| 2020 | 2021 | ||||||

| Price: | 34.70 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 345 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 11,970 | P/FCF | 9.2 | 0 | |||

| Net Debt (in $M): | 540 | EBIT | 0 | 0 | |||

| TEV (in $M): | 12,510 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- LIBERTY MEDIA SIRIUSXM GROUP LSXMK 07/10/2019

- LIBERTY MEDIA SIRIUSXM GROUP LSXMK 03/17/2017

- LIBERTY MEDIA SIRIUSXM GROUP LSXMK 07/17/2016

- BETA

- LIBERTY MEDIA SIRIUSXM GROUP LSXMA 05/11/2021

- SOFTBANK GROUP CORP SFTBY 08/26/2021

- Liberty University FLAMES 5.1 03/01/2042 Cor 09/16/2020

- LIBERTY MEDIA SIRIUSXM GROUP LSXMA 06/14/2019

- LIBERTY MEDIA CORP LMCA 01/08/2014

- SIRIUS XM HOLDINGS INC SIRI S 04/25/2017

Description

This was written by an electrical engineer who purports to understand the thinking of another. Electrical engineers are analytical minds seeking the highest signal-to-noise-ratio “SNR” for e.g. cable technologies such as DOCSIS 3.0 etc.

In the particular case of Cable Cowboy, he’s familiar with the investing equivalent as well, i.e. the reward-to-risk ratio “RRR” (remember finance professors rolling that off the tongue? right). Electrical engineers take this idea very seriously, which is why a certain finance insider crowd has a term for them “The Outsiders” (let us remember Dr. Singleton as well).

Dr. Malone has his sights on an attractive high SNR situation at Liberty Sirius (LSXM), which also happens to be his largest investment by absolute value after Charter.

From Barron's (GLIBA and LBRDK merge and both ~represent the Charter stake):

In this story, Liberty Sirius’ (LSXM) current 37% NAV discount is high signal, and its underlying value Sirius XM (SIRI) is low noise (stable, high customer lifetime subscriptions).

This wouldn’t be VIC if large buybacks at LSXM were already in place. Good: taxes stand in the way of cable cowboy freeing cash flow for buybacks (taxes’ certain loss of alpha has an RRR of #DIV/0! Error. No go zone.).

Luckily, cable cowboy is at work unlocking the “tax catalyst” by 2021.

Overview

Liberty SiriusXM (share classes with 1, 10 and 0 voting rights: LSXMA, LSXMB, LSXMK) is a tracking stock mainly tracking Liberty’s 73% stake in SiriusXM (SIRI). LSXM was issued by Liberty Media as part of a broader issue of trackers for its Formula One interest (FWONA) and the Atlanta Braves (BATRA).

LSXM background has been covered a few times here in its relatively short existence (2016). The current opportunity was created by a recent rights offering which was unpopular with many shareholders (though BRK, CEO and Malone participated in full; full disclosure: Malone took some money off the table later, perhaps to participate in LILAK rights offering). The offering money was used to inject cash at FWONA in exchange for its Live Nation (LYV) stake (along with a debt transfer and call spread).

I believe for those who are willing to look forward - not backward - the new situation seems interesting to me. I believe the underlying NAV is relatively stable, and an outsized ~58% event-driven return can be had in 12-24 months at the LSXM level.

A tax catalyst will either force LSXMK NAV discount to +- disappear in 18 months, and/or very accretive share buyback fireworks will start at the LSXMK level (only <$1B LSXM repurchases since ‘16 inception, as the holdco has no access to cash flow, yet).

With the discount at 37% and the combination of discount closing and/or share buybacks accretion, the rough math is a cool 58% return on top of any return from SIRI (this is simply the return to 100% of NAV; SIRI borrow is plenty & cheap).

How it will work:

- LSXM’s stake reaches 80%, i.e. tax consolidation in H2 ‘21

- SIRI starts dividending out most of SIRI’s FCF (as these are now tax free) to LSXM (as opposed to SIRI buybacks in the past)

- LSXM now has access to SIRI’s tax-free cash flow and starts buying back boatloads of shares at the LSXM level, as much as 14% of share capital (as long as LSXM’s NAV discount persists)

Why it will work:

-

For John Malone, PhD, an electrical engineer, capital allocation and numbers are core business (intrinsic value, NAV discounts, taxes, a preference of opportunistic and aggressive buybacks over dividends. If you’re not familiar with this Outsider archetype, you might want to join the herd in reading The Outsiders book). This is why Liberty Media’s earnings calls and slides always start with discussions about NAV discounts and buybacks (see investor days in the last 3 years)

-

Management has openly said it will use all cash it reasonably can (hence much more as from SIRI tax consolidation) to buyback LSXM if the current discount persists

-

To this end, management has said its capital allocation priority at SIRI is to buyback as much as possible to reach tax consolidation as soon as possible

-

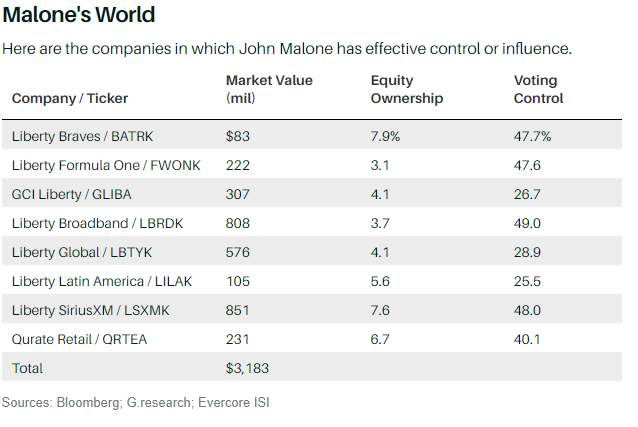

LSXM is among Malone’s biggest Liberty holdings in absolute value (after Charter if we combine GCI and Liberty Broadband)

-

Out of the three Liberty Media trackers, Malone highest ownership percentage is in LSXM. This means Malone is (at least financially) incentivized to avoid any re-attributions unfavourable to LSXM

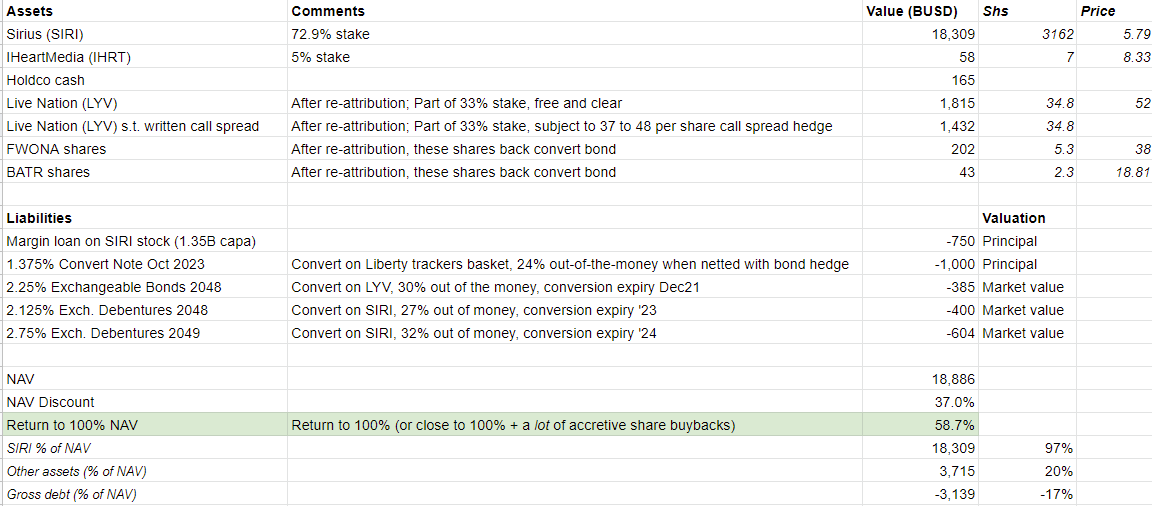

SOTP

The SOTP seems complex but is in essence quite simple. Roughly 100% of NAV is covered by SIRI stock. Another ~18% of NAV is debt, fully offset by the LYV stake. Should we concern ourselves much with the future value of LYV? We argue no, as half of the shares are burdened with an in-the-money written call spread. The negative value from this call spread is already deducted in our SOTP, which means that from this point of view, the call spread currently acts as downside protection for the LYV nation stock price drop between -6% and -28%. This means only ~10% of NAV representing debt fully offset by unburdened SIRI shares are truly risky.

Debt is mostly long-term with a low fixed rate (convertible but significantly out-of-the-money).

Note: look-through "unlevered" FCF yield of almost 11% if we ignore the debt that is ~fully offset by the LYV nation stake

Background

The underlying subscription radio company SIRI has been repurchasing its shares significantly faster than its FCF over the years (~1.7B p.a.), by holding the leverage ratio constant at 3X EBITDA on its growing business. The result is a 33% decrease of shares outstanding since ‘13 when Liberty took control and instituted aggressive buybacks. This is how Liberty’s stake in SIRI grew fast to ~73% today. SIRI’s dividend yield is only 1% as Liberty hates paying dividend taxes. Liberty Sirius has little access to cash flow. For now.

The current NAV discount (at 37%) is in the ~90th percentile of highest NAV discount since existence while a catalyst is sooner than ever. This seems to be caused by:

-

illiquidity discounts for holdco’s, which tend to blow up in the wake of general market dislocation

-

the recent re-attribution of the 33% Live Nation stake from Liberty Formula One (FWONA) to LSXM in exchange for a rescue shifting some liquidity and debt. This clearly was an emergency measure in favor of FWONA. It entailed opportunity cost for LSXM shareholders (buying LYV at market price) and it degraded LSXM’s “pure play” status as an investment in SIRI to a conglomerate with a discount

-

extra “contamination” risk assumed in a tracking stock as opposed to common stock

I argue these arguments are backward looking, while a forward look suggests the 180° opposite.

On the last point: tracking stock owners bear the extra risk of peer tracking stocks in the parent company “contaminating” its subset of assets meant to be tracked, as peer tracker debt holders have equal claim to all assets of the parent company in bankruptcy. The re-attribution has greatly diminished this worry here: FWONA’s holdco debt load was lowered from $2B to $0.7B. We’ll expand on the debt situation at FWONA later. Liberty Media’s management agrees with us on this:

-

“We also believe that there has been a more recent overhang on the LSXM equity at fear that we may take action to support the -- some stocks, particularly collapsing the trackers. We hope this [rights offering] eliminates that risk. With this reattribution, we strengthened both tracking stocks for the long term, as I mentioned, and removed this risk.” - Greg Maffei on the April transaction call

As for point two “conglomerate”, management had previously commented on various occasions that LYV fits better under LSXM as both are music assets. But it was really because of the unprecedented CV-19 crisis leading to a suspension of F1 races and hence income, which led to a covenant breach and a problematic looming debt maturity. As noted, Malone’s percentage ownership in LSXM is higher versus FWONA, and I believe this is the reason why management prudently chose for LSXM to buy the 33% stake in LYV from distressed FWONA simply at market price, and not lower.

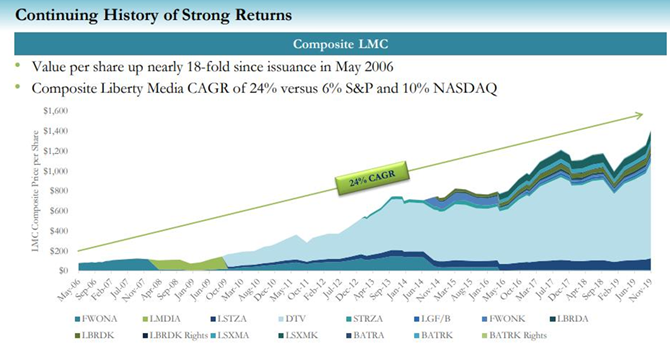

We do not buy the argument that LSXM will evolve into something more complex in the future however, i.e. a conglomerate. In fact, the complete opposite has been true for the Liberty complex as a whole. Simply look at the many splits which Liberty has pushed for to highlight the value of individual stakes. This has camouflaged investor CAGR:

While it’s not a relevant part in the steps to get the 58% return (see “how it works”), one simplification option is a reverse-morris trust (RMT) for the LYV stake. An RMT requires LSXM to invest more to get to a majority stake, and management has commented its priority - for now - lies in accretive repurchases instead to get to our catalyst asap. Another option is to make a proper tracker stock out of the LYV stake (this seems plausible as the Liberty Braves represent a smaller market value for example).

Lastly, the illiquidity discount point isn’t forward looking either: while liquidity has been better in SIRI (more than double), this will change as the SIRI free float is shrinking quickly. In 2009, LSXM owned 40% of SIRI. Today this is 73% and going up, solely because of the almost $2B annual SIRI buyback.

Tax catalyst

We have the holdco LSXM trading at 37% discount to NAV, while historically this has been ~15-25%. So what?

Why hasn’t LSXM - instead of SIRI - done a buyback then? It has done so, but in much smaller size than SIRI, using some margin loan debt. But unlike the cash cow that SIRI is, LSXM does not have access to any operational cash flow for buybacks. It takes a SIRI dividend for LSXM to get access to its cash.

If we simply extrapolate SIRI’s stable (after M&A) buyback policy we find LSXM’s stake growing beyond the 80% ownership threshold (US tax consolidation) by Septf-Dec ‘21.

In other words, if by YE2021 the NAV discount is still above low teens, expect huge tax free dividends from SIRI to flow to LSXM, and a lot of accretive buybacks at the LSXM level.

In fact SIRI has grown free cash flow over the years and kept a constant ~3.0X EBITDA leverage ratio, allowing it to do buybacks at ~120% of FCFE. If the budget for SIRI buybacks was instead used for dividends, LSXM would receive enough to repurchase a staggering 12-14% of LSXM’s shares outstanding at the current share price.

This number moves the needle and means that even if the NAV discount would not revert to low teens within 12-18 months, IRR would be lower but total investor return over a longer period would be more impressive through more (and more accretive) buybacks in total.

Management has mentioned this intention on multiple calls (the capital allocation priority at SIRI to get LSXM to 80% ownership, the intention to make money with the NAV discount by flipping the SIRI capital allocation policy from buybacks into dividends and using the cash to buy back at LSXM level).

So while LSXM is as close as ever to SIRI tax consolidation, it has never traded at a larger NAV discount than today (except for the COVID scare).

Although I do not recall in which call, I remember Malone thinking aloud how he might “optimally” buyback shares of a security, using verbs as “scaling into”. I believe it is possible Malone decides to take on some incremental debt at LSXM to repurchase LSXM shares one or two quarters before the tax consolidation (at the best NAV discount) in anticipation of cash dividends getting close.

Why future debt contamination between trackers is unlikely

The main question to be answered is: is it likely FWONA will need another liquidity injection? And in that event, is it likely another re-attribution is needed with LSXM?

The answers are both no.

The liquidity injection in May was needed because there was a $1B upcoming maturity and a covenant was breached as income fell to zero (no races). Both issues have been solved.

-

~Zero cash burn: Formula 1 has almost zero fixed cost and hence burns ~zero cash with zero races (despite revenue falling off a cliff to zero, H1 OIBDA was at -$48M, and note UFCF ~95% OIBDA).

-

Biggest cost is completely variable with revenue: team prizes (50% of revenue, fully variable).

-

Races (net FCF positive) have restarted since July

-

Plenty of liquidity (>$2B) dwarfing a few hundred million of ’22 and ’23 debt maturities, major maturity is in June 2024

-

After the re-attribution, FWONA negotiated debt covenant at 8.25X EBITDA to be suspended until Q2 2022

-

using pre-COVID 2019 revenue, this ratio would be around 5X today, but including recent re-attribution liquidity ~2X net debt

Formula One requires no capex, 95% of EBITDA converts into UFCF. Average interest costs of opco & holdco debt are low, together ~2.5%.

If in some remote scenario cash need should arise, help from SiriusXM will probably not be needed, nor defendable:

-

Not needed: FWONA has an impressive equity valuation today at 30X levered pre-CV19 free cash flow, net consolidated debt is at only 15% of enterprise value. A rights offering of its own would probably be possible.

-

Not defendable: F1 has no more non-core stakes that fit for Liberty SiriusXM (previously Live Nation that was transferred to Liberty SiriusXM). Note that management did not transfer some small stakes FWONA owns in AT&T, Viacom, Liberty Braves to Liberty Sirius in the May re-attribution. They were asked why and said these stakes simply do not fit at Liberty Sirius (not defendable for Liberty Sirius investors)

Long-short structuring

I am relatively agnostic about SIRI. I do not believe the results (of late quite good, churn down) will change for the worse quickly (vs thesis timeline). 25IQ had a nice post about SIRI. I shorted out SIRI for only 30% of my LSXMK dollar long exposure. This combination allows me to have a somewhat larger position in LSXM, while at the same time greatly mitigating worries about being stopped out of the short for whatever reason (discount blowing up, melt-up in both names etc).

Counterarguments to the thesis

The main counterarguments centre around "NAV discount is a mirage":

- SIRI stock price is inflated because it is plowing FCF into buybacks (pushback: buyback speed is less than 10% of daily volume)

- LSXM discount is a reflection of the takeout premium Liberty will have to pay in a future squeeze-out of SIRI minorities (pushback: don't see how that math works at 37% discount for 100% of LSXM when the real premium that could be paid - if any, if LSXM and SIRI won't be merged at price parity - for the remaining ~10% shareholders of SIRI)

Happy to hear any pushback or questions!

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

- (1) SIRI buyback continues; (2) LSXM reaches 80% ownership (US tax consolidation) in H2 '21; (3) SIRI cap allocation policy flips from buybacks into (tax free) dividends; (4) LSXM uses tax free dividends to buyback a lot of shares if the 37% NAV discount persists

- blue sky scenario: LSXM starts repurchasing in anticipation of the tax consolidation (e.g. H1 '21) - using incremental holdco debt that is subsequently repaid from SIRI dividends after US tax consolidation

| show sort by |