| 2016 | 2017 | ||||||

| Price: | 9.91 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 29 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 295 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 1,199 | EBIT | 106 | 0 | |||

| TEV (in $M): | 1,494 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- Spin-Off

- REIT

Description

Quorum Health Corporation (“NYSE: QHC”), which was recently spun out from parent Community Health Systems (“NYSE: CYH”) on April 29th, is a hospital management company comprised of 38 community hospitals located in non-urban areas in the US. QHC shares have sold off significantly post-spin with shares currently trading at $9.91 (down 33% from the spin-off price of $15) with a market cap of $295 million, net debt of $1.2 billion ($40 per share) and an EV of $1.5 billion ($50 per share).

The market has a negative perception of QHC given its portfolio of low margin, non-urban hospitals in areas bogged down by lagging economic growth and high leverage at around 4.5x 2016E EBITDA post spin after the incurrence of $1.3 billion of debt to pay a $1.2 billion special dividend to CYH. As a result, there was strong selling by CYH shareholders who didn’t want to own shares in <$300 million market cap company with a portfolio of hospitals that CYH was seemingly trying to get rid of. QHC is trading at around 5-6x 2016E EBITDA of $265 million (low end of management’s 2016E guidance of $265-275 million) with comps trading at a median EV/EBITDA multiple of around 7-8x.

Under the helm of a new management team and renewed focus on the portfolio, QHC is shaping up to be a classical spinoff opportunity with leveraged upside to a successful turnaround. QHC aims to follow the blueprint of other successful spinoffs of hospital portfolios in small cities/rural markets notably LifePoint Hospitals and Triad Hospitals which were both spun out of HCA and have performed well post-spin off in 1999. The sources of upside (not reflected in the current valuation) will come from (i) divestment of negative EBITDA hospitals, (ii) reinvestment in core hospitals to improve staffing and services, and (iii) deleveraging from free cash flows.

Spin Background

On August 3, 2015, CYH announced plans to spin off 38 hospitals and its hospital management advisory business into QHC. The spinoff was completed on April 29, 2016 through the distribution of 100% of QHC’s shares to CYH shareholders. CYH shareholders received one share of QHC for every 4 CYH shares resulting in a company with a much smaller market cap than CYH. QHC entered into a 5-year transitional services agreement with CYH to provide IT and administrative services of $5 million annually and QHC expects to incur an additional $3 million of costs annually as a standalone public company.

In connection with the spin-off, QHC issued $400 million in 11.625% senior notes due 2023 and entered signed a new $880 million senior secured term loan facility due 2022 in order to pay a $1.2 billion special dividend to CYH shareholders and fund working capital. QHC also has access to a $100 million senior secured revolving credit facility and a $125 million ABL facility which are currently undrawn and available for acquisitions.

Business Overview

Quorum Health Corporation (“QHC”) is an operator and manager of general acute care hospitals and outpatient services in the US. QHC has a portfolio of 38 hospitals (32 owned) with an aggregate of 3,582 licensed beds across 16 states. Its owned and leased hospitals generate revenues by providing generalized and specialized hospital healthcare services and other outpatient services to patients in local communities.

The company’s Quorum Health Resources (“QHR”) subsidiary provides hospital management advisory services to 93 non-affiliated hospitals in 33 states and consulting services more than 125 hospitals in 37 states. QHR’s hospital management advisory contracts run for 3-5 year terms under fixed fee arrangements and cover operational, financial and strategic guidance. QHR’s consulting services target the operational needs of hospitals including A/R management, information management, patient flow, compliance systems, purchasing, online solutions and other operational services.

In 2015, QHC generated $2.2 billion in net operating revenues after bad debt provisions (QHC: $2.1 billion, QHR: $0.1 billion) and $264 million in adjusted EBITDA with margins of 12.1%.

Source: QHC Investor Presentation (April 14, 2016)

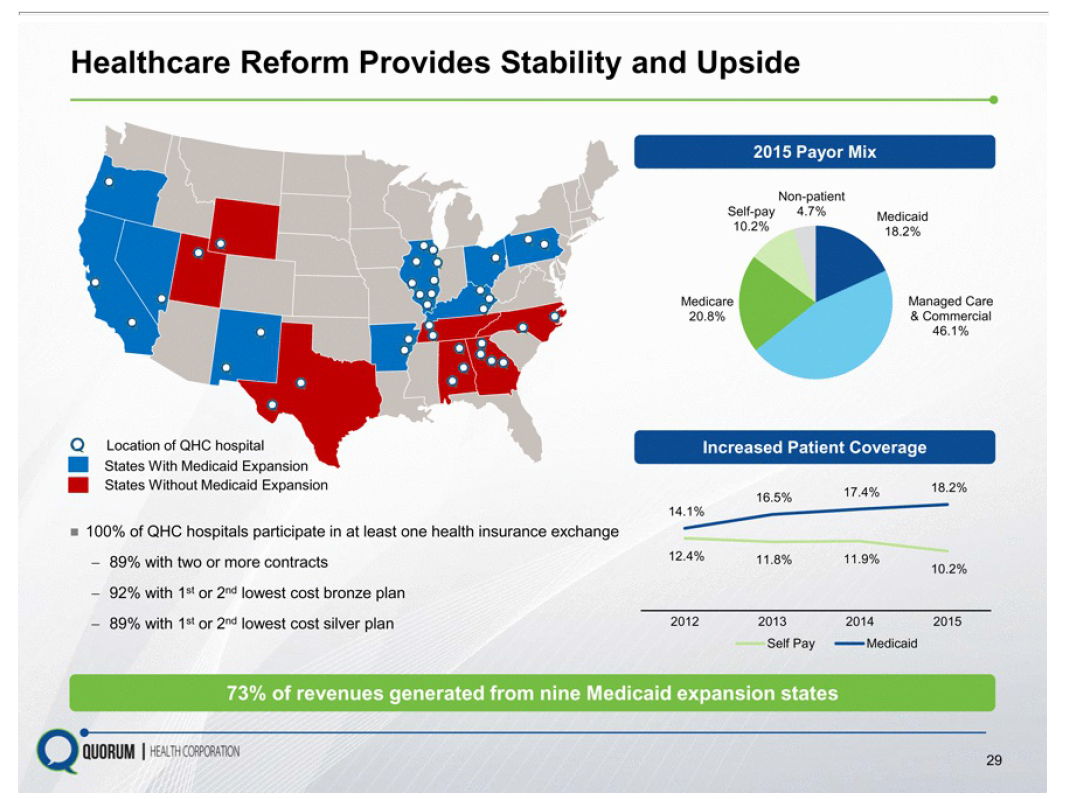

QHC’s portfolio is focused on rural areas (cities and counties with populations of 50,000 or less) and 84% of its hospitals are sole providers of care. 9 of the 16 states in which QHC operates have opted to expand Medicaid coverage with these states accounting for 73% of QHC’s revenues as shown below.

Source: QHC Investor Presentation (April 14, 2016)

A substantial portion of revenues generated from Medicare and Medicaid programs with around 46% of revenues generated from private/commercial payors (before bad debt provisions). The percentage of revenues derived from Medicare/Medicaid programs is expected to increase due to the structural aging of the US population and these are typically lower margin than managed care and commercial.

Source: QHC Form 10/12B Filing (April 1, 2016) p.68

Investment Thesis

QHC was an underinvested, orphaned business under CYH ownership

With a focus on smaller hospitals in non-urban areas, most of which are sole providers, QHC was an orphaned business within CYH which operates 194 hospitals in 28 states and is strategically focused on larger hospitals and regional networks. QHC hospitals generated EBITDA of $264 million in 2015 against CYH’s EBITDA of $2,670 million or roughly 10% of the total combined CYH/QHC. It also took CYH around 6 months to finalise the spinoff of QHC during which all QHC-related capex was stopped and recruitment was stalled at QHC’s hospitals.

The strategies for driving better operational performance at large vs. small community anchored hospitals differ significantly and the spin-off will allow QHC’s management to focus on levers that will improve the operational and financial performance of its hospitals. Specifically, QHC plans to increase physician engagement and recruiting efforts and to expand the breadth of its services beyond primary care which is expected to drive further volumes to its hospitals – currently QHC is experiencing outmigration in its emergency rooms due to lack of staff and resources so there is underlying demand.

QHC management is following the playbook for similar spinoffs

Other hospital spinoffs (LifePoint, Triad) have successfully turned around their rural/small cities hospital portfolios through divestments and focus on their core assets. LifePoint and Triad were able to take EBITDA margins to 19% and 14%, respectively in the year following the spin-off in 1999. Comparatively, QHC delivered adjusted EBITDA margins of 12% in 2015 with healthy EBITDA margins for the profitable hospitals.

The current CFO, Michael Culotta brings 30+ years of industry experience having previously served as CFO of LifePoint Hospitals from 2001-2003 and 2007-2013 which provides some comfort in the new management’s ability to execute a similar playbook.

Source: QHC Investor Presentation (April 14, 2016)

Restructuring/deleveraging opportunity by divesting unprofitable hospitals is not priced in

QHC can unlock significant value from portfolio rationalization and rebalancing. Of QHC’s existing portfolio of 38 hospitals, around ~8-11 hospitals are generating negative EBITDA margins today. Management indicated on the Q1 earnings call that the hospitals with negative EBITDA experienced admissions declines of 8.3% and adjusted admissions declines of 2.9% for Q1 2016 compared to Q1 2015. For the overall portfolio, admissions declined by 2.2% and adjusted admissions grew by 0.8% (partly impacted by the less severe flu season). Comps for the performing hospitals would have been positive without the impact of the unprofitable hospitals.

The 8-10 negative EBITDA hospitals are located in markets where there are large tertiary care providers and collectively generated operating revenues of $250 million, $8 million in operating losses, and incurred $12 million of capex in 2015 (Source: UBS research report dated June 10, 2016). Following the spin-off, management has been sounding the market to sell these hospitals and has estimated that around $100 million could be generated from divestitures which are expected to be completed by Q1 2017. Working capital can fluctuate due to the timing of receipt of reimbursement payments from state programs. The proceeds would be applied towards paying down debt, increasing equity value by around $3.36 per share. Even if QHC is unable to sell the hospitals for a positive purchase price consideration, closing these under-performing hospitals would boost run-rate EBITDA from around $265 million to $273 million, improving margins and reduce capex by $12 million.

Risks

Sluggish economic recovery given rural portfolio

QHC’s hospital portfolio is located in areas with lagging economic growth and higher unemployment which could impact utilization rates resulting in a deferral of discretionary medical expenses and higher bad debt expense from self-pay customers (already at 10.6% of net operating revenues). These areas have not yet benefited from an improving economy and a recovery in volumes as compared to urban hospitals. However the expansion of private health insurance and Medicaid is expected to increase reimbursement from individuals who were previously uninsured/self-paying which should reduce bad debt expense in the future.

Uncertainty around healthcare reform

An increasing proportion of QHC’s revenues are expected to be derived from Medicaid / Medicare where the amounts received are usually less than the hospital’s typical charges for the services provided and the recent reform legislation has reduced the amounts that the government pays healthcare providers under these plans. The increased revenue share from Medicaid/Medicare could put pressure on margins as the rates received under these programs are less than those received from private payors and self-pay.

Secondly, the trend towards higher enrollment in Medicare managed care may have a negative impact on revenue growth as managed care patients tend to make less frequent visits to hospitals for emergency care and acute services. Like other rural hospitals, QHC has already experienced a significant increase in revenues from outpatient vs. inpatient services from 53% in 2011 to 57% in 2015 due to a combination of advances in technology which allow more services to be performed on an outpatient basis and pressure from Medicare/Medicaid programs as well as insurance companies to save costs by reducing hospital stays.

Valuation

We believe that the shares are fairly valued on a DCF basis assuming:

-

Revenue CAGR of 3.5%

-

EBITDA margins at 11-11.5% of net operating revenues

-

Capex at 3-4% of net operating revenues

-

5.0x terminal EBITDA multiple (no multiple expansion)

-

WACC of 10%

QHC expects 2016 revenues in the range of $2.2 - $2.3 billion (3-5% growth) and EBITDA of $265-275 million. Interest expense on the $1.3 billion of debt outstanding will be in the range of $100 million. 2016 Capex is expected to be $100 million of which $7 million is IT and $35-40 million is growth capex (primarily related to the Oregon facility expansion with ~$88 million to be spent over 2.5 years). Once the Oregon project is completed, capital expenditures (excluding acquisitions) are expected to normalize from 2019 onwards to ~$50-60 million or 2-3% of revenues as regular maintenance/growth capex (for the purpose of the projections, we have assumed that capex remains in the $100 million range). QHC’s free cash flow projections are given below.

The current share price reflects fairly modest assumptions around growth and margins and is not pricing in the optionality of a successful turnaround of the business and deleveraging potential from free cash flows. With the expected deleveraging, QHC should be able to refinance its debt at lower rates, reducing interest expense. The impact of a $100 million divestment of negative EBITDA hospitals would amount to $3.36 per share and improve free cash flows by approximately $20 million.

Sources/links

Investor Presentation

I and/or others I advise do not hold a material investment in the issuer's securities.

Catalyst

Reporting of Q2 results on August 11th and more engagement with investors

Portfolio rebalancing and divestment of unprofitable hospitals which should drive EBITDA margin expansion and multiple re-rating

Renewal of institutional investor interest once QHC becomes a larger market cap stock

| show sort by |