| 2019 | 2020 | ||||||

| Price: | 780.00 | EPS | 31.92 | 39.31 | |||

| Shares Out. (in M): | 8 | P/E | 24 | 20 | |||

| Market Cap (in $M): | 6,050 | P/FCF | 29 | 24 | |||

| Net Debt (in $M): | -93 | EBIT | 305 | 375 | |||

| TEV (in $M): | 5,957 | TEV/EBIT | 20 | 16 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

Description

TPL has previously been written up and discussed on VIC, but I believe that this analysis adds to the discussion and is worth a full writeup. When I started this exercise, I thought this was going to be a short sale recommendation; TPL is an oil and gas company that trades at ~21x Q119 annualized EBITDA. However, after doing the work, I believe that TPL is a long.

TPL is a liquidating trust that was set up in 1888 to manage the assets of the bankrupt Texas & Pacific Railway Company. TPL has the ability to manage its assets with all the powers of an absolute owner, but it is not authorized to issue new equity. The business model of the Trust, in accordance with the trust indenture, is to manage the land and mineral rights and to divest those lands and mineral rights on an opportunistic basis, eventually liquidating all assets for the benefit of investors. Over the past few years, TPL has gotten more active, forming a water company and reinvesting the proceeds of asset sales instead of distributing all of the proceeds to investors. I will talk a little about governance and the current proxy fight later on. It is a cause for concern. Trustees serve for life, severely diminishing the ability for shareholders to exert influence.

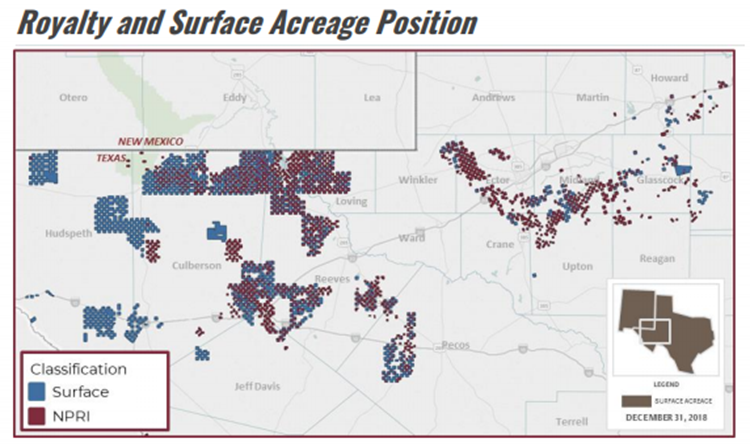

TPL has three main buckets of value: surface acreage/rights, water business, perpetual royalty interests. Below is a decent map of TPL’s acreage position.

Surface Acreage/Rights

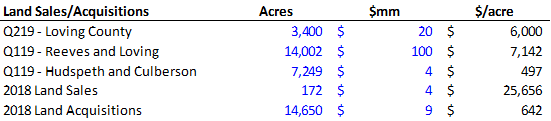

The simplest bucket of value to deal with is the surface acreage/rights. TPL’s surface rights generate revenue from easement contracts covering activities such as oil and gas pipelines and subsurface wellbore easements. The majority of TPL’s easements have a ten-year term (i.e. TPL gets paid again every ten years if the easement is still required). TPL also leases land to operators and midstream companies for facilities and roads. From time to time TPL will sell pieces of their surface acreage. Typically water rights are attached to the surface rights which makes it hard to separate the value of the two when looking at recent land transactions; however an attempt to do so must be made to avoid double counting the value of the surface and the value of the water business. Below is a table of recent TPL land sales and acquisitions and the implied $/acre metrics. There is a wide range. Anecdotally I have heard that pure goat pasture in the middle of nowhere West TX is ~$400/acre. The lowest value in the table below for the Hudspeth and Culberson sale appears to confirm that figure as being conservative. However, there are definitely parcels of land closer to oil and gas activity or small metropolitan areas where surface rights ex water would have more value than that.

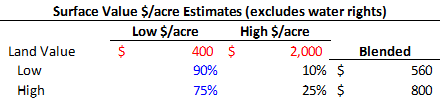

Below you can see my assumptions in coming up with a blended average surface rights value range of $560/acre to $800/acre.

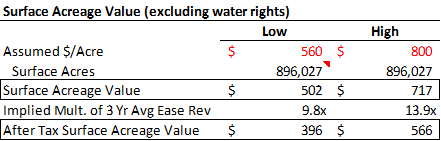

Using those blended averages, I calculated the pre-tax surface rights value to be between ~$500mm and ~$700mm (see table below), which implies a ~10x to ~14x multiple on the past 3 years average easement revenue ex water easements. Assuming no tax basis, that is ~$400mm to $565mm of after tax liquidation value to TPL.

It is worth noting that TPL is starting to get more active in this business line. They sold a large parcel at an apparently nice valuation to WPX in January 2019 for $100mm. Rather than pay the tax and distribute the proceeds to shareholders, management decided to structure the transaction as a 1031 exchange to defer the taxes and reinvest the proceeds. This is not necessarily bad, but it is out of line with the stated purpose of the trust and bears watching, especially given the aforementioned governance concerns.

Water Business

Over the past couple of years, TPL has started building out a team to take advantage of the water rights associated with its ~900k surface acres. The water opportunity in the Permian, and especially the Delaware, is huge. There are multiple private equity teams with massive equity commitments chasing deals (Goodnight, Waterbridge, etc). TPL’s water rights are extremely valuable and provide TPL with a competitive advantage in the water sourcing and disposal businesses. Most industry participants must make deals with surface owners for water sourcing rights, water disposal rights, and water pipeline easements. Typically these agreements involve up front payments and a royalty payment per barrel of water. TPL’s vast surface ownership gives it a cost advantage over its competitors when it chooses to compete head to head for customers because TPL does not have to pay anything (up front or royalty) to the surface owner. TPL is the surface owner. In addition, when the economics make sense, TPL can choose to partner with a competitor who will spend all required capital and pay TPL a royalty on any water produced from or disposed on TPL’s land. In short, TPL’s water business is far more capital efficient than its competitors. Since forming Texas Pacific Water Resources LLC in June 2017, TPL has invested ~$70mm in the water business. Q119 annualized EBITDA was $39mm (100% G&A burden) which implies a ~2.0x EBITDA multiple. Those are strong economics. TPL is hiring aggressively to build out its water team (employee count increased from 8 at 12/31/16 to 71 at 1/31/19). Getting the right commercial team in place is a key risk to this business, but TPL is making good progress. Robert Crain joined TPL in June 2017 as the Executive Vice President of TPWR. Prior to joining TPL, Crain was Water Resources Manager with EOG Resources where he led the development of EOG’s water resource programs in the Eagle Ford and Permian.

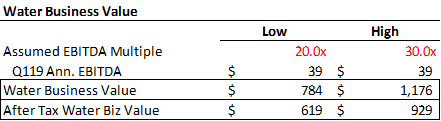

Below I have set a valuation range for the Water Business at 20.0x - 30.0x Q119 annualized EBITDA, and once again I have applied a 21% tax rate assuming no tax basis to get to a net liquidation value to TPL.

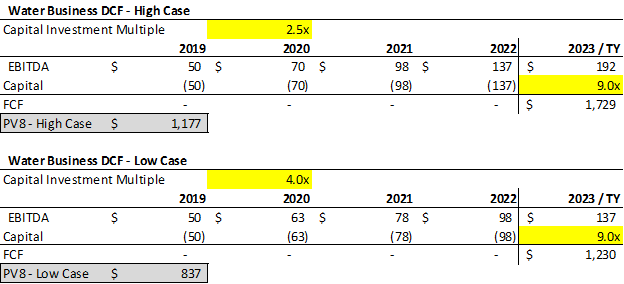

At first glance these EBITDA multiples appear to be insane. The only publicly traded source water business (WTTR) trades at a mid single digit EBITDA multiple and the produced water businesses changing hands in the private market seem to be in the high single digit to low double digit EBITDA multiple range. That said, I believe that 20.0x - 30.0x is correct. In the tables below I have laid out two simple DCF’s for the water business. In the top table, the High Case, TPL invests 100% of its Water Business EBITDA each year back into the business at a 2.5x multiple through 2023 at which point I applied a 9.0x multiple. In the low case we make the same assumptions except we are investing capital at a 4.0x multiple. The PV8s of these two simple DCFs line up pretty closely to the pre-tax values implied by the EBITDA multiple range assumed above.

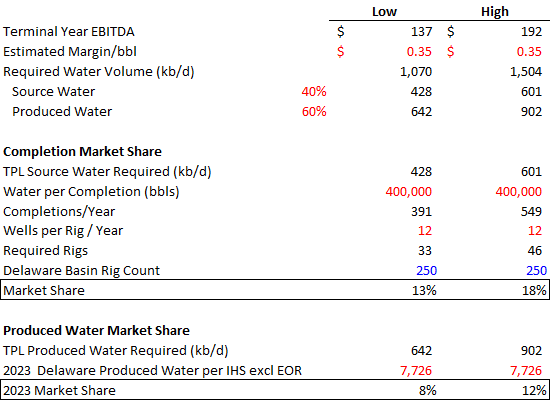

But how do we know that TPL will be able to invest that much capital efficiently? Maybe those terminal year EBITDAs and investment multiples are unreasonable. The table below lays out one example of how TPL’s water business could generate those EBITDA figures and the market share implications. Note that TPL does not provide any operating stats for its water business so we must make educated assumptions about volumes and unit economics. An assumed blended margin per bbl of water of 35c/bbl (higher for operated assets, lower for royalty bbls) implies 1.1mmb/d to 1.5mmb/d of water volume net to TPL. For illustration, lets split that volume 40/60 between the source water business (which I assume includes their recycling business) and the produced water business. We now have 428kb/d to 601kb/d of source water and 642kb/d to 902kb/d of produced water. Lets take the 428kb/d to 601kb/d of source water first. Assuming 400kbbls of water required per completion (per IHS and industry sources, that is the Delaware basin avg), that equates to 391 to 549 completions / year. At 12 completions per rig per year, that is 33 to 46 rigs. The Delaware rig count is ~250. That is a 13% to 18% source water market share which seem very reasonable when you look at a map of TPL’s water rights and historical produced water business EBITDA growth rate. The future 2023 market share will probably be even lower given that the Delaware rig count will almost certainly grow over that time period (increase production = increased cash flow = more rigs). With respect to the produced water side, the figures below imply a 8% to 12% market share of IHS’s 2023 forecasted Delaware basin produced water volume excluding EOR volumes.

One final note on the water business is recycling. Recycling is detrimental to the value of water rights, and we need to continue to monitor its adoption; however, I believe that significant fresh source water will continue to be required absent significant regulation against it (which in TX is not very likely). The source water business is driven by logistics. You need the right amount of water in the right place (right flow rate) at the right time. Having source water wells dotted across the Delaware sweet spot is going to be valuable in almost all future scenarios. Furthermore, the customer relationships built by TPL’s fresh source water business and produced water business will be an important advantage as they grow their exposure to the recycled water business.

Non Participating Royalty Interests

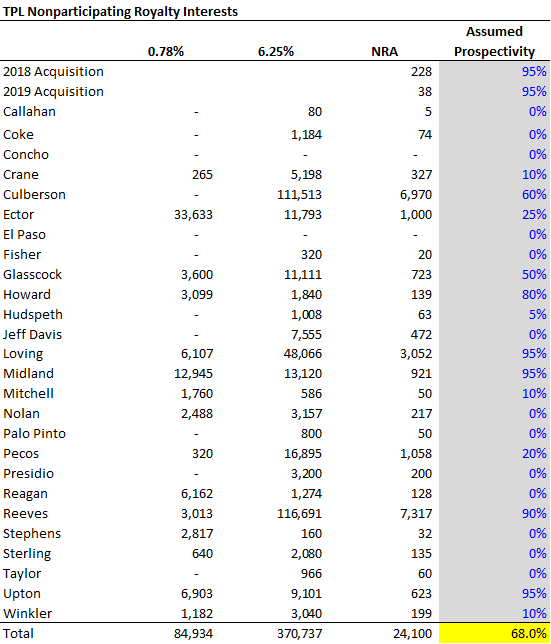

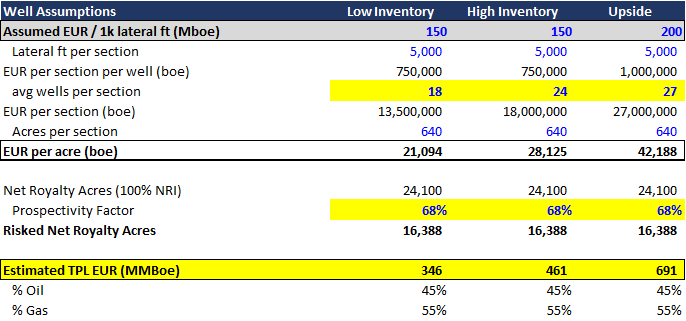

TPL owns a 1/128 royalty in ~84,934 acres and a 1/16 royalty in 370,737 acres. To get a more meaningful number I multiply the acres by the royalty fraction to get net royalty acres of 23,835 (100% NRI). In addition, TPL acquired ~228 NRA’s in 2018 and 38 NRA’s YTD in 2019 for a total of 24,100 NRAs at 3/31/19. Some of this acreage is in the core of the Permian Basin (mostly Delaware Basin). But not everything is prospective for oil and gas. Below I lay out my prospectivity assumptions that underpin the well inventory and EUR analysis discussed later. There is nothing magic here. I looked at the map and made a judgement.

It is worth noting that Chevron and Anadarko are the two largest operators underpinning the Trust’s royalty production accounting for 22% and 18%, respectively, of TPL’s royalty revenue in 2018. CVX recently laid out their ambitious long term plans for the Permian, and TPL shareholders will get to go along for the ride free of cost. I view the OXY/APC merger as neutral to negative to TPL. OXY is a very strong Permian operator and will have the pro forma scale required to underpin an efficient multi-well pad development program; however, the pro forma debt / preferred burden will slow down development if commodity prices do not cooperate by diverting cash away from the drillbit.

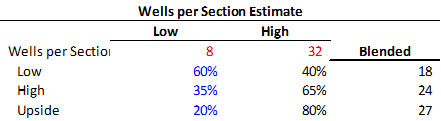

For the royalty interest valuation I made some assumptions around individual well EURs and average wells per drilling unit. I created three cases: Low, High, and Upside with 18, 24, and 27 wells per section, respectively. You can see in the tables below how I got to those numbers. On the high side a prospective drilling unit might have up to 32 wells across several benches and on the low side 8 wells. The different inventory cases assume different ratios of the two within TPL’s prospective acreage.

For the Low Inventory case and High Inventory case I assumed an EUR of 150Mboe/1k lateral ft. In the Upside case I increased that to 200Mboe/1k lateral ft. In the table below you can see the math to get to an estimated EUR for TPL’s royalty interests ranging from ~350MMBoe to almost 700MMBoe in the upside case.

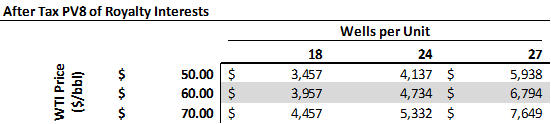

Using the above total EURs and individual well EURs I forecasted estimates for TPL’s oil and gas production from 2019 through 2058. I assumed 7.5% average production tax, 15% depletion shield, and a 21% corporate tax rate. I assumed a $4/bbl discount to WTI and 50c/MMcf premium for gas to account for the liquids value. The table below lays out the after tax PV8 of the different inventory cases and sensitizes WTI price ($2.75HHUB assumed for all).

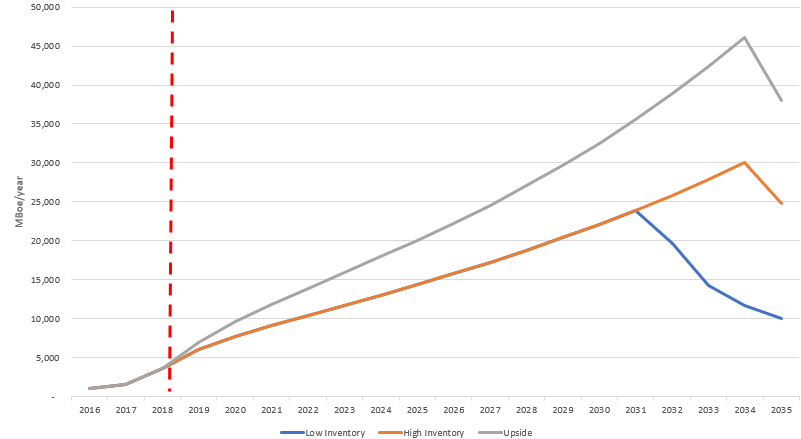

At $60/bbl WTI the value of the royalty interests ranges from $4.0bn to $6.8bn depending on the inventory and EUR assumption. It is worth emphasizing that I am forecasting significant production growth here. This is the bulk of TPL’s value, and if production growth starts to disappoint, that is a major red flag. The graph below lays out my modeled production growth (graph cuts off at 2035, but DCF runs through 2058).

Valuation

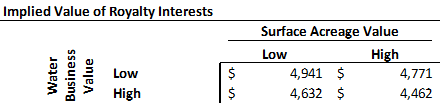

TPL’s current TEV is ~$6.0bn with no debt and $93mm of cash. The table below shows the implied value of the royalty interest based on the after tax high and low cases for the surface rights and the water business.

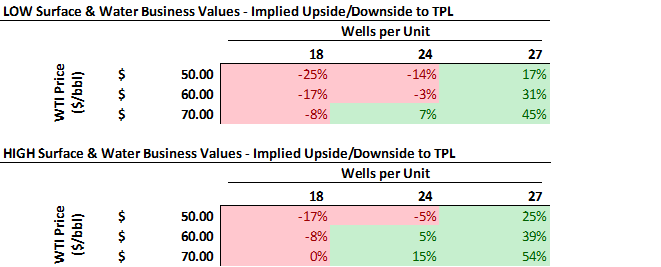

If we assume the Low case value for both the surface acreage and the water business then the royalty interest value implied by the current TEV is ~$4.94bn (top left quadrant above). Compared to the Low Inventory (18 wells per unit) $60 WTI royalty value of $4.0bn that implies ~17% downside to TPL. However, if we take the High case values for the surface acreage and water business (bottom right quadrant above), the implied royalty interest value is $4.46bn. Using the the Upside Case (27 wells) there would be 39% upside to the current TEV. The two tables below show the upside/downside to TPL under the different inventory cases and WTI price assumptions. The first table assumes the Low case value for both the water business and the surface acreage, and the second table assumes the High case for both the water business and the surface acreage.

You can argue about the right long term WTI price to use, but I am willing to bet on $60 WTI, despite being a little higher than the current strip. At that price the risk/reward ratio for TPL appears to be favorable at the current stock price, especially given the tendency for the acreage in its neighborhood of the Delaware to get better over time.

I would highlight that the water business and surface acreage combined after tax valuations account for 17% (low cases) to 25% (high cases) of TPL’s TEV. This is meaningful; however, the royalty interests account for the bulk of TPL’s value

Governance

There is a proxy fight going on right now between management and longtime holder Horizon Kinetics (“HK”) who owns ~23% of the stock. I am rooting for HK, and their presentation is worth a read. Even if HK loses, they have made themselves heard, and the mgmt candidate has committed to a 3 year term (trustees normally serve for life) which is a major win for shareholders. The TPL CEO, Tyler Glover, is young and has no experience running a multi billion dollar business. I would prefer someone with more experience allocating capital at the helm. Furthermore, maximizing TPL’s innate competitive advantages in the water business will take significant managerial skill. Fortunately, Tyler appears to be surrounding himself with experienced operators. Mismanagement is a real risk here given the lack of shareholder ability to effect change; however, the asset value is there.

Risks

-

Oil and Gas activity / commodity prices / long term oil demand destruction

-

The majority of value here is driven by a forecasted 5x - 10x increase in oil and gas production over the next 10 to 15 years. The rock is great, but this is a bet on commodity prices and the global economy’s continued reliance on oil.

-

The oil price risk is partially offset by latent long term upside in natural gas prices as there are significant natural gas reserves in this rock, and I am willing to bet we are at or near the floor for the domestic gas strip (famous last words).

-

Governance / management

-

We are forecasting significant growth in the water business. This will take skill to execute. So far so good, but this is a real risk despite the tailwinds.

-

The current proxy fight has been beneficial for shareholders no matter how it turns out, but at the end of the day, even if HK wins, a majority of the trustees will still be old guard, and shareholders have will still have little ability to effect change for the next 10+ years.

-

Significant cash flows will be generated over the next few decades. Current management has no history of allocating large $ amounts. My hope is that they stick to the stated purpose of the Trust, which is to return capital to shareholders. But there is no guarantee and recent actions are not encouraging.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

Continued significant oil and gas production growth

Continued capital efficient growth of the water business

| show sort by |