| 2018 | 2019 | ||||||

| Price: | 10.80 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 173 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 1,865 | P/FCF | 0 | 6.2 | |||

| Net Debt (in $M): | 1,175 | EBIT | 0 | 0 | |||

| TEV (in $M): | 3,041 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- None found

- BETA

- AMPLIFY ENERGY CORP AMPY 10/15/2020

Description

Extraction Oil & Gas (XOG) is one of the few fundamentally undervalued companies within the energy sector, trading at under 3x 2018 EBITDA and mid-teens sustaining FCF yield. We believe a very timely opportunity exists here, as low trading liquidity combined with a top shareholder shutting down its energy book has resulted in irrational stock underperformance versus peers.

XOG is the brainchild of Matt Owens, a young (he's now 32) petroleum engineer that partnered with industry veteran Mark Erickson to found the company in 2012. Owens and Erickson currently serve as President and CEO/Chairman, respectively. In only four years, XOG has amassed a 340k acre position across the Denver-Julesburg (DJ) Basin in Colorado, grown production to 66k barrels of oil equivalent per day, and proven itself as one of the most efficient operators in the DJ Basin. Fundamentally, we estimate XOG to be worth $28 per share, and believe a more disciplined capital allocation approach will ultimately drive shares towards our target. Importantly, unlike other energy names where management is entrenched and capital discipline is elusive, XOG's management owns 8.6% of the company. Private equity sponsors (Yorktown Energy Partners and Bronco) also own ∼35% of the company, and are obviously actively committed to ensure that management delivers.

For background, the DJ Basin resource covers the northwest corner of Colorado and stretches up into southern Wyoming. The basin has long history of oil and gas production beginning in the early 1900’s. Similar to other fields in the United States, the DJ Basin was first developed heavily through vertical drilling and has since experienced a resurgence in activity and significant production growth beginning in the late 2000’s with the advances made in horizontal drilling. From an ownership perspective, the DJ Basin is relatively consolidated. The majority of the acreage is held by Anadarko Petroleum and Noble Energy.

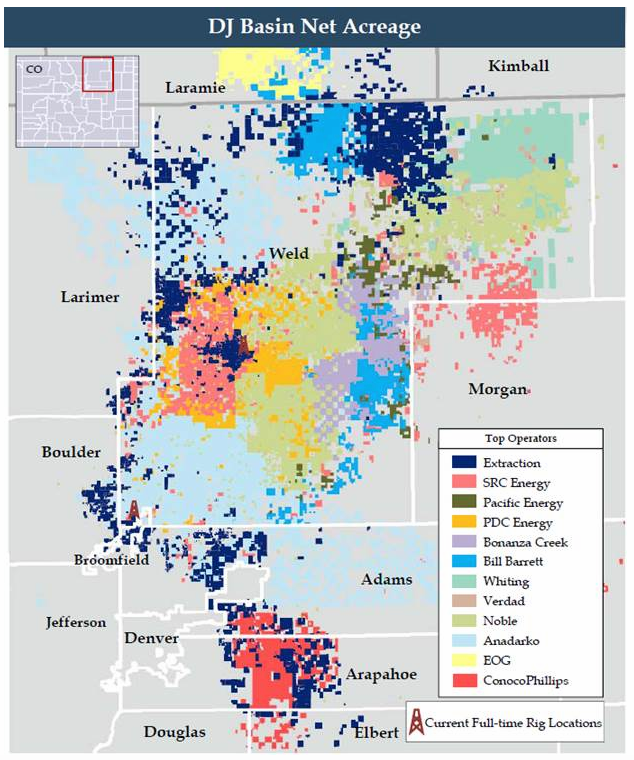

Source: Extraction Oil & Gas

The map above displays XOG’s acreage position across the DJ Basin. As can be seen from the map, XOG has tended to lease acreage around the edges of the core of the basin. Given how consolidated and how heavily developed the acreage was across the basin, XOG made a conscious decision to lease in areas that have historically been underdeveloped vertically. This strategy should and has yield better and more wells per section than offsetting leases given less historical depletion. XOG’s acreage position can be grouped into five key areas:

- Greeley (~12k acres, blue leases in the center of the field between SRC Energy & PDC Energy)

- Windsor (~30k acres, blue leases NW of Greeley on the border of Larimer county)

- Southern DJ (~50k acres, blue leases in Broomfield and NW Adams county)

- Hawkeye (~60k acres, blue leases primarily in Arapahoe county next to ConocoPhillips)

- Northeast Extension (~170k acres, blue leases in North Weld county).

Greeley is XOG’s most productive area given its location in the center of the basin. Reservoir pressures are higher in this part of the basin which yield more production per well with a much higher level of natural gas production.

Windsor and Southern DJ have similar oil production per well as Greeley, but less natural gas given they are located further from the center of the basin.

Hawkeye is a new area for not only XOG, but the operators in the basin. This Hawkeye area has not been developed vertically or horizontally historically given its location outside of the core of the basin. However, geologically the resource deposit in this area has similar characteristics as the core of the DJ Basin. In fact, recent well results from XOG and peer ConocoPhillips suggest Hawkeye could be as productive as the best parts of the DJ Basin. Additionally, this area has higher oil production than other areas of the DJ Basin which improves returns given oil is a higher value commodity today than natural gas.

Finally, the Northeast Extension area is similar to Hawkeye in that it is characterized by higher oil production than the DJ Basin core. However, the NE extension is geologically more complex and less mature from a development perspective. As a result, the NE extension acreage is not being developed by XOG today and is more likely to be monetized by XOG. A number of larger peers around the NE extension could have interest in growing their positions through the acquisition of all or a portion of XOG’s NE extension acreage.

From a development perspective, XOG has been most focused on drilling its Windsor and Greeley areas which is primarily a function of having acquired those positions early in the company’s formation. In 2018, XOG’s development activity is evenly spread across Greeley, Windsor, and the Southern DJ. Hawkeye is still in early stages of development and is receiving a smaller portion of development capital. Beyond 2018, XOG’s development activity will increase in Hawkeye and then be evenly spread across the four previously mentioned areas.

One of the key considerations for development in the DJ Basin is midstream infrastructure requirements, specifically gas processing. Today, gas processing capacity is in the northern part of the field (north of the Anadarko Petroleum leases) is fully utilized thus limiting production growth. DCP Midstream, the main natural gas processor in the north part of the field, is expanding capacity in the field by 25% in the third quarter of 2018 and an additional 25% in the second quarter of 2019. Following these expansions, XOG and other operators in the northern part of the field will enjoy a lifting of the current constraint and be able to resume strong production growth for an extended period of time. Gas processing in the Southern part of the field is owned by Anadarko Petroleum. Today, Anadarko’s processing capacity is not fully utilized which is allowing itself and XOG to grow production in this part of the field. Given its immaturity, the Hawkeye area needs gas processing capacity to be constructed to allow for full development by XOG and ConocoPhillips. Developing a midstream gas processing solution is one of the key strategic priorities for XOG in 2018. XOG has committed to not dilute shareholders and fund the midstream development in Hawkeye on its balance sheet. Instead, XOG is likely to partner with a private equity firm to jointly develop future gas processing needs using third party capital. In our opinion, this potential midstream joint venture could become a significant asset for XOG which it may ultimately monetize when developed. The specific midstream development plan for Hawkeye is likely to be announced in the second quarter of 2018.

Finally, any discussion of oil and gas development in Colorado would not be complete without a discussion of the political landscape. Oil and gas development, while having been a large part of the state’s economy for the past century, is facing increased opposition from local communities. As the state’s population has grown neighborhoods and businesses have been constructed much closer to oil and gas development than they have been in the past. This encroachment is creating tension between the public, who want to live unaffected by oil and gas development, and oil and gas companies, who want to develop the valuable resources in which they’ve invested significant amounts of capital. In the past, the anti-energy group has proposed restrictive setback requirements which would limit how close a well could be drilled to an existing structure. However, this proposal has never gained enough popular support to become an amendment to the state’s constitution. Colorado’s 2018 gubernatorial election will again increase the risk for oil and gas operators in the state. The leading Democratic candidate, Jared Polis, has historically been anti-energy. Were he to win the election, the energy industry could once again be at risk for more restriction on future development.

From a valuation perspective, we believe XOG is worth $28 per share. This net asset value assumes XOG develops ~1,800 of its remaining ~3,700 net drilling locations over the next two decades at a relatively consistent pace. The $28/sh net asset value ascribes zero value for the ~168k net acres the company holds in the northeast portion of the DJ basin. This northeast acreage is unlikely to be developed by XOG, but could be sold by the company for between ~$250-500mm ($1.50-$3.00/sh). Today, XOG trades at ~2.6x 2019 EBITDA vs an oil peer average of 5.5x.

Quantitatively, XOG screens well on several other key metrics including production growth CAGR through 2020 (42% vs. 18% peers average), return on invested capital (20.0% 2020 vs peer average of 11.2%), and most importantly free cash flow (9.5% of market cap in 2020 vs. peer average of 0.1%). Additionally, we estimate that XOG would generate ~$300mm of free cash flow per year (15% current market capitalization) if the company decided to simply maintain production at year-end 2018 levels near 115mboed. XOG’s combination of superior growth, returns, and free cash flow are all a direct result of its focus on quality acreage and efficient development.

Despite the company’s significant growth and track-record of execution, XOG’s stock has fallen from $19/sh at initial public offering to under $11/sh today. The decline in the share price and underperformance relative to peers in late 2017/early 2018 can be attributed primarily to concerns about management’s ability to be disciplined with capital. In 2017, XOG spent $522mm buying its Hawkeye acreage despite entering the year with 220k acres and over 25 years of remaining drilling inventory. Looking forward, XOG plans to stop spending money on non-productive leases and fund all future lease purchases with offsetting sales of non-core acreage. Given this shift, capital efficiency should improve enabling the company to generate substantial free cash flow beginning in the second half of 2018, which is not common in the exploration and production industry. More recently (YTD), we believe a couple of forced sellers are still pressuring the stock, as two large hedge fund holders blew up and their books are probably still being unwound. Primary near-term catalysts include additional acreage sales ($70mm year to date) and a midstream joint venture associated with its new Hawkeye acreage. As the company de-levers to its target of under 1.5x net debt/EBITDA, the company is also signaling a willingness to consider share buybacks late in 2018.

Primary near-term risks include increased Colorado regulations associated with the upcoming gubernatorial election, production misses related to gas infrastructure constraints in the DJ Basin, significant capital being invested in midstream gas processing, and additional acreage acquisitions. If you are uncomfortable with the Colorado risks, one potential hedge is to pair XOG with short positions in either PDCE or SRCI, which it has underperformed materially YTD.

Finally, management owns a combined 8.6% of the total shares outstanding (14.8mm shares), which is one of the highest levels of insider ownership in the industry. While young, the management team is well-aligned with shareholders and incentivized to maximize value.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

- Flow-driven: forced liquidation selling ends.

- Hawkeye midstream JV announcement (2Q18?)

- Non-core acreage sales (throughout 2018)

- FCF generation in 2H18 and buyback announcement.

| show sort by |