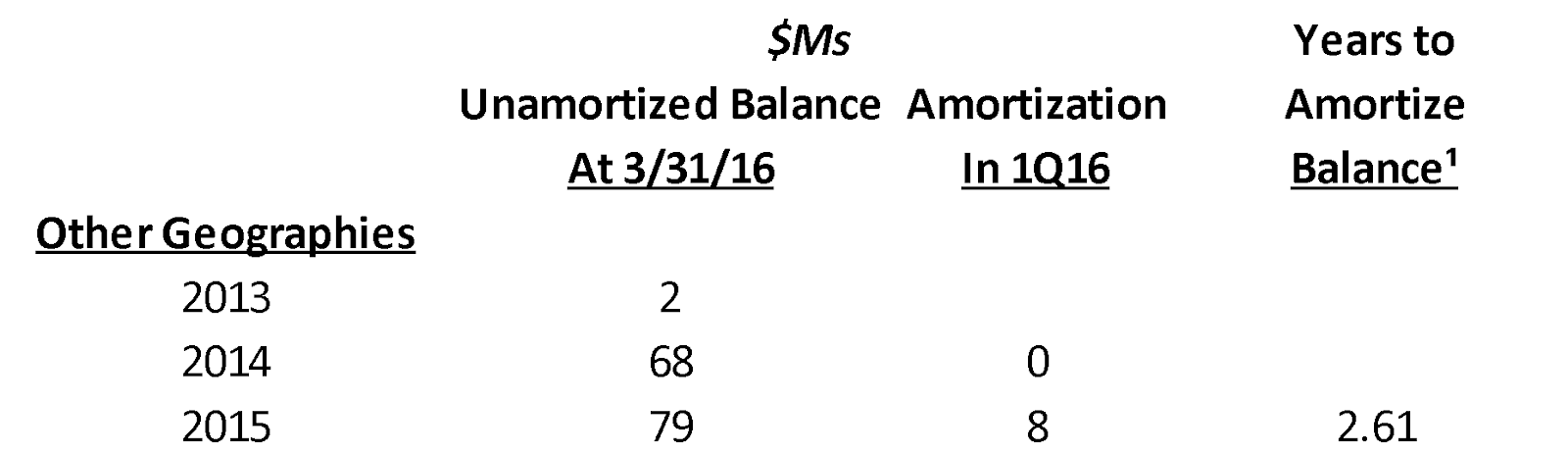

Encore Capital Group’s U.S. vintages are all carried at fairly tight ranges with the unamortized balance equal to approximately one to two years of annualized amortization, meaning if the pool continues to amortize at its current rate, it will be fully amortized in one to two years (the reality is that each pool’s cash collections decline and full amortization takes much longer) . Encore’s Europe 2014 and 2015 vintages carry unamortized balances representing five to six years of annualized amortization (I will review later why I have concerns with these vintages as well). However, the Europe 2013 vintage is carried with an unamortized balance equal to fifteen years of annualized amortization!

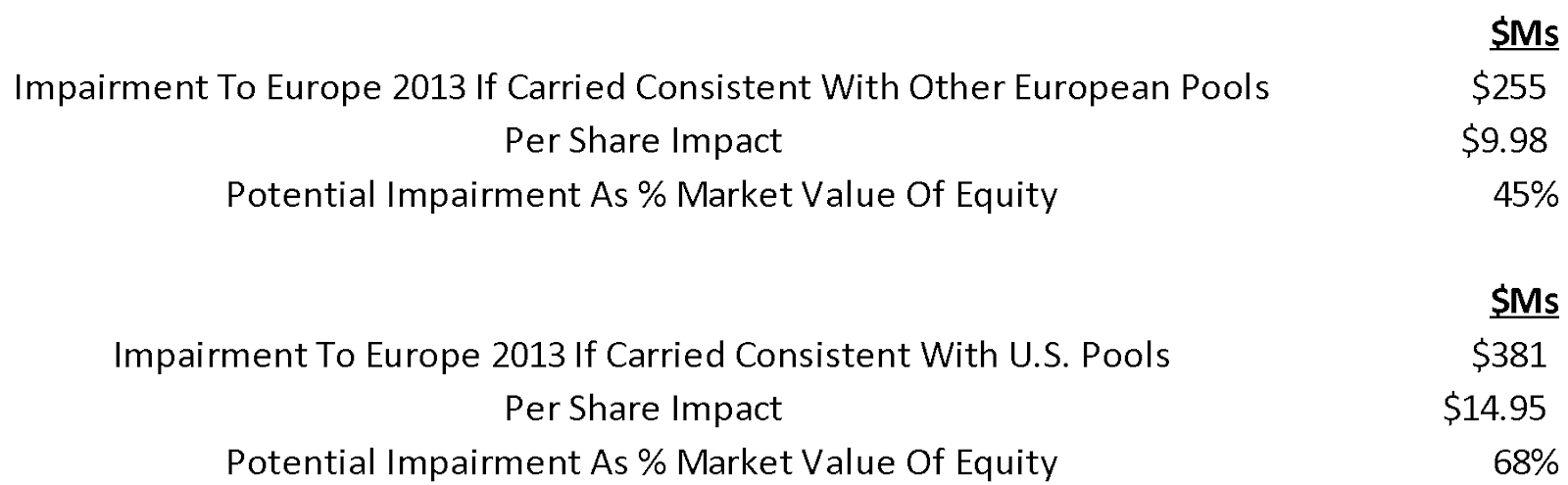

The 2013 European vintage is in need of impairment as has been documented earlier in this letter. To estimate the range of reasonable carrying values, and thus necessary impairments, I assumed a carrying value in line with the other two European vintages of 5.9x annualized amortization and 1.4x annualized amortization, the average of the U.S. Vintages. The result is that with the more aggressive European vintage assumption, a $250 million impairment would be necessary. With the more conservative U.S. vintage assumption, a $381 million impairment would be necessary.

Europe 2013 Years To Amortize Balance Is ~15 years Versus Other European Portfolios ~5-6 Years

¹Unamortized balance at 3/31/16 divided by amortization in 1Q16 multiplied by 4.

Source: Company Reports

If Encore Capital Group Made Similar Assumptions For Europe 2013 As Other European Pools, The Company Would Need To Take A $255M Impairment

Source: Company Reports

Other Areas of Concern

Chief Executive Officer Kenneth Vecchione Solely Focuses on Growth

Mr. Vecchione joined Encore Capital Group in 2013 and at his first investor day, made his priorities clear: Mr. Vecchione would pursue growth. The problem with this strategy is history shows the result is disaster. Commercial Financial Services, CrediTrust, and Asta Funding all blew up by targeting volume over profitability.

“So there’s a little saying in New York, you ask anyone on the streets in New York and you say to them, how do you get to Carnegie Hall? They’ll tell you practice, practice, practice. You ask anyone in Encore, how do you grow EPS, they’ll tell you the same thing, ERC, ERC, and ERC.”

-Kenneth Vecchione from June 2013 Investor Day emphasizing that his priority would be volume.

Under Mr. Vecchione, Encore has been an acquisition machine. Annual purchase volume increased 2.6x since he joined and Encore pursued the purchase of companies and international expansion. Under Mr. Vecchione, Encore has purchased Asset Acceptance (a publicly traded competitor), Cabot Credit Management, Marlin Financial Group, Hillesden Securities, Grove Capital, Refinancia S.A., and Baycorp Holdings.

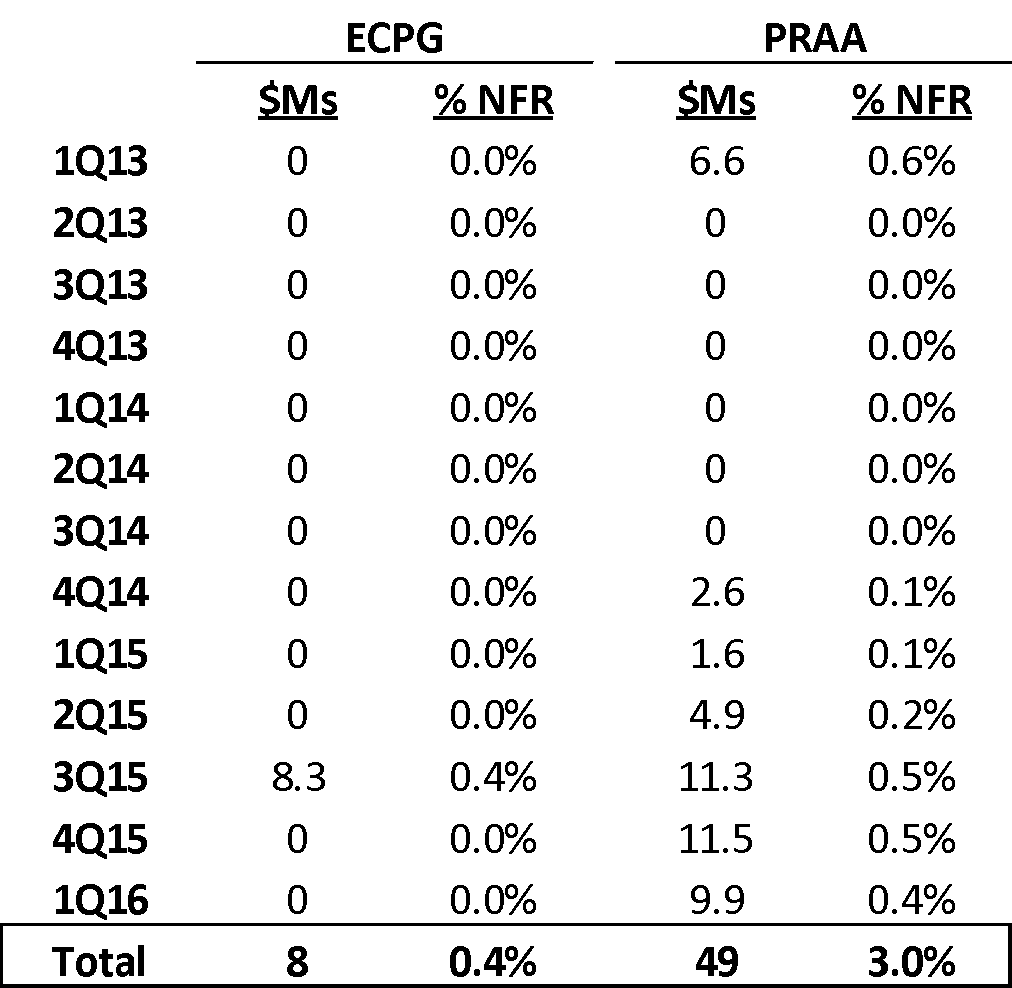

Direct Public Competitor PRA Group Realizing Impairments, but None from Encore

Encore Capital Group has only recognized one impairment in the last six quarters, while publicly traded PRAA has realized impairments for six consecutive quarters for a total of $42 million. Even the one small ($8 million) impairment that Encore did recognize was blamed on the new CFPB rules and settlement, and not on the company overpaying or under collecting. Encore almost entirely offset the impairment by reversing $5 million of impairments on older portfolios. This CFPB-induced allowance is the only allowance charge Encore has taken since 2013 and the only allowance under current-CEO Vecchione.

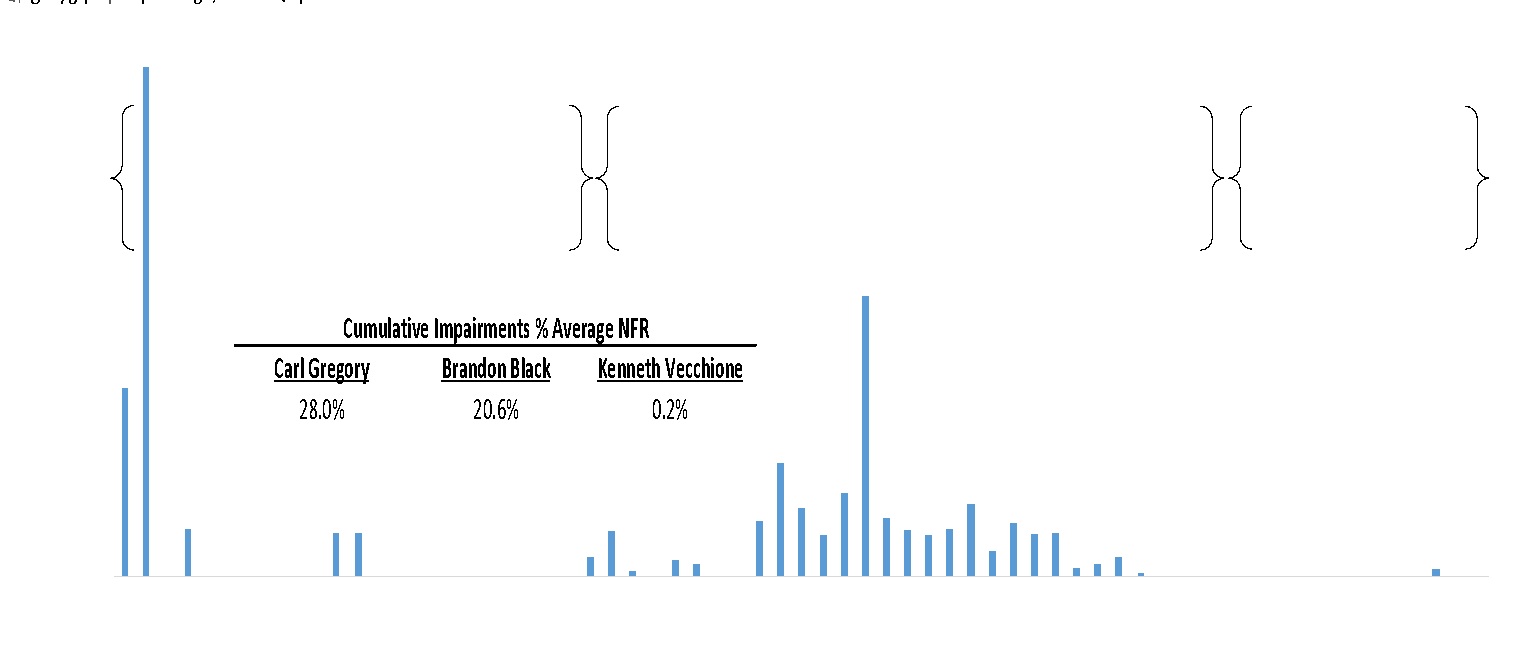

Quarters in Which Public Debt Collection Companies Have Recognized Impairments

Source: Company Reports

Mr. Vecchione Has Realized A Fraction Of Impairments Of His Predecessors

Since Mr. Vecchione became CEO, Encore Capital Group has only recognized the one CFPB-induced impairment. On the contrary, Carl Gregory (CEO from 2000-2005) and Brandon Black (CEO from 2005-2013) recognized numerous and regular impairments. The stark contrast shown in the chart below is telling as to the abrupt stop in impairments.

There Has Been A Clear Change In The Pace Of Impairments Since The New CEO Took His Post

Source: Company Reports

Mr. Vacchione’s Unique Interpretation of FAS ASC 310-30 Accounting Standards

On the 1Q16 earnings call, Mr. Vacchione gave investors some insight into his own unique interpretation of FAS ASC 310-30 impairment testing. On the call, the company explained that some of their legal collections were delayed due to increased regulatory scrutiny from the CFPB. A sell-side analyst asked if the cash collections were delayed, why did the company not take an impairment charge?

‘a couple of months does not shift or put us into an impairment phase’ – Kenneth Vacchione

This response directly contrasts with the accounting literature. In a FAS ASC 310-30 White Paper, Wilary Winn Risk Management LLC wrote:

‘We note that not only is it important to estimate the amount of the future cash flows, it is also important to estimate the timing of the future cash flows. Changes to the actual or expected timing of cash flows can have a material impact on the amount and timing of accretable yield recognized as income.’

Please see the following for a link to the white paper (https://www.wilwinn.com/assets/documents/fas-asc-310-30-loan-accounting-white-paper.pdf)

A ‘couple month delay’ could seem small or immaterial, however crunching the numbers reveals even a two-month delay can be material to results given that portfolios are valued at such high IRRs (Internal Rate of Return). I estimate that just a two-month delay in legal collections, all other factors being equal, should have resulted in a 6% impairment to the legal collection cash flow stream. Taking into account that 43% of Encore’s total collections are from the legal channel, I estimate an impairment of $26 million should have been recognized in 1Q16 results.

Encore’s Long-Time Chief Financial Officer Resigned

Paul Grinberg, Encore’s Chief Financial Officer since May 2015 oversaw much of Encore’s rebuilding in the prior decade. In October 2014, just over a year after Mr. Vecchione started with the company, Mr. Grinberg announced he would be resigning his post. Maybe this is just coincidence, but the timing should warrant attention.

Are Impairments Being Avoided to Satisfy Wall Street?

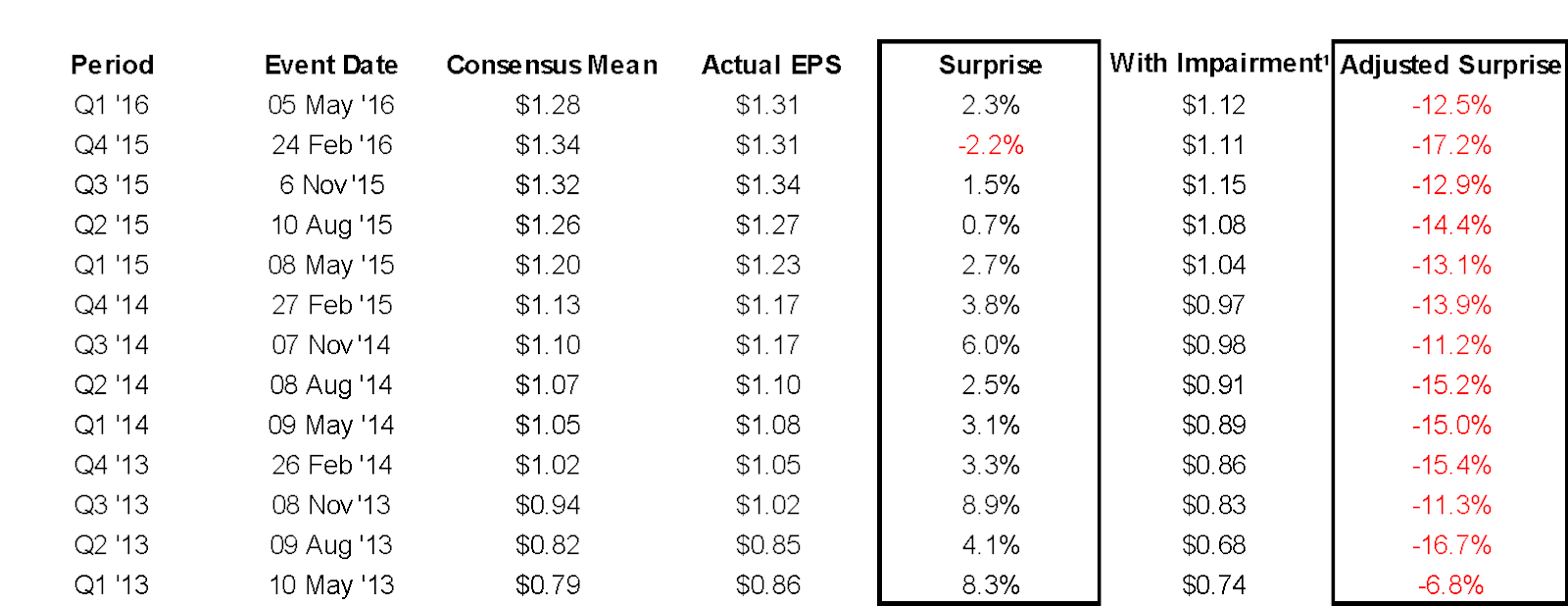

I see the push out of impairments as a result of management’s desire to beat earnings estimates set by Wall Street analysts. Under Mr. Vacchione, Encore has beat estimates every quarter except for 4Q15. However, if Encore realized impairments similar to PRA Group (0.2% impairment of net finance receivable per quarter), Encore would have missed every quarter.

Encore Capital Group Has Consistently Beat Earnings Estimates, Aided by Not Realizing Impairments

¹I adjust earnings result to account for $5M impairment, which would equate to a 0.2% impairment as a percentage of net finance receivable. This is roughly the average impairment as a percentage net finance receivable for PRA Group during the same time period.

Source: Company Reports

Misaligned Incentive Plan Rewards ‘Growth At Any Price’

Encore’s Executive Officers receive cash bonuses through the “Short-Term Incentive” program. This program solely targets increases in “Adjusted EBITDA”, a financial metric that adds back depreciation and amortization, including the amortization of all portfolios – those purchased in company acquisitions as well as those purchase as part of normal operations. The problem with using this metric is that it only rewards cash collections without considering the purchase price paid to generate these collections. As an example, Encore could spend $200 to purchase a portfolio that only generates $100 of cash collections and still report positive adjusted EBITDA despite the portfolio generating a financial and economic loss. This type of misaligned incentive plan gives Encore’s executives incentive to make uneconomic decisions and to purchase more and more portfolios regardless of price – the exact formula that has led to financial ruin in the debt collection industry.

Europe 2014 and 2015 Pools Have Similar Concerns

Encore Capital Group has made similarly aggressive assumptions with the Europe 2014 and 2015 pools – collection forecasts that do not match past experience. Cash collections are averaging a 17% decline on a year over year basis, but for accounting purposes, management projects only a 2% average decline in 2017. Focusing in on the Europe 2014 pool, management expects cash collections to go from a 24% decline to only a 3% decline, before returning to a 10% decline. As long as management is able to make aggressive forecasts in the future, they avoid taking an impairment today.

Management Is Projecting A 3% Decline In Europe 2014 And 2015 Collections Despite Actual Experience of A 17% Decline

Source: Company Reports

Note: 2016 has 1Q16 actual cash collections + remainder of year’s accounting assumption as shown in 10Q

Europe 2014 Pool Shows Extremely Aggressive Improvement

Source: Company Reports

Other Geography Portfolio Recognized More Revenue Than Received In Cash Collections

The expansion into Latin America spearheaded by Mr. Vecchione has shown a similar case study to the European experience. Cash collections have underperformed while management maintained optimistic forward assumptions. As shown below, the Other Geography portfolio has recognized more revenue than it received in cash collections, resulting in negative amortization.

The Other Geography Has Actually Recognized More Revenue Than Cash Collections…

¹Unamortized balance at 3/31/16 divided by amortization in 1Q16 multiplied by 4.

Source: Company Reports

…The Result of Aggressive Forecasts Is Negative Amortization

Source: Company Reports

Appendix

Please see a link to the OCC guidance:

http://www.occ.gov/news-issuances/congressional-testimony/2013/pub-test-2013-116-oral.pdf

Please see a link to the CFPB bulletin:

http://files.consumerfinance.gov/f/201307_cfpb_bulletin_unfair-deceptive-abusive-practices.pdf

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

Impairment charges coming.

| 2 show sort by |