Thesis: the turnaround in Barbie, plus continued benefits from restructuring, will drive EPS above consensus and expand multiples.

Catalyst

Barbie turnaround

The Barbie turnaround is being underappreciated by the market.

To address concerns of Barbie fitting a one-demographic stereotype, MAT introduced a new range of Barbie dolls that includes up to 12 complexions and multiple body shapes. Public reaction has been very positive to the change and is being reflected in brand sales.

Evidence:

TTPM (Toys, tots, pets & more) CEO/Editor-in-Chief Jim Silver commented on the Citi experts call that Barbie continues to do very well at POS, stating "some retailers are seeing 30-40% growth in Barbie". At the Citi leisure conference two weeks later he reiterated that Barbie continues to do well and said that momentum has begun to turn internationally (which he said usually lags the US by ~6 months in toy trends) and that international should continue to deliver strong growth for Barbie for many quarters. International is also a bigger market for Barbie than domestic so this is an important development.

UBS retailer channel check published Nov 21st had Barbie retail sell-through up "solid high to low teens in Oct through mid Nov".

Amazon bestselling toy search has the Barbie 2016 holiday doll at #3 - the highest position for a single-gender product. Walmart named the Barbie Rainbow Cove Princess Castle Playset on its hottest 25 toy for the holidays, does not offer rankings.

Catalyst Timing - 4Q16 EPS Jan 30th but expecting continued retailer feedback through the holidays selling season that will positively affect the stock.

Catalyst Relevance - Barbie is by far MAT's largest brand and is the most important for stock sentiment. Barbie's decline into negative constant growth from 1Q14 through 2Q15 coincided with a 58% drop in the share price from $45 to $20. Since Barbie returned to positive CC growth in 4Q15, the stock has appreciated 63% to $32. I would caveat that this period has coincided with MAT's restructuring that is delivering material margin expansion/earnings uplift.

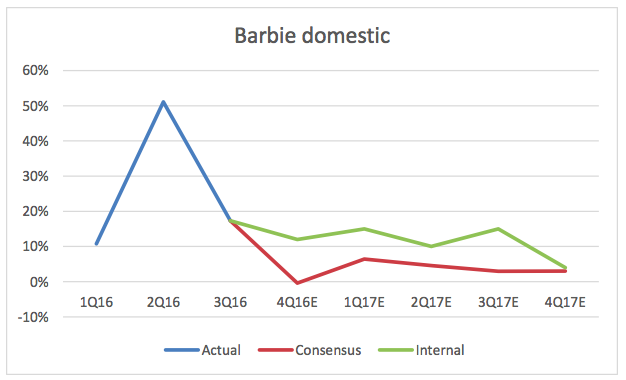

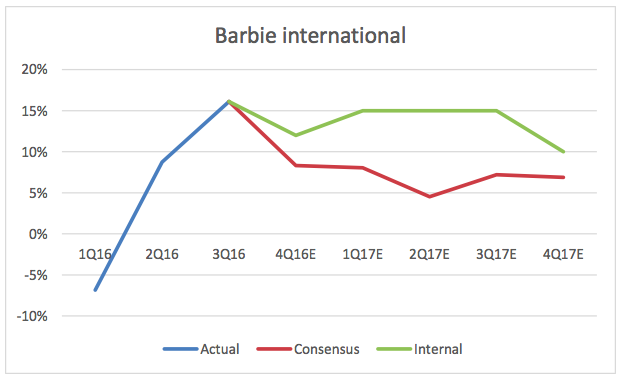

Reflection in consensus - Consensus is not capturing Barbie's growth in its forecasts. Consensus forecasts domestic Barbie flat in 4Q then growing L-MSD in 2017, while international is forecast to growth 8% in 4Q (in line with 3Q) then M-HSD in 2017. Charts below illustrate the sequential drop off in growth rate forecasts for both domestic and international Barbie which run contrary to POS feedback. For 2017, these differing growth rates alone account for an 80bps benefit from Barbie domestic and 65bps for Barbie international, summing to a total benefit relative to consensus of 1.45%. This is material in light of total revenue growth guidance of M-HSD.

Reflection in share price - The Barbie turnaround does not appear reflected in MAT's share price either based on:

Stock is flat since beginning of February, despite clear evidence restructuring is working

Stock is trading below its 1yr historic average trading multiples for PE and EBITDA

Stock is trading in line with peer HAS: 12.0x vs. 11.7x EBITDA and 18.6x vs. 19.6x PE, despite HAS not having the margin benefit of a cost save program and having weak POS trends.

2. Variance from consensus

Our 2017 sales forecast is 210bps ahead of consensus (9.0% growth vs. 6.9%) and guidance for M-HSD. As above, 145bps of this growth is due to Barbie, with the balance due to Wheels which will benefit from the 2017 Wheels movies, a view confirmed by Jim Silver.

Our forecasts for margins match consensus, primarily driven by guidance issued at the November Analyst Day for gross margin "to approach 50% over time". We therefore have a 49.4% gross margin vs. 48.2% in 2016, 49.2% in 2015 and 49.8% in 2014.

There is upside opportunity to SG&A which is where a material part of the restructuring cost saves are located. We forecast SG&A flat y/y, 220bps of expansion, but at the Analyst Day the CFO said they "plan to announce a significant incremental cost saving target in February" so there's potential upside to my forecast, which is slightly higher than the street's.

Those combined result in our EPS of $1.86 vs. cons $1.78 (5% ahead).

EBITDA multiple sensitivity: MAT trades at 12.0x EBITDA. A 1x move represents a $2.63 impact to the share price, ~8%.

3. Peak to trough

4. Valuation

The only true peer to MAT is HAS which is a strong operator but does not have MAT's growth prospects. As above, MAT trades in line with HAS at 12.0x consensus EBITDA vs. 11.7x.

HAS has historically traded at a premium to MAT vs. parity currently.

We argue that the difference in growth prospects (MAT 42% EPS growth vs. HAS 7%) warrants a premium to MAT irrespective of past ranges.

In addition to an expected multiple appreciation, or at least rerate vs. HAS, applying the same 12.0x EBITDA multiple to our above consensus forecast results in an additional $2 of share price upside (6%).

5. Risk/reward

There are two clear downside cases to consider: the first is that we’re wrong on Barbie, retailer feedback/channel observations are incorrect and the recovery has stalled, and the second is that MAT's restructuring program stalls.

We’re less worried about being wrong on Barbie because we see that as low risk given consistently of positive indicators and because consensus embeds a slowing of growth in the channel so there's cushion there.

We’re more worried about MAT's turnaround failing because expectations are very high here. The street models 200bps of operating income margin expansion in 2017 and it is difficult to get visibility on if this is being delivered. That said, MAT outperformed recovery expectations last quarter and the CFO has indicated cost save targets will be extended in February. Restructurings are momentum games and momentum is with MAT currently.

Downside case 1: Barbie slow: Should Barbie slow from +17% in 3Q to MSD growth in 2017 (vs. our forecast of +11%) (domestic), and +16% to MSD in 2017 (vs. our forecast of +13%) (international), our EPS falls to $1.73 (cons $1.78) because the benefit of Wheels is not enough to offset our conservative SG&A forecast. That would drive a share price $30.50, assuming current multiples hold.

Downside case 2: restructuring fails: This would likely come down to gross margin which is the contentious source of margin improvement. Some don't believe there is any gross margin upside at all. Assuming 2017 gross margins are flat, our EPS (including Barbie recovery) drops to $1.68 vs. cons $1.78. We view this as a particularly conservative bear case given management was reiterating 2017 gross margin upside only three weeks ago. That outcome would drive a $2.60 of share price downside, to $29.80 if current multiples hold, but would almost certainly be accompanied by a downward rerating of the stock. At a trough multiple of 10x EBITDA, that outcome would see the stock return to $25.

I do not hold a position with the issuer such as employment, directorship, or consultancy. I and/or others I advise hold a material investment in the issuer's securities.

Are you sure you want to close this position MATTEL INC?

By closing position, I’m notifying VIC Members that at today’s market price, I no longer am recommending this position.

Flag MATTEL INC for Removal

Are you sure you want to Flag this idea MATTEL INC for removal?

Flagging an idea indicates that the idea does not meet the standards of the club and you believe it should be removed from the site. Once a threshold has been reached the idea will be removed.

You Cannot Submit Message ... Yet

You currently do not have message posting privilages, there are

1 way you can get the privilage.

You can apply for full membership by submitting an investment idea of your own. Or if you are in reactivation status, you need to reactivate your full membership.