| 2017 | 2018 | ||||||

| Price: | 2.32 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 87 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 201 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 320 | EBIT | 87 | 90 | |||

| TEV (in $M): | 520 | TEV/EBIT | 6 | 5.8 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

Description

Internap is a catalyst rich, high risk, small cap data infrastructure company which recently hired a new top tier telecom CEO to turn the business around, streamline operations and potentially sell parts of the company or the entire business. The new CEO is highly incentivized to drive shareholder value, given his 1.5 million share restricted stock grant, given at the time of his hiring is largely dependent on the stock being ~150% higher than when he started.

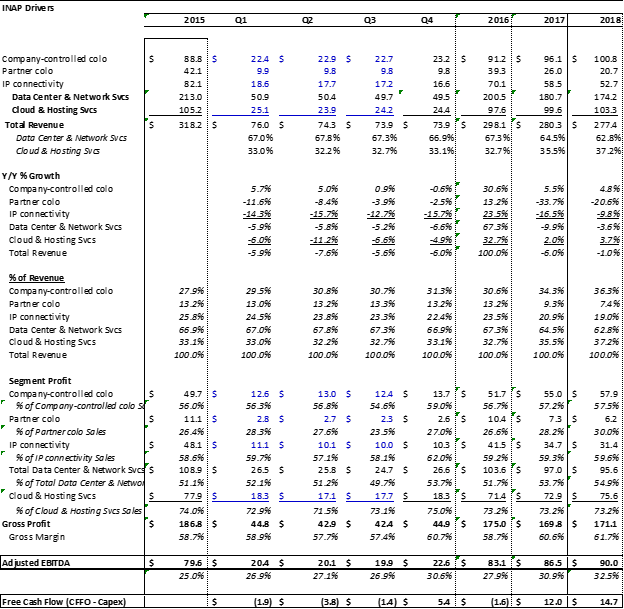

Internap was written up previously by frankie3 in June, 2015. At the time, the company was expected to generate $358 million of revenue and $101 million of EBITDA in 2016. The company, will announce numbers on March 9th (but reiterated their guidance last week), and will actually end 2016 with $298 million of Revenue, and ~$82 million of EBITDA - a ‘miss’ of 17% and 18% respectively. A lot has transpired since the idea was originally written up - with the stock trading then at $8.93, and now currently trading at $2.30.

Internap is a data infrastructure company, that combines a colocation business (company controlled and partner (effectively a reseller), an IP connectivity business as well as a Cloud and Managed Hosting business. Over the past several years, the company has refocused the business on company controlled colocation, as well as hosting and cloud, while deemphasizing IP connectivity and partner controlled colocation. THis has had the effect of driving up margins substantially, while also going through a large capex cycle in 2014 and 2015. While margins have been the bright spot, the company has struggled to execute in driving sales and top line growth. 2015 was largely a disappointment, and led the company to announce it was reviewing strategic alternatives for the business. The process dragged on, and during the Q4 2015 call in February, 2016, announced what was largely expected, the strategic review did not end with a transaction. The company commented at the time that while they received a wide range of financial and strategic parties to ascertain interest in a transaction, none of these turned into anything ‘due to a variety of factors, including the inability to obtain financing and volatility of the credit markets’. The Board determined that it would cut costs, reorganize the business into two ‘integrated’ business units - Data Center and Network Services, and Cloud and Hosting Services with the view that this could open up additional strategic options in the future.

2016 didn’t fare much better for the company, with the company reducing guidance 3x during the year. A combination of large churn events in its data center business from companies that were acquired by ‘large social media companies’ spike churn, and caused a contraction in the top line. On top of that, the continued decline in IP pricing and contract renewals hurt the IP business, while partner colocation continued to attrit. In September, the company announced another leadership change - the prior CEO Michael Ruffolo was a board member who stepped into the seat in 2015, was removed and replaced by Peter Aquino - a seasoned, experienced telecom industry veteran. We have been invested with Aquino in the past when he was the CEO of RCN (cable overbuilder) - which he brought out of bankruptcy in 2004 and sold to Abry Partners for $1.2 bn in 2010. He then moved to a more troubled asset, Primus Telecom, where he struggled to turn the business around, but ended up selling it in pieces, the largest of which was to York Capital.

INAP stock performance

The Opportunity

This is where the story becomes interesting. On his first earnings call - Q3, 2016 in November, Aquino explained his vision for the business, effectively laying out multiple catalysts that should transpire over the course of the year.

-

Reorganize the business into 2 pure-play business units colo and cloud - as opposed to 2 integrated business units. Separate the sales force and focus directly on the market opportunity, instead of selling through a hybrid organization

-

Attack low hanging fruit of cost cuts, while improving profitability. Initially identified $5-$10 million in OpEx run rate cost savings going into 2017.

-

Additional cost cutting to come: “We talked about $5-$10 million run rate savings, and I mean that’s after six weeks of looking. I didn’t find it all myself, the team here is all over it and they offered right away. And you’ll hear more about that through the reorganization announcements that come out down the pike”

-

Initial cost cuts targeted in administration space, some contracts that were unprofitable, and looking at partner colocation facilities

-

Company announced on December 20th, that it had already achieved of these cost cuts. In the press release, the company also laid out initial 2017 guidance, which showed a material decline in sales, but an increase in EBITDA

-

Recapitalize the balance sheet

-

After Q3 - the company’s leverage sat at 4.3x Net Debt/EBITDA, with a term loan making up the majority of the debt - with a 7% cost of capital

-

On February 22, the company announced that it raised $43 million of common equity in a private placement with Gabelli and Avenir Corp. - 2 existing shareholders that now collectively hold 30% of shares, and paid for the stock with no discount and with no warrants

-

Leverage post equity raise should be around 3.8x

-

The cash is being used to pay down the term loan, which will allow them to meet conditions under credit agreement waivers, that allow them to eases restrictions on interest coverage ratio and leverage coverage ratio covenants

-

Next up - The company is looking to complete a debt refinancing, lower the cost of capital and allow for greater flexibility around strategic alternatives

-

No debt is due near term, with the revolver is due in Nov. 2018 and the Term Loan in 2019

-

The company received waivers in late January to increase their ability to monetize non-core assets, raise equity and pay down the term loan.

-

Deemphasize Partner colocation

-

35 partner colo facilities that need to be ‘addressed’. This business has in aggregate ~25% segment profit - but certain assets are under water, while others generate significantly higher margins than that due to higher occupancy. The company is looking to cancel leases, sublet, or create some exit from unprofitable data center contracts.

-

“All else equal, we may end up with slightly less overall revenue, but be more profitable” - comment on Q3 call

-

The preliminary 2017 guidance looks for a 6% decline in sales - we assume/expect that this is from exiting certain partner colo contracts, and losing the negative margin revenue that is tied to that

-

Sell non-core assets

-

The company in the past has pointed to non-core assets that are not being recognized by the street - but have been vague in describing them

-

The only one they have pointed to, was a Software company they picked up in a larger Cloud acquisition called Ubersmith, which does <$5 mm in rev.

-

IP business is clearly non-core, generates decent margins but the revenue trajectory is clearly negative. This business could be interesting to a GTT Communications, or other IP reseller

-

Structural separation could lead to broader M&A of pure-play colo and cloud

CEO Compensation

-

The CEO was given 1,585,000 restricted shares, with a base salary of $505k.

-

The day the new CEO was announced, the stock opened at $2.10

-

Of the 1,585,000 shares, 300k have time-based vesting - 100k annually.

-

More interesting - The remaining 1.285 million - are stock price dependent - with $5 as the lowest stock-price target allowing for vesting.

-

700k shares are only stock price dependent

-

200k vest @ $5

-

250k vest @ 7.50

-

250k vest @ $10

-

585k are hybrid time/price

-

350k of those require a $5 stock price

-

235k of those require a $7.50 stock price

-

The options only see vesting acceleration from M&A for the time-based stock,

-

The CEO effectively took the role, knowing he won’t get paid out unless the stock is up ~150% from when he took the job.

Company Description

Colocation

-

The company’s colocation business utilizes 15 company controlled data ctrs, as well as 35 partner data centers, where the company effectively resells colocation capacity. While the company controlled data center business has 60% segment operating margins, with significant operating leverage as they get leased up, the 35 partner data centers have ~25% segment margins, with some data centers losing money.

-

The company controlled data centers are in North America, while the company operates its partner sites in NA, Europe and APAC.

-

As mentioned above, the company is reviewing the entire portfolio, and evaluating how to exit the unprofitable businesses.

-

On the Q3 call, they tried to quantify the amount of data centers that could be evaluated. “I don’t really want to give you a number. But it’s not half. But its’ a handful certainly that passed the test right away. The rest we have to do some analysis because it might be an area or market we want to keep and just got to hold it up a little bit better. And it could be a sales issue. So we haven’t really finalized the list, but it’s not a huge number. But it’s got some beef there and we’ll focus on it.”

-

Overall occupancy of the data center assets is low at 55%, leaving substantial room for continued lease-up with limited capex.

IP Connectivity

-

The IP connectivity business effectively resells bandwidth, with a patented software layer that improves the routing of traffic, thereby improving the reliability and latency of IP transit. The company gives the example of improving latency for Ad-Tech platforms by 40-50 milliseconds relative to those that do not use their services. While renewals are high, IP pricing is dropping in excess of 15% per year, which is flowing directly down the top line. The silver lining of this, is that they can also continue to reduce their costs, so while revenues and GM dollars are declining, margins have been stable to up.

-

The IP transit business is non-core to the company. One of the pushbacks historically is that it would be difficult to separate the IP business from the data center business, due to the fact that 95% of data center customers take the IP connectivity product.

-

Aquino addressed this during the Q3 call - and it seems like separation may be a focus.

-

“I think when you sell colo, just in general, a lot of folks are selling connectivity with it and IP with it. The idea that it’s not separable is a somewhat contractual nature as you approach the market. But I think if we do it with our eyes open going forward and I’ve talked to our guys about this, I think there’ll be ways to not make that a constraint”

Cloud & Managed Hosting

-

The company entered the cloud and managed hosting market through 2 acquisitions - Voxel for $30 million in January, 2012 and iWeb for $145 million in October, 2013. While Voxel gave the company an enterprise cloud and managed hosting offering, iWeb is focused on the SMB market, and has over 10,000 customers.

-

Cloud services involve providing compute and storage services via an integrated platform that includes servers, storage and network. The cloud platform is built on top of the Performance IP service, OpenStack and within high power density data centers. Cloud services are delivered in eight locations across North America, Europe and the Asia-Pacific region.

-

Key verticals utilize the high density, low latency and high performance offering - and include Gaming, media, healthtech and adtech.

-

iWeb is sold through online portal

-

Offer cloud in 3 NA data centers - NY, Santa Clara and Dallas. WIll be implemented in Montreal as well

-

50 sales people w 20 sales enginners

-

channel arrangements - 100 or so

-

iWeb- doing ecommerce - for bare-metal server products

-

Managed hosting offering provides a single tenant infrastructure environment consisting of servers, storage and network. This is generally offered as an enterprise-class technology to support complex application and compliance requirements for customers. Managed hosting is delivered in 11 locations across North America, Europe and the Asia-Pacific region.

Q4 and 2017 Expectations

The company announced in December preliminary 2017 guidance, and then reiterated after the equity raise in February. While top line is expected to contract 6%, EBITDA margins are expected to expand by 300 bps, and EBITDA $s are expected to grow 5%. The company during the Q3 call, commented that the large churn events experienced in late 2015 and 2016 they did not forsee again happening. Churn should return to more normalized levels in 2017, which are +-3% on the cloud/hosting segment and ~1.5% in the DCNS business. Obviously, anything is possible, but there is nothing coming out of the current pipeline. While we don’t have any color around the guidance, we know that it includes the $5-$10 mm of cost cuts already announced, however the company did comment that it was reinvesting into the salesforce, so not all of the gross savings would be realized.

In order to get to a 6% decline in the topline, and barring additional large churn events (~40% of churn in 2016 related to customers being acquired), one needs to make aggressive assumptions on the declines in the partner colo business to get to their guidance - which would also explain much of the expected margin expansion. I have forecasted in excess of 30% declines in the partner colocation business, with continued double digit declines in IP connectivity, offset by tepid growth in cloud and company controlled colo. Margins in company controlled colo, as well as partner colo should be buoyed by continued lease-up and scale benefits, combined with the exit of unprofitable data centers.

While I have not forecasted any additional savings, I would expect the company will identify additional areas to cut costs over the course of the year. Continued mix shift to the growing cloud and company controlled colo business, and away from the partner colo and IP business will also help margins.

Forecasts

Valuation

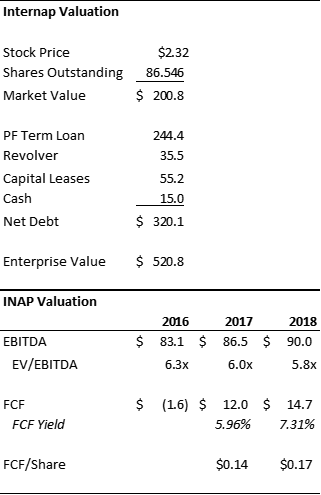

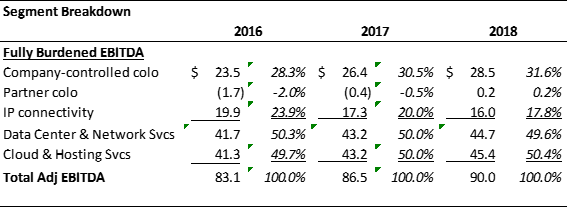

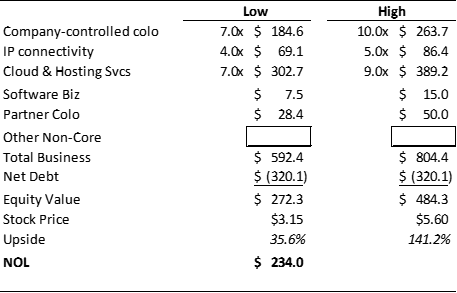

Given the disparate business units, we look at valuation on a Sum of the Parts Direct basis, fully allocating Direct Support as well as the much larger SG&A number across all business units. In an M&A scenario, this is overly punitive given that most of the overhead is likely redundant and given the fact that INAP is a subscale infrastructure asset.

-

Evaluated the 3 positive fully burdened EBITDA businesses on a range of EV/EBITDA multiples.

-

Took the NPV value of the runoff value of the gross profit attributable to the Partner Colo business.

-

Other non core assets - for the ‘rapidly growing’ Ubersmith business - took a conservative SaaS sales multiple of 2.5x

-

Added no value for the $234 million NOL as of 12/31/2015 that could have value. Net Income through Q3 2016 was -$91 million - the NOL value does not include that.

Catalysts

-

This is a catalyst rich story, with a significant amount of risk. Visibility into the operations is limited, and significant churn events can pop up at any time and derail the company.

-

That being said, the revenue guidance for 2017 seems conservative, and beatable with additional cost cuts coming down the line

-

While I hoped to get this write-up done before any financing - the company already did the equity financing, and the stock jumped 20%. The stock is now just above where it was when Aquino took over the CEO role.

-

Debt refinancing still to come

-

Sale of non-core assets, exit of IP business

-

Quarter to be announced on 3/9 - should have interesting color on progress of finding additional cost cuts as well as other strategic alternatives

-

CEO is heavily incentivized to get the stock above the high end of my valuation

-

Improving optics in data center and cloud results as lap the large churn events in 2015/6.

-

Improving financial disclosure, and clarity into underlying business drivers

-

Ramping FCF - as capex falls, interest costs are reduced. Will not have any cash taxes in the foreseeable future.

-

Other potential strategic alternatives (sale once biz is cleaned up?)?

Risks

-

Difficulty in modeling with accuracy underlying business trends

-

Potential for large churn events, like those seen in prior years

-

Inability to sell non-core businesses, or structurally separate IP business

-

Difficulty in differentiating cloud business, price compression as well competition from mega-cap companies

-

Declines in managed hosting business

-

Difficulty in refinancing debt with improved interest rates or additional flexibility

-

Salesforce upheaval has some are moved to cloud, while others to colo

- Inability to cut co

I and/or others I advise do not hold a material investment in the issuer's securities.

Catalyst

-

Low bar for 2017 results already set

-

Debt refinancing still to come

-

Sale of non-core assets, exit of IP business

-

Quarter to be announced on 3/9 - should have interesting color on progress of finding additional cost cuts as well as other strategic alternatives

-

CEO is heavily incentivized to get the stock above the high end of my valuation

-

Improving optics in data center and cloud results as lap the large churn events in 2015/6.

-

Improving financial disclosure, and clarity into underlying business drivers

-

Ramping FCF - as capex falls, interest costs are reduced. Will not have any cash taxes in the foreseeable future.

-

Other potential strategic alternatives (sale once biz is cleaned up?)?

| show sort by |