| 2017 | 2018 | ||||||

| Price: | 1.47 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 50 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 74 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 130 | EBIT | 0 | 0 | |||

| TEV (in $M): | 203 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

Description

Noranda Income Fund (NIF.UN-T)

I have literally waited for 3 years for this opportunity to present itself. With another income vehicle paying no distributions, the dislocation is sufficiently severe that I believe downside is limited and the upside, while uncertain, is substantial. In other words, modifying a popular phrase, “heads I win, tails I don’t lose”

My investment thesis boils down to this:

-

NIF’s balance sheet currently has C$2.50 per unit in net working capital while its land real estate value likely more than covers its environmental liabilities in a liquidation scenario. Downside is protected with any reasonable assumptions around balance sheet haircuts and/or near-term cash burn.

-

Zinc treatment charges are at or close to cycle trough and NIF is one of three remaining zinc smelters in North America of scale. At a mid-cycle treatment charge estimate, NIF fair value is close to C$3.50.

-

Opportunity exists because: a) complete distribution cut led to forced selling from income oriented investors, b) fear over cash burn from current year low treatment charge, c) facility currently on strike, d) market is inefficient on NIF

-

Glencore is a major unitholder and manager for NIF. While interests may not be perfectly aligned, it is important to note: a) Xstrata (prior to Glencore/Xstrata merger) attempted to take out NIF at $3.90 last time zinc treatment charges troughed, b) Glencore trading operations requires vertical integration and owning smelters to make aggressive bets, c) recent Trevali transaction highly incentivizes Glencore to direct more zinc to NIF for processing.

Background

NIF was previously written up by LA2NYC in 2015 and provides a good background to the story (https://www.valueinvestorsclub.com/idea/Noranda_Income_Fund/136302)

NIF is a one asset business – it runs a zinc smelter in Quebec, Canada that turns mined zinc concentrate into zinc end products primarily for stainless steel applications in automotive and construction uses.

(http://www.norandaincomefund.com/about/operations.html)

Essentially, NIF was created back in 2002 during the income trust days where it was a tax advantaged vehicle much like U.S. MLPs. To help juice NIF’s valuation, the sponsor (originally Noranda, then Falconbridge, then Xstrata, now Glencore) put in place a 15 year Supply and Processing Agreement (SPA) guaranteeing both the supply of zinc concentrate (need about 2 tons concentrate per ton of refined zinc) and a processing fee of C$0.35 per lb (or C$775/tonne) subject to a 1% per year escalator. By creating an income vehicle with fairly predictable distributions, NIF initially traded in the $12 range before the financial crisis came along and NIF opted to cut distributions to repay debt. Coming out of the financial crisis and coinciding with a drop in spot treatment charges to a trough of US$100/tonne in 2010, Xstrata made a bid for NIF initially at $3.40 then $3.90 before withdrawing its bid due to opposition from some activist investors including West Face Capital.

Heading into the expiry of the SPA, negative (from a smelter’s perspective) zinc market developments led to NIF cutting and ultimately eliminating its distribution at the end of January 2017 (there are 50 mln units outstanding, Glencore holds 12.5 mln subordinated units and the float is 37.5 mln priority units. Glencore has not been receiving distributions and is in arrears for about $34.5 mln in distributions should they resume at a high enough level). Just when NIF would soon transition to market zinc treatment charges (although Glencore is securing the supply of concentrate for 1 more year), the following negative developments transpired:

-

Zinc supply deficit due to mine closures, leading to concerns whether NIF could source enough input zinc concentrate

-

Combined with a zinc price spike, smelters’ bargaining position diminished leading to a precipitous drop in spot treatment charges

-

Workers at NIF went on strike

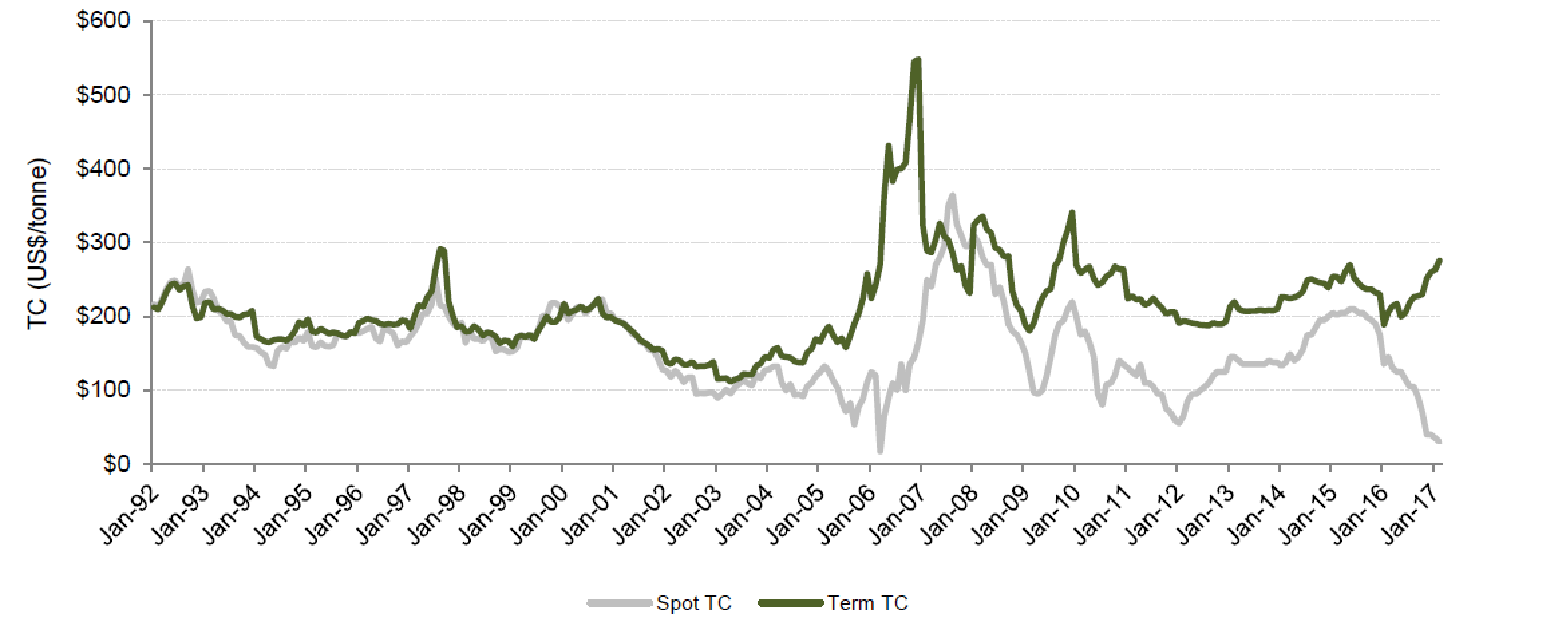

The following is a 25 year historical zinc treatment charge graph. Note while spot treatment charges are particularly volatile, smelters generally realize “term” or benchmark treatment charges as these are typically negotiated with zinc producers. Short primer on zinc smelting: http://www.nyrstar.com/investors/en/Nyr_Documents/English/zincleadsmelting.pdf

Source: TD Securities

Before we get into valuation, I believe there are 3 key drivers in play here worth discussing: Treatment Charges, Cost Structure, Zinc Supply

Zinc Treatment Charges

There are many macro factors here in play between zinc pricing, supply/demand and zinc treatment charges, and the US$/C$ exchange rate – none of which I can get precisely right.

The rudimentary commentary would be zinc prices had been relatively low in the past few years and marginal producers have finally cut production, leading now to a zinc price spike and a lack of zinc concentrate supply for smelters – resulting in a precipitous drop in treatment charges. To make matters worse, China has excess smelting capacity that is also hurting treatment charges.

However, I believe all we need to know is the implied $75/t treatment charge NIF locked in for 2017 likely represents a trough (negotiated at a time when spot charges went sub $50/t late 2016)

There are various ways to guess what a normal treatment charge should be but I’ll just provide some observations:

-

The LT average treatment charge is about US$250/t as per the chart earlier in the write-up

-

NIF itself suggested in a normal treatment charge (including paying only 85% of contained zinc vs. 96%*) should be 19-22% of the zinc price as per the 4Q14 conference call transcript

-

North American end users need NIF which provides about 1/3 of the product needed in the region. Like oil refineries, they are not building any more zinc smelters here and NIF already has regional and scale benefits. In fact, there are reports customers are scrambling to secure supply (article provided at end of write-up)

-

Teck Resources most recently settled zinc treatment charge of US$172/t with Korea Zinc, but without price escalator/de-escalators (https://www.metalbulletin.com/Article/3673432/EXCLUSIVE-Teck-Korea-Zinc-agree-annual-concentrate-supply-deal-at-172tsources.html)

*There is a slight nuance as NIF transitions from a fixed processing fee to market treatment charges. Basically, NIF had a relatively high processing fee but had to pay for 96% of contained zinc. With market treatment charges, NIF will only pay for 85% contained metal, so anything about 85% they produce, they can sell for profit. So while market treatment charges will be a lot lower, NIF gets essentially a ~10% of the zinc price per tonne as a kicker.

In coming up with a LT zinc treatment charge assumption, I went with US$200/t which is the approximate average between 1992-2000 to cancel out the influence of the Chinese commodity boom/bubble risk. I don’t believe this is an aggressive assumption considering the latest data point is already US$172/t.

Cost Structure

The two key components of NIF’s production costs are labour (about 1/3 of costs) and electricity (another 1/3). With the transition to market treatment terms, I am guessing production costs could adjust downward by 5-10% (up to debate) because:

-

Labour costs were down high single digits yr/yr during the financial crisis

-

The current labour strike at NIF is actually an opportunity to right size costs, especially when running the smelter would generate breakeven EBITDA anyway

-

Despite unionized employees being on strike, NIF is still managing to operate at 60% utilization!

-

NIF has received approval from Quebec government in receiving electricity rebates. The basic premise is Quebec hydro power is cheap and the left leaning government will offer generous rebates to keep the smelter running (http://www.usw.ca/news/media-centre/articles/2017/quebec-must-demand-investments-and-greater-transparency-from-noranda-income-fund)

Zinc Concentrate Supply

NIF requires approximately 520,000 to 530,000 t of zinc concentrate to produce 270,000 t of refined zinc. There is concern that with Glencore taking out 400,000 to 500,000 t of zinc production out of the market in the past few years, there is not enough feed for NIF.

While I can’t predict the precise flow of zinc concentrate, I can offer the following observations

-

Glencore itself recent did a transaction with Trevali mining where Glencore took a 25% equity stake in Trevali. While I don’t know (if any) zinc concentrate was already going to NIF, you can be sure Glencore will now direct more zinc concentrate to NIF. For reference, Trevali is expected to produce 180,000 t, which 25% owner Glencore is highly likely to direct a lot of that to 25% owned NIF. (https://www.vmbl.ca/portal/documents/49798/1295520/Trevali.pdf/f7250cbe-31ba-42a7-9ac2-85724753c2b9)

-

Teck Resources produces more zinc concentrate than its zinc refining capacity in Trail, Canada. They suggested they do direct material to NIF but did not disclose the exact amount. Perhaps there is something like 50,000 excess concentrate tonnes. (http://www.teck.com/products/zinc/)

-

NIF has spent capital to accept zinc concentrate from Europe. Lundin mining recently announced its intention to bring on an additional 100,000 t of zinc production (http://www.lundinmining.com/i/pdf/2017-05-neves-corvo-cp.pdf) – in essence we are seeing a supply response, as we always do in the commodity space.

Downside Valuation – We are Already There

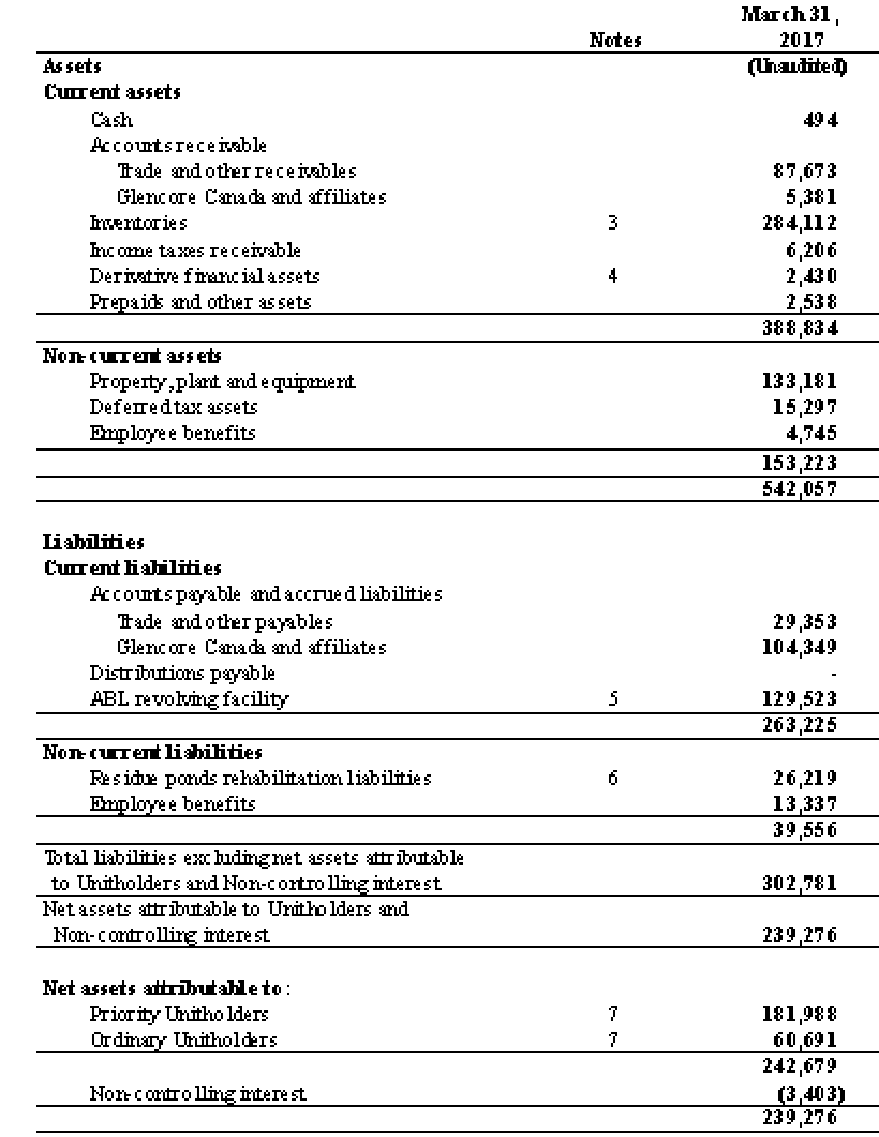

With the unit price this low, I believe the downside is well protected with ~ C$2.50 in net working capital. For a commodity company, the net working capital number is more believable as inventories, for instance, are not subject to obsolescence unlike a fashion retailer. With units trading at < C$1.50, any conservative haircut can be applied and our downside is still well protected.

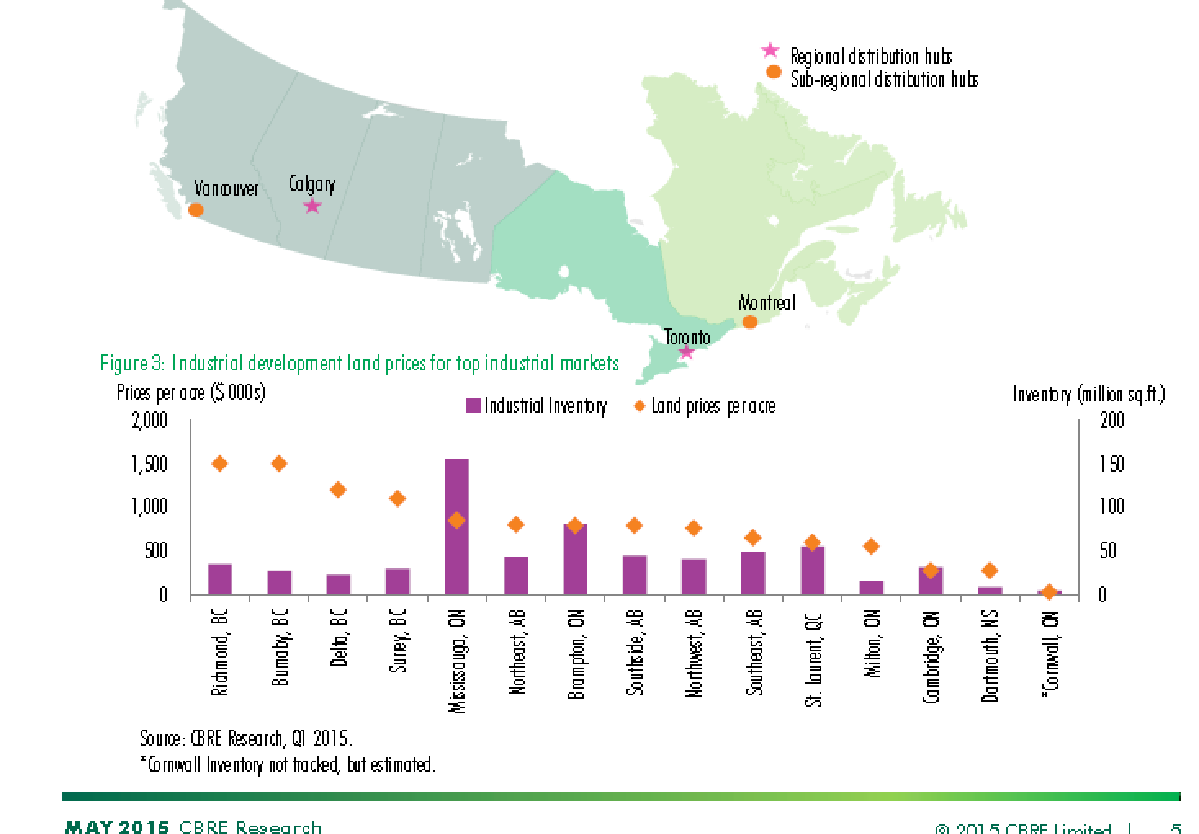

What about non-current assets and liabilities? Here I am making a broad judgement call that NIF’s 866 acres of industrial land would cover non-current liabilities (mainly environmental). Keep in mind on the March 11, 2015 conference call, NIF confirmed that its industrial land is on its books for $3.1 mln marked at cost from 1955 (62 years ago). Being located less than an hour from Montreal, I’m guessing the industrial site is worth a good amount:

A CBRE survey of Canadian industrial sites suggests high quality industrial land close to Montreal go for $500,000 per acre. We just need NIF’s industrial land to be worth $50,000 per acre to cover all non-current liabilities.

Normalized Valuation

As laid out earlier in the write-up, I conservatively estimate treatment charges could normalize at US$200/t with lots of uncertainty around when that might happen. My DCF value for NIF is ~C$3.40, more than a double from here.

An even easier way to look at it is this: At US$200/t normalized treatment charge, I get about C$60 mln in EBITDA and ~C$30 mln in FCF or C$0.60 per unit. If it takes about 3 years to get there, with discounting, cash burn and netting out the C$34.5 mln in dividends Glencore didn’t receive in its subordinated units, we get to about C$3.50 per unit as well. This broadly jives with the latest sensitivity table provided by NIF:

Why does this opportunity exist?

With such an asymmetric upside/downside, I think the opportunity exists because:

-

Forced Selling From Distribution Cut – NIF cut its distribution to zero at the end of January. NIF has 50 units outstanding. 12.5 mln held by Glencore and the rest by public unitholders. I see institutional investors own about 4 mln units so there is likely a high retail component here. For instance, if income oriented retail investors held 10 mln units, with 100-200K average daily volume, it would take a while before these investors could completely exit.

-

The Market is Inefficient on NIF – It may seem to be a stretch that the market isn’t paying attention to NIF but the fact pattern is this: NIF traded in the $2.50 range in the 2H16 despite anyone who googled “zinc treatment charges” could see treatment charges were dropping very sharply. In fact, in December there was an article suggesting Chinese TCs were headed to zero, yet NIF actually traded higher out of December 2016 into January 2017. But once NIF cut its distribution at the end of January, NIF tumbled 40% as if the market suddenly realized treatment charges have dropped significantly.

http://www.reuters.com/article/us-metals-zinc-processing-idUSKCN10T0U6

-

Management/Glencore Purposely Cagey – Possibly due to its predecessor Xstrata’s failed bid for NIF, current management/Glencore appears almost purposely overly conservative, especially with their language about NIF whether it can remain a going concern. There are many possible motivations for this kind of behavior including: a) Glencore may be looking at taking out NIF at an opportunistic price, especially after cutting the distribution, b) Glencore may want to paint a dire picture to get a better bargaining position in terms of electricity rebates and with the labour union and c) Glencore wants to create an impression zinc markets will remain tight for a long time, especially in light of themselves withdrawing ~ 500,000 tonnes of production from market.

As an aside, based on the recent unitholder proxy votes, it looks like the unitholder base may have turned over a bit – the possibility of an activist investor or at least an investor who would hold management to the fire exists as trustees had 6-13% votes withheld against them most recently.

At the AGM, there were 6 holders of Priority Units and Special Fund Units ("Units") of the Fund represented in person or by proxy, holding 19,669,176 Units and representing 39.35% of the Fund's 49,989,975 issued and outstanding Units. The results of the vote for the election of trustees was as follows:

|

Class |

Nominee |

Votes For |

% Proxy |

Votes Withheld |

% Proxy |

|

Priority and Special Units |

Chris Eskdale |

17,106,054 |

86.85 |

2,590,808 |

13.15 |

|

Yvan Jost |

18,011,040 |

91.44 |

1,685,822 |

8.56 |

|

|

Anthony P.L. Lloyd |

18,449,105 |

93.67 |

1,247,757 |

6.33 |

|

|

Jean Pierre Ouellet |

18,464,627 |

93.74 |

1,232,235 |

6.26 |

|

|

François R. Roy |

18,265,823 |

92.73 |

1,431,039 |

7.27 |

|

|

Barry Tissenbaum |

18,388,027 |

93.36 |

1,308,835 |

6.64 |

|

|

Dirk Vollrath |

18,025,630 |

91.52 |

1,671,232 |

8.48 |

The Short Case

I have to admit I was a bit surprised to learn there are investor(s) who are short NIF. My understanding is the short case boils down to 2 things:

-

Cash burn will be significant in the current environment with $0 EBITDA generation and still incurring meaningful capex ($25 mln+) and interest expenses ($5 mln+)

-

The environmental liability will end up wiping out the net working capital amount

As Charlie Munger was once quoted in saying:

“… Ask yourself what are the arguments on the other side.

It’s bad to have an opinion you’re proud of if you can’t state the

arguments for the other side better than your opponents.

This is a great mental discipline.”

Having spent considerable time re-thinking the short thesis, I actually got more comfortable with NIF as a long. Specifically on the cash burn, I would highlight:

-

The low TC environment is unlikely permanent as discussed previously, and recent indications suggest treatment charges have already moved higher.

-

NIF already provided commentary it will defer spending capex, especially given the current strike (what better time to defer capex and endure a strike when the TC environment is terrible)

-

Glencore owns 25% of NIF and would not want to see their equity wiped out.

-

Glencore also has a strategic reason for controlling NIF. Glencore generates over 15% of its EBITDA from its “marketing” division – which is really a proprietary trading operation that takes advantage of pricing discrepancies between different geographies and commodity type (i.e. concentrate vs. refined). My understanding is Glencore tends to be aggressive in its proprietary metals trading (accounting for over half of the group’s 2016 EBIT), and to do so, Glencore needs to take advantage of its integrated supply chain – meaning the need to own mines and smelters. That way, if Glencore were offside being long or short, they can always “cover” with physical material instead of being subject to a squeeze.

As for the environmental liability, it could be more but I would consider:

-

The rehabilitation liabilities on the balance sheet is only discounted at 1.96%. So NIF isn’t using a 8-10% discount rate assuming the liabilities will be incurred decades from now.

-

It seems like funding levels provided for various site clean-ups in the ASARCO bankruptcy is not order of magnitude different from NIF’s environmental liability on its balance sheet. In fact, NIF’s processing facility was built in 1963, relatively new compared to some of the cases in the ASARCO example (meaning contamination should be less). See here: https://www.epa.gov/enforcement/case-summary-epa-funded-sites-and-communities-asarco-bankruptcy-settlement

Disclaimer: The write-up is only intended for VIC members and not for dissemination (especially to the issuer).

Not investment advice, no warranties expressed or implied, subject to material and potentially egregious errors. Basically, do your own homework.

Steel mills seek CGG strip amid NIF strike NIF_u.TO - American Metal Market

26-Mar-2017 10:55:43 PM

NEW YORK Large U.S. steel mills have been asking various zinc alloy companies to produce the continuous galvanizing grade (CGG) strip jumbos that they require in case the ongoing strike at Noranda Income Fund's (NIF's) zinc-processing facility continues.

The strike at the facility in Salaberry-de-Valleyfield, Quebec, now entering its sixth week, has caused a serious dearth of material and has led to U.S. special-high-grade premiums to reach 8.5 to 9.5 cents per pound, up from 6 to 6.5 cents per pound the week the strike was initiated.

"We were approached by some people who asked if we could make CGG if they ran into trouble," one die caster told AMM .

"There are a lot of inquiries going around," a second die caster, who reported being approached by representatives from two or three mills, agreed.

Toronto-based NIF produces about one-third of the supply to North America, according to one market source. The other leading producers are Vancouver, British Columbia-based Teck Resources Ltd., Mexico City-based Industrias Peñoles SAB de CV and Toronto-based HudBay Minerals Inc.

"The zinc we produce that would be suitable for steel production is long sold by contract, and we don't produce a significant amount in the specific form (shape) required for the sector," a HudBay spokesman told AMM via email.

"We are operating at full rates for jumbo and slab production, and (are) fully committed under contractual agreements for our Trail (operations) production," a Teck spokesman said.

Peñoles did not immediately respond to AMM 's request for comment.

NIF announced in early March that the company had resumed partial zinc production, although the president of United Steelworkers union Local 6486 estimated that the facility could only produce at one-quarter of total capacity without the striking workers.

The first die caster told the steel mills that his company was able to deliver CGG, but not in the form of strip jumbo because the mill lacks the necessary molds. "We can always make alloys, but we can't make the precise ones that they want," he said.

Those steel mills were "unsure" about the material being in a different form and "didn't come back to us," he added.

Steel mills prefer strip jumbo ingots to slabs because they're safer to handle and reduce melting losses, and their size discourages theft more than readily portable slabs.

The second die caster's company has the necessary molds to make the slabs, but producing the requested 1,000 tonnes per month would be "outrageous." That amount would lead to a "serious upcharge" because a lot of manual labor would be required to make that amount.

"We gave them our prices and they shied away, said they were ridiculous," the second die caster said.

He hasn't been approached since, but, "if the strike is prolonged, they might come back," he said. "This is what happens when you get in bed with one guy. You get drawn into (thinking) they'll never go on strike."

To access additional CGG jumbo production, steel mills would have to resort to other primary zinc producers that are largely located outside of North America, the Teck spokesman said.

But while mills could go overseas, even if offshore producers "had the capacity and desire to produce the wide range of CGG required," it's unlikely that the material would be made and shipped to the United States in less than two months, one market source told AMM .

NIF's processing facility is the second-largest zinc refinery in North America and the largest in eastern North America, according to the company's website.

A reconciliation between unionized workers at NIF and company management is unlikely in the near term, as both sides refused concessions during a meeting in early March and have no plans to schedule another meeting in the future.

I and/or others I advise do not hold a material investment in the issuer's securities.

Catalyst

Higher NIF treatment charge for 2018

Improved operating cost structure

Miners produce more zinc in light of high prices

| show sort by |