| 2018 | 2019 | ||||||

| Price: | 0.12 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 628 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 104 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 0 | EBIT | 0 | 0 | |||

| TEV (in $M): | 50 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- None found

- BETA

- Neose Technologies NTEC 12/15/2005

- BV FINANCIAL INC BVFL 11/06/2023

- UNICREDIT SPA UCG IM 02/02/2023

- BayCom BCML 06/16/2019

- Axis Bank AXSB 01/26/2022

- RICHMOND MUTUAL BANCO INC RMBI 02/24/2022

- BANK OF IRELAND GROUP PLC BKRIF 12/08/2021

- DaVita DVA 10/28/2001

- CBB Bancorp CBBI 05/26/2019

- OTTAWA BANCORP INC OTTW 02/27/2020

Description

Link to the PDF of this write-up: https://www.dropbox.com/sh/riff0a0mpjktltv/AACwvO8qOtQUVMHbzJxWNwV_a?dl=0

I. Investment Thesis

· Overview: Correspondent banking has been used as the principle method for cross-border payments since the 1970’s. However, this network is slow, expensive, non-transparent, unpredictable, and error-prone. Earthport (EPO) offers an alternative network that is not burdened by the problems that plague correspondent banking. Through a single API, clients connect to a hub-and-spoke payment network capable of delivering payments to practically every bank in the world. A strong balance sheet, an open-ended growth opportunity, a blue-chip client base, and a strong competitive position create a compelling value proposition for a company trading at less than 1X EV/NTM Sales and 0.4x Mkt Cap/Invested Capital. We believe that EPO has an upside of 150-275% of over next 12-months based on an EV/Sales multiple of 3-5x.

· Strong Value Proposition to Customers:

Payment Network

1) Expansive global reach (190+ countries) with a growing network of local delivery capabilities (65+ countries); 2) EPO delivers global payments faster, cheaper, more transparently, and with greater accuracy than correspondent banking; 3) Clients access an evolving suite of best of breed payment options and service capabilities (i.e. blockchain, real time payments etc…), making it unnecessary for clients to place a large capital bet on a specific technology.

Compliance-as-a-Service Asset

1) EPO’s deep expertise in local country regulation creates an extensive compliance network, which a client can utilize upon integration; 2) EPO’s compliance network allows clients to minimize the time, money, expertise and resources it takes to be able to adhere to the complex, multiple layers of regulations in both the originating and receiving markets.

· Large Addressable Market: EPO should be able to capitalize on a large market opportunity. Management estimates an addressable market of approximately $2 trillion in annual flows of low monetary value, cross-border payments, equating to approximately 3 billion non-cash transactions. This amounts to a $9-$13B revenue opportunity for EPO. Currently, EPO only comprises 0.6% of an addressable market that is growing at a 10% CAGR globally, 17% in emerging markets.

· Tier 1 Client Base Has Validated EPO’s Technology: EPO has a Tier 1 client roster of large banks, money transfer organizations (MTO’s), e-commerce companies, and payment aggregators. These large clients are expanding their utilization of EPO’s platform from initial, small volume pilot projects to mainstream, higher volume payment products (e.g. Bank of America CashPro).

· EPO’s Growth Will Accelerate: We believe that EPO’s growth had been capital constrained; however, a £25M equity raise in October 2017 should provide EPO with the sufficient capital to re-accelerate growth. EPO’s above market growth will be driven by: 1) Growth within its existing customer base; 2) Expansion of EPO’s local payment network (65+ countries currently, 86 countries by Feb. 2018); 3) Growth within the e-commerce sector; 4) Addition of new clients; and 5) Expansion of product offerings.

· Short Term Missteps and Blockchain Misunderstanding Don’t Diminish Long Term Opportunity: EPO’s shares have dropped 40% from the price of its October equity raise (£0.20). We attribute this to the recent news relating to 1) management changes, 2) operational hiccups, and 3) fears that blockchain payments will disintermediate EPO’s business model. Despite these concerns, we believe the long-term investment thesis is still intact. Although blockchain fundamentally makes payments faster and cheaper, it does not reduce regulatory complexity, which is by far the most complex aspect of a cross-border payment. In other words, blockchain, unaccompanied by additional regulatory/compliance technology, is not a full stack payment solution. Ripple’s partnership with EPO highlights this distinction. EPO’s compliance-as-a-service functionality has a significant cost and barrier to entry, making EPO’s distributed ledger hub one of the few public ways to invest in blockchain.

· Mispriced Stock Price Creates Value for Investors: At EPO’s current price of £0.12, we believe shares have significant upside. EPO has no debt and should not require additional equity capital, yet its current trading multiple of <1x NTM EV/Sales is indicative of a company in distress, not one that has a long runway for growth. Financial payment companies trade at EV/Sales multiples between 1x-14x. Assuming an EV/Sales multiples at the lower quartile of the range (3x), despite a growth profile in the upper quartile, implies a value of £0.31 (150% upside). Even assuming a median EV/Sales multiple (5x) implies a value of £0.45 (275% upside).

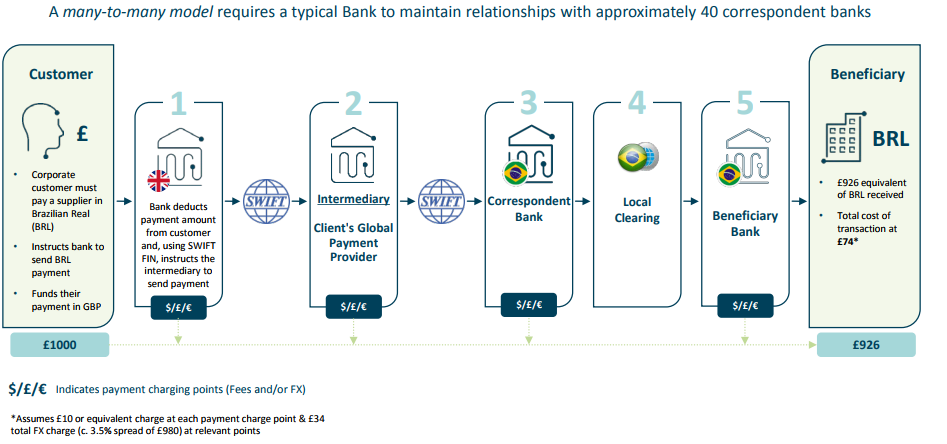

Figure 1-Example of how the correspondent banking system works

II. Correspondent Banking Model vs. EPO’s Hub and Spoke Model

Correspondent banking (Figure 1) - in which one financial institution carries out transactions on behalf of another, often because it has no local presence - has been used as the instrument for cross-border payments for decades. There are many disadvantages to the traditional correspondent banking system:

· Potentially many links with accumulating fees.

o A 2015 McKinsey survey on consumer cross-border payments found that consumers typically pay a fee of €20 to €60 on top of the prevailing foreign-exchange spread for a payment that took three to five working days to complete.

· Limited transparency on cost and delivery time for all parties.

· Delays in settlement and deposit along with potential rejection.

o A 2015 study by Traxpay indicates that about 60 percent of business-to-business (B2B) payments require manual intervention, each taking at least 15 to 20 minutes.

o Major variations in account structures, messaging, and bank systems generate far more corrections, investigations, returns and stalled payments than are seen in domestic payments or in payments where one party controls the transaction from beginning to end.

· Final amount reaching the beneficiary is unpredictable.

· Multi-faceted compliance requirements.

As margins for domestic payments were squeezed by regulation and competition in recent decades, banks were forced to pare back costs and improve the efficiency of their systems and products. Historically, cross-border payments have not experienced such pressures, so banks have had little incentive to work on their back-end systems/processes or to develop innovative customer offerings. However, the traditional correspondent banking model for cross-border payments has come under acute pressure from customers, regulators and competitors alike:

· Customer expectations for real-time, digitally enabled cross-border payments are growing as domestic retail payments undergo rapid digitization.

· Regulatory compliance is driving up the cost of cross-border payments systems and forcing banks to review their correspondent relations. Leading transaction banks can no longer afford to maintain large international correspondent bank networks and have been closing less profitable corridors.

· Digital innovators are attracting customers with new solutions and enhanced value propositions that threaten not only to cut banks out of their correspondent banking relationships, but also to loosen banks’ ties with end customers, at least where payments-related activities are concerned.

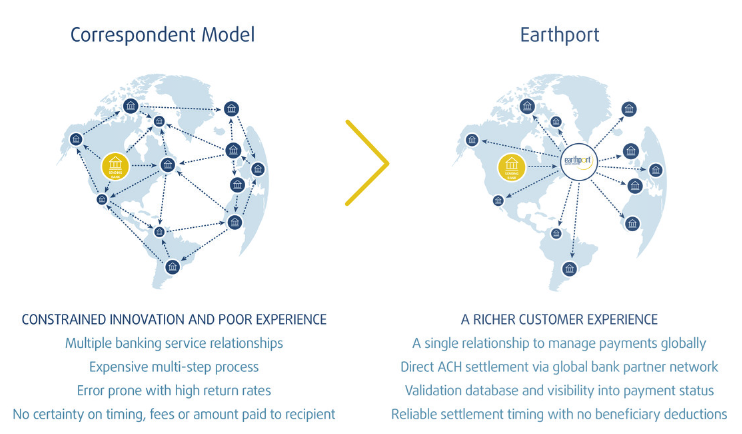

Figure 2-EPO's Hub and Spoke Model vs. The Correspondent Banking Model

III. EPO’s Model Delivers Significant Benefits to Clients

The problems that plague correspondent banking make it unfit for high volume, low value payments. At first glance, the inefficiencies with the correspondent banking network may appear technology related; however, technology is very far down on the stack of complexities that cause these problems. The main problem is regulation, data, and the number of links in the chain. Instead of a many-to-many model, EPO is a many-to-one model (Figure 2). EPO’s portfolio of technology and intellectual property facilitates high volumes of cross-border payments outside of the SWIFT correspondent banking model. EPO’s network of segregated trust accounts is linked to its processing platform, validation database, and compliance infrastructure, creating a white-labeled, central clearing platform. Through a single relationship with EPO, clients can make payments to almost any bank account in the world; therein, reducing costs, payment time, and complexity while meeting expectations of transparency and compliance. By removing the middlemen, EPO’s streamlined model delivers significant, quantifiable benefits to its clients:

Expansive Geographic Reach

· Access to deep expertise on local payment infrastructure and regulation in 65+ markets (87 by February 2018). An average large bank will have 40 countries covered by its correspondent banking network.

o In FY 2017, EPO executed payments across 193 destination countries and in 49 currencies.

· EPO has the largest ACH network in the world.

· Advisory services designed to assist clients with new market entry and new product development.

Significant Economic Gains

· Reduces the cost of banking relationships. Relationship management of ‘in-territory’ banking services across EPO’s local payment network is done by EPO.

· Lower cost of payment with reduced operational overhead.

o EPO’s revenue per transaction, which includes a transaction fee ($2-5/transaction depending on payment corridor) and FX spread revenue (25-100BPS), was £2.63 in 2017, which equated to 0.2% of the size of the average transaction (compared to upwards of 3.0%, not including FX fee, for the correspondent banking network).

· FX offering that complements clients’ own currency capabilities and provides new revenue opportunities.

o FX and treasury capabilities ensure that the clients have a broad currency offering to support major and minor currencies, with flexible funding options and liquidity management.

o Potentially greater FX benefits through aggregation.

· Material reduction in transaction repair costs.

o > 99% delivery of payments first time, without repair in FY 2017 (compared to the 12.7% error rate in correspondent banking).

o Lower cost of failure, with a reduced repair rate.

· Reduced operational overhead and elimination of redundant capital investments by clients.

Improved Operating Efficiencies

· A single service relationship with dedicated client management.

· Significantly increased Straight-through-processing (STP).

o 99.5% straight through processing rate in FY 2017.

o Optimized routing for price and speed. Access to Expedited, Faster and Real Time Payment channels.

· Reliability of receipt of beneficiary funds via local clearing model.

· EPO’s payments processing platform continues to perform at a 99.9% “up-time” rate, ensuring virtually uninterrupted service for clients.

· Major improvement in reporting, reconciliation volume, and speed.

Customer Satisfaction

· 100% of the principal payment value delivered to the beneficiary without deductions. (In the correspondent system, the final value delivered to the recipient is not known when the payment is initiated)

· Full transparency into settlement timing together with end to end payment tracking capability. (Correspondent system is not transparent or traceable)

· Reduced customer requests for tracking and exception handling, reducing the need for expensive reconciliation processes.

Ease of Adaptation and Integration

· Flexible options for connectivity including SWIFT, API and file-based solution.·· · Speed to market with low-touch integration.

· Expert project management support during implementation.

· Intelligent message transformation and validation capability.

o Capability to manage legacy, emerging, and proprietary message formats.

Secure and Compliant

· EPO’s deep expertise in local country regulation creates an extensive compliance network, and serves as compliance-as-a-service functionality for clients. Since clients do not need to replicate each link individually, EPO allows clients to minimize the time, money, expertise and resources it takes to adhere to the complex, multiple layers of regulations necessary in both the originating and receiving markets.

o Robust compliance operation: Anti-Money Laundering (AML)/Counter Terrorist Financing (CTF), Anti-Bribery and Corruption (ABC) sanctions screening, Customer Due Diligence (CDD)/Know Your Customer (KYC), data protection, and fraud protection.

o Reduces regulatory exposure at receiving and originating banks by flagging payments as fraud.

o Banks must do KYC on each connection and compliance refresh yearly. EPO does this for the client.

o Aside from the robust physical network, EPO’s core expertise is in regulation and data. Skilled in the technical and regulatory requirements for international payments around the world, EPO adopts a combination of licensing, registration, partnerships and physical presence designed for compliant and successful payments.

o 60-70% of the complexity of a global payment lies in regulatory compliance, stemming from the fact that regulation in every country in the world is different.

o EPO’s validation database is a core asset. EPO keeps a large, continually updating database covering all the relevant banking regulations, procedures and conventions in all the countries in which it operates. This database allows the group to validate over 99% of payments in real-time, eliminating the high error rate in the correspondent system.

· Fully funded segregated account structure to safeguard client funds.

o Results in no credit or counterparty risk.

· Accredited security controls.

o EPO is authorized and regulated by the FCA under the Payment Service Regulations 2009 for the provision of payment services, a SWIFT member and ISO 27001 compliant.

Figure 3-EPO gives clients access to an evolving suite of settlement options

Future-Proofed Technology

· Seamless access to an evolving suite of payment options and service capabilities (Figure 3)

o A broad spectrum of emerging technologies is supported on EPO’s network, with a focus on distributed ledger and other alternative payment channels (e.g. mobile wallets).

o As customer and market requirements change, EPO allows clients to flexibly and frictionlessly adapt.

· EPO’s expertise on new payment innovations supports product development of clients.

IV. Markets

EPO’s benefits are most acute in the low value, high volume payment space. These payments may be B2B, B2C, C2B, or C2C, but must be digital payments. EPO’s services support established use cases such as corporate pension and payroll disbursements; accounts payables; trade related payments; expense disbursements; royalty payments; peer to peer payments; global remittances; card schemes; and merchant settlements. EPO has a target market of approximately $2 trillion dollars in annual flows of low monetary value, cross-border payments. This opportunity can be decomposed into the following buckets:

· Remittances: $663B

· Direct / Retail E-Commerce: $538B

· Commercial Trade: $450B

· P2P & Social Payments: $240B

· Emerging Economy Marketplaces: $117B

· Other Emerging Payments: $27B

This TAM equates to approximately 3 billion non-cash transactions, implying an average transaction size of $667. Assuming revenue /transaction stays in line with management’s long-term targets of £2.25-£3.25/ transaction ($3.12-$4.50 at current exchange rate $1.38/£), this equates to a $9-13B revenue opportunity. This implies a transaction cost (i.e. infrastructure cost) of 0.5% to 0.7% of the average transaction size. This target market, as measured by non-cash transactions, is growing at an estimated CAGR of around 10% globally and 17% in emerging markets.This growth can be attributed to: the rise of e-commerce; dislocation in the banking industry; de-risking and reduction of global footprint of banks; and accelerating demand in emerging markets.

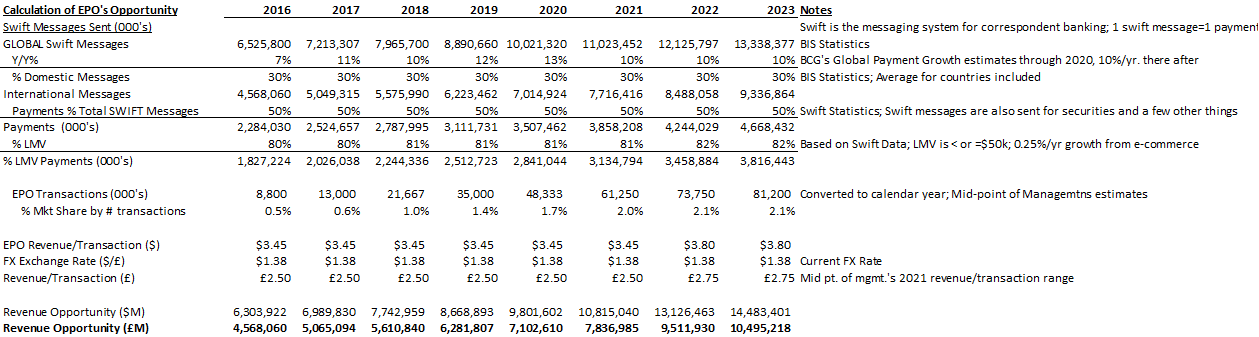

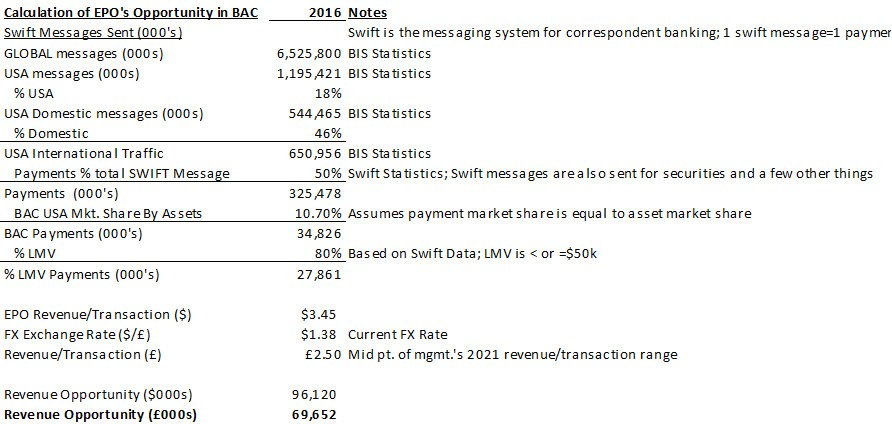

Figure 4-Estimate of EPO’s market share using SWIFT data

We supplement management's estimates with a bottom-up estimate based on swift messaging volumes (Figure 4). SWIFT messages are the payment messages in the correspondent banking system. Based on this analysis, EPO only has 0.6% market share by payment volumes of a market in 2017. We note that to get to the midpoint of management’s 2023 estimate, they only need to reach 2.1% market share. Given the benefits of EPO’s platform, we believe this is attainable.

V. Existing EPO Clients

Investments made over the past year have further cemented EPO’s position as the leading cross-border payment solutions provider. EPO serves 6 of the top 25 global banks, most major MTOs, and major e-commerce companies.

Banks: Rapid advances in technology combined with significant shifts in consumer behavior are transforming the payments landscape within banks and financial institutions. To confront new and non-traditional threats, these institutions are seeking faster payment solutions to avoid becoming disadvantaged. Major banking customers are looking for solutions that decrease regulatory and operational costs without reducing geographic reach.

· Bank of America (2nd largest bank in USA, 9th largest bank in the world):

o Announcement: 12/2016

o Scope: Payments via CashPro to 60 Countries and in 22 Currencies

· HSBC (largest bank in England; 5th largest bank in the world):

o Announcement: 5/2014

o Scope: Expand the coverage of its Global Disbursements™ product across countries in Central and Eastern Europe, and the Asia Pacific region

· Japan Post Bank (Japan’s largest consumer bank and 12th largest bank in the world):

o Announcement: 9/2015

o Scope: Cross-border consumer remittances

· Santander (largest bank Spain, 19th largest bank in the world):

o 1st Announcement: 1/2015

o Scope: International payment services

o 2nd Announcement: 11/2016

o Scope: Blockchain/distributed ledger technology for international payments using Ripple

· Standard Chartered (5th largest bank in England, 49th largest bank in the world):

o Announcement: 12/2014

o Scope: International Automated Clearing House (IACH) coverage in Asia, Africa and Middle East.

· DBS Bank (largest bank in Singapore, 74th largest bank in the world):

o Announcement: 10/2016

o Scope: Cross-border transactions in Asian markets

· Axis Bank (3rd largest private bank in India):

o Announcement: 2/2017

o Scope: Remittances

· Kotak Mahindra Bank (3rd largest private bank in India):

o Announcement: 8/2017

o Scope: Cross-border payment capabilities across all transaction types between India and the US, UK, Europe, Canada and Singapore

· Others: IFC World Bank; CIBC (Canada), PNC (USA); Citizens Bank (USA);

E-commerce: EPO enables online and digital E-commerce providers, including merchant acquirers and payment gateways to handle large volumes of cross-border consumer and corporate payments efficiently and transparently through a single connection. E-commerce companies often need a more effective means to quickly and transparently pay the proceeds of high volume sales to suppliers and global sub-merchants on a frequent, recurring and often, daily basis. This becomes a critical operation to realize their e-commerce marketplace economic model. Known customers:

· AirBnB – via a reseller – the largest shared economy global lodging business.

· Stripe – direct – one of the fastest growing e-commerce payments platform enabling websites

· Amazon – via a reseller

· Uber – via a reseller across a range of markets

· Hyperwallet

Traditional and Emerging MTO’s: Through EPO, money transfer companies can now offer more competitive, lower cost global online remittance products all through a single commercial and technical integration. EPO clients have found they can deploy new products quickly and scale their business into new markets, allowing them to focus on brand and customer service while leaving the infrastructure in the background. Known customers:

· TransferWise

· Stripe

· World Remit

· RIA

· XOOM (Purchased by Paypal)

· The FX Firm

· Skrill

· Azimo

· Western Union

· MoneyGram

Payment Aggregators: Companies providing banking software solutions and wholesale financial services benefit from integrating EPO into their service offering. EPO’s white-label service seamlessly enables these payment aggregators to offer more competitive services, generate new sources of revenue, and enhance client retention. Known customers:

· Skrill

· IBM

· Tipalti

· UNFCU

· Fiserv

VI. Validation of EPO’s Model within Tier 1 Clients

Clients typically test EPO on a non-core payment product. Once clients validate the technology, they expand utilization to additional payment products, which tend to be more mainstream, higher volume products. Consequently, the shape of the growth curve within an existing client can be characterized by a shallower growth trajectory initially, followed by exponential growth after validation.

Within EPO’s existing customer base, we believe EPO’s network has moved past the initial validation stage within the banking and payments industry. Existing clients are looking to increase volumes and new clients are piloting larger projects then had previous clients. We believe that the key validation event was Bank of America broadening its strategic relationship with EPO by expanding the its scope of service on CashPro®, adding numerous new countries and currencies to the bank's online and file based banking portal. Clients can now make payments via CashPro to 60 countries and in 22 currencies. They key takeaway is that penetration within existing customers is small, but we believe that market share within existing customers is poised to inflect upwards near-term.

VII. Competitors

To understand the competitive set, we must understand the difference between front-end companies, which are user acquirers, and back-end companies, which provide the payment infrastructure to front-end companies. Front-end companies, such as PayPal, Worldpay, Stripe, Skrill, or Transferwise, have a business model that revolves around user interface and user acquisition. While revenue models vary, they can be split into two categories 1) fixed or variable fee per transaction, which may or may not include a FX conversion fee and 2) no transaction fee, but revenue generated from the FX conversion fee, the float, or both. Importantly for EPO, these players are not trying to reform the back-end infrastructure and are therefore not competitors. In fact, in many cases these front-end players are clients of EPO because they recognize the EPO’s advantage over correspondent banking and are open to new technology solutions.

EPO does not have many direct competitors beyond correspondent banking on the back-end. Bancomer Transfer Services (BTS) and CurrencyCloud have been cited as competitors.

- BTS, which is part of BBVA, is a competitor in Latin America. EPO didn’t focus on Latin America initially, but is picking up market share there. BTS takes balance sheet risk, but EPO’s regulatory and compliance is better. We note that WorldRemit use both EPO and Bancomer Transfer Services, largely because of legacy relationships within specific corridors.

- CurrencyCloud delivers liquidity though SWIFT. It is closer to currency trading platform than a full stack payments solution. At one time, CurrencyCloud was an EPO client, but was offloaded because of regulatory and compliance concerns.

We also note that a lot of money is flowing into the blockchain payment space. However, we believe that the market has a misguided view that blockchain will disintermediate EPO’s business model in the global payments ecosystem. A global payment can be broken down into four main components: 1) messaging 2) regulatory 3) settlement/liquidity management 4) operational. By EPO’s managements estimates, 60-70% of the complexity of a global payment is regulatory, with the remainder split as follows: 10% is messaging, 10-20% is settlement/liquidity, 10% is operational. In theory, the long-term benefit of blockchain is that the messaging is always “synchronized” on both ends rather than being updated independently, thus there should not be any reconciliation issues. Distributed payments technologies are fundamentally changing how payments work in terms of speed, reach, security and cost-efficiency; however, blockchain doesn’t change the regulatory complexities of a global payment. The regulatory complexity grows exponentially for each new country to which an institution wants to send and receive payments. This uniquely positions EPO as a 3rd party compliance-as-a-service asset to institutions sending and receiving payments. EPO’s deep expertise in local regulatory laws represent both a barrier to entry and to disintermediation. This is one of the principle reasons why Ripple partnered with EPO. In January 2018, both Western Union and MoneyGram formed strategic partnership with distributed ledger fintech Ripple to pilot XRP technology in cross-border transactions. We believe it is more than likely that transactions that are using the XRP technology of Ripple would also involve EPO. If true, we believe this further validates EPO’s model.

The regulation barrier aside, a disintermediation by blockchain would involve a standardized blockchain protocol between all sending and receiving institutions. We view this as very unlikely. Rather, we believe that many different blockchain protocols may prevail. Winners and losers will be dependent on use case and geography. The number of different cryptocurrencies, which all use different blockchain protocols, that emerged over the past few years highlight the diversity and number of blockchain protocols that were created in a relatively short period of time. We believe that EPO’s distributed ledger hub will be a beneficiary of divergent blockchain protocols, given a payment can only be sent via a specific blockchain protocol if the receiver is set up to handle such a transaction (i.e. a bank only set up to receive Ripple will not be able to receive Ethereum or Hyperledger). Given the highly conservative/legacy nature of banks, we believe they will be less inclined to integrate many specific blockchains, but rather opt for a solution, such as EPO’s, which assembles best of breed solutions. We believe that EPO will announce partnerships with additional blockchain protocols (Ethereum, R3, Hyperledger etc.…) as demand dictates. This is the main reason why we believe that EPO’s distributed ledger hub has “future proofed” its business model and makes EPO’s distributed ledger hub one of the few public ways to invest in blockchain.

VIII. Growth Strategy

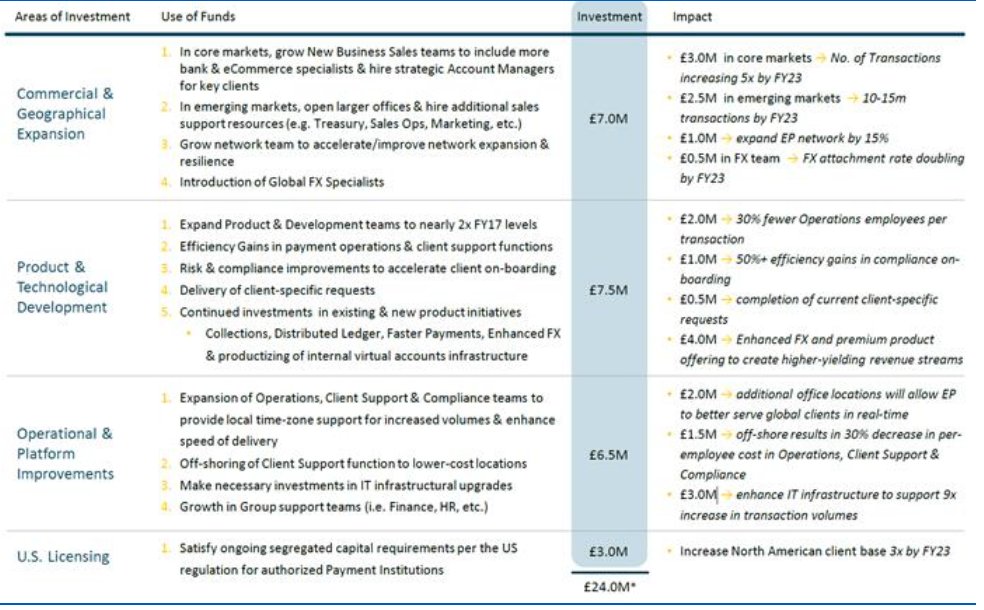

Currently EPO’s transaction mix is roughly 40% MTO’s, 20-30%, and e-commerce 20-30% banks. However, management believes growth opportunities are largest in large global banks, e-commerce and EM banks, in that order. As of June 2017, a total of 143 new opportunities, inclusive of existing and new clients, are currently in the commercial pipeline. The weighted and unweighted new business pipeline for FY2019 (ending: June 2019) is already over 2 times that of FY2018 (ending: June 2018) and continues to grow. Prior to the equity raise, we believe that EPO had been capital constrained and slow to take advantage of new opportunities in its’ pipeline. Converting leads and integrating client wins is time and resource-intensive, particularly with regards to integrating EPO’s significant compliance capabilities. The £25M of new equity that EPO raised in October 2017 should accelerate EPO’s growth profile. Figure 5 summarizes the uses of the proceeds:

Figure 5-EPO’s intended uses for equity raise proceeds

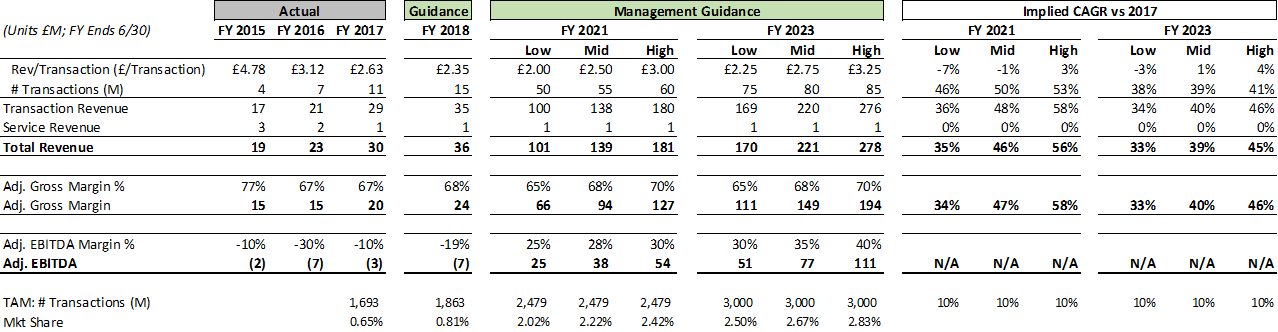

· Expansion Within Current Customers: 90% of the revenue growth in FY 2017 was driven by the existing client base; however, EPO’s penetration within existing clients is still very small and the volumetric opportunity within existing customers is very large. We estimate that EPO’s cross-border payment opportunity within Bank of America is 27M transactions worth £70M (Figure 6). To put this potential into better perspective, we estimate that in FY 2018 EPO will do 14M transactions and £36 in revenue. Now that EPO has validated its technology within these larger institutions, we believe EPO’s volumes will expand rapidly as these institutions expand EPO usage to higher volume payment products. EPO announced that several large existing clients are seeking to expand international corridors and offerings, including a major banking client in the USA targeting over 1 million incremental transactions annually into Asia. These volumes commenced in December 2017 and will ramp up over the coming months. To fully leverage the potential from its existing clients the group plans to expand its commercial team, including strategic account managers geared specifically toward winning new business lines at key existing clients. EPO expects the number of transactions from core market to increase 5x by 2023.

Figure 6- Estimate of EPO’s addressable market within Bank of America

· New Corridors/New Geographies: EPO has 67 corridors currently in operation and will have 87 by February 2018. EPO believes that there is a strong opportunity to expand its presence in emerging markets in Asia, Africa and India as a result of its existing clients within the banking sector. In November 2016, EPO gained approval for cross-border payments from the Reserve Bank of India, effectively a regulatory seal of approval for the Indian banking system. Volumes from key investments made in India in FY 2017 will begin to ramp up in FY 2018. India is one of the worlds’ most important and fastest growing markets for cross-border payments, with $260 billion in exports and $356 billion in imports in 2016. Further, India is the largest remittance-receiving country, with an estimated $63 billion of inward remittances in 2016. Over the medium term, securing emerging market outbound volumes brings significant benefits to EPO, both in terms of improved service to clients and improved economics that accompany bi-directional flows. By 2023 EPO expects 10-15M transactions originating from EM economies on its network.

· Expansion of E-Commerce: EPO plans to further expand in the e-commerce sector in the US. Early reception has been positive. EPO is currently obtaining direct licensing in New York, California and several other states. Once obtained, the group will be able to deal with non-licensed organizations directly (as opposed to via resellers), significantly increasing its US e-commerce opportunity. E-commerce companies are desired clients for EPO given their shorter sales cycles; their high volume of low value payments; and their modern technology stack, which makes EPO’s integration faster. EPO is targeting a three-fold increase in its e-commerce US client base by 2023.

· Growth of New Clients: Growth of new clients will be driven through expansion of the sales force/geographic coverage. The lead time from investing in new or enhanced client relationships to accelerated revenue growth can be 1-2 years. New clients require a detailed technical sales process followed by rigorous testing before moving significant volumes onto the platform. EPO is targeting a 15% increase in its partner bank network, with a focus on emerging markets.

· New Products: EPO will continue to make selective investments in existing and new product initiatives that will be integrated into its core offering. These include faster payments, global receivables, distributed ledger, treasury netting, enhanced FX functionality and alias payments.

· Increase FX offering: EPO expects to double its FX attachment rate by 2023. We believe the FX attachment rate on transaction volumes is currently relatively low (sub 10%). EPO makes 25-100 BPS on FX conversion.

IX. Financial Drivers

Figure 7-EPO’s target model

· Transaction Revenue: Transaction revenue is driven by the number of transactions and revenue/transaction.

o # Transactions: We expect transactions to increase to 15M in FY 2018 and expect growth to inflect starting in FY 2019. Management guided transactions in the range of 50-60M in FY 2021 and 75-85M in 2023.

o Revenue/Transaction: Revenue/transaction has fallen from £3.12 in FY 2016 to £2.63 in FY2017, stemming from a larger mix of transactions in developed corridors and a larger mix of e-commerce transactions. Notably, EPO management said they haven’t seen pricing compression in existing corridors on a like for like basis. While revenue/transaction will likely continue to fall in FY 2018, management believes that it will begin to rebound as EM corridors make up a higher percentage of transactions, FX attachment rate increases, and customers take advantage of new revenue streams. Partially mitigating these increases, e-commerce will continue to increase as a percentage of transaction mix. Management guided to a revenue/ transaction range of £2.00-3.00 in FY 2021 and £2.25-3.25 in 2023.

· Professional Service Revenue: EPO earns service revenue for assisting banks with the integration of the clients’ system and EPO’s API. We believe EPO has been subsidizing integration revenue as opposed to making it a profit center, consequently we expect service revenue to remain a small part of overall revenue going forward.

· Gross Margins: GM have been historically stable. Management expects gross margins to range between 65-70%.

· EBITDA margin: Networks, such as EPO, inherently have a high degree of operating leverage. Networks are about scale. They tend to have relatively fixed costs, so driving additional volumes creates even greater cash flow. For reference, we point out that V and MA have EBITDA margins of 70% and 58% respectively. EPO plans to invest in increased automation of payment operations, client support functions and risk/compliance functions. This will allow the group to scale successfully and reduce the operations and compliance proportion of overall admin costs. EPO’s target operating model also includes moving some client support functions to lower cost locations. Management believes it can achieve a 30% decrease in per-employee cost in these locations. EPO’s target margins (FY 2021: 25-30%; FY 2023: 30-40%) imply incremental margins of only 40-60%.

· Capex: Management has suggested that capex will eventually drop to 7-10% of revenues after increased levels of investment in FY2018/2019.

· Tax: EPO has a NOL of £112M. We assume post-NOL usage the cash tax rate is 20%.

· Other: EPO expects to be CF breakeven during FY 2019 (run-rate for H2 2019).

X. Why has the stock declined?

We attribute the stock decline to the recent news concerning 1) operational hiccups 2) management changes and 3) fears that blockchain payments will disintermediate EPO’s business model. Only two months after completing a £25M equity raise in October 2017, EPO announced a downward revision to FY 2018 guidance and management changes. Although we believe there are some short-term negatives associated with these announcements, we believe EPO’s long-term prospects have not diminished.

Operational Hiccups

· EPO warned investors that anticipated revenues are expected to be 10%-15% below current expectations for the financial year ending June 2018 ('FY2018'). This downward revision to guidance reflects several factors:

o “Delays in some expected contracts and client implementations”: Delays in contract signing, regulatory on-boarding, and completion of integration work all contributed to the overall delay. While these types of delays are unpredictable, they are a reality of doing business with banks. Management expects a 3 to 6 month delay from originally anticipated timing, but no loss in demand for EPO’s services.

· “A recent change at one existing e-commerce client has resulted in a loss of approximately 5% of 2018 projected revenues as this client changed its plans for a UK corridor for domestic. They remain a client and expect to work with EPO for other international corridors.”

o While the identity of the e-commerce company is unknown, management noted that the UK bank that will process these transactions gave the e-commerce company a line of credit, thus giving the e-commerce access to balance sheet/ immediate liquidity. The company noted that this was a one-off occurrence that is unlikely to occur in other corridors. We note that Amazon previously had accounts at banks all over world, but now uses aggregator banks to reduce the large overhead associated with these accounts.

Management Changes

· CEO, Hank Uberoi, will move to Executive Chairman to focus on strategic opportunities.

o Mr. Uberoi will continue to work full time for the company and will not seek employment elsewhere. This change allows a new CEO to focus on day to day operations while allowing Mr. Uberoi to focus on strategy/winning additional clients.

· CFO Simon Adamiyatt’s resigned due to personal reasons.

o We have no further insight into this situation other than what was released publicly.

· We think that the management change will be helpful in restoring investor confidence, and that the proceeds from the October 2017 equity raise will give the new management team sufficient capital to execute on EPO’s long-term growth plan.

Fears that blockchain payments will disintermediate EPO’s business model

· As discussed previously, we believe fears that blockchain payments will disintermediate EPO’s business model are misguided.

XI. Valuation

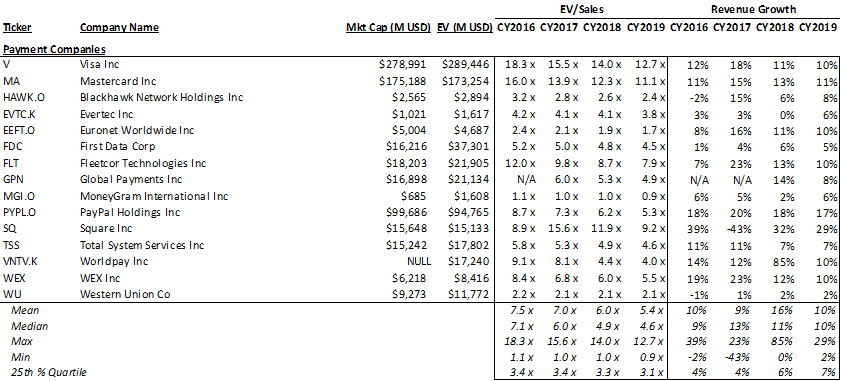

At a current price of £0.12, EPO’s shares have dropped 40% from the price of its equity raise (£0.20) in October 2017. EPO has no debt and should not require additional equity capital, yet its current trading multiple of <1x NTM EV/Sales is indicative of a company in distress, not one that has a long runway for growth. Financial platform companies trade at NTM EV/Sales multiples between 1x-14x (Figure 8).

Figure 8-Payment comps are trading at much higher EV/Sales multiples despite a lower growth profile.

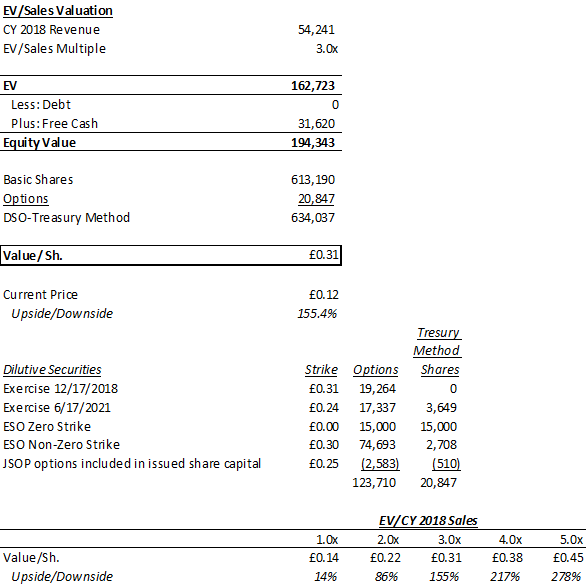

Assuming a EV/Sales multiples at the lower quartile of the range (3x), despite a growth profile in the upper quartile, implies a value of £0.31 (155% upside). Even valuing EPO at the median multiple (5x) implies a value of £0.45 (278% upside) (Figure 9).

Figure 9-Sensativity of EPO’s valuation to EV/Sales Multiple.

Since we believe managements long term targets are still achievable, we ran a DCF as a sanity check (Assumptions: WACC=12%; Terminal Growth =3%). At the midpoint management’s target, we believe EPO is worth £0.59 (388% upside). Based on any sensible valuation metric, we believe EPO is worth significantly more than where it is trading today.

XII. Catalysts and risk

Risks

· On-boarding delays in new customers

· Slower than expected ramp in transaction volumes

· Loss of key customers

· Profitability is less than projected

I and/or others I advise do not hold a material investment in the issuer's securities.

Catalyst

Catalysts

· Successful ramp-up in transaction volumes from growth initiatives

· Further expansion of local delivery network beyond announced geographies

· Increased FX attachment rate and faster adoption of new products by customers

· Wining business of additional Tier 1 customers

· Acquisition by larger player in the payment industry

| show sort by |