| 2023 | 2024 | ||||||

| Price: | 383.45 | EPS | 33 | 0 | |||

| Shares Out. (in M): | 300 | P/E | 11 | 0 | |||

| Market Cap (in $M): | 115 | P/FCF | 10 | 0 | |||

| Net Debt (in $M): | -1 | EBIT | 17 | 0 | |||

| TEV (in $M): | 113 | TEV/EBIT | 5.9 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- Regulated monopoly

- compounder club

- Mexico

Description

COMPANY OVERVIEW

Grupo Aeroportuario del Sureste (BMV: ASUR B) is a Mexican holding company which operates and maintains long term airport concessions in Latin America. Sixteen airport concessions in total nine of which are in the southeast region of Mexico. The most important asset being Cancun International Airport. Outside of Mexico ASUR also operates six concessions in Colombia, and the San Juan, Puerto Rico airport.

WHY ASUR?

We already liked Asur as an investment since, in our opinion, the risks regarding the opening of the new Tulum airport (supposedly December 2023, although we remain highly skeptical) and the negotiation of the 2024-2029 MDP (Master Development Plan) later this year had both created sufficient uncertainty that Asur already traded at a significant discount to what both their other Mexican peers traded at.

With this said, the Mexican government dropped the mother of all balls last week (late Wednesday October the 2nd) which gave us what in our opinion is perhaps a once in a decade opportunity to buy this quality legal monopoly at a very discounted, even distressed valuation.

What happened is the government apparently (we highlight apparently since to date no official information has been released either by government officials or the airport groups) unilaterally and “unlawfully” made changes to the airport groups concessions agreements specifically pertaining what these groups were allowed to charge (TUA or Airport Use Fee) to passengers going forward.

Maximum uncertainty since the three airport group’s press releases were essentially identical and with zero substance as to what changes were implemented on a going forward basis.

To all of us familiar with how the Mexican government operates- we believe the government is using force to negotiate tariff concessions but at the end the effect (if past negotiations are a guide) the effect for the concessionaires will be net/net not much different from how they stood before.

Let me be clear- I personally believe there’s a 90% chance the latter statement is what turns out to happen (again based on history and given 2024 is an electoral year in Mexico) but we are assuming a 50% haircut to TUA in all cases. Something that would be akin to the government illegally revoking concessions. I think chances are very low such a haircut would be implemented (perhaps 5%). We used that draconian scenario to underwrite this valuation and investment.

To continue with the story, last Thursday the Mexican airport groups had monumental selloffs in the Mexican Stock exchange that in our opinion make them all buys at current prices. It is just that our favorite investment within the group happens to be Asur.

How large was the selloff? Grupo Aeroportuario del Centro Norte (OMA) closed the day down 26% at P$148 per share (hitting an intraday low of P$112), Grupo Aeroportuario del Pacífico (GAP) ended 23% down at P$228 (intraday low of P$197) while ASUR closed 17% down at P$362 per share (with an intraday low of P$306). In other words, Panic prevailed.

What is the current valuation for the three airport groups in Mexico? See below-

Table 1. ASUR vs Peers

Table 2. Mexican Airports by PAX (thousand PAX)

They’re all cheap and Imo buys today. Having said that Asur is our favorite. Why? -

1. Cancun

2. Cancun

3. Cancun

Seriously, Cancun has been an amazing growth story for years now and see no reason for that to suddenly change. Passenger traffic has grown by 7.5% CAGR since 1990. International traffic being 64% last year.

Cancun traffic has increased by roughly 6m passengers from pre-pandemic levels. To put things in context, that is almost the total traffic that Los Cabos currently has.

Image 1. Illustrative flight times from various destinations

But is Cancun a resilient asset? We strongly believe so..

HOW DO WE FEEL COMFORTABLE WITH THE CURRENT REGULATORY UNCERTAINTY?

Let’s do the math-

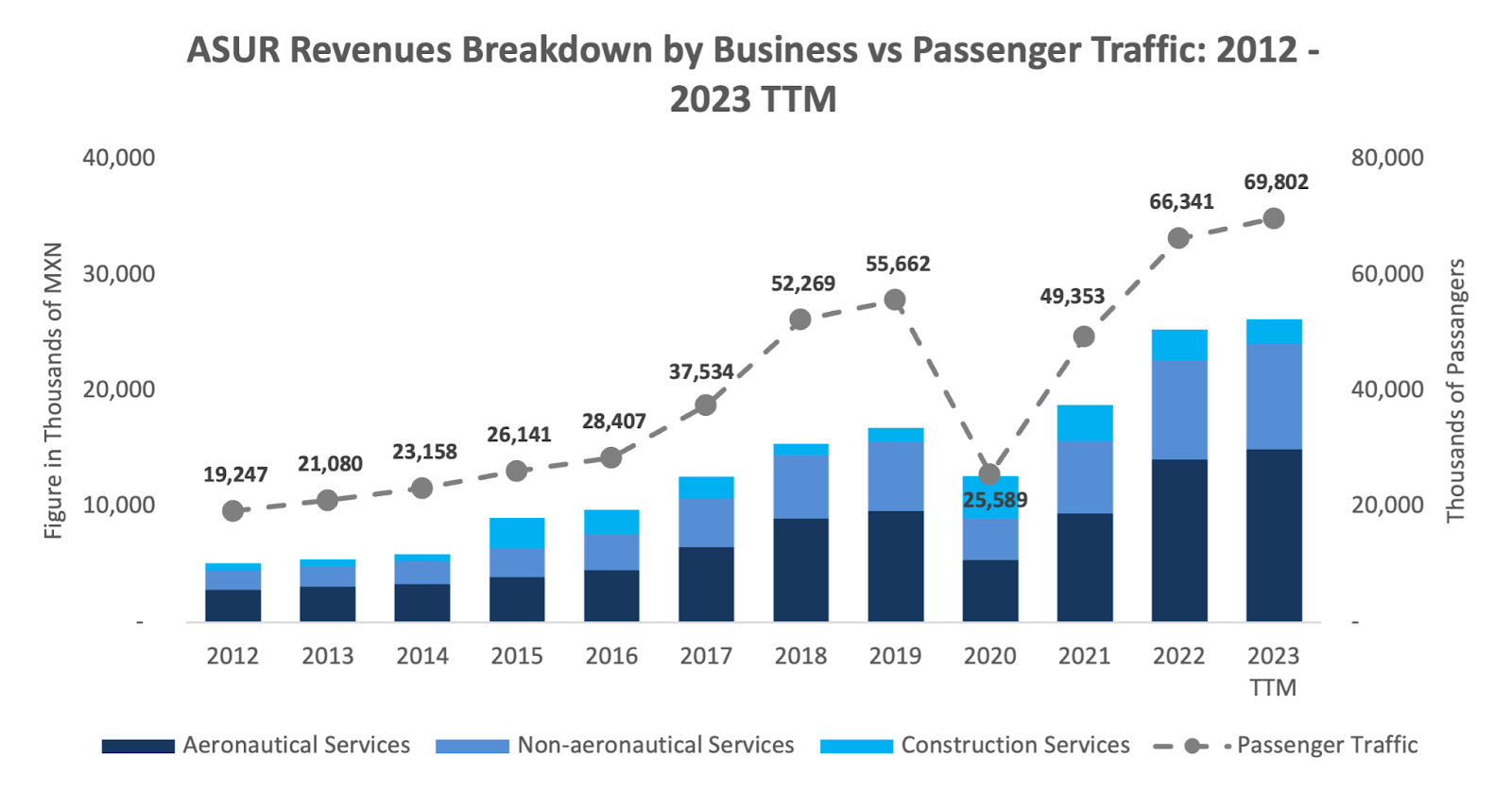

ASUR’s Aeronautical services make up about 57% of ASUR's total revenues. These revenues primarily come from passenger charges which are basically fees collected from departing passengers by airlines and then paid to ASUR. In 2021 and 2022, passenger charges represented 36.7% and 42.8% of consolidated revenues, respectively. This segment depends on passenger volumes and is core to ASUR's aviation-related income.

Non-aeronautical services have grown in importance, accounting for around 25.4%, 30.6%, and 33.8% of ASUR's total revenues in 2020, 2021, and 2022, respectively. They include income from leasing airport space to retailers, restaurants, airlines, and others, as well as access fees charged to providers of services like catering, handling, and ground transport.

In our valuation analysis of ASUR, we adopt a conservative approach by considering various haircuts to the TUA of up to 50%.

You can use your own assumptions but the fact is that using a 50% haircut, ASUR would then trade at a 8.5x EV/EBITDA and 7.5% FCF yield which we think is way too cheap for such a quality asset and a meaningful discount to its own history.

Catalysts

The obvious catalyst will be a favorable resolution regarding the concession amendments.

Having said that, the controlling groups, both Grupo ADO and Fernando Chico Pardo have been very savvy buyers of their own stock when it has been undervalued. We believe that could again happen should the shares at these prices for some time.

Risks

The new Tulum airport is a slight negative in our opinion but nothing more than that. Real risk would be the government going crazy and greatly affecting current concessions as they now stand.

COMPANY OVERVIEW

Grupo Aeroportuario del Sureste (BMV: ASUR B) is a Mexican holding company which operates and maintains long term airport concessions in Latin America. Sixteen airport concessions in total nine of which are in the southeast region of Mexico. The most important asset being Cancun International Airport. Outside of Mexico ASUR also operates six concessions in Colombia, and the San Juan, Puerto Rico airport.

WHY ASUR?

We already liked Asur as an investment since, in our opinion, the risks regarding the opening of the new Tulum airport (supposedly December 2023, although we remain highly skeptical) and the negotiation of the 2024-2029 MDP (Master Development Plan) later this year had both created sufficient uncertainty that Asur already traded at a significant discount to what both their other Mexican peers traded at.

With this said, the Mexican government dropped the mother of all balls last week (late Wednesday October the 2nd) which gave us what in our opinion is perhaps a once in a decade opportunity to buy this quality legal monopoly at a very discounted, even distressed valuation.

What happened is the government apparently (we highlight apparently since to date no official information has been released either by government officials or the airport groups) unilaterally and “unlawfully” made changes to the airport groups concessions agreements specifically pertaining what these groups were allowed to charge (TUA or Airport Use Fee) to passengers going forward.

Maximum uncertainty since the three airport group’s press releases were essentially identical and with zero substance as to what changes were implemented on a going forward basis.

To all of us familiar with how the Mexican government operates- we believe the government is using force to negotiate tariff concessions but at the end the effect (if past negotiations are a guide) the effect for the concessionaires will be net/net not much different from how they stood before.

Let me be clear- I personally believe there’s a 90% chance the latter statement is what turns out to happen (again based on history and given 2024 is an electoral year in Mexico) but we are assuming a 50% haircut to TUA in all cases. Something that would be akin to the government illegally revoking concessions. I think chances are very low such a haircut would be implemented (perhaps 5%). We used that draconian scenario to underwrite this valuation and investment.

To continue with the story, last Thursday the Mexican airport groups had monumental selloffs in the Mexican Stock exchange that in our opinion make them all buys at current prices. It is just that our favorite investment within the group happens to be Asur.

How large was the selloff? Grupo Aeroportuario del Centro Norte (OMA) closed the day down 26% at P$148 per share (hitting an intraday low of P$112), Grupo Aeroportuario del Pacífico (GAP) ended 23% down at P$228 (intraday low of P$197) while ASUR closed 17% down at P$362 per share (with an intraday low of P$306). In other words, Panic prevailed.

What is the current valuation for the three airport groups in Mexico? See below-

Table 1. ASUR vs Peers

Table 2. Mexican Airports by PAX (thousand PAX)

They’re all cheap and Imo buys today. Having said that Asur is our favorite. Why? -

1. Cancun

2. Cancun

3. Cancun

Seriously, Cancun has been an amazing growth story for years now and see no reason for that to suddenly change. Passenger traffic has grown by 7.5% CAGR since 1990. International traffic being 64% last year.

Cancun traffic has increased by roughly 6m passengers from pre-pandemic levels. To put things in context, that is almost the total traffic that Los Cabos currently has.

Image 1. Illustrative flight times from various destinations

But is Cancun a resilient asset? We strongly believe so..

HOW DO WE FEEL COMFORTABLE WITH THE CURRENT REGULATORY UNCERTAINTY?

Let’s do the math-

ASUR’s Aeronautical services make up about 57% of ASUR's total revenues. These revenues primarily come from passenger charges which are basically fees collected from departing passengers by airlines and then paid to ASUR. In 2021 and 2022, passenger charges represented 36.7% and 42.8% of consolidated revenues, respectively. This segment depends on passenger volumes and is core to ASUR's aviation-related income.

Non-aeronautical services have grown in importance, accounting for around 25.4%, 30.6%, and 33.8% of ASUR's total revenues in 2020, 2021, and 2022, respectively. They include income from leasing airport space to retailers, restaurants, airlines, and others, as well as access fees charged to providers of services like catering, handling, and ground transport.

In our valuation analysis of ASUR, we adopt a conservative approach by considering various haircuts to the TUA of up to 50%.

You can use your own assumptions but the fact is that using a 50% haircut, ASUR would then trade at a 8.5x EV/EBITDA and 7.5% FCF yield which we think is way too cheap for such a quality asset and a meaningful discount to its own history.

Catalysts

The obvious catalyst will be a favorable resolution regarding the concession amendments.

Having said that, the controlling groups, both Grupo ADO and Fernando Chico Pardo have been very savvy buyers of their own stock when it has been undervalued. We believe that could again happen should the shares at these prices for some time.

Risks

The new Tulum airport is a slight negative in our opinion but nothing more than that. Real risk would be the government going crazy and greatly affecting current concessions as they now stand.

COMPANY OVERVIEW

Grupo Aeroportuario del Sureste (BMV: ASUR B) is a Mexican

holding company which operates and maintains long term airport

concessions in Latin America. Sixteen airport concessions in

total nine of which are in the southeast region of Mexico. The

most important asset being Cancun International Airport. Outside

of Mexico ASUR also operates six concessions in Colombia, and

the San Juan, Puerto Rico airport.

WHY ASUR?

We already liked Asur as an investment since, in our opinion,

the risks regarding the opening of the new Tulum airport

(supposedly December 2023, although we remain highly skeptical)

and the negotiation of the 2024-2029 MDP (Master Development

Plan) later this year had both created sufficient uncertainty

that Asur already traded at a significant discount to what both

their other Mexican peers traded at.

With this said, the Mexican government dropped the mother of all balls last week (late Wednesday October the 2nd) which gave us what in our opinion is perhaps a once in a decade opportunity to buy this quality legal monopoly at a very discounted, even distressed valuation.

What happened is the government apparently (we highlight

apparently since to date no official information has been

released either by government officials or the airport groups)

unilaterally and “unlawfully” made changes to the airport groups

concessions agreements specifically pertaining what these groups

were allowed to charge (TUA or Airport Use Fee) to passengers

going forward.

Maximum uncertainty since the three airport group’s press

releases were essentially identical and with zero substance as

to what changes were implemented on a going forward basis.

To all of us familiar with how the Mexican government operates-

we believe the government is using force to negotiate tariff

concessions but at the end the effect (if past negotiations are

a guide) the effect for the concessionaires will be net/net not

much different from how they stood before.

Let me be clear- I personally believe there’s a 90% chance the

latter statement is what turns out to happen (again based on

history and given 2024 is an electoral year in Mexico) but we

are assuming a 50% haircut to TUA in all cases. Something that

would be akin to the government illegally revoking concessions.

I think chances are very low such a haircut would be implemented

(perhaps 5%). We used that draconian scenario to underwrite this

valuation and investment.

To continue with the story, last Thursday the Mexican airport

groups had monumental selloffs in the Mexican Stock exchange

that in our opinion make them all buys at current prices. It is

just that our favorite investment within the group happens to be

Asur.

How large was the selloff? Grupo Aeroportuario del Centro Norte (OMA) closed the day down 26% at P$148 per share (hitting an intraday low of P$112), Grupo Aeroportuario del Pacífico (GAP) ended 23% down at P$228 (intraday low of P$197) while ASUR closed 17% down at P$362 per share (with an intraday low of P$306). In other words, Panic prevailed.

What is the current valuation for the three airport groups in

Mexico? See below-

Table 1. ASUR vs Peers

Table 2. Mexican Airports by PAX (thousand PAX)

They’re all cheap and Imo buys today. Having said that Asur is

our favorite. Why? -

-

Cancun

-

Cancun

-

Cancun

Seriously, Cancun has been an amazing growth story for years now

and see no reason for that to suddenly change. Passenger traffic

has grown by 7.5% CAGR since 1990. International traffic being

64% last year.

Cancun traffic has increased by roughly 6m passengers from

pre-pandemic levels. To put things in context, that is almost

the total traffic that Los Cabos currently has.

Image 1. Illustrative flight times from various destinations

But is Cancun a resilient asset? We strongly believe so..

HOW DO WE FEEL COMFORTABLE WITH THE CURRENT REGULATORY

UNCERTAINTY?

Let’s do the math-

ASUR’s Aeronautical services make up about 57% of ASUR's total

revenues. These revenues primarily come from passenger charges

which are basically fees collected from departing passengers by

airlines and then paid to ASUR. In 2021 and 2022, passenger

charges represented 36.7% and 42.8% of consolidated revenues,

respectively. This segment depends on passenger volumes and is

core to ASUR's aviation-related income.

Non-aeronautical services have grown in importance, accounting

for around 25.4%, 30.6%, and 33.8% of ASUR's total revenues in

2020, 2021, and 2022, respectively. They include income from

leasing airport space to retailers, restaurants, airlines, and

others, as well as access fees charged to providers of services

like catering, handling, and ground transport.

In our valuation analysis of ASUR, we adopt a conservative

approach by considering various haircuts to the TUA of up to

50%.

You can use your own assumptions but the fact is that using a

50% haircut, ASUR would then trade at a 8.5x EV/EBITDA and 7.5%

FCF yield which we think is way too cheap for such a quality

asset and a meaningful discount to its own history.

Catalysts

The obvious catalyst will be a favorable resolution regarding

the concession amendments.

Having said that, the controlling groups, both Grupo ADO and

Fernando Chico Pardo have been very savvy buyers of their own

stock when it has been undervalued. We believe that could again

happen should the shares at these prices for some time.

Risks

The new Tulum airport is a slight negative in our opinion but

nothing more than that. Real risk would be the government going

crazy and greatly affecting current concessions as they now

stand.

Catalyst

New tariff clarity, valuation itself

| show sort by |