| 2015 | 2016 | ||||||

| Price: | 41.00 | EPS | 3.60 | 3.65 | |||

| Shares Out. (in M): | 614 | P/E | 12.4 | 12.2 | |||

| Market Cap (in $M): | 251,500 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | -9,465 | EBIT | 0 | 0 | |||

| TEV (in $M): | 17,435 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- FRANKLIN RESOURCES INC BEN 03/11/2019

- FRANKLIN RESOURCES INC BEN S 07/27/2016

- FRANKLIN RESOURCES INC BEN 02/29/2016

- BETA

- PERRIGO CO PLC PRGO 03/08/2016

- CALAMOS ASSET MANAGEMENT INC CLMS 06/27/2016

- JARDEN CORP JAH S 03/16/2012

- FRANKLIN STREET PROPERTIES FSP S 09/17/2010

- Franklin Covey FC 10/02/2002

- Village Supermarkets Cl A VLGEA 04/06/2001

- LEGG MASON INC LM 09/13/2011

Description

Buy BEN at recent prices of $41-42

INTRODUCTION: Downside protected by 8-9% earnings yield and net cash equal to roughly 40%+ of market cap

At recent prices in the low $40s, BEN trades at a P/E (LTM) of 11x. This is in the lowest decile of the S&P 500 even though Franklin’s return on assets is in the top decile and return on equity is in the top quartile. Moreover, Franklin holds over $15 per share of net cash and investments. The stock is not in favor with Wall Street brokers: just three of 20 analysts rate the stock a “buy.” The stated concern is punk near-term earnings growth given Franklin’s significant contribution to assets under management from fixed income funds held by retail investors who are expected to sell as they fear returns will suffer from rising interest rates. The unspoken concern is concentration risk given that Michael Hasenstab manages $190 billion, primarily the Templeton Global Bond Fund with over $100 billion.

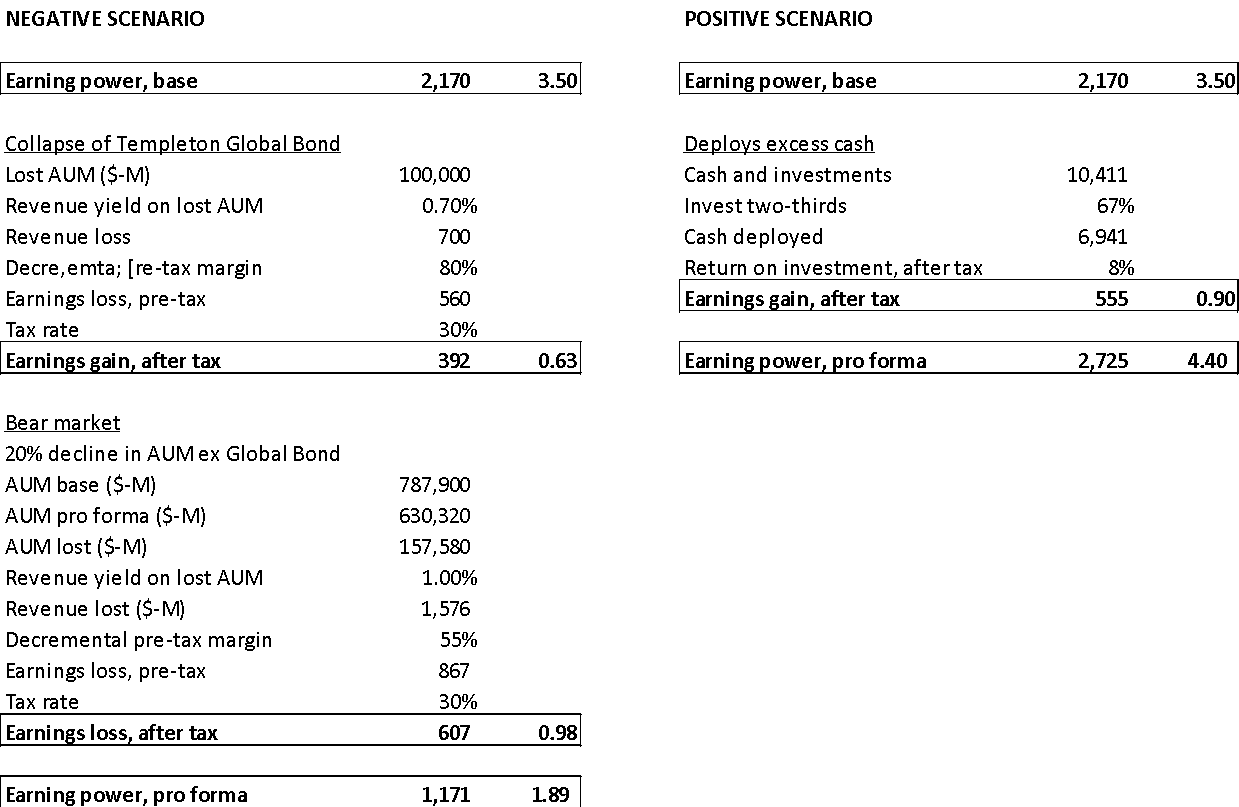

Downside is acceptable. Even should Franklin lose $100 billion from Global Bond and suffer a 20% bear market decline in the rest of its products, the earning power would still be $1.90 - $3.25, depending on whether it deployed any of its cash and the return on investment. This is a 4.5% - 8% yield on the current price, and the company would still have $4 per share of net cash. If the market ignored the cash and priced the stock at an 8-9% yield on $1.90, the value would be ~45% below the current price.

Upside is significant for such a quality business. Deploying just two thirds of the company’s $15 per share of cash at 8% could raise earning power to $4.40, even after adjusting the current run-rate down to $3.50 from the current run rate of $3.79 given my view that the company is over-earning. At a 20x multiplier, which has happened 15-20% of the time since 1992, the value is $88 or over 110% upside.

BUSINESS OVERVIEW

Franklin Templeton Investments is a global investment management company with $865 billion in assets under management. The company employs a staff of 650 investment professionals in fourteen different locations globally aiming to produce superior investment decisions for client assets under management in fixed income and equity securities. The company’s investment products are sold entirely through financial intermediaries such as broker-dealers, financial advisers, and banks.

Franklin is different from other asset managers in several ways:

-

Weak in faster growing new products like passives, alternatives, and solutions;

-

Strong brand names, including Franklin, Templeton, and Mutual Shares;

-

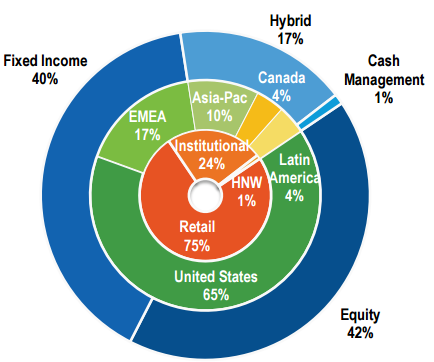

Diversified product offering with 40% fixed income, 40% equity, and 20% hybrid products;

-

Diversified customer base with half the products global and one-third of the investors outside the US;

-

Scale, both at the firm level and the product level, to leverage the global infrastructure;

-

Family ownership (30%+) and management (CEO and COO)

Franklin’s products in hot newer areas like passives, alternatives, and solutions are weak. Management has been developing product offerings in response to growing demand for solutions and alternatives, but the company has no passive product offering. The company’s AUM, revenue and profitability have all benefited during the past decade from growing popularity of its global product offerings.

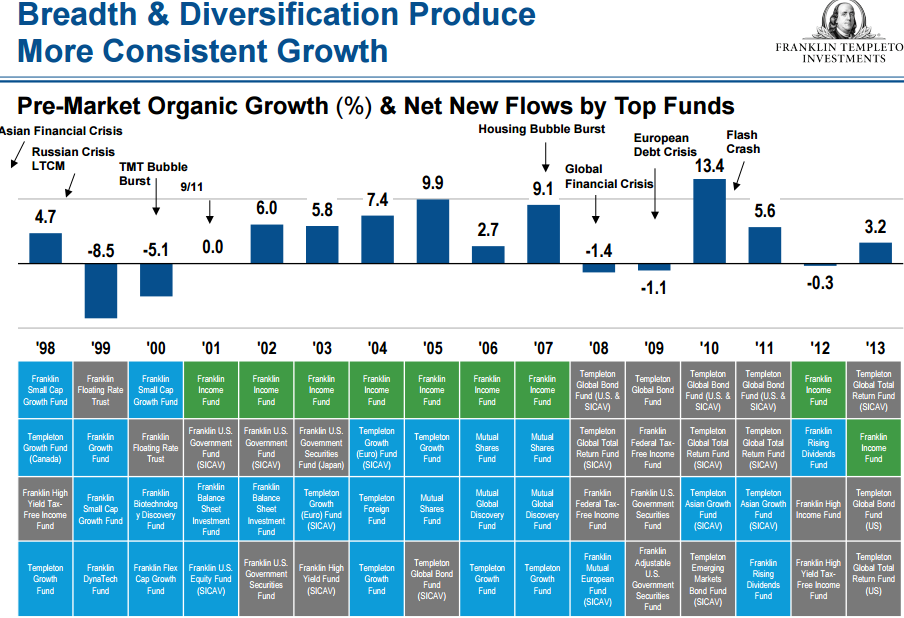

The three major brands are trusted and well recognized. Each of the three key brands (Franklin, Templeton, Mutual Series) has been around for over 60 years. Accordingly, a considerable amount has been spent on marketing to establish brand recognition. The funds are distributed by 1,400 intermediaries in the US and 3,400 internationally. Moreover, the funds have strong long-term performance and are associated with well known individuals. These two factors garner additional publicity and further name recognition of the brands. For some examples, see the slide below. All of the above factors contribute to what Morningstar calls: “some of the best-known brands in the industry.” In my own quick search, I did not find any direct evidence in support of this claim (i.e. brand awareness survey results).

A diversified product offering and client base should contribute to more stable AUM and cash flows. Franklin’s assets under management are balanced among traditional product lines with 40% in equities, 40% in fixed income, and 20% in hybrids. The company also has a diversified client base, with over two-thirds of customer assets from outside the US. The company relies more on retail than on institutional investors – retail accounts for 75% of assets under management – and the fickleness of retail investors has the Market worried about fixed income flows.

Diversification is valuable if it contributes to more stable levels of assets under management through different cycles. The value of diversification is difficult to evaluate because asset price cycles are so long (e.g. 30 years of falling interest rates). The value of diversification is easier to understand by inverting the case and studying concentration. The common cause for near death experiences amongst asset managers, like Artio and Pzena and even AllianceBernstein, has been a combination of bad performance in one product and sophisticated institutional clients. This combination can put companies in a negative feedback loop: bad performance -> client A pulls AUM -> client B fears pressure on revenue and bonuses will cause PM defections -> more AUM is pulled and bonuses are pressured.

Franklin has the sort of scale that delivers high profitability. Scale can be a positive or negative for investment managers. For AllianceBernstein, the company entered the bear market of 2008-09 with infrastructure to grow into. And then AUM collapsed by 50% from over $800 billion to nearly $400 billion. Franklin has a large global infrastructure and significant reliance on one product – Templeton Global Bond – that accounts for 10-15% of AUM. The economies of scale on this one product have enhanced Franklin’s scale and profitability.

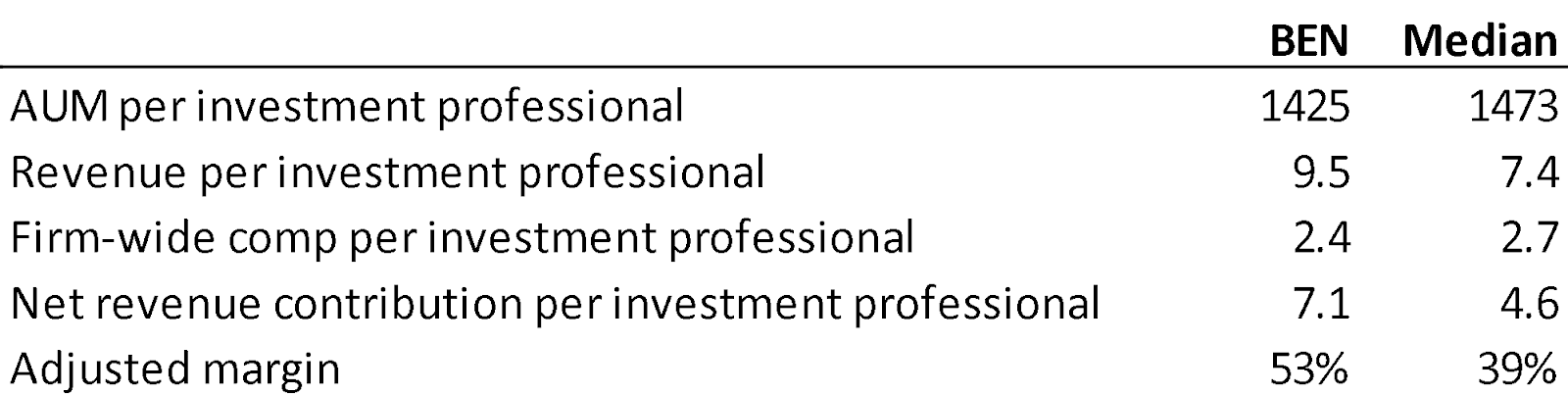

The table below illustrates Franklin’s scale on various metrics. The key metric appears to be the scale of revenue and profitability relative to the number of investment professionals. The $180 billion run by Michael Hasenstab’s 20 person global bond team contributes significantly.

The key driver of profits and business value is assets under management (AUM), which is a function of investment performance and market returns. Franklin earns a fee from customers in exchange for selecting investments. The fee is a small percentage of the value of client assets that Franklin manages. So the more client assets under Franklin’s management, the more fees the company earns from clients. Customers seeking investment counsel often prefer an advisor that has a history of better results than peers or benchmarks. Franklin’s products have a strong long term track record.

Significant net cash position gives staying power. Franklin holds over $10 billion in cash and investment, versus just $1.2 billion in debt. Given the $15 per share in net cash combined with Franklin’s diversified client base, a catastrophic loss of an investment in the common stock is unlikely. The more likely problem would be a significant loss in earning power.

MANAGEMENT: Family ownership and family management

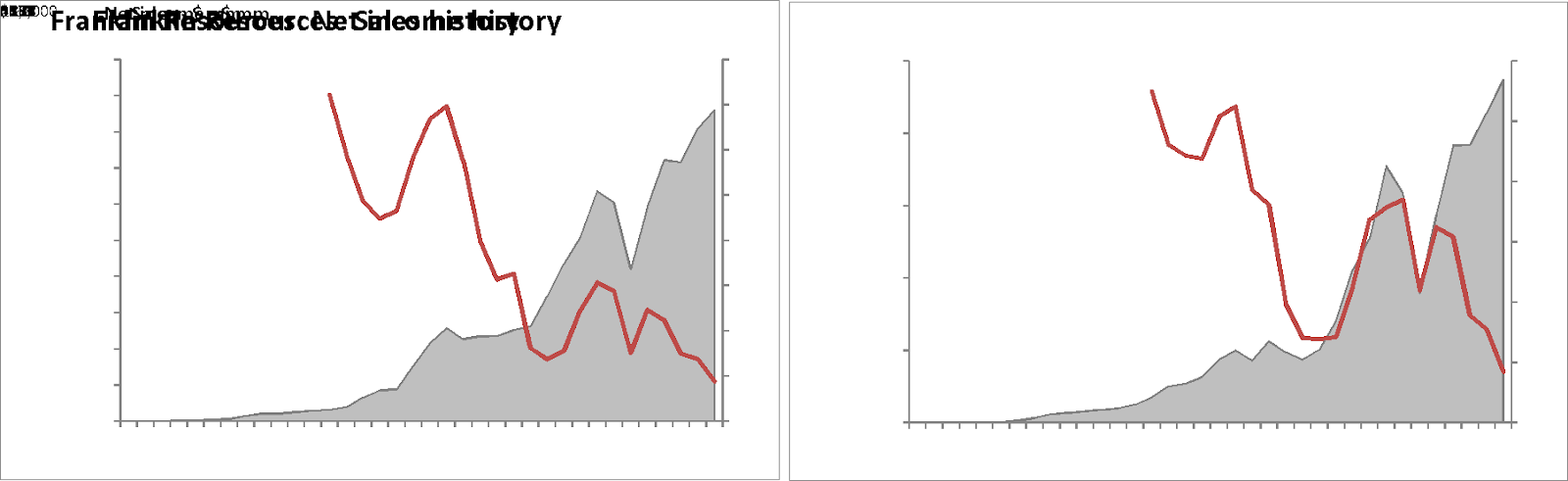

Franklin has posted solid historical results. Management might get the benefit of the doubt from those who take a quick look at historical growth in sales and earnings. The 7-year compound annual growth rate for sales and earnings are now at their all time lows of 4-5% (see charts below which didn't paste well, red line is CAGR and grey is total sales and earnings). While management is gratified by the company’s growth, there are no ambitious growth targets. Instead, the CEO emphasizes the factors within the company’s control that it can influence to drive growth, such as investment performance, customer service, technology, and global infrastructure. Finally, the company has not reported a net loss since 1979, and results are unblemished by regular restructuring or other “one time” charges. During market volatility, management has responded by reducing the cost base.

The Johnson family owns roughly one-third of the company. From a review of the proxy, one learns that no fewer than four family members are employed by the company: two from the second generation, who are sons of the founder, and two from the third generation. One of the older guys serves as Vice Chairman and director, while the other is a portfolio manager. One of the younger generation is CEO and his sister is COO. While I have not met management, feedback from folks who have is that the CEO is pretty good.

Overall, publicly traded family-influenced businesses have higher total returns to shareholders than leading indices, although the financial services sector seems to be an anomaly in this regard (maybe results skewed by AIG). The family seems to emphasize the long-term, which is an explicit aim of the compensation program, and something they highlight about employee tenure: 7% of the workforce has been employed by BEN for more than 20 years. They manage for the long-term by diversification and a very conservative balance sheet. “A strong balance sheet has always been a pillar of our financial management strategy…We are in the advantageous position of not having to rely on the credit markets to meet our operating needs.” (2008 annual letter)

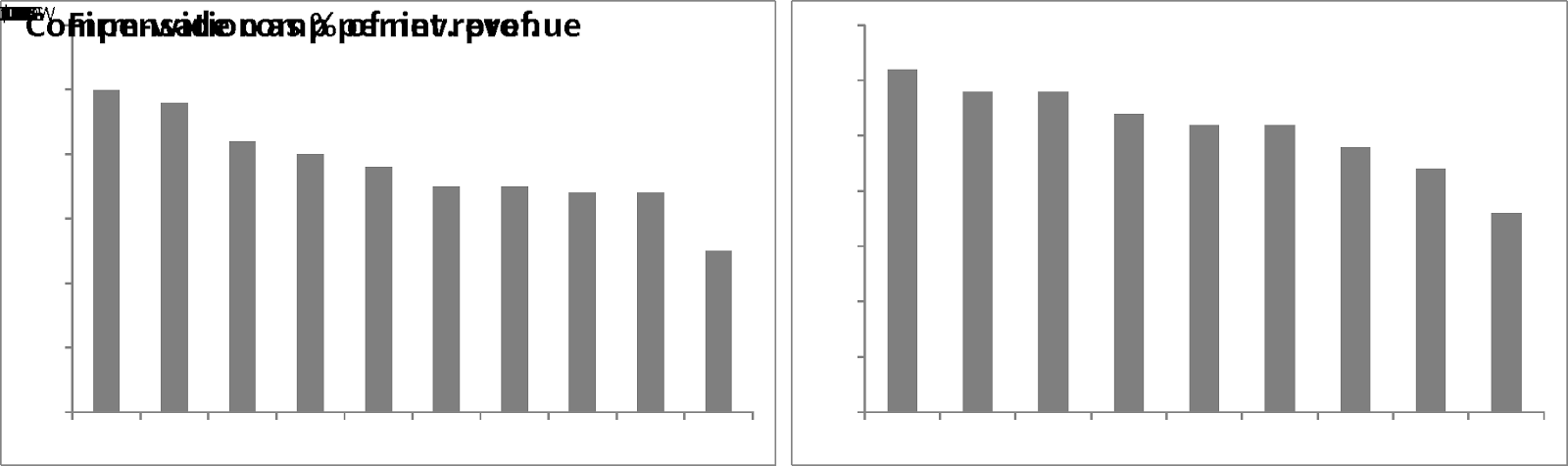

Compensation is conservative relative to peers, according to the company. That is hard to judge definitively. Most importantly, compensation is clearly lower than peers overall, today. Specifically, compensation as a % of net revenue of ~25% is by far the lowest among peers that range from 34% to 50%. And compensation per investment professional is also nearer the low than the high.

But looking at top executive compensation, which admittedly matters less for shareholders, then Franklin looks more middle of the pack. On a cumulative basis for named executives, BEN is only slightly below the median and the average.

The annual bonus pool is not to exceed 20% of pre-bonus operating income, and a portion is paid in restricted stock. Long-term awards are performance based and tied to three year total shareholder returns relative to other investment companies. Historically, the award was based on total shareholder return and operating margin.

Capital allocation has been fine. Franklin has made two significant acquisitions, buying Templeton in 1992 and Heine (Mutual Shares) in 1996. The company paid 10-11x EBITDA, which seems like a bargain today. Otherwise, the company returns lots of cash to shareholders through regular dividends, special dividends, and share repurchase. Most of the share repurchase has been completed since 2007.

The main concern with the company’s capital allocation is the large cash balance. The company has always maintained a cash position that is rather large as a percentage of the market cap. Currently the amount is over 40%.

GROWTH: More a concern than an opportunity in the near to mid term

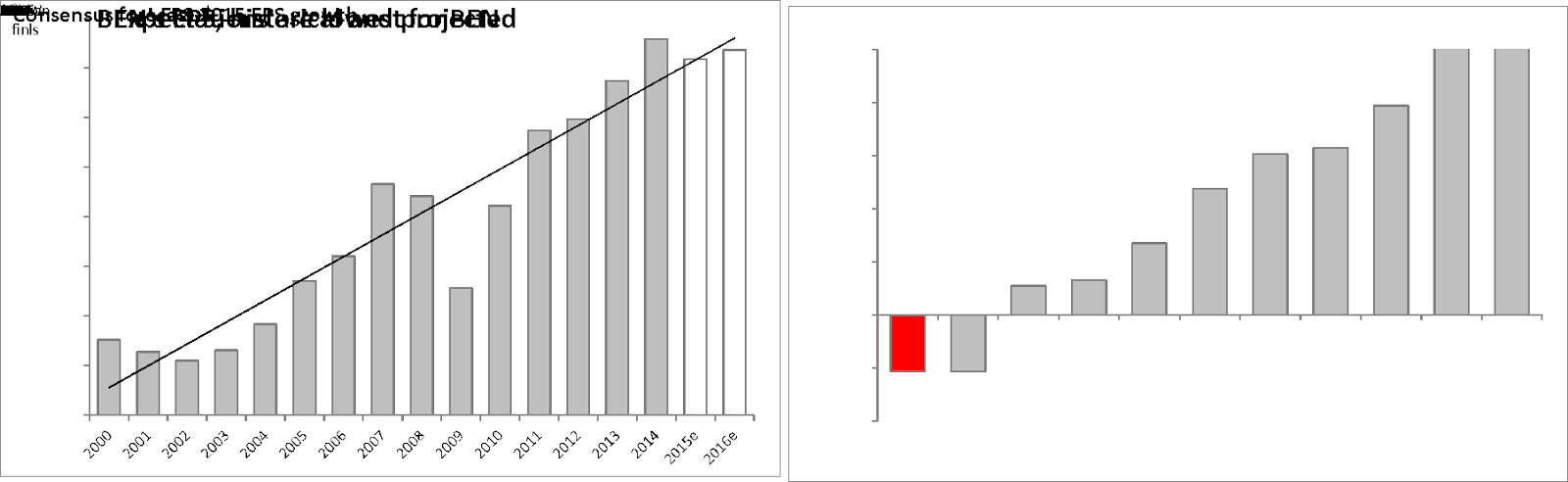

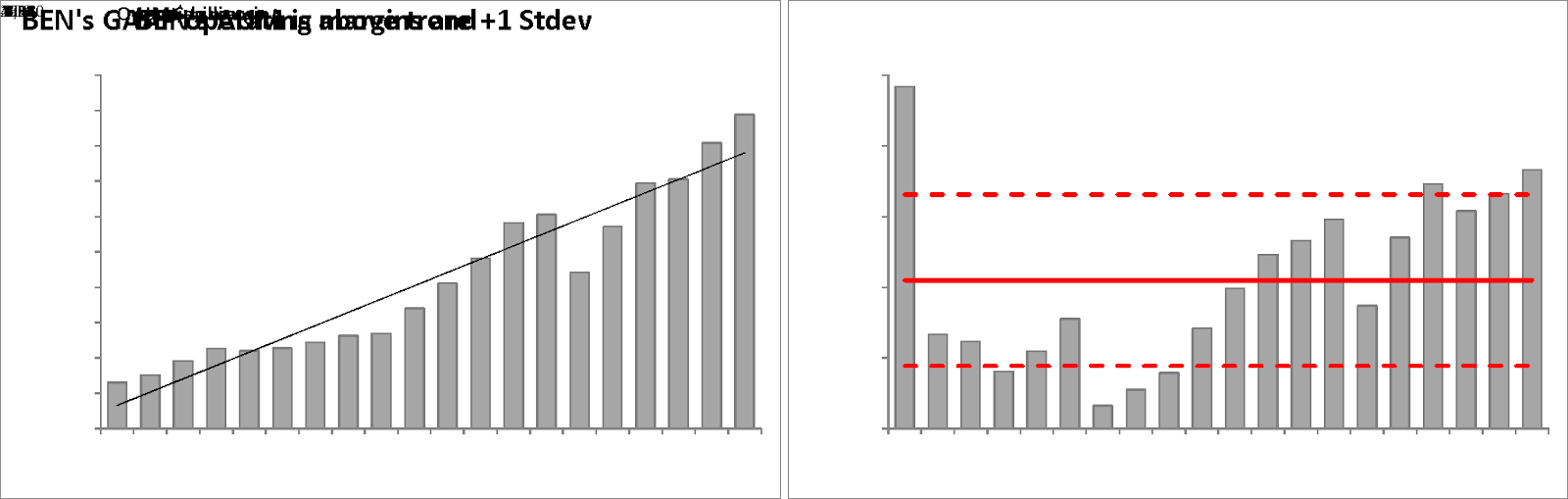

Growth is a bugaboo for the stock. The growth expectations for BEN are low relative to peers in asset management and in lower than 75% of stocks in the S&P 500. The chart below on the right illustrates that the consensus EPS forecast in 2015 for BEN in red is (5%), the lowest among peers, and well below the 12% median for around 150 financial companies. These concerns are somewhat warranted given that BEN’s recent earnings have been well above trend, as depicted by the chart below on the left.

Growth concerns relate to meteoric rise of Global Bond Fund and its contribution to total AUM. Those lukewarm on Franklin point to the under-performance of the stock when rates increase. Although management reports that its bond funds are positioned for negative correlation with US rates, outflows are expected to increase when rates rise.

The other major worry relates to the size of the global fixed income funds managed by Michael Hasenstab and his team. These assets total around $180 billion, about 20% of Franklin’s total AUM. These products have contributed to more than 100% of Franklin’s organic growth during the past decade. While organic growth in assets under management has been 3.6% compounded annually since 2008, without Global Bond, the CAGR is -0.6%.

Earnings are above trend for several reasons. First, the markets have appreciated significantly during the past several years, and assets under management are above the long-term trend (chart below on left). Second, the company’s operating margins are high relative to history and to peers (chart below on right). Management seems to acknowledge that normal margins are a bit lower. Specifically, half the long-term performance awards are tied to operating margins, and the 100% payout is awarded for achieving margins of 31%. The margins in the past five years have been well above this level: 38%, 37%, 35%, 37%, and 34%.

Conversely, more than $10 billion or $15 per share of cash and investments sit fallow on the balance sheet. If these were deployed more aggressively for a pick up in returns of 5% that would add $0.85 or nearly 25% to the 2015 EPS forecast.

Longer term, concerns about the company’s growth prospects are related to its more traditional product mix. Franklin has no passive products, like index funds or exchange-traded funds (ETFs). Moreover, the company’s “solutions” and alternative product offering is not a large contributor. On the other hand, the company has significant exposure to product areas that may experience poor returns and flows, specifically emerging markets and fixed income. In particular, the Templeton Global Bond Funds account for 10-20% of AUM. Ten years ago, the largest fund was only 9% of AUM.

Asset management should be a stable business – just avoid terrible performance. The industry’s traditional players face some challenges. For example, an increasing number of savers will choose passive strategies like exchange traded funds and index funds. And changes in distribution may re-allocate the profit pool. But the business is still pretty good. The outlook for demand is stable because most savers will seek professionals to allocate their investments. While ETFs and index funds have an appeal, a sufficient number of people will pay for the hope and opportunity of better than average performance. Hard work and emotional discipline will remain critical drivers of performance. But firms that deliver only average performance should still generate high returns. The main thing is to avoid terrible performance.

High returns on capital because nearly all the capital employed is the client’s. According to McKinsey, “the U.S. asset management industry continues to be the most consistently profitable business in financial services.” That isn’t saying much. The average ROE for FDIC banks during the past 20 years has been 11% with one standard deviation equal to 5%! But returns for asset managers have been superior to the S&P 500 too. The average ROE for the S&P 500 has been 15% while a group of 20 asset managers have returned 29% on equity and 15% on assets.

Industry does not require much capital to grow, but Franklin may be an exception. Normally, asset management does not require much capital for growth. And Franklin has a strong global infrastructure to support expansion. But Franklin may need to acquire in one of the higher growth product areas in order to revitalize its growth rate, and the company has $10 billion of cash on hand to fund deals.

The key driver of growth (and multiples) has been net flows. During the past decade, net flows have been the primary driver of growth since market appreciation has been muted. In retail, for example, net new flows accounted for 68% of growth, twice the contribution of market appreciation. And net flows are a key driver of P/E multiples. But only about 20% of asset managers have sustained above-average net new flows and growth in the past decade. The best growth has been achieved by large global specialists (more than 65% of AUM in one asset class). The biggest decline has occurred at large generalist firms which lost 6 points of AUM share over the last full cycle. Finally, independent players have significantly outgrown those firms owned by banks or insurers during the last cycle. Their share has increased from 28% of AUM in 2002 to 54% in 2011.

MARGIN OF SAFETY: in cash on hand, strong free cash flow, family ownership, and low P/E

Family ownership brings fiscal conservatism: Franklin has a strong balance sheet. Throughout history, the company has emphasized the importance of a strong balance sheet and has acted in concert with this principle. “A strong balance sheet has always been a pillar of our financial management strategy…We are in the advantageous position of not having to rely on the credit markets to meet our operating needs.” (2008 annual letter)

The balance sheet looks especially strong today. At the end of June 2015, Franklin held cash and cash equivalents of $10.8 billion. That is about 40% of the market cap. Only one-third of the cash is held in the US, while the rest is “trapped” overseas. This liquidity is significantly larger than the company’s $1.3 billion of debt, which consists of four issues maturing in 2015, 2017, 2020, and 2022.

BEN shares currently trade at a 8-9% yield, higher than 92% of stocks in the S&P 500. Franklin is a decent quality business when considering the high returns on capital, low capital requirements, and low financial leverage. I like the family ownership because it usually enhances stewardship and capital allocation over the long term. More surprising is the pedestrian valuation. The earnings yield is higher than 90% of stocks in the S&P 500. The company may be over-earning a little, but trying to normalize for that somewhat still results in an earnings yield higher than most alternatives.

While P/Es relative to a company’s own history may not be useful, nonetheless, I take some comfort from the fact that while the P/E for Market is near all time highs, the P/E for BEN is one standard deviation below the average from the past 13 years.

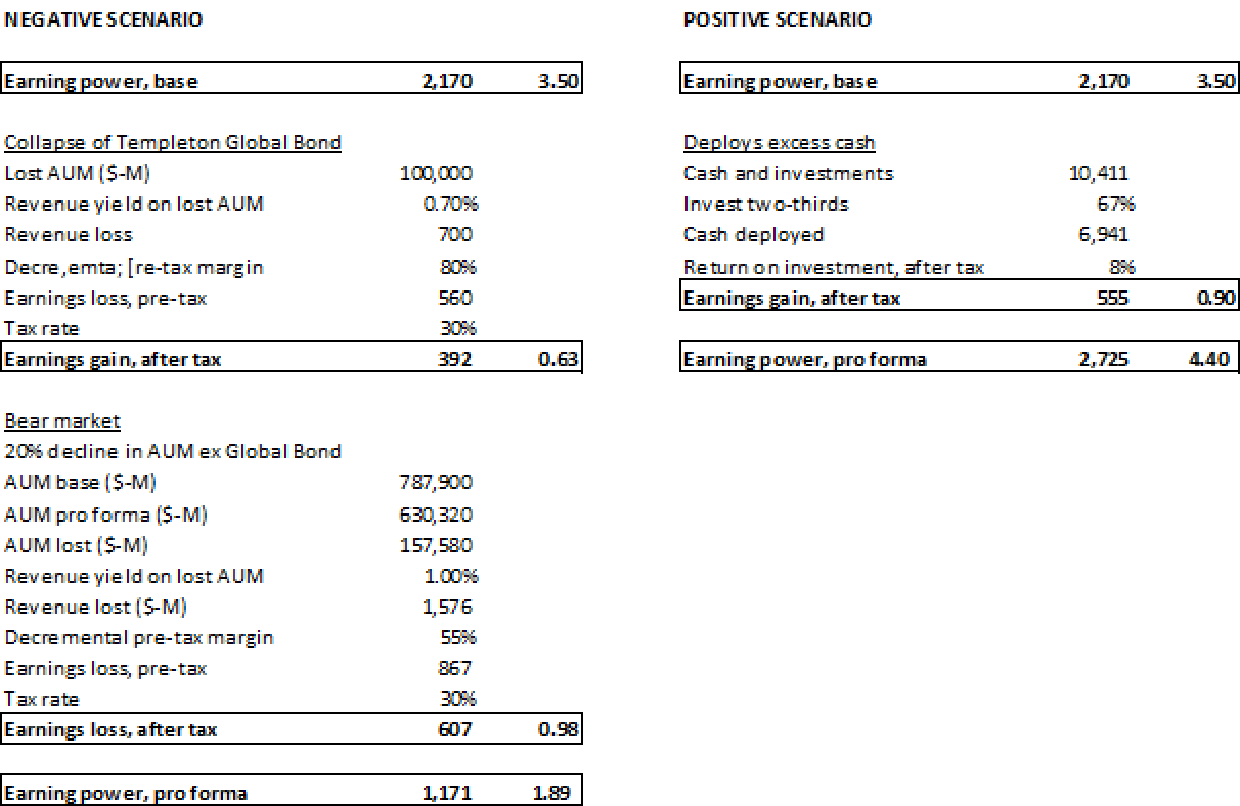

Scenario analysis points to earning power of $1.90 to $4.40. In a downside scenario, the value could approach $24 based on earning power of $1.90 at an 8% yield. This is ~45% below recent prices in the mid $40s. In addition to a business that was yielding 8% on cyclically low earnings, one would get $15 per share of net cash. That would reduce the cost basis in the business to $9, or a 20% earnings yield. In the downside case envisioned, the value of Franklin’s cash would increase because the supply of liquidity would decline. Hypothetically, Franklin could deploy the cash at higher returns, perhaps over 10%. In that case, there would be $1.50 of latent earning power, another 6-7% of the $24 stock. So the potential earnings yield at $24 would be between 8% and 14%.

The downside scenario I envision results from two big problems. First, the Templeton Global Bond Fund collapses and AUM in the product decline by $100 billion. The earnings lost would be about $0.65 per share. Second, the markets experience a bear market, so the remaining $765 billion of Franklin’s AUM decline by 20%. The earnings lost would be about $1.00.

In a positive scenario, the value could approach $88 based on earning power of $4.40 at a 5% yield. This is 110% higher than recent prices in the low $40s. The company would still have nearly $4 per share of net cash, the value of which is incorporated into the high P/E multiplier.

There is one large and one small adjustment to earning power in the positive scenario. First, the company deploys two-thirds of its $10 billion of cash at an 8% return on investment. This adds $0.90 to EPS. Second, the current earning run-rate is normalized to $3.50 from $3.79 – which I also do in the negative scenario.

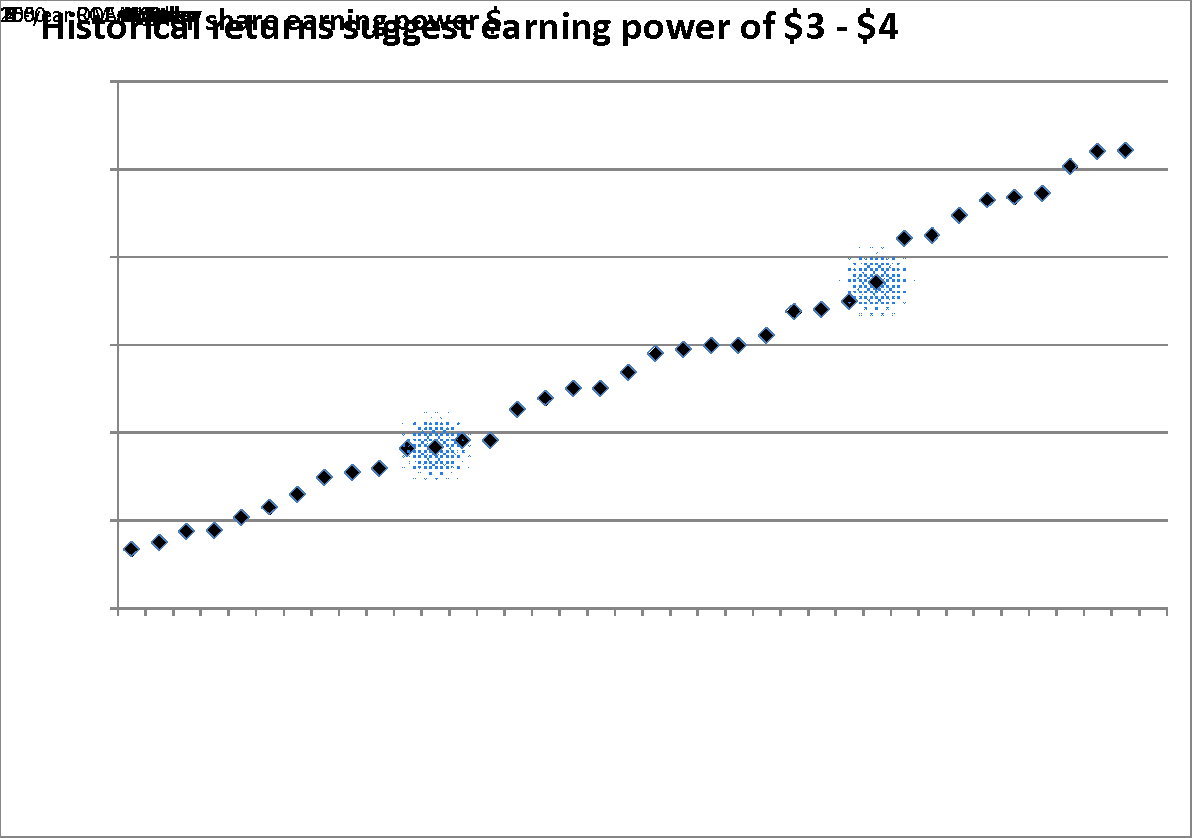

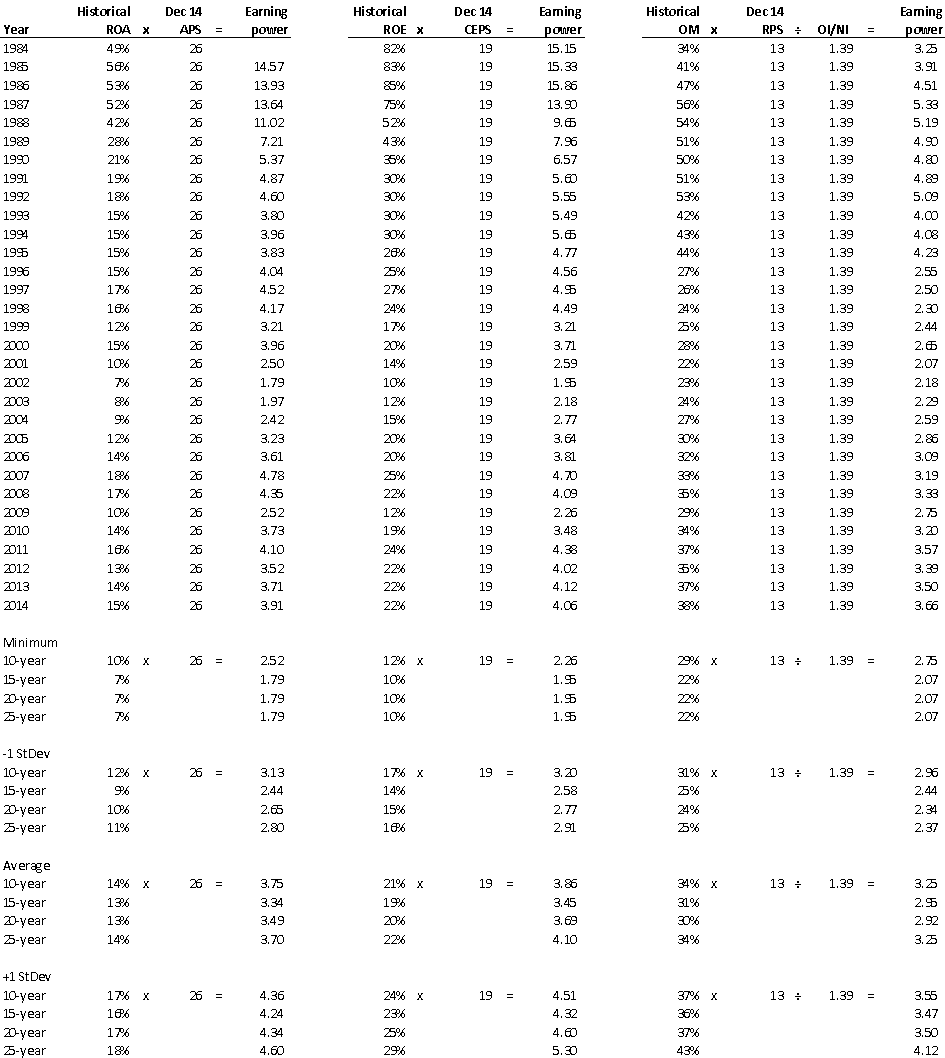

Historical returns suggest earning power of $3 to $4. Reviewing the past 25 years of data, I employed three methods to calculate normalized earnings power. One method employs historical returns on assets applied to the current assets per share. A second method does the same using return on equity. Finally, the third method applies historical operating margins to the current revenue per share. I employed 10, 15, 20 and 25 year averages, plus and minus one standard deviation for each. The chart below depicts the 36 individual results from smallest to largest. For example, the smallest value is $2.34 based on one standard deviation below the 20-year average for the operating margin method. This approach is backward looking and imperfect, but it does provide a foundation for earning power. Historical data for the calculations follows in a table below.

I and/or others I advise do not hold a material investment in the issuer's securities.

Catalyst

Generating a higher return on $15 per share of cash

| show sort by |