| 2023 | 2024 | ||||||

| Price: | 4.65 | EPS | .053 | .090 | |||

| Shares Out. (in M): | 4,423 | P/E | 11.23 | 6.61 | |||

| Market Cap (in $M): | 2,632 | P/FCF | 8.04 | 4.96 | |||

| Net Debt (in $M): | 368 | EBIT | 274 | 456 | |||

| TEV (in $M): | 2,999 | TEV/EBIT | 10.95 | 6.58 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- None found

- BETA

- NAGACORP LTD (NGCRY) 3918:HK 04/24/2023

Description

Summary:

In a volatile market with an uncertain H2’23, Nagacorp’s 7.95 07/06/24 bonds at 95 offer a 14% to 20% return over the next 6 – 12 months with minimal market risk.

The Hong Kong listed Cambodian gaming company has <1x forward net leverage and a $2.6bn market cap. Just over two thirds of the equity is owned by multi-billionaire founder Dr Chen, who also owns $45MM bonds. The company recently discussed refinancing plans that entail repaying $200-300MM of the $470MM bonds and refinancing the remainder at a UBS gaming industry conference. Cash on hand is $166MM with est 2023 FCF of $300MM+. The bonds are guaranteed by key subsidiaries. We expect greater details on the upcoming refinancing on an upcoming mid-July interim update. The bond’s current YTM is 14%, calling the bond on 3/31/24 at the call price of 101.988 amounts to a 20% return.

Company:

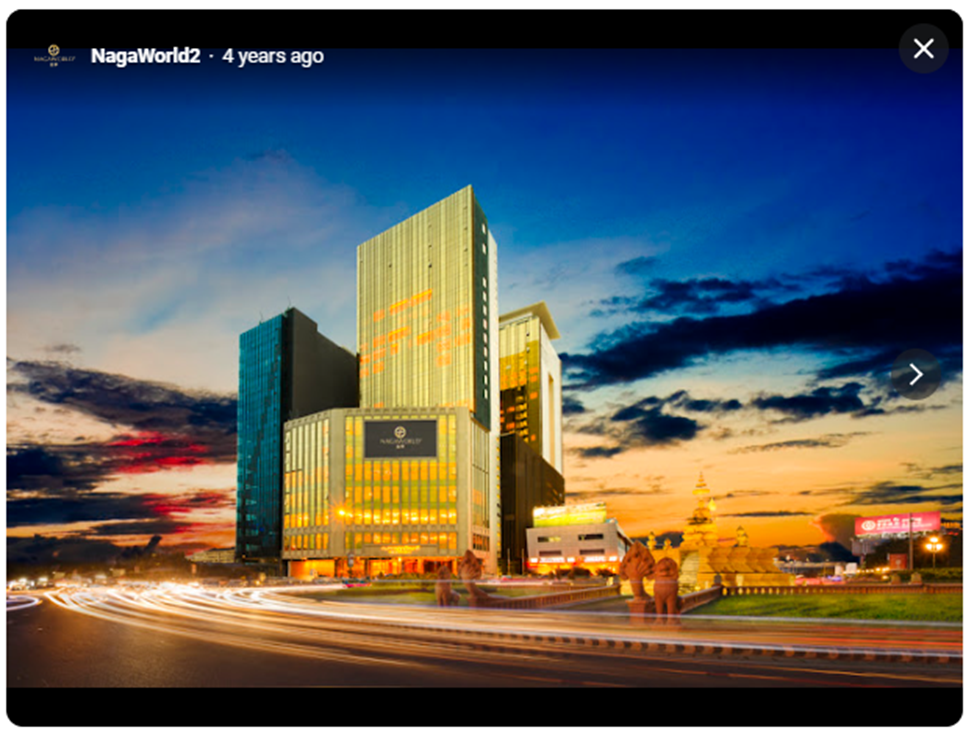

NagaCorp Ltd. (NagaCorp or the Company) was incorporated in the Cayman Islands in 2003 and listed on the Hong Kong Stock Exchange (SEHK: 3918) in 2006. The company currently has a $2.6bn market cap. It owns and manages NagaWorld, the largest integrated casino and hotel complex in Phnom Penh, Cambodia that consists of Naga1 and Naga2 with Naga3 under construction. It is the largest hotel, gaming and leisure operator in Cambodia. The company is a regulated monopoly with exclusive right to operate casinos within a 200km radius of Phnom Penh until 2045. Its casino license lasts until 2065.

NagaCorp was founded by Tan Sri Dr. Chen Lip Keong (Dr Chen), its chief executive officer and largest shareholder with a 69% stake in the company and ownership of $45MM in bonds. Tan Sri Dr. Chen Lip Keong was ranked No. 9 on Forbes' list of Malaysia's 50 Richest in 2021 with a net worth of US$3.4 billion.

Other casinos are located in border towns such as Poipet, on the Cambodian/Thai border, and Bavet, along the Vietnamese border. Casinos are also being built in emerging tourist destinations such as Sihanoukville.

Naga 1

A casino and hotel resort spread over a total floor area of approximately 113,307 square meters which opened in December 2006 The facility is open twenty four hours a day and features ten restaurants, several bars and lounges, and a hotel with 525 guestrooms, spa, pool, and gym. Hotel amenities include a complimentary breakfast, tour assistance, wedding services, and event catering.

Naga 2

A casino and luxury hotel resort spread over a total floor area of approximately 108,764 square meters which opened in November 2017 which is adjacent to Naga 1. Naga 2 offers at Least 300 Gaming tables, 2,500 electronic gaming machines, exclusive premium gaming halls and gaming suites.

NagaCity Walk

An underground walkway which links Naga 1 and Naga 2 that opened in August 2016. NagaCity Walk is Phnom Penh’s first underground shopping center and offers duty-free shopping operated by China Duty Free Group – one of the largest duty-free operators in China.

Naga 3 Construction Paused

Piling work (the process of drilling foundations through the ground to provide more structural strength to the weak soil underneath) for Naga 3 was at 96% completion at FYE2022 end. To date $800MM has been spent on the project, half by Nagacorp and half by Tan Sri Dr. Chen Lip Keong and the project was recently paused.

Bond Structure:

The unsecured bonds are issued by NagaCorp Ltd, and unconditionally and irrevocably guaranteed by the major operating subsidiaries of NagaCorp.

The original bond debenture (June 24, 2020) listed the guarantors to the bonds as:

• NagaCorp (HK) Limited

• NAGAWORLD LIMITED (NWL)

• NagaCity Walk Limited (formerly known as TanSriChen (Citywalk) Inc.),

• Naga 2 Land Limited (formerly known as TanSriChen Inc.)

• Naga 3 Company Limited

On September 30 2020, a supplemental indenture added to the guarantors under the notes the gaming license holder: Ariston Sdn.Bhd. (Ariston, holds the casino license).

Capital Structure:

Creation value through the bonds at par based on actual 2022 results is 1.5x, on 2023 guidance is 1x.

NagaCorp bought back $70MM bonds in November 2022, reducing the remaining principal amount of the bond to $472MM, or $427MM excluding insider bond ownership of Dr Chen at $45MM.

Company Performance

The company generated $461MM of revenue and $245MM of EBITDA in 2022, a sharp rebound from the company’s COVID lows in 2021 of $226MM in revenue and $22MM of EBITDA. The 2022 rebound in earnings occurred without significant mainland Chinese tourists.

Mainland Chinese tourists can now return after border reopening as of Jan 8th 2023, resumption of outbound group tours to 20 countries (including Cambodia) occurred on Feb 6 2023. Management in their releases has been hopeful for the recovery of Chinese tourists, pointed to improvement in services and facilities (e.g., better F&B offerings, upgrading slot machines, etc.) to attract tourists.

The 2023 recovery to date remains lopsided. For Q1’23, while gross gaming revenue (GGR) was up 15% QoQ (37% of 1Q19), reported EBITDA of US$59MM was -5% q/q (47% of 1Q19), an annualized 1Q23 EBITDA is US$251MM (flat y/y, ~40% of 2019). The weaker than expected EBITDA was due to legacy COVID travel restrictions.

Cash Waterfall

The below scenario looks at various EBITDA estimates for 2023, interest and capex as well as a minimum $100MM of cash to be held at the company to run the business.

Capex of $150MM for 2023 was the prior expectation before Naga 3 was paused in June 2023 reducing expected 2023 development capex to $50MM or $75MM including maintenance capex.

Under the consensus case, over 70% of the bonds can be refinanced comfortably and the remainder rolled into a new facility. Taking a haircut, or the Moody’s 2023 case, suggests nearly half repaid. Even in the event the company is unable to grow EBITDA from 2022, nearly a third of the outstanding bonds can be refinanced with the remainder rolled over into a new facility, in this case leverage would be just over 1x. The bond matures on 07/06/24, leaving an entire ½ of 2024 if needed to generate cash to pay down the bond that is not included below. Even the June 2023 Moody’s downgrade to B3 due to refinancing risk listed the company has generating enough cash to fully meet the bond at maturity.

The company uses a gearing ratio for determining how much debt outstanding can be taken. The current ratio would allow an incremental $500MM of debt to be taken. Management has indicated a preference for debt financing over equity placement under the current market environment.

Recent Equity Performance:

Nagacorp’s equity has been under pressure YTD. Part of this is due to overall peer Macau gaming weakness. Other factors include an upcoming July 23rd election in Cambodia, and Chinese tourism below expectations. Chinese tourism is however well above 2022 results and overall tourism above expectations / 2022 results.

Refinance Timing:

Given Nagacorp will use 2023 FCF to pay down the bond, a base case is a bond refinance on 3/31/24 (20% IRR).

Given the call schedule, Naga may creative and issue a new bond with cash placed in escrow and use that cash in addition to cash on hand, to repay the bond at 100 on 07/06/24. This is the lowest IRR scenario (14%).

Tourism:

Overall YTD 2023 international tourism to Cambodia is well above 2022 levels.

The overall tourism recovery is performing stronger than expected, even with Chinese tourism up sharply from 2022 its lighter than expected. Cambodia was expecting 4MM in total tourists for 2023 and 1MM from China, overall tourists are tracking above that number while Chinese tourists are tacking below. This is why Cambodia’s tourism minister on June 15th urged China to introduce more direct flights from its cities to Cambodia. Chinese tourists are better than peer tourists as they have higher purchase power.

Disclosure:

At the time of publication, the author of this article and one or more of the author’s affiliates holds a position in NAGACL 7.95 07/06/24. This article expresses the opinions of the author. The author has no business relationship with any company whose stock or bond is mentioned in this article.

The author of this article and one or more of the author’s affiliates has a long position in the company covered herein and stands to realize gains in the event that the price of the bond increases. Following publication, the author and the author’s affiliates may transact in the securities of the company, and may be long, short or neutral at any time. The author of this report has obtained all information contained herein from public sources believed to be accurate and reliable. The author of this report makes no representation, express or implied, as to the accuracy, timeliness or completeness of any such information or with regard to the results to be obtained from its use. Any projections, forecasts and estimates contained in this report are necessarily speculative in nature and are based upon certain assumptions. Accordingly, any projections are only estimates and actual results will differ and may vary substantially from the projections presented. All expressions of opinion are subject to change without notice, and the author does not undertake to update or supplement this article or any of the information contained herein. This is not an offer to sell or a solicitation of an offer to buy any security.

I and/or others I advise do not hold a material investment in the issuer's securities.

Catalyst

Refinacing

| show sort by |