| 2015 | 2016 | ||||||

| Price: | 16.65 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 583 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 9,690 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 0 | EBIT | 0 | 0 | |||

| TEV (in $M): | 0 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- Sum Of The Parts (SOTP)

- Spin-Off

- Murdoch

- Australia

- Print media

- Publisher

- Media

- Multi System Operator (MSO), CATV, Cable

- NEWS CORP NWSA 01/19/2021

- NEWS CORP NWSA 10/15/2019

- NEWS CORP NWSA 06/18/2013

- NEWS CORP NWSA 06/18/2013

- NEWS CORP NWSA S 10/14/2011

- NEWS CORP NWSA 08/19/2011

- BETA

- PERRIGO CO PLC PRGO 03/08/2016

- TWENTY-FIRST CENTURY FOX INC FOX 05/01/2015

- Brunello Cucinelli SpA BC.MI S 07/25/2021

- TWENTY-FIRST CENTURY FOX INC FOX 08/09/2018

- QUAD/GRAPHICS INC (5077B) QUAD S 02/22/2018

- NEWS CORP NWS 04/17/2023

- Salvatore Ferragamo SpA SFER S 07/18/2021

- "Core" News Corp CNWS 09/28/2016

Description

News Corp (NWSA is the more liquid, non-voting share class; NWS is the voting, slightly less liquid class which is trading at a 2-3% discount) is a collection of media and publishing assets around the globe. Often referred to as a newspaper company, the News & Information segment, of which newspapers are the largest part, represents only 38% of News Corp's TTM 12/31/14 economic EBITDA, with the remainder comprised of digital and cable businesses in Australia and a book publisher. The table below shows the breakdown in TTM 12/31/14 EBITDA, reflecting News Corp's economics in the segments rather than the accounting:

|

Foxtel & Fox Sports Australia |

37% |

|

Book Publishing (pro forma) |

16% |

|

REA Group |

9% |

|

News & Information |

38% |

News Corp was spun-off from 21st Century Fox (FOX/FOXA) in late June 2013. This spin was perceived as a split into a "good" company and a "bad" company, with FOX retaining the attractive cable businesses and News Corp getting the unwanted old media assets. As the chart above shows, this perception is unwarranted given the collection of assets News Corp possesses.

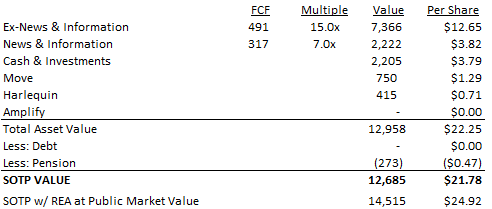

News Corp has a debt-free, cash-rich balance sheet and trades at a discount to the value of the sum-of-its-parts. An SOTP valuation shows News Corp is worth at least $22-$25 versus a current market price under $17. One could assign a value of zero to all of the News & Information segment and still get a value exceeding the current price. The non-News & Information pieces have collectively grown EBITDA at 14% per annum over the last three years (~10% organic), while News & Information has seen EBITDA decline at a 17% rate during this time. As the non-News & Information side of the business continues to grow and take a larger chunk of overall profits, the multiple investors assign to News Corp's economic profits will also move higher.

Valuation

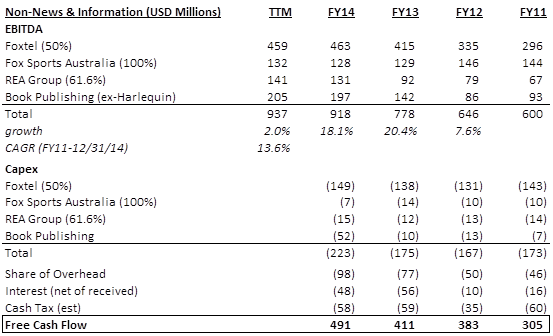

My preferred valuation route is to "look through" how the investments are held (e.g., Foxtel is an equity investment, REA is consolidated though News owns just 61% of the public shares) to get to News Corp's share of the economics. There are three parts to this approach: the higher-growth non-News & Information assets, the News & Information piece of the business, and cash & investments. All discussion in this write-up is in USD, unless stated otherwise, with numbers translated from AUD to USD for Foxtel and REA Group at year-end exchange rates. In the valuation below, numbers reflect News Corp's share of the results for the underlying companies as though it held its current percentage ownership stakes in each of the years, and corporate overhead is allocated based on share of EBITDA.

The non-News & Information assets (Foxtel, Fox Sports Australia, REA Group, and Book Publishing) have seen combined EBITDA growth of 15% per year from FY11-FY14, with Fox Sports Australia the only laggard, having seen its EBITDA decline by 4% per year (though flat in AUD). Foxtel, the dominant pay-TV operator in Australia in which News Corp holds a 50% stake (the remainder held by Telstra, Australia's leading telecom company) saw EBITDA grow by 16% rate from FY11-FY14, aided by its late FY12 acquisition of its largest rival. Book publishing grew EBITDA at 28% per year due to the popularity of the Divergent series and higher margins on e-books, which are taking up an increasing portion of overall book sales. REA Group, an online real estate business, continued its strong growth over the past three years, growing EBITDA 25% per year as online advertising continues to take share from print. As a group, the non-News & Information assets produced free cash flow of ~$0.85 per share in FY14. I value this collection of businesses at 15x free cash flow, a normal market multiple though this business has a better growth profile.

News & Information EBITDA declined by over 40%, though free cash flow by only 28% from FY11-FY14 as capital expenditures were reduced. This segment is facing ongoing challenges, but the deterioration in this business has slowed. News Corp owns highly regarded media properties with strong market share that should remain profitable. I assign a 7x FCF multiple to this business.

News Corp has over 20% of its market cap in cash with no debt. Since its spin-off, it has done two major acquisitions — Harlequin and Move. I am valuing the education segment, Amplify, at zero. Valuing REA Group at its public market value, rather than a 15x FCF multiple, boosts the valuation by $3.30 per share.

Australian Cable & Digital Properties

Over 45% of the News Corp's economic EBITDA comes from three Australian media assets: (1) 50% stake in Foxtel, a dominant pay-TV operator in Australia; (2) 100% ownership of Fox Sports Australia, which has several stations and the exclusive broadcast rights to both the Australian Football League and the Rugby League; and (3) 61.6% ownership of publicly-traded REA Group, which operates the largest residential property website, offering listings for new homes and apartments and other real estate-related information.

Both Foxtel and REA Group have grown revenues at double-digit rates since FY11 and EBITDA over 20% per year in AUD, while Fox Sports Australia has maintained relatively steady EBITDA in AUD even though revenues have grown. Doing a look-through on News Corp's share of EBITDA shows that collective EBITDA growth for the three Australian digital businesses has been 18% in AUD from FY11-FY14, but 12.4% in USD, reflecting the devaluation of the Australian dollar relative to USD.

Foxtel & Fox Sports Australia: In November 2012, News Corp bought out a minority partner in Foxtel and Fox Sports Australia, getting an additional 25% of Foxtel and 50% of Fox Sports Australia for $2bn in cash. This deal took News Corp's ownership stakes up to 50% for Foxtel and 100% for Fox Sports Australia. The combined valuation for News Corp's ownership stakes at the time of purchase was $4bn, ~$3.5bn in equity and ~$0.5bn in a subordinated note to Foxtel. Fox Sports Australia was debt free but Foxtel had $1.1bn of third-party debt allocated to News Corp's 50% stake. The enterprise value for Fox Sports Australia and 50% of Foxtel at November 2012 was $5.1bn and the EV/EBITDA multiple paid was 10.6x FY12 EBITDA. Applying this same multiple to FY14 EBITDA gives a value of $5.4bn for News Corp's debt and equity stakes, which equates to $9.30 per share.

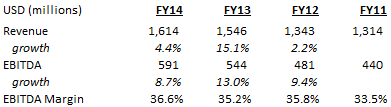

Australia has far lower cable penetration rates than those in the United States, ~30% of households compared to over 80% in the U.S. The lower cable penetration rates stem from strong competition from several free-to-air networks. Foxtel is the monopoly pay-TV operator in Australia with 2.7m subscribers as of 12/31/14, a 5% increase YoY. It is distributed via cable, satellite, and IPTV. Foxtel offers over 200 channels, but a key selling point is its sports content through Fox Sports Australia, with ~80% of Foxtel subscribers taking the sports tier for an additional A$25 per month. Because Fox Sports Australia gets all of its revenue from Foxtel, it cannot be as adversarial in negotiations as, say, ESPN might be with Charter given the overlapping ownership, which effectively limits Fox Sports' pricing power. Due to the intertwined nature of Foxtel and Fox Sports, it makes sense to value them together. Here is what these businesses look like combined, translated into USD and reflecting News Corp's share:

Foxtel acquired its largest rival, Austar, at the end of FY12 for $2bn or ~10x EBITDA. This boosted subscribers by 600 million and led to double-digit revenue and EBITDA growth in FY13. Foxtel's ARPU is among the highest globally at A$100, which, along with the quality of free-to-air programming in Australia, contributes to cable penetration rates that are among the lowest in the world. Foxtel is aiming to drive subscriber growth through offering exclusive sports broadcast rights held by Fox Sports, improving its TV anywhere service (Foxtel Go), and investing in other premium, exclusive content like Game of Thrones and other HBO programming.

REA Group: REA Group is an online real estate business offering residential and commercial classifieds through sites realestate.com.au and realcommercial.com.au. It has seen phenomenal growth with revenues and EBITDA up 22% and 30% per year, respectively, since FY11, leading to over 50% EBITDA margins in FY14. REA Group is a separate publicly-traded company (REA on the ASX), in which News Corp holds 61.6% of the shares. This business has been a major beneficiary of the move from print to digital advertising. Australia is 90% of its business, but it has nascent operations in Italy, Luxembourg , France and Hong Kong. Along with News Corp, it acquired Move November 2014, purchasing a 20% minority stake. REA Group makes money through listings, subscription, and display revenue, with listings now the largest revenue component. It has ~3x the traffic of its next largest competitor, Fairfax Media's Domain.com, and attracts agents and advertisers because it has the largest audience of customers, who flock to the sites for its real estate tools and information. REA Group is a very good business that trades at a premium valuation. News Corp's stake has a public market value of A$3.8bn, or approximately 41x TTM 12/31/14 free cash flow.

Book Publishing

The Book Publishing segment consists of HarperCollins, a leader in general fiction, children's literature, and Christian books. It is the second largest book seller in the world behind Penguin/Random House. This business is earning more than it was a few years ago, as higher-margin e-books take up a greater percentage of overall sales and boost margins, but revenue has moved sideways as e-books are priced lower than hardcover books. Sales of e-books were 22% of total sales in FY14, up from 19% in FY13. Though e-books are priced lower than hardcover books, the contribution profits of a $9.99 e-book are comparable to a $25 list price hardcover, as the former does not have manufacturing, distribution and return costs. E-books also have better working capital dynamics, as there are no inventory requirements. Total industry revenue has been relatively flat for several years, but margins are up across the board. The book business, like the movie business, is hit-driven, though to a reduced extent. HarperCollins revenue got a boost during FY14 from sales of the Divergent series.

News Corp completed its acquisition of the romance publisher Harlequin August 2014 for a price of $415m, or 8x 2013 EBITDA. Harlequin will help to expand HarperCollins global footprint, as nearly all of HarperCollins books are published in English, but only 60% of Harlequin's books are. Financials for this segment are below; note that at the beginning of FY13, News closed its acquisition of Thomas Nelson, adding approximately $200m to Book Publishing sales.

News & Information

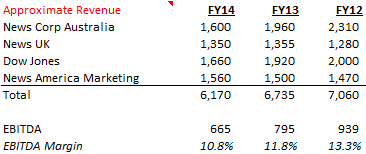

The newspaper business operates globally and, like all newspapers, is struggling. News Corp has a 60% market share of the Australian newspaper market through its ownership of several papers. In the UK, it has 33% market share through its two papers, The Sun and The Times. The Wall Street Journal, the company’s largest paper, and The New York Post make up the North American business. The Wall Street Journal is one of the few newspapers that has increased circulation over the past five years, with digital growth outpacing print losses. Also included in the News & Information segment is News America, a consumer marketing business best known for its SmartSource coupon inserts and mailers, and Dow Jones Institutional, a collection of products for institutional investors, including Factiva and LBO Wire.

News Corp doesn't break out results by product or geography in the News & Information segment, but one can back into approximate revenue numbers through the comments provided in the MD&A, though not enough information is provided to back into approximate profitability.

Newspapers will likely see continued declines in revenue and profitability, but News Corp delivers content that millions of people want and are willing to pay for. Moreover, News Corp management is realistic about the challenges facing the industry as seen through its cost cutting programs and digital initiatives. Its newspapers have strong market share, and the WSJ — and to a lesser extent, The Sun — possess what long-time media investor Walter Annenberg called "essentiality," that is, its content is deemed essential by a certain group of people. The Wall Street Journal’s "essentiality" has waned over the years, yet by delivering news and editorial content that people want, the paper should continue to be a part of investors' and business people’s daily routines.

Dow Jones results for FY14 look worse than they were due to a decrease in revenue of $130m from the sale of the Dow Jones Local Media Group, which was sold for ~$200m in early FY14. Apart from this, revenues were down ~6% with Dow Jones Institutional having a larger negative impact on results with an approximate 14% decline. New pricing initiatives and the roll-out of DJX, a suite of institutional products, have not gone well, so the company is re-positioning the institutional business in an attempt to stem revenue declines. Dow Jones Institutional is approximately 25% of overall Dow Jones revenue, with the consumer business, primarily the WSJ, accounting for the remainder. The consumer business declined approximately 4.5% in FY14. The WSJ slightly increased circulation revenue due to price increases but saw a decline in advertising revenue.

News Australia has struggled through a weak print advertising market in Australia, as well as adverse currency changes as the AUD has weakened over 20% relative to the USD since 2011. In local currency, News Australia saw revenues decline 8% in FY14 and 15% in FY13. News Australia has some hidden assets, namely taste.com.au, a food and recipe site; kidspot.com.au, a parenting site acquired June 2011 for $50m; a 50% stake in careerone.com.au, a JV with Monster.com; and a 50% stake in carsguide.com.au, a JV with numerous car dealers.

News UK revenue has been relatively flat in local currency since FY12, but experienced favorable currency changes in FY14, resulting in an overall ~5.5% revenue increase from FY12 to FY14. The Sun launched a Sunday edition February 2012 and has grown its digital subscriber base, having had success with the introduction of a paywall. Costs related to the hacking scandals are included in the Corporate segment instead of being allocated to News UK.

There are not great comparables for this business. No other newspaper company has the global reach, strong market share, and institutional and consumer marketing assets. Looking at other publishers can be instructive, however, as all are facing the same challenges. The New York Times Company (NYT) trades at 8x adjusted EBITDA. The recent Tribune Publishing spin-off (TPUB) trades around 4x EBITDA, after deducting the estimated value of its non-core assets. Another recent spin is Time Inc. (TIME), the magazine publisher, which trades for 7x EBITDA. Valuing the News & Information segment at 7x free cash flow (after deducting its share of corporate overhead) equates to approximately 4x EBITDA and is in the ballpark of its publishing company peers. This gives the segment a value of $2.22bn, or $3.82 per share.

Education

News Corp, through acquisitions, software development and cash losses, has invested ~$925 million in Amplify's suite of education products through 12/31/14. Amplify is headed by Joel Klein, the former Chancellor of New York City Schools. The business consists of three segments: tablets, digital curriculum (developed around the new Common Core standards) and data and analytics. Amplify is predicated on the idea that with the advent of the Common Core standards, school districts across the country will be re-examining their curriculum needs and that a new entrant with a technology-forward curriculum developed specifically around these standards has a good chance at taking share. The overall story here makes sense, but it will come down to how good the curriculum is and how successful the sales force is at articulating the curriculum's advantages. Thus far, Amplify has only developed a middle school language arts curriculum, so it is too soon to foretell its odds of success. In valuing Amplify at zero, I am assuming that if the curriculum does not gain success in the next few years, News Corp will cease continued development of this business. How long this takes though will depend, in part, on how emotionally attached Murdoch becomes to it. Losses have accelerated at Amplify as more resources are dedicated to the roll-out of the curriculum products. EBITDA loss was ($193) in FY14, up from ($141) in FY13.

Corporate

Corporate overhead, apart from UK Newspaper matters, was $169m in FY14 and $156m in FY13. Management at the spin-off presentation guided to ~$150m in overhead costs with an additional $20m going to the corporate Strategy and Creative Group whose goal is to identify new products and services across the range of businesses to increase revenues and profitability and to target and assess potential acquisitions and investments

At 6/30/14, News Corp had $1.1bn of NOL carryforwards, including $213m in Australia and $509m in the UK, both of which do not expire. There is a $350m U.S. deferred tax asset that came about in the separation from FOX. In addition to NOL carryforwards, News Corp has $2.3bn and $2.1bn of capital loss carryforwards in Australia and the UK. respectively. Its cash is all held in US other than $467m held by foreign subsidiaries as of 12/31/14.

Costs related to "U.K. Newspaper Matters" were $72m in FY14 and $183m in FY13. These are the legal and other costs related to the phone hacking scandal in the U.K. Some costs have been and will be paid by 21st Century Fox, but net of these total U.K. Newspaper Matters costs have been $470m from 6/30/10-6/30/14. News Corp has accrued a $44m liability for civil claims, net of the amount indemnified by 21st Century Fox.

Cash at 12/31/14 was $1.9bn and investments, not including the Foxtel subordinated note, the value of which is included in the Foxtel valuation, were $321m. News Corp is debt free but does have a $273m pension and post-retirement liability.

Move, an online real estate company that competes against Zillow and Trulia in the U.S., was acquired by News Corp and REA Group November 2014, with News Corp acquiring 80% and REA Group the remainder. News Corp contributed $750m including net debt assumed of $20m, and REA Group $200m. Move has an exclusive relationship with the National Association of Realtors and runs realtor.com. It also owns ListHub, which aggregates and syndicates MLS data to hundreds of websites (including to Zillow/Trulia until next month). The entire online real estate advertising industry trades at rich multiples — and Move is no exception. On 2013 revenue and EBITDA, the purchase price was 4.2x and 53x, respectively. I value Move at News Corp's purchase price, recognizing that it was an expensive acquisition on trailing numbers but it is an area News Corp understands and has strong tailwinds behind it.

Conclusion

News Corp is a unique collection of assets selling at a meaningful discount to its sum-of-the-parts value. The newspaper business will not return to its former glory, although News Corp has been effective at monetizing content by employing paywalls and exploiting the pricing power properties like The Wall Street Journal possess. The non-newspaper assets are worth more than the entire company on a standalone basis, have been growing revenue and EBITDA in the double-digits, have strong market positions and generate a lot of cash each year.

Rupert Murdoch at times has allowed the animal spirits to get the best of him, but he has created enormous value for shareholders over the years. News Corp has a good base of assets which will continue to grow and a great balance sheet with a lot of cash. At $16.65 per share, appreciating to fair value would be a return of 30-50%.

Risks

(1) Recession in Australia, which is heavily dependent on commodity exports to China, leading to cord cutting, a depressed real estate market, and currency devaluation — ~55% of News Corp's economic EBITDA is in Australian Dollars

(2) Continued investment in Amplify that isn't profitable

(3) Newspapers lacking essentiality or a "local" voice not being able to monetize content effectively as the company continues to transition from print to digital

(4) Regulatory issues from the U.K. phone hacking scandal

(5) Murdoch squandering the cash balance by doing silly deals for trophy assets (though somewhat de-risked in the near-term by the TPUB spin) or pursuing assets outside of the company's core competence (e.g., education technology).

With a margin of safety in the price and a group of businesses with a number of positive attributes, there is good downside protection but the margin of safety can be eroded by capital misallocation and economic circumstances.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

Continued growth of non-News & Information businesses

Stabilization of News & Information

Accretive use of $2bn cash balance

| show sort by |