| 2018 | 2019 | ||||||

| Price: | 17.60 | EPS | -0.42 | 0.42 | |||

| Shares Out. (in M): | 338 | P/E | nm | 42 | |||

| Market Cap (in $M): | 5,947 | P/FCF | nm | nm | |||

| Net Debt (in $M): | 2,345 | EBIT | -46 | 346 | |||

| TEV (in $M): | 8,292 | TEV/EBIT | nm | 24 | |||

| Borrow Cost: | General Collateral | ||||||

Sign up for free guest access to view investment idea with a 45 days delay.

- MATTEL INC MAT 04/22/2022

- MATTEL INC MAT S 08/28/2019

- MATTEL INC MAT 12/02/2016

- MATTEL INC MAT 03/10/2015

- BETA

- NEWPARK RESOURCES (NR) NR 11/27/2020

- Western Asset Global Corporate Defined Opportunity Fund GDO 12/15/2014

- HASBRO INC HAS 04/09/2023

- NOVA LIFESTYLE INC NVFY 10/21/2019

- Hasbro HAS 02/11/2003

- NV5 GLOBAL INC NVEE S 11/07/2018

- JAKKS Pacific JAKK 12/16/2002

Description

SUMMARY THESIS

MAT has emerged as a compelling asymmetric short candidate following a dramatic and arbitrary rise in shares to levels pricing in a low probability bull scenario despite a higher probability bear scenario capable of cutting shares in half (or more). Specifically, bulls believe that MAT can execute against an unprecedented turnaround plan in the face of severe operational and secular headwinds to more than quintuple EBITDA and do ~$1.00 of normalized EPS in 2020, aligned with aspirational posturing from a Company / ever evolving management team that has habitually burned unsophisticated longs over the years. More importantly, this utopian outcome is now fully reflected in today’s stock price, evidenced in part by MAT’s premium valuation relative to best-in-class peer Hasbro (where MAT should unequivocally trade at a discount) even on forecasts ascribing MAT the benefit of the most unrealistic go-forward profitability ramp of any publicly traded consumer / retail company (as implied by a review of hundreds of peers with comparable anticipated operating profiles and MAT's own historical precedent). More credible, quantitatively rigorous bottoms-up constructs suggest MAT may struggle to generate even a penny of positive earnings come 2020 and continue to burn cash in the interim. Such an outcome will have dire consequences for the equity given a swelling leverage burden that has quadrupled in just four years even as FCF has plummeted to significantly negative levels. MAT also appears to be aggressively manipulating earnings at an accelerating rate - a dynamic illuminated in a recent Q1 report containing a number of peculiarities reminiscent of channel stuffing allegations made against the Company just last year. In a more extreme downside scenario, MAT goes bankrupt / liquidates (a risk MAT even acknowledged in its latest 10K for the first time in corporate history) for many of the same reasons that led to the downfall of Toys “R” Us as summarized below:

Spin Master CEO (Ronnen Harary) on the Bankruptcy of Toys “R” Us (5/9/18)

“Let me start by saying that as a longtime participant in the toy industry, it is very sad to see Toys"R"Us demised in the U.S. and in the UK. We are of the belief that TRU had a great franchise. It is not a signal as to the strength or the weakness of the toy industry or retail in general for that matter, rather it is a function of Toys"R"Us's specific ownership, capital structure and operational issues.”

KEY ELEMENTS OF THE SHORT THESIS

Compelling Entry Point Created by a Non-Fundamental ~25%+ Rise in Shares - The broader retail rally over the last month has squeezed numerous highly levered / shorted stocks in and around consumer / retail and MAT is no exception. The stock is now up ~25% since the beginning of May vs. best-in-class, low short interest peer Hasbro up just 4% over the same period. In fact, MAT is now up ~15% YTD (vs. Hasbro flattish) and trading at considerable valuation premiums despite the Company’s most notable “accomplishments” being:

- Former CEO and initial champion of the turnaround plan, Margaret Georgiadis, jumping ship in April after a little more than a year on the job. Conversations with various stakeholders suggest that Margaret felt blindsided by the state of financial disrepair upon joining and the situation became so increasingly untenable during her tenure that the professional risk associated with being the CEO for a public company whose stock gets chopped in half both years of her tenure would be too great to bear

- Margaret was then replaced by Ynon Kreiz whose last leadership position was characterized by meaningful misses to aggressive expectations

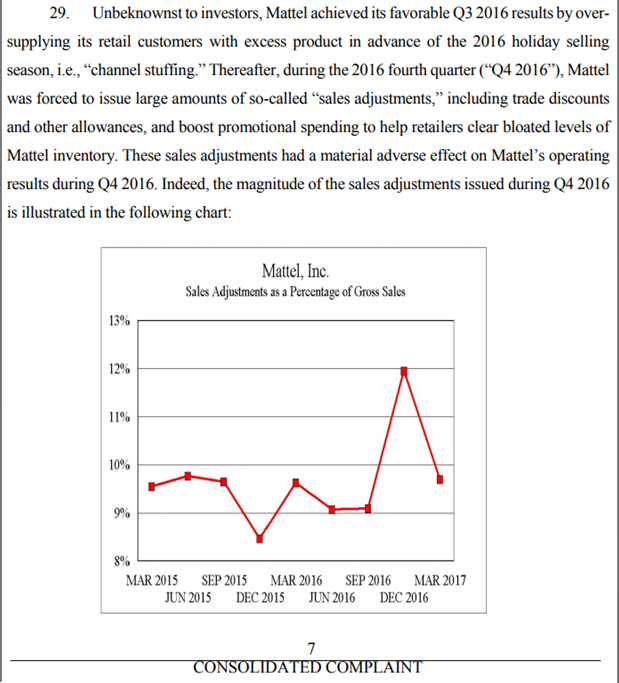

- Continued woeful financial performance that has caused Street 2018E EBITDA expectations to move down over 40% since the beginning of the year

- The official bankruptcy of Toys ‘R’ Us (7% of overall MAT revenues), MAT’s largest retailer, which is unequivocally a negative in 2018 and a best-case neutral after 2018 (as already reflected in Street earnings expectations)

- A series of credit ratings agency downgrades (LTM net leverage is north of 12x EBITDA)

- An expensive recent debt refinancing that will add $20+ million of annual interest expense (~5% dilutive) still not broadly reflected in Street models

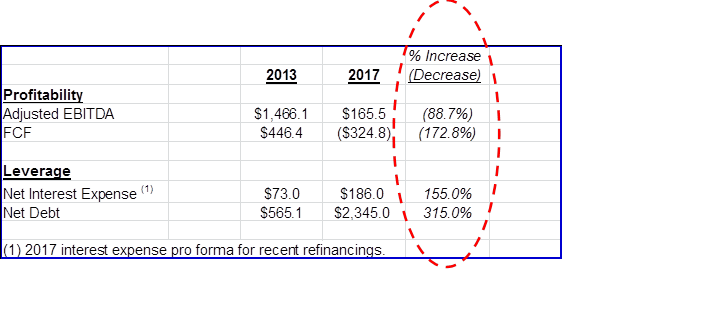

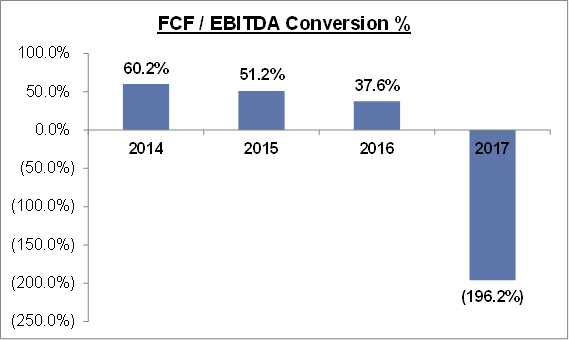

MAT is in Dire Straits Following Sustained Financial / Operational Ineptitude and Accelerating Secular Pressures - In four short years MAT has managed to QUADRUPLE its debt burden while losing ~90% of its EBITDA and ~200% of its FCF. These losses are particularly staggering considering MAT claims to have generated $416 million of cost savings over this period and these losses occurred before the official bankruptcy of its largest retailer, Toys R Us. Going forward, the structural backdrop for MAT is poised to become even more challenged than years past. Headwinds range from the tech industry's increasingly firm grip on children's free time (video games, tablets, etc.), which in addition to competition is leading to age compression in MAT's core demographic, millennials having far less brand allegiance than prior generations, consistently rising freight costs (~15% of COGS), a business model increasingly reliant on competing for the contract licensing of other brands (inherently lower margin), an increasingly strained balance sheet that will limit MAT’s operational flexibility and, of course, the aforementioned Toys R Us bankruptcy.

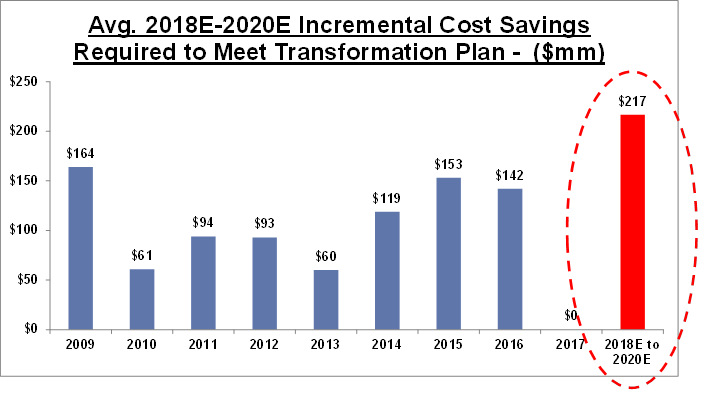

MAT Recently Announced an Unprecedented and Highly Aggressive Turnaround Plan in an Attempt to Retain / Attract Shareholder Interest - The current turnaround plan is headlined by a $650 million “Structural Simplification Cost Savings Program” initiated in Q317 along with an expectation to organically (and profitably) grow the top-line despite five consecutive years of negative revenue growth. Bulls believe these efforts will be able to collectively turn MAT into a business doing something in the zipcode of $900 million+ of Adjusted EBITDA (vs. $165 mm in 2017) and $1.00 normalized EPS (vs. significantly negative earnings in 2017) come 2020. The current cost savings program is actually MAT’s fifth such effort since 2008. Across its prior 4 cost cutting programs (2008 to 2016), it took MAT 8 years to cut a total of $886 million of costs (as quantified by the Company in its historical financials) and yet they now expect to cut $650 million more (off a current revenue baseline 20%+ lower than averaged 2008 to 2016) in just 3 years. Stating the obvious, once a Company has already taken aggressive efforts to right size it’s cost structure like MAT already has, it becomes exceedingly more difficult to cut incremental costs. Nevertheless, MAT’s current plan implies that on average, MAT will generate $217 million of incremental cost savings / year for the next three years, DOUBLE the $111 million averaged from 2008 to 2016 and 30% higher than the most cost savings ever generated in any single year. Not surprisingly, MAT’s largest cost savings year was 2009, the first year of its first cost savings program where presumably there was the most “fat” to cut.

Powerful HIstorical Precedent and Conversations with Multiple Formers Suggest MAT’s $650 mm of Planned Cost Cuts are a Red Herring - Consider the following hypothetical:

- Company X reports $100 million of revenues and $10 million of EBITDA in its most recent fiscal year (year 0)

- Company X completes an acquisition that will contribute $3 million of EBITDA the following year (Year 1)

- Company X announces a cost savings program that will contribute another $3 million of EBITDA to Year 1

- Organically, revenues will decline by 10% (or $10) in Year 1. Company X operates with a 100% fixed cost structure, thereby creating a $10 million EBITDA headwind in Year 1

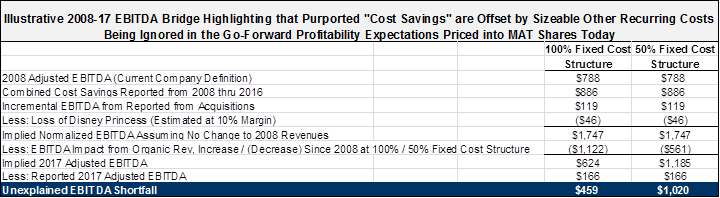

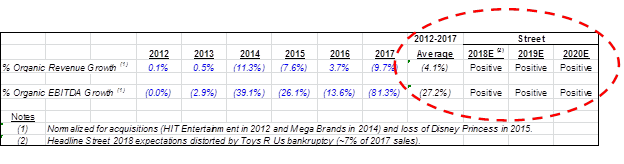

Year 1 EBITDA would thus be correctly and simply calculated to be $6 million (Starting baseline of $10 million, add $3 million from the acquisition, add $3 million from cost savings, and then subtract $10 million for the $10 million organic revenue decline with no offsets given its 100% fixed cost structure). MAT’s historical disclosures provide enough detail to replicate this construct and build a theoretical EBITDA bridge from 2008 (when the first of its 5 cost cutting programs was announced) to the most recent year ending 2017, retroactively adjusting historical profitability figures to align with its current (not to mention increasingly evolving) Adjusted EBITDA definition, acquisitions completed, and the loss of Disney Princess. Per the table below, the math doesn’t even come close to directionally reconciling even when assuming that MAT has a 100% fixed cost structure (which of course isn’t even close to true) suggesting that purported cost savings figures are red herrings that materially understate numerous other recurring operating costs in the business required to sustain even a dwindling top-line. Conversations with multiple former employees (including a former CEO) proved confirmatory of this seemingly obvious quantitative reality.

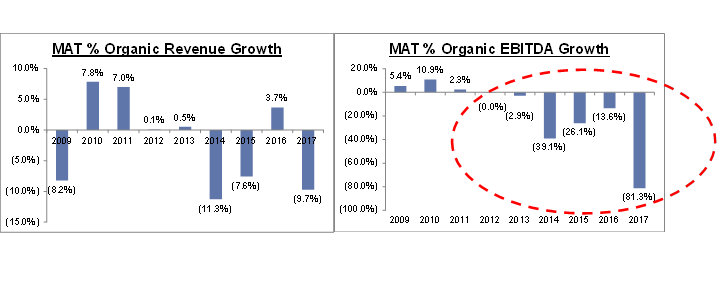

In Addition to Standalone Cost Cuts, Successful Turnaround Contingent on Multiple Consecutive Years of Profitable Organic Growth Despite All Tangible Indications Suggesting the Opposite - In addition to $650 million of incremental cost savings, the current turnaround assumes a favorable reversal in organic growth trends at dramatic odds with historical precedent and the unprecedented structural pressures impacting toy manufacturers today. As shown below,, the sustained pace and magnitude of MAT’s organic EBITDA growth declines over the years is staggering, making it that much more challenging to confidently underwrite a scenario where the plethora of headwinds that have caused MAT to average NEGATIVE ~30% EBITDA declines suddenly abate and inflect favorably.

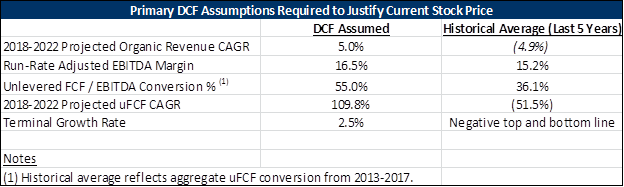

MAT Unlikely to do $1.00 of Normalized EPS in 2020 Even Should Current Turnaround Efforts to be the Most Successful in Corporate History - YE 2009 to YE 2012 was a proverbial golden age for this Company where MAT executed against its then cost savings program every single year AND organically CAGR’d the top-line for three consecutive years, a directionally similar case study to what is now being expected for MAT through 2020 with the following differences:

- YE 2009 to YE 2012 revenues organically CAGR’d at close to 5%, above the low single digit organic growth projected even by MAT bulls today

- The average revenue baseline was over 25% higher than it is today (i.e. growth off a higher baseline equals higher absolute incremental EBITDA dollars)

- Secular pressures were less pronounced relative to current (as evidenced by MAT’s absysmal financial underperformance over the last half decade as referenced above)

- MAT’s largest retailer (Toys R Us) was still going strong. Toys R Us is now bankrupt

- MAT exited 2009 with a net cash position of nearly $400 million dollars and the business was throwing off strong free cash flow. Presently, MAT carries over $2.3 billion of net debt and the business is losing hundreds of millions of dollars of cash flow, obviously now leaving the Company relatively far more operationally constrained to pursue growth opportunities capable of offsetting a continually declining top-line

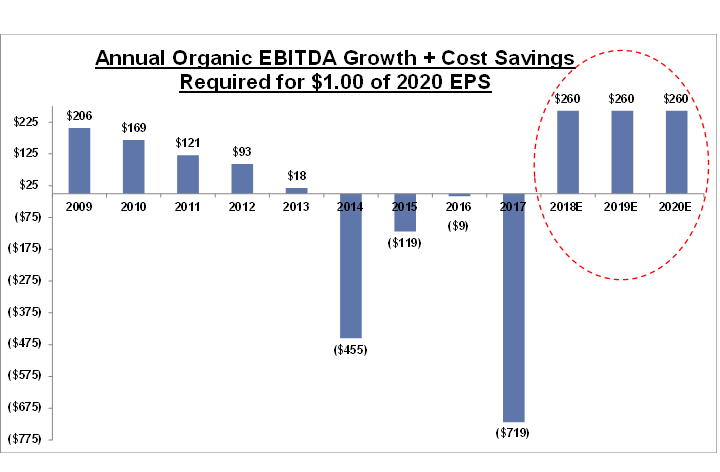

Recognizing the increasing number of operating headwinds today relative to a decade ago, one could make the credible argument that a dream scenario for MAT would be to replicate the organic EBITDA improvement and cost cutting successes achieved during this golden era. Unfortunately (for anyone long), this outcome would turn MAT into just a ~$550 million adjusted EBITDA business in 2020 (40% below the baseline required for $1.00 of earnings power), and a stock price 50% below current even undeservedly giving MAT Hasbro valuations. Below are the annual combined cost savings and organic EBITDA growth generated by MAT every year since 2009, calculated by normalizing historical profitability figures for MAT’s current adjusted EBITDA definition, adjusting for acquisitions, and then incorporating the cost savings figures MAT fortunately discloses in filings. During MAT’s three year golden era (2010, 2011, 2012), MAT generated a combined $383 million of incremental EBITDA from organic growth and cost cuts. MAT will need to DOUBLE this figure to generate the level of earnings / FCF being priced into this stock through 2020.

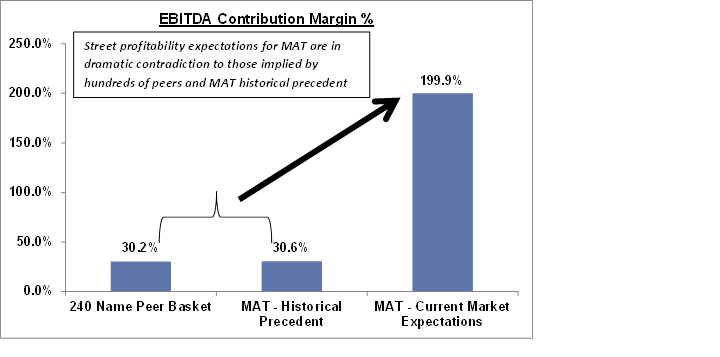

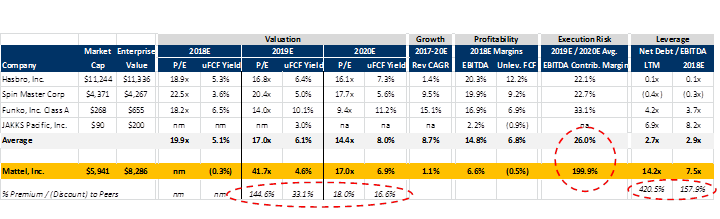

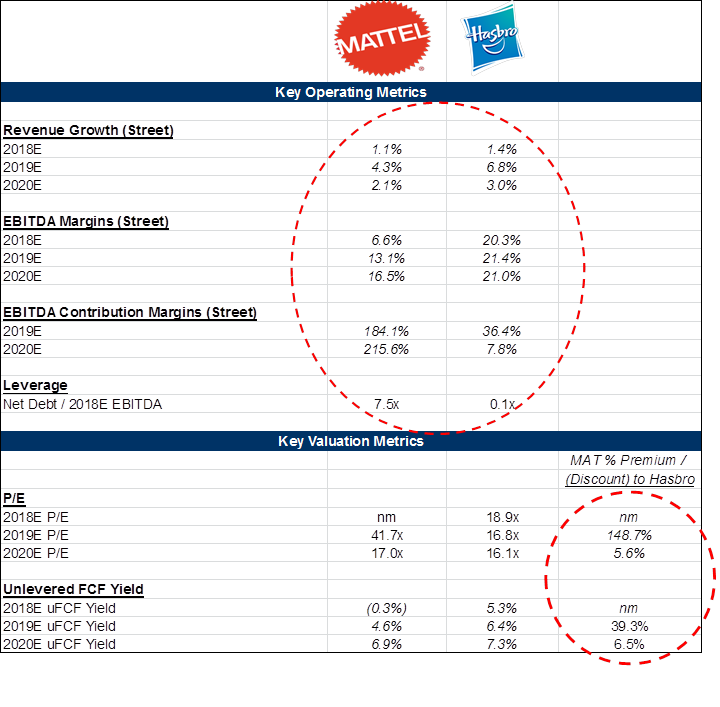

MAT is Potentially Being Ascribed the Most Unrealistic Set of Profitability Expectations of Any Publicly Traded Consumer / Retail Company - Taking a step back, if one were to generously assume that MAT can execute against current Street 2018 profitability expectations (vs, our work that suggests they will miss every single quarter by a wide margin), MAT will need to earn a ~200% contribution margin from the end of 2018 thru the end of 2020 to satisfy the bull case now being baked into the stock. This compares to hundreds of retail / consumer peers as well as MAT’s own historical precedent as follows:

- Consumer / Retail Peers with Comparable Operating Profiles - A ~200% contribution margin would be 7 TIMES HIGHER the average incremental margins expected for 240 consumer / retail peers with comparable operating profiles and nearly 50% higher than number two on the list

- MAT Historical Precedent - A ~200% contribution margin would be 7 TIMES HIGHER than MAT’s historical average and FOUR TIMES HIGHER the highest contribution margin ever earned by MAT when the Company was both organically growing the top-line (faster than the current MAT bull case is calling for no less) while simultaneously benefitting from cost cutting programs to a cost structure that by definition had more low hanging fruit than today

Accelerating Evidence of Earnings Manipulation Suggests MAT is Running Out of Ways to Sustain the Perception that a Quintupling of Adjusted EBITDA is Feasible by 2020 - These include:

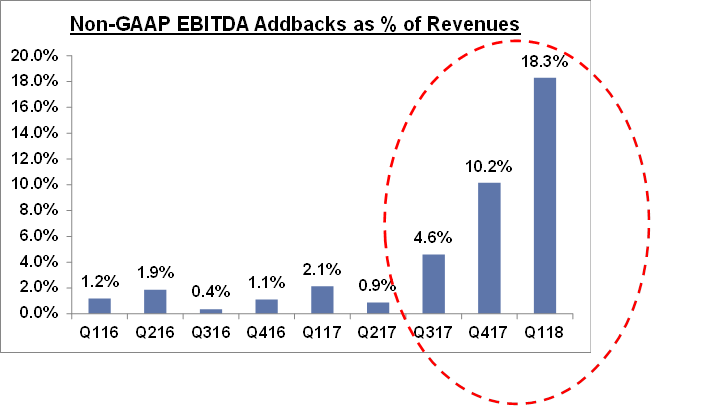

- Continually increasing number of Non-GAAP add-backs - The below graph should be fairly self explanatory and what is being shown for Q118 is not a typo. Even with the benefit of massive add-backs representing over 18%+ of revenues, Q1 adjusted EBITDA of ~negative $74.6 million was still nearly double the EBITDA loss in Q117

- MAT randomly started to add-back stock-based compensation in Q317 for the first time ever, which has distorted how the name screens relative to Hasbro on an EBITDA basis - Of the combined ~$92mm of Adjusted EBITDA MAT has reported for the last three quarters (Q317 to Q118) , ~55% is comprised of a new SBC add-back that the Company had never previously adjusted for in its Non-GAAP reporting. 55% is clearly a big EBITDA contribution in its own right, but this dynamic is also worth flagging because Hasbro does not add back SBC to its any of its reported EBITDA metrics, thus meaning that headline Street forecasts for each are apples and oranges

- Growing divergence between reported profitability levels and underlying FCF - Besides this dynamic being a tell-tale sign of earnings manipulation, it’s also important not to lose sight of the fact that MAT is hemorrhaging cash - not good for an extremely levered entity that is continuing to refi under more punitive terms. The Company burned $325 mm of cash in 2017 (over 5% of its current market cap), a number they impressively matched in Q118 alone

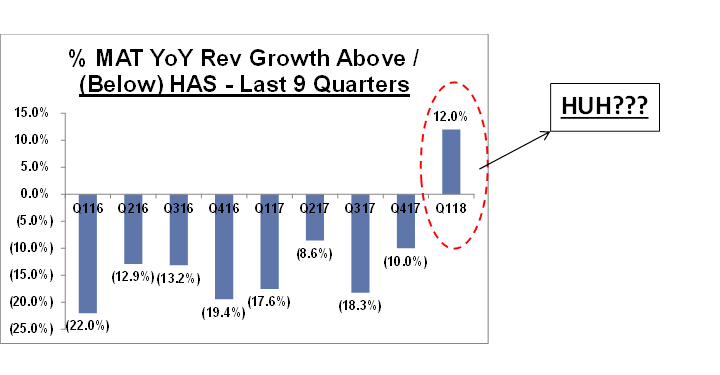

- Peculiar Q118 Reported Top-Line / Profitability Trends - Up until Q118, there was a clear pattern between MAT reported YoY growth trends and Hasbro to where MAT YoY growth would typically lag Hasbro by anywhere from ~900 bps to ~2,200 bps. This trend suddenly massively reversed in Q118 and MAT’s reported YoY growth actually came in 1,200 bps ABOVE Hasbro, allowing MAT to beat Street top-line forecasts (that everyone was expecting them to miss) while Hasbro missed by over 12% when Hasbro had never missed Street top-line forecasts by more than 7% in the preceding 20 quarters). With such top-line outperformance, one would think underlying profitability would have at least come in-line ish with expectations (particularly given the drivers of this strength were supposedly MAT’s highest margin, vertically sourced brands), yet MAT did the opposite, missing Q1 Street Adjusted EBITDA expectations by over 30%

- Aggressive discounting likely a key driver of Q1 top-line strength - Q118 results included the highest levels of sales adjustments in the Company’s modern history, a dynamic that even management admits won’t be changing anytime soon. The notion that recent retail strength is being largely promotional driven was further validated when I visited a California Target store in June just 2.9 miles away from corporate headquarters (pictures below). Also note that one the products being discounted below include “Barbie Go”, which was supposed to be their big break out product this year.

"Q118 Earnings Call - “We expect our full-year sales adjustment rate to be similar to the first quarter and do not expect a significant year-over-year variance for the full year.”

- Discounting practices / channel stuffing allegations a key focal point in recent lawsuits against MAT - MAT has been accused of top-line shenanigans before. Lawsuit link / relevant excerpt below

http://www.classactionsreporter.com/sites/default/files/mattel_channel-stuffing_sec_compl.pdf

http://www.classactionsreporter.com/securities/mattel-engaged-channel-stuffing-says-securities-class-action

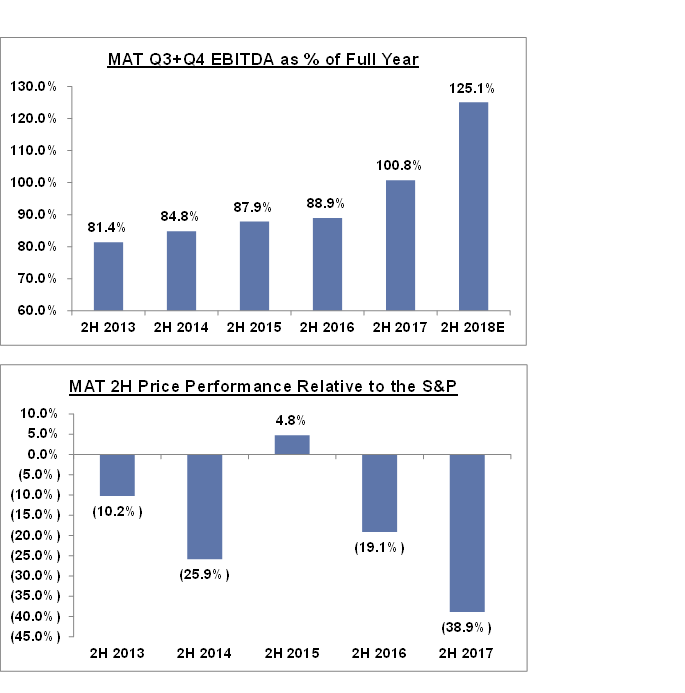

MAT has Consistently Walked Long Investors Off a Cliff in the Second Half of the Year, a Dynamic Likely to be Exacerbated in 2018 with the Most Backhalf Weighted Guidance in Corporate History - Not surprisingly, the majority of a toy manufactuer’s profits are earned in the second half of the year - a dynamic MAT is currently trying to use to its advantage to explain away recent financial underperformance. Notable comments from its recent Q1 call include:

“‘We also shared that the timing of those savings would be weighted towards the back half of 2018, and that our freight and distribution challenges from 2017 would likely persist into the first half of the year”

“The organization remains focused on achieving approximately 40% of the $650 million in 2018 with savings heavily weighted towards the second half of the year”

“And we remain committed to deliver a gross margin in the low-40s, with the majority of the year-over-year benefit coming in the back half of the year”

“Meanwhile, our Structural Simplification actions, including the recently implemented reduction of labor overhead in our manufacturing plants, are expected to be realized in the P&L in the back half of this year”

Management’s posturing has caused current Street Q3/Q4 EBITDA forecasts to represent 125% of the full year expectations, considerably higher than previous years. Even if the bar wasn’t set as high as its for the upcoming holiday season, trusting this Company’s forward looking commentary on on holiday sales has in aggregate been an extremely expensive mistake for MAT long holders from 7/1 to 12/31 over the last half decade.

New CEO’s Last Leadership Role Characterized by Significant Misses to Overly Aggressive Financial Targets - Prior to MAT, Ynon Kreiz’s last leadership role was at Maker Studios, which was purchased by Disney in May 2014 and led by Ynon until his departure in early 2016. This of course is known by all and referenced in all the Sellside notes recapping the management change in April. What you will not hear discussed is that after the deal closed, Ynon was at the helm as Maker missed multiple financial performance targets to where Maker ultimately received just $175 million of a potential $450 million worth of earnouts. The below article from Digiday discusses Maker’s post deal troubles in detail.

https://digiday.com/media/disney-maker-studios/amp/

“In this environment, aggressive growth targets — some departments were tasked with tripling or quadrupling revenue from 2015 to 2016, sources said — were impossible to meet”

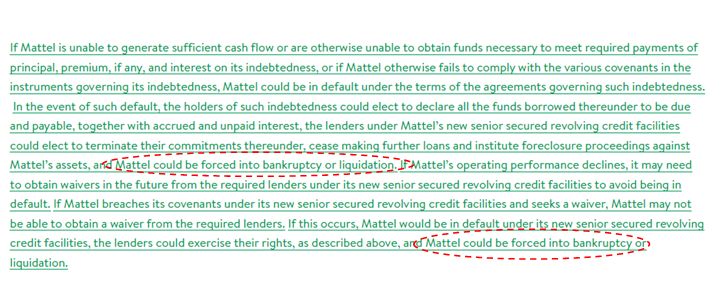

Multiple Relevant New Risk Factors Introduced in Latest 10-K Related to Potential Bankruptcy and the Achievability of Stated Cost Savings Goals - MAT’s latest 10-K blackline is worth a read for anyone (long or short) interested in the MAT story given the number of new and highly topical risk factors around MAT’s current cost savings plan and the potential adverse consequences of the Company’s current leverage burden. Below is one notable example as it is the first time in corporate history MAT has acknowledged bankruptcy / liquidation as a potential consequence of its massive debt burden.

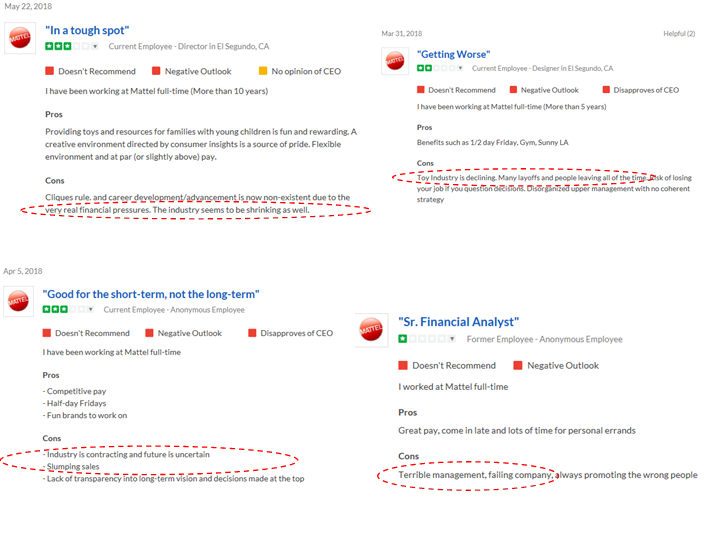

Employee Glassdoor Reviews Offer Anecdotal Evidence of Significant Corporate Dysfunction - Obviously Glassdoor is anecdotal, but reviews such as the below are a dime a dozen

VALUATION

Relative Valuation: Recent Rise in Shares has Created an Unsustainable Relative Valuation Disconnect - MAT is now by far the most expensive public toy manufacturer (on headline Street numbers that are poised to come down dramatically) despite being universally inferior across all meaningful financial and operating metrics. MAT also will continue to burn cash far in excess of peers and thus will continue to screen more and more expensive as time marches on. At a minimum, one would think that even modest shortfalls in coming quarters could reverse MAT’s current premium to best-in-class peer Hasbro to a healthy discount, particularly considering that, relative to Hasbro, MAT offers investors:

- Inferior growth

- Inferior profitability

- Inferior scale

- An inferior management team

- Substantially more leverage

- Substantially higher execution risk

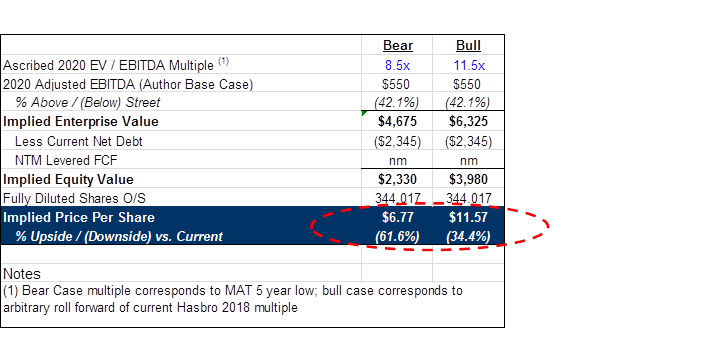

Asymmetric Risk / Reward with 50%+ Downside Over the Next 12 Months - Relative to MAT’s absysmal last 6 years of financial outperformance referenced above, YE 2009 to YE 2012 was a proverbial golden age for this Company where MAT executed against its then cost savings program every single year AND organically CAGR’d the top-line at close to 5% off a starting revenue baseline 15%+ higher than current. Over this time period, MAT added ~$380 million of total EBITDA (organic growth + cost cuts) to its starting EBITDA baseline ending 2009. Well, If MAT is able to heroically match this number and add ~$380 million to its current EBITDA baseline by the end of 2020, the Company would be doing in the zipcode of ~$550mm of EBITDA, over 40 % below where the Street sits today, which would obviously have material valuation consequences given its leverage profile.

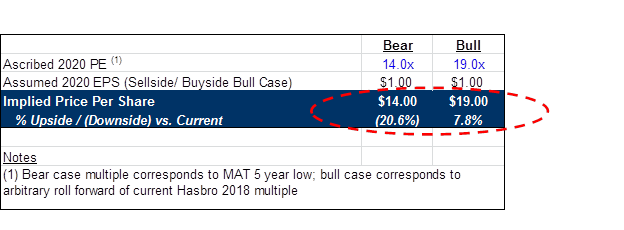

And If my current skepticism ultimately proves overblown and MAT ends up restoring profitability to levels that make this a $1.00 EPS business (and EPS finally a relevant metric once again)? Well, who cares given the stock is now already pricing in this lower probability outcome.

PRIMARY RISKS / MITIGANTS

Takeout by Hasbro - A takeout / merger with Hasbro today would make less strategic and financial sense now than it ever has at any point in the combined 170 years these two companies have been in operation (where no deal has taken place). In no specific order, key issues worth flagging:

- Ex MAT CEO Margaret Georgiadis jumping ship in April despite a meaningful change in control bonus

- Hasbro having sold all of its manufacturing facilities in recent years and its deliberate focus on digital / TV / movies (MAT would put them right back into traditional toy manufacturing)

- Recent capital allocation announcements from Hasbro (acquisition of Power Rangers, $500 million buyback) that strongly contradict a transformational merger of equals is of interest

- Even if Hasbro were interested, the M&A math doesn’t work for Hasbro at MAT’s currently inflated trading levels. The transaction would be highly dilutive even giving credit for healthy synergies and require a sizeable equity component that would put considerable downward pressure on Hasbro shares at announcement. The transaction would also require Hasbro to bear the execution / monetary risk around

MAT’s ambitious execution while getting nothing in return - Potential antitrust issues (MAT / HAS pro forma would comprise over a 1/3 of overall U.S. toy sales, but 60%+ in certain product categories)

- MAT’s own persistent adherence to a long-term transformation narrative

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

Multiple upcoming earnings misses

| show sort by |