| 2018 | 2019 | ||||||

| Price: | 15.13 | EPS | .44 | 1.01 | |||

| Shares Out. (in M): | 47 | P/E | 35 | 15 | |||

| Market Cap (in $M): | 712 | P/FCF | 35 | 15 | |||

| Net Debt (in $M): | -42 | EBIT | 44 | 72 | |||

| TEV (in $M): | 670 | TEV/EBIT | 15 | 9 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- Unfixable

- perpetual value trap

Description

RGS is a very attractive under-the-radar turnaround with potential to double on the back of EBITDA increasing 67% over the next two years. There is a relatively new management team with an A+ CEO who is in high gear executing on a credible turnaround plan. A key part of the plan includes significant EBITDA improvement from recent steps to sell and franchise, or close, almost all of its underperforming salons. These improvements have not hit reported results yet and are unappreciated by the market. On top of this, it is a recession resistant business with a net cash balance sheet which provides stability, downside protection, and optionality for buybacks.

Business Overview

RGS is the largest hair salon chain in the US, operating 6,300 owned salons and 2,600 franchised salons under brand names such as Supercuts and SmartStyle. The salon figures are as of the most recent fiscal year ended June 30, 2017, but they are changing due to recent transactions as I’ll describe. RGS is primarily focused on the value segment with prices in the $18-$22 range for a haircut. The revenue mix is 77% Services, 20% Product and 3% Royalties and Fees. RGS receives a 4-6% royalty on revenue at franchised salons.

The 6,300 owned salons fall into four somewhat distinct brands/groupings with different dynamics and financial profiles. RGS does not neatly breakout profitability by brand, but there is enough info to piece it together as I’ll describe.

Supercuts

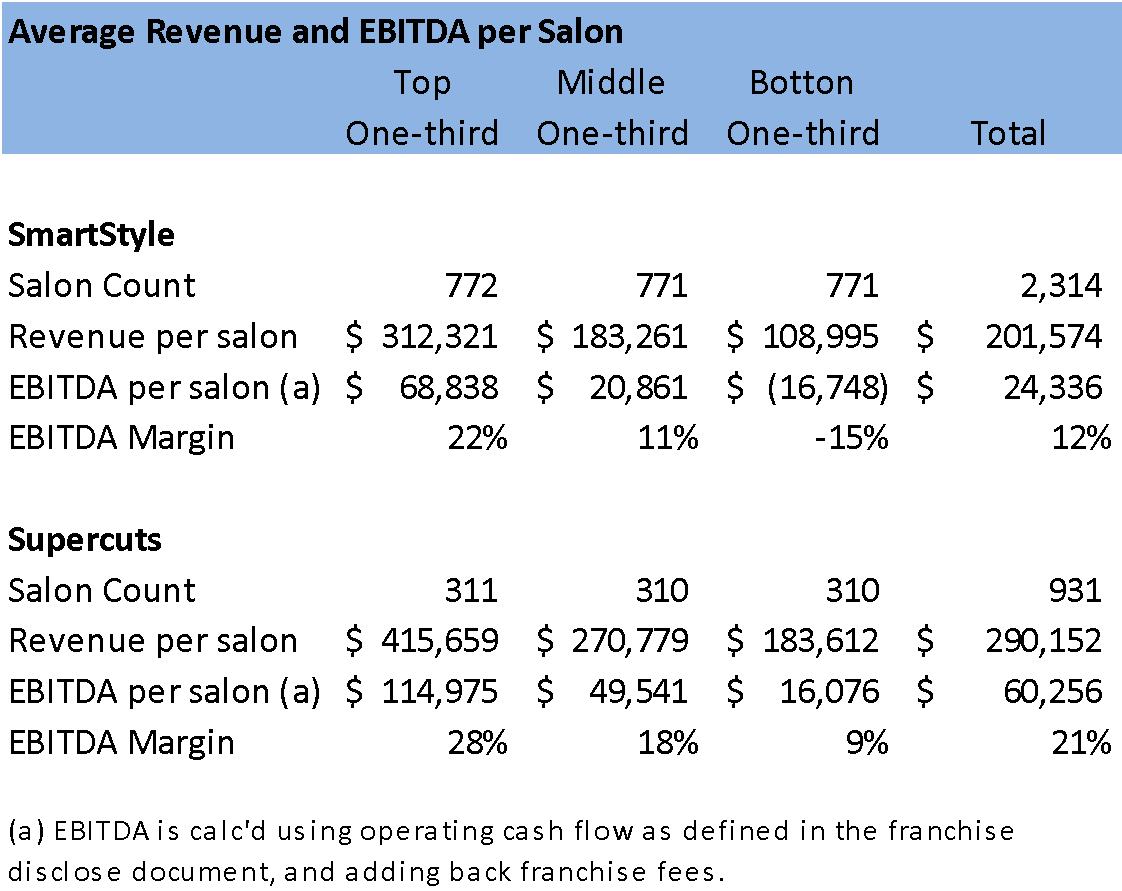

Approximately 1,000 Supercuts salons. This is RGS’s flagship brand and its best performing brand, with the highest margins in the company. The margins are disclosed in the Supercuts’ Franchise Financial Disclosure document (FFD). Conveniently, the FFDs break out margins for the top, middle and bottom third of Supercuts salons. Even the bottom third are decently profitable.

SmartStyle

Approximately 2,700 SmartStyle salons. The SmartStyle brand salons are located exclusively in Wal-Marts. This is a decently profitable brand which we can see in SmartStyle’s FFD. However, the bottom third are big money losers, costing RGS approximately $13mm of EBITDA at the store level before taking into account the associated regional management overhead. The table below shows the summary of the average revenue and EBITDA per salon for Supercuts and SmartStyle as disclosed in the FFDs. Note: these are the only two brands which RGS franchises, so they are the only two with FFDs.

Shopping Mall Salons & UK

Approximately 900 salons based in shopping malls under the Regis and Mastercuts brand names, and 250 UK salons. This grouping is RGS’s worst performer due to the negative traffic trends for shopping malls which have harmed many retailers. RGS recently sold and franchised these salons in late October 2017 and disclosed these salons were losing $4mm of EBITDA.

SignatureStyle

Approximately 1,500 SignatureStyle salons. This is a catch-all for a 50+ regional brands that RGS acquired when it was in a roll-up stage 10-20 years ago. You can back into the margins for this segment by subtracting the other segments from the total company results. The EBITDA margins are approximately 15%, so in between Supercuts and SmartStyle. However, like SmartStyle, I think the bottom third are losing money. I estimate the bottom third have negative EBITDA of $3mm.

Franchised Salons

Approximately 2,600 franchised salons consisting of roughly 1,700 Supercuts, 800 SignatureStyle and 200 SmartStyle.

Background

Consistent Underperformer & Activist Target

RGS has been consistently underperforming for years, with negative comps in seven of the last eight years, averaging -2% annually. The lead up to the present day requires some explanation. RGS was created through a roll-up in the 1990’s-2000’s and was run by its founders until the activist Starboard pushed management out in 2011 through a proxy fight. (Starboard invested at ~$15 per share in mid-2011, and the share price is relatively unchanged since them.) Starboard successfully argued that RGS was underperforming and had bloated costs. Shortly afterward, in 2012, Birch Run invested and joined the board. Birch Run remains RGS’s largest current shareholder.

Failed Turnaround Under Prior CEO

In 2012 Starboard brought in a new CEO, Dan Hanrahan, from Royal Caribbean, and a new CFO from Unilever. Long story made short, Starboard exited in 2012-2013 between $13-19 per share without much success. The CEO was never able to sufficiently improve the business. The CEO finally left after five years in April 2017 when he was replaced by the current CEO (more on the new CEO later).

The old CEO’s turnaround efforts were mainly focused on incremental operational improvements including better store management, formalized training, and closer district management support. He accurately identified the main problem, namely that the bottom one third of salons where unprofitable, bleeding comps, and dragging down the performance of the overall company. Unfortunately, his initiatives to fix the bottom third of salons with better management and training were insufficient. This was in part because it was too hard to outrun the secular traffic decline at shopping mall based salons. This leads up to the present strategic transformation and the bull case today.

Thesis

1. New CEO is a Rock Star

Simply put, the more you get to know the new CEO, the more you will be impressed with him. He’s been the CEO of nine companies as a turnaround manager, so he brings a lot of turnaround experience. People who have worked with him in the past think very highly of him. I think it is a very strong signal that he advised RGS as a consultant at Huron Consulting for six months, so he got under the hood before accepting the job. He says he only took the job because he knew he’d be successful, and he found the opportunity to be so attractive that he delayed his retirement in Florida to move to Minneapolis. On his first earning call he said, “This will be my last role as CEO. I have no intention of failing. I would not have accepted this role if I did not believe it could be done well.” We did several reference checks which were phenomenal. The punchline is that he is a force of nature with a rare combination of competence, intelligence, ethics, and drive, and he excels at pushing for change and creating value. I think his early actions at RGS are consistent with his reputation. We learned that his services as a CEO are in high demand, so RGS is lucky to have snagged him.

The CEO is well incented with 1.0mm shares of stock appreciation rights with a strike of $11.15, and 90K restricted stock units that vest if the stock is above $12.27. These awards are only exercisable after three years from his April 2017 start date, so the CEO is locked into the shares over a reasonable investment horizon. At my target price, the awards are worth $20mm.

2. Exit Virtually All Unprofitable Salons

The new CEO is in high gear executing a more radical plan to sell or close most of the bottom third of salons. This should reveal the profitable core business. He’s wasted no time since joining in April 2017. First, In October 2017 he announced the sale and re-franchising of 858 mall-based salons under the Regis and Mastercuts brands, as well as 250 Regis and Supercuts salons in the UK, to a private equity firm called Regent. While terms are not disclosed, RGS received negligible compensation and will receive a franchise royalty that ramps over a couple of years. These salons contributed negative $4mm of EBITDA in FY 2017. I believe the franchise royalty will contribute $8mm of EBITDA when fully ramped in two years (3.5% royalty rate on ~$230m of revenue). Second, in January 2018 he announced the closure of 600 underperforming company-owned SmartStyle salons (i.e. salons in WMTs). These salons were losing $17-$19mm of EBITDA.

3. Increase Franchise Mix

The new CEO is moving more aggressively to franchise stores. Obviously franchise royalty revenues are higher margin and garner a higher multiple, so this is a very positive shift. Management has not given targets around how many salons will be franchised beyond saying it is “an important element of the strategic transformation.” Shortly after the new CEO joined, he announced that RGS reached agreements to sell 200 SmartStyle salons to franchise owners, and he promoted the General Counsel to the new position of President of Franchise Operations to help accelerate the franchise effort. Management has said they are open to opportunistically selling clusters of salons to private equity similar to the large transaction with Regent in October.

RGS receives a 4-6% royalty rate on revenue at franchise stores. RGS does not breakout the margin on franchise royalties (instead it groups royalties in with product sales to franchisees). I assume a 60% EBITDA margin on royalties although other public franchise companies have 80% EBITDA margins.

4. Operational Improvements

The new CEO is making common sense operational improvements which should yield success. First, in October, RGS announced that it is repositioning the SmartStyle brand. Previously it was a positioned as a slightly higher-end full service salon catering to women (think color, blow dries, etc). Now it is being positioned as a value oriented brand for busy families (think getting your three kids quick haircuts during a Wal-Mart shopping trip after soccer on Saturday morning). Our channel checks were unanimous that Smartstyle’s prior brand positioning was idiotic because women don’t think of going to Wal-Mart for a “salon experience.”

Second, RGS is stepping up its marketing efforts. The new CEO almost immediately replaced the head of marketing when he joined, and RGS is making major pivots including: 1) RGS is starting to advertising the SmartStyle brand for the first time. Oddly, it is RGS’s biggest brand in terms of salon count, and they have never advertised it. 2) RGS is starting to do digital/mobile marketing for the first time. It has partnered with Buxton & Co which does consumer analytics for 4,000 retailers. 3) In January it announced an exclusive multi-year sponsorship with Major League Baseball for promotions around games and including broadcast, digital, mobile and social.

Third, RGS has a sophisticate labor scheduling system which matches stylist hours to demand levels. Under the old CEO, RGS used the data to offer guidance to store managers, but ultimately store managers had discretion over labor scheduling. This led in some cases to long waits at peak hours, like Saturday mornings, and overstaffing at slow times like Tuesday mornings. New management has now taken discretion away from store managers and corporate is dictating staffing hours to the salons. Management has said they are already seeing a significant benefit from this change.

Fourth, RGS is cutting corporate G&A, with new management saying that RGS is relatively inefficient. For example, last quarter RGS announced it is reducing headcount by 65 at headquarters. However, I don’t expect an absolute cut in SG&A because I think the efficiency savings will be used to fund increased marketing.

5. Major Investor on the Board

Birch Run owns 23% of RGS and has been on the board for six years. Given the long term struggles at RGS, Birch Run obviously has a strong incentive to turn the business around.

6. Stable Recession Resistant Business

Everyone has to get their hair cut on a semi regular basis. It is a simple and essential service business, and demand is fairly stable. There is no threat of technology disintermediation, offshoring, or getting the merchandising wrong (to use a retail analogy). Demand show grow with the population and pricing should grow with inflation.

7. Conservative Capital Structure

RGS has a net cash balance sheet with cash of $3.50 per share, and net cash of $0.90 per share. Cash is 23% of market cap. Gross debt is only 1.4x EBITDA. Management has offered minimal guidance on the capital structure going forward beyond saying they will eventually look at buybacks, and that the gross leverage level is on the light side.

8. Underfollowed Company

RGS is only followed by one sell side analyst. RGS has not given financial targets, and so far management is leaving it to investors to connect the dots regarding the financial impact of the strategic transformation taking place. I think this helps create the opportunity today. As an aside, management is not promotional, keeps their heads down, and does not offer any guidance. In my view, the lone sell side analyst is totally overlooking the EBITDA improvements from the recently announced salon closures/sales, not to mention the other operational improvements.

9. Good Fit for Private Equity

RGS would seem to be a good fit for a private equity acquirer because its enterprise value is not too large, the business can sustain high leverage, and there is ample opportunity to create value from operational improvements.

The Numbers

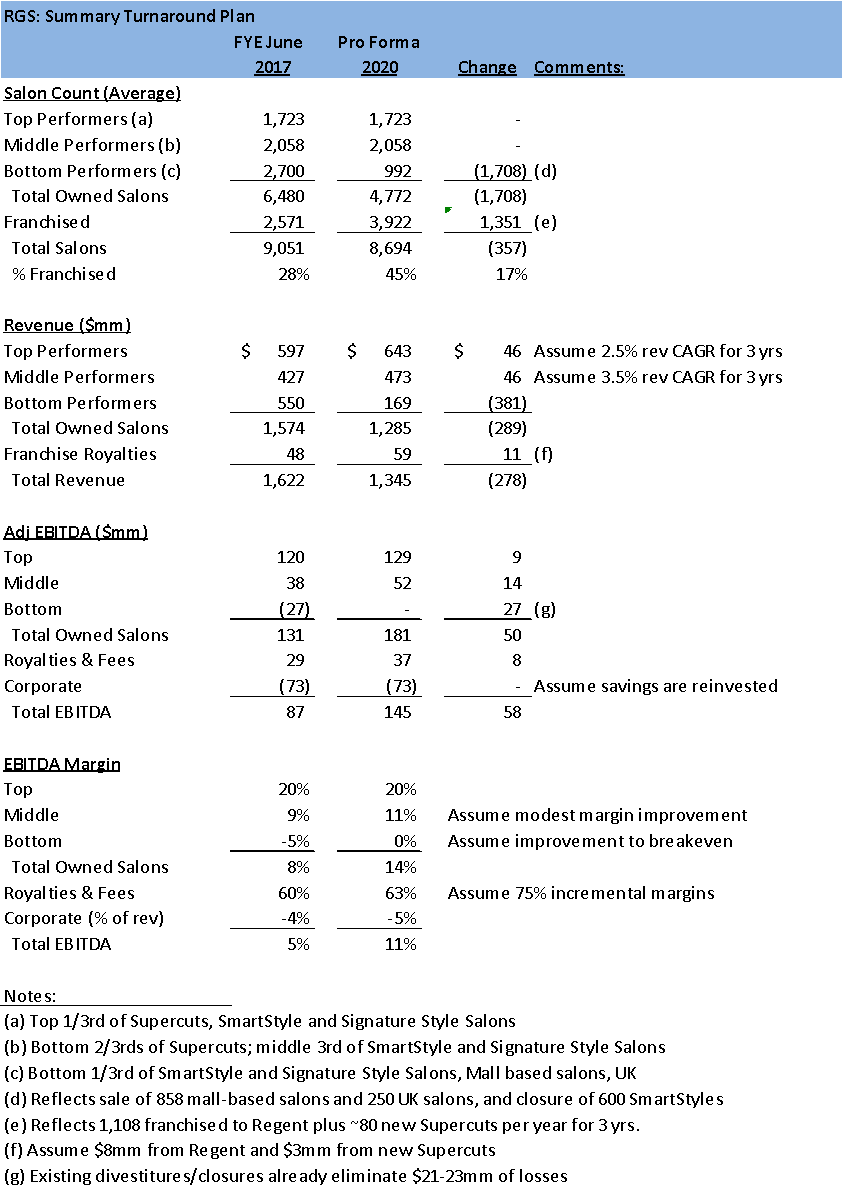

Below is a summary of my bridge from $87mm of EBITDA in FY2017 to $145mm in FY2020. I’d note that RGS already announced the sale/closure of unprofitable salons which were causing a $22mm EBITDA drag, so this implies current pro forma EBITDA of $109mm, and that’s before any other operational improvements. The lone sell side analysts forecasts FY 2019 EBITDA of only $90mm.

The detail behind this bridge comes from my effort to dis-aggregate the business into the top, middle and bottom performing salon groupings using data extrapolated from the FFDs mentioned above, and from RGS’s other disclosures. The basic assumptions are: 1) RGS eliminates all of its unprofitable salons either by closing/selling or fixing. This is not a stretch because RGS has already resolved ~80% of its money losing salons with the announced sale and closures. 2) The middle performing salons experience a modest 200 bps EBITDA margin improvement from 9% to 11% as a result of the common sense operating improvements. These salons are still far less profitable that the top performing salons which have 20% EBITDA margins. 3) The topline grows at a low single digit rate (LSD). I assume the top performers comp at an inflation like 2.5% while the middle performers comp at 3.5% because there is more room for improvement as a result of initiatives like increased marketing. 4) Franchise royalties grow as a result of the sale and franchising of the 1,100 salons to Regent (I assume a 3.5% royalty rate vs the typical 4-5% for other franchisees, although it is not disclosed) as well as business as usual new franchise openings. Note: I am not assuming any additional large sales of owned salons to franchisees, although there is optionality for that to occur.

Stepping back as a sanity check, I assume RGS gets to an 11% EBITDA margin which I think is very reasonable because most half-way decent retailers have EBITDA margins in the double digits. Furthermore, while management has not given guidance, I think they feel very comfortable with a double digit EBITDA margin.

Here is the summary output of my assumptions so you can get a sense for the moving parts:

Valuation

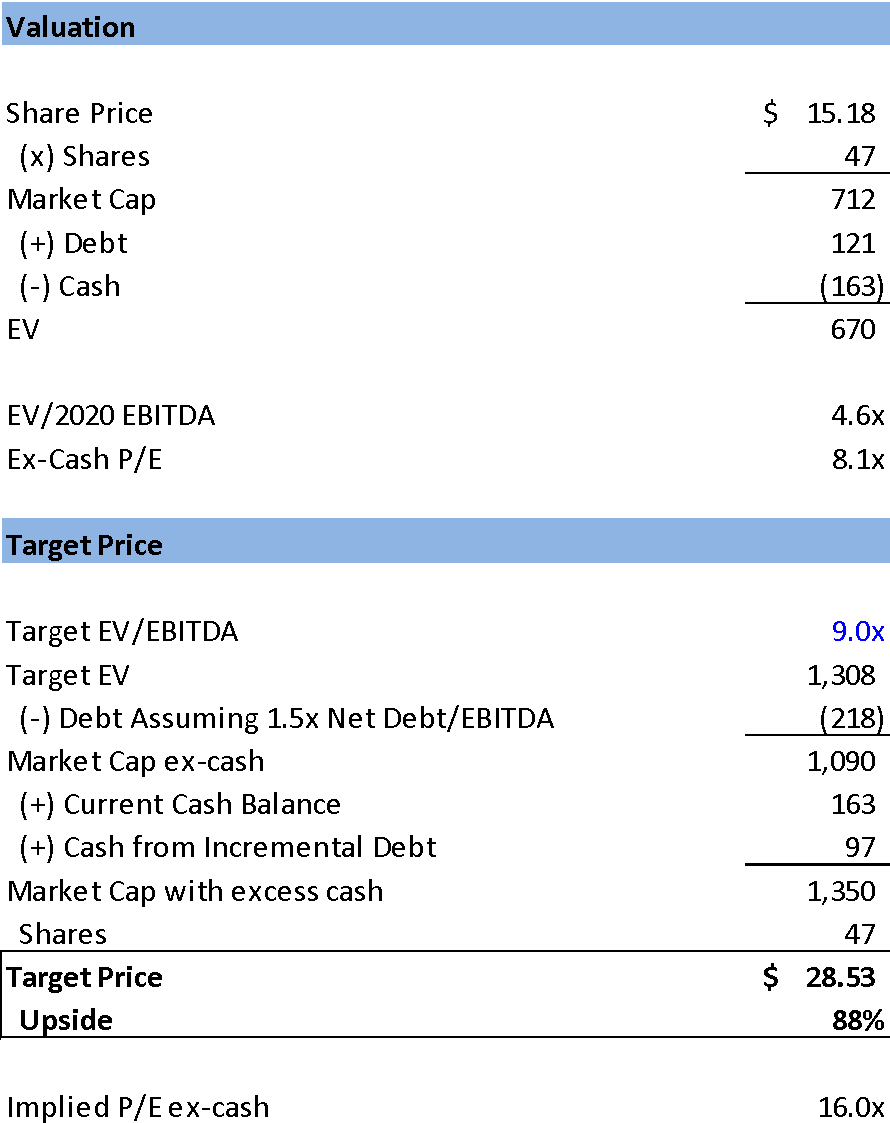

On my forecasts, RGS trades at less than 5x FY 2020 EBITDA and 8x EPS ex cash. Because RGS has a large cash balance, I think it makes sense to look at the P/E excluding the cash. For a price target, I assume 9x EBITDA and 16x earnings. I think these are reasonable multiples for a stable, profitable, branded hair salon chain which is partially franchised. I also assume that RGS adds incremental debt while maintaining a conservative 1.5x debt/EBITDA ratio. This results in an additional $100mm of cash by the end of FY 2020. So, RGS ends FY2020 with almost $6 per share of cash. In reality, I assume most of this cash will be allocated to buybacks.

Issues

The Turnaround has Already been Tried Before

In other words, why will the new CEO’s operational improvements work when Starboard’s handpicked CEO could not get it done? First, it was the prior CEO’s first time being a CEO, and in hindsight his experience as an executive at Royal Caribbean was not especially relevant. Second, the new CEO is clearly taking a much more aggressive approach to fixing the business as seen by the multiple changes he’s made in his first year, notably the sale and closure of unprofitable salons. Third, the operational improvements sound like common sense: digital marketing, repositioning SmartStyle (i.e. Wal-Mart) to be more low-end, cutting corporate G&A, better optimizing labor hours, etc. The prior CEO did not do any of these things.

Competition

It is a competitive business and RGS has faced incremental competition from the rise of other chains such as Sport Clips and Great Clips which have “fresher” concepts and make better use of technology (e.g. allowing customers to track wait times on their smart phones). There is competition to attract and retain stylists. It is also price competitive. Customers will move in order to save $1 on a haircut. I think the rise of competition has contributed to the slow bleed at RGS in the last five years, but the new CEO is taking steps to help RGS regain its competitive mojo, for example the partnership with MLB.

CEO is Not Permanent

Reading between the lines, I think the CEO will be at RGS for 2-3 years in total, so another 1-2 years from this point. He’s 63 and has delayed his retirement for this job. He’s said his plan is to eventually recruit an outside CEO and manage the transition. I think the CEO will only leave after declaring a decisive victory.

IT System Upgrade

Management has talked about needing to upgrade its IT systems. Sounds like it is a long term project that is still in the contemplation phase and might not ramp until 2020. RGS has aged systems, and the new upgrade is expected to result in significant cost saves, but there will eventually be incremental capex and potential for distraction.

Minimum Wage Increases

Stylist wages are obviously a big cost for RGS. So far RGS has been able to pass on minimum wage increases through higher pricing, and it is confident that it can continue to do so. Positively, RGS expects higher minimum wages to result in less stylist turnover.

This posting is solely for the evaluation of club members and is not a recommendation to buy or sell this stock. The views expressed are those of the author individually and should not be attributed to any affiliated investment firm, which may or may not hold positions consistent with the views expressed herein and may buy or sell shares at any time.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

Executing on the turnaround plan.

| show sort by |