| 2016 | 2017 | ||||||

| Price: | 17.90 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 14 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 256 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 6 | EBIT | 0 | 0 | |||

| TEV (in $M): | 262 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- Professional Services

- Value trap

- FRANKLIN COVEY CO FC 08/02/2023

- FRANKLIN COVEY CO FC 08/16/2021

- FRANKLIN COVEY CO FC 12/27/2017

- FRANKLIN COVEY CO FC 03/05/2013

- FRANKLIN COVEY CO FC 07/21/2009

- Franklin Covey FC 02/18/2008

- Franklin Covey FC 07/11/2006

- Franklin Covey FC 10/02/2002

- BETA

- ADVANCE AUTO PARTS INC AAP 11/17/2023

- INFORMATION SERVICES GROUP III 05/25/2017

- BARRICK GOLD CORP GOLD 07/17/2021

- ADVANCE AUTO PARTS INC AAP 07/11/2022

- Universal Stainless USAP 02/23/2023

- ADVANCE AUTO PARTS INC AAP S 11/01/2023

- Allstream ALR/B CN 09/24/2003

Description

In choosing a stock ticker FC, the company should have added another F on FC(F) given the business model has quite attractive Free Cash Flow dynamics. We wrote up FC a little over 7 years ago at $6.20 a share. A great deal has changed for the better. In short, I think FC will generate approximately $225+ million in free cash flow over the next 5 years on a market cap/EV of $259/$265. In short, this quarter guidance is for $20 million in EBITDA, $31+ million for 2016. We believe in 2017, EBITDA will run $42 million ($3.00 per share +/-) and in 2018, $51 million on +/- 14.5 million shares. I believe that most of excess free cash flow will go back to share repurchases and possibly a dividend if the stock reaches fair value in the 12-14x+ EV/EBITDA range. We think FC is a $30+ stock over the next 12 months, driven by 20% EBITDA growth, 100% growth in All Access Pass revenue, while trading at a 8x multiple for a business with strong returns on capital.

Franklin Covey focuses on best in class content to offer training and consulting advice across categories like: Leadership, Strategy Execution, Productivity, Trust, Customer Loyalty, Sales Performance, and K-12 Education. Recently, FC came out with a new go-to-market strategy called All Access Pass (“AAP”) which offers an all-you-can-eat subscription model for $20,000 annually per 100 people ($200 per person) vs. their previous a-la-carte model. This could be a game changer for the company as the strategy will generate higher revenues from new and existing customers with significant incremental EBITDA margin. The business currently operates with approximately 15% free cash flow margins and we think the business should operate north of 20% as All Access Pass continues to scale. Management did not provide official guidance given the early phase of the launch, but is directionally targeting revenue to be $12 million (Aug 2016), $35 million (Aug 2017), and $55 million (Aug 2018) for AAP. On the most recent earnings call the CEO stated from June-July 10th, FC closed $5.2 million or 260 contracts at $20,000 each. FC economics are not very different from Gartner Group (1/10 the size in terms or both revenue and EBITDA) but only 3% of the valuation ($265 million vs. $8 billion). In fairness, FC does not have the revenue growth and is in early days of a transformation process.

We believe there are seven goldmines inside of FC:

FC is a 70% gross margin business that is not a billable hour business, but owner proprietary time-less content (e.g. '7 Habits' is over 25 years old and has generated way over $1B of revenue) with powerful global distribution model (Client Partners, International Licensee’s, All Access Pass, Facilitators).

-

Gold mine #1: Facilitator business: about 5,000 active facilitators/trainers that buy FC materials/content to train large internal work forces….essentially a sticky licensing revenue generating $45-50 million a year w/ estimated 80% gross margin.

-

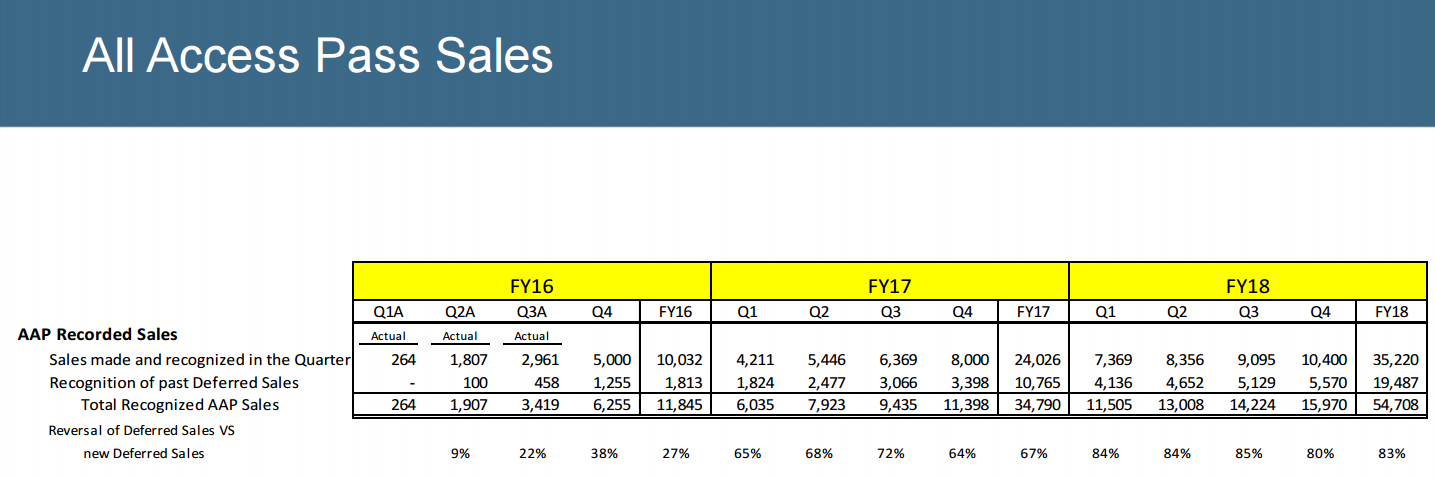

Gold mine #2: All Access Pass (AAP) which is a web based $20,000 a year subscription. AAP is a new distribution model launched three quarters ago that could be a game-changer. Instead of selling their training IP piecemeal, AAP is an all-you-can-eat subscription offering which not only increases the average customer spend by 40% but has incremental margins in the 45%+ range (vs. 25%-30% for piecemeal approach). FC should generate about $12 million for first year ended in August 2016 and possibly $30-40 million in 2017. This will bode well for earnings power in the coming couple of years and beyond.

-

“In the full fiscal year 2015, these particular 139 clients spent $3.7 million for the whole year, a median of $17,700 per client based primarily on facilitator materials. These same clients, who are now All Access Pass holders, have already spent $5.2 million this year -- year-to-date through the third quarter, a median spend of $25,250 and most of them just became pass holders recently, relatively recently. Now approximately $1.5 million of this spend is being treated as deferred revenue we just keep talking about. So a lot of the difference -- we haven't seen much of that difference come through yet, but it will. But the actual spend is higher, and so that's an important thing.” – Bob Whitman on 3Q16 earnings call

-

Gold mine #3: International Licensee’s (royalties of $17 million a year)

-

Gold mine #4: Global distribution…150 countries, #1 brands, best in class results based on annual retention rates, grossed up global revenue $300 million (this is a big asset, to attract talent)!

-

Gold mine #5: installed base of 4,000 clients that renew annually 80-90% range

-

Gold mine #6: strong capital allocation skills in both buy backs + innovation. Current access to capital of July 2016: $50 million and $30 million open on their current share repurchase.

-

Gold Mine #7: strong board and management with aligned incentives: 30% ownership and 17 years at the company

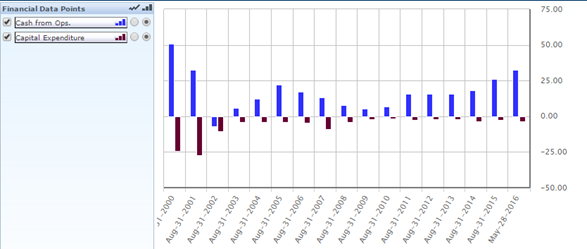

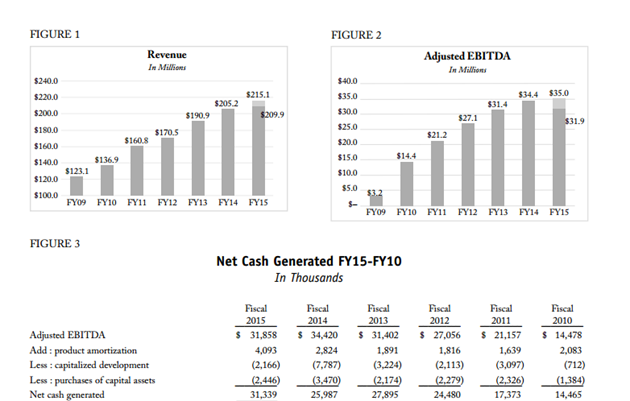

CEO from January 2016 letter: “Using our Strong Liquidity and Balance Sheet Strength: Our net cash generated has been strong and consistent, our Cash Flow from Operations is substantial ($26.2 million in fiscal 2015), and our cash position strong (just over $16.0 million at August 31, 2015, after having utilized more than $14 million to repurchase shares during the last half of fiscal 2015). In addition, our $30 million credit facility was undrawn at year-end, and we have received bank approval for an additional $20 million term loan facility. We have a strong conviction about the underlying strength of the business, significant liquidity, and a belief that purchasing shares at this time provides us the opportunity to create additional shareholder value. Consequently, we recently initiated a $35 million modified Dutch tender offer, which we expect to close in early January 2016.”

(ABOVE CHART is NOT GUIDANCE) 2016: Year ended AUG 2016. Should be close to $12 million 1st year.

All Access Pass:

AAP allows the salespeople to not sell individual solutions but a whole suite of solutions. This allows FC to add more verticals / brands to their solutions, further strengthening the offering, and allowing for cross selling and deeper organizational opportunities.

“As you know, when we sell an All Access Pass, we enter into a contract with a client. It has 2 primary components. One is an IP license for up to 26 of our content areas, which represents approximately 60% of the contract value and the revenue for that portion is recognized immediately. And the second component is the digital library, representing 40% of the contract value, which is put on the balance sheet and recognized over the following 12 months…..Gross margin associated with that deferred revenue is very high, almost -- with some intellectual properties, so it's close to 95% and that will then serve as -- we'll have a bank of deferred revenue embedded in which is nearly $5 million of also gross margin, most of which is EBITDA contribution moving to next year.” (Source: 3Q16 Earnings Call CEO: Bob Whitman)

“They're just model. But assuming the recognition of $4 million of new All Access Pass revenue each quarter in -- through fiscal 2017 through 2018, the annual renewal of 80% of these All Access Passes -- it's early and as we don't really know what that number will be, we're targeting at least 90%. But let's say for this model's purposes we're saying 80%, using those 2 assumptions, you see the total recognized All Access Pass revenue would increase from $11.8 million in fiscal 2016 to nearly $35 million in fiscal '17 to then $55 million in 2018.” (Source: 3Q16 Earnings Call CEO: Bob Whitman)

CEO explaining business model transformation of AAP: ( Source: 2Q16 Earnings Call)

“Just like to note 3 ways we expect All Access Pass to accelerate our business.

First, it will leverage our significant investments in content development. Over the past 10 years or so, we've invested more than $150 million [ph] in content development and content applications, including millions of dollars for content area, developing courses, customize film libraries and tools, creating portals, tools and process to support and sustain lasting changes and performance improvement. As a result, we believe that we're better positioned than anyone in our space, providing offering such as the All Access Pass. Recently, some clients have purchased All Access Pass have told us that whereas in the past, they had many different content suppliers. Now that they have purchased the All Access Pass, with its extraordinary quality, flexibility and reach, they are dropping the rest of their content suppliers and using the All Access Pass as the foundation for all their people development and performance improvement needs. That won't happen obviously in every case, so it has a powerful impact.

Second, All Access Pass also leverages our significant investment in practices and in building integrated solutions with premium services. While many will find -- many customers will find that all or a significant portion of their needs to be met with All Access Pass content alone, others will find that purchasing additional services, co-chair events, toolsets will help them to achieve their objectives in certain areas. Perhaps a little bit like Gartner Group on top of the platform of intellectual property sales, where they have add -- another 1/3 of their revenue comes from premium services, we have built a strong capability around these services for execution, Sales Performance, Customer Loyalty, et cetera, and we believe that this All Access Pass at the center of the circle, we can add pieces around the circle where it will be a natural way to go bigger and broader inside companies.

Third, we expect that All Access Pass will allow us to better leverage our broad reach and strong go-to-market approaches. It creates one compelling offering, which can be sold by all of our sales forces worldwide, in addition to the individual offerings that they sell. It gives one consistent offering that can be sold that we think it has the potential to help our sales force to ramp up even more quickly, create larger and more pervasive client engagements and sell additional services.

We have operations in more than 100 countries either directly or primarily through our licensee network. And having one offering that we can sell across the world in multiple languages creates a big competitive advantage for winning global deals and really establishes given the costs and difficulty of getting the content and getting it all translated establishes a large barrier to entry for others. These global deals are becoming an increasing portion of our revenues. So while this will be just one of the offering, just an -- this is just added to our array of existing offerings, it provides a particular -- particularly strong value proposition for those in the circumstance of having lots of different jobs to be done and not having the resources to really do it or having to work with 30 different suppliers to meet those.

Finally, in terms of ways it will impact. As we expect, it will create increased recurring revenue. We expect the smaller clients, All Access Pass will increase our average revenues from transaction even after deferring approximately what was in this last quarter, 37% of the revenue, from each All Access Pass sale due to the value associated with the access as to our digital content library. I figured it will also increase our renewal rate for these smaller customers. It also increases our deferred contract values. I mentioned that to give you an idea of that in a minute. But with this deferred revenue of $1 million in this quarter, we expect that could be many millions by the end of this year.”

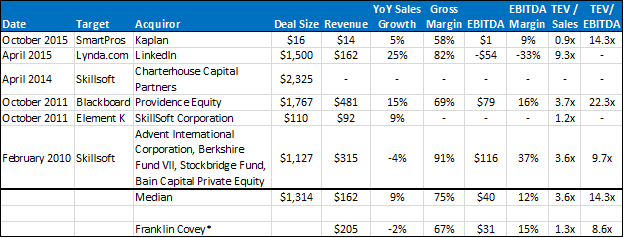

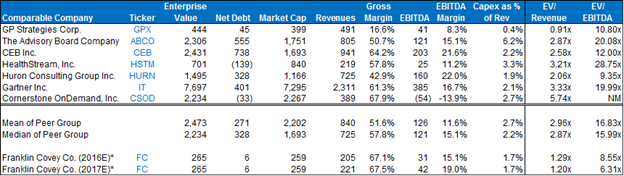

Comps:

*2016 Estimates

*Estimates

http://www.franklincovey.com/ 7 verticals

http://www.theleaderinme.org/ very strong brand in K-12 $40 million a year business...teaches Leadership.

Disclaimer: This does not constitute a recommendation to buy or sell this stock. We own shares of the company, and we may buy shares or sell shares at any time without updating the board.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

Catalysts:

-

All Access Pass ramp up: Much better value proposition for the customer (100% of content), want web based vs. paper, FC generates 40-50% higher revenue, becomes platform SaaS business, gets much higher multiple than 6x with great FCF margins.

-

New Subscription products rapid growth: All Access Pass $30-40 million in FY 17 (August) 15-20% of total revenue

-

Significant EBITDA: $20 million is the guidance for the quarter (seasonally best qtr)

-

Resuming EBITDA growth: $40 Million + in 2017 ($3.00 per share +/-)

-

Likely continued aggressive share repurchases given strong free cash flow, access to capital, and repurchased 18% of company at current valuation over the last 24 months

-

FC should grow its access to capital from $50 to nearly $100 million over the next 12 months and most likely place to reinvest capital is aggressive share repurchases.

-

We would love to see an increase to $80 million share repurchase and if executed at $20, the share count would be down to 10 million and pushing $4.20 in EBITDA per share for 2017.

| -1 show sort by |