| 2016 | 2017 | ||||||

| Price: | 5.40 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 22 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 118 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 0 | EBIT | 0 | 0 | |||

| TEV (in $M): | 106 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- PRGX GLOBAL INC PRGX 12/27/2017

- PRGX GLOBAL INC PRGX 10/19/2015

- PRGX GLOBAL INC PRGX 12/05/2012

- PRG-Schultz Int PRGX 12/21/2003

- BETA

- ARCTIC GLACIER INCOME FUND AGUNF 11/18/2019

- VALEANT PHARMACEUTICALS INTL VRX. 05/12/2017

- First National Bank of Anchorage FBAK 04/18/2000

- FIRST ADVANTAGE CORP (FA) FA 09/22/2023

Description

Investment Highlights

Cheap

PRGX trades at 5x 2017 ebitda. In a world where nothing is cheap, this stands out.

Pricing Pressure Abating

PRGX’s only national competitor to its core business aggressively tried to take share in order to pretty itself up for a sale/IPO. Being public has now forced them to be disciplined on pricing.

Competitive Position Strengthening

PRGX has reinvested in its core business while its primary competitor has de-emphasized the business. The competitor publicly stated they are “harvesting the business for cash.” It only represents 15% of their total revenue, but with the other 85% growing 30%, it really only represents about 3% of the market value. Simply put, its language, actions and incentives indicate it is not a priority. Beyond their only national competitor, there are only a handful of regional players, and they themselves indicate the switching costs are just too high for them to win away national retailers.

Board & Insiders Buying

PRGX has bought back 25% of the shares in the last 2 years and InsiderScore ranks PRGX in the top 3% of all companies in terms of insider activity. Though PRGX isn’t “harvesting the business for cash,” the cash flows are ample enough to effectively be taking the company private… publicly. Consider it a public market LBO without the leverage. Meanwhile, managers, board members and 13D&G holders have all been notable buyers over the last 2 years.

Consistency of the Business and Downside Protection

· Recurring Revenue

· Aggressive Buyback Program

· Activist Involvement

PRGX’s customer retention rate is 99% and most of their larger clients have been with them for decades. Recoveries, while different each year, are perpetual and yields tend to be fairly consistent. PRGX also becomes a more valuable partner in periods of economic slowdown as their recoveries become a bigger percentage of earnings. Yields on recoveries can also increase as businesses tend to offer more one-off promotions in an effort to move product. These help to dampen the effect of a slowdown in the number of transactions that come with a downturn.

On the stock side, the company has been opportunistic and aggressive in buying back shares when the stock is down. Activist involvement, though not a guarantor of a floor, also protects against poor capital allocation decisions and always presents the threat of a sale if the business isn’t managed well.

Growth Prospects are a Call Option

At 5x ebitda, the investments made in growth are pure call options. If the growth comes, the stock will most certainly re-rate to a much higher multiple. If investments don’t bear fruit, ebitda will increase and uncertainty around the business will likely decline as the company pares back growth efforts.

Underfollowed and Misunderstood

Not unlike most $100mm enterprise value companies, the shares are underfollowed. Only two smaller sell-side firms follow the name. Unlike other microcaps, however, I think PRGX is also living down a dubious reputation built under the former CEO. Just about every investor I speak to that is familiar with PRGX recollects the company under Romil Bahl (2009-2013), but hasn’t paid much attention to it since. The former CEO’s “enthusiasm” for entering new markets and driving accelerated growth pushed the stock to its highs ($8.85) in August of 2012. Needless to say, results did not live up to the hype, and the stock along with profits cratered under a bloated infrastructure. New management cut costs, refocused their efforts on the core business and pared back the growth avenues to a selected few that they think have the best economics. They have not done much marketing, instead taking a more nose to the grindstone mentality.

Business Turning the Corner

Management is now beginning to see the fruits of their refocused efforts and better competitive position. North American retail recovery audit has returned to growth, International seems to be moving past some client disruptions and the pipeline in their newer businesses is growing to a level where it could finally become a meaningful addition.

History

It amazes me that three years after Bahl’s departure, investors’ perception of the company is still tied to his strategy and tenure. PRGX had 5 or more sell side firms covering the stock at the time. Coupled with the CEO having a penchant for telling an exciting growth story, it was marketed well but unfortunately burned more than a few investors.

Here are some of my notes from a meeting I had with Romil back in September 2012:

“I have an uneasy feeling about the CEO. Admittedly, he has a quiet calm about him that instills confidence. I think his consulting background also gives him a polished air. But I fear he is promising results that he can’t deliver. He is long on high level ideas but seems to be underestimating executional challenges. There’s too much strategic macro (most of his presentation was focused on how much his strategy expanded the total addressable market) and too little strategic micro (who is the competition, what is our edge and how can we take share?). The answer to the last two questions seems to be “we have data,” but it doesn’t seem to go much deeper than that. In my 1 on 1 session, he was all too quick to throw various heads under the bus. It feels like he is insulating himself from blame (“I expanded the market and gave the salesforce a $30B playground to play in, why couldn’t they get a sliver of that”).

Finally, something that rubs me the wrong way is that I received an “investor packet” that only included a CD of the CEO ringing the Nasdaq morning bell. I can understand including that amidst SEC filings and presentations, but it was a single CD with a video of the CEO being introduced, being told what a great job he has done, and then him saying a few words before he rang the bell. It seemed self-congratulatory and possibly telling for this first time CEO.”

Now, I recognize the irony in me calling the CEO self-congratulatory as I seemingly congratulate myself on calling this one correctly. That’s not my intent. Believe me, I’ve had my share of whiffs. I do think the best way to shake investors’ past perception of the company though is to provide a contrast in management teams and their strategic visions. Whereas the past CEO was a big picture guy who loved to talk about the total addressable market, this CEO and CFO are in the weeds operational and finance guys. Whereas the past team had grand visions of becoming a large Medicare recovery audit contractor, developing a large healthcare practice, and using data in numerous ways to build a large consulting and advisory business, the new team has exited non-core businesses, returned its focus to its core, while selectively cultivating a couple of prospects for growth. Whereas the last team spent pretty liberally to expand into other practices, this team quickly cut costs to get margins back toward historical levels. And finally, whereas the past team was promotional and seemed to enjoy being in the spotlight, this team’s fault might be not marketing to investors enough.

The Business

PRGX breaks its business into 3 segments:

· Recovery Audit Services – Americas (70% of Rev)

· Recovery Audit Services - Europe/Asia-Pacific (25% of Rev)

· Adjacent Services (5% of Rev)

Recovery Audit mines clients’ purchasing data to retroactively identify payment errors made to third party suppliers. Although the majority of transactions are processed correctly, PRGX recovers almost 1% of the overall spend. With PRGX processing over a $1.2 trillion in client spending, this can result in meaningful dollars for organizations. These errors can result from discounts, allowances, complex vendor rebate arrangements, duplicate payments, fluctuating prices, shipping discrepancies, and one-off contract stipulations. The data and agreements can reside in purchasing, payment, receiving, and POS databases as well as in written and online communications such as contracts and emails.

Recovery audit can further be segmented into retail recovery audit, commercial recovery audit and contract compliance. Retail recovery audit is the most mature of the businesses. PRGX works for 75% of the top 20 global retailers and has been servicing a number of them for decades. Enhancements to accounts payable software, particularly large enterprise software solutions used by many large companies, have reduced the extent to which these companies make simple disbursement errors. However, the introduction of creative vendor discount programs, complex pricing arrangements and activity based incentives has led to an increase in auditable transactions and potential sources of error. A typical retailer will purchase close to 50k separate SKU’s. While retailers try to learn from their mistakes, the majority of the errors are just too costly to permanently fix internally. PRGX is typically working with 6 petabytes of live client data at any one point, accessed from multiple systems throughout the organization. One competitor executive told me building an internal system to recover $1mm in savings could cost $20mm to develop and implement, but then need to be updated with every divisional ERP upgrade. So PRGX’s recoveries can be a meaningful part of retailers’ P&L, making the difference between missing and beating numbers.

Commercial recovery audit is just the industry’s term for recovery audit work done for industries other than retail and healthcare. The industries that PRGX serves include automotive, energy, financial services, manufacturing, pharmaceutical, technology, transportation and utilities. The business is identical to retail recovery except that supplier arrangements are typically less complex, but involve higher dollar volumes. The business is also less mature as it has been growing 5-10%.

Contract compliance is the fastest growing of the recovery audit businesses. As the name implies, contract compliance audits suppliers' billings against the original contract. PRGX has found contract compliance to be rife with opportunities because the majority of suppliers' bills are self-reported. PRGX audits everything from labor rates and overtime to meal allowances and rental equipment hours. Here is a description of some of the contract compliance problems companies face from an industry trade rag.

"Contracts are on people’s desktops, they are on servers, they are even in informal – but no less legally binding – email exchanges. But they are not accessible in a single place and nobody really knows what the company’s actual or contingent liabilities are. The problem is no less challenging today, even though corporate information systems have improved considerably over the last 15 years. That’s because the nature of the problem has evolved: now, often the information procurement needs to determine if suppliers are overcharging actually resides solely within the suppliers themselves. If a supplier offers products on a cost-plus basis of say, 10% and advises the customer that the cost price is $10 a unit, then procurement and its colleagues in accounts payable will be looking for invoices priced at $11. But what if supplier’s costs fall? How would procurement even know? And what if the supplier is securing volume discounts and rebates from their suppliers?"

Most contracts have a “right to audit” clause that allows a company like PRGX to come in and review that information. I believe Anthem’s lawsuit against Express Scripts is a result of such an audit. PRGX has found lots of opportunity in the oil & gas industry as they are big users of outsourced services and subcontractors. They have also found auditing labor arrangements to be a particularly promising growth area. Mistakes are abundant and dollar amounts are high. PRGX sees this as a double digit grower for years to come.

The final segment is their adjacent services business. This is a collection of upstart businesses that PRGX has been investing in:

· Advisory Services

· Data Analytics

· Supplier Information Management (SIM)

Today, the majority of the revenue comes from advisory services. Think of PRGX as your accounts payable consultant. As the PRGX website indicates, “Because we have a bird’s-eye view of some 350 global clients’ operations while at the same time our experts are immersed in your individual data and processes, we can provide clients with a view of their own item-level data in new and unique ways across time, business units and geographies.” For example, PRGX is often brought in prior, during and after M&A work to help identify purchasing synergies and other areas of opportunity from a merger. In another engagement, PRGX assessed payment terms across the organization to identify $120mm in working capital improvements. And last quarter PRGX identified 2.5% in savings just from a company purchasing the same items at different prices across the organization. An industry executive told me that P&G doesn’t have a consolidated view of their SKU’s. They have 6 different SKU’s across the organization that are all the same product; they are simply in different geographies under different ERP systems.

Management views advisory as the least desirable of the adjacent services businesses as engagements are shorter and, like with any consulting organization, the company has to manage the variability of project work with employee counts. It is, however, the relationship builder that drives their other services and is a great lead-in to the recurring revenue, subscription based Data Analytics and Supplier Information Management (SIM) businesses that they are building. Once rolling, these businesses do not require a commensurate increase in labor.

After aggregating the spend across an organization, PRGX will often be asked to perpetually refresh the data so that it can be constantly monitored and used for better negotiations. For example, a merchandise company may want to monitor their 100 most important SKU's so that price leakage and working capital issues can be addressed real-time. That data often resides in 30 different divisional ERP systems. PRGX looks horizontally across the organization whereas most companies are organized vertically.

To me, the Supplier Information Management (SIM) product is the most promising. A supplier portal provides a mechanism to interface, communicate and capture information between the supplier community and the internal organizational customers. Data allows companies to process transactions efficiently and correctly, perform more accurate reporting and analysis and mitigate vendor risk and fraud, all of which are quickly growing as focal points and concerns for businesses. Customers will generally use a SIM to more efficiently manage compliance and on-boarding of suppliers. For example, in the food industry, the FDA is requiring companies to report the percentage of ingredients that come from outside the US. None of the food organizations know what percentage of their suppliers’ ingredients come from specific countries. But by setting up a SIM that the suppliers populate, it provides recourse back to the suppliers. These types of regulatory requirements are rampant, whether verifying OSHA certificates, foreign policy obligations or insurance prerequisites. And when bringing on new suppliers, companies need a wealth of information ranging from tax IDs to location information. With organizations working with thousands of vendors, this can be a nice opportunity. Some competitors in the healthcare space are doing $75mm in revenue from SIM alone.

Putting it all together, here is how I think the business can grow over the next 2-3 years.

|

Business |

% of Bus |

Exp. Growth (Rate Used) |

|

Retail Recovery Audit |

71% |

GDP (2%) |

|

Commercial Recovery Audit |

14% |

5-10% (7%) |

|

Contract Compliance |

10% |

Double Digit (10%) |

|

Adjacent Services |

5% |

30%+ (30%) |

|

Total |

100% |

5% |

The stock’s multiple will re-rate higher if they come anywhere close to doing these rates of growth. At 5x ebitda, the current stock price is presuming the business is a melting ice cube. Understanding the history, how the competitive dynamics have changed and seeing the recent results should provide investors comfort that this is not the case. Even if none of the adjacent service businesses pan out, the company should be able to grow the top line 3% while using cash flow to shrink the share count. Should the adjacent services businesses gain traction, not only will the growth rate accelerate, but the recurring SAAS based nature of the businesses should drive higher margins and better multiples.

Customers, The Process & How They are Paid

In its Retail Recovery business, PRGX services 75% of the top 20 global retailers, plus another 200+ retailers from around the world. The global 20 includes Wal-Mart, Kroger, Tesco, Carrefour, Aldi, Costco, Target, The Home Depot, Walgreen’s Boots Alliance, CVS, Amazon and Safeway. PRGX has worked for many of these clients for decades, evidenced by their 99% retention rate.

Commercial Recovery Audit serves industries such as automotive, energy, financial services, manufacturing, technology, transportation and utilities (companies such as Ford, Exxon, Schlumberger and UPS).

Recovery audit contracts vary in length between one and three years. Usually audit work is done perpetually throughout the year. Once they identify and validate transaction errors, they present the information to the clients for approval and submission to vendors as “claims.” PRGX is usually the agency making the claim and handling vendor communications since the clients are less familiar with the details of the discrepancies. PRGX is then paid on a contingency rate basis (a percentage of the recoveries). It is typical in the retail industry for large firms to engage a primary audit firm at one contingency fee rate and then a secondary firm to audit behind the primary at a higher rate (that’s not the case in commercial recovery and contract compliance). PRGX is not able to book the revenue until the claim has been accepted by the vendor. In the US, most of the recoveries are automatically credited against future purchases. PRGX is trying to work towards a similar arrangement in Europe.

I like the contingency rate model because it’s a riskless mechanism for the client to achieve quantifiable, hard savings. They are not selling a product that promises revenue synergies, worker efficiencies or other squishy cost savings. Employees often find ways to “reclaim” the 5 minutes of savings coming from offerings that promise greater work productivity; here the savings are concrete.

All of the recovery audit customers are cross-selling prospects for the adjacent services businesses. Whereas, the advisory business is project oriented and shorter term in nature, data analytics and SIM are subscription based. In the SIM business, retailers pay an initial set up fee, but the majority of the revenue comes from the suppliers who pay anywhere from $100-$500 a year to be in the database. With larger organizations working with thousands of suppliers, this can add up fairly quickly. As I mentioned, there are a couple SIM providers in the healthcare business doing $75mm in revenue, but beyond that it is a very young and fragmented business.

Competition

In the retail recovery audit business, PRGX’s only national competitor is a division of Cotiviti. Cotiviti is de-emphasizing the business (i.e. not reinvesting) while PRGX has rededicated itself with a new focus and upgraded technology. To understand the dynamics, it helps to look at the ancestry of Cotiviti. Cotiviti was formerly known as Connolly, a retail and commercial recovery auditor. Connolly established a successful and rapidly growing healthcare business and sold itself to venture capital/private equity firm Advent International. Advent merged it with iHealth Technologies, one of its quickly expanding healthcare portfolio companies and suddenly the recovery audit business was the ugly and forgotten step-child. Advent later renamed the company Cotiviti and looked for opportunities to shed themselves of the low growth recovery audit businesses.

Soon after the merger, Cotiviti sold off the commercial recovery business to its employees (more on this later). It then tried to dress up the results of the remaining retail recovery business in order to sell it. To achieve this, they first got aggressive on pricing in the hopes of showing top line momentum from market share gains. PRGX took the brunt of this action. At the time, an industry veteran postulated, “I imagine they [Connolly] are just trying to maintain retail revenue or maintain the people until they can be redeployed into healthcare.” To counterbalance the lower rates (or maybe just to make it look like top line was growing while margins were expanding), the private equity firm later cut recovery auditors compensation. This did not have the results they were hoping for as many dissatisfied employees jumped ship to PRGX. I speculate at this time that Cotiviti just decided to stabilize the recovery audit business (15% of revenue) and move forward with their planned IPO anyway. With healthcare growing at 30% per year, retail recovery audit would soon become just a blip. Cotiviti made little mention of the business during their roadshows. It, and all the analysts I spoke to that follow them, simply stated it’s a stable business that generates cash that can be used to fund the growth in healthcare. It’s interesting how followers of Cotiviti accept the “stable business” tag while potential investors in PRGX presume it’s a dying business. This is particularly confusing since Cotiviti admits that aren’t putting resources back into the business while PRGX is investing in its people, processes and technologies.

So what is PRGX doing to differentiate itself? The most important thing is using technology and best practices to accelerate the auditing process. Shortening the time period from point of transaction to request for recovery should increase recovery yields, reduce supplier abrasion and generate quicker cash flows. Vendor irritation is particularly notable in Europe where suppliers have fought back against the dominance and excessive influence of large retailers like Tesco. Clients detest having to reconcile overpayments that occurred 500 days prior as they can’t do a lot to fix the problem at that point. In the grocery segment, European suppliers successfully enlisted politicians to enact the Groceries Supply Code of Practice (GSCOP), which among other things restricts the age past which claims can be recovered. PRGX is addressing the problem through the automation of processes and databases. For example, some datasets sent over from Amazon used to take 45 days to structure, but now only take 5.

So the question becomes if Cotiviti quietly withdraws from the business, can the next largest player step into their position. Possibly, but the drop off is dramatic. Except for regional players, this is really a duopoly. The smaller recovery audit firms generally do not possess multi-country service capabilities and do not have the centralized resources or broad client base required to support the technology investments necessary to provide comprehensive recovery audit services for large, complex accounts payable systems. I spoke to a number of these competitors and most agreed they are generally only successful competing on smaller regional organizations.

Finally, a regional competitor made the following comment to me. “[Retailers] get the math. If a company recovers $100mm for you at a 10% contingency rate, then the company is up $90mm. Even if a competitor offers to do it for free, it needs to collect at least $90mm, otherwise the retailer has lost money by “saving.” Larger firms just won’t risk losing numbers that big, especially since every new provider would have to ramp up the learning curve to find which files are available and where they can dig.

On the commercial recovery audit side, the primary competitor is Apex Analytix, a private company out of North Carolina. CapIQ reports revenue as $35mm. PRGX is the next largest provider, but will approach Apex’s size with their recently announced purchase of Cost & Compliance Associates (CCA). CCA was the 3rd largest provider. This was the former commercial recovery business owned by Connolly that was spun off to management after the Advent acquisition. I’ll discuss more about the CCA transaction in the Recent Acquisitions section, but suffice it to say this transaction will make the commercial recovery audit business a duopoly not too dissimilar to the retail recovery business.

In contract compliance, the business is more fragmented. Most of PRGX’s contract compliance competitors either charge a fixed fee or by the hour. PRGX is having success breaking into new business with its no risk, contingency fee model.

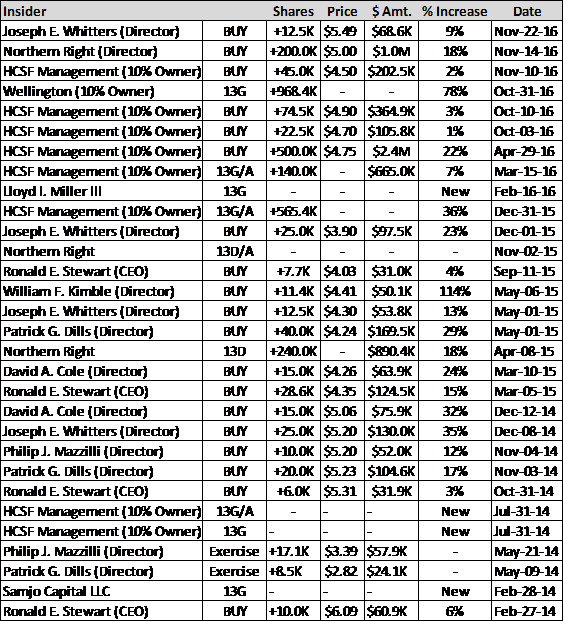

Share Repurchases and Insider Activity

“It’s almost a mathematical impossibility to imagine that, out of the thousands of things for sale on a given day, the most attractively priced is the one being sold by a knowledgeable seller (company insiders) to a less-knowledgeable buyer (investors).” Warren Buffett

Study after study indicates the inverse applies as well and PRGX and its insiders have been buying shares hand over fist. First, let’s look at insider activity.

As you can see, there has been steady buying from management, board members and large 13D and 13G filers. InsiderScore rates PRGX’s insider activity as a 10 on a 1 to 10 scale. They estimate only 2.9% of the 5,000 companies currently have a score of 10.

Activity on the corporate side has been even more impressive. The company has reduced the share count by 25% over the last two years. Having watched the activity, I will also say they have been opportunistic, buying the bigger blocks of stock within the quarter when the price is down. This is a great way for a slow growth business to generate “extra return” for its shareholders. Remaining shareholders benefit from the compounding reduction of the share count. As I mentioned in the thesis, the company is effectively “publicly” taking the company private. Eventually, I think they will reduce the shares to a level that will allow for a bite-sized going private transaction.

Activist Involvement

While I don’t think having activist activity guarantees a floor, I think it makes the floor sturdier. The combination of investor representation, strategic oversight and a watchdog holding management accountable induces boards and executive teams to run at their best. PRGX currently has three activist holders. I’ll start with the group that was recently added to the board, Northern Right. This is how one publication described their involvement:

Northern Right knows this Company well. Matt Drapkin, the founder of Northern Right, has owned it on and off for over seven years and has filed two previous 13Ds on the Company at his predecessor fund, Becker Drapkin. [That fund’s] average return of 89.89% [bested the] 24.79% for the S&P500 over the same time periods. When Becker Drapkin was a 13D filer in 2014, it was because they had issues with the CEO. This is a totally different story. Northern Right is very supportive of the current CEO who is on the cusp of dramatically turning around the business. He has resolved the execution and strategy issues of the past and is taking the business to the next level by, among other things, converting service issues into strong client relationships, executing on strategic M&A and turning over the board. The retail business is showing the first signs of growth in the past six years, which will give them the stability and cash flow to build out ancillary businesses and services for its current clients, such as contract compliance, spend analytics and supplier verification. This is a situation where management can continue operating and executing on the business plan and the board can analyze the best use of the cash from operations. Matt Drapkin has an extensive track record of adding value from a board level and should be very helpful in assisting with capital allocation and M&A decisions as well as being a public face to tell the company’s story and a shareholder advocate for the CEO. In fact, Northern Right bought $1 million of stock on his first day on the board, even further aligning themselves with shareholders.

It’s tough for me to describe the situation much better.

PRGX’s largest shareholder (13% of shares outstanding), is a concentrated small cap fund that labels itself “constructive activists.” Out of San Francisco, Headlands Capital (it shows up on filings as HCSF Management), owns just 10 names and, despite its already hefty ownership size, has been adding to its PRGX position. Here is how they describe their process: “Once we build a core position in a company, we seek to support management to drive future growth and increase shareholder value. Headlands Capital's collaborative initiatives have included capital structure optimization, identification of growth opportunities, advising on acquisitions and divestitures, introduction to outsourcing resources and/or enhancing communications with Wall Street and the investment community.”

Finally, Cannell Capital has also begun rebuilding a position. Cannell was the sixth largest holder back in December 2013. They presciently sold their position in Q413 and Q114, likely in the $6.40 to $7.20 range right before the stock began a steady slide into the 3’s. Two and a half years later, they obviously see something in the stock, as they began buying in Q216 and as of the end of Q316 are the 12th largest holder.

Recent Acquisitions

PRGX recently made two acquisitions. I’d classify the first, Cost & Compliance Associates (CC&A), as an immediately accretive tuck-in to the growthier, higher margin side of the core recovery audit business. About 35% of the business is in contract compliance (the fastest growing and highest margin part of the core recovery audit business) and the remainder is in commercial recovery audit (still less mature than retail recovery audit). CC&A had lost a couple of clients to PRGX due to PRGX’s upgraded technology and cross saleable adjacent service offerings. CC&A’s management team realized PRGX was becoming a tougher competitor and that CC&A was going to have to invest a lot of money back into the business if they were going to remain relevant in the upcoming years. PRGX acquired the business for an attractive 5x ebitda.

The second acquisition, Lavante, Inc., is very small, but provides PRGX award-winning and name recognizable technology that will allow them to accelerate their growth in the Supplier Information Management (SIM) business. The company was founded by a former PRGX employee and has a strong pipeline of interested Fortune 500 companies. As a small venture backed company however, its balance sheet and staying power had been a sticking point to pushing contracts across the goal line. With a strong pipeline, the VC firm decided to sell the business to PRGX at an initial loss, but can make a decent return if they can meet the earn-out. PRGX also thinks they will be able to expand the business by introducing the offering into their established retail base (Lavante only sold to commercial clients). This acquisition had apparently been in the hopper for a while, so the company had postponed putting some new clients on their own platform knowing they would later have to move core pieces over to the Lavante platform. In summary, Lavante appeared to be 2-3 years ahead of PRGX from a technology perspective, and PRGX can now leverage its balance sheet, staying power and client base and avoid the capex spend to catch up.

Future Acquisitions

I would not expect PRGX to make additional acquisitions in the near future. They have indicated their plate is full with the opportunities they just acquired.

Acquisition Candidate?

I think PRGX itself will eventually be taken private. In the core recovery audit business, being subject to public pricing scrutiny puts them at a distinct competitive disadvantage (management agrees). It would be far easier to run this company in a vacuum without competitors and clients being able to decipher pricing concessions and contingency rates. Throw in public company overhead expense for a smallish $100 market cap corporation and this company could undoubtedly be run more profitably as a private entity.

In addition, a private equity firm not burdened with satisfying investors and meeting quarterly projections could be more aggressive in building out the adjacent services businesses. As a backdrop, a private equity transaction in the $7-9 range reportedly fell through back in 2012. I’ve heard different rumors as to why. One indicated the CEO at the time wasn’t interested at that price. The other, that the principal participant championing the purchase for the private equity firm unexpectedly died during the negotiating period. Nonetheless, I see other slow growth microcaps like Lionbridge (LIOX) recently being taken out at 9x ttm ebitda. That would amount to 94% upside to PRGX in a year’s time. Note: LIOX is in a different service business (language translation services), but curiously, they have strikingly similar financial metrics. Gross margins, SG&A percentages and cash conversion cycles are very similar. PRGX has a better balance sheet and historically has better bottom line margins, but LIOX has historically grown faster. PRGX’s growth metrics, however, are skewed by the businesses they shuttered and LIOX’s were boosted by the six acquisitions they have made over the last 4 years. I expect PRGX to grow at mid-single digit rates going forward, consistent with LIOX’s past growth rates. Both also have lumpy businesses that have resulted in quarterly fits and starts (though it looks like PRGX has had a much better track record of late). I readily admit this is a one-off comparison, but it was interesting that companies with very similar economics trade for strikingly different multiples, particularly considering PRGX feels like it’s just starting to turn the corner.

Finally, although I think a strategic buyer could show interest (perhaps a consulting firm looking to leverage PRGX’s Fortune 500 client list and treasure trove of data), I think it is less likely. The greater the success of the adjacent services businesses though, the greater the likelihood of the interest of a strategic acquirer.

Valuation

In deriving my $9.27 target (70% upside) I use an 8x ebitda multiple on 2017 estimates and assign NO value to the upstart adjacent services businesses (I simply add back the $4mm in ebitda losses from those businesses). From the enterprise value, I subtract $13mm for the present value of their NOLs ($90mm) and then add $3mm for possible residual healthcare claw backs from a business they discontinued a couple years ago.

In a bear case scenario in which none of the adjacent services businesses are successful, the company would simply shutter the operations and let the cash flow from the core operations shine through. In that scenario, I think it would be likely the company would go private to harvest the cash flows, unburden themselves from public company expenses and avoid competitors and customers being able to use public market information and commentary to their advantage during renewals.

In a bull case, I think the company blows through Street 2017 revenue estimates. Today, the street presumes 11% revenue growth, but 9.5% of that will simply come from layering in the revenue from the CC&A and Lavante acquisitions. Should those businesses grow (they are incented to via the earn-outs), we could hit street estimates without needing any growth from the existing business. As a reminder, the existing businesses grew 5.3% in the past quarter. I again caution that the business is lumpy and that the last quarter did benefit from some previous quarter delays, but the company is just at the beginning of ramping up the adjacent services businesses and their long term goal does equate to a mid-single digit growth rate.

From an ebitda perspective, I should point out that some unusual items hurt 2016 and should not recur in 2017. PRGX’s two acquisitions resulted in $750k of M&A expense. As I mentioned, the company has no plans to make additional acquisitions at this time, nor does the duopolistic nature of its businesses offer many opportunities. The company also experienced $1.3mm in above average healthcare claims due to a couple unfortunate serious illnesses. I think a safe assumption is to presume healthcare expenses remain elevated and we only get maybe $750k of this back. Together these should provide a $1.5mm bump while the CCA acquisition will likely add another $2mm. This $3.5mm helps bridge the gap from 2016’s 15.4mm assumption to 2017’s 20.4 estimate with the rest coming from margin expansion and/or additional revenue.

From a free cash flow perspective, the company did 13.5mm in CFO in 2015 against 4.5mm in capex or $0.41 share (8% FCF yield). Adding back the investments for growth would drive free cash flow to $0.60 and the free cash flow yield to 11%, but they also benefitted from the CFO’s focus on A/R. Those two just about offset each other, so I think the $0.41 is probably the truest representative of what the company earned. The investments in growth won’t make FCF in 2016 or 2017 look as robust. Capex will rise to 6mm and likely creep higher in 2017. PRGX will likely still see $4-5mm in annualized losses up until the 2nd half of 2017. From my perspective, the business has only gotten better from 2015, and layering in the acquisitions should prove to be more accretive over time.

Summing it all up, you have a solid, improving and moderately growing business trading at a shrinking business price despite free optionality in upstart businesses. Management is focused and dedicated and insiders, who should have the best insight into the true value of the business, have repurchased over 30% of the stock in the last two years.

Risks

- The business remains a lumpy business. Though the majority of the business “recurs” (most recovery audit contracts are for 3-5 years and the company’s retention rate has been 99%), revenue recognition comes in clumps when the client’s supplier accepts PRGX’s claims. This means the results of any one quarter can hinge on whether the deal is closed on September 30th or October 1st. It is thus common for the company to beat or miss earnings based on deferrals (either business slipping into the next quarter or benefitting from slippage the previous quarter). The company has been pretty good at calling these out. Note: some may view a management team that goes on the road telling their story and then misses one and half months later as promotional, but I distinguish between being promotional (promising what you are unlikely to deliver and overtly touting the massive market opportunity at the expense of near term results) from the difficulty of managing quarterly estimates in a lumpy business (telling the long term story and realistically talking about the opportunities, but missing numbers b/c revenue recognition occurs several weeks later)

- Customer concentration. PRGX’s top 5 customers represent 32% of their business. None are larger than 10%.

- Exposure to retail. We all know offline retailers have had a tough go of it. PRGX audits for online retailers as well though. In fact, Amazon is one of their largest and fastest growing customers. Also, PRGX becomes a more valuable partner (discovering a greater percentage of their profits) as offline retailers decline.

- The stock, which is not terribly liquid, is heavily concentrated in a few hands. To date, sales have generally been done in an orderly manner. Because the base is strictly made up of value investors, you generally don’t see a “blow it out at any cost” mentality. Sellers have found block buyers (sometimes the company itself through their buyback program) or bled the stock out over long periods of time. I think the activists’ involvement also provides some downside protection.

I and/or others I advise do not hold a material investment in the issuer's securities.

Catalyst

- Valuation re-rates

- Business turns, returns to consistent growth

- Losses from investments cease, new businesses become growth vehicles

- Continued share reduction

- Insider activity

- Going private transaction?

| show sort by |