| 2022 | 2023 | ||||||

| Price: | 2.35 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 3,949 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 9,281 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | -5,978 | EBIT | 0 | 0 | |||

| TEV (in $M): | 3,303 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- None found

Description

CERTAIN STATEMENTS CONTAINED HEREIN REFLECT THE OPINION OF THE AUTHOR AS OF THE DATE WRITTEN. NO INVESTMENT DECISIONS SHOULD BE BASED IN ANY MANNER ON THE INFORMATION AND OPINIONS SET FORTH IN THIS REPORT. YOU SHOULD VERIFY ALL CLAIMS, DO YOUR OWN DUE DILIGENCE AND/OR SEEK ADVICE FROM YOUR OWN PROFESSIONAL ADVISOR(S) AND CONSIDER THE INVESTMENT OBJECTIVES AND RISKS AND YOUR OWN NEEDS AND GOALS BEFORE INVESTING IN ANY SECURITIES MENTIONED. Please see additional Important Disclaimers at the end of this analysis.

Business Overview

I believe that Grab is the best positioned mobility/food delivery led super-app ecosystem in the world and the only global player with best-in-class franchises in both mobility and food delivery. According to Grab’s 4Q21 earnings presentation, it has #1 positions across SE Asia in high frequency, large underpenetrated total addressable markets (“TAM”) – 71% share in mobility (3.9x the #2 player); 51% share in food (2.1x the #2 player); and 21% share in e-wallet fintech/digital payments (1.3x the #2 player). For perspective, Grab’s relative share/scale advantages is akin to combining Uber and Doordash into a single ecosystem.

Grab was founded in 2012 as part of a HBS business plan competition by classmates Anthony Tan (son of Tan Chong Motor Holdings founder, one of Malaysia’s biggest auto distributors and one of its wealthiest families) and Tan Hooi Long. The business operates across delivery, mobility, and digital financial services and has established relationships with 25MM consumers, >2MM merchants, and >5MM driver partners across >400 cities in 8 SE Asia countries – Cambodia, Indonesia, Malaysia, Myanmar, the Philippines, Singapore, Thailand, and Vietnam. It provides a single “everyday everything” super app that enables millions of people to order food or groceries, send packages, hail a ride or taxi, pay for online purchases or access services provided through its platform such as lending, insurance, wealth management, and telemedicine. Singapore and Indonesia are its two largest markets and collectively account for >50% of Adjusted Net Sales in 2020, while only Singapore accounts for more than 50% of IFRS revenue (Adjusted Net Sales less Customers/Drivers’ Excess Incentives). Malaysia and Vietnam were the other major IFRS revenue contributors at mid/high-teens % each. The company reports results from four major segments:

-

Mobility

Grab dominates across SE Asia except for Indonesia where it splits the mobility market ~50/50 with Gojek. Other reports say Grab has been gaining share over time and has nearly 60% share of revenues given its dominant 60%+ share in the higher ASP car and taxi segment vs. Gojek’s leading 50-60% share in motorbike rides. Given the size of Indonesia’s market, it will be important for Grab to win (or at least maintain its equitable split) with Gojek. Charts below are from UBS report on 12/9/21 (left) and Citi report on 12/15/21 (right):

-

Delivery

Grab is #1 in all markets with the exception of Vietnam where it is a close #2. It is generally a share gainer across these markets. However, I want to note that ShopeeFood (Sea) is a newer entrant into the regional oligopolies. Given Sea’s strong historical execution and super app ecosystem, I believe it is important to monitor its progress and disruption to the market equilibrium. Encouragingly, Sea recently internally announced layoffs in its ShopeeFood business citing focus on sustainable scaling and reallocation of resources on priorities, a signal that competition may be rationalizing. (https://www.channelnewsasia.com/business/shopee-layoffs-southeast-asia-shopeefood-shopeepay-e-commerce-giant-2745751). The chart below from Evercore report on 12/15/21 shows the delivery competition in Southeast Asia.

-

Financial Services

The segment includes both fintech and digital banking. Within fintech, there are four key revenue streams – payments, insurance/investment referrals, remittances, and buy-now-pay-later. Today, revenue is driven primarily from digital payment processing fees charged to merchant partners based on total payments volume (“TPV”) processed through the Grab platform. Currently, I estimate that TPV is split 60/40 on-platform vs. off-platform though off-platform is expected to grow 1.5-2x faster over time. Fintech includes revenue from effective interest earned on loans and advances provided to merchant partners, driver partners, and consumers; fees for wealth management; and insurance distributions. Over the long term, insurance/investments referrals are expected to be the biggest contributor. On digital banking, Grab is in the process of setting up a digital bank in Singapore with Singtel after being awarded a license by the regulator in December 2020; Grab-Singtel was also recently awarded a digital bank license in Malaysia. Financial services increases user retention and engagement vs. cash users – for example, GrabPay users have 2.2x increase in TPV per monthly transacting user (“MTU”), 2.2x increase in 10+ month retention after first use, and a 1.8x increase in % of users who use a 2nd Grab product (>50% of Grab’s MTUs use GrabPay) per its April 2021 investor presentation. While fintech/digital payments is still in top of the 1st inning, we believe there is sufficient TAM to accommodate multiple winners with super apps have structural advantages in customer acquisition, retention, and engagement.

-

Enterprise & Other

This segment has all the other non-core businesses and new initiatives. Today, the largest contributors are advertising (46% of Grab’s merchant partners utilized GrabAds in 2020) and anti-fraud offering to the company’s financial institution partners and on-demand delivery relationships. GrabAds over-indexes on profit given its high margin revenue stream (we estimate ~90% gross margin).

SE Asia is structurally attractive vs. developed markets

Globally, the online food delivery, ride-hailing, and digital wallet payments are in the earlier stages of being penetrated. This is especially the case in SE Asia where the markets and opportunity are structurally more attractive than developed markets for a few reasons: * all stats below are sourced from independent market research report carried out by Euromonitor (commissioned by Grab) and Grab Holdings F-4, unless otherwise specified

-

Large population: There are 670MM people across SE Asia; if considered together as a country, SE Asia would be the third largest population in the world. Population growth is also above average, with the exception of Thailand and Singapore whose flattish growth is more in-line with developed markets’ (source: World Bank 2020 stats) – Indonesia 1.1%, Malaysia 1.3%, Philippines 1.3%, Vietnam 0.9%, Cambodia 1.4%, Myanmar 0.7%

-

Young population: Nearly 50% of its population is

-

Mobile first: One of the largest smartphone markets in the world with >90MM units sold in 2020. The % of households having at least one smartphone was 68% in 2020 and expected to grow to 84% in 2025. SE Asia has one of the most digitally engaged populations in the world, spending on average >8 hours a day on the internet (vs. 6.9 hours globally). The % of SE Asian population accessing the internet daily increased from 27% in 2016 to 48% in 2020.

-

Urbanization: Urban population is expected to grow by >35MM over the next five years. At only 51%, SE Asia’s urbanization rate trails China’s 60.5% and US’ 82.5%.

-

Underdeveloped infrastructure: The Asian Development Bank estimated there is an annual infrastructure investment shortfall of >$100Bn in SE Asia (ex-Singapore) to meet demand which has resulted in undeveloped and increasingly crowded mass transportation as population density is high and increasing. Separately, private car ownership is prohibitively expensive relative to incomes for a large segment of SE Asia. According to Euromonitor, the ratio of car prices to average gross income in SE Asia is on average 6-18x that of the US and average passenger car ownership rate is 80 per 1K people vs. 167 in China and 436 in the US.

-

Leapfrog without needing to break customer habits/inertia: Given the underpenetrated digital market and underserved informal economy, Grab has the opportunity to leapfrog the linear development of advanced economies and scale more quickly and achieve structurally higher rate of adoptions across its categories. The reason: Grab does not have to contend with changing ingrained customer behavior or dislodging strong incumbents (e.g. credit cards, car ownership, etc). Its platform’s superior value proposition (e.g. convenience, access, ease of use, etc) and $ value creation for all ecosystem participants should show through without adoption friction.

-

Large unbanked and underserved population: Demand for financial services has been unmet in SE Asia. Cash payments are >80% of transaction volumes due to lack of cashless payment options or access to cashless alternatives. Digital financial services overcomes some of banking’s the key structural impediments: [1] relative lack of physical infrastructure outside the major cities as it is costly for traditional financial institutions to build physical branches; [2] limited availability of public registers, identification systems and reliable credit information, resulting in limited understanding of the consumer credit profile. The majority of the population in SE Asia is left out of the formal financial services system as >40% of the population >15 years old are unbanked (i.e. lack of a relationship with financial institutions, lack of transactional or demand deposit accounts, not possessing credit cards, not having any type of insurance or not utilizing any long term savings products). Out of the banked population, ~39% is underserved (i.e. having access to only one of a credit card, checking/current account or savings account services). Penetration rates are significantly below developed markets:

-

Highly fragmented and largely offline informal (M)SME (micro/small medium enterprise) economy: As is the case with the typical emerging economy, the local SE Asian economies are driven and mostly comprised of informal businesses, often (M)SMEs. Per Euromonitor, there were >70MM MSMEs in SE Asia accounting for >99% of all businesses in the region and collectively drive >35% of the region’s GDP (gross domestic product) and provide employment to 150MM people. <20% use digital technologies to improve their productivity or expand their business, while many still do not have significant digital presence. These businesses are ready to expand consumer reach beyond their limited store front presences with these technology enabled marketplace models. Additionally, these underserved MSMEs have a need for financial services such as lending.

-

High GDP growth: SE Asia is among the fastest growing economies in the world and expected to become the world’s sixth largest economy by GDP in 2030. Nominal GDP is forecasted to grow 7% CAGR (compound annual growth rate) over the next 5 years.

-

Rapid income growth: Total disposable income is expected to grow 8% over the next five years, which should increase the affordability and penetration of these digital services.

Digitization of services is in the early innings

Grab estimates that it is mid-single digit/low-double digit % penetrated across delivery, mobility, and financial services. These are very underpenetrated when compared to US and China resulting in an open ended growth runway. Below are a few high level comparisons of penetration per Euromonitor (note: data is not great but methodology should be consistent across geographies leading to relative and directional takeaways):

SE Asia should be able to narrow the gap with US and China over time. I believe at steady state maturity, SE Asia penetration should theoretically be as high (if not higher) than developed market peers. In addition to the region’s characteristics discussed above, I would like to note/emphasize the following reasons:

-

Delivery: Grab’s markets shares similarities with highly penetrated markets such as China – higher density, bad traffic in cities (premium on time), highly fragmented restaurant/grocery base with informal mom/pops (less chains), cheap labor arbitrage, and digitization (and consumer conversion) of breadth/depth of restaurants. Consumer adoption should continue increasing as company optimizes for consumer facing fees (price), convenience (ETAs), and restaurant selection. These are all a function of scale and local network density that accrue to the market leader. As a data point on penetration potential, Grab’s 25MM monthly transacting users represent <5% of Grab’s market population vs. Just Eat Takeaway’s ~40% penetration (monthly active users as % of population) in its most mature market (Netherlands).

Charts below are from Evercore report on 12/15/21:

Chart below is from UBS report on 12/9/21:

-

Mobility: SE Asia penetration should be higher than in the US and closer to China given underdeveloped mass transportation systems and expensive car prices, result in low car ownership. The traditional taxi industry has lagged technological advancement as it relates to routing and mapping, handling of digital payments and standards in place to create a safe operating environment. The charts below are from Evercore report on 12/15/21:

Chart below is from UBS report on 12/9/21:

-

Digital financial services: In my opinion, fintech/payments is Grab’s single largest opportunity that is not being recognized or credited by the market today (pure optionality). GrabPay is significantly more than just payments and extends to data analytics/lead generation (e.g. GrabFinance, GrabInsure, and GrabInvest) and BNPL. The potential for outsized economics is real considering the large TAM, which is universally seen across other markets globally. Because competitive evolution is highly uncertain and the path to monetization is long and unclear, the market has understandably ignored its value especially as we believe it will likely lose money over the medium term as it inevitably runs into execution mishaps. The digitization of financial services is nascent but leapfrog effect is the most impactful in this segment given further smartphone and internet adoption rates within the region; increased availability to transact digitally via merchant adoption; and increased rewards and convenience vs. cash payment options. Further, governments are promoting the transition from cash to digital payments. Unlike the US, SE Asia e-wallet adoption is relatively unconstrained for the reasons highlighted above – predominantly cash economy; unbanked/underserved banking population; less consumer friction given low credit card and commercial banking products usage – with characteristics that are very similar to China and India. Chart below is from Evercore report on 12/15/21:

Fintech serves not only consumers but also merchants and drivers. Grab has a strong sense of the business or driver’s financial performance in a digital payments ecosystem vs. traditional cash sales. As digital wallets and payments expand, Grab has better access to data for its in-house credit scoring model, allowing the company to support better lending services, which should lead to higher adoption than traditional banking services that are not integrated with the core functions of the merchant. For example (all data per Grab Holdings F-4): in Malaysia, >1/3 of GrabFood partners were Financial Services customers in 4Q20; for drivers, Grab is able to provide extra protections such as insurance products for critical illness protection via a micro-premium paid on a per trip basis (facilitated 130MM micro-insurance transactions between April 2019 – March 2021); also, cash paid trips accounted for nearly 43% of Grab’s transactions in 2020. Therefore, Grab will aid drivers through setting up a bank account and/or aid purchase of a smartphone, which further deepens the company’s relationship with its driver ecosystem.

Grab is best positioned to win across its core businesses with its super-app

While the broader question of which super app will be crowned king (i.e. Grab’s mobility/delivery vs. Sea’s ecommerce/gaming are both high frequency and engagement), I believe Grab will sustain its market leader position across its core categories of online food delivery and ride-hailing. In contrast, I believe its position in digital payments is more debatable in spite of Grab’s early lead, though I’ll add there is sufficient TAM for multiple winners especially with the disruption of traditional/legacy players. Grab has successfully achieved the ultimate success that has evaded its global delivery and mobility peers: #1 businesses in both mobility AND delivery where cross-platform advantages should result in higher lifetime value, lower customer acquisition cost, and superior retention. The early cohort and customer usage data shows that its super app strategy is resonating with customers and should result in its dream coming to fruition (per Grab’s 4Q21 earnings presentation):

![]()

![]()

![]()

Grab should earn structurally higher steady-state margins at maturity than developed market peers

I believe Grab has the highest margin potential of all global mobility and food delivery businesses. For whatever it’s worth, management targets long term margins (% of GMV) of 12% in mobility and 3% in deliveries. Mobility margin compares favorably to Uber’s 10%+ margin but delivery is lower than its global comps (5-8% Delivery Hero and >5% Uber and Just Eat Takeaway). For now, the Company does not guide on financial services given its evolving business model but long term margin potential should settle out between mobility and food delivery. Grab aims for segment Adj. EBITDA breakeven in deliveries by end of 2023, though this could change depending on competitive dynamics/rationality and reinvestment opportunities.

In my opinion, the main driver of its superior steady-state profitability profile comes down to the success of its super app strategy relative to the pure-play nature of its competitors (or strong in one; mediocre in the other). Perhaps more importantly, in my opinion, Grab is the only food/rideshare player worldwide that has meaningfully built a digital payments/fintech services platform. The combination of the three should result in higher LTV from wallet share/cross-sell opportunities, high incremental margins, low/minimal CAC, stronger retention and user stickiness, etc. The super app benefits extend beyond consumers to merchants and drivers. For example, 2/3 of two-wheel drivers in Indonesia/Vietnam/Thailand drive on both food and mobility (different peak demand periods), which increases driver utilization rate à lowers cost per trip unit economics à potential reduction in incentives with the benefits accruing to Grab given it maximizes driver earnings from more trips. Further, financial services (wealth management, insurance, lending, etc) present incremental monetization potential with little CAC (i.e. customers are already acquired and engaged) and Grab should be the best positioned to score credit risk and serve this difficult to reach underbanked segment. These opportunities for incremental economics do not exist for its global players, which contributes to Grab’s superior unit economics.

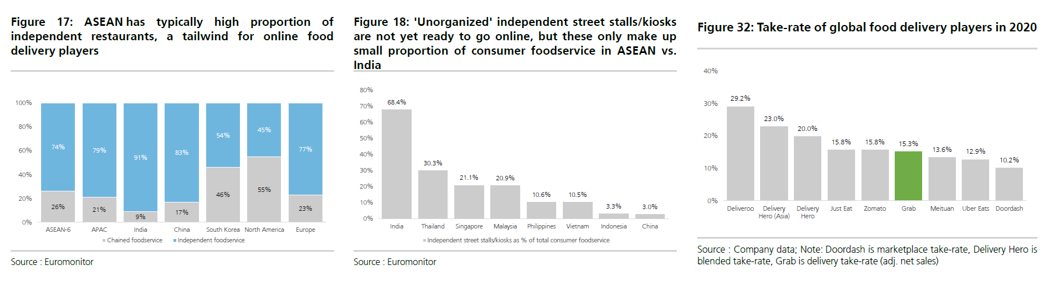

My hypothesis is that Grab’s markets lend themselves to greater economic capture for the platform – higher relative scale advantages over #2 as competition rationalizes/Grab gains share (especially when considering super app); greater order/network/population density à reduce incentives for riders and consumers without compromising value to each participant or user experience; greater % of MSMEs where Grab should have greater bargaining power; less developed infrastructure and services so Grab’s importance and wallet share to its partners could be higher; and time arbitrage with lower labor costs. For example, Mobility earns much higher margins than Uber/Lyft given super app cost advantages and lower insurance costs vs. US players. In delivery, 90%+ of the restaurants are independent/non-chain in its largest markets – Indonesia and Vietnam (Philippines is notable exception at only 32% independent/non-chain) per UBS report on 12/9/21. As a result, its take-rates and margins should be structurally higher than developed market peers at equilibrium. I suspect that it is currently keeping its take-rate in-line with peers given the early land grab phase of industry development (e.g. signing up supply to improve selection). Charts below are from UBS report on 12/9/21:

The range of outcomes is wide but downside is truncated given current valuation

SE Asia market is in its early stages of development. As a result, there is/will be a lot of capital chasing the market opportunity given the large greenfield TAM that is available. As seen in developed markets, the interim financials will be messy given the need to defend market share against competitors or to reinvest upfront and expand into new businesses. I’m more focused on the long term given most of the value is in the terminal value, which is a function of [1] Grab’s ability to win and [2] steady-state economics when the business is at scale and the market is mature/rational.

I believe Grab is interesting at its current share price because of the upside convexity with little downside. Grab has ~$6Bn of net cash on the balance sheet which is >60% of its market cap. However, I conservatively estimate that $4-5Bn will be burned over the next 3-5 years as it approaches free cash flow breakeven. I do not believe the Company needs to raise equity to achieve its growth plan, though this could change with more aggressive discretionary investments in fintech/payments. Given the Company is years away from generating profits, I prefer to assess Grab on IRRs assuming normalized economics across Low/Base/High scenarios over a 5-10 year period rather than using traditional multiples. I recognize that there is high uncertainty in my forecasts (only certainty is they’ll be wrong) but the scenarios are intended to simulate Grab’s wide range of outcomes. My scenarios are as follows:

1. Base Case (mid/high-teens IRR): Gross merchandise value (GMV) grows high-teens CAGR while Adj. EBITDA margin (% of GMV) hits management’s targets (12.5% in mobility, 3% in delivery, and 3% in financial services) in 2030, which I believe are highly achievable at steady-state.

2. Low Case (LSD % IRR): GMV grows low-teens CAGR while Adj. EBITDA margin (% of GMV) falls below management’s targets and global peers (10% in mobility, 2% in delivery, and 2% in financial services) in 2030, which I believe is conservative and suggest structurally deficient markets which my research has not uncovered to date.

3. High Case (30%+ IRR): GMV grows mid-20% CAGR while Adj. EBITDA margin (% of GMV) exceeds management’s targets (14% in mobility, 5% in delivery, and 4% in financial services) in 2030, which would be on par with global peers targets (note: mobility would be best-in-class).

The biggest uncertainty in my view would be financial services GMV and EBITDA development given the business is in its infancy. However, management’s directional comments (supported by comps) suggest that segment margins could potentially reach 5-10% of GMV depending on business mix.

Important Disclaimers

The provision of this report does not constitute (and should not be construed as) a recommendation, financial promotion, investment advice, encouragement or solicitation to buy, sell, or hold the security of the subject issuer (the “Security”), or any other securities, discussed herein. This report is for informational purposes only. All of the information contained herein is based on publicly available information with respect to the security and the author’s analysis of such information. Past performance is no guarantee, nor is it indicative, of future results.

Certain statements reflect the opinions of the author as of the date written, may be forward-looking and/or based on current expectations, projections, and/or information currently available. The author cannot assure future results and disclaims any obligation to update or alter any statistical data and/or references thereto, as well as any forward-looking statements, whether as a result of new information, future events, or otherwise. Such statements/information may not be accurate over the long-term. The views are those of the author acting in his individual capacity and not as a representative of the firm. The author’s opinions on this Security may change at any time in the future and the author will not, and disclaims any obligation to, update this report to reflect any change in opinion. The author further disclaims any obligation to respond to any comments or questions posted regarding the Security discussed herein.

NO INVESTMENT DECISIONS SHOULD BE BASED IN ANY MANNER ON THE INFORMATION AND OPINIONS SET FORTH IN THIS REPORT. YOU SHOULD VERIFY ALL CLAIMS, DO YOUR OWN DUE DILIGENCE AND/OR SEEK ADVICE FROM YOUR OWN PROFESSIONAL ADVISOR(S) AND CONSIDER THE INVESTMENT OBJECTIVES AND RISKS AND YOUR OWN NEEDS AND GOALS BEFORE INVESTING IN ANY SECURITIES MENTIONED. AN INVESTMENT IN THE SECURITY DOES NOT GUARANTEE A POSITIVE RETURN AS STOCKS ARE SUBJECT TO MARKET RISKS, INCLUDING THE POTENTIAL LOSS OF PRINCIPAL.

The author or his or her respective employer or employer’s clients, affiliates, officers, managers and directors, may or may not hold positions in the Security noted in this article. These parties may trade at any time, without notification to this community, and will not disclose this information to this community. The author and his employer disclaim any liability for investment losses that you may incur under any circumstances.

The author does not hold a position with the issuer of the Security such as employment, directorship, or consultancy.

I do not hold a position with the issuer such as employment, directorship, or consultancy.

I and/or others I advise do not hold a material investment in the issuer's securities.

Catalyst

Rationalization in competitive intensity

Margin inflection

Fintech/payments development

| show sort by |