| 2017 | 2018 | ||||||

| Price: | 1.65 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 352 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 585 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 0 | EBIT | 0 | 0 | |||

| TEV (in $M): | 569 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- oil service recovery bet

- Standard Drilling SDSD 04/24/2020

- Standard Drilling SDSD 10/09/2018

- BETA

- VANECK VECTORS OIL SVCS ETF OIH 04/30/2018

- Ovintiv OVV 06/30/2022

- CENTENNIAL RES DVLPMNT INC CDEV 02/08/2020

- TIDEWATER INC TDW 01/05/2018

- SPDR S&P OIL&GAS EQUIP & SVC XES 09/20/2018

- Dolphin Group DOLP 07/16/2013

- Ensco International esv 05/08/2018

- VALARIS LTD VAL 05/23/2021

- HALLIBURTON CO HAL 10/18/2021

Description

Standard Drilling (SDSD NO Equity)

Thesis summary

-

Standard Drilling is a small cap (585m NOK or 70m USD) trading on the OSEBX and is incorporated in Cyprus. Its largest shareholder is a very smart self-made norwegian billionaire, Øystein Spetalen. Especially relevant to this particular investment is his track record in the energy space. Spetalen has successfully executed several opportunistic investment projects in the energy sector before (e.g. Noble Denton 2006-2009, OFFRIG 2005-2006, Ferncliff Drilling 2006) and is widely recognized as one of the sharpest investors in the Nordic region.

-

Standard is underanalyzed, unpopular and deeply undervalued looking a few years out. The stock is covered by only one analyst (at Clarkson Platou). My base case assumptions imply a 3 NOK share price by 2020 or an 18% expected CAGR. In a bull case scenario where dayrates in the offshore supply vessel space reach historical averages, the share price could be 6 or 7…

-

I think oil prices will move upward in the coming years (though not by that much), as I believe global demand will outstrip supply and US shale will not be able to fill the gap. I think the rig market and drilling activity offshore will subsequently improve, not only due to higher oil prices, but also because the economics of offshore exploration are probably better now than they were at 115 dollar oil in 2013. Offshore costs are down more than 50% (CPS Offshore Cost Index), and oil companies have streamlined their organizations more generally. Oil company cash flow is thus rapidly improving again and will stimulate exploration and production demand from 2017/18 onward. This increased activity will in turn lead to improvements in utilization and dayrates for offshore supply vessels from current levels. Finally, I think there are several underestimated supply side factors that will help get rid of large parts of the current overcapacity in the OSV market.

-

When that happens, the market should dramatically reprice Standard Drilling. At newbuild parity (NB) in 2020, the NAV of Standard is about 3 NOK. At historical average dayrates, the NAV could approach 7 NOK. (The stock is currently trading at 1.62 NOK). Over time, vessel values have historically been valued around newbuild parity – see appendix. Due to the negative market environment currently, vessels are currently valued much, much lower. Essentially, I’m bettting that we will see at least a partial mean reversion in utilization, dayrates and ship valuations as oil prices rise modestly, offshore drilling activity increases again and overcapacity is phased out of the market.

Fleet & ownership structure

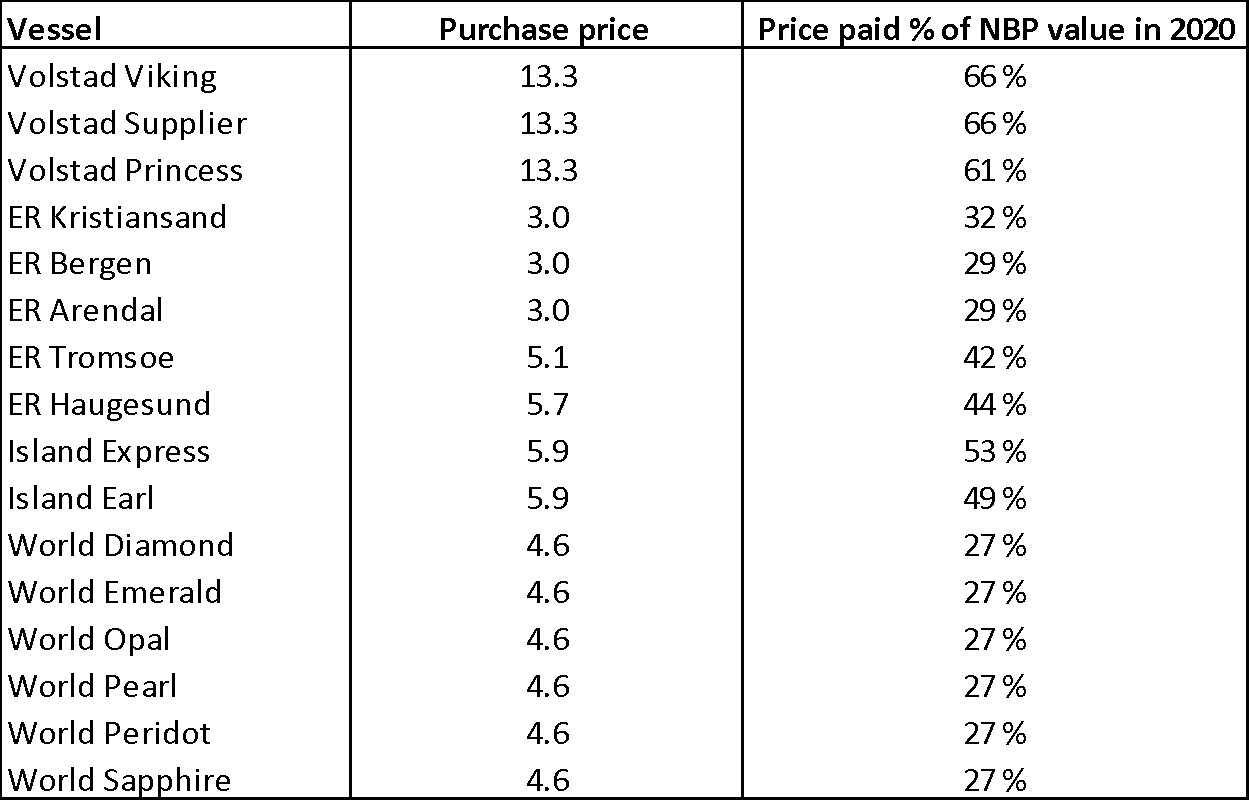

Standard does not, as the legacy name implies, engage in any sort of drilling activity, rather it owns interests in offshore supply vessels (OSV). It was set up in its current form to take advantage of extremely depressed prices for offshore supply vessels – a market that has been crushed during the recent downcycle in the oil and offshore markets. Standard has purchased interests in a fleet of platform supply vessels at deeply discounted prices and is 100% equity financed.The fleet is operated by Fletcher Supply Vessels Ltd and Tschudi Shipping. Today, it looks like this (some ships renamed):

|

Metric / vehicle |

PSV Opportunity I |

PSV Opportunity II |

PSV Opportunity III |

Ice-class PSVs |

New World Supply |

|

Vessels |

3 |

2 |

2 |

3 |

6 |

|

Ownership |

20% |

20% |

35% |

100% |

26% |

|

Purchase price / vessel (USDm) |

3.0 |

5.1 / 5.7 |

5.85 |

13.3 |

4.6 |

|

Yard |

Kleven Norway |

Aker Aukra Norway |

Aker Brevik Norway |

Aker Brattvaag Norway |

Damen (Netherlands / Romania) |

|

Built |

2006 / 2006 / 2005 |

2009 / 2008 |

2007 / 2008 |

2008 / 2007 / 2007 |

2013 |

|

Design |

VS 470 MK II |

UT 755 LN |

UT 755 LN |

ST 216L CD |

PSV 3300 |

|

Deck area in m2 |

700 |

680 |

710 |

1,060 |

728 |

|

Deadweight |

3,544 |

3,270 |

3,130 |

5,100 |

3,500 |

|

Length (LOA) in meters |

73.4 |

73.6 |

76.5 |

93.4 |

80 |

|

Additional specs |

DP2 (after upgrades) |

DP2, Fire-fighting (1x) |

DP2 |

DP2, Ice-Class B, Diesel-electric engines |

DP2, Diesel-electric engines

|

Operational status fleet

*(World Wide Supply Vessels in lay-up).

Characteristics of Standard’s fleet and the offshore supply vessel market

All vessels except the three Volstad vessels which are large PSVs with Ice Class capabilities (commands higher rates as they are larger and can operate under very harsh weather conditions) are mid size PSVs of newer date with around 700 m2 deck space. These are all units that provide various supplies and offshore operations support to offshore drilling units and fixed offshore installations.

PSVs are generally classified based on size (dead weight tonnage and length) what kind of dynamic positioning system they have and their ice-handling, fire-fighting and oil-recovery capabilities. Deepwater offshore jobs generally require a size over 4000 DWT, that is «large» vessels.

Markets for medium and large PSVs are primarily the North Sea, Brazil, deepwater GoM, East and West Africa and Australia. The offshore vessel industry is global, but most PSVs work specific geographies due to both technical specifications and marketing issues as well as cabotage restrictions. Through an offshore cycle the dayrates still tend to correlate pretty well across geographies. Owners are able to arbitrage differences across geographies as a rule.

Demand drivers and recent developments

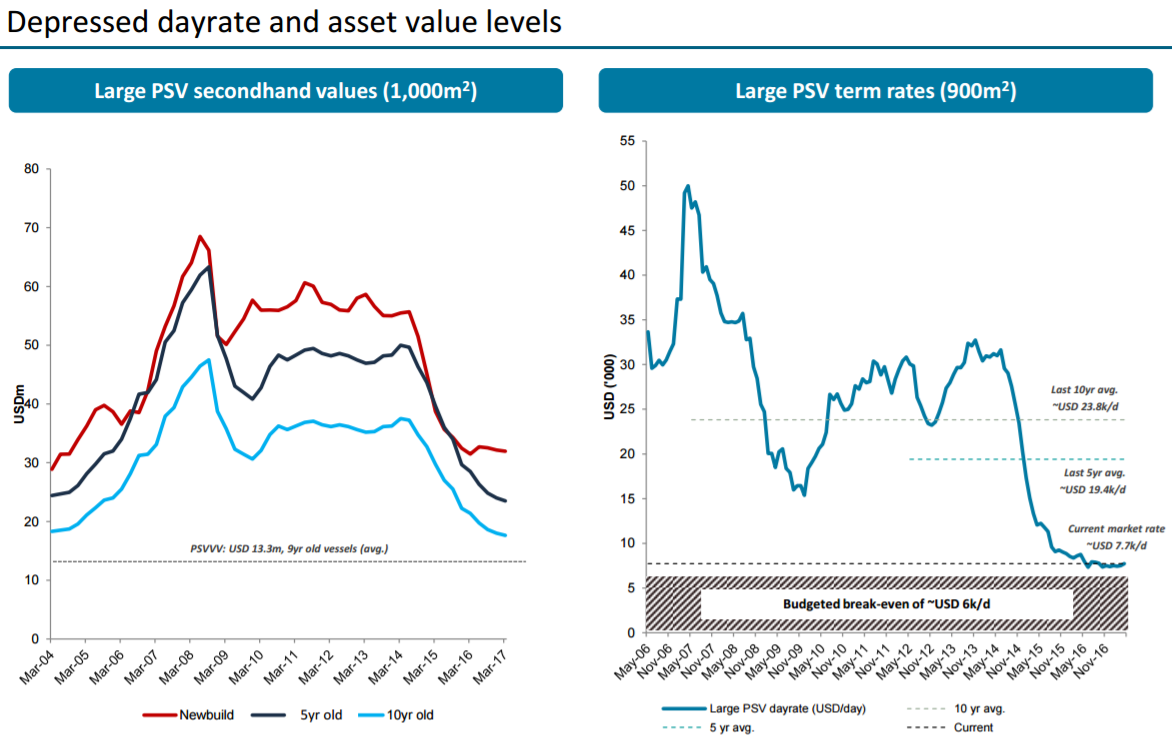

The two important drivers for OSV demand are rig demand and production support demand. Falling rig demand led to a very weak OSV market in 2015 and 2016, as oil companies virtually stopped awarding new drilling contracts as a result of the collapse in oil prices. From september 2014 until december 2016, rigs under contract dropped by 38% (rig count fell from 700 to < 300). The worst decline was seen in the floater segment, where rigs under contract dropped by 48%. Since the offshore supply vessel intensity is highest for floaters, the demand for OSV dropped off a cliff. As did the second hand values and newbuild values for vessels (source charts: SDSD prospectus, Q1 report).

Production services demand, that is the servicing of offshore infrastructure, is not looking as bad. This market is currently expected to grow until 2020 based on projects commisioned before 2014 alone. Standard claims an analysis of the Infield global database indicates that the installed weight of offshore topsides will expand by 8% as we approach 2020 (relative to 2015).

The supply side and recent developments

During the boom years in oil services, OSV companies ordered massively. This came to a halt in 2016 when only one newbuild was ordered. There are still a number of vessels under construction (9% of a total global fleet of about 1722 PSV vessels), 191 in total, but many of these will never be delivered. 124 of these PSVs (65%) are ordered at chinese yards, and in the diplomatic parlance of Standard there are «substantial doubts of their delivery status». The reason for this wording is that slippage rates for PSVs at chinese yards was 33% in 2013, 31% in 2014, 53% in 2015 and 61% in 2016. Lots of ships that were ordered on spec have no operational owner to take delivery. So expecting anything more than about 50 ships out of China seems optimistic. So the likely maximum total supply growth in 2017/18 could be 50+67 ships or about 6.7%. It will likely be lower still.

When times got tough after the oil price collapsed, operator balance sheets were destroyed and this led to a massive increase in stacking. By the end of last year, over 600 vessels (AHTS + PSV) were cold-stacked. GoM and the North Sea (NS) were the worst hit, with almost 200 vessels and 170 vessels cold stacked respectively.

Source: CPS

This looks very scary in terms of ever getting back to a balanced market, but I think this fear is overdone. Sure, some of these ships will return to service, but many will not, and certainly not until rates improve a great deal. There are two reasons for this. One, many of the stacked ships are old. Over 20% of the fleet was built before 2000 and bringing them back into service will be difficult to defend economically as survey and maintenance costs are just too high. On many of these ships, there has been done little maintenance over the last couple of years as well, as operators have focused what little cash flow they have seen on maintaining ships in service. Looking at the maintenance spending of TDW, GLF and HOS is illuminating: it has been reduced by 70% from 2014 to 2016e! There are also lots of reports of owners picking stacked vessels for parts for example. 1-2 million dollars just to reactivate is the norm for stacked ships, higher for the old and really run-down ones. Oil companies also know this, and according to one industry executive I’ve talked too, avoid recently cold stacked vessels and operators with financial problems completely because they view the risk of subsequent operational problems as too high and unacceptable.

By 2020, 84% of the fleet will be forced through the obligatory 5-year survey. For many operators, this is not doable with current economics. Which means unless rates rise, then there is no supply side, basically. (SDSD has enough cash on hand/ in the PSV structures to reclass its ships as needed).

Current state of the market – still weak, but showing some small signs of improvement

The main players in the OSV market are DOF, Solstad Offshore, Rem Offshore, Siem Offshore, Tidewater (ch 11), Farstad, Hornbeck Offshore Services, Deep Sea Supply, Havila, Gulfmark (ch 11), Eidesvik, Nordic American Offshore and Viking Supply Ships. As a result of the crisis resulting from the above developments, several large players are being (or have recently been) restructured. Even after these developments, the large players remain financially strained. This snapshot of indicative prices and yields for supply company bonds illustrate this clearly. (Source: Arctic Securities).

Unecured bonds

Secured bonds

Anyway, at current dayrates, virtually the whole industry is losing money. Term rates in the first quarter was about 8000 USD/day in the North Sea, and opex not including financing costs were about 6000 USD/day. For some perspective on how low that is, the long term average over the last 10 years is 18300 USD/day. For the players with levered balance sheets, this is oviously not sustainable. At these rates, everyone (except Standard and maybe NAO) are out of business in 4-5 years, and in mid-May, both Tidewater and Gulfmark filed for Ch.11 (previously announced).

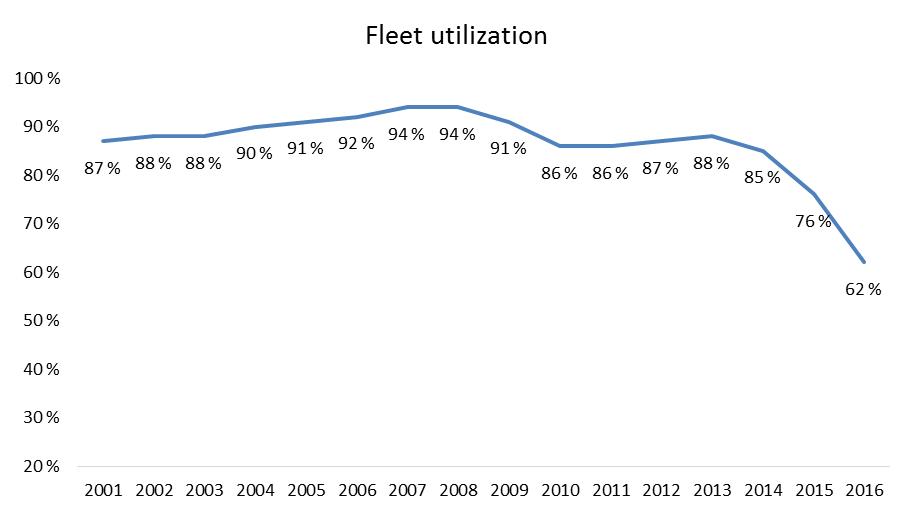

Unlike its competitors in the space, Standard is debt free – a competitive advantage in a depressed market as its real operating breakeven level becomes much lower than that of peers who have significant financing costs. SDSD clearly has an advantage when contracts are scarce. In Q1, SDSD operated at roughly break even and 6/16 ships were employed. Utilization in the industry is currently near all time lows. The utilization rate for the total global OSV fleet stood at 62% versus a long term average of about 87% as of mid-april. The spot utilization rate was 76% as of mid-may, and spot rates in the NS are at 8k. In other words, there is no question the market is still weak. Reading through the reports of the supply companies, everyone is still bearish on the outlook and expect continued weakness, but there are some green shots to be seen as well: The number of working jack-ups and floaters globally has increased over the last two months, the first two-month uptick since 2014. OSV activity is significantly up from a year ago (outstanding North Sea PSV tenders stood at 16 vessels for a total of 526 vessel months vs 8 vessels and 77 vessel months in april of last year), and oil companies are starting to renew their term fleets. In the North Sea, the spot market saw the highest spot rates since 2014. As of the end of Q1, the number of available vessels had decresased from 17 to 10.

Sources: BP, IHS, Rystad, Clarkson Platou

A return to NBP ship values by 2020 implies lots of upside in Standard

Like Howard Marks says: Most things will prove to be cyclical, and some of the greatest opportunities for gain and loss come when other people forget that fact. I think SDSD belongs in this category.

Based on a 25 yr straight line depreciation of SDSD’s vessels, the NAV contribution from the fleet should be about 107.5 mUSD in 2020. NAV per SDSD share in 2020 should then be 2.98 NOK, assuming an unchanged cash position and share count. That implies an 18% CAGR in the interim.

Should rates reach historical average levels of 18-19k per day, I believe NAV could reach as high 6-7 NOK, but I’m thinking of this as fairly unlikely blue sky scenario given the depressed state of the OSV market. But you never know.

|

NAV calculation |

At NBP 2020 |

NBP 2017 |

|

Value vessels USDm |

107.5 |

131.6 |

|

Net cash |

16 |

16 |

|

NAV USDm |

124 |

148 |

|

USDNOK |

8.5 |

8.5 |

|

NAV NOKm |

1,050 |

1,255 |

|

# shares |

356.7 |

356.7 |

|

NAV/share |

2.94 |

3.52 |

|

|

|

|

|

Current price |

1.62 |

|

|

Upside |

82 % |

|

|

Investment horizon |

3.6 |

|

|

Exp CAGR until 2020e |

18 % |

|

Conclusions

Standard seems like a good bet on a cyclical recovery in OS supply. Based on the arguments above, I’d say a recovery is likely to happen within the next 3-4 years. This is probably not an opinion that is unique. A recovery must happen, or the industry ceases to be. Several leading industry experts say the same thing - but most investors don’t like to wait 3-4 years, which is why this opportunity exists.

This is an investment that will require patience and fortitude (I expect high volatility). Fortunately, Standard’s debt free balance sheet gives us some time to wait for that recovery (I estimate cash on hand and in the PSV structures covers capex needs at least through 2019e even at current rates).

Standard is controlled by a savvy investor with a solid track record in the industry (and incidentally, a degree in petroleum engineering). He is a restructuring and dealmaking specialist, and not a typical long-term operator. I expect an exit through a sale of the company down the line. He is known to sell sooner rather than later, I'm hoping he won't rush this one.

Risks

An investment in Standard carries above average risk for sure. There are risks relating to the operations of the boats, currency, reasonable but limited liquidity in the shares etc, but oil prices are the biggest uncertainty. I am at the mercy of the oil price over the next 4 or 5 years to a great extent here. Should it go lower from here and stay there and/or offshore rig activity not recover by 2020, an equity raise will most likely be necessary to secure funding of continued operations. SDSD seems unlikely to be a zero in any scenario, but quantifying the downside exactly is obviously difficult. What can be said with some degree of certainty is that the upside is many times the downside should OSV rates recover to its historical averages. And even if they only reach NBP in 2020, the potential upside should still be much larger than the potential downside from here.

Appendix 1: Why I believe oil prices will rise and that offshore E&P activity will improve

A thorough discussion on this subject is beyond the scope of this write-up. I will however briefly summarize my thinking on the matter.

Global oil demand is rising, and renewable energy, while an increasingly important part of the energy mix, is not a major contributor yet. 80% of primary energy consumption is still fossil-based. Over the last couple of years, lower oil prices have created a strong demand response. In 2017e, world liquids demand will be 97.9 mbd (IEA). It will then have increased by 1.16 mbd per year on average since 2015. Assuming a global demand increase of 1 mbd per year by 2020, world demand will be 101 mbd. The global crude, condensate and NGL output in 2017 will be 98.5 mbd according to IEA.

With a net decline rate on existing fields of 4% (the average for 2014 and 2015) until 2020, today’s existing fields will produce 98.5 mbd *0,96^3 = 87.1 mbd. So new production must supply 13.9 mbd. Sanctioned Opec and Non-Opec projects should provide 5.6 mbd + 3.9 mbd = 9.5 mbd (Source: Rystad, Energy Aspects). That leaves a shortfall of 4.4 mbd that must be supplied by increased shale production. Should the decline rate instead be 6%, which I believe is entirely possible given the monstrous capex cuts that have been implemented in the oil industry since 2014, the shortfall after sanctioned opec & non-opec projects will be 7.2 mbd and shale must make up that difference. The most bullish shale growth estimates I have seen say US shale could increase an average of 1 mbd over the next 2 years and 700 kbd over the next 4 (M-L, Rystad). Even if decline rates were only 4% and that production growth came true, that would only cover about 2/3 of the supply needed to balance the market at current prices. As a side note I don’t see that happening without cost inflation for the shale producers, increasing their breakevens which should also put upward pressure on oil prices all else equal (and make offshore production more competitive relatively speaking).

All in all, I think the most likely path for oil prices over the next few years is up. I am going for direction, and I’m not trying to estimate a price level. As an example of how difficult that is, the futures market predicted 90 USD brent for jan ‘16 in 2012. The actual price turned out to be 30...

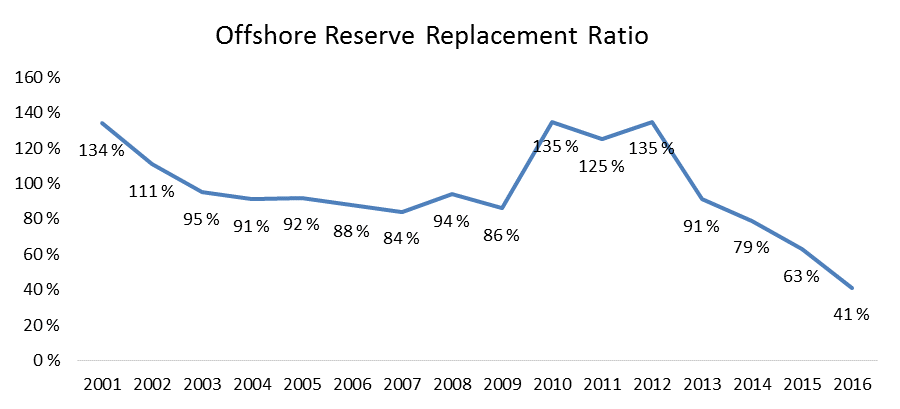

The offshore capex cuts have been brutal. After E&P spending offshore increased by a 13% CAGR from 2003-2013 (from roughly 55 Bn to just shy of 200 Bn USD), we will be back at 90 Bn in 2017, a 48% decline! This suggests a risk of lower production growth than expected if you ask me. The offshore reserve replacement ratio (discovered resources/production) is currently at a 30-year low.

Breakeven prices have fallen a great deal for US shale fields. Wellhead breakevens are at 30-40 USD for Bakken (lowest), Eagle Ford, Niobrara, Permian Delaware and Permian Midland. In 2013, wellhead breakeven prices stood at 65-100 USD! Adding 10-15 USD to account for facility costs, the real breakeven range is about 40-55 USD.

The question is if it is sustainable. Rystad writes: “Even though the BEPs have fallen across the shale plays due to (structural changes like improved well performance; efficiency gains), the most important question to answer is how much of this change is sustainable. Rystad Energy studied and quantified the different cyclical and structural drivers of the changing BEP and arrived to a conclusion that if all of the cyclical effects are reverted when the oil price starts recovering, the BEP might grow by 62% over the next couple of years for US shale plays.”

-

So extrapolating cost reductions in shale further might prove to be a really bad idea.

Anyway: Can offshore possibly compete with 40-60 USD breakevens? Yes it can, as it turns out. About 50% of all known discovered, undeveloped offshore resources now have a breakeven at or below that level. In many cases, this is half the cost of what it used to be. As an example, we can look at Statoil’s Johan Castberg field, which in 2013 had an estimated breakeven price of 80 USD/b. Statoil now estimates a breakeven below 40 USD/b, over 50% lower.

Perhaps it is not so surprising after all then (it surprised me when I first saw the numbers), that offshore greenfield capex is actually outpacing N-A shale capex in 2017 for the first time in 3 years. I think this is an indication that the worst is over for offshore exploration and that we will see an increase in activity going forward.

Anecdotally, I’m seeing several signs of improvement in the first quarter reports from the seismic and offshore drillers providers (leading indicators of increased E&P activity and later OSV activity). Although they are mostly very cautious and also point to several potential challenges and a business environment that is basically still crap compared to the good old days of say 2013, I think it’s important to note that all is not as black as it was last year around this time.

From Transocean’s Q1 conference call:

«Looking at the macro environment, we remain encouraged that global demand for oil continues to increase and according to the IEA, 2016 marked a record low in new discoveries, which certainly raises questions about future supply. We’re also encouraged to see that OPEC has demonstrated both the willingness and ability to adhere to their stated production cuts. We also see that many of the main deepwater projects that have been on hold for the last couple of years now carry break-evens at or below $50 per barrel and in increasing numbers at or below $40 per barrel. And finally, we see the cost inflation onshore coupled with structural and sustainable cost savings offshore are nearing the risk reward gap between onshore and offshore investments. As a result, our conversation with customers remain constructive. During our last earnings conference call, we stated that a price per barrel in excess of $50 seem to spark demand from certain independent international oil companies. We also stated that we are seeing pockets of demand emerging in the UK, Norway, India and Southeast Asia (…) As we look out over the balance of the year, demand for our assets and services will continue to be driven primarily by oil prices. If prices continue to hover around $50 per barrel then we would expect to see more contracts materialize over the coming months.

From Schlumberger’s Q1 conference call

«Turning next to the business outlook. We maintain our constructive view of the oil market, and we made further inventory growth in the second quarter, driven by the OPEC and non-OPEC production cuts put in place in January.

At present, the region in the world showing clear signs of increased E&P investments in 2017 is North America land, although investment levels in the Middle East and Russia are also expected to remain resilient this year. However, for the rest of the world, which still make up more than 50 million barrels per day of oil production, we are heading towards a third year of significant underinvestment, which increases the likelihood of a medium-term supply deficit as produced reserves are not replaced in sufficient volume. In particular, the market continues to focus on headline decline numbers that suggest that production is holding up well, while a closer examination of the underlying data clearly shows that the rate of depletion of proved undeveloped reserves is rapidly accelerating in several key non-OPEC countries.

The current level of underinvestments is most visible in exploration, where the record-low investments, including both drilling and seismic, led to a total amount of industry discoveries of less than 5 billion barrels in 2016 versus a produced volume of over 30 billion barrels, dropping the industry-wide reserves-to-replacement ratio to 32% (…) we expect an acceleration of the activity growth towards the back end of 2017 and into 2018.»

From Seadrill’s Q1 report:

«The offshore drilling market remains challenging and we expect this dynamic to continue in the short to medium term. The majority of customers remain focused on conserving cash and are still reluctant to commit to significant new capital projects offshore until an increased consistency and upward trend in oil prices is demonstrated. The significant rig supply overhang remains and a faster return to a balanced market will require drilling contractors to be more disciplined in retiring older units.

Tendering activity has continued at increased levels, albeit from a low base, over the past few months, especially in the North Sea floater and South-East Asia and Middle-East jack-up segments. Market behavior points increasingly to the market having reached its bottom. An increasing number of recent tenders released by oil companies seek to contract at current bottom of cycle dayrates for increased durations and / or with multiple fixed price options periods. We remain committed to keeping our units working in the short-term and have successfully re-contracted a number of our units. We still believe in the long term fundamentals of the offshore drilling industry, driven by years of under-investment in new fields and the competitiveness of offshore resources on a full cycle basis.»

From Borr Drilling’s Q1 report:

«The global marketed utilization for Independent Cantilever (IC) jack-ups has currently reached 70% (May 2017), up from 68% at the start of the year. Jack-up contracting activity has been on a steady increase in 2017, number of contract awards year-to-date is almost 40% higher comparted to the same period in 2016 (…) Jack-up attrition since the start of 2014 now totals 38 rigs of which 58% have been retired since the start of 2016.Tenders and market inquiries have been on a steady increase since inception of the company late 2016. This trend is visible across all our key focus regions and we remain optimistic about contract opportunities for our young and highly capable fleet».

From Aker Solutions’ Q1 report:

«The outlook for oil services remains challenging as projects continue to be postponed amid a volatile oil-price environment. There are some signs of a recovery, particularly in the brownfield segment where oil companies are focusing on optimizing output from existing fields. Industry cost cuts are bringing down break-even costs on developments, which is expected to spur new investments and project sanctions this year. Increased demand for front-end engineering services is also an early indication of a pickup in activity ahead. Tendering activity is healthy and Aker Solutions is currently bidding for contracts totaling about NOK 50 billion. The majority of these are in the subsea area, where the company anticipates several greenfield projects to be awarded in the next 12 months.

"While we continue to face market uncertainty, the signs of improving brownfield activity and expectations of key subsea projects moving forward bode well for 2018 activity levels.»

TGS Nopec’s Q1 report

«Due to the substantial reduction of exploration budgets, discovery of new hydrocarbon resources dropped to historically low levels over the past couple of years. This has driven reserve replacement ratios down to unsustainably low levels. Oil companies will need to increase exploration efforts at some stage in order to grow production levels in the longer term to meet the long-term oil demand, which is likely to continue to increase in the foreseeable future. Simultaneously, both the E&P sector and the service industry are continuing to cut costs, leading to substantial reduction of marginal costs of bringing new resources on stream.»

-

Q1 net revenues of 86 mUSD, up 35% yoy, late sales up 82% yoy.»

-

Near term oil/demand supply balance looks uncertain

-

Exploration spending likely to decline further 15% in 2017 due to lower drilling rates

-

Some signs of increasing activity – TGS has successfully increased backlog in Q1.

The most important take-away from the TGS report was this slide, showing the positive FCF impact of the cost reductions over the last couple of years on the oil majors. This cash flow is what will fund the next wave of offshore capex.

Appendix 2: Various charts, top shareholders, company history.

Second hand ship values have historically traded around newbuild parity (Source: Clarkson Platou)

Top 20 shareholders

Company history – from the SDSD Prospectus dated february 22nd 2017

Link to prospectus http://norma.netfonds.no/release.php?id=20170222.OBI.20170222S83

(The company has since increased its ownership stake in WWS to 26% on two separate occasions).

Share price history:

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

Oil price increase

Increased rig activity

M&A

| show sort by |