| 2021 | 2022 | ||||||

| Price: | 40.00 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 120 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 5,000 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 2,900 | EBIT | 0 | 0 | |||

| TEV (in $M): | 7,900 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- Hedge Fund Hotel

Description

Note that I put in the PF cap structure for the Diamond merger above, not the current cap structure, so numbers won't match Bloomberg or anything.

One theme I’ve been beating pretty consistently since late last year is that I don’t understand the valuation of “pandemic recovery” plays. These are things like cruise ships, airlines, restaurants, and a variety of other things that have been shut down by the pandemic. Almost all of these are trading at valuations significantly in excess of their pre-Covid valuation despite currently burning significant amounts of cash as they wait for the reopening. I can understand some of the logic: the market thinks there will be a period of super-normal profits as the country reopens (the “roaring 20s”) and the recovery plays see a swell of demand alongside a barren competitive landscape given smaller competitors have gone bankrupt.

Consider, for example, Dave & Buster’s (PLAY). Their current stock price is ~20% above where it was prepandemic, and their EV is ~50% higher given all the shares they issued during the crisis. The company will be ~breakeven in the near to medium term while we wait for reopening, and even once they reopen this is a business that the market was looking at pre-pandemic and saying "bleh." If you look past a potential boom in the near to medium term from reopening, I’m not sure why the market would be super excited about the business in the long term.

But there is one set of companies that I think will be uniquely positioned to benefit in the long term from the roaring 20s. And among those companies, there’s one in particular that I think is particularly mispriced.

The companies? Timeshares. And the specific mispricing? Hilton Grand Vacations (HGV). I think HGV’s recent merger is an absolute home run, and on reasonable assumptions I could see HGV as a >$80/share stock in the next ~3 years.

I’m going to break the rest of the article into two separate parts: to start, I’m just going to do some brief hits on the timeshare industry overall, including an overview of why I think timeshares in particular are interesting into a roaring 20s style boom, and then a deeper dive into why I think HGV in particular is interesting.

Timeshare background

In general, timeshares have bad reputations. At best, timeshares are associated with a super hard pitch that often leads to consumers plopping down thousands of dollars for a “lifetime” of vacation. At worst, you have flashbacks to the 90s, when the industry was more immature and rife with fraud.

The high price tag, hard sales tactics, and history of fraud makes timeshares a juicy target. Once every few years, newspapers will run an expose skewering the industry (NYT in 2008) or a specific company (NYT on Diamond in 2016), and South Park even devoted an episode to the timeshare hard sell.

While there are still some areas of roughness, in general I think the industry is much better today. The largest players in the industry (HGV, WYND, TNL) are now associated with the major hotel chains (like Hilton or Marriott; also worth noting Disney is also a big player); those hotel chains / Disney have a reputation to worry about so they’ve generally cleaned up the practices.

So, at this point, I think a lot of the stigma with timeshares dates back to legacy issues as well as the fact that the typical investor / wall street analyst tends to look down on timeshares because Wall Street analysts probably aren’t the perfect demo for timeshares, even though the timeshare demographics skew much higher than most would guess (at least among the branded players; in general the average member does >$100k in annual income with >700 FICO scores and ~$1m in new worth).

I think it’s important to keep that in mind for two reasons: First, when you bring up timeshares to someone who hasn’t looked at them recently, their first response is generally “aren’t those all frauds selling worthless vacations?” They’re not; timeshares are absolutely products that are designed to be sold but they are a real business and, in general, their customers like them. Second, Diamond in particular had a bad reputation several years ago; I’ll discuss this more in the merger section, but I think that area was a clear area of focus for HGV in their DD and that Apollo did a nice job of cleaning Diamond up (shocking, I know!).

Why timeshares benefit from the roaring 20s

Timeshares are absolutely perfectly positioned to benefit from the “roaring 20s.” Yes, they are perfectly positioned alongside all of the obvious reasons. You can break it out in a bunch of different ways, but the simple way to put it is timeshare is 100% leisure, and leisure should return much faster and be in much higher demand than business travel (and the early signs are the the demand is off the charts).

But timeshares should benefit significantly more than your typical recovery play for a few reasons:

-

A lot of the competing products for vacations remain out of business. Consider two popular vacations: international travel and cruise lines. Demand to go on vacations is going to be off the charts in the near term, but cruising and international travel will be at much, much lower capacity than normal throughout the year. Cruise ships almost certainly won’t be allowed to sail at anything approaching full capacity until 2022 at the earliest, and a ton of foreign countries are still in lock down. So as we hit the back half of the year, a lot of the places people would normally turn to for vacations will be out of commission / full. I think timeshares will be well positioned to pick up some of that slack.

-

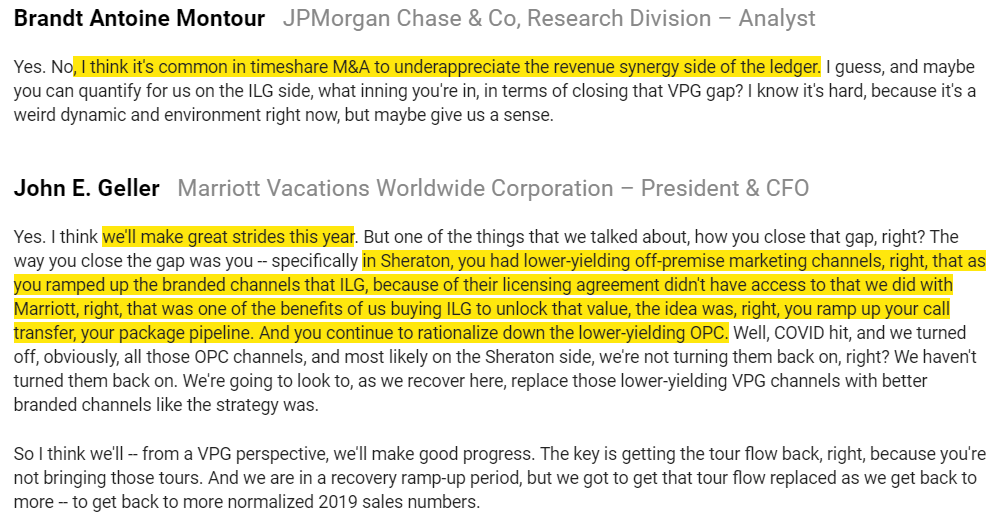

Timeshare’s best sales channel is “get people into our properties with discounted vacation packages, and then get them to fork over a lot of money with a hard sell.” Obviously, that benefits from increased occupancy driven by a boom in vacations / lack of alternative product. But I think the boom in vacation plays into timeshares hands in another way: people are going to be excited to go on a vacation for the first time since the pandemic, and they’re going to be in a fantastic mood. That’ll make them much easier sells once they get into the timeshare pitch (“Hey, you love vacations. Don’t you miss them? Why don’t you precommit now to a lifetime of vacations and save yourself some money in the long run?”), which should result in incrementally better closing rates on timeshare tours.

-

A super-normal profit cycle for a normal hotel or travel company is a one time event. But for a timeshare company, it’s a long term boon. Their whole goal is to get people into their properties in then sell them a vacation package that will turn them into a member for decades (meaning that they will gets decades of membership and maintaince fees from them, and who they can then hit with subsequent upgrades!).

To sum: timeshares should be a unique beneficiary of COVID because a lot of their key competitors are offline or operating with reduced capacity, a “roaring 20s” mindset should make for easier sales, and increased occupancy / easier sales creates customers who will generate fees and revenue streams for decades on end. In fact, we’re seeing early signs that the boom is just getting started. Here’s TNL at a conference in March:

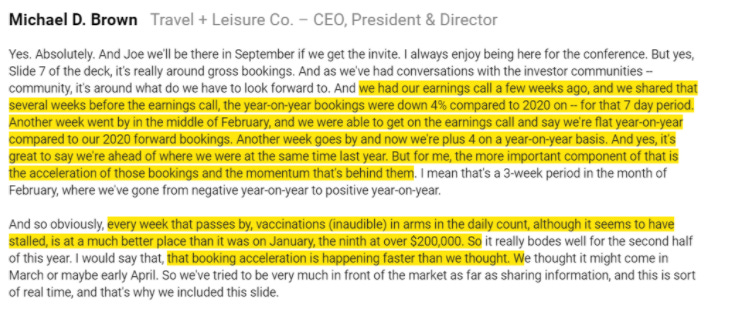

And here’s some quotes from HGV on how demand is trending.

Remember, all of these quotes are being made about demand in Q1’21. The country is barely even open yet; as we move into the back half of the year and the country fully opens up / people get fully vaccinated and start thinking about taking their first vacation in ~2 years, I think demand is going to remain off the charts.

Timeshares cost of capital should improve dramatically going forward

I’ll keep this section brief, as it could apply to a lot of different businesses / sectors, but I think everything associated with timeshares could (and should!) see a significant drop in their cost of capital going forward. 2020 was an environment far, far worse than most analysts had factored into even their most bearish cases for any timeshare or leisure company heading into the year, yet somehow every timeshare company posted positive adjusted EBITDA for the year. In addition, despite an economy that rivalled the Great Depression and their properties seeing huge capacity restrictions and/or shutdowns through most of the year, the timeshare companies managed to keep their membership base roughly flat year over year in 2020 and we never saw a mammoth increase in defaults on their consumer finance portfolio. Over time, I suspect that combo means that everything associated with timeshares should see an improved cost of capital / higher multiples because investors are simply more confident that they can handle economic distress in the future (if these guys were profitable during a pandemic when they literally couldn’t operate, are they really going to be bothered by a garden variety recession?).

HGV’s deal to buy Diamond is a home run (though not without risks!), and the combined company is too cheap

So far, everything discussed has just been talking about the timeshare industry in general. Let’s turn now to the heart of the idea: HGV’s acquisition of Diamond is an absolute home run, and the combined company is significantly too cheap.

At a very high level, the easiest way to think about the deal is this: HGV is a “branded timeshare”, meaning they are partnered with one of the big hotel chains (in this case, Hilton) and can sell into Hilton’s membership base. Being a branded timeshare company is a huge advantage; a hotel’s loyalty base is a perfect target market for timeshares, and being able to sell to them dramatically improves customer acquisition costs.

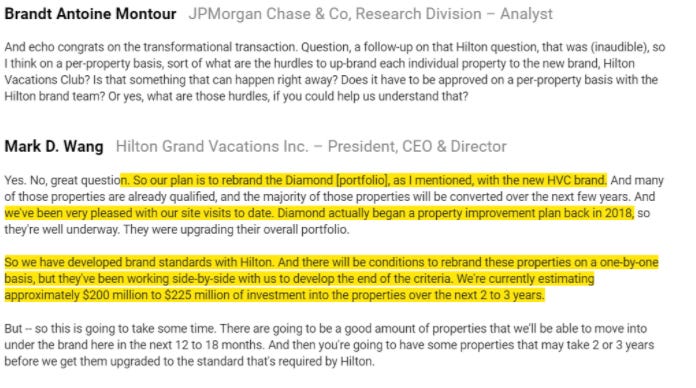

However, HGV’s properties were generally high end, meaning that HGV could only target and sell to the higher end of Hilton’s membership base. That left millions of Hilton loyalty customers who HGV couldn’t effectively target; with the acquisition of Diamond, HGV now has a product that they can go after the upscale market with (quote and slide below from HGV’s Diamond merger call / slides)

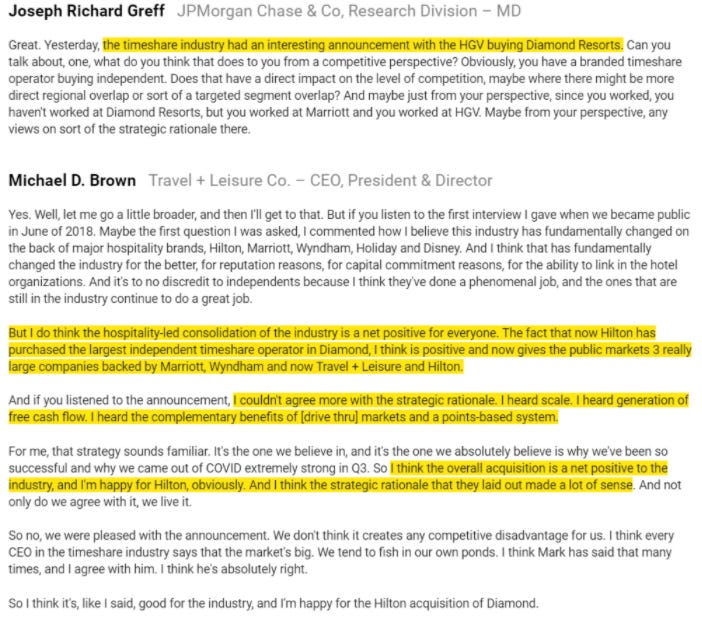

I’m not the only one who thinks the HGV / Diamond deal makes sense. Both TNL (Wyndham Timeshares) and VAC (Marriott and Hyatt timeshares) were at conferences a few days after the HGV / Diamond deal was announced, and both were pretty effusive about it. Obviously, feel free to take that with a grain of salt; it’d be pretty strange for a competing exec to come out and blast a peer for a merger that consolidates the industry, but directionally I think they are right on with all of their points / praise.

TNL on HGV / Diamond

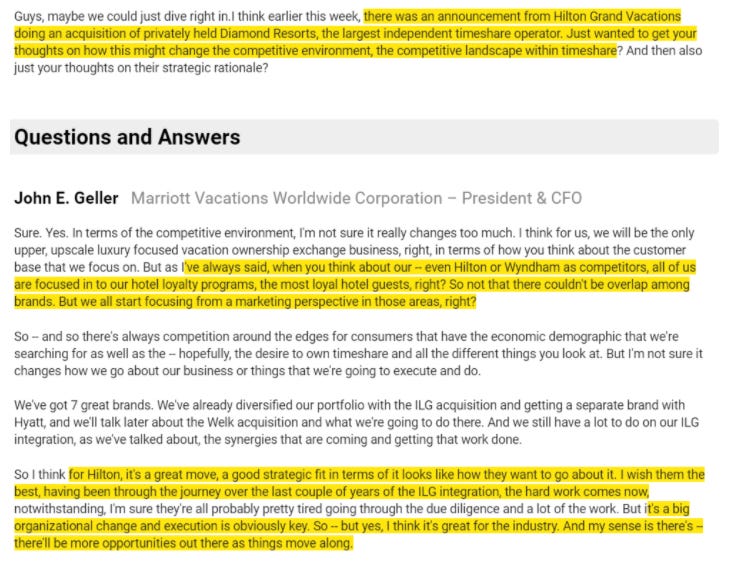

VAC on HGV / Diamond

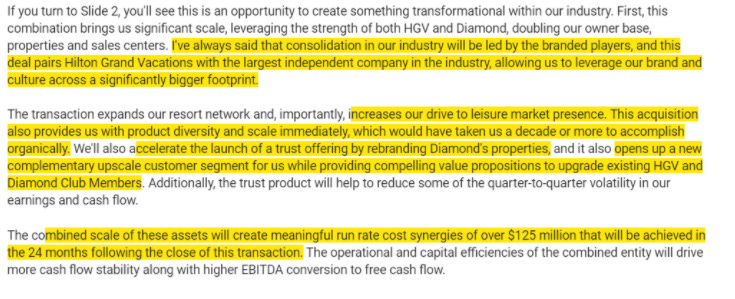

So, on its own, I think the Hilton / Diamond deal makes sense. But I think it makes even more sense when you consider the environment that they are closing the deal in. If you believe that we’re about to have a “roaring 20s” type boom, Diamond is an absolutely perfect acquisition for Hilton. Diamond has significant excess inventory, so they have product that they can sell into the coming boom, and Diamond’s slightly lower income target demographic is probably more likely to participate in a “roaring 20s” reopening boom than the higher end demographic legacy HGV targets (simply because the highest end consumers suffered much less in the COVID shut down).

But the great thing about HGV today is that you’re not paying anything for that “roaring 20s” upside. If you just value the company on their PF 2019 numbers + deal synergies, you’re paying a cheap to very cheap price for the combined companies. And I think there should be upside to those numbers; as I’ll discuss later, I think the synergy numbers for the companies are significantly sandbagged.

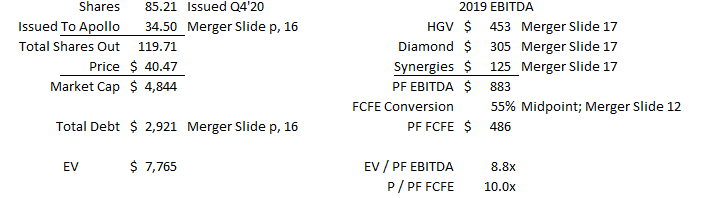

Let’s start with just the headline numbers. HGV is currently trading for $40.50. If we adjust for the shares they’ll issue to Apollo to acquire Diamond and their new debt load, their market cap is $4.8B and their EV is $7.8B. Post synergies, the combined company is projecting $883m in EBITDA w/ 50-60% of that dropping down to free cash flow for just shy of $500m in free cash flow to equity. That gives the combined an EV / EBITDA of ~8.8x and a P / FCF of ~10x.

Obviously, those are very cheap numbers if you believe the company can hit their targets, and they don’t include any type of “roaring 20s” bump. To me, the key question is if you can trust the synergy and FCF conversion numbers; if you can, this is screamingly cheap. If you think the FCF conversion numbers or synergy numbers are overstated, then this isn’t as cheap and it raises a host of management credibility questions.

Let’s start with the free cash flow conversion number, because it’s the simplest to discuss. Both VAC and TNL (the other two branded peers) have historically converted 50-60% of EBITDA into free cash flow, and both of them continue to target that level going forward. So I don’t there’s any controversy with assuming ~55% EBITDA conversion for HGV post merger; in fact, given the new scale of HGV and the operating leverage a roaring 20s boom would have for them, I don’t think it’s aggressive at all to think HGV could easily push the high end of that target.

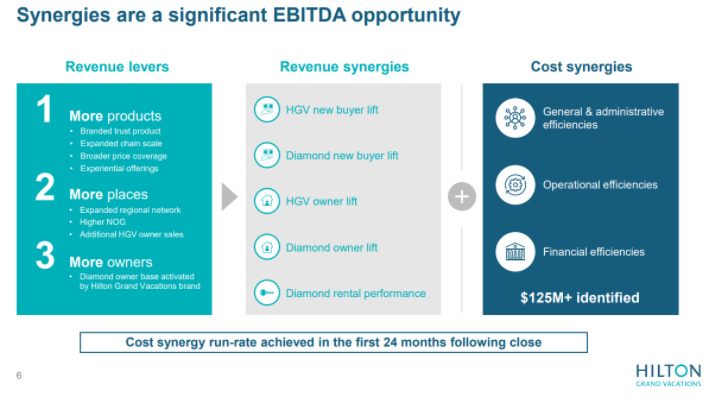

So let’s move on to the synergies side. HGV is targeting $125m in run rate cost savings for their EBITDA number. I think that number is not only achievable, but I think it’s likely to prove extremely conservative once the merger is fully integrated.

Let’s start out with why I think the $125m number is achievable, and then build off that to why I think it’s too low.

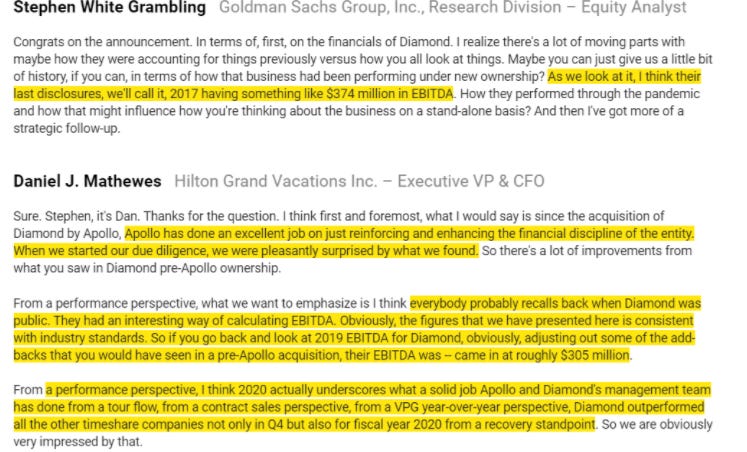

Diamond did $305m in EBITDA in 2019. HGV is projecting $125m in cost synergies, so they think they can realize ~40% of EBITDA as synergies. There has not been too much M&A in the timeshare space, but the precedent deals suggest those numbers are not out of line.

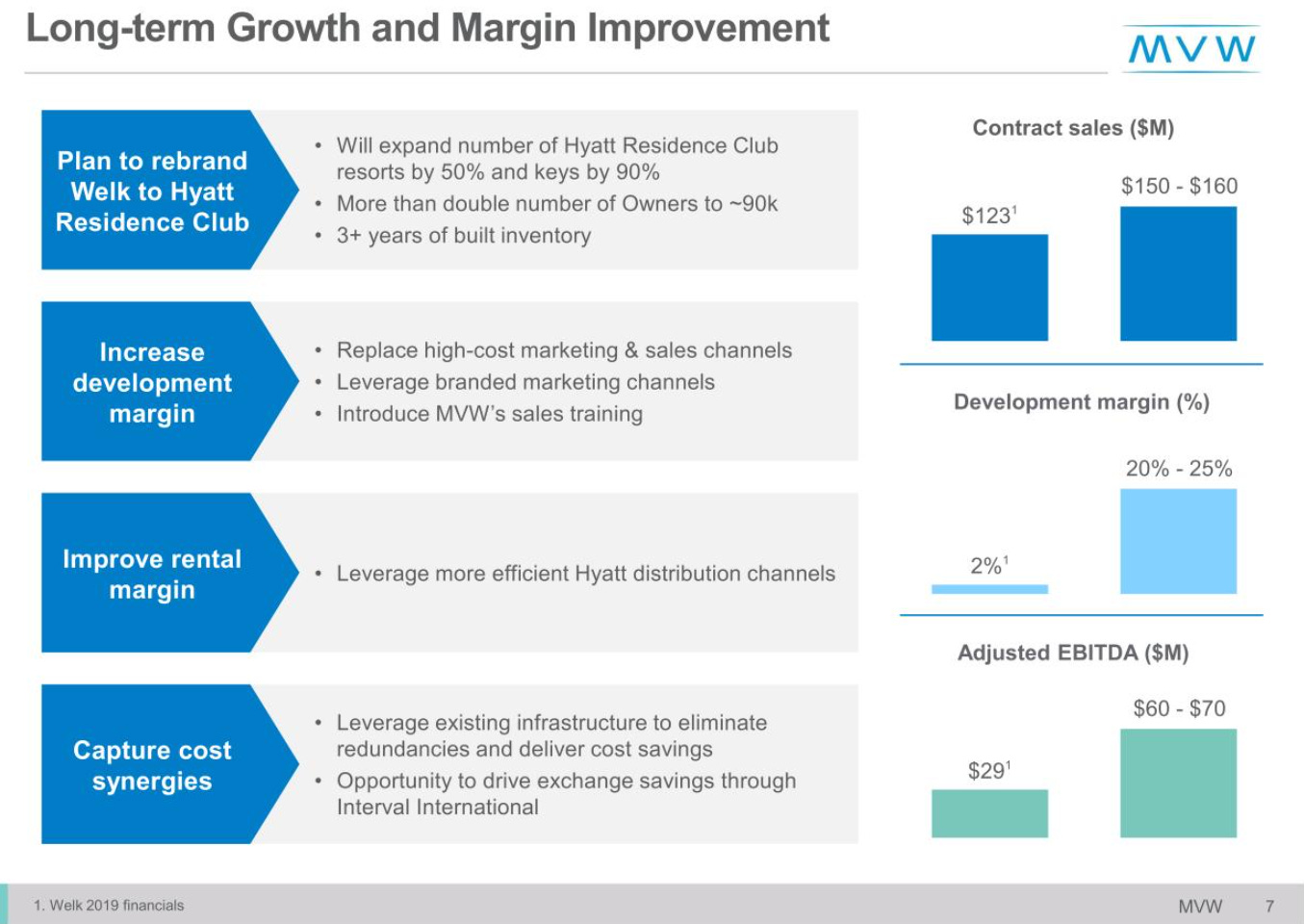

The most recent timeshare merger was VAC buying Welk in January. Welk did $29m in EBITDA in 2019, and VAC thought they could grow EBITDA to $60-70m in the medium term. I’ll discuss this deal more later, as it’s an incredible blueprint for the HGV / Diamond deal, but for our purposes what’s important here is simply the cost synergies. If you go read the merger call, VAC’s CFO guides to “roughly $12m” of the EBITDA increase coming from cost synergies. That’s 40% of Welk’s 2019 EBITDA number; right in line with HGV’s projection for Diamond.

The other recent merger in the timeshare space was VAC’s deal to buy ILG back in 2018. ILG did $361m in EBITDA in 2017 (the year before the merger); at the time the companies projected $75m in synergies (~20% of pre-deal EBITDA). By the end of 2020, they had increased that estimate to $200m (~56% of pre-deal EBITDA).

So that’s only N=2, but both examples suggest that the cost savings HGV is projecting are within reason or even conservative.

But I think the real reason to be excited about this deal is actually not in the cost synergies; it’s in the potential revenue synergies.

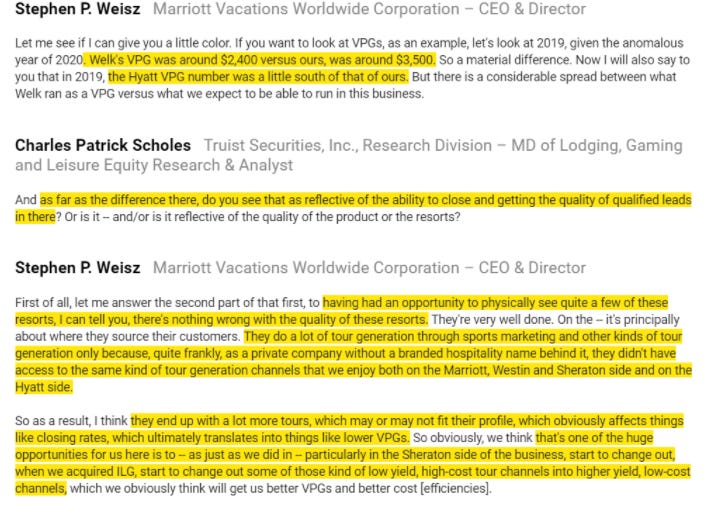

Again, Diamond is a non-branded timeshare. Acquiring customers for non-branded timeshares is very expensive (think mall kiosks, selling at a sporting event, etc.). Rebranding Diamond resorts to Hilton and selling them into the Hilton loyalty program should result in huge upside both in terms of lower cost to acquire customers and significantly better sales for the Diamond properties. Adding the Diamond properties into the HGV network should also yield some synergies as adding properties and locations into a timeshare network should increase the value of the system (i.e. if you have a timeshare company that only has Hawaiian properties, adding some Orlando properties or some skiing resorts and letting your current owners swap points into the new properties improves the value of your network), but those are looser and because Diamond and HGV’s properties target different sections of the market they might not be as strong.

Still, the revenue synergies are real and the potential is massive. Again, look at the VAC / Welk acquisition; VAC is projecting that they can more than double Welk’s EBITDA simply by plugging them into the Hyatt network. The quote below is from a recent conference VAC attended; I think it drives home just how large the opportunity from taking a nonbranded business and attaching it to a brand is.

Here’s one more quote from a VAC conference to emphasize how large the opportunity from brining a non-branded timeshare into a brand is.

Hopefully at this point I’ve hammered home that the opportunity for this merger is massive. Based on precedent deals (though admittedly a small sample size), HGV should be able to blow away their cost synergy number and realize significant revenue synergies as well. Given the combined company is trading at <9x EBITDA and <10x P/FCF off the lowball EBITDA numbers, that combination should drive eyepopping earnings and free cash flow growth (and, of course, send shares significantly higher).

Of course, there are risks here. I tend to think this merger will inevitably be a success in the long run, but in the short to medium term it could certainly create some noise in HGV’s number. And I am worried about this management team; HGV has never done an acquisition, so now their first acquisitions doubles as one of the largest deals in industry history during a pandemic that is reshaping society. If that doesn’t scream “integration and execution risk,” I don’t know what does.

Digging deeper, there are two key concerns with this merger.

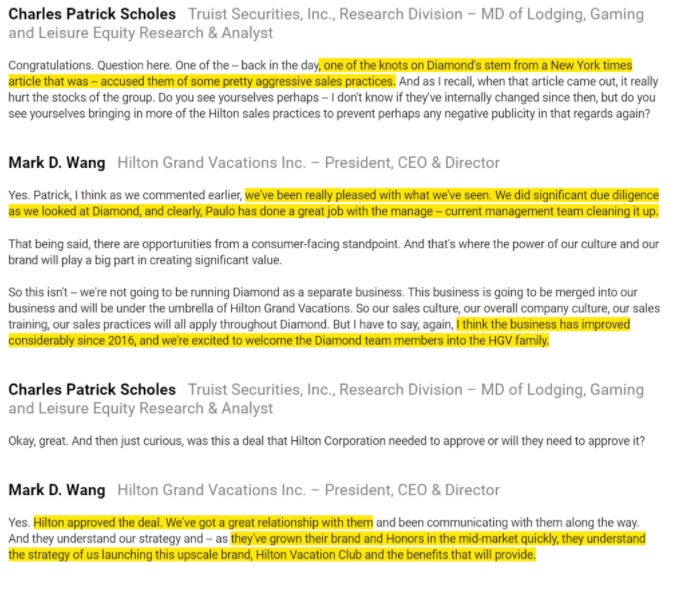

The first concern is the Diamond asset itself. Diamond was public several years ago, and everyone knew the asset had hair on it. Their accounting was a mess, their sales tactics were aggressive, and their properties probably needed a little TLC. Apollo bought them a few years ago, and Apollo’s reputation is certainly more along the lines of “cut costs to the bone and let some other sucker worry about the long term” than “invest through the income statement to build sustainable value for the long term.”

So yes, Diamond has hair on it. But I take some comfort in a few things. First, it’s not like HGV didn’t know about / diligence those issue heading into the deal.

And remember; for HGV to buy Diamond required consent from Hilton (the parent company). So it’s not just HGV that diligenced Diamond and got comfortable; Hilton had to diligence them as well and get comfortable that buying Diamond and slapping “Hilton” on their properties wouldn’t tarnish the Hilton brand. That doesn’t mean that Hilton is co-signing the financials or strategic rationale or anything, but I think having them as an extra set of eyes that Diamond isn’t about to implode or face a scathing legal scandal or anything is comforting.

The second risk here is management. The obvious management risk is that HGV has never done an acquisition, and their first one is one of the biggest in industry history and will require lots of integration work.

But I think the management risk runs deeper than that. I personally have followed the HGV team for some time and always liked them, but there’s no doubt that the team has tarnished their credibility in the past and a lot of investors just think they are bad actors.

I’ll highlight this risk with three examples, though all of them kind of work together.

-

The first example relates to guidance. Back in 2018, HGV held an investor day where they provided long term guidance. That guidance lasted all of two quarters; by Q2’19 earnings the company had pulled the long term guidance. That’s a pretty quick flip, and I know it burned management credibility with a lot of investors

-

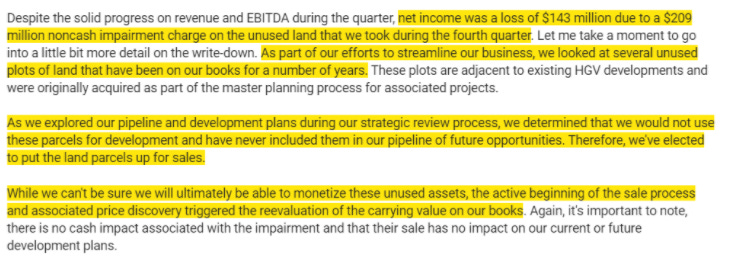

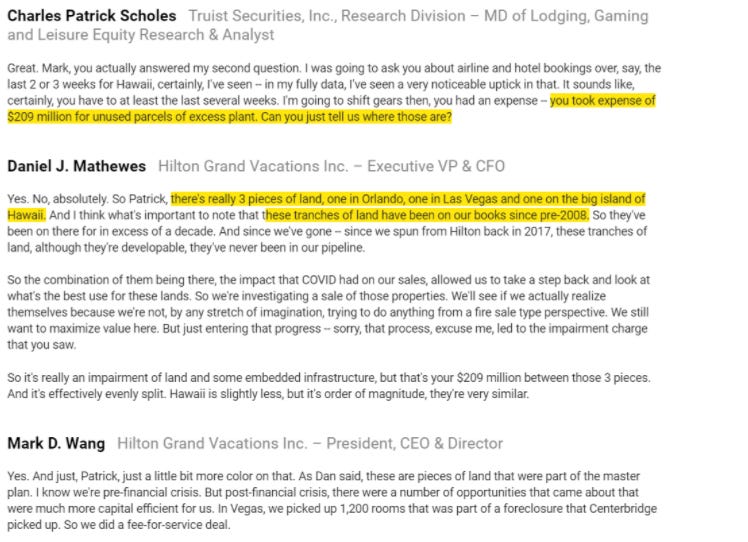

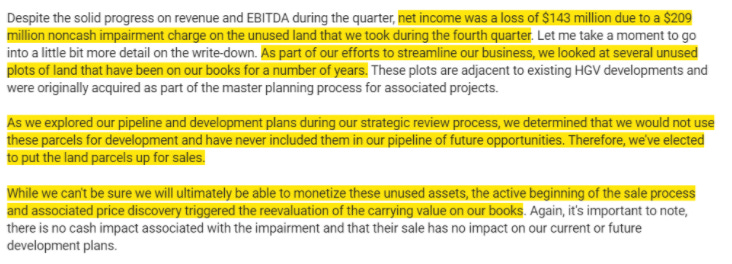

In their Q4’20 earnings, HGV took a >$200m write-down on some legacy used land. Management tried to explain this away by emphasizing it was a noncash charge and the land had been on their books since pre-financial crisis…. but it certainly raises a bunch of red flags that management had hundreds of millions worth of land sitting on their books for over a decade and just now decided to write it down. Why hadn’t these been assessed as part of the spin in 2017 or at some other point? (I’ve included the commentary on this write-down from the earnings call below)

-

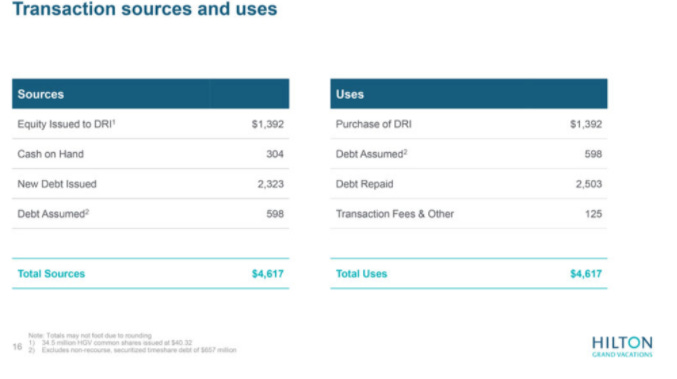

The sources and uses slide they gave for the Diamond deal was weird and confusing; for some reason they included the refinancing of overall HGV in the sources and uses and didn’t mark that clearly. Analysts were asking about it on the call, and I know tons of people were following up with the company on it for the next several days because it was so dang confusing. I’ve never seen a company botch a sources and uses page; that HGV couldn’t get that simple thing right raises some questions on both management competence and integrity. I’ve included both the misleading slide and an analyst questioning the slide on the merger call below.

Those are real questions and real risks…. but I’m comforted by a few things here.

-

Most importantly, the industrial logic of the deal makes sense. You can see that in the competitor quotes I mentioned above, and these quotes are not new; for years, the branded players have been discussing how rolling up nonbranded players would be accrettive. You can see that in the valuation and synergy work above. None of the HGV assumptions seem aggressive; in fact, based on peer deals and the industrial logic here, I think the synergy numbers are significantly lowballed.

-

Apollo is taking all stock for their deal. Apollo is a very rational player with lots of insight into the Diamond asset and the potential of the combined company; for them to take all stock suggests they see significant upside here.

-

It’s worth remembering that Apollo offered to buy HGV for ~$40/share in late 2019/early 2020; my understanding is that deal was held up because Hilton worried about Diamond / Apollo hurting the Hilton brand name and then the pandemic put the nail in that deal’s coffin. I think that’s worth remembering for two reasons:

-

That Hilton blessed this deal and wouldn’t bless the deal the first time around suggests that Apollo did make some headway into cleaning the Diamond up as well as that Hilton was a lot more comfortable with the HGV team buying and controlling the asset as a public company than with Apollo controlling it as a private company.

-

That Apollo has been trying to do the deal for this long suggests they are taking stock because they really believe in the industrial logic of this combination.

-

-

-

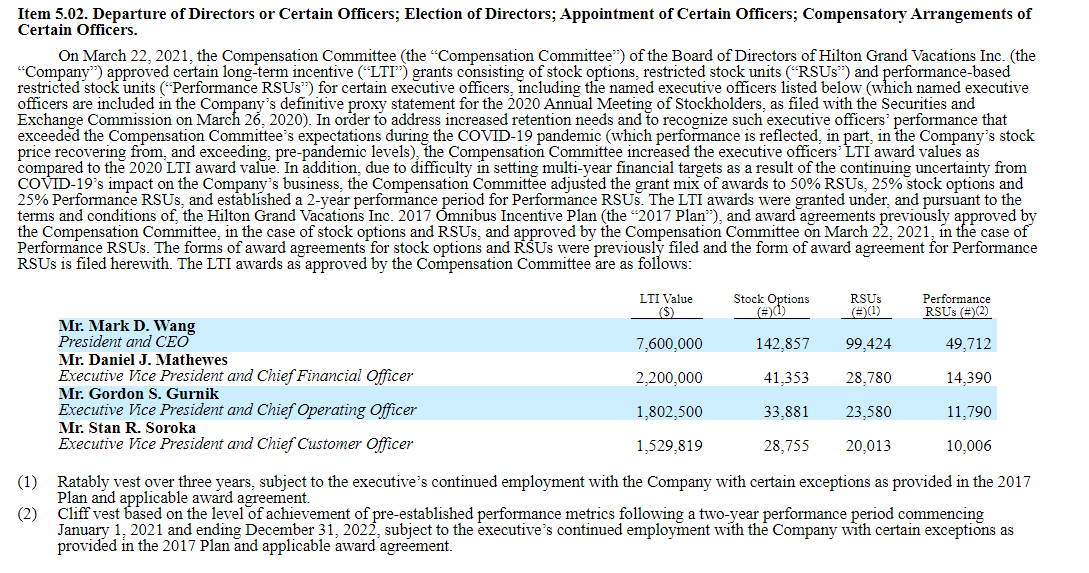

Right after announcing the Diamond deal, HGV struck a new comp deal with their management team. The deal is exclusively equity based. There’s lots of ways to read into this agreement, but I think the simplest takeaway is the management in the board struck this deal knowing how large the potential upside from a successful integration of the Diamond transaction was and this deal fully incentivizes them to successfully realize that upside.

So, yes, there are risks here. The merger integration can and likely will be messy. I would be shocked if we didn’t have a poor earnings report that way misses analyst estimates and causes the stock to drop 10%+ in the next few years. But I think all of those risks are easily made up for by the industrial logic and huge synergies from the deal (plus the incredible industry backdrop we’re buying into!)

To wrap this up: the timeshare industry overall has not participated in the current travel boom / rerating. I think that’s wrong; the companies should be among the biggest beneficiaries of the boom. And HGV’s merger with Diamond positions them perfectly to take advantage of the boom. Combine that with the massive upside to synergies and the revenue potential from the merger, and I think HGV is much too cheap and should enjoy a swift rerating once they close the deal and begin to successfully integrate.

Odds and ends

-

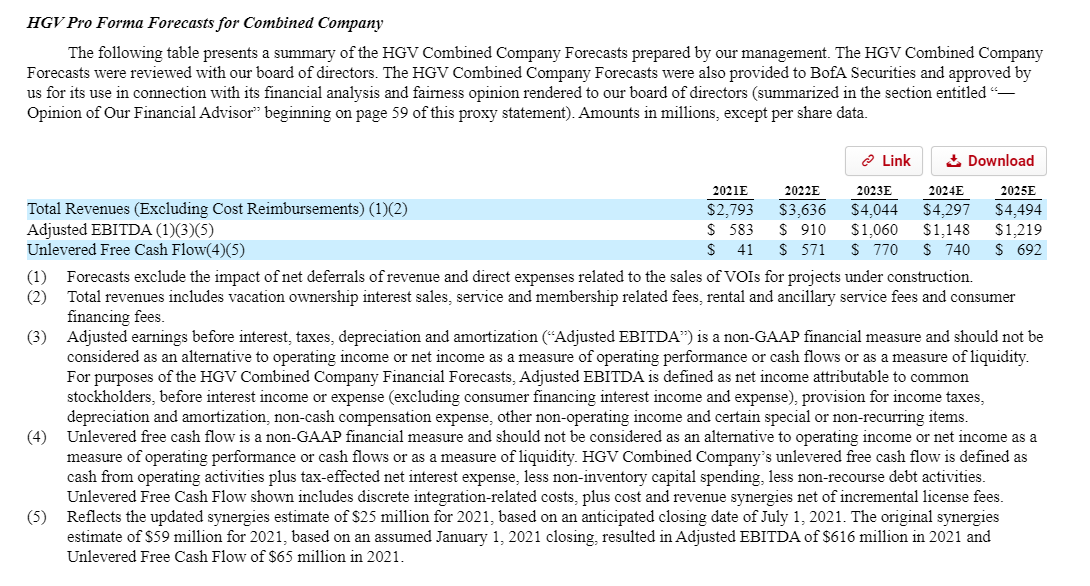

I was going to post this yesterday, and of course the company decided to file their prelim proxy roughly as I was set to press publish. I spent most of the afternoon going through the proxy, and it was largely confirmatory of everything I put in this write up (I’ll provide an update if I go back through it and notice anything new). The key stuff is probably the projections on p. 72, which I’ve pasted below. The company is forecasting >$1.1B in EBITDA for 2024; I think that’s reasonable and think there should be significant upside longer term from larger cost synergies and revenue synergies, but hitting that number should easily be enough to support the ~$80/share price target mentioned above.

-

The other interesting thing about the proxy is in the background of the merger section. Merger talks for HGV to buy Diamond started in June 2020, and it’s interesting to watch the companies trip over themselves to raise their forecasts as they start to understand the strength and pace of the recovery. The terms of the agreement are largely agreed to on December 15, and the time between then and deal announcement in March are largely spent on tax and legal diligence as well as ironing out specifics of the merger agreement.

-

-

An obvious question: if this merger is so good, why hasn’t the market responded more enthusiastically to the deal / why does this opportunity exist? I think it’s a combination of three things:

-

We have not seen much M&A in the timeshare industry. The only major M&A we’ve really seen was VAC buying ILG. That deal was a homerun; the synergies were enormous. But that’s really it for M&A in the timeshare industry (the Welk / VAC deal was pretty small; it more qualifies as bolt-on than full scale M&A even though it is useful for benchmarking), so I think analysts and the market might not be used to giving companies credit for value accrettive M&A in the industry. And HGV / Diamond is even more unique than ILG / VAC, as HGV is buying a non-branded company. That means the synergies should be significantly higher than in the ILG / VAC deal, thought there’s probably more integration risk.

-

Lingering skepticism over the Diamond asset. Diamond was public until Apollo bought them out and it was a hugely controversial stock. I quoted some of it above, but HGV’s merger call clearly reveals lingering skepticism among analysts. It’ll take a while to disprove that skepticism, but it should dissipate overtime (most likely once HGV begins to show signs of a successful integration) and that should lead to a rerating.

-

The company is using 2019 numbers to benchmark their valuation. I think that’s fine, but basically every travel / leisure company has blown through their 2019 EBITDA multiples and is clearly pricing in some type of boom cycle. By not providing forward projections, I think the market could be anchoring a little on the 2019 EBITDA numbers and leaving HGV behind in the travel boom. That should normalize in time; most likely once HGV closes on Diamond and gives a clean 2022 guidance number.

-

-

I mentioned at the front that I thought HGV could be an ~$80 stock in ~3 years (let’s call it by mid-2024). How did I get there? I think you start with the $883m PF 2019 EBITDA number the HGV gave for the post-Diamond company, add in some growth from the “roaring 20s” boom, and add another $125m in synergies from the Diamond purchase to bring the total synergy number to $250m (double their initial target; remember, VAC initially guided for $75m and did more than $200m plus revenue synergies, so I think $250m in synergy is still reasonably conservative). In total, that gets you to roughly $1.1B in annual EBITDA (roughly consistent with their proxy projections) for the 2022/2023 time frame, and the company should generate over a billion in free cash flow over the same time frame. If you assume that all goes to debt paydown, the company ends 2023 with <$2B in net debt. Slap a 10x multiple on $1.1B in EBITDA, take out the net debt, and you get a >$9B market cap. ~120m shares out gets you to >$75/share on those numbers, and I think every number I put in there was conservative (they’ll do better in cash flow, they’ll realize more synergies and growth than I put in here, they’ll do better on capital allocation than just paying down debt, and they should even free up some cash from some excess receivables they haven’t financed yet).

-

Note I wrote this section before the proxy with forecasts came out, but the proxy was largely confirmatory of every number above so I kept it the same.

-

-

HGV has a history of share repurchases; they bought back ~10% of their shares in a year from late 2018 to late 2019, and they had always been clear that returning capital to shareholders was their top capital allocation priority after funding organic growth. They paused repurchases in 2020 given the pandemic, and I don’t think repurchases are on the table for the near term for very obvious reasons (while the company has survived the pandemic, it’s not like they’re minting money currently!). However, once they get the Diamond deal done and they deleverage a little, I’d expect repurchases will very much be in the cards, and if their shares continue to languish both their history and the presence of Apollo as a major shareholder suggests that HGV will be aggressive with retiring shares.

-

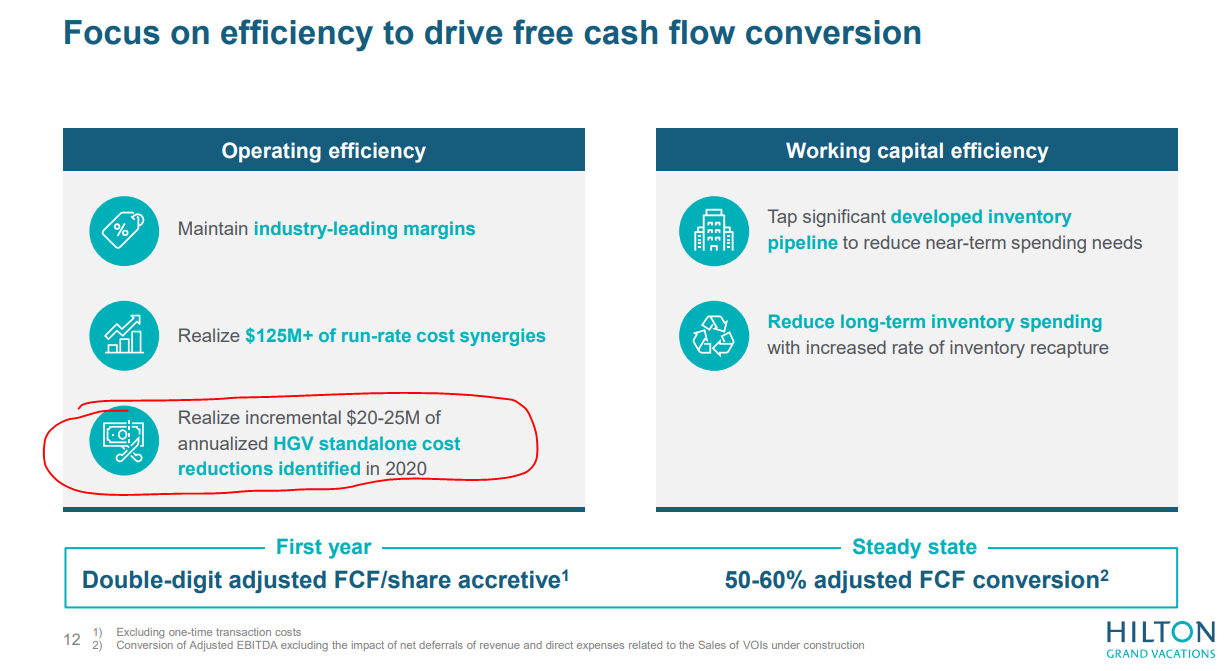

I’ve been valuing the company on “2019 PF EBITDA + synergies.” As mentioned above, I think the synergy number is probably much too low. I’d also note that HGV believes they took $20-25m in cost out of their business in 2020; valuing them on 2019 numbers plus synergies does not give them any credit for those cost cuts. Small in the grand scheme of things, but just adds a little more fire to the “the 2022/2023 EBITDA numbers are going to be way higher than projected” fuel.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

Successful integration of Diamond assets; big increase in synergies

| show sort by |