| 2016 | 2017 | ||||||

| Price: | 10.38 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 5 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 61 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 50 | EBIT | 0 | 0 | |||

| TEV (in $M): | 111 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- Holding Company

- Special Purpose Acquisition Company (SPAC)

- None found

- BETA

- STARBOARD VAL ACQ CORP SVAC 04/24/2021

- DIGITAL MEDIA SOLUTIONS INC DMS.WS 11/22/2022

- ITASCA CAPITAL LTD ICL. 01/22/2017

- EAST RESOURCES ACQUISITION COMPANY ERESW 04/16/2022

- CHURCHILL CAP CORP II CCX.WS 04/24/2021

- PERSHING SQ TN HOL LTD PSTH.U 09/03/2020

- POLISHED.COM INC POL.WS 03/21/2023

- API GROUP CORP APG 06/24/2021

Description

Note: unfortunately Craig Hallum came out with coverage on Limbach this morning with a $17 price target, causing the underlying to trade up 6% and the warrants to pop 17% as of this writing. In light of this, I've decided to post a condensed version of our write-up now, rather than risk another big run up over the next few days while I race to edit the 30 plus pages of qualitative analysis tthat we've put together on this extremely interesting name. In lieu of this, we recommend reading through both the company's presentation decks here and here), as well as Dane Capitals solid write-ups over at SA (here and here) for a more detailed analysis of the the business and current set up.

At any rate, apologies ahead of time for the lack of completeness here, as it was either post an incomplete write up or not at all. We chose the former. Moreover, as frustrating as this mornings run is, keep in mind that the warrants still possess substantial near and long-term upside, with returns approaching several hundred percent over the next 12 to 24 months.

As always we're happy to discuss any and all factors not addressed below in the comments section, so please don't hesitate to ask should any questions and concerns come up.

LMBHW VIC Thesis

We believe an investment in the warrants of Limbach Holdings, Inc. (LMBH), which are exchange-traded under the ticker LMBHW, present a compelling investment opportunity at 99c.

Specifically, we have a twin thesis that:

1. The warrants are mispriced due to SPAC trading dynamics that cause historical volatility to be understated relative to future volatility, creating a “kink” in the Black-Scholes model that we believe will be market-corrected over the next few months; and

2. The warrants are further undervalued as we believe the underlying shares of LMBH represent a compelling fundamental investment opportunity and LMBHW is an attractive leveraged play on this security.

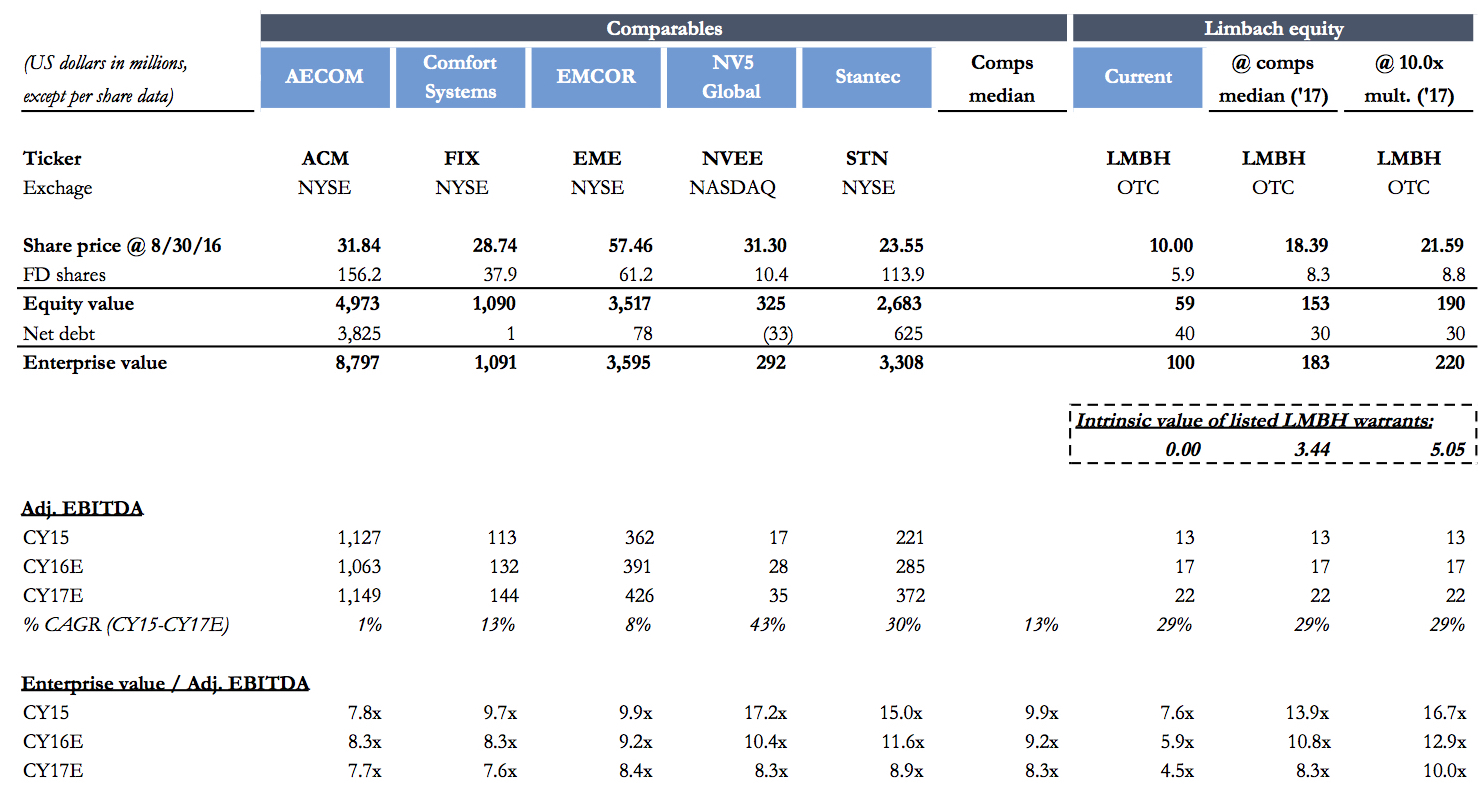

In our view, a correction of the technical arbitrage opportunity results in upside of 40-100% to fair value. In addition, we think that as the company (i) up-lists from the OTC to the NASDAQ, (ii) presents at investor conferences for the first time, (iii) receives sell-side coverage for the first time, and (iv) generally becomes better-known in the investment community, a stock that currently trades at 5x 2017 EV/EBITDA will re-rate closer to its peers that trade at 9-10x EV/EBITDA.

In sum, we believe the combination of a technical arbitrage thesis and a directional fundamental thesis create a unique and compelling risk/reward with potential upside to $3-5 per warrant should LMBH trade in-line with its peers.

Introduction

Over the last few years, one area of the market that has become particularly hated and neglected are SPAC's, blank check companies that short-circuit the IPO process by acquiring a private company via a public shell. Though some SPAC's have done well, most have not, leaving a trail of wary investors in their wake.

We see this as an opportunity. Successful post-deal SPAC's tend to share certain characteristics: they generate substantial cash flow, possess strong, incentivized management teams with skin in the game, and tend to operate unsexy businesses with little or no hype (i.e. – because they were not “hot” issues, the shares were never bid up beyond fair value). Moreover, it seems the combination of these traits with a peculiar structure and general investor aversion to SPAC’s writ large, can create attractive opportunities for discerning value investor that knows how to pick his/her spots.

All of which is to say that if your able to overcome the conventional bias against investing in SPAC’s, and you’ve got a great search strategy in place, we think one can do extremely well if they are willing to wait for the right opportunity. The key, as always, is to choose wisely.

We believe we have found one such attractive situation with the warrants of Limbach Holdings (LMBH). The company is an unsexy, asset-light engineering and construction services business run by a high-quality and motivated CEO. Better yet, the company's shares trade at less than 5x 2017 EV/EBITDA vs. peers at 9-10x as the company has no sell-side coverage (yet), has little recognition in the investment community (yet), and does not trade on the NASDAQ (yet). All of these factors are set to change in a matter of weeks.

The Arbitrage Opportunity

SPACs tend to receive their initial funding from merger arbitrage funds. These funds provide capital at $10 per unit, for which they generally receive two securities: one common share of stock and one warrant (either for half or a full share, usually with an $11.50 strike). Upon the announcement of a deal, these arbitrage funds can redeem their common shares for $10 in cash and sell their warrants for a profit. With a bit of leverage, investing in SPACs can make for an attractive arbitrage opportunity.

In order to complete the deal, the SPAC must find new investors to take the place of the arbitrage shareholders by acquiring the arbs’ common shares, usually at $10 apiece. In the case of LMBH, for example, the SPAC needed $18M of capital from common share ownership to replace the arbitrage funds, a figure successfully achieved in July 2016.

Following the announcement, and then completion, of the deal, ownership of the warrants turns over almost entirely as the arbs sell their positions at a profit and move on to the next deal. This “non-fundamental selling” provides fundamental investors with an opportunity to purchase warrants at depressed levels from forced sellers.

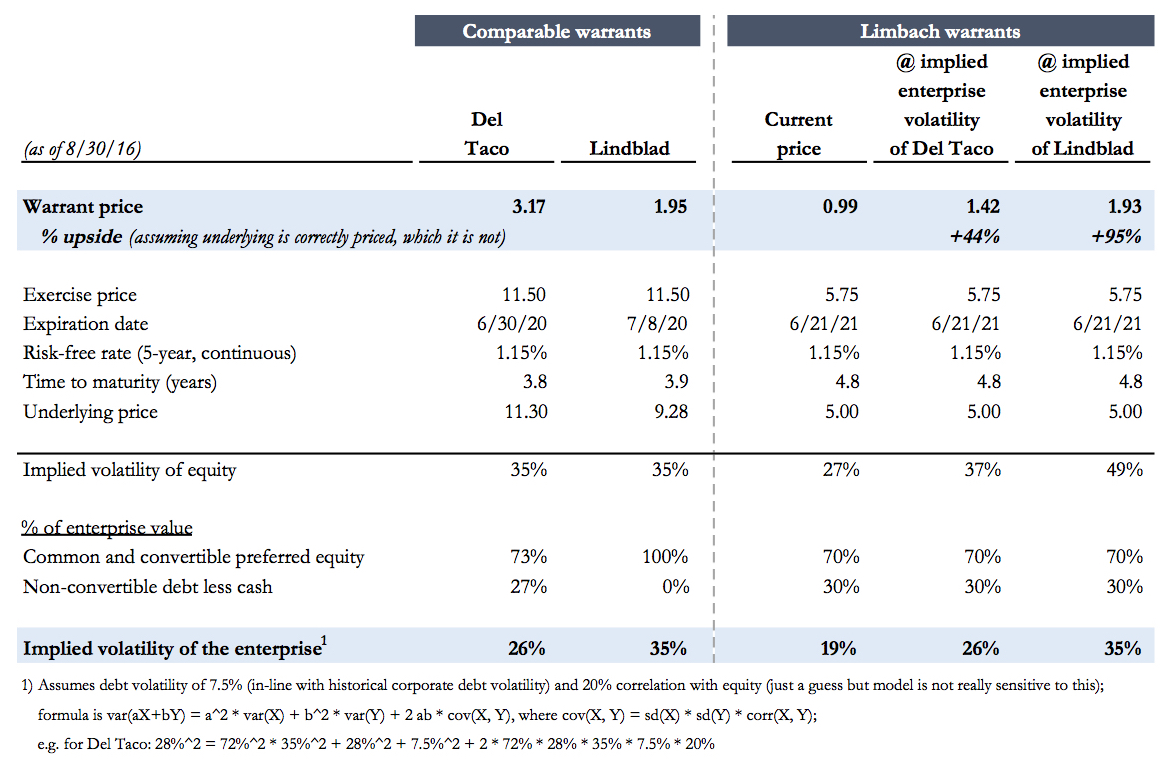

Moreover, the opportunity is doubly-interesting due to the mechanism of using the Black-Scholes model to calculate option values. A key input in the model is volatility, specifically the implied volatility of the underlying security. The implied volatility, a forecast of volatility in the future, is often closely connected to the security’s historical volatility – a low historical volatility goes hand-in-hand with a low implied volatility, and vice-versa. With SPACs, however, historical volatility is often extremely low as the underlying shares usually hover just below the $10 per share listing price within a very tight trading band; only after the deal completes does normal volatility arrive for the shares. Thus, for several months after the completion of a SPAC deal, historical 90-day trailing volatility is far lower than what go-forward volatility will be. As the shares trade post-deal, historical volatility gradually rises to a more appropriate level.

We can see both these dynamics with LMBHW. We are now at an opportune moment where nearly 4M of the 4.6M freely-traded warrants have traded since the beginning of June, so we should be mostly past the “non-fundamental” arb selling. In addition, the shares are trading with significantly more volatility than they have had in the past, and historical volatility is rising (which should lead to a higher valuation for the warrants under Black-Scholes).

Two recent SPAC comps should give us confidence that the warrants are undervalued but are in the process of repricing to fair value. Del Taco (TACO), a recent and fairly comparable SPAC, has warrants outstanding that trade at an implied equity volatility of 36%. This contrasts with Limbach’s 19%. If Limbach’s warrants were to trade at Del Taco’s implied volatility figures, they would be worth ~100% more than where they trade today.

The Up-Listing

Part of the reason LMBH is undervalued is that the shares are not currently listed on NASDAQ. We believe this will be remedied by the end of September.

The lack of a NASDAQ listing is due to the company's failure to meet the NASDAQ's 300 shareholder requirement (to count, a shareholder must own at least 100 shares) immediately following the closure of the deal in June. Our understanding is that the shareholder register reached 230 as of mid-August and has been climbing quickly - in part due to two recent Seeking Alpha write-up of the company here: LINK (highly recommended). Moreover, we believe the count will get an extra boost in the coming weeks as the company attends investor conferences for the first time as a publicly-traded company and receives its first round of analyst coverage.

The truth is that this obscure, grossly mis-priced 100+ year old dominant market leader is simply not well known or understood by investors at this point (at least yet). Actually, its probably more accurate to state that the company is invisible considering the the small, closely held nature of it’s float (insiders collectively own 80%+ of the company, all of which is subject to lock-ups), the fact that the deal just closed in late July, and above all, its current listing on the bulletin boards. But again, all of this is set to change rapidy as the company up-lists from the bulletin boards, sell-side coverage picks up in earnest, and the all around informational black hole currently surrounding this owner operated, high quality “compounder” (and the high end niche of the subcontracting supply chain it dominates) begins to dissipate over the next 30 to 60 days.

Remember too that as long as the stock remains un-investable for the vast majority of institutional investors, prospective investors have a chance to effectively “front-run” a substantial liquidity unlocking event that we expect to unlock material value in the relatively imminent future. So this temporary lull effectively ensures investors can skate where the puck will be so to speak - and then sit back and enjoy themselves while the up-list results in a sharp, upward revaluation in the common and by extension, the warrants.

As an aside, keep in mind that with all the forced selling exhausting itself, the marriage of a tightly held, illiquid float with a nonsensically cheap high quality business experiencing rapidly improving revenue and profitability strikes us a a very volatile combination – exactly the type of “coiled spring” like dynamic where even a modicum of incremental buying pressure could send these securities soaring. Indeed, that’s been our experience since acquiring our stake at roughly 50 cents in late July, but.

The Fundamental Thesis

As already noted, we have a directional thesis that a business with an enterprise value today of roughly $110M will achieve $22M EBITDA in 2017 (and upwards of $50 million at some point within the next 3 to 5 years), causing a fundamental re-rating of the shares and a levered effect on the warrants.

The takeaway is that depending on the extent of the fundamental re-rating - as well as the accuracy of our estimates concerning how the business will evolve at the margin over the next few years (and beyond) – we see a number of relatively conservative scenarios where the warrants could be worth 5-10x the current quote - and without aggressive assumptions as you’ll see below.

For some quick background on the business, we’ll start by noting that we view Limbach as a leading candidate for the “best business that no ones ever heard of” award. Unfortunately, for the sake of getting this out as fast as possible, we’re going to take the lazy way out and simply crib from the original press releases announcing the deal, as they provide some great background on the company, while also providing some insight into the unique attributes of Limbach’s high quality differentiated business model and the long-term opportunity in front of the company. Please see the various deck slides in the appendix for further detail.

We’ll start with Kingsway, who had this to say…

• Full Lifecycle Services. Limbach’s broad portfolio of services addresses the full lifecycle of a facility, from design and engineering to system installation, retrofit, maintenance and energy management. In addition, Limbach has long-term, “cradle-to-grave” relationships with facility owners that drive high margin revenue streams on a recurring basis.

• Strong Growth Outlook. After out-performing its peer group during the recession, Limbach is well-positioned to capitalize on the strength of the recovery in the non-residential construction market. Limbach has an established presence in core healthcare, education, institutional and commercial end-markets providing solid long-term growth prospects.

• Diversified Operating Platform. Limbach’s broad geographic presence provides exposure to more than ten states in five distinct regions of the United States, each with unique economic drivers and regional influences. Limbach does not rely on a limited number of projects and customers across its platform. Limbach’s diversity of contract structures allows it to tailor each project within acceptable levels of risk.

• Experienced Management Team. Limbach’s has a long-tenured management team with considerable experience in construction and facilities services, and has a desire to grow the platform to several times its current size. Limbach’s management team is well recognized throughout its industry for leadership in workforce safety, innovation in fabrication and project delivery methodologies, as well as provided quality building services.

• Significant Competitive Advantages. Limbach has deep customer relationships, a skilled and long-tenured workforce, a unique safety and service culture, and substantial bonding capacity. It is a leader in the utilization of rapidly emerging technologies and design/build services, and has a scalable central services operating platform.

• Attractive Financial Profile. Limbach has a strong and visible backlog, a mix of project and recurring revenue, and a focus on increasing its margin.

• Multiple Growth Drivers. Limbach’s platform is positioned for growth with established and scalable operations and infrastructure applied with a clear strategic direction. Limbach believes cyclical and secular trends drive facility owners and construction managers to comprehensive service providers such as Limbach for the more complex and challenging projects.

Here’s the official release, which adds a fair amount of color.

Limbach Highlights

Founded in 1901, Limbach is the 12th largest mechanical systems solutions firm in the United States as determined by Engineering News Record. Limbach provides building infrastructure services, with an expertise in the design, installation and maintenance of HVAC and mechanical systems for diversified commercial and institutional facility owners, employing over 1,200 employees in 14 offices throughout the United States. The Company’s full life-cycle capabilities, from concept design and engineering through system commissioning and recurring 24/7 service and maintenance, position Limbach as a value-added and essential partner for building owners, construction managers, general contractors and energy service companies (ESCOs).

Through its comprehensive service offering, Limbach is able to partner with its customers to deliver optimized outcomes which reduce the costs of facility construction and ownership, accelerate construction and renovation timelines, and mitigate financial risk.Limbach’s 27 in-house engineers offer state-of-the-art mechanical system technologies and practices, enabling innovative techniques such as Building Information Modeling, Integrated Project Delivery and offsite prefabrication that align the interests of all facility stakeholders and optimize economic returns.

Limbach is led by CEO Charlie Bacon who, since joining the Company in 2004, has taken the Company to an industry-leading position in maintaining safe work environments, developing the next generation of talented industry leaders, and providing an increasingly broad portfolio of value-added mechanical services to the nation’s leading developers and facility owners. At present, Limbach maintains branch locations serving 24 major U.S. markets, including New England, Southern California, the Midwest, Mid-Atlantic, and Florida. This diversified footprint allows the Company to leverage key customer relationships and a deep institutional knowledge base across a broad geography, and through this portfolio approach, serves to mitigate regional economic volatility and building cycles.

Niche Industry Verticals / Blue-Chip Customer Base

Limbach focuses on end-markets and project opportunities that require specialized engineering expertise and differentiated project delivery capabilities, including industry verticals such as healthcare (hospitals); transportation (rail and airports); education (K-12, higher education campuses and research centers); entertainment and hospitality (theme parks, arenas, convention centers and hotels); and general institutional markets (federal and local government offices and facilities). The Company’s blue-chip customer base includes leading construction managers and general contractors such as Barton Malow, DPR, Gilbane Building Company, Hensel Phelps, Skanska and Turner Construction; and property and facility owners such as Disney and Hospital Corporation of America (HCA).

Limbach reinforces its customer relationships across all markets with its rapidly growing maintenance and service capabilities which create a high-margin, annuity-like stream of recurring revenue with customers such as Amtrak, CBRE, Constellation Energy, Jones Lang LaSalle, Marriott and the University of Pennsylvania.

Financial Results

Limbach has capitalized on the strengthening non-residential construction market, generating 2015 revenues of $331 million, an increase of 12.2% over 2014. The Company’s backlog of committed projects has similarly grown, reaching $343 million at year-end 2015, an increase of 14% over the prior year. Improving market conditions are expected to support continued expansion in both the volume of new project opportunities in the market, and the gross margins available for companies like Limbach with a diversified service offering.

Limbach recorded preliminary earnings of approximately $13 million of Adjusted EBITDA in 2015 and anticipates continued growth in the current calendar year given the strong backlog and a robust pipeline of new opportunities, as well as the continued growth in high-margin service and maintenance opportunities which are not reflected in backlog.

Transaction Rationale

1347 Capital believes that Limbach, an industry leading construction and maintenance services platform, offers an attractive opportunity to participate in the growth of the non-residential construction market which is in the early stages of a cyclical uptrend. Following a post-recession bottom in 2011, the non-residential construction put-in-place has climbed steadily and is forecasted to continue growing for at least the next several years, according to FMI’s 2016 U.S. Markets Construction Overview. Limbach is a compelling platform from which to benefit from this expansion given its long history of financial and operating success, broad and well-established industry relationships, and a sterling reputation that differentiates the Company and positions it as the contractor and maintenance service firm of choice for technically demanding mechanical systems applications.

1347 Capital expects Limbach’s extensive capabilities, leading market position, and strong customer relationships to reinforce its competitive position in the expanding market, and to increase market share, especially in the technically challenging, demanding projects which Limbach specifically targets. By providing Limbach with access to the capital markets, 1347 Capital anticipates that the Company will be able to accelerate its growth plans, both organically and through strategic acquisition of local and regional mechanical, electrical and fire protection contractors who address a compelling geographic and/or service line offering complementary to the Company’s current footprint and capabilities. Limbach believes that it would be an attractive acquirer for such firms given its industry reputation, committed investment in people and technology, and culture of safety and project deliverability.

Management Commentary

1347 Capital’s President and Chief Executive Officer, Mr. Gordon G. Pratt stated, “Limbach has a long and proud history of delivering value for its blue-chip customer base of general contractors and end-users. We believe that this merger will allow the Company to achieve greater scale and leverage its management, engineering, and financial infrastructure, which are very highly evolved for a company of its current size. Limbach stands out both for its engineering/design-build services and its vertically integrated fabrication and assembly capabilities, thus reducing costs, increasing reliability, and speeding construction when compared to standard build-on-site procedures. Limbach’s focus on complex, technically challenging projects in largely institutional end markets such as health care, education, transportation, and hospitality/entertainment, mitigates the cyclicality and price competition inherent in the commodity segments of the construction industry. The management team at Limbach, led by Charlie Bacon, has brought together all the critical elements needed to succeed: depth of industry expertise, long-standing relationships, and a focused, shared understanding of Limbach’s goals and how to achieve them. Operating as a public company is one such goal, and we are proud to be partners with Limbach as the Company makes this transition.”

Mr. Bacon stated, “Becoming a public company is an important milestone in Limbach’s history, and we believe that the timing is right for the Company to leverage the opportunities we see in the marketplace by having access to the capital markets in support of our multi-faceted growth strategy. Non-residential construction markets have recovered from post-recession lows and our deep engineering capabilities are a key differentiator that we do not believe is easily replicated by our competition. Improved access to capital and a robust corporate infrastructure further differentiate Limbach, both in the pursuit of individual project opportunities, and as we explore acquisitions to expand our geographic footprint and to add complementary lines of business. We are pleased to take the next step in the evolution of Limbach, as the capital markets will provide our Company with a wider range of financing options to fund our future growth.”

Management and Board Post-Closing

Following the completion of the transaction, the senior management of Limbach will continue to be led by current Chief Executive Officer Charlie Bacon. Mr. Bacon leads an experienced team that averages 14 years of experience at the company.

The Board of Directors of the combined company will initially consist of seven members, including Mr. Bacon, two Limbach representatives, two 1347 Capital representatives, and two independent members to be appointed upon closing.

Growth Potential / Conclusion

Mr. Bacon concluded, “We believe that post-transaction, Limbach will be well positioned to increase its market share by pursuing several strategic growth paths. Unlike many other contractors in our space, we excel at selling the breadth of our building system capabilities through the efforts and abilities of our design and engineering group. In doing so, we are able to deliver tremendous value for our clients while also generating improved financial performance for Limbach. We see considerable upside from operating in the public markets in 2016 and beyond.”

***

With that, a couple of quick thoughts (in no particular order)…

Our belief is that as the company starts articulating its strategy publicly, and the sell side and other investors begin to see said strategy unfolding (as advertised), shares should substantially re-rate as investors begin to grasp not only the true quality of Limbach’s underlying business, but the sheer magnitude of the multi-faceted value creation runway in front of it.

Morevoer, as alluded to earlier – we don’t believe that a rapidly growing, highly resilient, wide moat business run by a well regarded management team operating in a growing market on the cusp of a cyclical upswing, should ever trade at a valuation implying the opposite – e.g. a commoditized, low return business in terminal decline.

Especially when the business under consideration is characterized by a number of extremely attractive qualitative attributes, including: durable competitive advantages that should widen substantially over the next few years, predictable, highly visible revenue and cash flow – not to mention low fixed costs, supply side network effects, operating leverage, minimal ongoing capital requirements, high/improving ROIC, and the potential to grow at orders of magnitude faster then GDP for the foreseeable future.

And that’s to say nothing of the proven, well regarded management team executing a focused, fundamentally sound growth plan, nor the embedded margin expansion coming down the pipe.

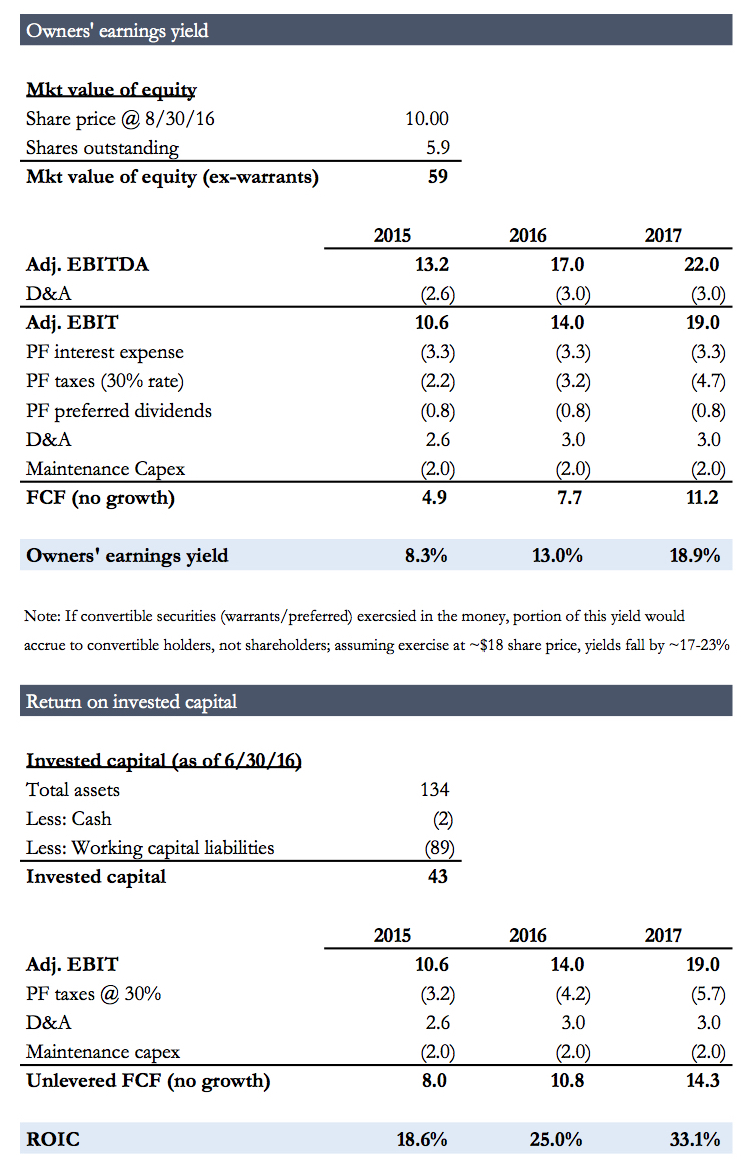

Speaking of margins, keep in mind that historically speaking, Limbach’s mid cycle gross margin was 15 to 16%. This is compared to 13.6% as of last quarter, implying there is a considerable amount of mean reversion still on the come (all things equal).

The thing is, the business is considerably better today relative to where it was the last few cycles, as the company has a much higher proportion of its revenue coming from its higher margin annuity like service business (where gross margins are 2 to 3x higher then the contract business) – plus they now have pre fab manufacturing operations and electrical, all of which is to suggest that "normalized" gross margins should be quite a bit higher this cycle then the historical mid cycle gross margin mentioned above).

Furthermore, note that since 2013, pricing has gradually improved as the supply/demand balance began to shift decisively in Limbach’s favor. And honestly, with interest rates hovering above zero, our view is demand for the types of large, technically complex high profile projects that Limbach specializes in will far outstrip supply for the foreseeable future.

After all, with the cost of capital so low, the time for businesses and governments to embark on the type of large scale capital spending projects is clearly now. There has arguably never been a better backdrop. This is intuitive, not to mention reflected in the architectural billings index as well as the expected 6% annualized growth rate across the company’s various sub-verticals between now and 2020. Perhaps you’re in the camp that believes interest rates will spike substantially in the months and years ahead, but if not, it's hard to imagine a more ideal environment to own this business.

But our point is this; considering all the company has done in the interim as well as the power of interest rate and various other tailwinds propelling the business forward, we see today’s 13.6% gross margin improving to 15% and beyond in the years ahead. Likewise, this is very clearly a scarce and valuable asset likely to receive considerable financial and strategic buying interest in any environment, but especially in today’s secularly slow growth world where organic growth is sputtering along at 2% and (real) interest rates look pinned at zero indefinitely. To be clear, we don’t expect the company will sell until its been able to realize its vision – just highlighting that, at the current quote, investors have a chance to buy in at a deep discount to Limbach’s private market value.

Value Enhancing M&A

While Bacon & Co. have multiple levers at their disposal to drive organic and acquisition related growth in the years ahead, we wanted to take a moment to discuss the M&A opportunity, particularly with respect to strategically acquiring leading electrical businesses within their existing footprint. Granted, we fully expect organic growth to remain the company’s core focus in the years ahead, if only because the company’s current $2.1 billion deal pipeline is so large relative to the current backlog – and of course because management has said much the same thing.

Regardless, we think the market is effectively discounting no value to what I consider to be a “high impact” consolidation opportunity that has real potential to substantially increase Limbach’s regional market share – and their top and bottom line along with it.

As far as the consolidation economics, note that small, leading electrical firms operating within Limbach’s footprint simply cannot command high prices when they sell themselves, and the data confirms it - as EBITDA multiples in M&A deals for electrical subcontractor's have historically been done for 3.5x to 4.5x EBITDA. Mind you, that’s before accounting for estimated revenue and cost synergies - so from LMB’s perspective, the implied purchase price will generally amount to less then 3x EBITDA when all is said and done.

This is because many of the leading electrical subcontractor's LMB has its eye on lack diversification, are relatively sub scale, and aren’t typically self-sustaining without the talent and motivation of their founders. Naturally this dynamic doesn’t leave them with a very strong position from a negotiating perspective.

In contrast, established mid-sized and large asset light engineering and construction firms generally trade for 9x to 10x EBITDA, making the opportunity for value creation through M&A self evident given the size of this adjacent market as well as the sheer magnitude of the private/public arbitrage currently available to publicly traded consolidators with decent scale.

At the same time, it’s not all bad news from the seller’s perspective. Yes, they generally lack options but most leading electrical firms will want to sell to a recognized industry leader that cares about culture and quality - and Limbach is most definitely that. Think of these deals then as a de facto liquidity program for a number of highly successful electrical subcontractors operating within the company’s current (and future) footprint. To quote Limbach’s CEO Charlie Bacon, “we know who the acquisition targets are because we build buildings with them”. Read into that what you will.

And what’s their alternative anyway? At least this way said owners can receive full value for a business that otherwise would have little to no franchise value once its owners retired. Plus, the seller is likely to have an option to receive LMB equity in lieu of cash - equity mind you, that will likely prove far more valuable in time then anything these owners could have created on their own. Which is why we think these acquisitions ultimately amount to a true win/win deal for everyone involved. Exactly as it should be.

Of course the option value presumes management’s valuation discipline will hold and that they’ll continue to prove themselves capable integrators as they continue to execute their strategy over time, but assuming the center holds – and we believe it will - owners of leading electrical firms lucky enough to get acquired early on and with a good chunk in equity, have the potential to create immense wealth for themselves as LMB scales.

Lastly, its critical to understand that growth via strategic M&A actually de-risks the business “one high return deal at a time” thanks to the increased economies of scope and incrementally more attractive “one stop shop” value proposition that comes with it. After all, this is about much more then high returns on reinvestment, as executing the strategy should diversify the business while broadening and deepening the scope of the company’s service offerings across its existing footprint.

So not only does the incremental revenue come with high contribution margins, the business will be more diverse with considerably more (local) market share and the only true integrated “end to end” MEP solution, not just in their markets, but across the entire US. It should also allow Limbach to better leverage its sterling reputation for quality and innovation while further entrenching long standing relationships with premier customers - both existing and acquired.

We could go on, but the fact of the matter is this strategic transformation into the only one stop shop in the US (via strategic M&A) makes fantastic business sense on a number of levels. Not only will Limbach be left with a much stronger market position, it will run a permanently improved, more operationally efficient business that operates across a more diverse set of end markets while serving a much larger, more diversified customer base – which should lead to a pricing advantage, and an ability to maintain better top and bottom line performance under adverse market conditions. Clearly less cyclicality and higher margins with respect to the companies already remarkably stable, highly visible revenue and cash flow stream is a good thing.

Quantifying the Compounding Opportunity

As a quick thought experiment, let’s assume management kicks off a multi year, relatively continuous game of multiple arbitrage where the company is able to acquire an incremental $20 million in EBITDA over the next 4-5 years. In that case, if one adjusts for revenue and cost synergies that would be realized through consolidation and feels comfortable assuming public markets will eventually assign Limbach a multiple of 10x EBITDA, so something on the low end of its inferior peers and in line with a decent, stable business (as opposed to the great, rapidly growing business that this company is) – we propose that the math speaks for itself.

For example, in the case above Limbach will have spent roughly $60 million to create in incremental $200 million in equity value - so the implied value creation in the above scenario from this lever would be over 4x the value of the company's equity current market cap alone!! If that’s not one hell of a public/private arbitrage I’m not sure what it!

Valuation

Conclusion

At the end of the day, our internal calculus tells us that essentially all roads lead to Limbach’s warrants being worth considerably more then what one can purchase them for in the open market today. In the short-term, the value of these warrants should be valued 50-100% above where they currently trade simply as historical volatility moves higher and the forced selling from arbs abates with fundamental investors taking their place. Longer-term, we have a fundamental thesis that the shares are worth at minimum $18-21 apiece, or $3.50 to $5.00 per warrant vs. $0.99 today.

In conclusion, investors have a rare opportunity to purchase a 5 year LEAP on a grossly mispriced, rapidly growing microcap offering a compelling, highly asymmetric risk/reward with a low probability of permanent loss.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

Uplist to the Nasdaq

Increasing investor recognition of a great business

| show sort by |