| 2020 | 2021 | ||||||

| Price: | 95.84 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 19 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 1,781 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | -296 | EBIT | 0 | 0 | |||

| TEV (in $M): | 1,485 | TEV/EBIT | 0 | 0 | |||

| Borrow Cost: | Available 0-15% cost | ||||||

Sign up for free guest access to view investment idea with a 45 days delay.

- INNOVATIVE INDUSTRIAL PPTYS IIPR S 11/09/2019

- BETA

- AYR STRATEGIES INC AYRWF 02/06/2021

- ASCEND WELLNESS HOLDINGS INC AAWH 06/16/2022

- CHICAGO ATLANTIC REA E F INC REFI 06/15/2023

- The Parent Company (TPCO Holding Corp.) GRAMF 02/12/2021

- WM TECHNOLOGY INC MAPSW 07/15/2022

- GREEN THUMB INDUSTRIES INC GTBIF 12/06/2021

- GLASS HOUSE BRANDS INC GLASF 12/09/2021

- CRONOS GROUP INC CRON. 09/14/2023

- Anebulo Pharmaceuticals ANEB 08/02/2022

Description

Innovative Industrial Properties (NYSE:IIPR)

Business Overview and Investment Thesis

Innovative Industrial Properties is an internally managed REIT focused on the acquisition, ownership and management of cultivation and manufacturing properties leased to state-licensed cannabis operators. The company acquires properties through sale-leaseback transactions and third-party purchases. By the end of 2019, the company managed 46 properties with 3.1M square feet in rentable space, out of which 34 properties (consisting of approximately 1.9M square feet) were acquired during FY2019. Year-to-date, the company has acquired a total of 11 properties with 1.2M square feet of gross leasable area to bring the portfolio total to 4.3M SF across 57 properties. The company is trading at 32.3x 2019 P/FFO. Based on 2020E FFOps, the company is trading at 17.2x P/FFO.

Capitalization Table

As elaborated through this report, we believe investors are not adequately compensated for the operational and counter party risks that IIPR is taking. Also, while the company has historically earned yields in magnitudes of mid-to-high teens, the outsized returns have started to meaningfully compress and will further decline (for the same level of counterparty risk) as operators access alternative sources of funding. In early April this year, Grizzly Research published a short report (Link) on IIPR highlighting several red flags with IIPR’s business that we wholeheartedly agree with, including extreme counterparty risk, massive overpayments for properties to inflate book value of portfolio, lack of disclosure on the condition of the existing portfolio, and Alan Gold’s (IIPR’s Executive Chairman) involvement in another real estate life science development venture. Grizzly’s team visited sites in person and found many assets past their construction dates with no meaningful cash flow or revenue generation capabilities in sight. All-in, they see 38-49% of IIPR’s rental income in jeopardy.

Despite the clear warnings, the stock continues to remain significantly inflated. In the last two years the stock has appreciated massively (albeit with significant volatility), up +150%, on the back of hype in the cannabis sector, scarcity (being the only major publicly traded cannabis REIT), an incorrect perception of unlimited pipeline of acquisition opportunities, and outsized return on investments that provide arbitrage opportunities for the company vs. its cost of capital. However, as the cannabis hype fades, and the economic environment deteriorates as a result of the global pandemic, investors should focus more closely on the company’s fundamentals that are increasingly alarming and pose serious downside risk to valuation and even the viability of business. We identify the following issues as primary focal points for investors:

- Unsustainable Business Model

- A Concentrated and Risky Portfolio of Assets

- Concerning Developments from the Latest Quarterly Results

- Overvalued Relative to the Underlying Fundamentals

- COVID-19 Spurs Tenant Failures

- Regulatory and Competitive Risks

Unsustainable Business Model

IIPR attracts investors with a yield arbitrage that the company generates as it deploys capital at a ~13% average yield while raising capital at a current 6.7% implied cap rate. However, a deeper look reveals that this model is not sustainable for very long and the yield is not enough to reward investors for the risk that the company is taking. There are two likely scenarios that the company will have to pursue going forward, both of which will likely result in the collapse of the arbitrage and/or higher risk of default by tenants:

- IIPR will grow its tenant base with the primary focus on larger scale Multi-State Operators (MSOs). While these operators have better operating prospects than smaller regional players, there are fewer such opportunities available to IIPR and these MSOs demand much lower yields given their broader access to capital (traditionally in the form of equity but more recently in fixed income as well). Some of IIPR’s larger tenants have also secured traditional debt financings at rates that raise concerns on whether IIPR investors are adequately compensated for the risks that the company is taking. For example, Cresco, Trulieve, and Green Thumb Industries have all raised debt at 9.75%-13% coupon rates on senior secured bases (plus warrants) vs 11-12% yields for IIPR sale leaseback transactions that are lower priority in bankruptcy scenarios. As these companies execute on their milestones, they will become less reliant on outside funding with 10-20-year lease commitments. A continued path on this strategy would surely result in collapse of the yield arbitrage for IIPR, while still presenting meaningful default risk on leases. In fact, the company’s weighted average portfolio yield has shown signs of substantial compression in recent quarters, declining from 15.3% in Q4/2018 to ~13% and will continue to decline going forward given increased competition in capital. In fact, the company has stopped disclosing individual property acquisition yields and more recently has even refrained from releasing average portfolio yield all together, which we think is a red flag.

- IIPR will pursue riskier transactions with lower quality tenants to boost scale and yields. Until about a year ago, this was IIPR’s strategy – to transact with regional or smaller private multi-state operators who were in desperate need for funding and demand heavy yields. At a time when the market was very receptive to the space and private funding wasn’t very scarce, this strategy seemed practical – at least in the short term. However, IIPR soon realized that these smaller players are running out of funding alternatives to finance their rent commitments. As such, the management team showed reduced willingness to pursue this strategy but given investors’ expectations of a robust pipeline and capital deployment, management has recently shown a higher propensity to transact with smaller private operators (e.g. Transactions with Holistic, Kings Garden, Ascend Wellness and Greenleaf in recent months). Ultimately, this acquisition strategy will increase credit risk and the probability of default which will lead to a re-rate in valuation. Once again, this should eliminate the existing yield arbitrage for IIPR. As the industry evolves and companies move towards a CPG oriented ecosystem, manufacturing scale, diversified product delivery forms, brands and management experience will take over cultivation capabilities. These pressures will weigh more heavily on smaller operators that lack experience, funding and valuable partnerships, potentially resulting in bankruptcies. Unlike some of the legacy transactions that IIPR was able to execute on during the cannabis hay-days a couple of years ago, this will be a much riskier route to pursue going forward.

The company’s underwriting practice is also very troublesome as evidenced by one of its tenants, DionyMed. Shortly after IIPR signed an agreement with the company, DionyMed became the first credit default in the public US cannabis industry. This makes us question management’s investment/due diligence process, risk mitigation and financial acumen. There is a good chance we may see further credit defaults, a notion that is even speculated by sell side analysts. On a report from March 10, 2020, Craig Hallum reported, “However, one small tenant (1.0% of portfolio by square footage) has defaulted and we wouldn’t be surprised to see more small tenants default over the next 2 years though IIPR closely monitors tenant financials and sees no short term risks”.

We also have concerns on the magnitude of tenant reimbursements that IIPR has committed . Given the structure of their transactions and target properties (high tenant improvements vs acquisition prices), IIPR is highly exposed to properties that are not yet fully operational and lack any meaningful cash flow generation ability in sight. As of the latest quarter, the company had $265M of tenant improvement capex that were committed but not yet funded (including $119M that have been incurred but not yet funded). Additionally, IIPR provides incremental reimbursement options to a couple of its tenants (including Trulieve and GrassRoots), in the amount of $53.8M which exposes the company to further deteriorating credit risk. These are essentially a form of “options” offered to tenants which will likely get exercised if the tenant is unable to receive funding from alternative sources. IIPR would be doing more harm to themselves once these options are called by the tenants; further increasing credit risk.

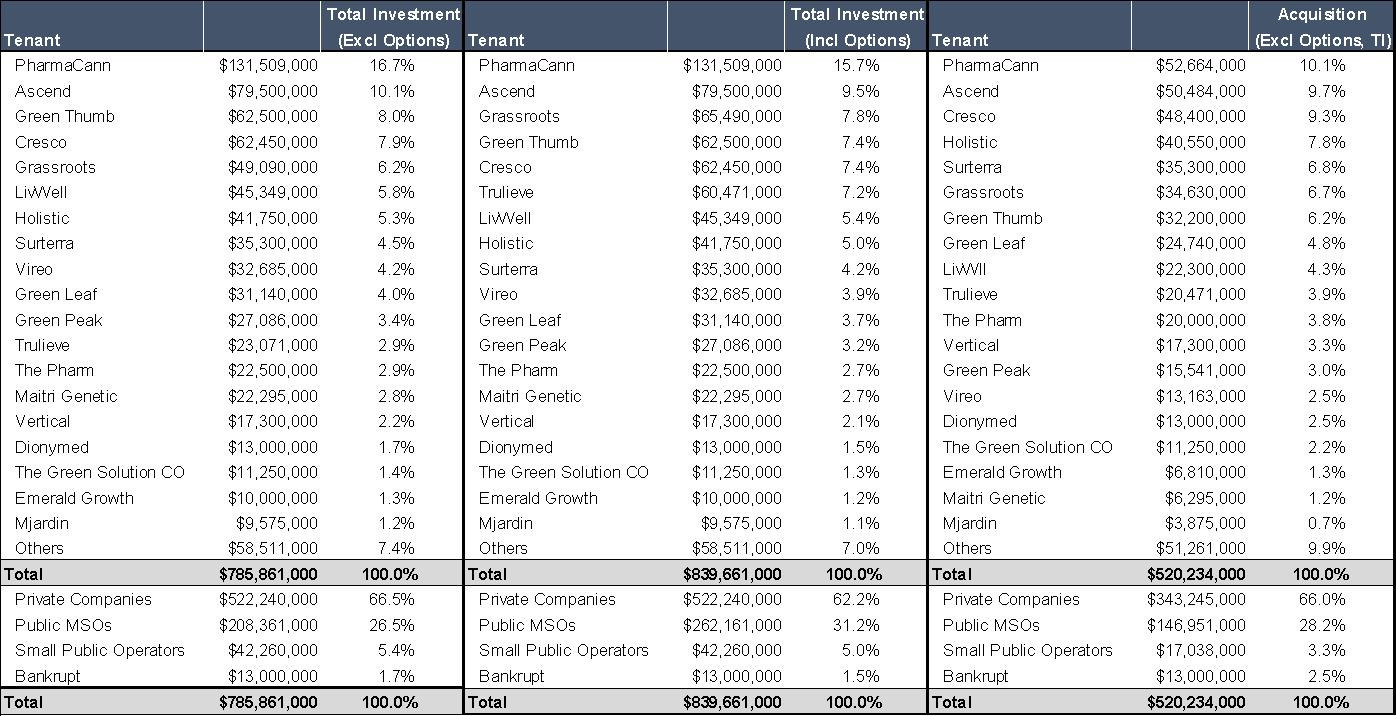

Concentrated and Risky Portfolio of Assets

Despite some recent transactions with larger multi-state operators, IIPR’s portfolio is still heavily comprised of smaller, lower quality tenants. Private company tenants together with smaller public tenants make up ~70% of IIPR’s portfolio (as shown below):

Portfolio Composition

In particular, private companies make up over 66% of IIPR’s portfolio. According to the company’s most recent financials, PharmaCann accounted for 24% of the company’s rental revenue while Ascend Wellness was ~9% rental revenue. A number of these companies are cash strapped, with limited access to capital and a majority have been unable to go public due to inadequate investor demand and/or slow progress in operations. Other smaller public operators face similar issues with very limited cash runway, low trading volumes and negative cash flows which limit their abilities to raise equity and debt.

Many of these smaller tenants have completed numerous transactions with IIPR at onerous yields which has further exacerbated their financial positions. While this has boosted portfolio scale and rent income in the short term, it has deteriorated the portfolio quality. A few examples include PharmaCann and Vireo which are two of the earliest IIPR tenants and have continued to transact with IIPR with 9 combined properties. Both have experienced numerous difficulties as described below:

- PharmaCann struggled through most of 2019 with the termination of its agreement with MedMen and had to pay a termination fee through a transfer of membership interests in three entities (weakening its credit quality). The company’s Co-Founder and CEO also resigned. Lastly, all PharmaCann’s cultivation properties are now encumbered and it doesn’t have further sale-leaseback alternatives. As private capital to cannabis is heavily challenged, the company’s financial position only becomes weaker.

- Vireo’s gross margins have lowered and the company has lagged expectations for dispensary rollout. The company also recently cut ties with its high profile Chairman, Bruce Linton, who had joined the company in the hopes of further bringing additional capital and investor interest. However, upon his departure, Mr. Linton made a statement that indicates the company is running behind in operational execution and investor expectations – “If I invest and bring people’s money along I’m a pretty demanding guy”. With four properties tied up with IIPR at high yields (13.5% to 16.5%), Vireo already faces an uphill battle in generating meaningful cash flow to meet these obligations. Vireo’s has also faced legal issues in the past, with two of its previous employees allegedly involved in illegally smuggling cannabis oil between states.

IIPR tenant financial and credit health is paramount, especially since its portfolio is so concentrated. However as private funding dries up and cash flows continue to underwhelm, it is only a matter of time before additional tenant defaults surface. So far, as shown by the Dionymed bankruptcy, replacing tenants for cultivation and manufacturing facilities is a very challenging task. IIPR’s portfolio almost entirely consists of industrial properties, most in remote locations, that provide very limited recovery value. IIPR typically acquires these properties at expensive valuations, with heavy tenant improvement requirements. On average, IIPR has acquired properties $209/SF vs. an average $145/SF for more traditional industrial REITs (Source Green Street Advisors Company Analysis), about a 44% premium. Outside of cannabis operators, no tenant will be willing to pay anywhere close to these levels for IIPR’s properties. It will likely be just as difficult to find new tenants or buyers for the assets for cannabis purposes. Unlike in the earlier days of the cannabis bull-run, investors are far more focused on cash flows than topline growth and one of the key hurdles for companies to achieve this has been expensive lease and interest obligations. Also, with a more challenging capital markets environment for the sector compared to 2015-2019 period, management teams are far more cautious in undertaking expensive obligations such as 10-20 year lease durations. IIPR’s precedent tenant, Dionymed, should present a very clear example to investors on difficulties in tenant replacement. The company’s Esperanza property is located just 3 miles from downtown Los Angeles and is considered a premium property relative to IIPR’s other assets. Regardless, the asset is still pending a new tenant even after 7 months since defaulting on rent.

Concerning Recent Developments

The latest quarter and subsequent events have revealed some early signs of tenant distress with several rent deferrals as well as tenant improvement cancellations.

- Cancellation in Tenant Improvement ProjectsIn the first couple of months of 2020, several tenant improvement projects were cancelled. There will possibly be more following the pandemic. These include:

- PharmaCann - Cancelled a $4M funding commitment related to a lease at one of its Pennsylvania properties

- Green Peak - In January 2020, IIPR and the tenant amended the lease terms which among other things, cancelled the remaining tenant improvement allowance of about $15.2M

- DionyMed - The tenant defaulted which resulted in the cancellation of $2M in tenant improvements to be provided by IIPR

- Numerous Requests for Rent Deferrals Show Early Signs Financial Struggle for TenantsOn the latest earnings call, management revealed that 3 tenants (Vertical in CA, Green Peak in MI, and Maitri Genetics in PA) have already requested rent deferrals in the early weeks of the pandemic. While the management and sell-side analysts have downplayed the impacts of the deferrals, they do represent a relatively meaningful portion of the revenues on an annualized basis (i.e. Over 10% of annualized revenue based on Q1/2020 performance). What is even more concerning is that these operators are not even the riskiest tenants in IIPR’s portfolio. The problem can amplify much further if tenants that make up a larger portion of the rental income (PharmaCann, Vireo, Holistic, Ascend) start to defer or even default on their rents and there exists a relatively high probability that these tenants will do so. We also learned that the repayment timeline for rent deferral is relatively long (18 months starting on Jul 1st) indicating cash flow difficulties for these tenants for potentially an extended period of time.

- Increasingly Dilutive Down-round FinancingsIIPR just recently completed a $115M financing, which while smaller than the company’s previous financing rounds, highlighted a continued trend of frequent and increasing dilutive financings. For perspective, the recent financing was issued at a 12.7% discount to the last closing day vs 7.8% and 8.4% in the previous two rounds respectively. The latest round, though in-line with the January 2020 financing, (~$74/share vs $73.25/share) was more dilutive than the ATM drawdowns ($78-$79/share thus far) and far more dilutive than the financing completed in 2019 ($126/share). With a pro-forma cash balance of $432M and $265M in tenant improvement capex, it wouldn’t be surprising to see the company further access the ATM facility (which has $59M available) or complete another dilutive financing before year-end.

Overvalued Relative to the Underlying Fundamentals

IIPR vs. Traditional Net Lease REITs

Given its risk profile compared to the rest of the REIT landscape, IIPR is highly overvalued. The stock is currently trading at an undeserving premium valuation relative to other net lease REITs. The traditional net lease REIT subsector has a substantially lower risk profile than cannabis focused real estate for the following reasons:

- Better tenant quality and investment grade tenants

- Diversified in multiple sub-sectors of real estate

- Larger scale portfolios

- Higher sensitivity to tenant bankruptcies

- Higher quality properties in terms of location and repurposing value

- More transparency in reporting traditional REIT metrics

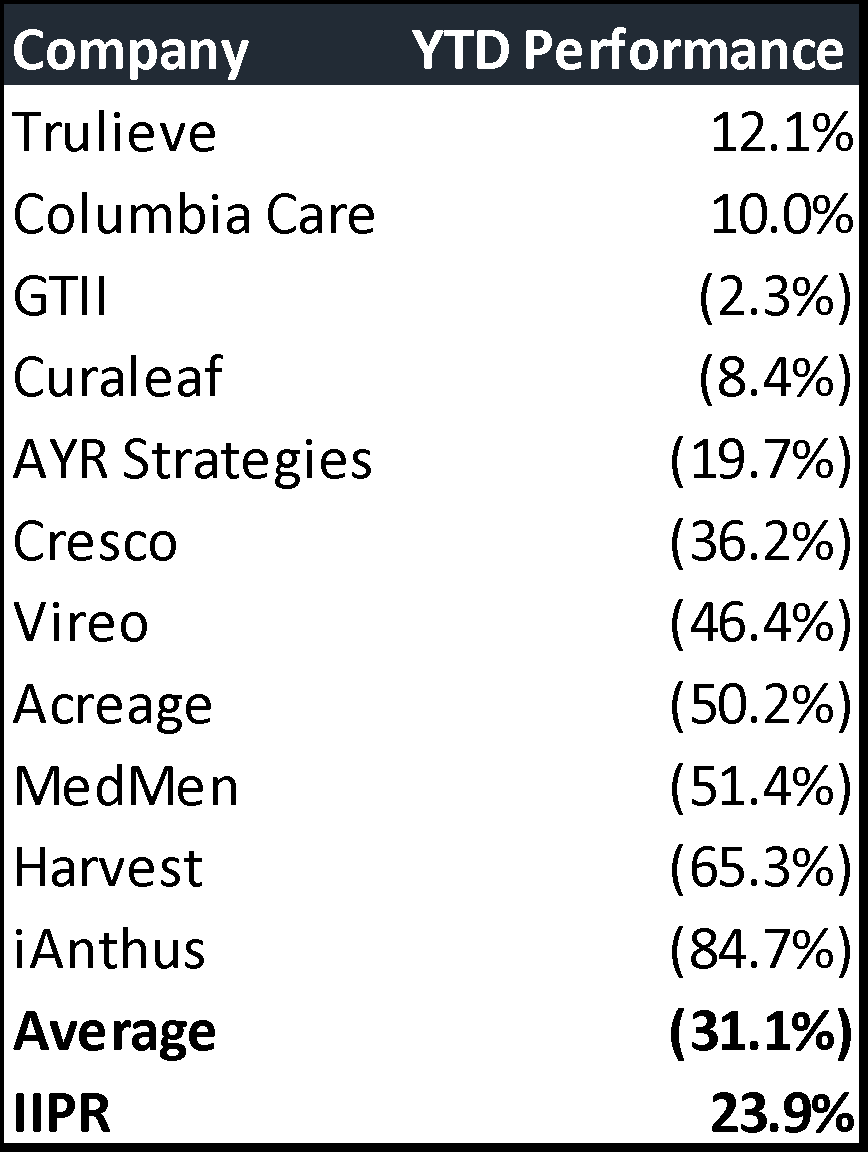

There is a massive disconnect between IIPR and the rest of its tenants (using the US cannabis sector as a proxy) which leaves significant downside for IIPR shareholders. While the rest of the sector is down an average of ~31%, IIPR is up ~24%. Furthermore, the current premium valuation does not include the following considerations:

- This valuation also has not accounted for the bankruptcy of Dionymed or the lower quality tenants that IIPR has compared to other net lease REITs

- This valuation also implies a perfect execution plan in an environment where the pace of acquisitions have slowed down sequentially ~50% (seasonality not a material factor according to management)

Cannabis Operator Share Price Performance

COVID-19 Spurs Tenant Failures

Like many businesses operating today, IIPR has been impacted by the COVID-19 pandemic. In the best case scenario, the pandemic results in diminished demand and disruptions to operations while the worst case scenario involves COVID-19 virus being the final blow to many of IIPR’s struggling tenants. At the very least, a good portion of IIPR’s rental income is in jeopardy. Lease up speed is harmed as COVID-19 only delays negotiations and negatively impacts the company’s portfolio. Some operators in the sector are already facing financial difficulties and have started to default on their obligations. For example:

- iAnthus announced default of interest obligations to debenture holders due March 31, 2020 and is expected to default on interests due June 30, 2020

- Green Growth Brands filed for bankruptcy following entering receivership on its CBD business, and defaulting on note

- MMEN shut down 7 of its FL dispensaries

- Acreage temporarily shut down a portion of its operations

- Several operators have revised down or suspended their operation guidance for the year

There have also been several operational setbacks in recent months, some being a direct result of COVID and others due to pre-existing challenges within the sector that are further amplified by the pandemic. For example, we have seen a meaningful number of management resignation and departures in recent months (e.g. MedMen, Cresco, Harvest, Acreage, iAnthus, Vireo and more) and several M&A terminations (including Cresco/Tryke, Acreage/Deep Roots, Acreage/Greenleaf Compassionate Care Center, Harvest/Verano, MJardin/Cannabella). These are all credit negative developments and though they save the acquirers from upfront cash outlays, they meaningfully hurt pro-forma cash flows.

COVID-19 has also caused huge disruption to dispensary operations. Visitor counts are in decline and continue to remain low because of social distancing measures. Some states such as Massachusetts and Nevada fully suspended recreational stores for over two months. Many others that resorted to curb-side pickups and home-deliveries are seeing meaningful decline in sale volumes vs in-store purchases. Latest numbers indicated that recreational cannabis retailers were losing on as much as $1.8M of daily sales in Massachusetts while dispensary sales were shut (and likely still losing as much as over half of that with curbside pick-up and delivery). In Nevada, medical and recreational dispensaries were ordered to close their store fronts through an emergency declaration which lasted over two months. And while the state has re-opened dispensaries, there are very strict social distancing rules in place.

The impacts go further than just retail operations. COVID-19 will impact tourism in states such as California, Nevada (56M visitors in 2018), Massachusetts (30M visitors) and Illinois (117M visitors in 2018). COVID-19 will be a huge blow to these states that derive a large portion of their adult use sales from out of state/foreign visitors. IIPR is specifically impacted as the company has a large exposure to facilities in these states. Last and perhaps most importantly, the pandemic is causing significant delay or termination for construction projects, as well as license and regulatory approvals for cannabis operations. These impacts will result in smaller and slower tenant improvement capital deployment. Massachusetts and Illinois, which are some of the top jurisdictions for IIPR’s tenants, are among the worst hit regions by the pandemic. The virus is impacting demand, construction and even state legalization efforts. Thus far, efforts to include cannabis as part of a broader coronavirus relief package have been unsuccessful. Current efforts face serious push back by Republicans, particularly in the Senate, leaving the sector to meaningful liquidity risk.

Regulatory and Competitive Risks

IIPR faces a significant headwind from US federal legalization and other legislations like the SAFE act and STATES act. The mentioned legislation would introduce the cannabis industry to alternative financing sources. The Secure and Fair Enforcement (SAFE) Banking Act passed in September 2019 in the US House of Representatives and there are several positive commentaries on the potential passing of the bill in the Senate over the next few months. COVID-19 has revealed the weakness of the current financial system for the cannabis industry and may act as a catalyst for the bill to be passed.

The latest bill proposed by the House (HEROES Act) is a large omnibus bill containing emergency appropriations for the coronavirus pandemic and it includes the SAFE Banking Act. The House has already passed the bill and it is being negotiated at the Senate level. According to Bloomberg, there is a very good chance the cannabis provisions survive the senate negotiations which would be positive for the cannabis industry but a negative catalyst for IIPR.

On another front, the Marijuana Opportunity Reinvestment and Expungement (MORE) act, which would end federal cannabis prohibition, passed in the House Judiciary Committee in November 2019. With an upcoming election, cannabis legalization would be a key topic as brought up by many of the former candidates and Joe Biden.

IIPR Target Price

Given all the aforementioned risks and developments, we believe IIPR is worth $45 (a ~50% discount vs current price) after factoring in a 20% erosion in NOI and assigning a 25% discount to NAV as the public realizes the underlying tenant risks associated with the current business model. Additionally IIPR’s re-rated share price will reflect the reality of the new deal environment implying a cap rate of ~10% at $45 share price.

Risks to Current Investment Thesis

There are some risks to potentially shorting IIPR. Below are some of these risks and the mitigating factors for them.

- Large Acquisition Pipeline

- Pace of acquisition is slowing down and tenant quality is deteriorating. As state level regulation changes with more federal legalization openings, yields will compress as operators have alternative financing sources.

- Scarcity value

- Backlogs of ready to go public names will fill the space (Canadian listed cannabis REITs can provide immense competition for IIPR in terms of capital)

- If the SAFE Act passes, it can provide a pathway for cannabis REITs listing on major US exchanges that will create heavy competition for IIPR

- Attractive lease terms

- These lease terms come at a cost of lower quality tenants. While they may seem attractive, they have opened up IIPR to significant credit risk. More attractive leases would just put tenant in worse cash positions

- IIPR is last resort and other financing opportunities will further pressure yields

- Quality tenants

- Many tenants are being poached by competitors and the quality of IIPR’s portfolio is deteriorating (ex. Dionymed and its peers). Cash burn levels plus the current COVID pandemic on top of a lack of access to capital makes default for many of these tenants imminent

- Low leverage

- This partly reflects IIPR’s lack of access to low cost capital

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

- Potential second wave of COVID-19 or slower than expected reopening of the economy

- Update on the three rent deferrals (Vertical, Green Peak, and Maitri Genetics) including potential extensions

- Additional rent deferral requests – Likely to be disclosed in quarterly results

- Additional credit default in the cannabis sector, in particular by any of IIPR’s tenants

- Continued trend of transacting with regional operators and/or smaller private MSOs (as we have seen in recent weeks – E.g. Holistic, Kings Garden, Ascend Wellness, etc.)

- Progress on any of the Federal legislation relating to cannabis

- Additional drawdown on the ATM

| show sort by |