| 2016 | 2017 | ||||||

| Price: | 2.75 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 9 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 26 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | -5 | EBIT | 0 | 0 | |||

| TEV (in $M): | 21 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- Personal Account Idea

- Nano Cap

- NOLs

Description

QUMU Corporation (Nasdaq: QUMU)

Overview

Shares of Minneapolis based Qumu Corporation offer asymmetric upside of almost 100% over the next 12 months as the company transforms from a consumer of cash to a solidly EBITDA positive recurring revenue business. A host of factors give us confidence in the Management team, the Company’s path to profitability, and private market value of the business.

What does QUMU do?

Qumu provides an enterprise software platform that large organizations use to create, manage, secure, distribute and measure the success of their videos. All of this happens behind the firewall within their internal environment.

Why do large organizations use video?

Large organizations use video for a host of reasons including:

-

Sales workshops

-

Corporate messaging

-

Training sessions

-

Culture building

-

Basic communication

-

Compliance related matters that must be archived

The market for QUMU’s business is estimated at $1.8b-$2.0 with a 20% CAGR

Enterprise communications must reach all employees securely, across devices and time zones, in all languages, and without comprising the organizations network infrastructure. It is for this reason that enterprises utilize a service such as QUMU versus YouTube or email, which can take a network down as large unsecure files strain resources.

Company History

If you bring up QUMU’s financials it appears to be a business in decline. That is because QUMU was formerly Rimage, a company focused on selling mostly CD and DVD recordable publishing systems. This business started its decline in the 2006-2007 time frame thanks to the well documented shift towards digital publishing and distribution systems. Rimage acquired Qumu in 2011 and changed the Company’s name and sole focus to video solutions. In 2014, the company both sold its legacy disc publishing business and acquired Kulu Valley, a U.K. based provider of video content creation solutions. Kulu allowed QUMU to accelerate sales of their cloud-based offerings, sold as a subscription.

Product Capabilities

Qumu’s offering is substantial, offering customers the following features:

-

Video Capture: Offerings include a portable software enabled device that records, edits, and publishes; a browser based applet for the creation of videos captured from a computer screen or camera; integration with videoconferencing systems to enable their use as studios for the creation of live or on demand content .

-

Video Management: An enterprise scalable solution that provides control for all video applications, content, and resources involved in the production of video; it also manages both live streamed video and video on demand workflows.

-

Speech Search: Allows for the searching and indexing of spoken dialogue within the video.

-

Live Broadcast Console: Manages and deploys live streamed videos with broad security capabilities.

-

Video Delivery: Secure download allows videos to be delivered to mobile, viewed offline, and managed/disposed of on prescribed policies.

-

Mobility and Integration: Mobile apps for iOS and Android with complete out of the box native video apps built using their software development kits. They integrate with leading mobile device management and mobile application management platforms such as Good Technology and XenMobile; also integrates with key business applications such as Microsoft SharePoint, Lync, Office365, IBM WebSphere, Jive, Citrix (XenApp/XenDesktop) and other social platforms.

-

Qumu Cloud: Fully managed solution delivered as a subscription (SaaS) platform; creates and delivers video seamlessly; used by organizations to rapidly and clearly present their messages as well as drive business opportunities through the integration of video with their web sites.

How are organizations using QUMU?

Below are some examples of how organizations use QUMU to drive ROI.

-

A Pharmaceutical firm saves $25,000/sales representative annually with mobile video communications.

-

A global bank increased customer satisfaction by 15% and saved over $1M annually with technical support videos.

-

A top 10 technology company generates seven-figure revenue per event with video webinars.

-

A top 10 information technology company garnered 250,000 views for a live and on demand CEO broadcast.

-

A large technology company CEO live-blogs to his employees, helping shape corporate culture.

Who are QUMU’s customers?

QUMU counts 63 of the Forbes Global 1000 as customers. These customers span a wide range of industries, from financials to healthcare and professional services firms. Some names include:

-

Visa, BNY Mellon

-

Credit Suisse, Citi, Barclays

-

GSK, Bayer, Sanofi

-

AT&T, Vodafone, BT

-

KPMG, Deloitte, CAT

So where does QUMU trade, what happened this year, and what do we think it is worth?

Capital Structure

Shares Outstanding: 9.3m

Price 2.75

Mcap $25.5m

Debt: $8m**

Cash: $12.6m**

EV: $20.9m

Ttm sales: $32.4m

EV/Sales: .64x

** (post Q3) On Oct 25th QUMU closed an $8 million credit agreement with Hale Capital Partners, LP. The credit agreement provides an $8 million term loan drawn at close, with principal due on October 21, 2019 and interest set at prime plus 6% payable monthly. The credit agreement includes a detachable 10-year warrant to purchase 314,286 shares of the company’s common stock at an exercise price of $2.80 per share. We have added $8m to the quarter end debt and cash balances but have not accounted for the warrant in the above table.

QUMU’s stock has been volatile, yet roughly unchanged from the beginning of the year.

In July of this year, QUMU preannounced a disappointing second quarter due to timing issues related to large customer activity. The Company scrapped full year guidance and the shares suffered. Regardless,

Adjusted EBITDA for the six months ended June 30, 2016 is expected to be a loss of approximately $6.0 million, compared to a loss of $14.5 million last year.

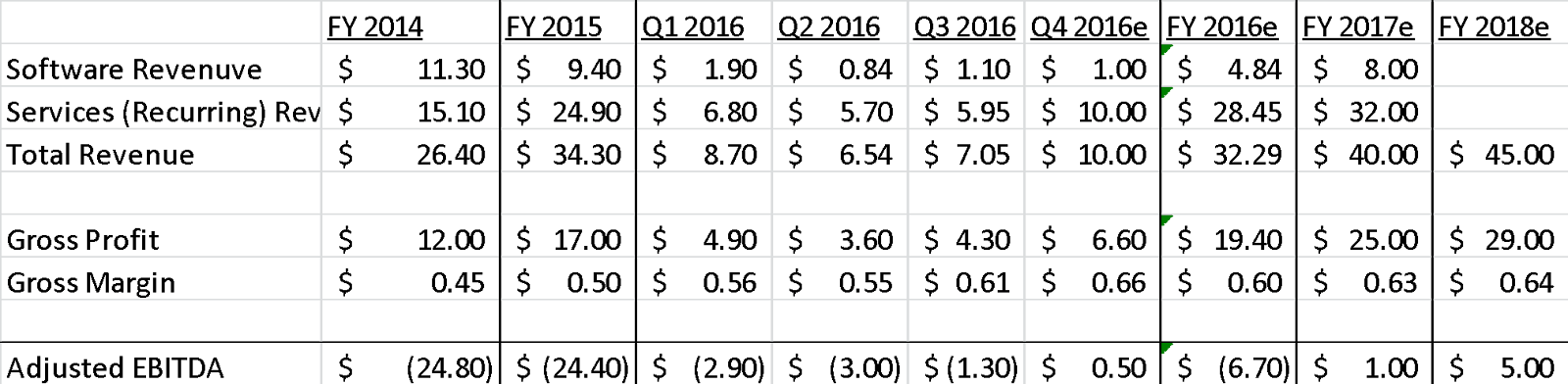

Here is a look at historical and projected results:

We feel confident in these projections for a number of reasons:

-

The CEO has publicly stated that adjusted EBITDA is expected to be in the range of $300,000 to $800,000 compared to adjusted EBITDA loss of $3.7 million in the fourth quarter of 2015.

-

The Company’s recent decision to take on debt versus initiate an equity offering demonstrates Management’s confidence in the sales pipleline.

-

A recent meeting with the CEO at the Craig Hallum Alpha Select Conference further enhanced our confidence as the CEO was asked about sales coverage in the pipeline to which he replied that he felt very comfortable with where things stood. CEO had previously noted 3x coverage in the pipeline for guidance on their 3Q conference call.

-

QUMU is still highly underpenetrated amongst its existing customer base. With 63 of the top 1,000 companies in the world as customers, QUMU could easily double the size of their existing business simply by doing more with its existing audience.

Keep in mind that QUMU only needs $10m per quarter to CF break even, a level that they will attain in Q4.

Management & Other Shareholders

QUMU is led by CEO Vern Hanzlik. Vern is a career technologist and entrepreneur. He formerly ran Stellant, a $140m software business that was ultimately sold to Oracle in 2006. Vern has been around the cloud computing space since 2007 building software. Vern has spent the last 12 months taking almost $20m of SG&A out of the business.

Almost 40% of the stock is controlled by 5 entities.

Ariel has been a long term holder, adding to their stake over last 3 – 4 years. Dolphin is also a large holder as Donald Netter came in primarily as an activist when the Company’s cash balance was higher. Netter was able to obtain a Board seat.

Competitor Valuations

The comp most cited when discussing QUMU is Brightcove (Ticker: BCOV). BCOV is a $150m revenue business, is not profitable, yet trades for 1.7x EV/Sales

Several other video companies have raised capital or have been acquired at meaningful multiples:

Kaltura

Open-source video platform Kaltura raises $50M from Goldman Sachs, confirms plans to IPO

http://venturebeat.com/2016/08/08/open-source-video-platform-kaltura-raises-50m-from-goldman-sachs-confirms-plans-to-ipo/

Upstream

IBM Said to Pay $130 Million to Acquire Video Startup Ustream

http://www.bloomberg.com/news/articles/2016-01-21/ibm-said-to-pay-130-million-to-acquire-video-startup-ustream

Oovala

Australian Telco Telstra Acquires Video Distribution Startup Ooyala

https://techcrunch.com/2014/08/11/telstra-ooyala/

Panopto

Panopto raises $2.4M, adds ex-Amazon exec as COO

http://www.saturnpartnersvc.com/2013/06/panopto-raises-2-4m-adds-ex-amazon-exec-as-coo/

Acano

Cisco acquired Acano one year ago in a $700M deal, speculated to be 8x revenue.

https://techcrunch.com/2015/11/20/cisco-snags-acano-for-700-million-to-enhance-video-conferencing-capability/

We ran the following screen to see where EBITDA positive software companies trade.

The criteria were as follows:

-

US & Canada

-

Market Cap between 0 and $500m

-

Revenue greater than $18m

-

EBITDA positive

The screen turned up 82 companies. The average EV/Sales for these companies was 1.55x and the median EV/Sales was 1.29x

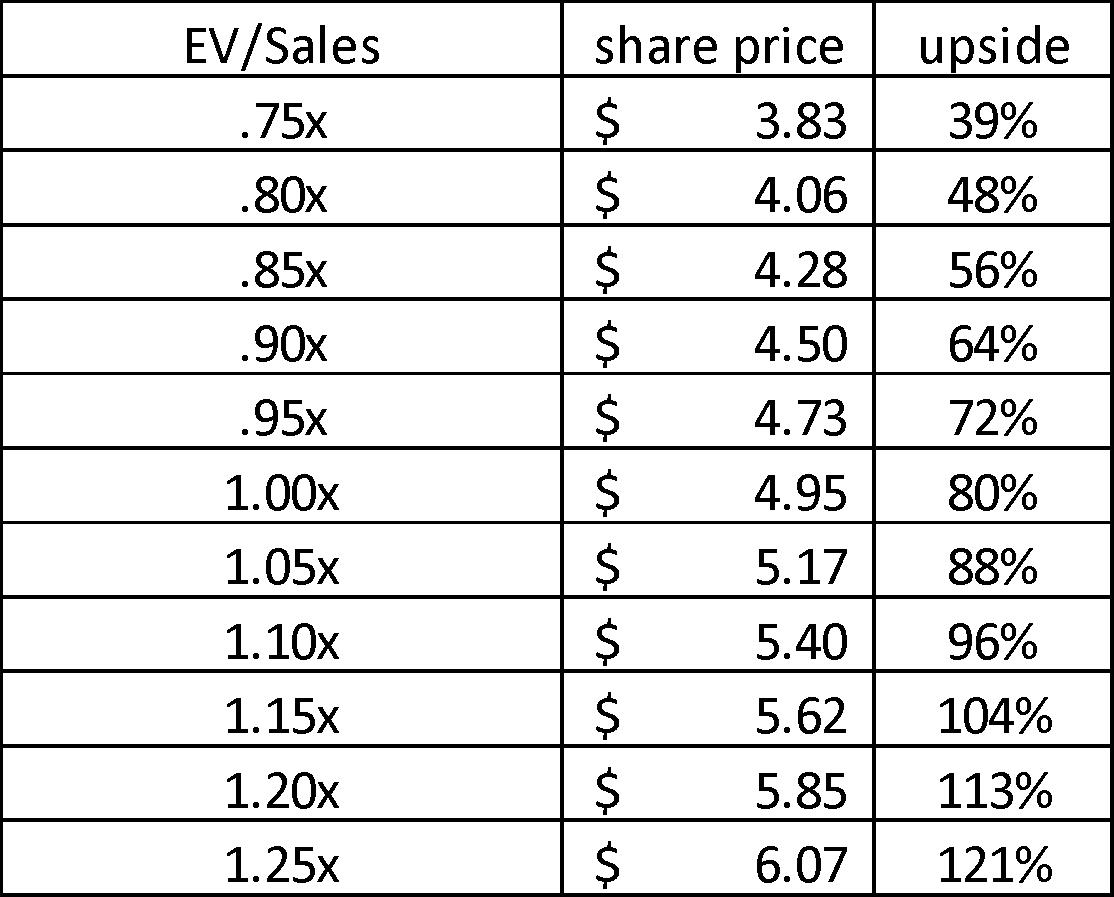

Here is where QUMU would trade at a range of .75x projected sales of $43m, which is the midpoint between our 2017 and 2018 estimates.

*note that the share price used in this computation includes the dilution from the Oct 2016 Hale Capital warrants

Other Considerations

QUMU has an investment in the preferred stock of an Israeli video & security Company called BriefCam on its balance sheet listed at a cost of $3.3m. BriefCam enables law enforcement and security personnel to review hours of surveillance video in minutes. The ex-CEO of Orange Spain is now running the Company, which has gained excellent traction globally. Its investors include Motorola Solutions, who invested $6.5m into the Company in 2013.

Most recently, BriefCam was used in the Rio Olympics:

http://briefcam.com/category/briefcam-on-tv/ - used in Rio Olympics

BriefCam was also the integral piece of technology that helped solve the Boston Marathon bombing incident in 2013.

http://www.pri.org/stories/2013-05-09/israeli-technology-may-have-helped-identify-alleged-boston-bombers

Vern has indicated that QUMU seeks to monetize its investment in BriefCam in the near future. If this can be achieved, it could be worth $0.30-$0.35c per share to QUMU, assuming there has been no appreciation on the investment.

Net Operating Loss Carryforwards

As of December 31, 2015, QUMU had net operating loss carryforwards of $68.4 million for U.S. federal tax purposes. The Company also had $58.8 million of various state net operating loss carryforwards. The loss carryforwards for federal tax purposes will expire between 2023 and 2035 if not utilized. The loss carryforwards for state tax purposes will expire between 2022 and 2035 if not utilized.

Conclusion

QUMU has come a long way over the last few years and is finally in a place where getting to (and staying) EBITDA positive is a reality. When this happens, the valuation will change from a distressed-like software company to one that trades at an appropriate EV/Sales level commensurate with a business that features:

-

A multibillion dollar addressable market.

-

Substantial recurring revenue base of > $30m per annum.

-

A high quality Tier One customer base.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

The Company will move to a substantially EBITDA positive position next year and show higher growth in it's recurring revenue base. It will no longer trade like a shrinking or distressed software player and move towards a more reasonable multiple of EV/Sales. When this happens, the shares may appreciate 100% or more.

| show sort by |