Description

Thesis

Evans & Sutherland (OTC: ESCC, “ESCC”) is a capital-light, market-leading business that produces high-quality advanced visual display systems used primarily in full-dome video projection applications. We believe ESCC, at the current valuation, presents a compelling long-term investment opportunity. Our investment thesis is:

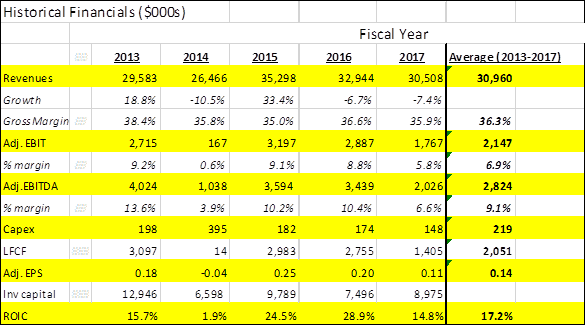

(1) ESCC is more profitable than it appears historically: historical financials before 2016 were plagued with pension troubles and structurally higher corporate overhead. The company has restructured the pension and reduced its corporate expenses and will therefore be highly cash-generative going forward.

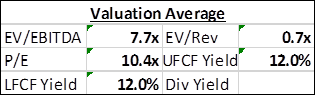

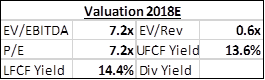

(2) ESCC is cheap: ESCC today trades at, on an average 5-year-proforma-basis, ~10x P/E and a ~12% LFCF yield. On next year’s numbers, ESCC trades at an absurd 7.2x P/E and 14.4% LFCF yield. ESCC has historically been a 15%+ ROIC business.

(3) A direct competitor, Sky-Skan, has entered bankruptcy proceedings: this potentially creates a sizeable opportunity for ESCC to increase its sales by 15%+.

(4) Hidden value: The company has real estate worth ~$4M, or almost 25% of the current market cap.

Note: this idea may be more suitable for smaller funds and personal accounts.

Business Description

Advanced visual display systems (~70% of revenues): If you’ve ever stepped into your city planetarium or science center and have experienced what it’s like navigating through the icy rings of Saturn, there is a good chance that ESCC is behind it. ESCC is behind the software (the Digistar software + show content) and hardware (projectors + domes) that produce the immersive dome experiences in planetariums, schools, science centers, and other educational/entertainment venues. Our primary research indicates that their hardware + software are unrivaled in quality, performance, service, and reliability. The view is that for any planetarium or exhibit, the immersive dome experience is required. The dome experience for the visitor needs to be best-of-class, and for the planetarium, they need unrivaled long-term support, technical expertise, and service to create it. ESCC’s software + hardware are made for these requirements, and claim a technical superiority that has given them a high degree of customer loyalty and a commanding 50%+ market share.

The reason is as follows: these are long-term, expensive projects for the museums (as a % of budget). If they spend upwards of $100k to almost $2-3M for a planetarium project, they want the best possible solution and support. The source of these funds is fundraising. These exhibits can last for almost a year or more, so they want to make sure they have the best and most reputable partner helping them. They also want to know that their partner will exist for the long-term because they need continual support and service. In fact, ESCC is the pioneer of this field and has been around for 50 years now, and has built up a well-regarded reputation. This is advantageous because customers tend to go back to ESCC for new planetarium projects. ESCC sells to planetariums in the US (50%) and international (50%).

ESCC primarily charges for the software (with optional show content) + hardware (projectors), and the metal dome and sells direct to its customers. Customers also have a service contract lasting multiple years, which is a smaller (yet recurring) component of the sale.

Domed Structures (~30% of revenues): A smaller portion of ESCC’s business is the sale of metal domes to theme parks, casinos, and museums. These are custom-built domes for the customers. ESCC acquires its healthy margin by customizing the metal structure to specification. Most of ESCC’s sales are to theme parks, where the metal domes are simply part of larger structures. Management estimates they’re the dominant player in this space with one other smaller competitor.

Valuation

Without going into too much detail, ESCC restructured its Pension during 2015 because of the massive burden it placed on its financials. 2016 was the first “clean” year without the burden of massive interest costs and pension expense of the Pension. ESCC will not be a cash tax-payer for the foreseeable future due to a massive NOL ($169M federal, $70M state) and has minimal capex requirements ($100k-$200k/year). We went back and generated 5 years of pro-forma financials assuming normalized pension interest costs and expense:

In other words—looking past the fact that ESCC is lumpy—ESCC is a ~$30M+ revenue, ~9% EBITDA margin business. On this average basis alone, ESCC trades for:

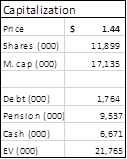

Note that cash includes cash & cash equivalents, restricted cash, and lease receivables (since this is cash owed to them for a one-time event).

The current backlog and forward sales are highly correlated as we show below. Using this relationship, we forecast 2018E revenues and EBITDA:

Based on 2018E revenue and ~9% EBITDA margins, ESCC trades for:

ESCC owns a 47,000 square-foot building on approximately 15.2 acres in Chadds Ford, Pennsylvania. This is worth ~$4M, and is used for office space for ESCC employees.

At first glance leverage may be a concern, but this shouldn’t be of any worry: ESCC has only ~$1.8M of actual bank debt and the Pennsylvania property it owns serves as collateral under debt agreements. The ample free cash flow ESCC generates should more than cover the total interest cost (~$750k/year) of the now-restructured pension and debt.

More importantly, a direct competitor to ESCC called Sky-Skan entered bankruptcy proceedings last year in November and this opens up a $5M revenue opportunity, which can add up to ~$450K of EBITDA.

Management/Owners

The largest majority owner of ESCC is Peter Kellogg, the successful billionaire investor. He owns ~37% of the company, and has been recently and aggressively adding to his position.

The other 10% owner is Stuart Sternberg, the owner of the Tampa Bay Rays. He owns ~11% of the company.

Management + directors in aggregate own ~8% of the company. Management and directors don’t seem to be overpaid for a company this size, and have authorized share-holder friendly actions such as a ~15% buyback program.

Risks

Customer budgets: these are primarily driven by fundraising. If local economies are impacted, customers can be impacted, which can then affect ESCC’s sales.

Customer concentration: one customer represented 11% of sales in 2017. However, this is not a huge risk (as mentioned above, customers tend to stick with them).

Trade War: only 5% of COGS is aluminum/steel, so this is not the bigger issue. The bigger threat is an outright trade war that can impact international sales.

I do not hold a position with the issuer such as employment, directorship, or consultancy.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

Catalyst

More coverage

Increase in earnings power

Financial sponsor or strategic player acquires ESCC for a premium