| 2019 | 2020 | ||||||

| Price: | 20.00 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 39 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 783 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | -391 | EBIT | 0 | 0 | |||

| TEV (in $M): | 392 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- None found

- BETA

- SYNAPTOGENIX INC SNPX 06/14/2021

Description

G1 Therapeutics, Inc (GTHX)

While binary, G1 Therapeutics (GTHX or G1) stands out as one of our favorite risk/reward set-ups. The stock price has moved in stark contrast to the underlying fundamentals of the company, falling 70% from $67/share to $20/share despite reporting four successful Phase 2 trials for its lead drug candidate Trilaciclib (Trila) over the past year, and solidifying the balance sheet. GTHX is a clinical stage oncology focused biotech with one significant shot on goal and two additional large product opportunities. The combined market opportunity G1 is targeting is currently $10B and could double to $20B over the next few years. The primary program, Trilaciclib, could be the first preventative myelosuppression therapy (harmful chemotherapy side effects) and has been meaningfully de-risked. We think GTHX is worth $80/share making this an attractive entry point.

Fred Eshelman

What initially prompted us to look was board member Fred Eshelman. Eshelman is a phenomenally successful biotech entrepreneur/executive who founded Furiex Pharmaceuticals; one of the best performing investments of my career (10 bagger). Fred has a great record, including founding and running Pharmaceutical Product Development Inc (PPDI) which sold to Carlyle for $3.9bn in 2011. Furiex spun from PPDI and later sold to Forest Labs for $1.5bn in 2014. Lastly Fred knows when to sell as evident by his involvement in The Medicines Company, which Fred left his Chairman of the Board position at the stock’s recent peak this past August. Fred eats his own cooking, investing along-side common share-holders; making him worthy of following. In the case of Furiex, Fred purchased over 20% of the stock personally on the open market (in addition to the 5% he owned at the spin) before ultimately selling the company for multiples higher. While, Fred did not found GTHX, he maintains a 10.5% stake through his family office Eshelman Ventures. He purchased $17.5M in the Series B and C rounds and has added to his position by an additional $9.4M buying the IPO and through open market purchases. Investing alongside Fred has been a perennial green flag.

Background

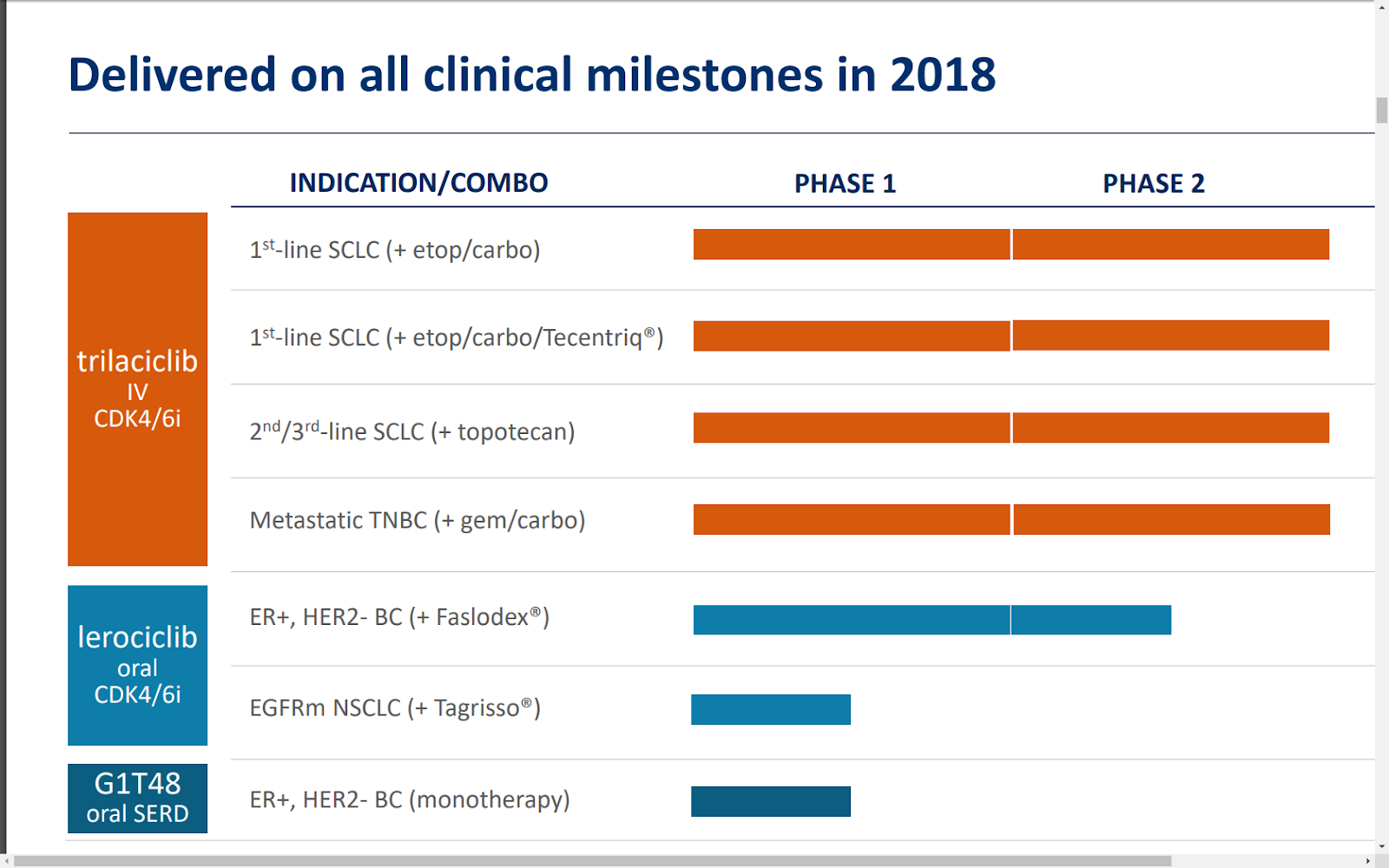

While chemotherapy is effective, the collateral damage to healthy cells is a significant side effect. Myelosuppression is a broad term for the negative effects of chemotherapy impairing the hematopoietic stem and progenitor cells HSPCs (healthy cells). This weakening of the immune system increases the risk of infections and viruses, and induces anemia. G1’s lead drug candidate is the first preventative myelopreservation therapy to protect HSPCs during chemo and minimize side effects. Currently, G-CSF rescue therapies taken in response to side effects are the only option. Trilaciclib (Trila) is a short acting CDK 4/6 inhibitor administered intravenously prior to chemotherapy. Trila has read out 4 successful Phase 2 trials in the past year. In our view Trila is G1’s crown jewel asset.

Lerociclib (Lero), is an oral CDK 4/6 inhibitor in Phase 1/2 trials, with significant potential benefits over existing oral competitors Ibrance, Kisquali, and Verzernio. The current three therapies generate approximately $3.5B combined and are growing rapidly toward street estimates well north of $10B as the CDK 4/6 class of therapies received FDA approval a short 4 years ago. Rounding out their pipeline is G1T48, an oral selective estrogen receptor degrader (SERD) that would compete with Faslodex, which generates $1bn revenue. Faslodex is approved for monotherapy but is often used in combination with current oral CDK 4/6 inhibitors. It is administered by painful intra muscular injections. G1T48 would be the first in class oral alternative. G1’s three clinical pipeline candidates are wholly owned by the company.

Pipeline drilldown

Trilaciclib (Trila)

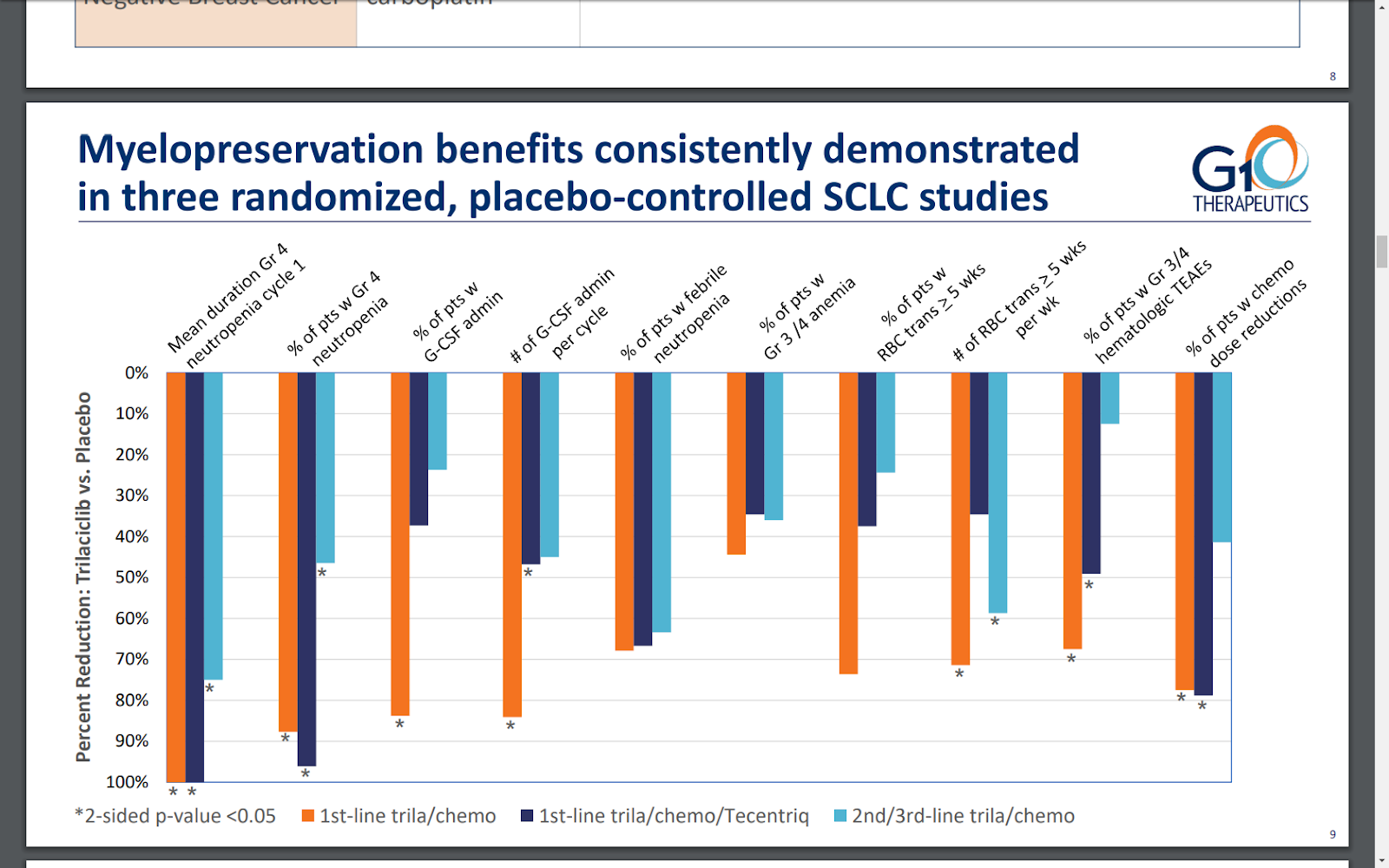

The lead candidate and primary reason to own GTHX is Trilaciclib. The backbone of oncology remains chemotherapy, which is great at killing cancer cells. Unfortunately, chemo also damages healthy cells leading to a variety of complications and expensive rescue therapies. This so called myelosuppression creates morbidity, chemo dose delays and significantly increases the cost of care. As chemo hurts good cells (HSPCs), patients frequently suffer febrile neutropenia and grade 4 neutropenia. Myelosuppression decreases immune system response and increases patient risk to virus and infection. Trila’s mechanism of action preserves HSPCs which allows for prophylactic protection of multi-lineages of healthy cells (neutrophils, red blood cells, platelets and lymphocytes) rather than the current post cell damage rescue therapies including transfusions of red blood cells and G-CSF infusions (Neulasta). Trilacilib is the first preemptive myelopreservation therapy (an IV CDK 4/6 inhibitor) and has shown profound efficacy across 378 patients in 4 separate randomized, placebo controlled Phase 2 trials. Three of the trials were completed in small cell lung cancer (SCLC) and 1 in triple negative metastatic breast cancer (TNBC). All SCLC trials hit their primary endpoint of reduction in duration of grade 4 neutropenia and reduction of percentage of patients with grade 4 neutropenia. It’s important to note that Trilaciclib is not a replacement for standard of care therapy, but is complementary to current treatments. It has shown efficacy with chemotherapy alone, and with chemotherapy plus checkpoint inhibitors which is the more current standard of care. Composition of matter patent protection runs through 2031 and additional method-of-use patents extend the patent life to 2034-2037 timeframe.

Lerociclib (Lero)

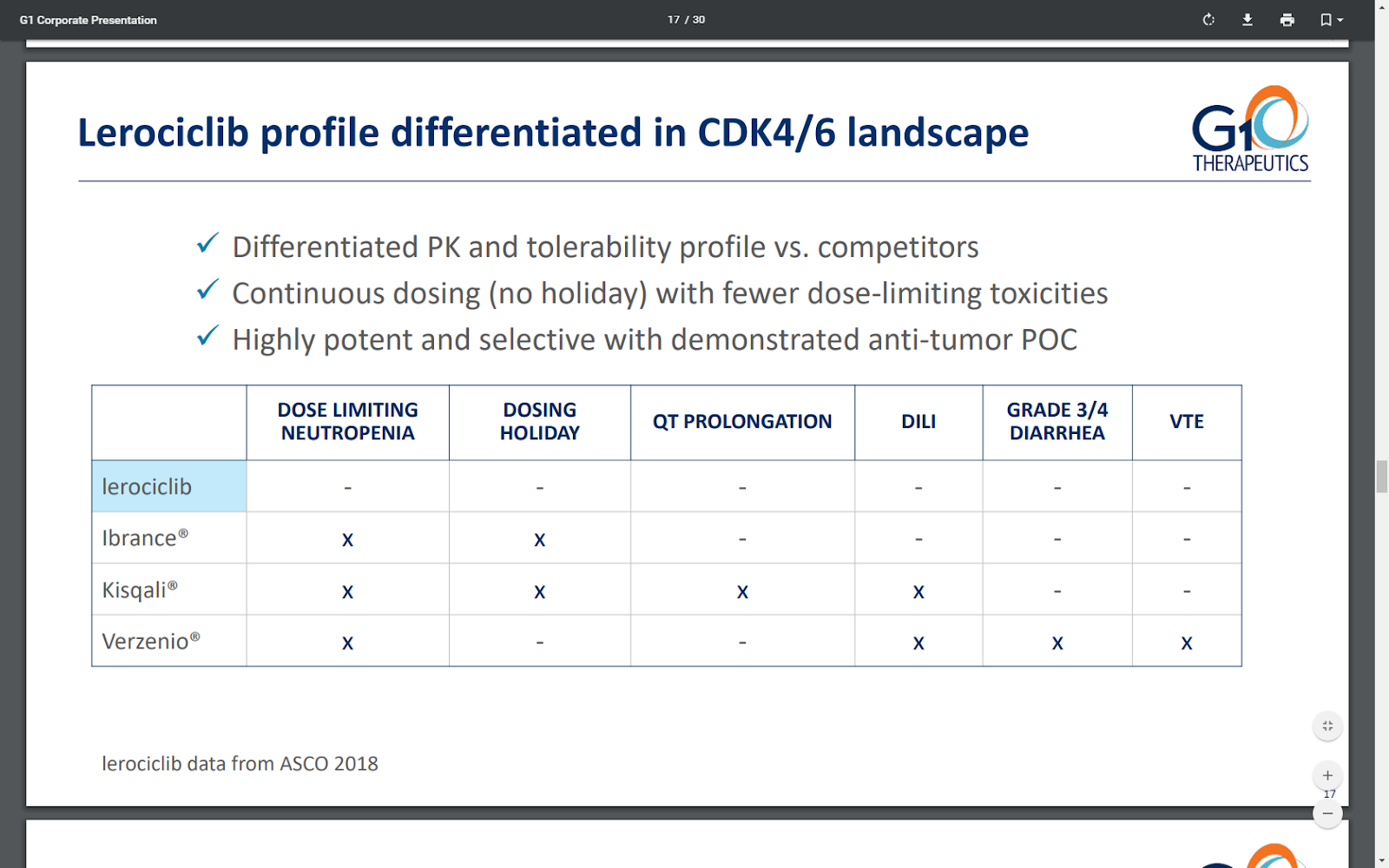

Lerociclib is an oral CDK4/6 inhibitor that has shown safety advantages over the existing competitors. The market is dominated by Pfizer’s Ibrance selling over $3B per year, while newly approved Kisqali (Novartis) and Verzenio (Lilly) currently annualize at $400M and are growing rapidly. Analysts estimate Ibrance peak annual worldwide sales will exceed $7B with a combined market over $12B. Ibrance and Kisqali require dosing holidays while Lero’s Phase 1b does escalation study demonstrated Lero can be dosed continuously with less limiting grade 4 neutropenia. The Phase 1b trial was in combination with Faslodex for breast cancer and also showed preliminary anti-tumor activity. The Phase 2a dose expansion study is enrolling. A second Phase 1b trial in combination with Tagrisso in lung cancer is also enrolling. Pending data, G1 has additional plans to run Lero in trials for prostate, lymphoma, melanoma, and pancreatic cancers. Composition of matter patent protection runs through 2031 and additional method-of-use patents extend the patent life to 2034-2038 timeframe.

G1T48

G1 has an oral Selective Estrogen Receptor Degrader (SERD) currently in Phase 1 dose escalation study as a monotherapy in 2nd/3rd line breast cancer. Faslodex is the only approved SERD and is a painful intra muscular injection, approved for monotherapy and in conjunction with oral CDK 4/6 inhibitors. Faslodex currently generates $1B in revenue. G1T48 aims to be the first in class oral SERD. However, the larger potential value to G1 is combining it with G1’s own CDK 4/6, Lerociclib, to create an all oral solution to ER+ breast cancer. G1 plans to initiate a combination Phase 1/2 trial of Lerociclib+G1T48 in 2019 pending successful standalone data of G1T48 expected later in 2019. G1T48 was licensed from University of Illinois upon which G1 will owe low single digit royalties on net sales. Pharmaceutical composition patent protection runs through 2036.

Why did the stock crater on good Trilaciclib news?

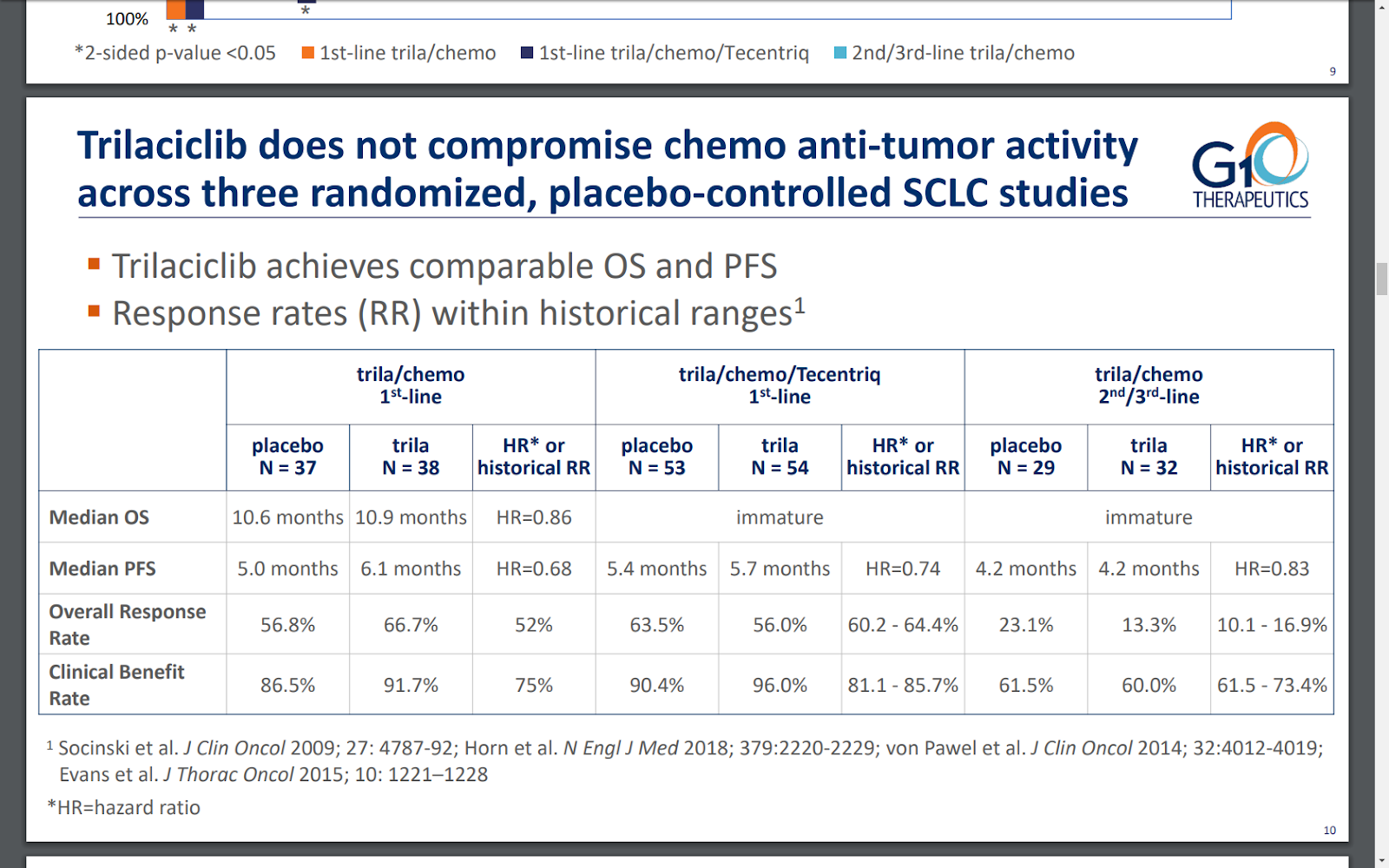

While the primary endpoint of the SCLC trials was myelopreseravation, the secondary endpoints of progression free survival (PFS) and overall response rate (ORR) did not show any difference versus placebo. Overall survival (OS) was only disclosed in the 1st line Trila+chemo trial as the data is immature in the other trials. This overshadowed the statistically significant successes on the primary endpoint. The miss on PFS and ORR is surprising since patients experiencing less side effects of chemotherapy should theoretically be able to tolerate more rounds of chemo and demonstrate better outcomes. Management contends that the two first-line SCLC trials have such high response rates to current standard of care that lowering the side effects probably shouldn’t increase the efficacy even if it makes chemo more tolerable. For the second/third line trial management contends that improvements in PFS and ORR were not observed (OS is not yet known due to data immaturity) because late stage SCLC is so aggressive that it is very hard to effect the standard of care 3.5 month of PFS. While these explanations on survival efficacy sound rational, they are only conjecture at this point. However, we think the primary endpoints of myelopreservation are more important.

Conversely, the metastatic breast cancer trial showed statistically significant increases in PFS across an analysis of its two treatment arms vs. placebo. Management attributes this to the slower growing nature of tumors in TNBC vs. SCLC allowing more cycles of chemo+Trila treatment before disease progression. While the TNBC trial did not statistically reduce neutropenia it did achieve statistical significance in lowering G-CSF administrations and lowering red blood cell transfusions. Trila patients also remained healthy enough to receive more cycles and more weeks of chemo therapy. The market has weighed in skeptically on G1’s recent data despite what we and the company view as good outcomes. After announcing the third SCLC data in mid-December the stock fell 50%, one sell side analyst report title put it best, “4th Trial Positive: Can the Stock Take More Good News?”

The company is meeting with the FDA this quarter to determine the appropriate regulatory path going forward. Management has intimated, and we agree, that there is some likelihood that the FDA encourages the company to submit an NDA for SCLC based on the already completed 3 Phase 2 trials. This would be a homerun scenario and the complete opposite conclusion the market has opined on the data. The FDA more likely will require a Phase 3 trial. Looking forward, the company will likely need to do additional trials for breast and other solid tumors to achieve its ultimate goal of a tumor agnostic myelopreservation label. While the market is treating the recent data readouts as mostly failures, there are number of reasons why we believe the data is excellent:

-

The primary endpoint of myelopreservation was achieved with statistically significance in all three SCLC trials which were double blind and placebo controlled. This is generally the most important aspect of a clinical trial. The type of sell off in GTHX’s stock on the data is usually reserved for trials that miss their primary endpoint but maybe hit some secondary endpoints.

-

The FDA had advised the company on its trials and is supportive of the myelopreservation primary endpoints company has chosen. The company did not design its trials in a vacuum. They have been engaged with the FDA.

-

G-CSF rescue therapy Neulasta was approved on the basis reducing the duration of grade 4 neutropenia, which Trila hit with very high statistical significance in all three SCLC trials (plus trial provides additional multi-lineage benefits).

-

The therapy is safe and well tolerated. From a high level, why wouldn’t one want this therapy? There is minimal downside and patients are less sick during chemotherapy, which means they feel better and have lower expensive hospitalizations for sever neutropenia, virus, and infection. They also require less doses of G-CSF rescue therapy saving $4K+ per administration.

-

Newly issued guidance from the FDA for clinical trial design in oncology fits with Trila’s efficacy in reducing toxicity (myelopreservation) without impairing the anti-tumor efficacy of the underlying chemotherapy.

Capitalization

As of 9/30/18, G1 had a healthy cash balance of $391M ($10/share). GTHX has been prescient in their capital raising, taking in $94M at $29.50 in March of 2018 and $195M at $60 in September of 2018. G1 spent $63M in 2017 and $63M in the 9 mo YTD and expects current cash to provide runway through mid-2021.

Market size and valuation

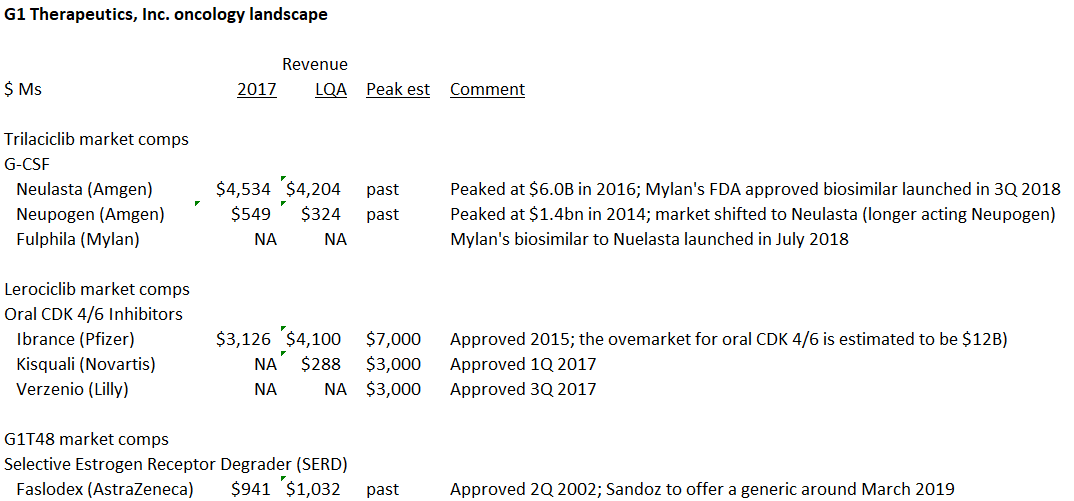

Valuation of a clinical stage drug development company is an inherently subjective task. Precision is subject to the “garbage in-garbage out” adage where small changes in underlying assumptions produce enormous swings in NPV calculations. At the current price of GTHX, we think precision is unnecessary. If Trilaciclib is approved, GTHX should be worth multiples of the $780M market cap ($390M enterprise value). Additional upside could be generated from Lerociclib, G1T48 and combo Lero+G1T48. To frame the context on valuation, below is a table of sales the various competitor drugs and competitor markets.

G1 has provided its own preliminary analysis of the market for Trilaciclib generated from surveys of 100 doctors and 15 payers and concluded that a SCLC indication is worth $1B in revenue, TNBC is worth an additional $1B and a tumor and chemo agnostic label adds an additional $2B+ of commercial opportunity. In the context of the current Neulasta $4-5B market, this makes sense. Trila reduced G-CSF administration per chemo cycle by 45% to 85% across its three SCLC trials and by 50% in the TNBC trial. The Neulasta market is the closest analog to potential for Trilaciclib, however it’s not perfect. Trila is taken preventatively ahead of chemo to prevent severe neutropenia as opposed to G-CSF/Neulasta, which is a rescue therapy for patients whose neutrophil counts have already bottomed out. The multi-lineage protection of Trilaciclib goes beyond protecting neutrophils, but also protects platelets, lymphocytes and red blood cells equating to less red blood transfusions. By preventing healthy cell damage prophylactically, commensurate reductions in febrile neutropenia, viruses and infections should decrease hospitalizations which are a significant cost savings for payers and clearly better for patients.

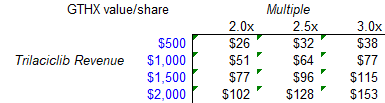

Below is an undiscounted range of value based on revenue multiples across varying sales outcomes for Trilaciclib. Trila could be approved in 2020 in SCLC, though that could materially be pushed back pending feedback from the FDA in Q2.

Only valuing the company on Trilaciclib:

The range of outcomes is large and obviously contingent on an approval of Trilaciclib. Investors can choose their own discount rates and haircuts, but we think the approval outcome of Trilaciclib is a homerun for the stock. Beyond Trila, the potential value of Lerociclib, an improved oral CDK 4/6 inhibitor is significant in the context of a $5-12B market. G1T48 as an oral SERD is very early stage but a significant improvement over a painful intra muscular injection competing for $1B. The 70% selloff of GTHX despite achieving positive statistically significant outcomes in their primary endpoints across multiple phase 2 trials creates a very attractive valuation for G1 Therapeutics.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

Catalysts

-

March 6 Investor day

-

Feedback from Trilaciclib’s regulatory path; best case scenario would be submitting an NDA on based on the Phase 2 data

-

Overall Survival Data from Trila+EP/Tecentriq 1st line SCLC and Trila+topotecan in 2nd/3rd line SCLC

-

Lerociclib additional Phase 1b data from breast cancer Lero+Faslodex trial

-

Lerociclib preliminary Phase 1b data from lung cancer Lero+Tagrisso trial

-

G1T48 Phase 1 monotherapy data

-

Lerociclib+G1T48 Initiate Phase 1 trial for breast cancer based two GTHX therapies

-

Partnering opportunities with their assets as GTHX holds global rights to all three of their programs

| show sort by |