| 2008 | 2009 | ||||||

| Price: | 6.13 | EPS | |||||

| Shares Out. (in M): | 0 | P/E | |||||

| Market Cap (in $M): | 1,540 | P/FCF | |||||

| Net Debt (in $M): | 0 | EBIT | 0 | 0 | |||

| TEV (in $M): | 0 | TEV/EBIT | |||||

Sign up for free guest access to view investment idea with a 45 days delay.

- SILVER WHEATON CORP SLW S 04/25/2012

- BETA

- ISHARES SILVER TRUST SLV 12/07/2010

- US Silver & Gold Inc. USGIF 10/24/2013

- ISHARES SILVER TRUST SLV 02/27/2017

- PERRIGO CO PLC PRGO 03/08/2016

- GLD Call Option Spread GLD 01/18/2012

- ISHARES GOLD TRUST IAU 06/02/2018

- CENTRAL FUND CANADA -CL A CEF.A 03/02/2015

- BARRICK GOLD CORP GOLD 07/17/2021

- SPDR GOLD TRUST GLD 03/15/2010

Description

Executive SummaryTraditionally, miners have desired to hedge precious metal prices to lower their very high risk. However, historically miners who have hedged were punished with lower multiples since most of the investors in precious metal shares are speculators looking for upside to prices. Thus, Wheaton River (a predecessor entity to Goldcorp) came up with the novel idea of spinning out silver production from their Luismin mine into a separate entity, SLW, in October 2004. Thereafter SLW slowly matured from its initial purpose as a vehicle for hedging/unlocking value from Goldcorp’s significant silver production at Luismin to an independent company, with a fully independent board and management (though everyone at SLW used to work at Goldcorp and their office is in a Goldcorp Building). As an operating company SLW has signed 8 new deals and has not needed to fund any of its projects through equity financing since April 2006.

Description of Mines

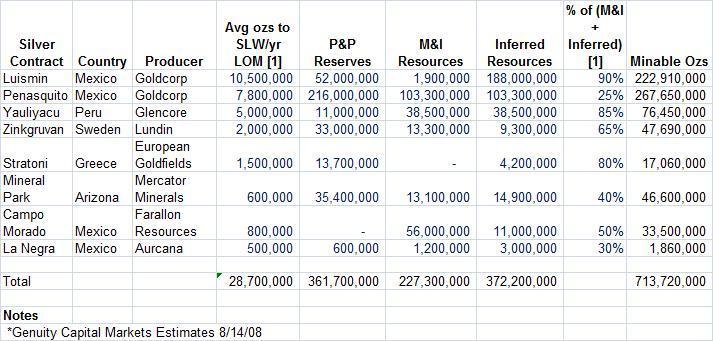

Luismin/San Dimas

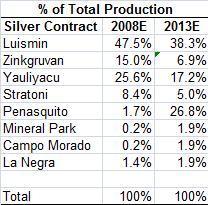

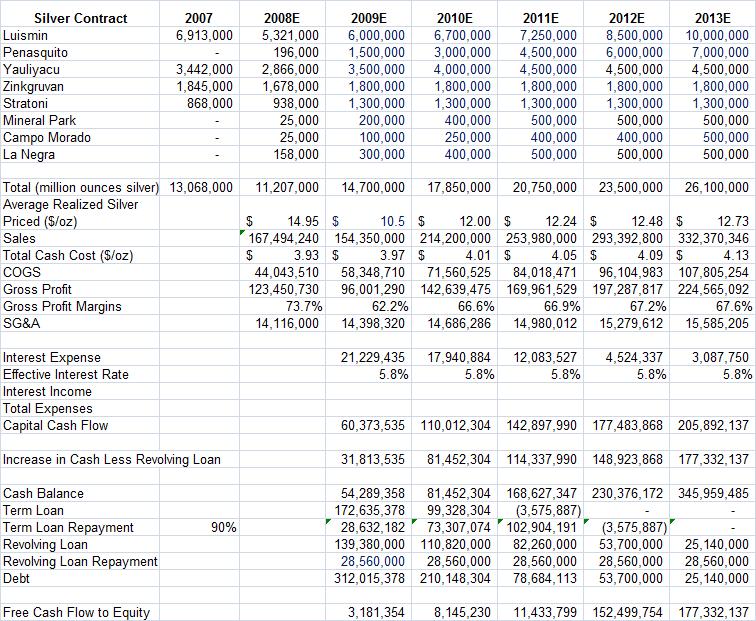

Luismin is one of the key mines for SLW and was formed through a mostly equity transaction that gave SLW rights to all silver produced for the life of this mine. Still owned/operated by Goldcorp, it is located in Mexico, arguably the best country in which to mine. It is a very low cost mine, having been in continuous operations for over a century, making it very low risk. There has recently been a temporary reduction in the grade of the ore, leading to lower production (a little under 5.5 million oz now expected in 2008 and around 6 million for 2009), which has caused SLW to miss their 2008 forecast. However, production is expected to ramp up by 2011-2012 due to a planned mill/underground expansion that will unlock higher grade ore. The risk here is that Luismin is low on the priority list for Goldcorp, particularly at the moment due to Goldcorp’s priority in opening Penasquito with experienced Luismin employees relocated to nearby Pensasquito. Luismin only produces about 8% of Goldcorp’s production. While this is potentially concerning, Luismin remains very low cost for Goldcorp at only $231 net by product cash in the very high cost year of 2007, so there is little risk SLW won’t realize at least most of Luismin’s silver reserves. It just may be delayed and continually below management projections. We have assumed Luismin will not hit the 12 million target management expects by 2012. Instead we project the ramp up will be slower and top out lower with just 8.5 million by 2012 and 10 million thereafter. Given Luismin’s 90% historical conversion of inferred resources to reserves, Luismin has 22 years of remaining life remaining mine life, which just happens to be until the contract expires.

Penasquito

Penasquito, also located in Mexico, is the crown jewel of Goldcorp, which acquired it in their merger with Glamis in 2006. Penasquito will be one of the lowest cost precious metal mines in the world (and largest in Mexico) as well as the largest silver mine with 13 million ounces of gold, 860 million proven and probable reserves of silver (and 410 million M&I, 510 Inferred) as well as significant amounts of zinc and lead. These numbers are from 2007 and Goldcorp says there will be significant revisions upward in 2008 data based on further completed exploration. At $650 gold, $12 silver, $.90 zinc and $.50 lead, Penasquito was expected to have negative $500 by product credit gold cash costs. Production is expected to produce at least 500k gold and 30 million oz silver for at least 19 years. Heap leach production (under 10% of total expected production) started this summer. Construction of the first mill is nearing completion, giving a start date for mill production of around Q3-Q4 2009, with construction of the second mill to be completed in late 2010 and ramping up to near full production in 2011. SLW financed the $485 million purchase of 25% of the silver for the life of the mine with debt in April 2007. We have high confidence in Goldcorp to execute the ramp up on time or with only slight delay. Nevertheless we have been cautious in assuming just 4.5 million by 2011 ramping to 7 million in 2013. Our forecasts finally have production at 8.5 million from 2018 onwards. However, there is significant upside to this, given that the great potential for expansion, better recovery rates and SLW's contract with Goldcorp for the life of the mine. (of which SLW has no more funding obligations), production could easily reach 10 million or more. Goldcorp, unlike most miners, has a history of meeting projections, and with the revisions already up to 7.5 million/year vs. 5.4 million when the deal was signed, we believe more could be coming. This seems particularly likely since Goldcorp, unlike tired large peers like Newmont, Barrack, Anglo Ashanti and Goldfields is not pressed to show growth with already the best growth profile of major miners.

Yauliyacu

Yauliyacu is a Peruvian mine that has been in production for over a century and is operated by industry behemoth Glencore. The 3rd deal SLW signed, it calls for up to 4.75 million per year for 20 years for $285 million. If there is a deficit in one year then SLW will get extra to make up for it in years above 4.75. SLW also has right of first refusal on any more silver stream deals from any Glencore mine. Since Yauliyacu produced 2.9m, 3.4m, and just below 3m from 2006-2008 respectively, SLW is likely to get all of the silver from Yauliyacu in the coming years as per the catch up clause. Yauliyacu has underperformed, ostensibly because with high zinc prices, Glencore had been focusing on higher grade zinc ore to the detriment of the higher silver-lead ore. With a relative shift in commodity values, Glencore has told SLW it plans to shift to higher silver grade ore in 2009. It is unclear whether SLW miscalculated the production potential of Yauliyacu, or if there will be a dramatic upward shift in production in the coming years. While we believe that is highly probable, at least in the short run we are forecasting just 3.5 million in 2009 up to 4.5 million in 2011 for the duration of the LOM/Contract. We view the risk here to be low as Peru is a mining-friendly country and Yauliyacu has a long stable history.

Zinkgruvan

Zinkgruvan, an aged mine with old facilities is a low cost silver/zinc mine in Sweden that has been in operation for over a century. The 2nd deal SLW signed and costing $78 million, it calls for 100% of silver for the LOM. It is expected to continue to provide slightly under 2 million consistently for another 12-20 years. Zinkgruvan recently changed hands but like all of SLW’s deals, their claim on the mine is not impacted by the operator’s identity. The new operator, Lundin, is experienced and Zinkgruvan should continue to be a low cost stable mine with very minimal risk.

Stratoni

Stratoni is a lead-zinc-silver mine located in northern Greece and operated by Hellas Gold, a subsidiary of European Goldfields. Stratoni, has ancient mining dating back 2500 years, and commercially operations since the 1950's with a ramp-up of the new deposit in 2005. SLW signed a deal in early 2007 to acquire 100% of the LOM silver for $58 million. Stratoni has only 13 million of P&P reserves and 4 million of inferred though there is some potential for further exploration. At expected annual levels of production between 1-2 million, Stratoni is expected to have a mine life less than 10 years. It is a low risk, mature mine that should provide a moderate level of production until new mining projects come fully online.

Campo Morado, Mineral Park & La Negra

Camp Morado run by Farallon in Mexico, Mineral Park run by Mercator in Arizona and La Negra run by Aurccana in Mexico are all small deals SLW signed within the last 1.5 years with upfront payments of $80 million, $42 million and $25 million respectively. Combined they should produce conservatively 1.4 million by 2011 and have mine lives of well over 34 years for Camp Morado and Mineral Park and at least 22 years for La Negra. Again, there is substantial upside as the contracts are for the life of the mines and there could be significant discoveries to come. These deals represent a shift for SLW from large deals on big low risk, low cost mines that have been in production for a long time and have experienced large operators. The projects were all late stage, near production under mid-tier operators when signed and thus can be argued represent the optimal value proposition for both SLW and the operator. However they obviously carry more risk. Nevertheless, this is balanced by the small nature of each deal. We believe this change in strategy, particularly more necessary in 2007-2008 when high metal prices made large advantageous deals more difficult was a smart one. These deals have a good likelihood of working out, and we believe represent only a minimal overall increase in risk for SLW's production profile.

Keno Hill

Keno Hill is a famous silver district in Alaska owned by a small company called Alexco and was SLW’s most recent acquisition. They agreed to pay $50 million for 25% of all silver for the life of the mine. Keno Hill has inferred reserves of only 18 million oz, but 213 million oz of silver have been mined here over the last century and it has some of the richest silver grades anywhere in the world. The current production potential recovers the investment and there is considerable upside in exploration for new silver, which is expected and part of the allure of the deal. The mine is scheduled to open in 2011 and produce 800k oz for SLW annually for 5 years. If Alexco does not complete the rest of the financing, SLW has some recourse through completion guarantees.

This deal was signed in September right before the stock collapsed and silver fell further. Therefore, while of little significance, with their debt burden it is slightly disconcerting that they did this deal which while potentially interesting was certainly unadvisable as the $50 million could have been used more productively for deals now or debt repayment/stock buyback. We have valued this project as if it is worth zero in this environment. Companies like Alexco that lack cash flow from existing projects are in trouble in an industry that is treacherous even in good times. While SLW’s claim exists on the property should it change hands, there’s no guarantee this site will be developed for many years. To be conservative, we think anything out of this deal is gravy and we can only hope SLW learned its lesson.

Evaluation of Management’s Deal Making Record

We believe that overall management has made sound silver stream acquisitions since gaining autonomy from Goldcorp. In a period of skyrocketing silver prices they generally did not get swept up in the rise and kept a conservative view. Arguably, they could have slowed on the deal pace, but their strategy of small deals besides the special situation of Penasquito, limited the risk of large mistakes. We also believe that adding a level of debt was a smart choice given the consistent nature of cash flows. We think that SLW has a good grasp of what they need to do in the current climate, as evidenced by their recent cancellation of a tentative deal with Augusta for their Rosemont Mine in Arizona; a deal that would have cost SLW about $165 million to be paid sometime in 2010. Clearly it would have been nice if they had saved cash in 2008 for a buyback or wildly accretive deals, but one could say this about so many companies.

Management/Goldcorp

Equity Investments

SLW owns 10-20% strategic stakes in 4 silver companies, 3 of which are in the pre-feasibility stage. These stakes have fallen dramatically in value like everything in recent months and now carry a mark to market value of less than 15 million combined: nevertheless they remain attractive silver properties with significant reserves. Two of these companies own rights to what would be top 30 silver mines in the world. SLW’s end game here is likely to turn their stakes into silver stream deals (they have right of first refusal on two of them) and a 25% stake in production, which could come online in 4-5 years and could add up to 8 million ounces annually. These companies will be in need of significant capital, making SLW’s positioning still attractive. However, in this market these companies are in dire straits as it will be hard for them to fund a mine development even with SLW's capital.

Financials/Valuation

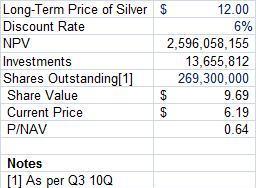

Two inputs drive the Silver Wheaton model: the price of silver and production. Everything else is superfluous. In our model, we significantly sandbagged the management's production estimates to extenuate our margin of safety. We also believe the sell-side is grossly optimistic when it comes to mine output in the current environment. Whereas management sees production ramping up to 15-17 oz in 2009, we project only 14.7m oz based on continued delays at Penaqsuito. By 2013, we project production of only 26.1m versus management's guidance of 30m. We have production topping out at 26.9m whereas management believes it is more along the lines of 30m. At current silver prices, we project debt will be paid off by 2013 based on our production numbers. Management provides a nice sensitivity analysis in their investor presentation of debt repayment -- of course based on their numbers. (http://silverwheaton.com/insitepresent/08-12-01%20SLW%20Presentation%20FINAL.pdf). We used a long-term price of silver of $12, which is below most analyst expectations and used a 2% annual growth rate in price. SG&A for Silver Wheaton is among the lowest in the world for a company of its size at only $3.5m/quarter. We grew this at 2% annually because the company's marginal cost of production is zero. It costs SLW zero SG&A to produce an additional oz of silver. Cash costs per oz are projected to grow at the inflation rate as per the inflation escalator in the contracts with the mine operators. We then utilized a 6% discount rate given SLW’s low risk profile and our emphasis on conservatism. We added back investments of $0.05 for a net asset value of $9.69, based on 269.3m shares outstanding. This leaves us with a price to net asset values of 0.64 and does not account for the optionality inherent in Silver Wheaton's business model or the added production, which we simply did not include because of our tendency towards conservatism.

Volatility

Silver Market Fundamentals

While SLW is a good investment should silver prices only grow from current prices at a rate near inflation, we believe there could be significant upside in (gold and) silver prices. Silver is truly a unique commodity, being both a precious and industrial metal. As a result unlike gold, the existing supply on the market is far smaller, leading to increased volatility. Gold and silver over the last 10 years have roughly a .96 R2 correlation and in old times traded at a fixed 16 to 1 ratio. In the last decade that ratio has averaged about 60 to 1 and been anywhere from 44-82 to 1, currently sitting near its all time high of about 80. This could suggest silver is due to correct relative to gold (or that the bigger impact on industrial demand has weakened it relative to a pure monetary metal). What is perhaps most interesting about silver is that about 2/3 of production comes as a by-product. In fact, the production of silver is more correlated with the production/price of copper-zinc than it is with the price of silver due to the high amount of silver coming as a byproduct of copper-zinc mines. The implication of this is that silver is perhaps the most inelastic of all commodities as there is always limited liquidity, and higher prices don’t always lead to higher production due to silver’s relative unimportance to operators of gold or zinc-lead-copper mines. Thus, the common knock on commodities that they should revert to the long run cost of production does not necessarily hold true for silver. Further, the long time bear case on silver was that photography demand would lessen silver demand considerably. What has actually happened is the market overestimated the drop off from photography, which has been completely compensated for by a rise in new industrial applications, such as medical antibacterial uses among many others. Industrial demand for silver, unlike many base metals is very inelastic as the amount of silver used for most applications is trivial.

The rational case for gold (and by extension silver) can be found in many other places, including a great post by Biv about the gold miners in general. What we would mention briefly is that historically gold has thrived in bear markets for obvious reasons and people have been perplexed about its performance this time. However, we believe in a liquidity crunch everything was sold, even gold to meet margin calls, hence gold’s unusual weakness (though still relative strength). Historically the strongest indicator of gold prices has been the real rate of return measured simply by fed funds minus inflation. Despite the theories and conspiracies of goldbugs (Comex shorts like Goldman Sachs discouraging bulls and suppressing the price are bankrolled by the US government for various nefarious purposes), along with a 20 year overcorrection from 1980, the negative or very low rate of return for much of the decade was the overaching reason for the reemergence of a gold bull market. Again, today we have at least nearly negative real returns, so while “inflation” may be low, the indicator of gold’s strength is strongly bullish. Historically, while gold has performed well at the beginning of a recession, miners tend to first fall with the markets then diverge. This trend appears to have started last month and creates a great buying opportunity still in the early part of a bear market.

Risks

Silver Prices

Obviously all this analysis on production rates is meaningless if silver continues to decline and fails to recover. More specifically, while SLW can't lose money on production, their debt, covenants and interest coverage have the potential to become an issue. However, we don’t see lower commodity prices as a risk to production shut downs, as SLW has been savvy in making deals only on the lowest cost mines. A bear argument for silver is there are a couple of large silver focused mines in the near term coming online. However, 2 of these mines, Apex's San Cristobal and Coeur's San Bartolom are located in Bolivia and have run into serious issues as Bolivia has made efforts to nationalize the mines, causing serious financial distress to both companies. Other projects in early stages of development are likely to run into serious trouble obtaining the large amount of necessary financing to startup a mine. We believe it is likely new supply of silver will come in under expectations for the next 5 years.

Debt Service

A near term concern is SLW's ability to service debt and remain under covenant leverage ratios. As silver stays above $10, the chance of problems even as the covenants increase in Q4 2009, lessens. While SLW’s lack of operational control leaves them at the whim of the mine operators, we believe there is very little chance of a doomsday scenario. SLW is in no danger of failing to make interest payments or principle above $6.73/oz in 2009 according to our projections and even lower prices after 2009. With stable cash flows, we believe SLW could cut a reasonable deal with creditors or at worst sell a smaller asset.

Increased Competition

While there are no real players successfully doing what SLW has done, startup copycats have sprung up such as Silverstone resources and Gold Wheaton (no relation). In the current climate, these unproven competitors' ability to succeed is questionable. However, due to SLW’s success and historical premium valuation to operators, in the future it is likely there will be more competition for silver stream deals, making the market more efficient. Additionally, SLW would likely trade at a lower premium given the increased investment vehicles (this has also potentially been the case when they introduced the silver ETF). We don’t see this as too impactful at least for a while, as SLW’s attractiveness stands on its own, solely from the free cash flow its assets generate.

Lack of Operational Control

A potentially large and growing problem for SLW is their lack of operational control, particularly at Luismin. Even with deals structured to minimize this issue, SLW has already at times suffered from the disincentives of operators to mine higher grades of other metals at the detriment to higher grade silver due to the lack of upside in deals where SLW gets 100% of silver production, notably at Yualiyacu and Luismin. We believe this is particularly of concern at Luismin, where silver will account for 38.3% of our projection silver production in 2013. At the time this deal was structured, Goldcorp owned 50+% of SLW so Goldcorp was realizing the upside at the time. Since Goldcorp completed the sale of its last 48% stake in March 2008, this incentive has been removed, and at the least Goldcorp has reduced attention on Luismin with Penasquito coming online. In the long run all economical ore will be mined, but the timing of cash flows is at the whim of the operators, and this has the potential to at best delay the realization of some value if not lower it altogether

Change in Canadian Tax Law

SLW’s tax status is a big reason for its attractiveness. Should Canada change the rules about overseas income, this could have a material impact. We have no special insight on Canadian tax politics and while a change seems unlikely it is certainly possible.We would say the large presence of mining companies in Canada, and the friendliness of Canada to the industry might lessen the possibility, but this large risk is hard to ascertain succinctly. The Conservative Party though just won recent reelection to parliament, which ought to bode well for miners.

Conclusion

While SLW was a sure fire slam dunk a month ago below 3 dollars, we believe even that these higher levels in the 5-6 dollar range it remains undervalued and an interesting addition to most portfolios. We believe it is the safest way to gain strong optionality to precious metals without taking on the downside risks of derivative products. On the back of Biv’s post on buying GDX, this idea is simply a detailed example of why miners are so cheap right now and a unique way to play the trend. We believe SLW is a convincing argument of a better alternative than buying a gold or silver ETF, as you get turbocharged equity upside with only slightly higher risk than buying silver itself. We believe this is a compelling tradeoff which one gets on top of a nice discount to NAV. Furthermore (though this is unquestionably greater fool theory) there is no doubt that should silver take off again, SLW will trade far above NAV. If you believe a hypothesis like Biv’s that gold should trade at $2k, silver should rise proportionally higher, perhaps to at least $35. Not to get carried away, but on top of the mania NAV premium, in such a scenario we wouldn’t be surprised to see SLW worth over $40. Additionally, economically viable reserves will increase dramatically, which SLW will profit off of without any further capital outlays. Clearly this is an outlier scenario, but it isn’t out of the realm of possibility in these unprecedented times. Silver Wheaton gives investors multiple ways to win and given the transparency and consistency of cash flows, a relatively low risk opportunity.

Catalyst

Silver prices.Production ramp up.

Market turning to inflation-safe investments.

| show sort by |