| 2024 | 2025 | ||||||

| Price: | 0.58 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 218 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 126 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | -115 | EBIT | 0 | 0 | |||

| TEV (in $M): | 11 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- None found

Description

Homology Medicines/Q32 Bio (FIXX)

Long equity

Homology (FIXX) is a failed gene therapy developer reverse merging into an inflammation and immunology company, providing investors 1) a valuable contingent value right (CVR) on its legacy assets and 2) a standalone newco trading near a neutral enterprise value (ignoring the value CVR). Buyers of a PIPE concurrent with the merger are paying 2.3x the current public market price for newco, also excluding the CVR. While illiquid, the setup is attractive for investors that can play small. The transaction is expected to close in Q1. Following the merger, investors will own:

-

A CVR for Homology’s 20% ownership of Oxford Biomedica Solutions which includes a contractual put option to sell the stake back to Oxford Biomedica (OXB) on 3/10/25 based on a predefined formula. It also includes the potential proceeds for monetizing Homology’s remaining gene therapy programs of PKU, MLD and its AAVHSC capsid platform. The CVR alone is potentially worth the entire stock price.

-

Q32 Bio (Q32, newco) is a well-funded, mid-stage biotech backed by biotech specialist funds Atlas, OrbiMed, Abingworth and Acorn. Randomized data read outs from their lead program in atopic dermatitis and alopecia areata are expected in 2024. The rights to the lead asset were regained by Q32 in November by way of a non-economic seller. Q32 had originally licensed bempikibart to Horizon Therapeutics (HZNP) in August 2022, however the acquisition of HZNP by Amgen shortly thereafter created FTC pressure for the divestiture of the asset. A clean (no-warrant) $42M PIPE concurrent with the reverse merger is priced at $1.36 per share and is backed by the same funds that invested in the prior $20M Series B at a similar valuation. Pro forma for the deal and ignoring the CVR, the market cap at $0.58 is $126M with $115M of cash.

CVR components

CVR for the Oxford Biomedica Solutions manufacturing assets

The CVR pertaining to Oxford Biomedica Solutions provides a value equal to 5.5x LTM revenue as of March 10, 2025. In March of 2022, UK based gene/cell therapy CDMO Oxford Biomedica (OXB LN) acquired 80% of Homology’s Massachusetts based manufacturing assets for $130M to Homology and it invested an additional $50M cash in the newly named Oxford Biomedica Solutions (OBS) subsidiary. Homology retained a 20% ownership in OBS and the agreement provided for a sale (put) of their stake back to Oxford Biomedica (parent company) for 5.5x LTM revenue any time after March 10, 2025. At the creation of OBS, the revenue was approximately $30M annually. If the revenue remained flat, the CVR associated with OBS would be worth approximately $0.57 per share (5.5 x $30M revenue x 20% ownership / 58M shares). Since Homology was intended to be one of the largest initial customers and its clinical programs are currently paused, it is unclear what the revenue is today. Oxford Biomedica has discussed customer expansion on recent calls though there are no specifics. Homology/Q32 is working to sell the PKU program (see second part of CVR below), ideally to an entity that would use OBS for clinical supply. The $30M revenue number was only a fraction of capacity utilization. On its September 2023 call, Oxford management stated, “Homology announced a few months ago that they were seeking strategic options… we are supporting them as their CMC partner on their lead programs which they are trying to out-license. We are not planning any further revenues from that piece of the business for 2024…We’re looking to utilize that capacity from 2024 onwards for lenti programs.” Given the shortages in lentiviral manufacturing in the US (BMY/TSVT’s Abecma and JNJ/Legend’s Carvykti are notable examples), it’s possible the revenue hole could be filled by new customers and another party could pick up Homology’s PKU program. We are not modeling this, but it should be noted that the maximum contractual put price of FIXX’s stake in OBS is $74.1M ($1.28 per share). Our best guess is revenue ends up somewhere between $15M and $30M by March 10, 2025, equating to $0.28 to $0.57 per share.

CVR for development assets

Homology was a clinical stage AAV gene therapy company with programs in rare diseases including HMI-103 for Phenylketonuria (PKU) in clinical dose escalation and HMI-204 for Metachromatic Leukodystrophy (MLD) in IND enabling studies. Following the closing of the Q32 Bio/Homology merger, Q32 must engage commercially reasonable efforts to monetize these legacy assets for the benefit of CVR holders for 6 months. The PKU in vivo editing program provided encouraging data on the first three patients in Cohort 1 in July and October 2023. In a more buoyant biotech market, the data would have been financeable. Biotech markets continue to sputter, and the large cash burn needed to advance the trial coupled with the out-of-favor gene therapy/editing sector, caused them to pause development. There is potential value in the PKU and the MLD program. PKU is a potentially very large market as demonstrated by sales of standard of care enzyme replacement therapies (ERT) Palynziq and Kuvan selling a combined $750M annually (pre-genericization). Less than 25% of PKU patients are on current therapies due to tolerability and response rates. Homology had estimated a $2B opportunity for PKU. There is a reasonable likelihood of value recognition for the development programs though we have no estimate on where a deal might land as comps range from $5M to hundreds of millions.

Homology will also try to monetize its proprietary AAVHSC capsid platform. There have been some sizeable deals in the capsid space, though they have been with engineered chimeric capsids rather than the wild type capsid technology of Homology. Voyager converted from gene therapy developer to a propriety capsid developer inked a $100M upfront dea from Novartis plus $1.2B milestones and royalties on net sales. Voyager also executed license deals with Neurocrine and AstraZeneca in 2023. AstraZeneca also acquired LogicBio for $68M in October 2022 for its sAAVy engineered capsid technology. We ascribe $0 to the capsid platform, but there may be some IP value to someone.

The CVR is at least worth the OBS put and the therapeutic programs provide additional value. For a sanity check, the S-4 merger document estimates the fair value of the CVR at $14.3M ($0.25 per share).

Q32 Bio (QTTB) aka Newco

Before delving into the merits, let’s highlight what investors are paying for Q32. Pro forma shares outstanding are 218M. At $0.58 the market cap is $126M and the pro forma cash at deal closing is projected to be $115. Consequently, excluding the CVR detailed above, investors are paying roughly $10M for a well-funded, highly pedigreed biotech with randomized readouts coming this year.

Q32 Bio has a mid-stage pipeline of immunology and inflammation assets consisting of bempikibart, an anti-IL-7/anti-TSLP mAb in randomized controlled trials in both atopic dermatitis and alopecia areata, each reading out in 2H 2024.

Q32 also has a C3 complement inhibitor with data in Lupus Nephritis/IGA Nephropathy (LN/IGAN) and Anca Associated Vasculitis (AAV) with data coming in 2024 and 2025.

Bempikibart

Bempikibart is an anti IL-7/TSLP mAb in randomized Phase 2 clinical trials atopic dermatitis (AD) and alopecia areata (AA). While both categories are competitive, they are blockbuster commercial markets with room for newer, safer therapies.

Q32 originally licensed bempikibart (bempi) from BMY in 2020. After running P1 SAD/MAD PK/PD trials Q32 was able to license bempi to Horizon Therapeutics (HZNP) for $55M upfront, $645M milestones and net sales royalties. We believe Amgen acquiring Horizon precipitated the sale of bempikibart back to Q32. The FTC heavily scrutinized the AMGN/HZNP merger, and Amgen already markets a TSLP, TEZSPIRE, approved in asthma and currently selling $161M per quarter in its second year of launch. It’s a blockbuster in the making.

Atopic Dermatitis (AD)

AD is a competitive but massive market. Current therapies run the gamut of basic steroids, newly approved topicals including OPZELURA (JAK), VTAMA (AhR agonist), ZORYVE (PDE4 inhibitor), and systemic treatments like JAKs or anti IL-4/IL-13 mAb blockbuster Dupilimab (Dupixent, Dupi). Bempikibart would compete with Dupixent, which currently generates $11 Billion in sales, dominated by AD. As noted in the slide below, 30% of patients are not controlled by Dupi which leaves a lot of the market available. Bempi could also potentially compete directly. Dupi is the only biologic approved for AD in the US though LLY’s copycat Lebrikizumab is coming in the near/mid-term despite its recent CRL for CMC (Lebrikizumab LLY CRL). Bempi is an anti-IL-7/TSLP, which is targeting a different pathway than IL-4/IL-13. Since bempi has only shared data from healthy volunteers and PK/PD data in patients to date, we can’t handicap the efficacy outcome of the trial. It’s a big TAM, Horizon bought into the concept, and randomized data is coming in months.

While bempi is a combo mechanism of action more directly hitting IL-7 than TSLP, it should be noted that Tezspire (tezepelemab), the fast growing TSLP inhibitor in asthma, failed in AD in 2018 tezepelemab in AD. This was well known long begore HZNP/Q32 began their campaign.

Q32/HZNP dosed its first patient in AD in October 2022. The trial design is detailed in the slide below; N=102, randomized vs. placebo with mean % change in EASI at week 12 as the primary endpoint. The data is expected in 2H 2024.

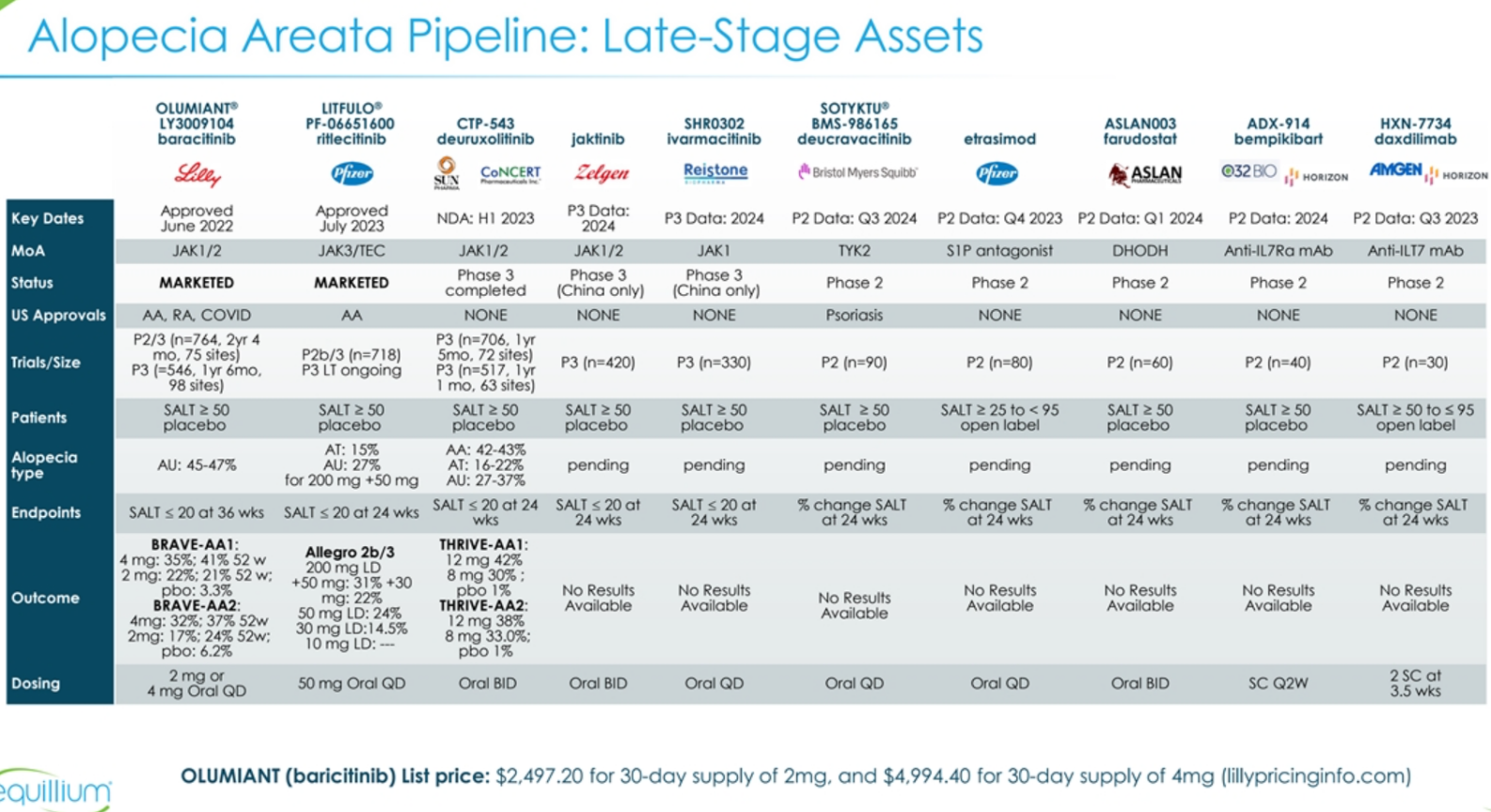

Alopecia Areata (AA)

AA became a major market with the approval of Eli Lilly’s Olumiant (barcitinib) in June of 2022 and the approval and Pfizer’s Litfulo (ritlecitinib) in June of 2023 along with Sun Pharma/Concert’s deuruxolitinib upcoming PDUFA. JAKs are highly effective at restoring hair growth, however they have serious adverse effects, and all come with a black box warning for “serious infections, mortality, malignancy, major adverse cardiovascular events, and thrombosis.” JAKs are known to lose their effectiveness very quickly after stopping treatment or even reducing the dose. Catastrophic side effects coupled with the need for chronic dosing leave the door wide open for a safer, effective treatment. Q32 is one of the most advanced competing programs.

Q32/HZNP dosed its first patient in AA in September 2023. The trial design is detailed on the slide below; N=40, randomized vs. placebo with mean % change from baseline in SALT score at week 24. Like the AA trial, top line data is expected in 2H 2024.

Below is a good overview of the approved JAKs and novel MOA’s running programs in AA.

Bempi Asthma on the come?

TSLP just recently became a very hot target. This month, GSK just announced it would acquire private TSLP company Aiolos Bio for $1B upfront and $400M of additional milestones (GSK/Aiolos). Aiolos is focused on asthma, which we speculate could be an additional area of focus for Q32. As noted earlier, Amgen’s TSLP TEZSPIRE is experiencing a very robust commercial launch in asthma. At the JPM conference earlier this month Amgen CEO Bradway said:

“With respect to the future of our inflammation franchise, as I mentioned, we're investing heavily in TEZSPIRE based on our confidence in this novel mechanism of action and what we think this can do for patients that struggle with the effects of autoimmune disorders. In addition to COPD which I already mentioned, I would remind you that we have a Phase III study underway in eosinophilic esophagitis as well as a study in chronic rhinosinusitis.”

While there are no trials planned, management thinks bempi could be effective in asthma.

ADX-097 C3 mAb Tissue Targeted Complement program

Complement activation in autoimmune has been a productive field with the 2021 approval of TAVNEOS (avacopan) and Amgen’s subsequent acquisition of its developer Chemocentryx for $4B in mid-2022 (AMGN/CCXI). Q32 has a C3 complement inhibitor engineered for tissue specific targeting designed to improve tolerability efficacy. To date Q32 has run 56 patients in SAD/MAD P1 studies arriving at a recommended P2 dose (450mg subcutaneously weekly). Q32 is running 2 Phase 2 trials with ADX-097: 1) A 30-patient basket trial for patients with either Lupus Nephritis, IGA Nephropathy or C3 glomerulopathy with interim data year end 2024 and 2) An 85-patient trial in AAV (TAVNEOS’ indication) with Part A data in 2H 2025.

Conclusion

Homology/Q32 looks very mispriced at $0.58 with a CVR possibly worth more than the stock price alone and the valuation of Q32 Bio zero despite an attractive pipeline of therapies and an investor base of biotech validators. A part of the CVR should be realized in 2025 when OBS is put back to Oxford Biosciences and buyers could also materialize for the legacy PKU and MLD programs. Ignoring the CVR, investors are paying approximately $10M for Q32 while the PIPE investors are paying $200M valuation ($317M mkt cap - $115M cash) for their $42M PIPE concurrent with the reverse merger. The PIPE is coming in at $1.36 on a FIXX price equivalent basis and they are not entitled to the CVR. The biotech heavyweight funds sponsoring include Orbimed, Acorn, Atlas, and Abbingworth and all participated in the prior $20M Series B in December 21 at $1.097. Q32 Bio’s therapeutic programs are in attractive new MOAs that have experienced recent M&A, large pharma has validated its lead asset, management is credible, and randomized data is coming this year. Put together, FIXX is an attractive collection of assets.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

- Closing of the reverse merger of Homology (FIXX) and Q32 Bio

- Distribution of the CVR for legacy FIXX holders

- Stand alone Q32 Bio debuting in the market and introducing investors to newco

- Randomized bempikipbart data in atopic dermatitis in 2H 2024

- Randomized bempikipbart data in alopecia areat in 2H 2024

- Interim data on ADX-097 in lupus nephritis/Iga nephropathy and C3 glomerulopathy

| show sort by |