| 2012 | 2013 | ||||||

| Price: | 38.10 | EPS | $3.87 | lower | |||

| Shares Out. (in M): | 39 | P/E | 9.8x | higher | |||

| Market Cap (in $M): | 1,470 | P/FCF | neg | neg | |||

| Net Debt (in $M): | 2,423 | EBIT | 304 | 304 | |||

| TEV (in $M): | 3,893 | TEV/EBIT | 12.8x | higher | |||

| Borrow Cost: | NA | ||||||

Sign up for free guest access to view investment idea with a 45 days delay.

TAL INTERNATIONAL

Tal International (TAL) is a lessor of intermodal freight containers. They generally purchase freight containers and lease them to shipping lines under spot or longer term contracts. The business has been performing extremely well due to a pick up in world trade after the 2008-09 downturn and due to greater demand from “slow steaming” (see explanation below). However, the businesses of their customers, the shipping companies, are in dire shape due to weakness in world trade and overcapacity and, thus, as one would expect the peak conditions in the leasing business to moderate quickly. This appears to be happening as most indicators of the health of the business have rolled over and are showing negative comparisons.

Given the amount of capital TAL has invested over the past two years using mostly leverage at, arguably, the top of the cycle, the equity value is at risk of a substantial price decline should the unhealthy trends accelerate. We think that it is reasonable to assume that the trends will do just that.

Container Shipping Business is Weak

As per the graph below of container ship time charter pricing, the container shipping business is was very weak. Until recently, prices were very depressed.

http://i619.photobucket.com/albums/tt271/vacationpn/Graph1.jpg

Ebit margins for the industry were negative in the first half of 2011 and prices deteriorated in the second half further.

http://i619.photobucket.com/albums/tt271/vacationpn/Graph2.jpg

Source: Maersk 1h 2011 presentation

It should not be a surprise to anyone that certain players in the industry are experiencing difficulties. TAL’s fourth quarter press release stated:

“The main risks we see . . . for this year include . . . the potential for a major customer default. We don’t currently consider [this] event[s] likely, but we are wary of a variety of potential event risks for 2012 due to the current high level of uncertainty in the global economy and the significant financial pressures facing our customers.”

For more on this subject, see the Bloomberg article on “slow steaming” attached to this report.

Due to these problems, companies have idled a lot of capacity. This idling of capacity has led to the rebound in pricing indicated on the graph above.

http://i619.photobucket.com/albums/tt271/vacationpn/Graph3.jpg

The Container Leasing Business

For some reason, most sell side commentary on the leasing industry ignores the health of the customer base as a significant risk and portrays the increase in container rates as good for container lessors. This ignores the fact that rates have gone up because capacity has been taken out of service which creates less demand for leased containers. TAL and others portray the weakness as good for operating results because shippers do not have the capital or are reluctant to otherwise invest in new containers, thus increasing demand for leased containers. Perhaps there is some truth to that, but strong underlying container demand is necessary for that to benefit the lessors. If demand weakens, as it must be due to the lay-ups indicated on the chart above, the benefit becomes a detriment. That is because around 55% of containers are owned by the shippers. Leased containers are always swing demand. Shippers must try to utilize their own assets prior to leasing someone else’s to generate the highest returns.

In understanding the container business it is important to keep in mind that containers are simply steel boxes. There is not technology involved or barriers to entry. It is a pure commodity business. Thus the price of steel has a substantial relationship to the price of containers and thus per diem lease rates necessary to make a reasonable return on such capital investment. As indicated by the graph below, the price of Chinese domestic hot rolled steel sheet, the product used by the manufacturers of containers, dropped about 15% last summer and is below where it was during much of TAL’s recent capital expenditure boom. Thus, it would appear that TAL added much of its new capacity at peak prices.

http://i619.photobucket.com/albums/tt271/vacationpn/Graph4.jpg

LOW RETURN COMMODITY BUSINESS

As one would expect from any commodity business, renting out steel boxes is a very low return business. We created a single container economic model using a $2800 box, a $.80 per diem lease rate and reasonable utilization assumptions and concluded that a single box generates a return of around 6%. Better returns are generated simply by financing the boxes with a huge amount of debt. Below shows the unlevered returns generated and the change when the boxes are 70% debt financed, which is the capital structure of TAL.

http://i619.photobucket.com/albums/tt271/vacationpn/Graph5.jpg

A look at the actual returns of TAL and another publicly traded container leasing company supports the conclusion drawn from our single container economic model.

http://i619.photobucket.com/albums/tt271/vacationpn/Graph6.jpg

RECENT DEMAND & SLOW STEAMING

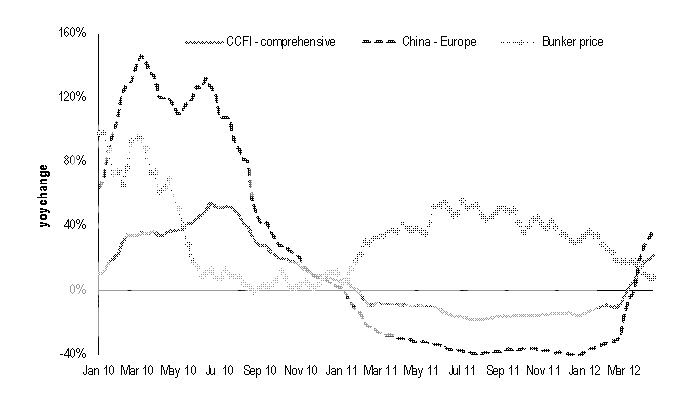

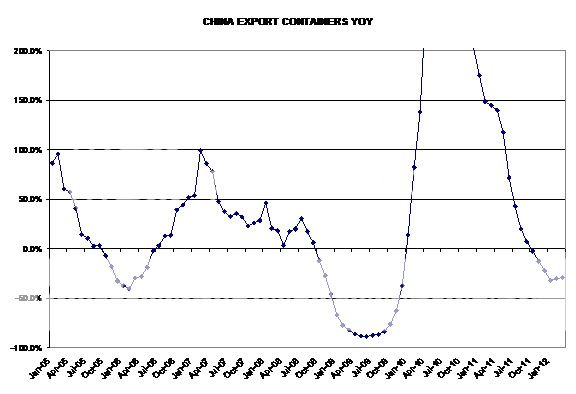

Besides the Shanghai Container index price referred to above, there are other objective indicators of weakening in container demand. It appears the number of containers being shipped is slipping all over the world. The following graphs show containers in certain majorU.S.ports and containers leavingChina, respectively. These are places where, presumably, the world economy is “decoupling”.

http://i619.photobucket.com/albums/tt271/vacationpn/Graph7.jpg

http://i619.photobucket.com/albums/tt271/vacationpn/Graph8.jpg

Despite the slowing world trade, it appears that TAL and it competitors are operating at very high utilization rates. This appears to be due to a strategy called “slow steaming”. This is when shipping companies slow down their ship speeds to conserve fuel costs and drive higher utilization. According to some sources, these slower speeds may have increased the demand for containers by greater than 10%. Slow steaming is described more fully in a Bloomberg article attached to this report. What is significant is that shippers appear to have reached the limit of how slow they can go. “Super slow steaming” is likely to be suboptimal.

Thus, continued year over year declines in traffic and/or increases in container capacity should start to bite into utilization more. Judging by the recent capital spending of TAL and its public competitors, Capacity growth continues unabated. In addition, as mentioned, leased containers are swing capacity. A large portion of leased containers are on long term contract. It is likely, given a slowdown in demand, that as these containers come off contract they will be redeployed into the spot market at lower spot rates or will become idle.

A CLOSER LOOK AT TAL

TAL appears to be a cheap stock when compared to multiples of near term results. That may be why it has performed so well lately. However, if one considers that earnings are peaking, it is expensive. There are few stocks more vulnerable than commodity companies that expand rapidly at the top of the cycle using leverage. If they bet wrong, they destroy a lot of equity value. That appears to be the vulnerability of TAL.

GROWTH AND CONTRACTS

As indicated by the chart below, TAL is growing rapidly (The high growth in earning assets in 2007 and 2008 relative to TEU growth is partially due to the extremely high prices paid for containers in that period). What is clear from the chart is that TAL has expanded capacity rapidly. What is not shown on the chart is, as mentioned above, that expansion is done with 70% leverage.

http://i619.photobucket.com/albums/tt271/vacationpn/Graph9.jpg

Fortunately for TAL, a reasonably high portion of its assets are under long term contracts (the average duration as of the end of the third quarter was 49 months). However 30% of the assets are subject to the declining spot market and existing contracts end regularly and must roll to current rates. Although we do not know the distribution of the 49 months of average duration of the contracts, it is reasonable to assume that between 35% and 40% of TAL’s boxes are subject to market rates over the next six months. That creates a big problem for the company if rates remain stagnant, retest their lows or, as we expect, go even lower. The possibility that some of these contracts have credit risk is also very high. As noted above and in the article attached below, customers are experiencing substantial financial hardship.

VALUATION AND THE SMALL SLICE OF EQUITY

TAL is trading at 2.4 times book value. In this case, book value is a reasonably good approximation of the liquidation value of the firm since the assets of the firm are straightforward and they are depreciated according to a decent approximation of the useful life of the equipment. Judging by the gains booked on the sale of equipment, the values are likely understated by a little, but not a material amount. So, the question is would one pay 240% of liquidation value for an, at best, 6% return on asset business? The material returns to TAL’s business come from levering up the 6% return assets. The answer is that a strategic or private buyer most certainly would not and thus TAL’s appreciation potential is limited.

Importantly for the downside case is that the leverage creates a situation where TAL has a very large enterprise value ($3.5 billion) and a much smaller market capitalization ($1.4 billion). The equity value represents only 40% of the total enterprise value. Given expectations for $500 of ebitda, the firm is trading for 7x ebitda. Not hugely expensive for a commodity business at mid cycle earnings, but certainly not cheap, considering the low returns and the leverage. However, the multiple is extremely rich for peak earnings.

Market perceptions can change quickly and are likely to given the deterioration in the business. Based on likely lower utilization and thus lower per diem pricing, it would be very easy for TAL to earn $125 million less in EBITDA over the course of the next several quarters. If that were to happen and TAL continued to trade at a 7x ebitda multiple, theEnterprisevalue would decline to $2.6 billion, a decrease of $.9 billion. Unfortunately for equity holders, that would leave the market cap of the company at $500 million or a loss in value of 64%.

Similarly, even if the ebitda level stays at $500 million, if the weakness in the business becomes more of a concern and the multiple contacts (which is common when investors in commodity companies realize they are at the peak of the cycle), the equity value could be severely impaired. For example, a drop to only 5.5x ebitda would take $500 million out of the enterprise value and market cap . . . a drop of 36% in the value of the equity.

It is our belief that a combination of these two scenarios will occur. The ebitda level will be judged to be too high and the multiple will contract. If so, the stock price will be materially lower.

MOST RECENT QUARTER SHOWS DETERIORATION

Albeit not large and not dispositive, it appears that the most recently released quarter show evidence that peak has been reached. One example is the steady and perhaps accelerating rate of utilization decline:

3/31/12 12/31/11 9/30/11 6/30/11 3/31/11

Ending Utilization 97.7% 98.6% 98.7% 98.9% 98.6%

Another example is that despite year on year revenue gains of ~ 25%, operating income only increased 12.7% and per share income only increased 4.4%.

Why the street raised numbers based on the most recent quarter is a bit of a mystery.

Also, note the substantial selling by the private equity backers lately.

Container Lines Steam Slower to Restore Profit

Friday, 27 January 2012 | 00:00

Container ships can’t go any slower. Shipping lines are running out of options to stop losses as sailing speeds reach their lower limit, exhausting a solution that helped restore profitability in 2010.

The global container fleet is now cruising near record-low speeds after slowing 11 percent from August when the freight rate market collapsed, according to data compiled by Bloomberg and Lloyd’s Register. Drewry Shipping Consultants Ltd. estimates some of the smallest shipping lines will run out of cash in the second half of this year as the industry fails to adjust to overcapacity that’s allowing customers to push down rates.

“Container lines have already exhausted most of the tricks for absorbing capacity,” said Bjorn Vang Jensen, a Singapore- based vice president at Electrolux AB (ELUXBB) who oversees about 150,000 shipments a year. “Some of these container ships are now so slow that they’re close to the speeds of the old sailing ships. The clippers might actually have been faster.”

With options running out, investors in container-line stocks should brace themselves for losses. Still, shares in Copenhagen-based A.P Moeller-Maersk A/S (MAERSKB), the world’s biggest container line, may fall less than smaller competitors this year because its bigger ships are more cost-efficient, said Rikard Vabo, an analyst at Fearnley Fonds ASA in Oslo.

Slow-steaming, pioneered by A.P. Moeller-Maersk’s container unit, Maersk Line, helps carriers cut costs when times are tough. By sailing at lower speeds, ships need less fuel and can offset capacity stresses by using more vessels to make up for the longer sailing times.

Losing Money

With speeds unlikely to get any slower, the industry is growing more vulnerable to rising fuel costs, and all container lines are now losing money, according to BIMCO, the biggest international shipping association.

“The potential for further slow-steaming seems to be of little significance to the overall market balance,” said Peter Sand, a Bagsvaerd, Denmark-based analyst at BIMCO, whose members control 65 percent of the world’s tonnage. “Compared with the 2009 crisis, we don’t see the same level of idling.”

That’s the message the industry is hearing from advisers including Paris-based Alphaliner, which estimates that slower- steaming may even start raising costs for carriers as they deploy more vessels to meet demand.

“There’s much less potential than in 2009 to mop up excess capacity in reducing the speed further,” Alphaliner said in a Jan. 23 e-mail.

Maersk Shares

Nomura International Plc today cut its recommendation on Maersk shares to “neutral” from “buy,” saying the container unit will also be unprofitable this year.

“Burdened by an unfavorable supply/demand balance at the industry level and an unwillingness by the bigger operators to remove vessels from service, we see only a modest recovery at Maersk Line in 2012,” Nomura analysts, including London-based Mark McVicar, said in a note.

Maersk B shares slipped as much as 0.8 percent today before trading 0.2 percent lower at 40,160 kroner as of 9:52 a.m. in Copenhagen. The 20-member OMX Copenhagen benchmark index gained 0.3 percent today.

For a nine-week trip with ships that carry 8,500 containers, a carrier can cut 3 percent of costs by slowing to 17.2 knots from 19.8 knots. Slowing further to 15.2 knots, by contrast, actually pushes up costs 0.5 percent as the expense of operating the additional ship starts to outweigh fuel reduction, Alphaliner estimates.

‘Super Slow’

Maersk Line says it may be able to bring its speeds down even further. The company cut its average speed to about 17 knots last year from 20 knots in 2008, according to Morten Engelstoft, Maersk Line’s chief operating officer. The company’s whole fleet currently sails at about 16-18 knots, he said.

“There is still some potential for slow-steaming, both for us and probably for the industry,” Engelstoft said in a Jan. 23 interview. “We are looking into the possibility of super slow- steaming. That would be 12-16 knots.”

The 19th-century clippers, the fastest ships of their time, transported tea to the U.K. and U.S. from China and India, according to the website of the U.K. Tea Council. The ships, which had three or more masts and dozens of sails, could reach a peak average speed of more than 16 knots.

Slow-steaming, coupled with idling ships, helped turn a 2009 industry-wide operating loss of $19 billion into a $17 billion profit the year after, according to Drewry. The industry reverted to a $5.2 billion loss last year and prospects for 2012 are “dire” because the gap between supply and demand will grow even wider, the London-based consultant said in a Jan. 4 report.

‘Too Early’

Engelstoft said Maersk Line hasn’t yet committed to even slower-steaming as a strategy for weathering the crisis.

“We are looking at Asia-Europe, but it’s still too early to say if we will introduce super slow-steaming there and to what extent,” he said. “It’s also important for us to maintain a high level of reliability for our customers.”

Maersk may emerge a winner among the world’s biggest container lines, according to analyst Vabo. Still, the company’s shareholders probably will lose money in the short term because there are no immediate solutions for overcapacity, he said.

Vabo estimates Maersk shares will plunge 18 percent over the next three to six months from their levels of Jan. 17, while TUI AG (TUI1), the listed owner of the world’s fourth container line, Hapag-Lloyd, will fall 21 percent. Neptune Orient Lines Ltd. (NOL), the world’s sixth-largest listed line, will drop 37 percent, he estimates. Shareholders of Hyundai Merchant Marine Co. Ltd. (011200), the world’s 18th-largest line, will suffer the most: The company stands to lose more than half its value.

Winners, Losers

“The winners will be the companies that have the lowest costs on their ships, run them efficiently and have good balances,” Vabo said. Maersk could gain more than 50 percent after the container market has recovered, he said. The shares lost 25 percent in 2011, its second-worst share performance over the course of a calendar year since 1998.

Other options for adjusting to overcapacity in the shipping industry are also proving untenable. Many ships haven’t yet been paid off by their owners, and scrapping vessels that represent a financial liability isn’t feasible, Sand at BIMCO said.

The average age of the world’s container fleet is less than five years compared with about 11 years for the global dry bulk fleet and nine years for tankers, according to BIMCO.

Closely held CMA CGM SA, the world’s third-largest line, said “there is still room to reduce the speed” of its vessels, though the Marseille-based company didn’t provide details in an e-mailed reply to questions. Hapag-Lloyd, based in Hamburg, could also sail slower, though it doesn’t have any plans to do so, Rainer Horn, a spokesman, said by e-mail.

Going Bankrupt

Meanwhile, freight rates earned by carriers weren’t enough to cover fuel costs in the fourth quarter, according to BIMCO’s Sand. The price of container-ship fuel rose to a record on Jan. 20, up 32 percent from a year earlier, according to a Bloomberg index on global average prices for 380-centistoke bunker.

Global freight rates dropped on average 25 percent last year, according to RS Platou Markets AS. Prices fell the most on Asia-to-Europe routes, where the decline was almost 60 percent, the Oslo-based broker said in a Jan. 4 note.

“The container market can’t stay at this level for a prolonged period of time as everyone then will basically go bankrupt,” Vabo at Fearnley said. “It’s at unsustainable levels.”

Source: Bloomberg

| show sort by |

Are you sure you want to close this position TAL INTERNATIONAL GROUP INC?

By closing position, I’m notifying VIC Members that at today’s market price, I no longer am recommending this position.

Are you sure you want to Flag this idea TAL INTERNATIONAL GROUP INC for removal?

Flagging an idea indicates that the idea does not meet the standards of the club and you believe it should be removed from the site. Once a threshold has been reached the idea will be removed.

You currently do not have message posting privilages, there are 1 way you can get the privilage.

Apply for or reactivate your full membership

You can apply for full membership by submitting an investment idea of your own. Or if you are in reactivation status, you need to reactivate your full membership.

What is wrong with message, "".

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}