| 2019 | 2020 | ||||||

| Price: | 11.16 | EPS | 0.18 | 6.03 | |||

| Shares Out. (in M): | 3 | P/E | 61 | 2 | |||

| Market Cap (in $M): | 33 | P/FCF | 2.2 | 1 | |||

| Net Debt (in $M): | -12 | EBIT | 0 | 16 | |||

| TEV (in $M): | 21 | TEV/EBIT | 0 | 1.3 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- Turnaround

- Outsider-type CEO

- Multi-bagger

- Speculation

- Retail

- FRANCESCAS HOLDINGS CORP FRAN S 10/09/2012

- BETA

- FIVE BELOW INC FIVE 04/08/2020

- Grocery Outlet Holding Corp GO 01/09/2023

- GROCERY OUTLET HLDNG CORP GO 09/28/2021

- Vera Bradley VRA 01/04/2023

- Kirklands KIRK 07/10/2020

- DAVE & BUSTER'S ENTMT INC PLAY 12/30/2022

- CREDIT ACCEPTANCE CORP CACC 02/06/2020

- STAGE STORES INC SSI 11/21/2019

- PARTY CITY HOLDCO INC PRTY 10/20/2019

Description

FRAN Q3 comps projected +8% with $15 million of incremental cost reductions available. NTM price target: ~$30.5/share (~170% upside).

Thesis Summary

We have been following FRAN since 2014 and were short the stock for large portions of 2017 and 2018 due to prior management’s merchandising missteps and structural brick & mortar retail traffic headwinds. However, we believe the stock overcorrected by underestimating FRAN’s potential for self-help under a new regime. Although we do not claim that FRAN is out of the woods, its current market cap is difficult to justify if we are correct about the trajectory of the business.

Left for dead a month ago (~$8M trough market cap), FRAN is staging an impressive turnaround. Our alternative data ensemble, store channel checks, and conversations with REITS & management indicate that the positive inflections FRAN reported in 2Q across its income statement are accelerating further in Q3 for sustainable reasons. The simultaneous combination of strong positive comps & reduction in clearance activity, along with SG&A reductions, rent concessions and unprofitable store closures will drive significant operating leverage and FCF beginning in 2H 2019. If we’re right, these inflections should cause significant share appreciation in this highly shorted stock (>40% short interest / >50% cost to borrow).

We are projecting $22M of EBITDA / $15M of FCF in 2019 and $33M/$26M in 2020. On our numbers, FRAN will generate ~$41M of cash by the end of next year relative to the current $33M market cap. A blended FCF yield on Enterprise Value of 35% on 2019E / 45% on 2020E implies an NTM price target of ~$30.5/share.

Business Overview

Francesca’s Holdings Corp (FRAN) sells apparel and accessories for women online and through 700+ small footprint lifestyle center and mall retail stores. The Company’s main categories include dresses, tops, sweaters, denim, jewelry and accessories.

What Went Wrong Under Previous Management

-

FRAN abandoned what made it successful

-

FRAN’s historical success was rooted in providing an eclectic, trend-right assortment, highly responsive to the whimsical tastes of its core customer. Appropriately, FRAN’s merchandising philosophy favored short lead times and high ‘open to buy’ percentages. This approach helped FRAN limit unrecoverable merchandising mistakes and take advantage of trend changes. The previous management team abandoned these principles in favor of a more ’consistent’ and ‘timeless’ assortment, and lead times on several categories ballooned from days/weeks to multiple months. This blunder left FRAN unable to respond when its merchants failed (unsurprisingly) to predict fashion trends months in advance. FRAN was unable to deal effectively with the resultant inventory backlog because it had not previously developed sophisticated channels and procedures for clearance. FRAN entered a vicious cycle, trying to clear stale inventory, clogging up its sets and preventing new merchandise from taking the spotlight. That is how FRAN managed to stack a -14% comp in 2018 on top of a -11% comp in 2017.

-

High ROIC on new stores kept FRAN focused on unit growth rather than efficiency

-

FRAN’s small footprint (~1,500sqft avg) stores generated payback periods of less than 12 months as recently as 2016. Therefore, FRAN kept opening new stores and focusing on store growth rather than efficiency even after comps turned negative in 2013. As a result, FRAN’s SG&A entered 2019 bloated and store-level costs on a large percentage of stores became unsustainable, with more than 10% of the fleet running double digit negative 4-wall contribution margins according to our estimates.

What is Driving the Turnaround

-

New Management Took Chapter 11 Off the Table

-

Early in 2019 FRAN’s board appointed Michael Prendergast of Alvarez & Marsal (A&M) interim CEO. Some investors saw this appointment as a signal that Chapter 11 was imminent, which is why (we suspect) FRAN’s market cap came about as close to zero as we recollect ever seeing for a retailer with no non-operating debt and untapped cost reduction opportunity. It is now clear that Michael’s intent is not to guide FRAN through Chapter 11, but rather return it to sound footing. FRAN’s recent success in securing a $10 million term loan from Tiger Financial is further evidence of this intent and adds more cushion to the balance sheet.

-

Michael’s background combines deep expertise in both retail operations and restructuring, which we believe is exactly what FRAN needs. We are impressed by Michael’s rapid diagnostic of FRAN’s top line woes and supply chain opportunities. Equally, we believe Michael’s status as an interim outsider to the organization gives him the ability to make unsentimental organizational changes and the leverage to drive a hard bargain with landlords. As we discuss below in more detail, our calls with REITS convince us that every major FRAN landlord has recently committed to rent concessions and is incentivized to keep FRAN in business even if its turnaround is bumpy.

-

Top Line Inflection

-

Reversing Past Mistakes

-

In Spring of 2019, FRAN reverted to its prior merchandising model of high open to buy rates and flexibility in chasing real-time trends. Lead times in most categories have already shrunk back to days/weeks vs multiple months in the same period a year ago. Open to buy rates entering the fall season were as high as 50% in many categories. A pivot this rapid would have been impossible were these principles not already a part of FRAN’s DNA; however, FRAN’s buyers already knew how to execute this approach and its major suppliers were equally eager to get back to a model which works. As a result, the company reported that comps accelerated dramatically from May to June to July:

-

“May was challenging due to the large amount of legacy product on hand marked down in June. However, once our new receipts landed, we saw a dramatic improvement in sales which led to better than expected performance in June, and an inflection point in July.” - Q2 Earnings Call

-

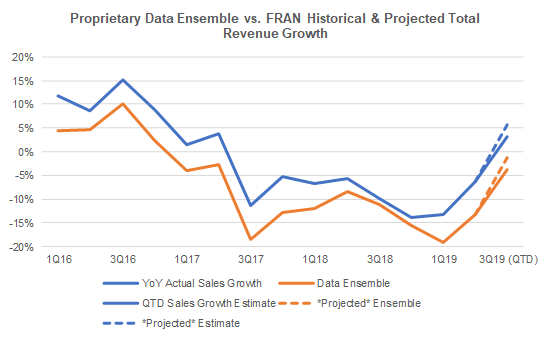

Our store checks indicate that dress, shorts, jewelry and hair categories led the way, driven by FRAN’s reinvigorated buying approach. Our data ensemble suggests FRAN exited Q2 comping positively in July. See Appendix for direct quotes from several FRAN store managers.

-

Denim Shop

-

In late July, FRAN significantly expanded its Denim Shop selection, a category in which it has not made significant investments in recent years. Our channel checks suggest FRAN’s denim collection has been very well received this season and is driving significant incremental sales, including to new customers. We believe this innovation in the assortment could be sustainably incremental, especially during colder seasons.

-

Impact

-

Q2 comps accelerated 8% sequentially vs Q1 (11% on a 2yr stack). Roughly 60% of the way through Q3 (as measured by total expected sales), our data ensemble* suggests that comps have accelerated by another ~10.5% and are running ~+5.5%. Furthermore, our ensemble, combined with FRAN’s earnings call commentary last year, suggest that the remainder of FRAN’s Q3 faces a significantly easier YoY compare than the Q3 QTD period did. Therefore, if 2yr stacks in our ensemble hold steady for the remainder of the quarter, we project FRAN to achieve a ~+8% comp in Q3 without any YoY increase in overall discounting.

*We are using a similar data ensemble that we’re using in our ongoing PETS short thesis. Our data ensemble includes a proprietary blend of multiple credit/debit card panels, geo-location data and transactional eCommerce data. We are assuming comps are 2% greater than sales in Q319 due to incremental store closures; projected ensemble is calculated by assuming the ensemble’s YoY growth remains constant in the remainder of the Q319 period relative to the current Q319 QTD period.

-

Cost Reductions

-

SG&A

-

Management has already identified $8 million of SG&A savings, which should be fully implemented this year and benefits fully annualized in 2020.

-

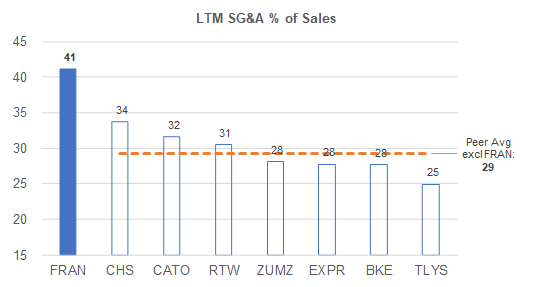

We believe more SG&A efficiencies will be found in 2020 as FRAN’s LTM SG&A rate remains highly elevated relative to peers:

-

FRAN’s 12% SG&A percentage gap to peers implies that ~$10 million of incremental SG&A savings could be available (~6% reduction) if FRAN were to bring its expense structure in line with peers even if we assume sales recover by ~6%.

-

Gross Margins

-

The company has already announced $7 million in store labor savings, to be realized this year.

-

Prior to the recent improvement in business trends reported in 2Q19, we believe Michael leveraged FRAN’s precarious financial position to negotiate meaningful rent concessions from every major landlord (top 8 REITs hold >55% of leases). Our independent conversations with REITs and brokers suggest FRAN has recently gotten concessions even at some “A” malls, and has achieved rent reductions of “up to 40%” on a “meaningful portion” of their store base.

-

While it is difficult to estimate the total size and timing of occupancy savings, if FRAN got a 40% occupancy reduction on just 15% of its store base and no other concessions it would translate to an incremental ~$3 million in annualized savings.

-

The largest single driver of FRAN’s ~900bps gross margin reduction since 2017 is comp deleverage. This should partially reverse as FRAN recaptures a portion of its previous productivity. Each 1% of comp is worth at least ~20bps of gross margin, so an incremental 13% acceleration in store productivity (as we project in Q3 alone) could be worth at least 260bps of gross margin expansion.

-

Merchandise margins have been hurt every quarter for the past two years by sales shortfalls which necessitated markdowns. This trend should also reverse if FRAN remains committed to more flexible purchasing whilst comps turn positive.

-

Store Closures

-

The 23+ stores FRAN is closing this year (including 10+ in 2H 2019) are running double digit negative 4-wall contribution margins and below average comps. Management has also identified ~25 additional such stores with leases expiring next year.

-

If we assume FRAN closes an incremental 35 stores through 2020 with average ~12% negative 4-wall contribution margins and AUVs of ~$400K/yr, it could create $1.7 million in annualized savings.

-

Cumulative Cost Reduction Potential

-

In aggregate, we estimate FRAN has at least $15M in near term incremental cost reduction opportunity, plus a further 260bps of near-term GM% expansion opportunity from comp leverage. This equates to over $25M in incremental EBTIDA opportunity.

Financials

-

Financial Projections

-

Modeling assumptions

-

Comps: +8% Q3 per our data ensemble and holding 2yr comp stack steady though Q1 2020. Modeling full year 2020 at a ~3% comp, which implies FRAN regains only ~12% of the productivity lost in 2017-2018.

-

SG&A: $12 million reduction by 2020 from 2018 level represents $4 million reduction achieved in Q1 2019 plus the $8 million of additional savings specifically identified by management since then. We do not model in any of the $10 million in additional SG&A savings we hypothesize above even though we do believe the company is likely to realize some of it over time.

-

Merchandise Margin: Recovers ~150bps from 2018 to 2020 due to less clearance; this implies FRAN recovers only ~25% of the ~620bps lost from 2016 through 2018. We feel this assumption is likely conservative if we’re right about a return to positive comps from down double-digit negative comps.

-

Stores: Closing net 10 stores in 2H 2019 and 25 in FY 2020.

-

Rent Expense: Declining 6% through 2020 (equal to cumulative net store closures) plus ~$3M from rent concessions as described above.

-

Output:

-

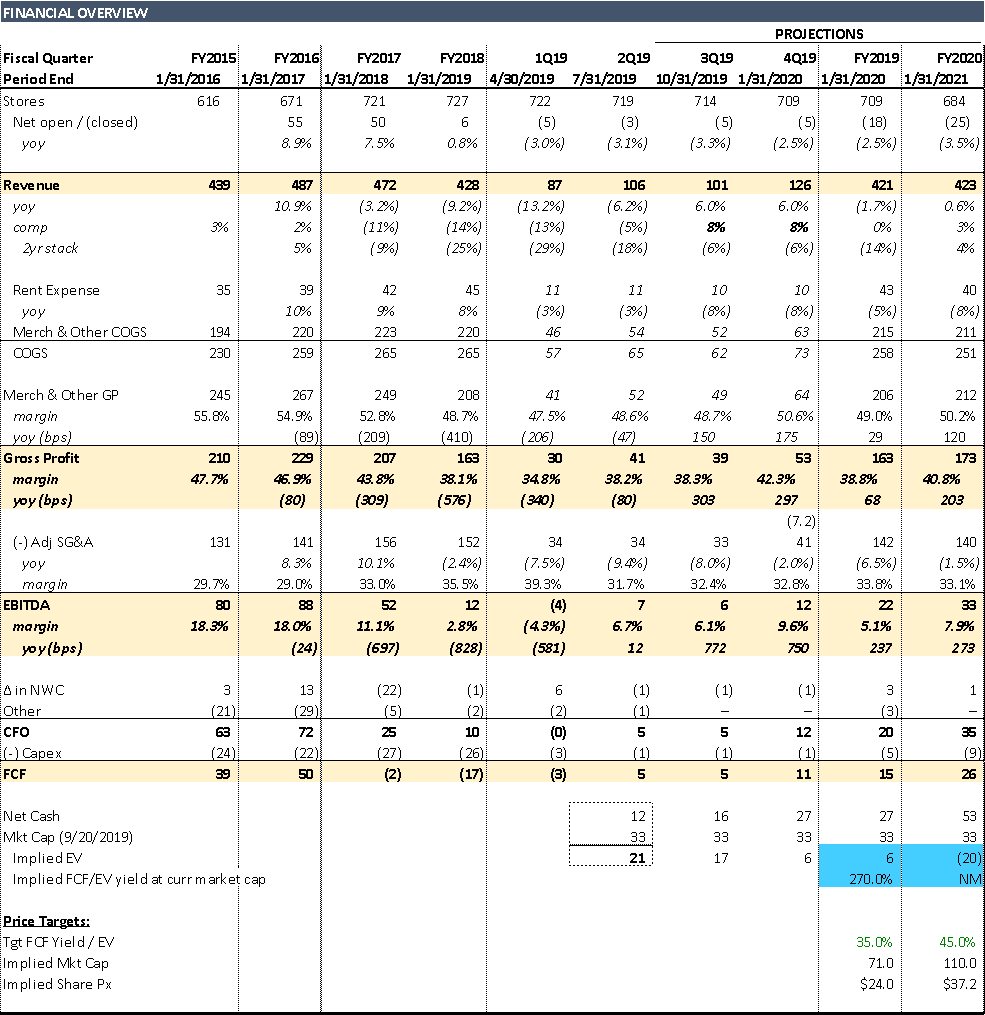

FRAN generates ~$22mm & $33mm of EBITDA in 2019E & 2020E, respectively, yielding $15mm & $26mm of FCF, respectively. We roll forward the net cash balance at the bottom of our model to illustrate the implied EV on today’s market cap (highlighted in blue).

-

Valuation

-

We suggest FCF relative to Enterprise Value (EV) is an appropriate valuation framework for a company in an admittedly volatile turnaround process. As of Friday’s close (9/20) the market cap was $33mm with a net cash balance of $12mm excluding operating leases. On our 2H 2019 projections, net cash balance will be $27mm by year end, implying an EV of $6mm vs today's $21mm, a ~270% FCF yield at Friday’s share price.

-

We suggest the average between a 35% FCF yield on 2019 & 45% FCF yield on 2020 numbers is an appropriate balance between the downside that FRAN’s turnaround could sputter and the “home run” upside of a >5x return if the turnaround continues into 2021.

-

On our projections, a 35% 2019 FCF yield implies $24/share and a 45% 2020 FCF yield implies $37/share, which is how we arrive at our current NTM price target of $30.5/share (equivalent to just $3 prior to FRAN’s reverse stock split).

-

Of course, it’s difficult to predict FRAN’s turnaround cadence precisely, especially beyond 2019; however, in more qualitative language we believe risk/reward is strongly tilted to the positive if comps turn positive while rent costs fall and other savings continue to accrue.

Risks

-

FRAN could appoint a permanent CEO after the turnaround is complete, with uncertain consequences

-

FRAN remains susceptible to merchandising mistakes and fashion fluctuations, though we believe their return to flexible merchandising reduces these risks

-

Ongoing brick & mortar retail traffic headwinds, though FRAN is not remotely unique in this regard.

Appendix

-

Quotes from our recent conversations with several FRAN store managers

-

“Since that time [referring to Q1], the company has becoming significantly more responsive and actually are within a feedback loop with their store managers. They do things like pulling poorly selling items off the shelves and moving it over to clearance sooner based on feedback.”

-

“We also had a serious palpable buyer issue in Q1. I saw first-hand that customers didn’t like what they were seeing at all and were not willing to spend money. Merchandise turnover was simply not happening. However, now we have a new buyer who is much better and actually knows how to pick the right merchandise. Many of my customers who I’ve gotten to know definitely are noting the significantly better product that to them, feel like high quality merchandise, but not too expensive.”

-

“We had a bad buyer that was not good at selecting apparel. The guests would come in, but end up not leaving with anything, which is opposite of what we want to do. A few months ago, thank goodness we replaced the old buyer and now my loyal guests are returning to buying product again.

-

“I think the products are getting better and better, especially this year. Dresses, tops, clothing, and jewelry are all good sellers and I think this is why we are experiencing better performance. The product is higher quality and is at that perfect point for our customers where it doesn’t feel cheap and looks luxurious but does not carry the same price tag as well-known luxury brand products.”

-

“Yes, I think we got a new buyer recently that helped with sourcing better merchandise”

Disclaimer: At the time of publication, the author of this article holds a long position in FRANCESCAS HOLDINGS CORP (FRAN). This article expresses the opinions of the author. The author has no business relationship with any company whose stock is mentioned in this article.

The author of this article has a long position in the company covered herein and stands to realize gains if the price of the stock increases. Following publication, the author may transact in the securities of the company, and may be long, short or neutral at any time. The author of this report has obtained all information contained herein from sources believed to be accurate and reliable. The author of this report makes no representation, express or implied, as to the accuracy, timeliness or completeness of any such information, or as to the results to be obtained from its use. All expressions of opinion are subject to change without notice, and the author does not undertake to update or supplement this article or any of the information contained herein. This is not an offer to sell or a solicitation of an offer to buy any security.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

-

The next scheduled catalyst is FRAN’s regular Q3 report

-

FRAN announced a poison pill on August 2nd, shortly after Cross River Management announced a >20% position in the company. It is possible that a bidder could attempt to buy the company before the turnaround we believe to be taking hold is more broadly appreciated. We know nothing of Cross Rivers’ intentions but speculate that a buyer wouldn’t take a 20% position in a stock like FRAN if they wouldn’t at least entertain the possibility of owning the whole thing.

| show sort by |