| 2018 | 2019 | ||||||

| Price: | 21.92 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 38 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 823 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 0 | EBIT | 0 | 0 | |||

| TEV (in $M): | 0 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- Failed drug launch

- Going to Zero

- None found

Description

FLXN (Long):

Market Cap: $823M

Share Price: $21.92

Target Price: $55.00

Introduction

We think FLXN represents a timely and exceptional cheap idea in a de-risked biotech/spec pharma stock. The stock has underperformed this year (and last) as they launch their first product, Zilretta, an extended release corticosteroid for osteoarthritis (OA) pain of the knee. We have found (warning: broad generalization) that biotech specialists love to short drug launches and we think this creates inefficiencies and can present attractive investment opportunities for patient holders: Flexion represents a case study in this kind of opportunity.

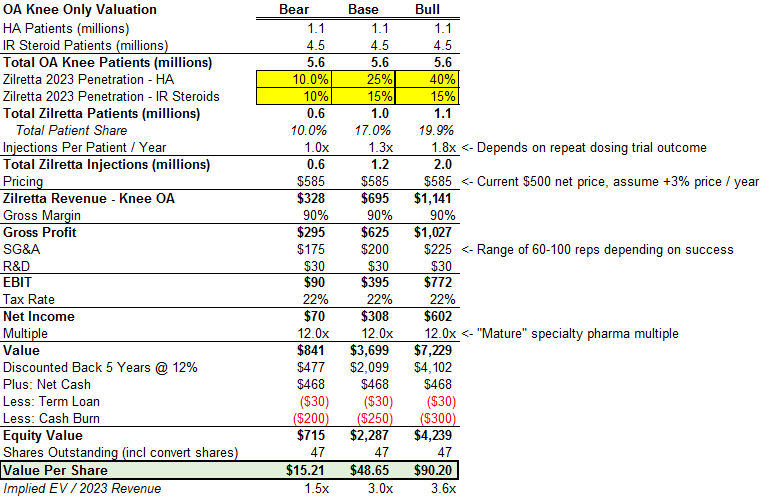

We think Zilretta in the knee alone has the opportunity to do ~$700M in revenue by 2023 in our base case, leading to a valuation of ~$49.00 per share. We don’t think $700M is unreasonable considering Hyaluronic Acid (HA) injections, which are currently advised against by major medical societies, does ~$1B in revenue in the US treating OA. In addition, this drug has a clear therapeutic benefit for patients with diabetes which represent a disproportionately high percent of OA patients and we believe it is poised to become the preferred treatment option for these patients (this alone if fully penetrated is a $700M opportunity). Adding on incremental joints, such as shoulder and hip, which have phase II trials ongoing, could add an additional $8.00 onto this target assuming 20% penetration. There is also a pipeline of early stage assets which could have promise, but we don’t include in our valuation. Our Base Case value of $49.00 + 75% weighting on the $8.00 (so, $6.00) from other joints = $55.00 per share or ~150% upside to the current price.

Assuming Zilretta only makes modest inroads into the market and none of the pipeline assets succeed, we see downside of ~$15.00 assuming 10% total patient penetration. As discussed below, given the therapeutic dynamic for diabetic patients, we think this is very conservative.

Capitalization

-

As of September 30, 2017, FLXN had cash and cash equivalents of $159.2M and marketable securities of $175.9M. Adding the net proceeds from the October 2017 secondary of ~$132.4M gets you to $468M in pro forma cash ($12.50 per share).

-

FLXN has gross debt of ~$226M, consisting of $201M of face value convertible notes and $25M in term loan. The convertible notes are out of the money (strike: $26.78) and carry an interest rate of 3.375%.

-

Net cash is thus $242M as of 9/30 or ~$6.36 per share (~30% of current market cap).

-

FLXN also has ~$170M in gross NOLs as of 9/30.

Valuation

Acquisition Optionality

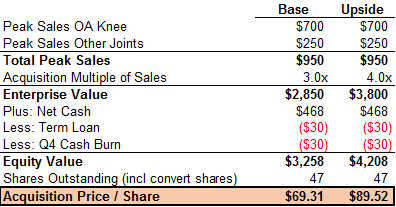

We would be remiss if we didn’t walk through the math on a takeout and discuss the prior news on this topic. Roughly a year ago there was press speculation that Sanofi had agreed to buy Flexion (https://www.fiercepharma.com/pharma/sanofi-verge-1b-plus-deal-for-arthritis-focused-biotech-flexion). We can only speculate on the veracity of this article or the reasons why this purported deal didn’t occur, but FLXN is still independent and the case for an acquisition by a larger organization with an ortho sales force remains as compelling as ever. We use a range of multiples (3x - 4x) since it appears multiples have drifted up on peak sales for acquisitions, but as generalists we still like the 3x revenue rule of thumb (call us old fashioned).

What is Zilretta and why are we excited about it?

Zilretta is the first and only extended-release, intra-articular, or IA (meaning in the joint), injection indicated for the management of OA related knee pain. It was approved by the FDA in October 2017 and formally launched in late November. It terms of IP, FLXN has composition of matter patent protection out to 2031.

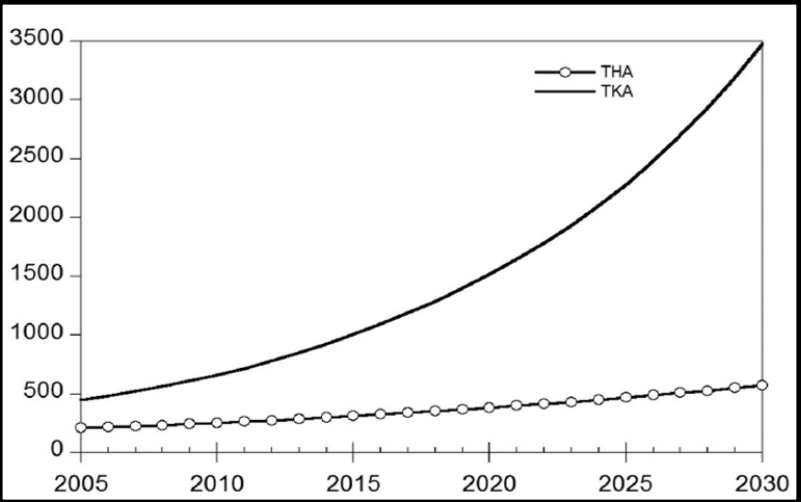

Zilretta’s initial indication, osteoarthritis of the knee, is a growth market. Here is a study regarding total knee and total hip replacements from 2007 that shows the expected growth in the market given American demographics (https://www.ncbi.nlm.nih.gov/pubmed/17403800).

Here is the key slide, which FLXN pulled out for use in their investor day in June as a proxy for knee OA market growth (note: TKA = Total knee arthroplasty = knee replacement).

In short, this will be a growth market for many years to come due to an aging (and heavier) population reaching peak years of osteoarthritis prevalence (the linkage between Body-Mass Index and knee OA is expounded upon here: https://www.ncbi.nlm.nih.gov/pubmed/18467514).

Diabetic Opportunity: We Think This Market Supports a Robust Downside Case

As mentioned above, the research is clear: diabetes is linked to higher rates of osteoarthritis and therefore the population of diabetics being treated by orthos for their knee pain is relatively large (estimates rates from ~14-20% of total patients, here is one meta analysis: http://rmdopen.bmj.com/content/1/1/e000077 ). Literature suggests that immediate release steroids have a transitory impact on the blood sugar levels of diabetic patients, complicating their management of their diabetes. A study worth mentioning: http://journals.sagepub.com/doi/abs/10.1177/1941738117702585, which gives a review of a number of studies regarding the magnitude and transience of the increase in glucose.

FLXN ran a phase II study to address complication and found that Zilretta did not increase blood glucose levels like IR steroids (http://www.abstractsonline.com/pp8/#!/4297/presentation/44287). We think this data represents a clear point of differentiation and diabetics are likely to be the first patients switched onto Zilretta as doctors begin to use the product.

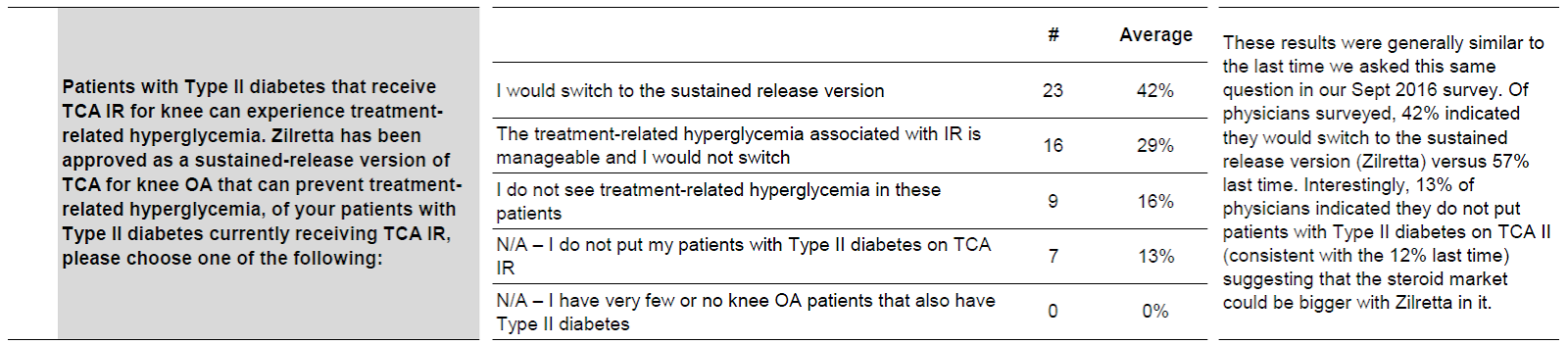

But don’t just take our word for it. A November doctor survey by RBC asked a question about diabetic patients with OA, with 42% of respondents suggesting they would switch those patients to Zilretta and 13% indicating they don’t even use IR steroids in diabetic patients (presumably due to the blood glucose issue), representing potential upside to the patient pool for Zilretta.

Putting some numbers behind this opportunity:

-

~20% of OA patients have diabetes

-

If we limit it only to patients receiving injections today, that is 1.1M patients

-

There is the potential for incremental patients to be added to this pool given some doctors appear to not give these patients IR steroids at all (although we cannot rule out them getting HA)

If we round up to 1.2M to account for this potential untreated population and assuming 40% Zilretta penetration, that would represent ~$280M in 2023 revenue. Using a pharma rule of thumb (3x sales) and applying our downside case cash burn, we get $23.00 / share in value from this opportunity alone.

The Thing about Hyaluronic Acid

The strong sales generated by Hyaluronic acid in the U.S. give us confidence in the size of the opportunity. In 2015 U.S. revenue for Hyaluronic acid (HA) brands was ~$950M. Last year one of the leading HA brands, Synvisc (Sanofi) generated ~$475M in revenue worldwide ($360M of that in the US). These figures were achieved despite HA as a class receiving a strong recommendation against use in OA of the knee by the American Academy of Orthopedic Surgeons in their most recent guidelines (2012, link: https://www.aaos.org/research/guidelines/oaksummaryofrecommendations.pdf ) finding that “the overall effect of hyaluronic acid did not provide minimum clinically important improvement to patients”. Similarly, Osteoarthritis Research Society International found the evidence “uncertain” for HA in their 2014 guidelines on non-surgical treatment of the knee (https://www.ncbi.nlm.nih.gov/pubmed/24462672). Finally the National Institute for Health and Care Excellence (NICE) flat out states “ Do not offer intra-articular hyaluronan injections for the management of osteoarthritis.” (https://www.nice.org.uk/donotdo/do-not-offer-intraarticular-hyaluronan-injections-for-the-management-of-osteoarthritis). It’s worth noting that the American College of Rheumatology does conditionally recommend for HA injections - in knee only. Rheumatologists currently write a small % of overall OA injections.

Let me reiterate this. Hyaluronic Acid:

-

Is recommended against by leading orthopedic surgeon societies

-

Is priced between $500-$1,000 (so generally higher than Zilretta @ $570)

-

Has poor reimbursement, which poses a headache for doctors

-

Anthem/Empire Blue Plan “ Effective for dates of service on and after December 1, 2017, intra-articular injections of hyaluronan are considered not medically necessary for the treatment of pain due to osteoarthritis of the knee and all other knee conditions.”

https://www11.empireblue.com/provider/noapplication/f5/s1/t2/pw_g320441.pdf?refer=ehpprovider

-

Aetna’s [onerous] step through requirements for HA authorization: http://www.aetna.com/products/rxnonmedicare/data/2014/MISC/viscosupplements.html

And yet HA generates ~$1B in revenue in the U.S. alone.

We think Zilretta, with its novel formulation of a known steroid which mitigates some of the systemic effects doctors worry about with IR steroids while offering longer lasting pain relief has the potential to gain significant share vs HA and IR steroids.

A Brief Word on the Pipeline and Future Clinical Readouts

Near term the most important pipeline item is the Zilretta repeat dosing study. This is important for a few reasons: 1) Zilretta’s current label has a limitation of use (literally: “ZILRETTA is not intended for repeat administration.”) FLXN naturally thinks this warning shouldn’t be there, so is running a study to prove it’s safe when used repeatedly. 2) The trial has clear commercial implications regarding efficacy and patient outcomes, specifically we’ll find out a) when patients come back for another dose after their original treatment and b) how many patients elect to get that second treatment (a rough proxy for satisfaction with treatment).

On January 8th FLXN gave an initial readout of their 205 patient repeat dosing study .

-

95% of patients achieved clinical benefit from a single administration (defined as agreement between patient and doctor)

-

90% of eligible patients received a second dose (with 3 patients still pending), with those occurring between week 12 and 24

We think this is pretty positive data: our diligence suggests doctors are hard wired to expect IR steroids to last 3 months and are increasingly wary of giving IR steroids more frequently than 4 per year to people who need dosing more frequently. If this trial reads out (Q3 2018 results) and patients are not getting second doses until 16-20 weeks on average, that would be a substantial real world improvement over IR steroids and give doctors incremental comfort on the duration of Zilretta.

FLXN is also running a Phase II bilateral knee with data expected in 1H and a Phase II OA hip and shoulder pain study to read out in 2H 2018.

Preclinical Pipeline Assets (we don’t assign value to these currently)

FX101: Basically next generation Zilretta, an extended release fluticasone intended to have a 6 month duration.

FX201: A recently acquired novel gene therapy intended to bind to IL-1Ra receptor aimed at suppressing joint inflammation. Years away, but would be curative if it works and a monster opportunity. Lots of hype in gene therapy land today and this is an interesting shot on goal.

Near Term Numbers Look Reasonable

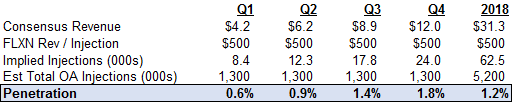

Part of the reason this opportunity exists is because it is pharma investing mantra to “short the launch”. We think numbers here are achievable in both 2018 and 2019 which derisks the idea substantially. Management has repeatedly guided that 2018 will be a year focused on setting the groundwork for a 2019 ramp, partially informed by the fact Zilretta has a miscellaneous J-Code from CMS (which is harder to get reimbursement for) in 2018, but will get a permanent product specific J-Code on Jan 1, 2019.

Another things that gives us comfort is the sales leadership, who have specific experience in selling injections for OA to orthopedic surgeons. Specifically: Dan Deardorf, VP Commercial who spent 14 years at Genzyme where he launched Synvisc-One, the very successful HA product now owned by Sanofi I referred to earlier. We believe FLXN has also hired a number of reps from Ferring, which sells another leading HA brand, Euflexxa (http://www.cafepharma.com/boards/threads/where-ortho-reps-going.613266/).

Looking at consensus and its implications:

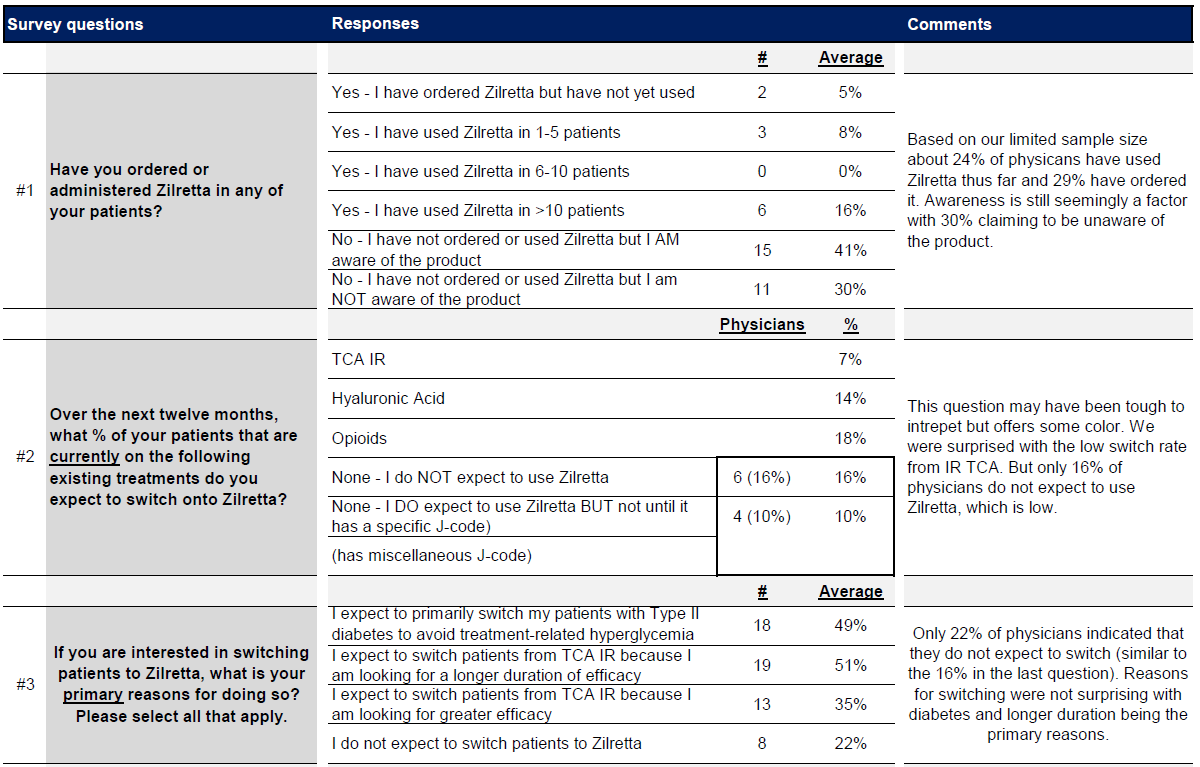

So basically the street is looking for FLXN to steadily build up to a bit under 2% penetration by YE 2018. If you look at the January RBC survey of orthos below you see that 24% of doctors said they had already used Zilretta, ~2 months into the launch and another 5% had ordered. The earlier survey revealed 42% of doctors would switch diabetic patients (20% of the OA market) to Zilretta. Bottom line, we think Zilretta is getting traction in a market where repeat IR dosing worries doctors and HA is beginning to struggle with reimbursement. Zilretta will struggle with reimbursement as well, but we think the bar is appropriately low.

Primary Research

While this isn't an exhaustive list, let us walk you through some of the work we have done ourselves as well as highlight some work on the sellside that we found particularly helpful.

General Feedback

-

One orthopedic surgeon mentioned they would use Zilretta in diabetics (“lay up”) which is 20% of OA patients. IR steroids cause elevated blood sugar if it escapes the knee.

-

Another doctor, when asked about if he would be more inclined to use Zilretta in diabetes, said: “absolutely, we can now show these patients its safe”.

-

For more information on this issue, here are some links to peer-reviewed studies on both prevalence and the problem with giving steroids to diabetics with OA

-

Prevelance of OA and Diabetes : https://www.ncbi.nlm.nih.gov/pmc/articles/PMC4254543/

-

Impact of steriods on blood glucose: https://www.ncbi.nlm.nih.gov/labs/pubmed/27500431-blood-glucose-levels-following-intra-articular-steroid-injections-in-patients-with-diabetes-a-systematic-review/

-

An ortho mentioned that at the hospital where they teach medical students are taught to cut back on cortisone use due to systemic effects of repeat steroid injections

-

The main source of this fear appears to be this study in JAMA from last year: https://jamanetwork.com/journals/jama/fullarticle/2626573. The bottomline of which is that long-term use of steroids reduced cartilage volume in the knee vs placebo - obviously a negative side effect for patients already facing that degradation due to OA.

-

The doctors we talked to had mixed opinions on HA, but clearly HA has some strong advocates in the market, although we heard about a worsening reimbursement environment

Specific Quotes

KOL #1: Practicing Ortho & Team Physician, NBA/MLB team, sees 25-40 patients per month

“The glucose issue, certainly the diabetic population is probably disproportionately afflicted with osteoarthritis, but when you look at the millions of people who have osteoarthritis, there's a relatively low number of diabetes. That being said, it is a marketed advantage, and anyone would find that to be an advantage. You would not want to build a market, however, around the diabetic population.”

“I would generally use it before HA, but in a setting where HA is not being reimbursed, I would absolutely use it first...And I might use it first anyway because it's a single shot versus multiple shots”

“Q: Let's say that it does get reimbursement. Let's say that is not an issue. Then where would you see using this versus IR steroid injections?

A: I would probably replace it with IR. This would replace IR.

Q: 100%? You'd just use this instead with insurance?

A: If there was no issues with cost, risk, burden. Yeah, I think I would.”

KOL #2: Practicing Ortho & Team Physician, USA National Soccer Teams

“Currently, right now, we're limited to some degree to straightforward cortisone injections, or hyaluronic acid derivatives, although now I've recently had two to three major insurers that do not cover any hyaluronic acid injections any further, because of the literature that's been put out, both in publication, as well as by our own society with regards to the no‐difference‐from‐placebo aspect of that.

Q: That's recently?

A: Yes. Yeah, United and Blue Cross patients, I've recently had where they will cover no version of a hyaluronic acid.

Q: Really?

A: Yeah.

Q: Leader: How recent has that been? Is that a recent change that they put in place?

A: Yeah, yeah, probably within the last two months, three months”

“I think the other place where this potentially is very beneficial, is in the fact that we're understanding more and more about the long‐term use of NSAIDs, anti‐inflammatory medications, and I'm seeing more and more people that … Whether it's diabetes, that have kidney issues, or that have stomach problems, or that just don't tolerate or can't take anti‐inflammatory medications, and that when we really rely on steroid injections. There's a lot that we're missing, in terms of the conservative management of osteoarthritic pain, and I would hope that this would be, certainly, something that fills in a needed void. But, I would agree that it's a huge market opportunity, no doubt.”

On diabetics: “currently my alternative is either kind of, "Live with the pain that you're having, or deal with this injection, and your blood sugars may bump." I've never had the option of where I say, "Here's something that can give you relief, without a bump in your blood sugars." I think that if it truly does not change blood sugars and a regular injection does change blood sugars more, or raise blood sugars more. I think that that is a real benefit. Diabetics that have blood sugars that go high certainly know when that happens, and don't like it. We do have patients that come back after injections, that say, "You know, my blood sugar skyrocketed, and I couldn't get it under control for a day afterwards, or two days afterwards." That's not ideal, and there's medical issues associated with that”

Q: On a scale of 1 to 10, 10 being really excited, and 1 being not so, where would you put your level of excitement in terms of this launch?

A: I'd put it kind of 9 or 10.

RBC Survey of 37 Orthopedic Surgeons (1/30/18)

Zilretta Clinical Data Review

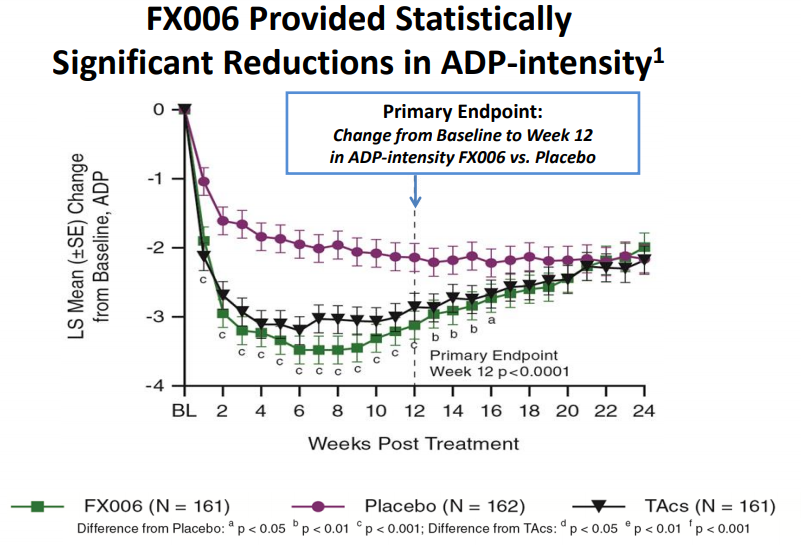

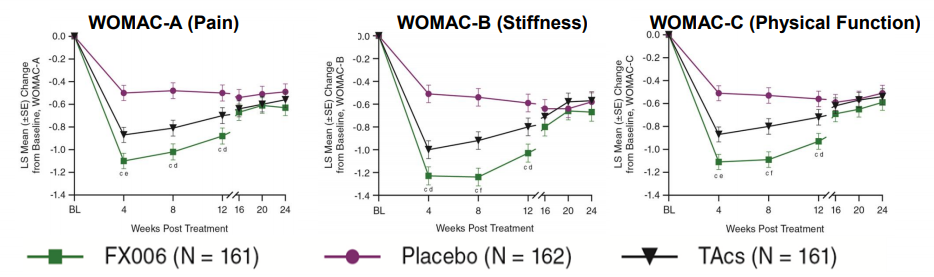

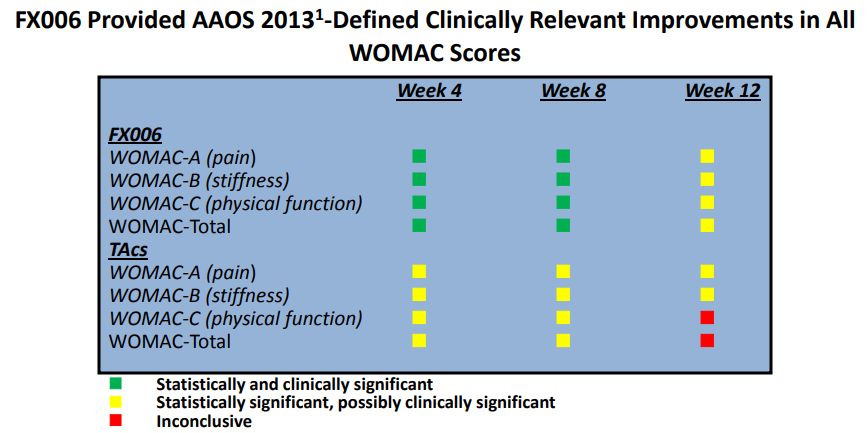

Let’s review what Zilretta does:

-

Zilretta reduces the pain associated with osteoarthritis better than placebo and TAcs (Triamcinolone injections = immediate release (IR) steroids).

2) Zilretta improves patient WOMAC scores (http://onlinelibrary.wiley.com/doi/10.1002/1529-0131(200110)45:5%3C453::AID-ART365%3E3.0.CO;2-W/full) over placebo and TAcs. Zilretta works better.

3) And those improvements are more durable than immediate release steroids on the American Academy of Orthopedic Surgeons-defined clinical benchmarks using those WOMAC scores. Zilretta lasts longer.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

1. Better than expected launch execution setting up rapid growth in 2019

2. Acquisition

3. Success in repeat trial leading to removal of the "repeat dosing" prohibition in the label (2H 2018)

| show sort by |