| 2017 | 2018 | ||||||

| Price: | 7.71 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 415 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 4,120 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 1,362 | EBIT | 0 | 0 | |||

| TEV (in $M): | 5,484 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

Description

Introduction

RPC is a large, defensive, plastic packaging company trading at 6.8x FY2019 (CY2018) EBITDA with peer leading organic growth (3% CAGR) and an under-levered balance sheet (1.8x). The setup seems too good to be true, leading many to doubt its veracity, which has ironically (partially) created the opportunity to buy this business at a massive discount to industry competitors. As we will explain, we think the short thesis espoused by a small sell-side research firm in the UK (Northern Trust/Aviate) is incorrect and benefited from a technical overhang tied to the RPC shareholder base. Our diligence suggests RPC is a best in class operator with solid assets. With approximately £600 GBP of PF EBITDA, we view RPC as the BERY of Europe, rolling up the European market as BERY rolled up the US. Applying a multiple between BERY and the broader peer set (despite our belief that this business should trade at a premium), RPC is worth 50-80% higher than the current quote.

Business

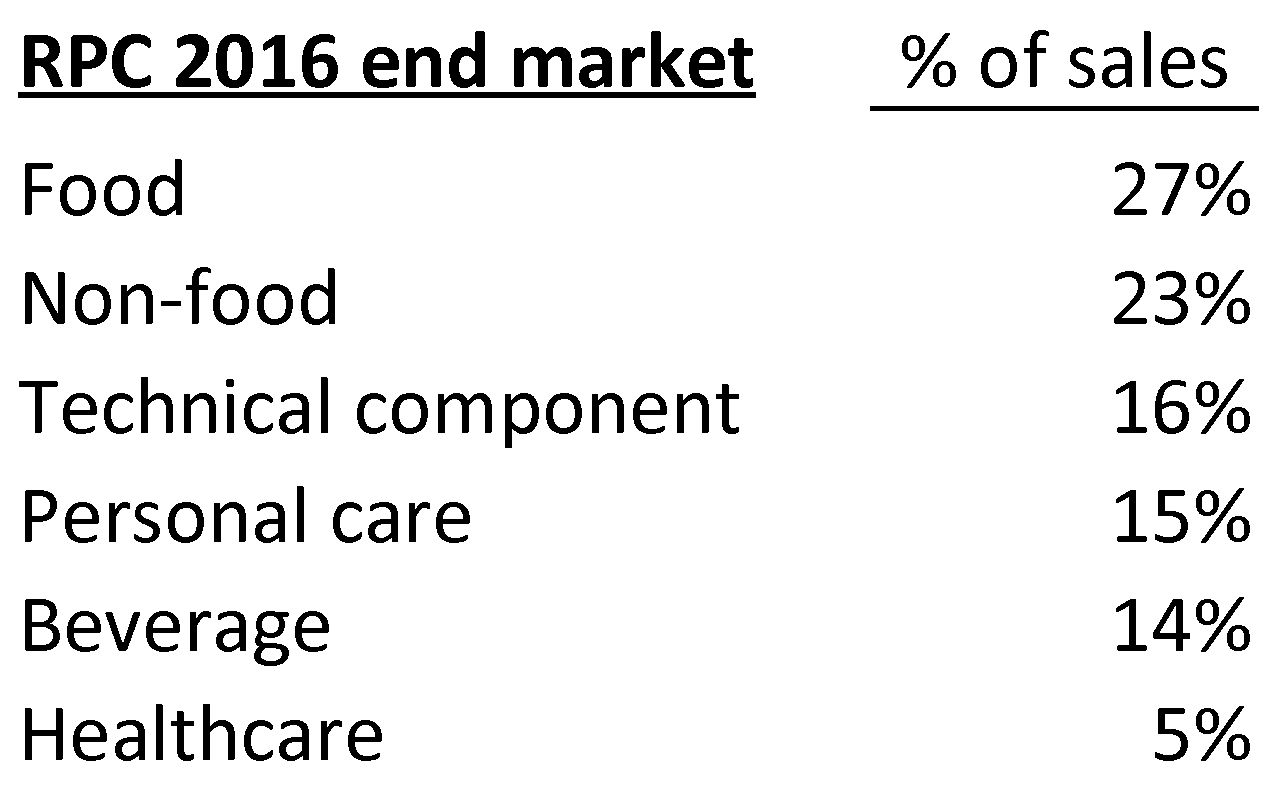

RPC is a global plastics manufacturer supplying to a diverse set of end markets with a host of patented / technically sophisticated product offerings. It has been predominantly focused on European rigid plastic containers but has recently diversified into other geographies and into flexible container end markets. RPC’s peers include companies such as Berry, Aptar, Bemis, Sealed Air, Amcor, and other plastics manufacturers. RPC’s £3.6bn of sales exposes them to the following end markets:

The European plastic packaging market can generally be described as a stable GDP+ business. Plastic containers have been a strong market over time, generally taking market share from other packaging materials. This, in conjunction with lower per capita consumption in Europe relative to the US, creates opportunities for further market penetration. On the negative side, increased light-weighting decreases plastic use and general pressure from certain competitive markets (such as consumer packaging) dampen some of the industry upside potential. Generically, the industry is stable with consistent cash flows, leading to strong market valuations.

Background

Context is important for understanding the current predicament that RPC has found itself in. RPC was historically a sleepy European packaging company focused on a few niche markets. Approximately 4 years ago, Pim Vervaat took over as CEO the company started to execute on an acquisition strategy. There have been two types of acquisitions. The first type of acquisition is larger in nature with real synergies that result from increased scale, footprint optimization, cross-selling opportunities, and restructuring of acquired operations. These types of acquisitions include Superfos, Promens, GCS, and BPI. The other type of acquisitions are small roll-ups that are primarily used to leverage RPC’s scale and technical knowhow to reduce polymer costs while keeping the operations largely intact.

In these 4 years, RPC has grown from a £1bn in sales and £1.5bn EV company to becoming a £3.6bn in sales and £4.3bn EV company. With only 1.8x of leverage, RPC funded the majority of the acquisitions through equity rights offerings.

The acquisition / rights offering strategy worked well for a few years and shareholders were rewarded with strong stock returns. However, a problem started to emerge - to fund its numerous rights offerings, RPC forced its cadre of small capitalization London investors to consistently subscribe to its rights offerings in ever increasing size, forcing increased capital exposure to the company. We believe this resulted in many investors owning too many RPC shares relative to their other portfolio holdings. This shareholder over-exposure is not relevant as a stock performs (investors are patting themselves on the back for a good investment decision), but when things stop “working”, “de-risking” ensues. In this instance, a confluence of events has led to substantial “de-risking” in RPC shares and a material de-rating of the valuation of the company. Early this year, RPC announced the acquisition of a US company called Letica, financed, as usual, through a sizable rights offering. Secondly, the company was attacked by a short report put out by Aviate, a small broker dealer subsidiary of Northern Trust, that to our knowledge, does not have a history of advocating short sales. The short report focused on a few specific things:

-

When examining the polymer pass-through accounting, the deterioration of the underlying business became clear

-

Labor inflation was on the rise in Europe which should squeeze margins

-

FCF items were mislabeled and underlying FCF quality is poor given the multitude of restructuring and exceptional items

-

Management incentives were poorly designed

While the Company increased the level of disclosure with its last earnings call in order to address some of these concerns, the stock sold off after the earnings as Northern Trust/Aviate continued its short call and long investors continued to de-risking (to our knowledge, the short interest in RPC is fairly small). At this point, even benign criticisms from Northern Trust/Aviate leads to substantial declines in RPC stock. In the universe that houses RPC shares, Northern Trust/Aviate is more powerful than the best short sellers - Muddy Waters, Jim Chanos, pick your favorite. Northern Trust/Aviate can question with impunity the veracity of all numbers with the market in apparent full agreement with their conclusions.

While the bear case continues to morph, we believe the Northern Trust/Aviate bear case is currently premised on the following:

-

Concerns around exceptional items and FCF

-

Given that company acquired over ½ of its sales in the last few years, there is significant integration of operations and severance leading to elevated exceptional items causing optically lower than expected “clean” CFFO and FCF numbers

-

Concerns around the M&A strategy

-

Management defended its M&A strategy on its recent earnings call (expecting a strong stock price reaction from a strong set of numbers), which appeared to not be what the market wanted to hear. It seems shareholder’s want to see the FCF and earnings proven out to disprove the bear base before returning to the large acquisition roll-up strategy

-

Funding mechanism for their M&A strategy is broken

-

The company has historically funded acquisitions through rights offerings, which is a much higher cost of capital than debt. Given the currently depressed multiple, the equity market is essentially closed for executing on further transactions. Furthermore, UK investors seem to be less comfortable with leverage so the company is reticent to use lower cost of capital debt to fund their strategy. This has hamstrung RPC as it can’t aggressively pursue its M&A strategy, leaving many investors questioning whether this is “dead money” until they can prove out their earnings and FCF. In the private markets, RPC could utilize far more balance sheet leverage, a significant incentive for RPC to go private.

Primary diligence

We did a number of calls with former employees of RPC and competitor employees. I have included some select takeaways below:

-

Former employee of RPC (spent significant portion of career at RPC and 20+ years in packaging)

-

Company is extremely well run with professional leadership

-

Thinks M&A process was incredibly selective and done thoughtfully while he was there

-

Promens, GCS, and BPI offered opportunity for significant synergies given overlapping sites

-

Synergies take time – 2/3 years to integrate larger transactions with plant closures is not unreasonable

-

Organic growth has upside once through acquisition integration given factory moves and restructurings

-

Questioning of accounting is unreasonable; nothing but integrity when he was there and strong working relationship with Big 4 accounting firms internally

-

Significant opportunities from Letica acquisition integration with legacy Superfos assets

-

Former employee of RPC (spent significant portion of career at RPC and ~20 years in packaging)

-

Pim is a capable leader with a strong ability to balance details versus big picture issues

-

Synergies were historically achieved or exceeded even if it took more time and costs than initially thought

-

Letica / Astrapak are great types of acquisitions for RPC

-

Organic growth is quite reasonable and ~3% would be his “base case”; thinks their growth capex supports this compared to peers

-

Members of the senior management team have extensive experience and are thoughtful around M&A

-

CEO of competitor

-

Management viewed favorably – feedback is they are focused and good at driving productivity and are operationally focused internally

-

No structural reason their margins should be lower than peers

-

Thinks organic growth targets are reasonable and believable

-

Synergies take time and cost to flow through – no surprise about financial statements

-

Did not give much credence to the short report – thought the main points were either misguided or incorrect

-

Thinks it’s a good collection of assets that could be a potential take-out target if strategics or PE wanted to expand into Europe

Furthermore, given the implicit allegations of accounting shenanigans, I think the auditors bear mention here. Following EU accounting rule updates around the length an auditor can serve, the company decided to put out to tender for its external auditor. As a result, the company switched from KPMG to PwC in 2015. Furthermore, the company hired Deloitte as its internal auditor as well (around the same time). Fraudulent companies would seem unlikely to change auditors (presumably adds risk of getting caught) and having a company employ three out of the big four auditors should give comfort that the accounting controls are sound.

Insider Buys

After the recent stock move, there have been several insider buys as detailed below in early June:

-

Pim Vervaat, CEO - ~£77k

-

Simon Kesterton, CFO - ~£76k

-

Jamie Pike, Chairman - ~£100k

-

M G Towers, Audit Chairman - ~£76k

It is also worth mentioning that on 2/24/17, in conjunction with the rights offerings to acquire Letica, the CEO, CFO, and several members of the board subscribed by monetizing outstanding options and putting new money into the company:

-

Pim Vervaat, CEO - ~£140k

-

Simon Kesterton, CFO - ~£43k

-

Jamie Pike, Chairman - ~£166k

-

M G Towers, Audit Chairman - ~£43k

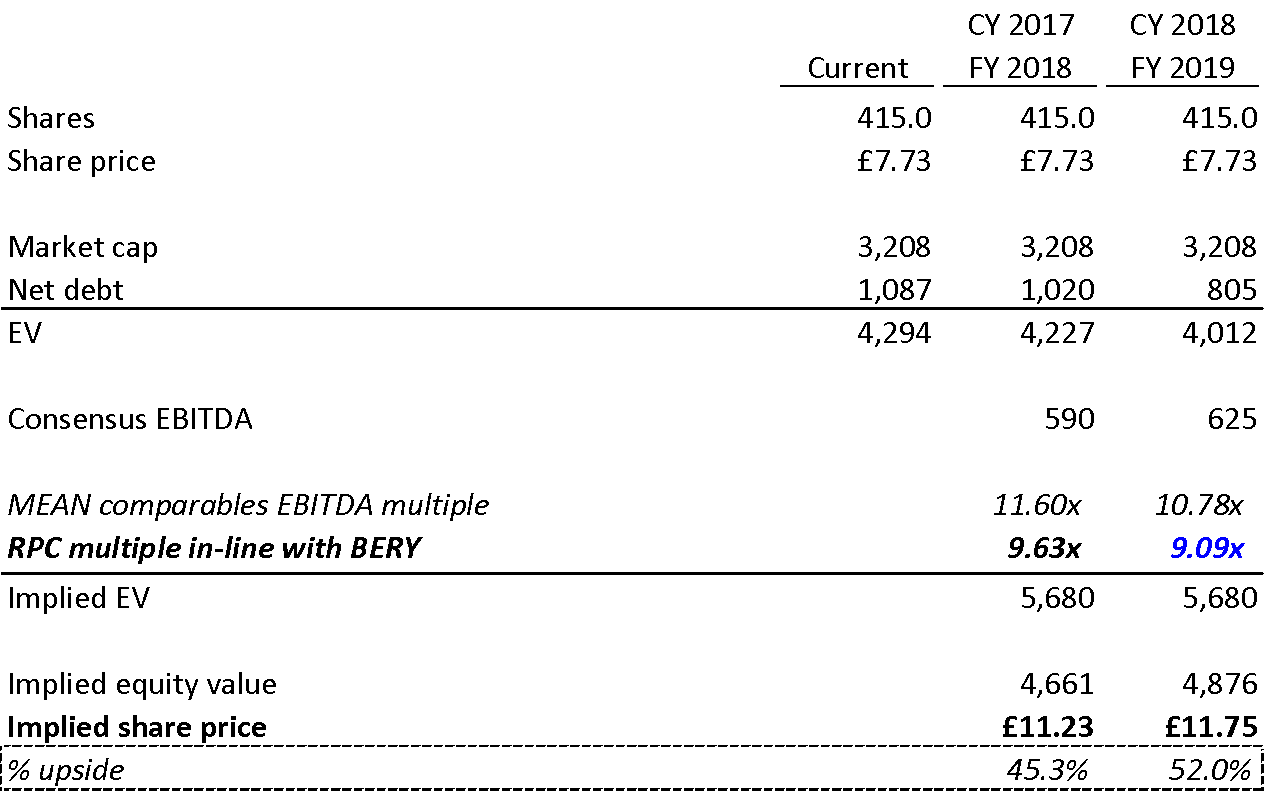

We believe this confluence of factors has created an incredibly favorable risk/reward skew. We have included a comp table below and the upside should be clear as the company is cheap both on a relative and nominal basis. Applying a multiple between BERY and the broader peer set, RPC is worth 50-80% higher than the current quote.

Note: RPC’s shown 2018 EBITDA is for FY2019 EBITDA (ended 3/31/19); BERY’s shown 2018 EBITDA is for FY2018 (ended 9/30/18); Amcor’s shown 2018 EBITDA is the blended average of FY2017 and FY2018 as its fiscal year ends 6/30.

Source: Bloomberg estimates

Below, we will walk through the bear case and why we think it is misguided. In our opinion, the market is assessing a high likelihood of the bear case being true. While messy and complicated, we believe that most FCF issues can be explained by analyzing industry comparable transactions and we hope that as more investors spend time on RPC and, as the company’s financials become cleaner, the stock will rerate.

Analysis

It is important to start with the initial short report as the stock continues to react to negative notes put out by Northern Trust/Aviate. Let’s start by examining the first two parts of the initial short report:

-

The underlying business is deteriorating when you examine the Polymer accounting

-

The main tenet of the thesis was that, given the tailwind from Polymer, the company should have had much higher earnings. The company passes through polymer costs on a 30-60 day lag (as do most plastics companies), so when polymer prices move down, the company should generate a meaningful earnings tailwind. However, the short report looks at simply the YoY change in polymer pricing, not the sequential change, and thus is doing the wrong mechanical calculation. Secondly, the short report uses the wrong polymer indices when attempting to prove its thesis. It is our understanding that the company reached out to Northern Trust/Aviate and explained the fault in that logic as well as providing more disclosure around polymer costs in the latest earnings note. Subsequently, Northern Trust/Aviate seemingly abandoned this initial accusation in its 6/6/17 note.

-

European wage inflation is increasing and should squeeze margins

-

This one seems silly. Firstly, if there was inflation in Europe it would probably be because of good economic conditions benefitting GDP growth and this company. Secondly, the concept that there is secretly labor inflation in only the plastics industry workforce that will negatively affect these types of companies seems unlikely.

While these main points have been largely disproven or ignored, the point around FCF is one that is more difficult to explain and is empirically true, giving credence to the Northern Trust/Aviate. While Northern Trust/Aviate Trust has seemingly stopped publishing notes, the institution occasionally put out blurbs attacking the company that lead to sizable stock moves.

In our opinion, to believe the bear case and sell the stock at this valuation, you must believe a few things about the company’s FCF potential:

-

The cash costs to achieve the stated synergies are too high

-

The timeline for achieving these synergies doesn’t make sense

-

The pro forma margin profile of the company doesn’t make sense in the context of the industry

-

The company’s capex spend doesn’t make sense

Stepping through these individually:

-

The cash costs to achieve the stated synergies are too high

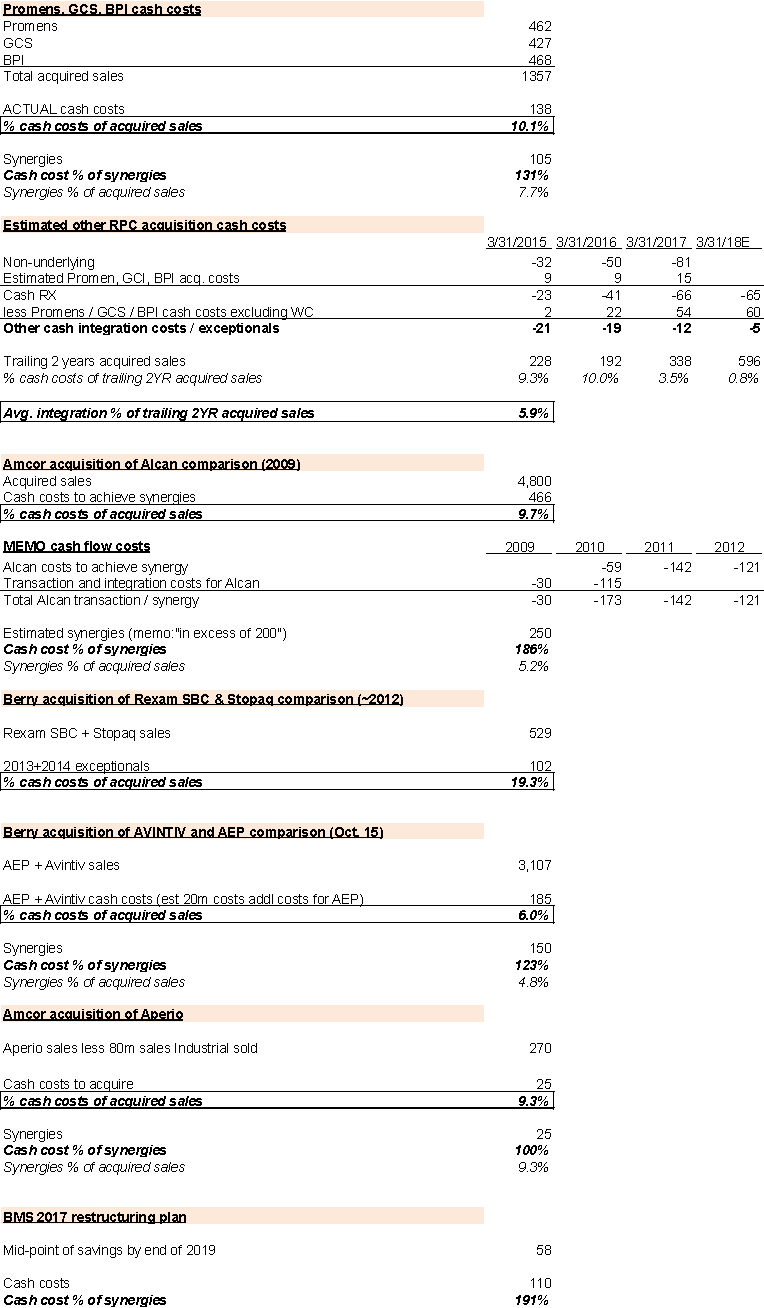

A reasonable way to judge the synergy targets is to examine them as a % of acquired sales and compare them to other successful acquisitions in the space. We include some quick analysis below with the takeaway that RPC synergy targets and restructuring costs appear reasonable compared to peers:

Source:Bloomberg estimates, company financials

The best comparable is probably the Amcor acquisition of Alcan packaging. It is similar in size in terms of percentage of sales being integrated, and is primarily a European based business. As you can see, the cash costs as a percent of acquired sales is pretty similar to the cash costs to acquire the synergies that RPC has set out.

Looking at Berry, it is clear that the cash cost to enact synergies is lower as a percentage of sales. However, European acquisitions like Alcan, Promens, BPI, and GCS have more stringent payments associated with severance and lease cancellations so this intuitively makes sense.

This analysis serves to illustrate that, while incredibly messy, the guidance RPC gives for cash costs as a percentage of acquired sales, synergies as a percentage of acquired sales, and cash costs as a percentage of synergies is relatively in line with industry peer metrics. Given these examples, it seems reasonable that the FCF will revert to peer levels (as management has guided) over the next few years.

-

The timeline for achieving these synergies doesn’t make sense

Looking at the Alcan acquisition – it was acquired in in FY2009 and completed in 2012 – it required 3 years of full integration. Looking at Berry, Avintiv was acquired in October 2015 and is still being integrated through this year. BMS is guiding their most recent restructuring plan to fully benefit results by the end of 2019. Thus, integration time seems to be somewhere between 2-3 years. RPC acquired Promens in early 2015 and GCS/BPI in early/mid 2016. RPC is guiding for cash costs to integrate these acquisitions to roll off after 2017. Again, these timelines seem consistent with peers.

-

The pro forma margin profile of the company doesn’t make sense in the context of the industry

Without getting into too much detail (mix, geography, scale, etc), a simple comparison suggests that RPC’s Adjusted EBITDA margins aren’t crazy in the context of the industry once exceptional charges roll off.

Source:Bloomberg estimates

-

The company’s capex spend doesn’t make sense and its FCF is lower than its peers

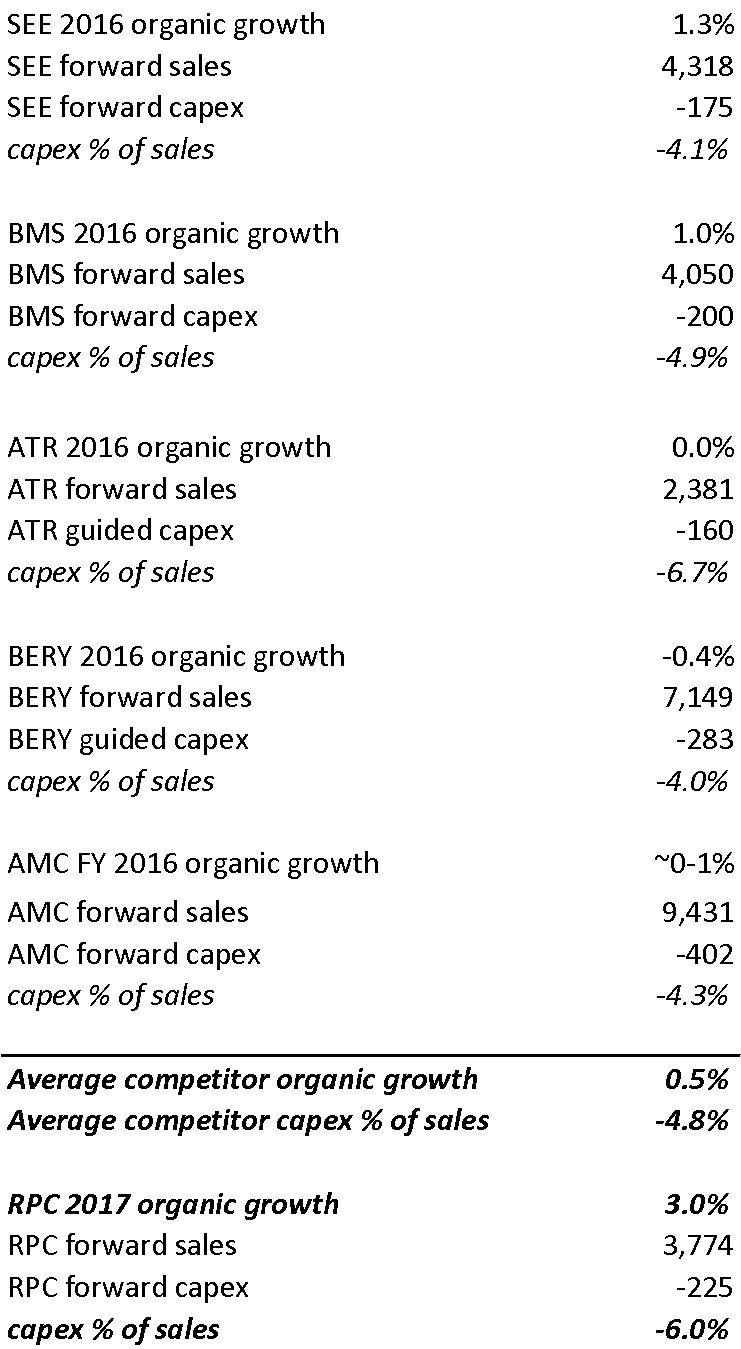

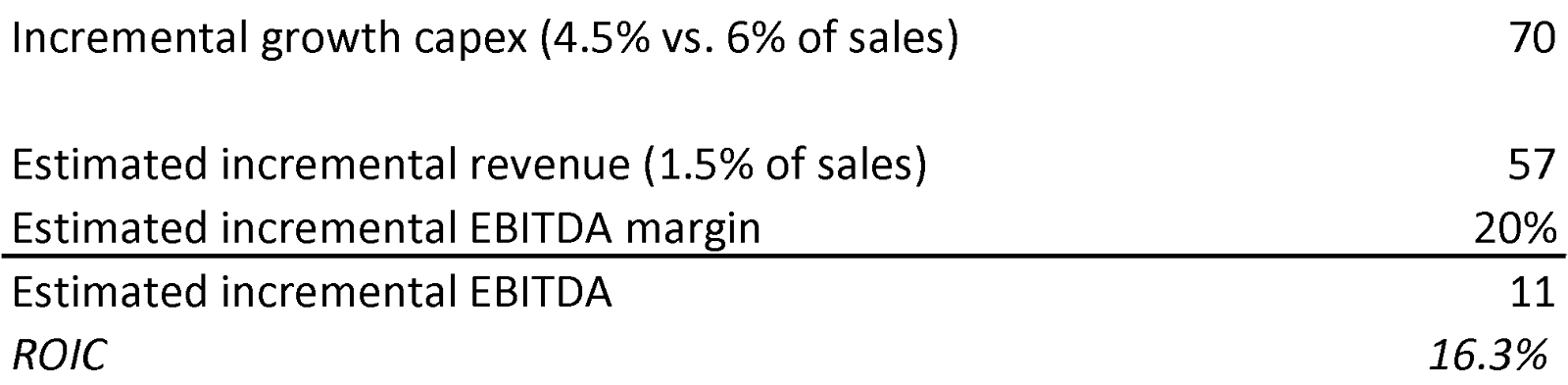

One of the factors that obfuscates this companies FCF yield relative to peers is its capex in excess of D&A. While one could criticize the company for spending more capex as a percentage of sales relative to its peers, RPC’s results suggest that it higher level of capital spend leads to superior organic growth. A comparison across peers illustrates RPC’s strength:

Source:Bloomberg estimates, company financials

This is actually a good use of capital when you compare their growth relative to peers.

Clearly, spending the growth capex in order to grow EBITDA makes sense on a ROIC basis. This is also important to note as the FCF valuation relative to US peers needs to be normalized in order to fully understand its relative valuation. Furthermore, one should remember that RPC is much less levered when comparing its valuation to something like a BERY that is 4.3x net levered. Looking at valuations on an enterprise value to cash flow basis (we use EV/EBITDA – Capex) normalizes for balance sheet leverage.

Source:Bloomberg estimates, company financials

BASE CASE VALUATION

Source:Bloomberg estimates, company financials

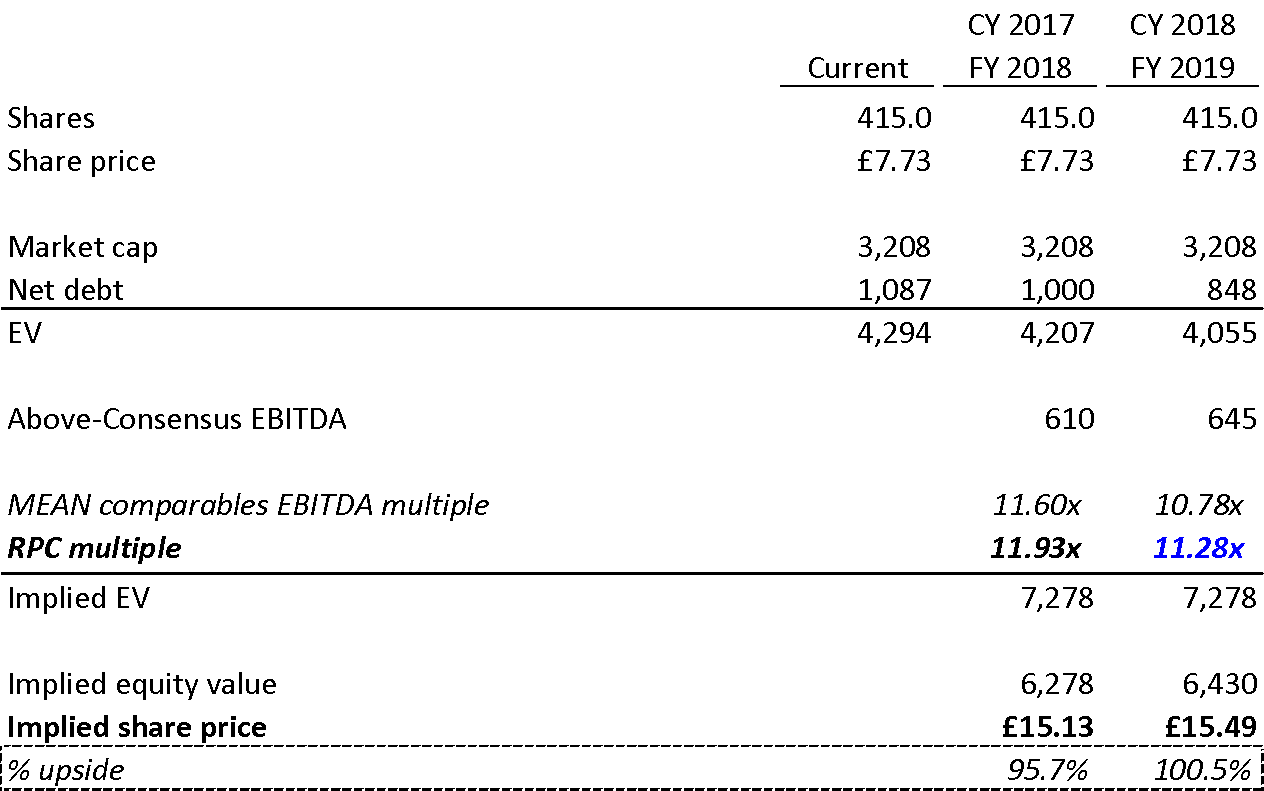

BULL CASE VALUATION

For the bull case, we apply a premium multiple to an above consensus EBITDA given the company’s superior organic growth and M&A integration strategy.

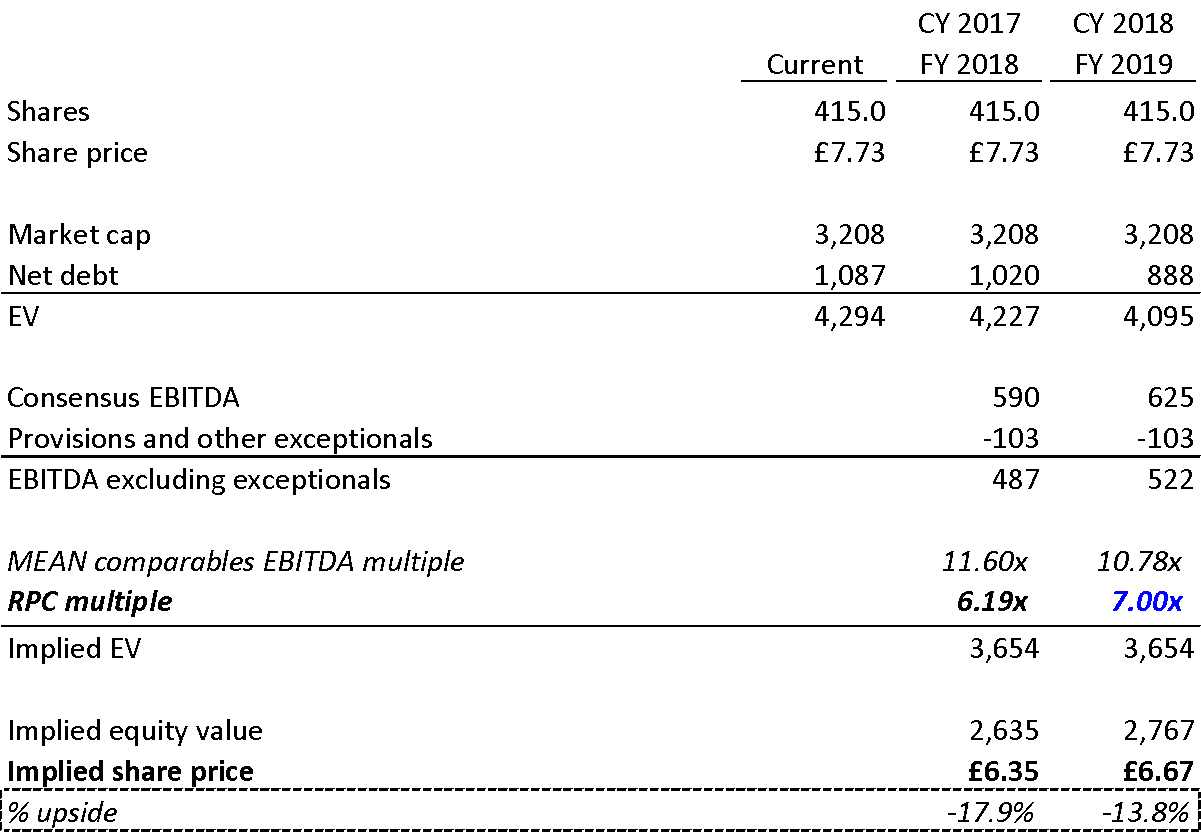

BEAR CASE VALUATION

For a bear case, we assume a heavily discounted multiple on current year EBITDA and assume all the guided exceptional charges are real and never roll-off:

Source:Bloomberg estimates, company financials

Conclusion

We think the market has heavily discounting the bear case being true for RPC, an outcome that our diligence suggests is unlikely. As we highlighted earlier, our checks with former employees and industry contacts did not suggest any operational or asset quality red flags. The risk/reward skew in RPC seems super attractive and could ultimately result in the company being taken private for a substantial premium.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

- Re-rate as FCF converts

- Takeout by Strategic or PE

- Change in capital allocation / management behavior

| show sort by |