| 2017 | 2018 | ||||||

| Price: | 32.50 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 62 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 2,015 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 285 | EBIT | 0 | 0 | |||

| TEV (in $M): | 2,300 | TEV/EBIT | 0 | 0 | |||

| Borrow Cost: | Available 0-15% cost | ||||||

Sign up for free guest access to view investment idea with a 45 days delay.

- MeToo

Description

DISCLAIMER: At risk of looking dumb, I'm post this before earnings on 8/2/2017.

Recommendation

Initiate a short position in Teladoc, Inc. (“Teladoc”, “TDOC” or the “Company”) with a ~12 month price target of ~$15 per share representing over a 60% return.

Business Description

Founded in 2002 and brought public in July 2015, Teladoc is the sole publicly traded telehealth provider. Teladoc contracts with employer health plan sponsors, managed care companies and other payers to provide beneficiaries access to its on-demand network of providers 24 hours a day, seven days a week, 365 days a year. The Company deploys its multimodal technology (no patents) to connect patients with providers on-demand. Teladoc can connect patients with providers either via voice telephone (~80%+ of visits), a smart device, or a PC.

Teladoc’s platform connects its more than 4,000 payer clients representing almost 20 million beneficiaries with its network of more than 1,100 board-certified physicians and behavioral health professionals, commonly treating ailments including sinusitis, allergies, and urinary tract infections. Teladoc’s business model is straightforward, charging payers a per-member-per-month fee for access to the network ($4 to $5 per year), plus a fee for the provider visit ($45 or free for certain plans). TDOC’s doctor network consists of 700+ doctors, who receive ~$25 per consultation.

For the LTM period, Teladoc generated $182MM of revenue and an Adj. EBITDA loss of $39.4MM.

Recent Transaction Overview

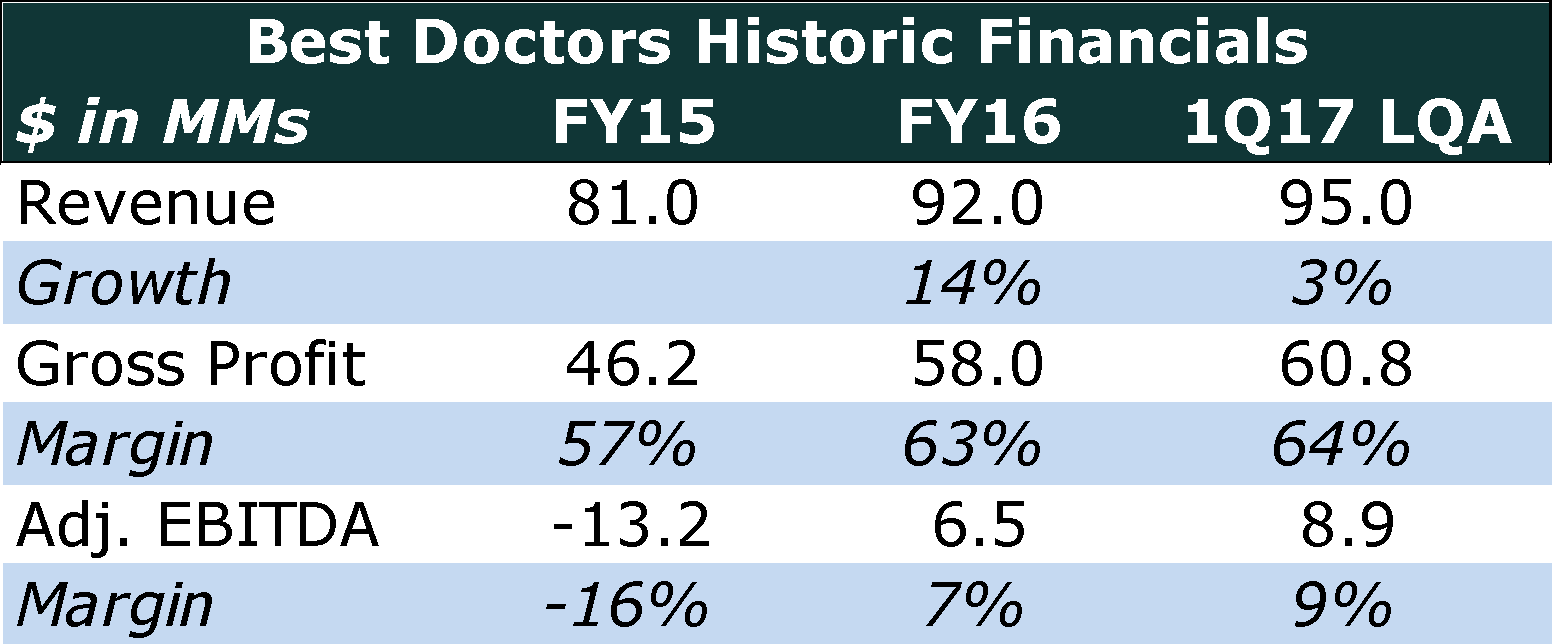

On 6/19/2017, Teladoc announced the acquisition of Best Doctors Inc., a specialist network provider focused on the second opinion market, for $375MM in cash and $65MM in stock. This represents a 4.4x FY17E revenue and 55x FY17E Adj. EBITDA multiple. Best Doctors operates in a segment outside of Teladoc’s core telehealth offering with little cross-selling capabilities. Best Doctors is expected to grow in the high single digits to low teens range, which is materially below Teladoc’s historical growth rate.

Founded in 1989 and headquartered in Boston, Best Doctors is the largest provider of second opinion diagnoses. Best Doctors contracts with ~800 clients, mostly employers whom use their services to provide their employees with second opinions on complex and often costly medical issues. For FY16, Best Doctors generated $92MM in revenue and $6.5MM in Adj. EBITDA.

Short Selling Thesis

Market euphoria amongst momentum tech equities has created an attractive short selling opportunity which resembles a floundering business straight out of the script from the HBO sitcom, Silicon Valley. Teladoc is perceived as a high-growth technology company yet contrary to the sell-side thesis, Teladoc is a structurally challenged middle-man provider with 15 years of negative cash flow and EBITDA. While the telehealth industry is growing overall, the Company faces a variety of challenges for which the current stock price is not pricing in:

-

Disintermediation by both clients (Aetna, etc.) and doctor/providers;

-

Lack of operating leverage and an increase costs;

-

Declining gross margins due to pricing pressure, dissipating recurring PMPM fees and a decline in take-rates which is materially higher than that of low/lower skilled industries such as Uber, GrubHub and Soothe;

-

Cost disadvantage vis-à-vis traditional in-person offerings such as urgent care;

-

Increased competition and new entrants such as Amazon;

-

Saturated employer end market answered by an irrational acquisition strategy;

-

Cash burn and financial leverage

While the health care industry is often slow to evolve at times, it is clear these trends are materializing and for that reason we believe significant EBITDA growth is improbable.

Teladoc’s stock price performed well over the past year, appreciating by over 120%. This has been partially driven by market acceptance of Teledoc reaching their goal of Adjusted EBITDA break-even by 4Q17E and aggressive growth goals. The story narrative has morphed as Teladoc has entered upon an expensive acquisition spree in order to meet aggressive guidance, purchasing low quality assets such a HealthiestYou and Best Doctors, financing these acquisitions with expensive debt and little regard for valuation paid as well as re-entered the uneconomic small business market which generally lacks PMPM fees and boasts lower margins. In the case of Best Doctors, Teladoc paid $440MM and $24MM per annum in interest expense for a business generating $5MM in Adj. EBITDA, growing 10% per annum.

Teladoc is not a transformative technology business worthy of artificial intelligence, virtual reality or advanced biotech valuation(s). Teladoc is a combination of an early 2000s’ call-center, a 1980s’ healthcare business and a failed mobile application, conjuring the public of its ability to revolutionize healthcare. Conversely, it is highly probable Teladoc fails to deliver on its lofty profitability goals and top-line revenue goals as well as utilization guarantee made to clients. Nonetheless, we expect further EBITDA losses and cash burn.

Saturated Market & Style Drift

At its IPO, Teladoc noted the large employer market as a prime opportunity and sole focus for sustainable 50%+ revenue growth. Channel checks paint a vastly different picture, noting that the large employer markets are saturated with little evergreen opportunities for telehealth providers. This has forced Teladoc back into focusing on the uneconomic SMB space which are generally structured as visit fee only carrying vastly inferior margins despite carrying similar cost to service and nearly bankrupted the Company in the 2000s’. Moreover, Teladoc has started to dabble new verticals which have been demonstrated lackluster results thus far.

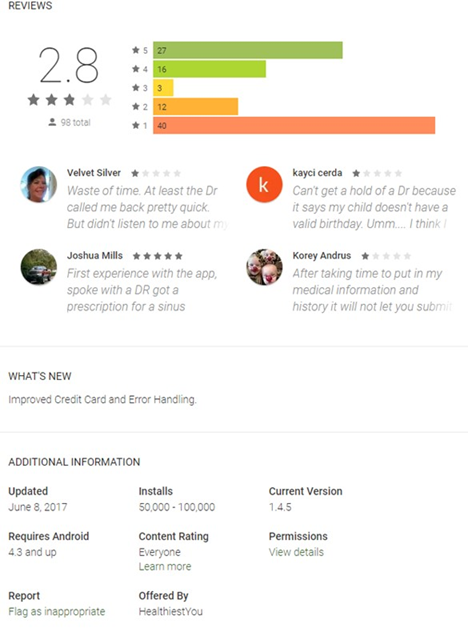

In June 2016, Teladoc paid $155MM paid for HealthiestYou, an app with ~$10MM in revenues, poor reviews and a meager 50K to 100K downloads on Android with a decline in new downloads. TDOC purchased HealthiestYou simply to artificially boost their PMPM fees.

Teladoc has painted the story of growing visit fees through new growth vertical such as behavioral health (Better Help). Instead, this segment which has seen a ~32% decline in downloads versus competitors such as TalkSpace whom have experienced ~20% growth in downloads. Even with the new initiatives, a combination of PMPM fee only contracts and likely visit fee concessions, blended visit fees have remained under $25, implying a gross loss per visit.

With new initiatives floundering, Teladoc has taken desperate measures to reach EBITDA breakeven, overpaying for Best Doctors, an asset outside of its core telehealth segment, creating tremendous risks mainly related to integration as well as financial leverage for a meager ~$5MM in adjusted EBITDA.

Threat of Disintermediation & Pricing Pressure

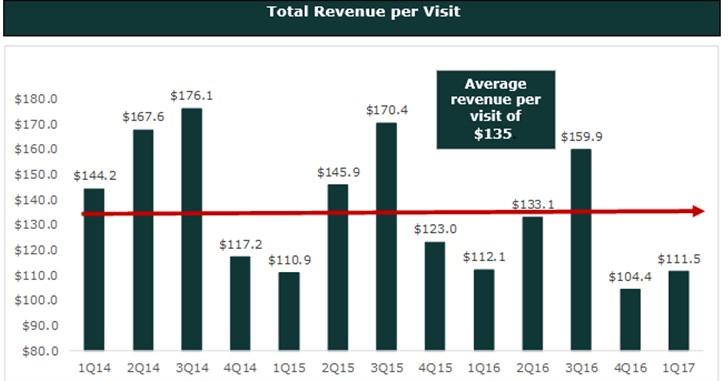

Due to the continued increase in healthcare costs, Teladoc faces a real risk of disintermediation as providers and payors could easily forgo middlemen such as Teladoc and opt for direct telehealth solutions utilizing a mix of white label software and in-house solutions (such as Aetna’s solution) to increase efficiency and maintain margins. Rolling out a similar business in-house would not be a daunting task considering the low barriers to entry and lack of technology required. Teladoc notes that it’s solutions are one of the lowest cost methods to provide healthcare, this is simply not true. The total cost per visit (PMPM fees plus visit fees divided by visits) has remained over $130 per visit, which is materially more expensive vis-à-vis other options, such as urgent care clinics such as Medspring or WAG’s partnerships which are often available anywhere from $10 to $90 per visit.

Historic & Consensus Quarterly Gross Margins

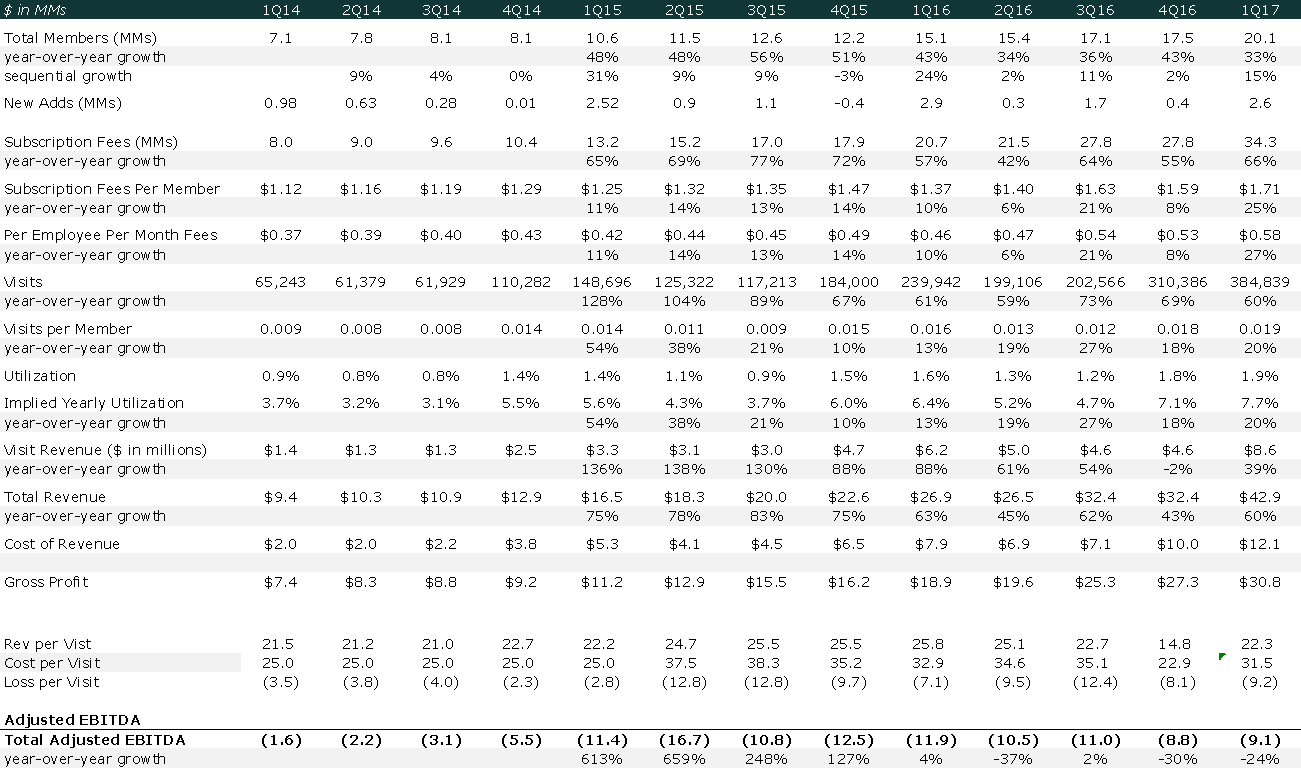

Henceforth, insurers such as Aetna are likely focused on white label solutions, internally developed platforms as well as including lower cost telehealth providers without PMPM fees on their respective platforms. This is particularly material if the rumored changes materialize at Aetna, which recently launched their internally develop vHealth app or a second source/white label is added, considering Teladoc sourced 2MM out of their 2.6MM members added in 1Q17 or 40% of the total membership base (accounting for over 75% of Teladoc’s member growth). Note this wouldn’t be the first time an insurer exited the or added as secondary source to a Teladoc platform.

Pricing pressure is likely to increase due to competition, which does not bode well for the Company given its negative gross margin visit business and high estimated gross margins on its subscription access revenues. Recall that Teladoc purchased peers include plans that are structured as free visits per member versus the $40 per visit fee historically paid or PMPM only. The PMPM fee only model is not optimal given the higher the utilization (higher member usage/positive for the employer), the higher the cost to service on Teladoc’s behalf and lower margins. The industry has slowly shifted to visit fee only with providers such as Doctors on Demand charging $40 to $70 per visit, Teladoc has also followed this trend, structuring some contracts in a similar manner. This set up is also not profitable given the cost to service. Industry participants suggest recurring PMPM fees (70%+ of revenue) will dissipate over a 2 to 3 year time horizon.

No Moat, Low Barriers to Entry Industry with Undifferentiated Peers

While telemedicine is a growing industry, it has little in terms of barriers to entry, defined as having multiple competitors such with no pricing power and low switching costs. For example, a new entrant would simply need to license technology, hire an outsourced call center and sign up doctors/providers in order to start their business. Switching costs to onboard new telehealth providers with over 10 comparable providers today, it won’t be a surprise to see new participants enter the space or experience in-sourcing by payors/providers. Moreover, this is supported by the Company’s lack of patents and low R&D spend over the past 13 years.

-

Service is also undifferentiated amongst offerings from other telehealth providers or difference in outcomes versus office visits. At the end of the day there is very little differentiation in the industry beyond wait times and care – for in-person offices have the clear advantage due to the ability to write any prescription needed. Note most competitors also note quick response times.

-

Amazon is likely entering the space through it’s 1492 team. https://www.cnbc.com/2017/07/26/amazon-1492-secret-health-tech-project.html

-

With consistently negative gross profit per visit, Teladoc has no pricing power as with every additional visit, the Company experiences negative 10%+ gross margins. With no operating leverage (costs per visit are one for one), TDOC faces declining pricing and gross margins particularly as competition continues to intensify.

-

Issues with doctor quality are a concern given the low absolute profitability for the MD per visit which incentives them to quickly complete a visit leading to a poor quality of service. While this anecdotal information has come up in diligence calls, it can also be seen through recent Yelp reviews: https://www.yelp.com/biz/teladoc-dallas-2

Growth Multiple for a Glorified Call Center

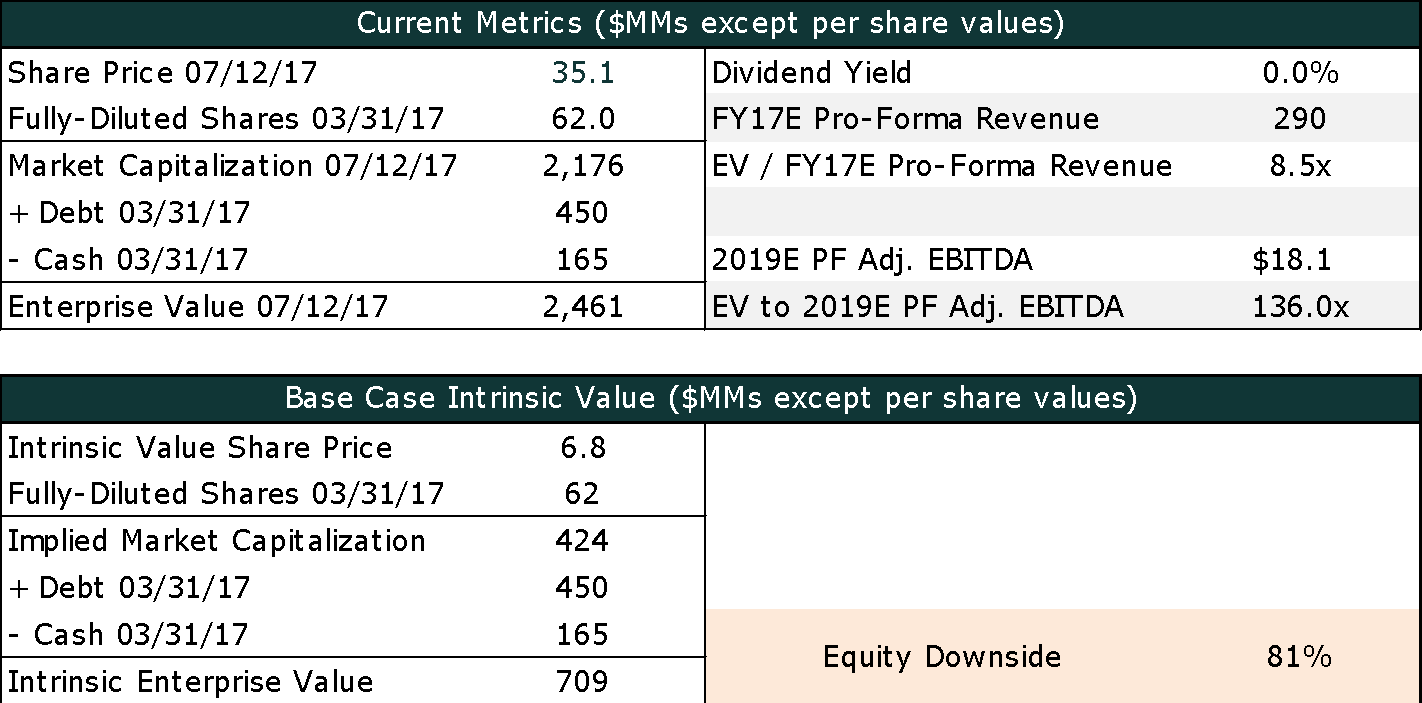

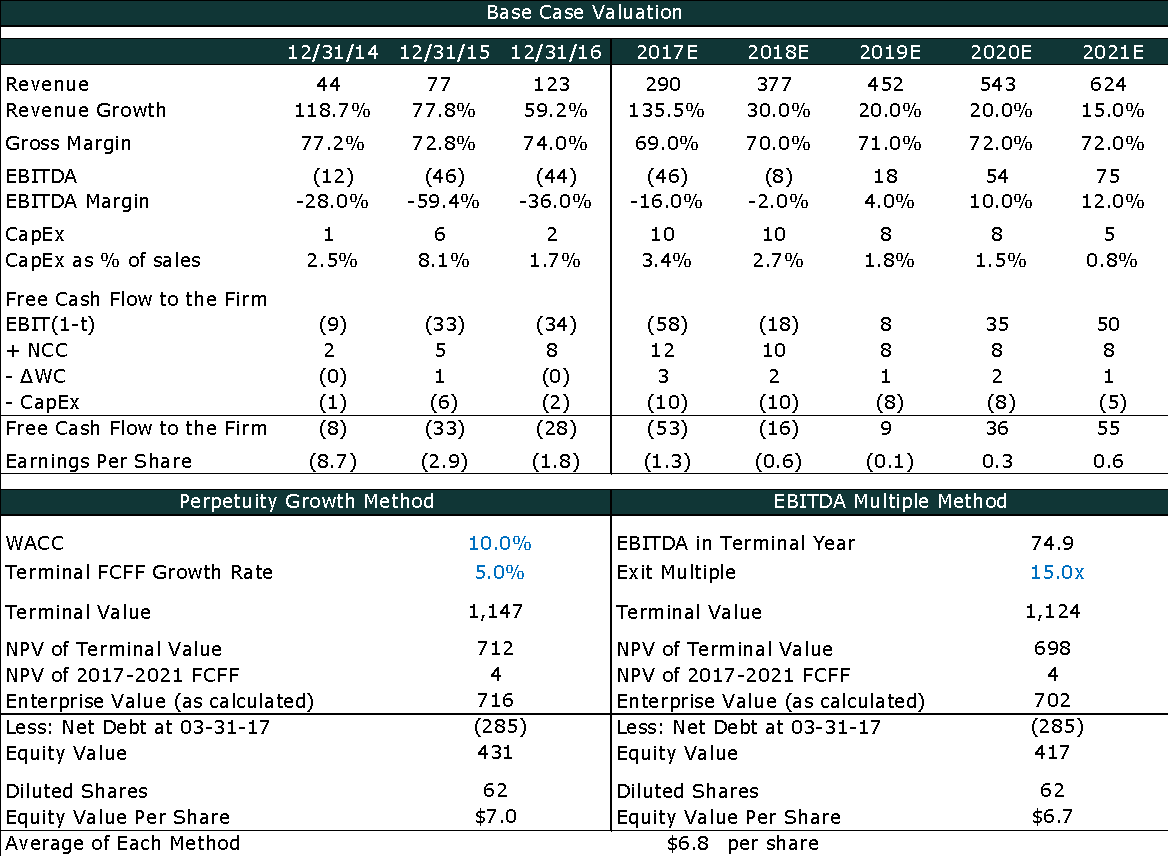

Teladoc currently trades for a staggering 8.5x pro-forma FY17E revenues which offers no margin of safety considering the Company is expected to continue its 15+ year track record of negative EBITDA and cash flow generation over the next year. Teladoc has also acquired peers and its largest asset Best Doctors at ~3x – 5x revenues which in its own merits are expensive yet reflects the irrationality of TDOC’s current multiple. For essentially a call center operator with little in terms of patents and IP, TDOC should trade below 3x revenues particularly as organic top-line growth decelerates.

Moreover, assuming aggressive margin assumptions and operating leverage for which TDOC has lacked to demonstrate, Teladoc would be valued at ~$7 per share, significantly below the current price and squarely highlights the irrationally high expectations baked into the stock price.

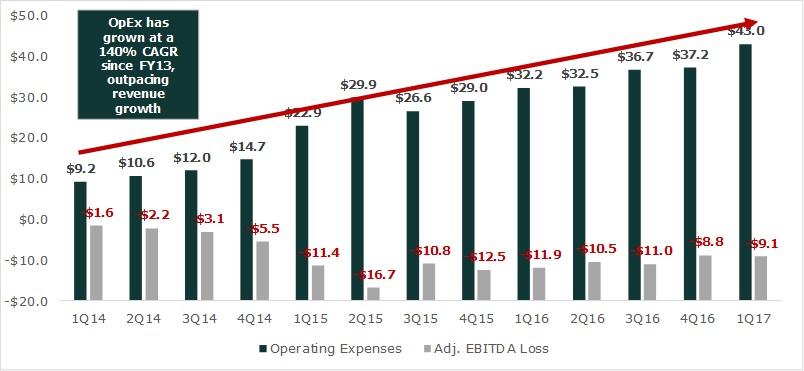

Lack of Operating Leverage

Teladoc’s business model exhibits little operating leverage as demonstrated by the continual degradation of its margin profile. For instance, with each visit Teladoc generates negative gross profits, implying with every additional visit TDOC will lose greater gross profit dollars. Moreover, the business has no pricing power and cannot raise visit fees given their positioning vis a vis primary care physicians. The perceived first mover advantage holds no merit as TDOC contracts are typically one year contracts which can be switched over to other providers with ease.

Despite growing the top-line in excess of 50% and consummating various acquisitions such as HealthiestYou, Teladoc has yet to demonstrate operating leverage and a material improvement in profitability. For instance, in 1Q16, TDOC added 2.9MM members and generating $26.9MM in revenues and an EBITDA loss of $11.9MM. For 1Q17, TDOC added lower number of new members (2.8MM), had 59% growth in revenues ($42.9MM) yet still managed to generate a $9MM+ EBITDA loss, or a meager $2MM improvement in EBITDA losses. Nonetheless, the consensus expects TDOC EBITDA losses to improve by $4MM to $6MM per quarter with a meager $1MM to $2MM sequential increase in revenues.

Historic & Consensus Quarterly Gross Margins

|

Nonexistent Operating Leverage |

Gross margins will likely decline as Teladoc’s take rate is fairly egregious vis-à-vis other service platforms such as Uber, Soothe, GrubHub etc. On a total baked per-visit basis, a doctor on the TDOC platform will earn ~$25 to $30 per visit or a 75% take-rate versus other service platforms such as Soothe which take in ~20% to 30% per visit/massage. While the health care industry tends to move slow, there is no logical reason to explain why a highly-trained doctor should earn significantly less per visit than a masseuse (~$60 to 70 per visit). Over the coming years, this spread will likely collapse particularly as TDOC is disintermediated.

Per the disclosed pro-forma financials, the Best Doctors acquisition does not materially improve an increase in profitability on a combined basis. The reality is that unit economics for TDOC’s business are terrible. Even if revenue guidance and gross profit margins are maintained or held flat, TDOC would need to reduce quarterly cash operating expenses from $47MM to $43MM within their core business. Meanwhile operating expenses continue to increase.

Minimal Insider Ownership & Insider Selling

While not core to the short thesis, management have been recent sellers as of recent, while VC firms originally involved with TDOC and its acquisitions have been net sellers. Moreover, employee turnover and poor employee reviews have been of concern.

For instance, the head of sales for Teladoc’s employer market recently quit, not a positive and supports our notion that evergreen opportunities within the large employer market are few and far between.

Purchase of a Low Growth Asset Has Left Teladoc in a Precarious Financial Position

Due to likely future deterioration of the core business and an aggressive plan to reach adjusted break-even by 4Q17, TDOC’s management believed it to be a great idea to purchase an old-line healthcare services business in an adjacency outside of telemedicine. In layman’s terms, Teladoc paid $440MM for a business and is on the hook for $24MM per annum in interest expense in exchange for a business generating $5MM in EBITDA, growing 10% per annum.

Highlighting their lack of financial savviness, Teladoc’s management paid over 4.4x revenues and ~55x forward adjusted EBITDA for an asset growing under 10%, significantly below Teladoc’s historic growth rate. Not only was this asset outside of Teladoc’s core competency, the financial profile is drastically different with revenue growth under 10% expected for FY17E (3.2% using 1Q17 annualized), and gross margins 7% - 10% lower than the TDOC historic average.

Importantly, the Company has levered up with over $450MM gross debt/$285MM debt to EBITDA while generating more than $30MM in EBITDA losses per annum and consistently negative free cash flow. Given that Teladoc in its public history nor its management team have operated with net debt nor have consummated a large acquisition, the entity is at risk of financial stress. Said simply, how is it prudent that a business with impending headwinds, $40MM in EBITDA losses and steadily burning cash, cover the yearly $22.7MM interest obligation?

We believe Mr. Mark Hirschhorn’s comments from the M&A call highlight their nervousness around the sustainability around the current capital structure as well as the potential for future dilutive equity issuances:

“Yes, that's a good question, Jamie. I'm currently looking at a number of options. Clearly, where the market is today, where we're performing today, we have a number of options in front of us which we'll pursue. I could resoundingly tell you that I'm not comfortable maintaining a level of debt at the level which we would require to complete this transaction for too many quarters.”

Why Does This Opportunity Exist & Variant View

-

Telehealth is a Growing Market & Teladoc is the Only Public Entity to Invest in the Theme:

Rebuttal: Telehealth is a growing industry, with TAM likely to total in excess of $3B by FY20E, yet the consensus fails to address competition, and white labeled solutions, particularly as health care providers and plans eliminate middlemen and likely opt to license technology.

TDOC’s stock has substantially increased over the past year being portrayed as the only public pureplay investment and beneficiary within telehealth. This is misleading as the market is overlooking the real beneficiaries and winners within telehealth, notably the providers and insurers. Moreover, we lay out the following scenarios for which Teladoc achieves their “evergreen” top-line estimates:

Note in this scenario we assume Teladoc maintains their pro-forma gross margins. Realistically due pricing pressure, TDOC take-rates being too high and SMB/MM as well as enterprise transitioning to visit fee only methods, gross margins will likely fall below 50%.

In this more likely scenario, Teladoc cannot achieve profitability outside of significant cost cuts.

Lastly, likely due to an impending slow-down within their respective business, Teladoc has muddied it’s narrative and is no longer a pureplay on telehealth due to the acquisition of an “old-line” healthcare services provider, Best Doctors which shares little in terms of synergies.

-

EBITDA Break-Even by Q4 2017

Rebuttal: TDOC’s EBITDA break-even goal by 4Q 2017 appears unachievable given the business model’s lack of operating leverage as OpEx continues to grow in addition to future pressure on PMPM fees by large insurance providers such as Aetna. Moreover, Teladoc effectively loses money each time a visit is consummated which is contrary to its estimates.

Notably, the street expects operating expenses to decline by over $3MM per quarter, while gross margins increase. However, operating expenses have been on the rise, increasing at a ~140% CAGR over the past years while gross margins have declined and will continue to decline due to the inclusion of Best Doctors and pricing pressure.

Henceforth, TDOC has attempted to purchase its way into meeting its 4Q17 through the $440MM acquisition of Best Doctors as well as the shifting of expenses into SBC. Per the Company’s disclosed pro-forma financials, TDOC’s combined operating loss shows no improvement over the combined entity on a standalone basis, and on a cash basis is materially worsened. While Teladoc may reach “Adjusted” EBITDA break-even in a downside scenario, it will be squarely negative on a CFO and FCF basis given the burdensome increase in debt and corresponding interest expense. At the end of the day, cash losses and burn are material and a driver of value over “empty calorie” Adjusted EBITDA full of pro-forma dubious add backs.

-

Clear Cost Savings for the Consumer

Rebuttal: While the argument for ease of use holds some merit, cost savings for the end consumer is false. While some portray as the cost of a Teladoc vist in the $40 to $45 dollar range, the blended average cost per visit inclusive of PMPM fees is in excess of $120 per visit which is more expensive than primary care ($24 to $80), and urgent care ($36 to $100).

Although not directly quantifiable, phone or webcam visits open up a higher probability for misdiagnosis as well as potential abuse (i.e. online visits to obtain medication). Moreover, multiple reviews we read led to doctors suggesting patients go to a local provider for an in-person visit.

-

Value Proposition for Doctors

Rebuttal: The Company pitches itself as a prime offering for doctors due to the ability to earn $150 per hour versus ~$99 per hour running their own offices. This is flawed, as it would require the doctor to triage over 6 patients or an implied 10 minutes per visit versus an average visit of 14 minutes. Per industry sources, the average doctor would see 2-3 patients per hour yet under the TDOC model they would have to see 4 at minimum in order to achieve comparable payment levels. Not only is this extra work, it leaves room for error and potential medical mistakes hence the quality of care may actually decrease.

Additionally doctors are restricted to what they can treat by phone (top ten cases per TDOC are flu/cold/nasal congestion/UTI/yeast infection). It is perhaps safe to assume many doctors did not attend medical school in order to be able to just treat 5-10 common of which Teladoc has only attracted 675 over the past 13 years.

-

Disruptive Technology

Rebuttal: Teladoc is not a disruptive tech company nor is it even a “web 1.0” business. Teladoc holds no patents, spends very little on research and development and has over 80% of health consultations by phone. While the sell-side compares TDOC to disruptive SaaS companies such as Veeva, a more reliable comparable set would include call-center businesses and BPO providers.

Catalysts to Value Realization

|

Catalyst |

Description |

|

Insurers and Employers Remove Teladoc as Sole Source Supplier |

|

|

Financial Leverage |

|

|

PMPM Fee Pressure |

|

Risks & Mitigants

|

Risk |

Impact |

Mitigant |

|

Technical |

Short Squeeze |

|

PMPM Fee Pressure Does Not Materialize |

Operating margins improve |

|

Cost Controls |

Inflection in Profitability. |

|

New Member Growth and Increased Utilization |

Top-Line Growth |

|

Trading Considerations

-

Daily liqudity of $32MM.

-

Short interest of 24%. Lending pool utilization is not worrisome.

-

52 week high of $36.9 per share, 52 week low of $13.5.

-

Sell-side coverage preodomiantly consists of boutique and regional banks such as Craig Hallum, Chardan and William Blair.

-

Sentiment is strong with ratings mainly consisting of buys/overweight.

-

Expectations are high – with estimates in-line with management guidance.

-

Shareholder base is predominatly GARP and growth managers per CapIQ as well as remnant venture capital firms whom have been net sellers.

-

Per the following chart, estimates have steadily declined while the stock price has appreciated highlighting the irrationally high expectations.

Historic Financials

Capital Structure

Scenario Valuation Analysis

Base Case

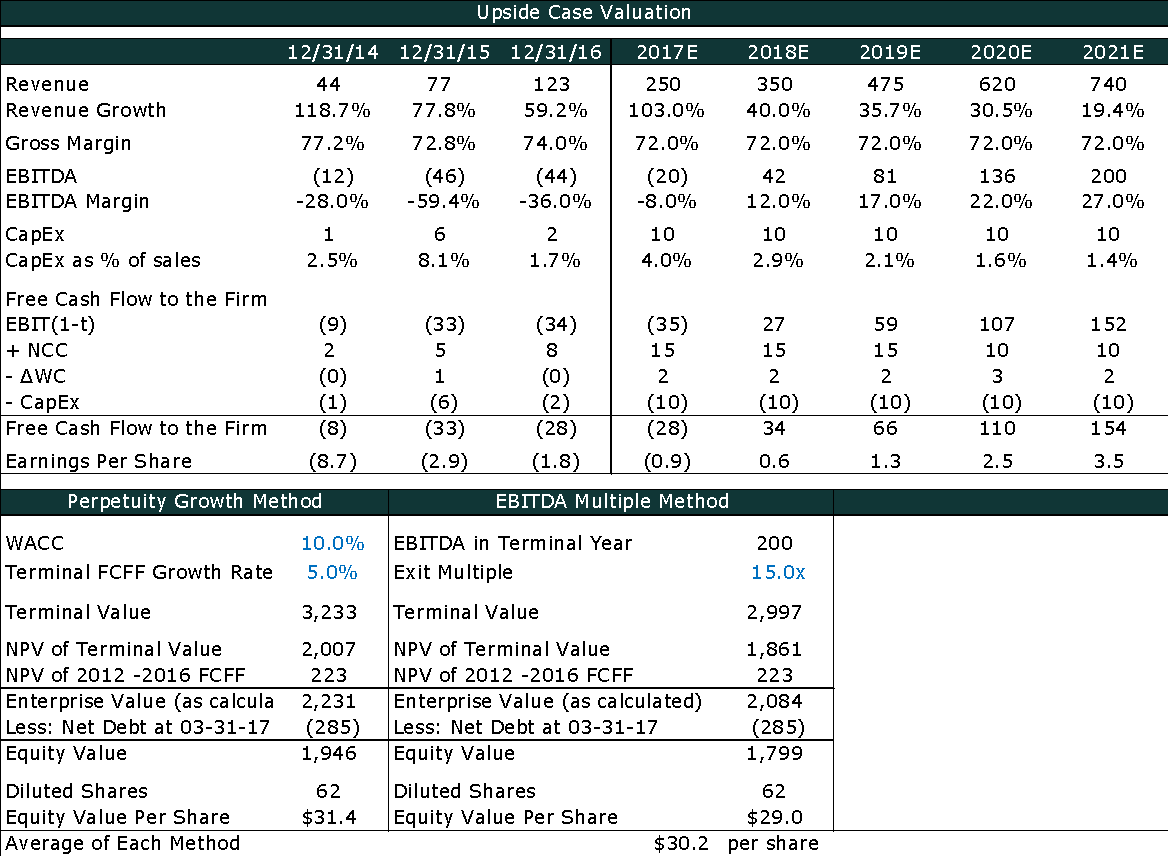

Upside Case – Sell Side Consensus

Conclusion

The current market environment has been highly irrational, especially for momentum tech names with dubious product offerings, no moats and “X as a service” in the business description. Teladoc is the main beneficiary of this current euphoria creating a highly attractive short set-up given the balance sheet leverage, lack of cash generation and impending competition.

The process behind the valuation and set-up can be perfectly explain once again by tech investor extraordinaire, Russ Hannenman of Silicon Valley in the following clip:

"Who is worth the most? Companies that lose money."

https://www.youtube.com/watch?v=BzAdXyPYKQo&t=2s

I and/or others I advise do not hold a material investment in the issuer's securities.

Catalyst

Please see above in the respective writeup.

| show sort by |