| 2017 | 2018 | ||||||

| Price: | 15.08 | EPS | 1.22 | 0 | |||

| Shares Out. (in M): | 251 | P/E | 12.3 | 0 | |||

| Market Cap (in $M): | 3,784 | P/FCF | 9.5 | 0 | |||

| Net Debt (in $M): | 528 | EBIT | 410 | 0 | |||

| TEV (in $M): | 4,311 | TEV/EBIT | 10.5 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- None found

- BETA

- B&M European Value Retail BME 12/06/2019

- FIVE BELOW INC FIVE 04/08/2020

- AO World PLC AO 01/03/2018

- Volution Group plc FAN.L 01/08/2019

- Howden-Joinery Group PLC HWDN 09/06/2017

- SLEEP NUMBER CORPORATION SNBR 08/21/2018

- BUILDERS FIRSTSOURCE BLDR 11/08/2017

- GROCERY OUTLET HLDNG CORP GO 09/28/2021

- Next NXT LN 03/22/2017

- Grocery Outlet Holding Corp GO 01/09/2023

Description

Company

Travis Perkins is the largest builder’s merchant in the UK with roughly ~25% market share. The Company is completely multi-format, with stores that serve the entire spectrum of consumers, including 1) the retailer – everyday joe schmo’s 2) the tradesmen - independent professional installers that buy regularly and generally have credit accounts and who maintain the with the joe schmo’s, and 3) big customers – homebuilders or government contracts.

Even though the end customers are extremely disparate, Travis believes serving all end users creates strong distribution synergies[1]. This allows the company to reduce the two main costs to a distributor –cost of goods sold through scale rebates, and cost of distribution through delivery densities.

Travis stocks >100k SKUs and has been revamping its logistics and digital sites to offer next day or 2 day delivery on the stock of commonly demanded items. The Company sells heavy-side (timber, cement, marble) as well as light-side products (tools, appliances). Travis operates 2,000 stores that cross a wide spectrum from smaller sized “Home Depot”-type outfits targeting the retail customer to more trade stores for the professionals.[2]

What is a Builders Merchant?

A builder’s merchant is a distributor of building , generally with minimal or no involvement in the manufacture of products. As such, they are in the business of logistics (and credit). A good builder’s merchant will have a combination of 1) quick delivery, 2) multiple access points for convenience, 3) diverse selection (ideally, a one stop shop), and 4) reasonable prices.

Customers for builder’s merchants are largely professional tradesmen and small to medium size contractors. Larger customers (i.e. national homebuilders) can be a customer of a merchant, but often can source directly from the manufacturer (or where a BM serves as a logistics intermediary)

Quick delivery and convenience – reflected through footprint - is important for tradesmen because professionals require quick turnarounds to make a living –a professional kitchen installer waiting 5-10 days to get the parts he needs for a job (countertop, marble top, cabinets, sink, etc.) can do many fewer jobs than one who can acquire parts 2 days out. In essence, a builder’s merchant tackles the complexities of buying from a fragmented and large supply base in order to deliver products cost effectively to local tradesman or DIY-ers.

Thesis:

We believe Travis Perkins is attractive today as 1) the Company is exposed predominantly to UK RMI (remodeling and maintenance) and therefore less correlated to the housing starts environment in the UK, 2) is exposed to an end market that is at 20+ year lows and which analysts are neutral towards (“waiting for sentiment to change”), 3) is the dominant player with density advantages in a consolidated (and consolidating) market where main competitors are closing stores, and 4) is available for ~11-12x P/E and P/FCF. While we don’t have a strong view on Brexit’s impact in the short term (and believe that the true impact may be felt closer to 2018 than 2017, a swap from sell side estimates), we think Travis is an above average quality business trading at low multiples of a market that appears more likely to be at a trough than a peak.

Valuation

Travis Perkins has historically traded at a low teens ROE since 2008 (was at high teens/20’s prior to that), despite a consistent decline in RMI spending as GDP for the past decade. The weak trading environment has forced TPK and competitors to restructure the business to maintain profitability - these changes should result in a structural improvement to returns when RMI spending recovers. The Company currently trades at 10x EV/EBITA and ~11.5x P/E. While our model suggests we can obtain a ~15+% IRR on sustained performance in the Company’s retail division (with no multiple expansion), we think the valuation is so undemanding that few assumptions need to be made to obtain a reasonable return. Assuming no improvement whatsoever in the business, the company is trading at a >8% yield. Current valuations assume a 12% ROE, 0% organic growth, and a 10% discount rate.

Why Now (Timing)?

As we head into Brexit, recent trends have show deceleration, and the numbers are being reflected amongst all the major merchants/home improvement companies. We think the timing could be interesting now as Travis noted the slowdown in late October, stating: “Against an uncertain market, it's very difficult for us to forecast precisely demand for building materials for 2017 at this stage. However, we believe our outturn for 2016 will be slightly below market consensus, which is around £415 million EBITA.” The street has EBITA estimates for the full year at £404, which implies 5% miss against original numbers. When pressed on the miss guidance, management responded: “the start point is, yes, a slight miss to consensus is from P&H really. I would say, it's only a very slight miss and, as John said, it does depend on the performance in the final quarter of the year, but we're going pretty well at the start of October, well, we did say that last year…. So, October has stepped up above the like-for-like performance in September – sorry, in July, August and September” Last year, the markets melted between November through February, a factor we don’t believe is happening this year according to our conversations. We think that Travis is likely to beat consensus given we believe >5% begins to get out of the “only a very slight miss” category. Furthermore, recent results from Howdens and Masonite (who does not see a noteworthy slowdown in the UK) seem supportive.

Going into 2017, estimates are for a -3% decline on 1% revenue growth, which indicates pricing pressures from foreign exchange. EBITA margins are estimated to compress from ~6.7% to 6.3%. However, given there is a ~6 month lag on pricing, management has said that the impact from price inflation won’t be felt until end of Q1, Q2. This implies a pretty steep margin drop-off in 2H’17 (~80bps simplified)[3]. We think, given the tone from competitors around passing of price through (and noting that TPK has the highest margins and so suffers the least from price fall through), estimates are skewed conservative and upside exists for the big 4 to find grounds for more rational pricing.

The Company

Travis Perkins plc (the Group) is the UK’s largest product supplier to the building, construction, and home improvement markets. LTM 6/30/16, the company achieved £6,112 million in revenue and £422 million in adjusted EBITA (6.9% adjusted margins). Adjusted FCF was £326 million (85% conversion from EBITA)

The Company originates back from 1797 and has been a story of “absorb” and grow, with a handful of large mergers over the past couple decades including Keyline Builders Merchants (101 branches), City Plumbing (CPS- 48 branches), Jayhard (53 branches), and Wickes (171 branches). Recently, growth has been strongest in the consumer side as TPK’s main retail competitors are retrenching. However, general merchanting is slowing down due to macroeconomic concerns, and plumbing has turned down significantly since Q2 as P&H suffered from industry-wide overinvestment from 2010-2014. Like all players, Travis has been “right sizing” its store base[4]. LFL for 2016 has progressed from +4.2% in Q1, to +2.3% in Q2, and +2.0% in Q3.[5]

Travis operates 2,000 trading outlets in the UK, compared to just under 1,000 by Saint Gobain (Jewson), and ~800 by Grafton (Others include SIG, Wolseley, and Howdens, though those only compete in single verticals). Wolesely operates just over 700 branches in the plumbing and heating segments. The Company broadly segments its business to the following:

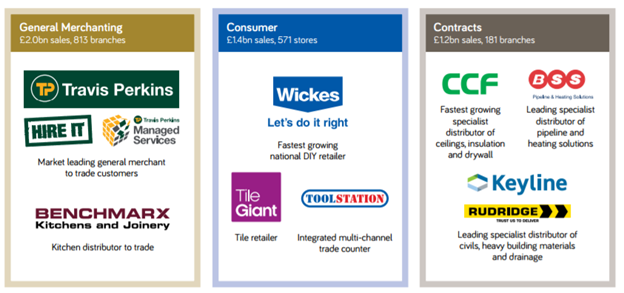

General merchanting (represents ~34% of revenues, £2.04 billion, and 49% of pre-corporate adjusted EBIT, £210 million. 10.3% margins) includes Travis Perkins (the namesake of the business), as well as Benchmarx, which focuses on kitchen fitting. This business rEven though Benchmarx stores are broken out as separate branches, they are generally “embedded” into an existing Travis Perkins, which optimizes stores that may be over-spaced. Benchmarx serves as general merchanting for kitchens, but also as a showroom for customers and builders.

A Travis Perkins store is generally structured around ~1.5 acres (plenty of open space for hard assets) and offers 100k SKUs to professionals and self-builders.

In Consumer (represents ~24% of revenues, £1.46 billion, and 23% of pre-corporate adjusted EBIT, £97 million. 6.7% margins) Travis operates largely across 2 platforms, Wickes (which competes against B&Q and Home Base, similar to Home Depot / Lowe’s format), and Toolstation (a much smaller version). Wickes stores are much smaller than competitors who are over-spaced and currently downsizing. Stores run around 25,000 sq ft vs. competitors at 60,000-75,000 sq ft. They are also generally located in grade B retail locations and commercial locations, versus prime real estate often occupied by the likes of B&Q (Kingfisher). Toolstation is the ultimate “small store format” with stores that are 4,000 sqft and which carry a small order of SKUs. Biggest competitor is Kingfisher’s Screwfix, which is a 6,000 sqft model that otherwise operates similarly. In 2015, 20% of sales from Toolstation were done online[6]. This small format is designed to cater to the evolving “right now” and “next day delivery” requirements.

Plumbing and heating (represents ~23% of revenues, £1.38 billion, and 10% of pre-corporate adjusted EBIT, £43 million. 3.1% margins) revolve around supplies involving the “pipes” of a home, largely supplying pipes, boilers, bathroom oriented goods. This is not a great segment as there is generally less differentiation in bathrooms[7]. This is because bathrooms typically have “white space” which means that the individual components of a bathroom are generally disconnected – the toilet is separate from the bathtub is separate from the sink/vanity counter, etc. On the other hand, a kitchen is intertwined and if you get a cabinet measurement wrong, it can create significant re-work/delays. As such, there is much more DIY in bathrooms over areas like kitchens. Furthermore, the heating segment is unlikely to turn around for a long time due to overcapacity issues. 95% of the profit of the segment comes from the ~50% of revenues tied to plumbing, implying roughly 6% margins for bathrooms and 0% for heating.

Contract businesses (represents ~20% of revenues, £1.23 billion, and 19% of pre-corporate adjusted EBIT, £81 million. 6.6% margins) – This business also sells pipes, ceilings, insulations, and heavy building materials, but typically to big developers in large construction projects like rail infrastructure or power generation. Margins here are lower than traditional trade as there is less value-add in this segment (and lower then consumer once consumer “matures” its store base)

Industry[8]

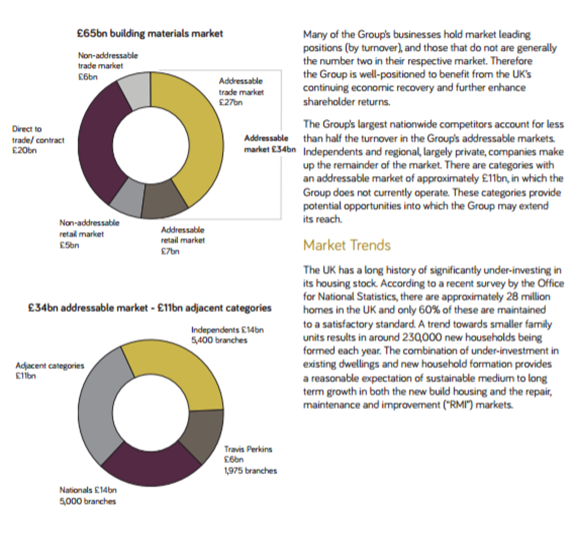

The total UK construction and home improvement materials market is worth approximately £70bn. The Group’s addressable market is around £37bn, which excludes certain trade and DIY categories and direct from manufacturer to end-user supplies, which are not currently served by the Group’s businesses.

TPK believes that the nationwide competitors have less than half the market, with the remainder dominated by independents and some strong regionals like MPK. Cannacord Genuity defines the builders merchant market as a smaller £12bn market, where Travis has ~23% market share[9]. Either way, the market is consolidated among the top 4 players, but is still significantly fragmented with mom and pop shops holding on to strong established relationships. The trend towards slow obsolescence of mom and pop shops reminds us of the trend in auto parts suppliers in the U.S.

The majority of TPK’s businesses distribute building materials to repair, maintain and improve existing homes and commercial, industrial and public buildings (70%). The remainder is tied to housing growth. UK population growth trends, immigration and smaller family units continue to create demand for housing, with the formation of around 225,000 new households per year. In 2015, around 160,000 new homes were built. This shortfall in supply, combined with historic underinvestment in the existing 28 million dwellings in the UK means the Group expects continued growth in both new house building and, importantly, in the repair, maintenance and improvement (RMI) market.

Thesis Points 1+2: RMI Correlation, and RMI Spending at Troughs

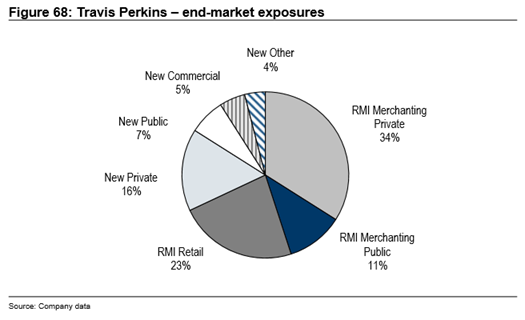

For TPK, ~70% of business tied is tied to RMI, with much lower reliance on new housing starts:

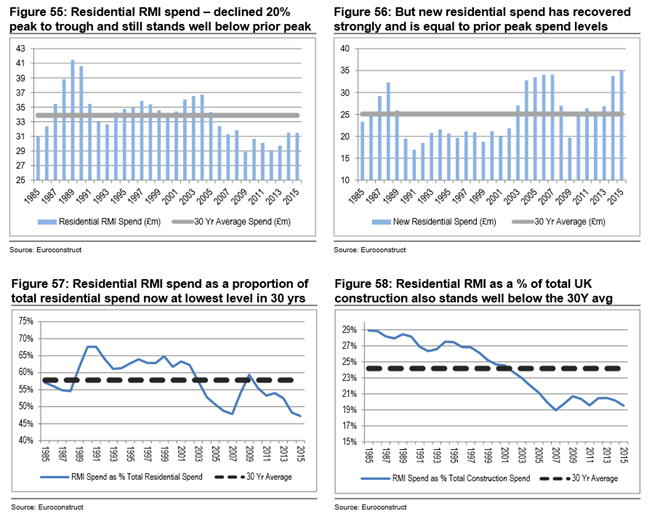

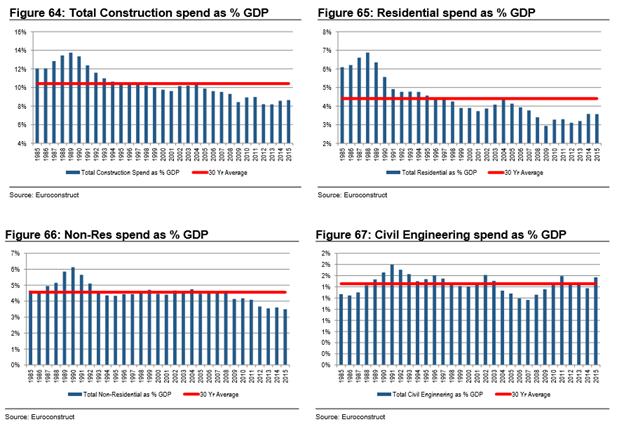

Residential RMI spend declined by ~20% from its peak in 2004 to the trough in 2012 and is currently 12% below the prior 2004 peak. This compares with new residential spend, which, although it declined materially during the housing crisis, has now grown such that it is broadly in line with prior peak spend. However, plenty of literature out there exists about the supply/demand imbalance of housing in the UK, and we believe TPK’s 30% exposure to new construction is more likely than not to benefit from the UK new construction market given a 5-10 year view.

From CS: “RMI Spend decoupling: over the past 30 years the RMI segment has accounted for c 58% of total residential spend (total = new build + RMI). However, in recent years it has trended well below that long-term average such that in 2015 it stood at 48%, the lowest level of the past 30 years. Residential RMI spend as a proportion of total UK construction spend has decoupled to the downside such that it now accounts for 19% of total spend, compared with the 30-year average of c 24%”

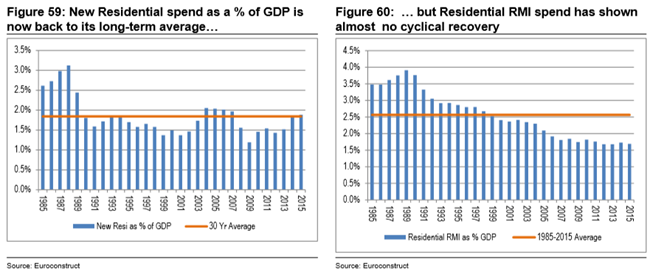

RMI also declining as a share of UK GDP: the share of spend in new residential as a proportion of UK GDP is back to longer term averages, but residential RMI stands at 1.7-1.8%, below the historical average of just above 2.5% of GDP:[10]

CS believes that RMI spending will begin to pick up as UK home equity moved back into the black in 2015: “Equity dynamic across the UK, suggesting that in the next year a material share of owner occupiers will start to experience positive Home Equity for the first time in this cycle. We believe that in turn this will be a material driver of RMI spend in the coming year….” The thesis revolves around the fact that most homes in the UK (on average, some areas like London aside) broke into positive home equity in 2015, and most owners are more likely to spend money on non-essential remodeling when they have positive equity rather than not. While this view is somewhat tempered by uncertainties related to Brexit, unless real estate prices begin to turn downwards, the tailwind from positive equity should continue to be supportive of a “trough” in RMI spending that has occurred since the Great Recession.

Our view is the same as the experts we talked to, which is generally summarized: “RMI will come back at some point, but I don’t know when.” One participant (who is now involved in modular housing) talked about the supply demand imbalance being roughly 80k+ homes a year (225k required, ~145k build rate). There is increased interest in modular housing as it increases the opportunity to transform existing large homes into separate, smaller modular homes (i.e. taking a 3 story house and converting it to 3 single floor homes), which will drive increased RMI spending in installing the necessary plumbing, kitchens, etc.

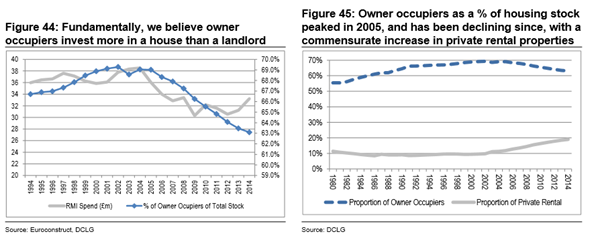

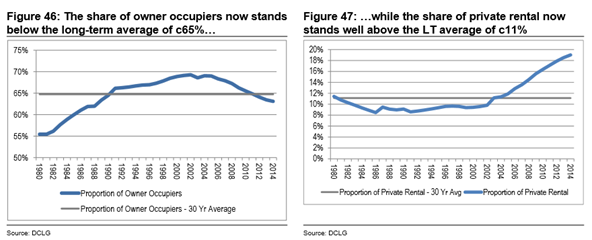

Ultimately, RMI spending is far below long term averages, housing is in short supply, and home ownership has dipped below long term averages. While this could all continue to worsen in the short term, we believe there is a decent chance that these changes are not structural, and will return to long term levels over time.

Thesis Point 2: Economies of Scale [11]

The big 4 have bargaining power over independents that give them 1-2% of benefit (independents and regionals can typically participate in buying groups), hence the permanent margin advantage that should allow the big players to earn higher returns on capital. Our conversations suggest that the big 4 distributors most likely receive similar pricing concessions from their supplier base. Hence, the migration of market share from independents to the big distributors will continue over the long term given the marginal advantage on gross margin (the migration is structural), combined with efficiencies related to sales, marketing, and distribution on the bottom line. As such, independents compete on price and set the floor on pricing. The big 4 generally compete on quality of service – where product availability and ease of procuring any product within a minimal amount of time is the key differentiator. In general, the big 4 distributors have the comfort of a dual advantage both on pricing and on cost.

Our conversations with competitors suggest that Travis Perkins is “world class” because it has an advanced internal IT system which allows it to distribute products and react to market demand much faster and efficiently. To quote: “I can’t emphasize enough how a quick decisive IT system is key to run the business. What appears to be a simple business operating model is very complex. Let me expand on that, in a builder’s merchant operation you buy an item from a supplier, the supplier gives it to you at your branch, and you sell it. The complexity is that branches are allowed to trade with customers and so there is not a “set price” for each customer; so there is a whole bunch of complexity. Without having a good reliable flexible responsive system across the system is critical. TPK always able to steal the march from Jewson, without a shadow of a doubt. They are a first class business there are no 2 doubts about it.” Jewson’s IT system, while lacking in comparison to TPK, to our understanding is more advanced than Wolseley (i.e. ability to tell which store/customer was responsible for a 10bps decline in margins on a particular day). The complexity of an internal IT system to our understanding allows for efficient high density from servicing which is not easily replicable from mom and pop shops and from competitors without strong insight into individual customer profitability. It is our understanding that culture is also very important, particularly in context of Jewson being <10% of revenues of a huge French conglomerate where the culture is more controlling/overarching (“approval process is monolithic”).[12]

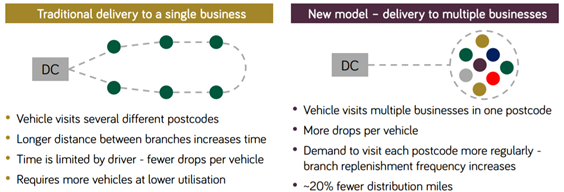

Per Travis, the ability to co-habitat industrial parks, along with proximity of tradesmen offerings to consumer retail, allows for reduced branch replacement and stock handling time. Travis states that inter-branch transfers are reduced by 40% and that the density reduces miles traveled by 20%. From an inventory perspective, Travis has slightly lower stock days than Woseley, Howden’s, and Grafton, which may speak to the efficiencies of inter-branch handling. In aggregate, Travis has a massive working capital days advantage – 14 days vs. 48 at Grafton, 39 at SIG (Jewson), and 35 at Wolseley

It is difficult to assess the costs related to distribution efficiencies, but in general, Travis has spent around 24% of revenues in selling, distribution and administrative expenses, while Grafton spends 26-27%, and SIG spends 24-25%. In general, we believe Grafton is a closer comparable given that SIG distributes largely insulation (which is depicted by a gross margin of 27% vs 30% at Travis). As such, the numbers seem to give credence to Travis’ lower distribution cost. Logically, sharing industrial parks reduces the fixed costs of the site and is a core synergy across multiple brands. The co-location also drives increased traffic as it creates a stronger “customer destination” than single stand-alone entities:

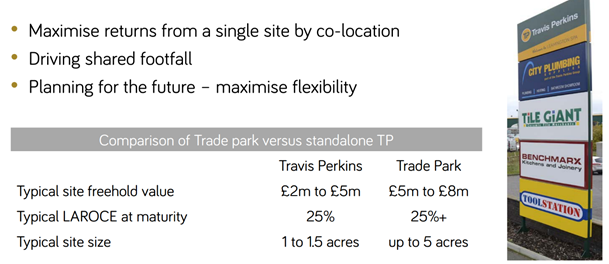

Thesis Point 2B: Structural Advantage in Consumer Also

While it was somewhat surprising for Travis to enter the retail space, the strategy has been working very well as the recent weakness in RMI/Brexit fears has caused TPK’s main retail competitors to rationalize their footprint. Particularly, B&Q has been closing ~15% of its store base and will likely continue to close more stores given the trend towards downsizing real estate space. Wickes has been a clear beneficiary of this trend:

While Kingfisher has plans to massively reduce its supplier base to reduce costs (which will undoubtedly create pricing pressure if successful), TPK believes it is structurally better positioned to compete because of the base real estate footprint. Wickes pays generally 15-18 / sqft for their boxes which are less than half the size of B&Q, while Kingfisher pays 20-30. As more and more purchasing moves online, B&Q must continue to downsize its increasingly burdensome fixed-cost footprint. We think this is a trend that will be benefitting Travis at least for the short/medium term (the lower SKU, low cost profile vs. huge many SKU boxes reminds us of Aldi/Lidl vs Tesco).

Furthermore, TPK is somewhat skeptical about Kingfisher’s ability to reduce its supplier base across continental Europe given the very different preferences/styles even across the UK (North vs South). We will be able to observe B&Q’s success as they move beyond their trial period into consolidating more SKUs beginning this year.

Thesis Point 3: Long Term Investments to Increase the Moat

The barriers to entry in a distribution business are readily understandable, but the barriers are also only modestly powerful and can erode over time if technology by competitors chip away at the margin differential by reducing waste or improving efficiencies beyond what is achieved at TPK. What is impressive about Travis Perkins is how very long-term the Company plans, and we believe that operational delta against competitors will persist or even expand over time.

From former employees of competitors, we often hear about the world class IT system TPK has. Even in consumer, which has a separate standalone distribution, Wickes has best in class ERP system that allows the company to do same day delivery, click and collect, assign hour slots, which are still unavailable at B&O and Homebase. The Company has been trialing delivery slots so that they can get products to trade professionals in an 1 hour time slot (generally this is for time sensitive products where the cost of delivery exceeds that of the product). TPK is taking the system from Wickes and upgrading their merchant infrastructure to be able to replicate Wickes’ ERP at Travis Perkins[14]. Our understanding from management and from competitors is that a lot of this infrastructure is very old, requiring up to 80 tabs to put in an order, whereas new implementations would reduce that to 2, 3 clicks.

Grafton has criticized TPK saying that this same day delivery/hour slot system is “solving a problem that does not exist.” However, while TPK believes this may be true today, they are aware that many trades professionals are in their 50’s and 60’s and have much different shopping habits than their sons/daughters who will take over the trade at a future point in time. They are investing heavily today to create buying habits (and also create scale) among the next generation of professionals who will take over in the next decade. Competitors who are not investing now will likely find it more expensive to change buying behavior and create necessary scale at a later point in time.

Thesis Point 4: Valuation & Growth

TPK believes it still has significantly more room to grow, particularly as it hasn’t achieved national scale (except contract). While we think there might be room for another 15-20% more stores over the next 5+ years, the more interesting growth tailwind is the ~50% of the market still owned by independents. “local independents are our key competitors today…they will never be able to invest in digital, distribution centers, market share… what keeps customers away from TP is the relationships. Kids [of the trades professional and mom & pop] go to school together; they go to pubs together…the only way you pull those customers away is a substantial service that is different from your local independent.”[15] [16]

The Company’s own model contemplates 2-3% market volume growth, 0-2% inflation, 1-2% market share capture, and 1-2% new space growth. If this is achieved, the company will have organic growth of 4%-9% and bottom line growth in the mid single to low double digit growth. Given the current valuation of the business at 8% FCF yield, there is very little if any credit given to the normalized growth of the business model and seems valued for no growth.

While we don’t have an “exit” multiple in mind, for a business earning 11-12% ROIC given the current conditions in RMI with reinvestment opportunities consuming ~60% of OCF, long term runway to consume mom & pop businesses, and “world class” operations against market peers, we think the current multiple of ~10.5x EBITA is too low. Assuming no improvement in ROIC, roughly 50% reinvestment, and 3% organic growth long term, we think the business is worth 12-13x EBITA.

Risks:

Pricing Obscurity: There is a substantial amount of obscurity in professional pricing. Each tradesman has a separate account with TPK or HWDN and they are quoted prices separately, which they can choose to reveal to end consumers or keep hidden. I have read many stories of UK consumers getting massively different price quotes from different Howdens shops. I am not sure if Benchmarx operates the same way, but this could lead to lack of confidence in consumers getting the best or fair deal. If there is a move towards complete transparent pricing, margins in the industry could potentially migrate down

Gross margins Pressure: there hasn’t been inflation in the market in a very long time. Companies have been able to pass it on with varying degrees of success. What would happen is that a price increase would go through, but it would stick only for a week or two because by nature of the industry, people are allowed to trade and negotiate pricing, so the price increase would get traded away. Hence, in the short term, margins might compress if commodity prices begin to climb up. Our conversations suggest that a 3% price increase, you might make 1% of that back through increased prices to the end consumer. The rest would need to be protected through increased claims and rebates, reducing supplier count, etc.

o Q3’16: “The gross margin question, Charlie, is always complicated, especially when you're on a Q3 trading update. All of our businesses are operating in different segments of the market, and we adopt a trading stance to give us the best earnings and returns from those. We feel just at the moment, given the headwinds of what could be coming through on price inflation, that at the moment for TP, we're just adjusting that trading stance slightly. And I would stress slightly in terms of gross margins that we're aiming to at least hold or improve a little bit where we can. We're working really hard with our suppliers to mitigate and find ways around those increases using our supply chain and Range Centres and [ph] P&Hs in different ways. We're looking at some of the traditional purchases from the Far East of bringing them back into the UK”

o DB: “As cost inflation picks up into next year, a key question is whether this will be passed on in pricing or margins will be squeezed. On TPK’s highest margin General Merchanting division, the group said it intended to at least maintain but hopefully improve its gross margin, although this is unlikely to be the case in Consumer and Contracts where market share appears a bigger priority. However, the group kept emphasising potential ways to mitigate input cost inflation (e.g. more direct sourcing, shifting to domestic suppliers where possible) but also a reduction in operating costs (closure of 30 underperforming branches announced).

o See below quotes from competitors addressing margin pressures

Brexit Impact: While we believe the long term thesis around RMI should prevail, we acknowledge that timing is difficult given the lags in sentiment. While 2016 seems to shaping up roughly in line with expectations with a weaker 2H vs 1H, we think the general sentiment that 2018 will rebound back may be at risk given the ~12 month or so delay that consumer confidence generally takes to reset purchasing expectations.

Competition/Amazon: While we don’t think amazon is likely to be a big competitor in the short run, they can definitely move into light-side products given their immense distribution in the UK. We think this is probably lower on their priority list, particularly given the density / heavy-side offering key competitors already have in this market. However, it is something to watch longer term.

Main competitors:

· Retail side: B&Q (Kingfisher), Homebase (Bunnings)

· Trade side: Howdens (Kitchen), Woseley (Plumbing), Jewson (General), Grafton (General), SIG (insulation)

· P&H side: Woseley (Plumbing)

· Grafton: #3 player in builders merchant in UK and #4 plumbers merchant. Operates 668 branches as end of 2015, with 2.2 billion in revenue and 127 million in adjusted EBIT. Brands consist of Selco, Buildbase, Plumbase, Chadwicks, and a few other smaller concepts. Also has a small retailing operation in Ireland called Woodies. Grafton has 518 merchanting locations in the UK.

· Wolesely is a big player with 15.2 billion in revenue in 2016. However, over 70% of that is derived in North America (Ferguson), and only ~15% in the UK through its Plumb Center and Parts Center branches. The company has been restructuring its UK business as there has been immense overinvestment in plumbing/heating due to government policies that pulled forward installation of boilers in homes over the past years.[17] As boilers tend to last ~20 years, the pull forward of demand is now falling and requiring players across the board to right-size their investments. Wolesely has closed 22 branches already, and is in the process of combining the two brands into one (737 end of 2016, 2 billion turnover, 3.7% margins).

o #1 player in plumbing and heating, #2 in pipes and climates (pipes and valves to non-residential construction)

· SIG: Generated 1.4 billion in revenue from 325 branches in the UK and Ireland. Business is just over half UK, and half mainland Europe in Germany, France, Benelux, and Poland. In UK, #1 technical insulation, structural insulation, interiors, and specialized exteriors. SIG is less concentrated on the traditional tradesmen – roughly half the business is residential and the other half is non-residential and industrial.

o Gross margins in 2015 was 26.6%

o Underlying profit margin was 4.3%

o LFL in UK was 0.8%

· Saint Gobain: Owns the Jewson brand. Saint Gobain has 996 branches in the UK (Jewson and Graham). UK is 10% of Saint Gobain’s sales, which amounted to 28.8 billion GBP (so around 2.9 billion GBP in UK), slightly bigger than Grafton. There is little information with regards to this business since Saint Gobain is a large global heavy-side business and does not disclose segment data

Quotes from Recent Competitor reports:

Kingfisher: UK & IRELAND

• Total sales +2.5%. LFL +5.8% reflecting continued strong Screwfix performance and solid B&Q performance o B&Q UK & Ireland sales -3.6% reflecting store closure programme which is now nearly complete (7 in Q3; 59 to date of 65 planned).

· LFL +3.5% including c.2% benefit from sales transference associated with store closures.

· LFL of seasonal +5.3%. LFL of non-seasonal, including showroom +3.1%. Screwfix sales up +23.1% (LFL +12.7%) driven by its leading digital capability, new and extended ranges and 11 new outlets

· “If we start with this space rationalization program, well, it's well advanced. Just as a reminder, 15% of space equated to 65 stores to be closed. And that program is now 80% complete. We've got 52 stores closed to-date. We did 30 last year, and they were mostly backend loaded. And we've done 22 closures in the first half of this year. That leaves us 13 stores to close in the remainder of the year.

· We've got 50 exits secured to-date, so different from the closure. That's actually terminating our lease liability one way or another. And at the end of last year, we had completed 40 exits. We've now increased that by 10. You may remember that in quarter one, we announced that we were actually outsourcing the remainder of this activity”

Wolesely:

· “In the UK, revenue was 2.9% lower like-for-like. RMI markets, which is where we get the most of our sales, have stayed pretty weak. As you know, we'd worked hard over a considerable period of time now to try and improve the gross margins in the business, which we did this time in highly competitive market conditions. It was great to see gross margin actually ahead in the quarter. So, trading profit was £2 million behind last year.

· “Just touching on restructuring actions. The turnaround in restructuring plan in the UK, that is proceeding well. We are very pleased with the progress on that. We've made some very strong appointments. We're working through the first phase of 22 branch closures all subject to consultation. But we're also making very good progress, for example, with the customer side, the RMI side and also on the supply chain solution side.”

· “ Yeah. Yes. I mean, the UK market absolutely remains very competitive, but pricing is something that we have to set. The same rules really apply, too, in Ferguson, which is if we're delivering a great service and that service is differentiated, and we do think we are making great progress in doing that in the UK. Our Net Promoter Score has continued to move forward. We're very pleased with that. We have to make sure that we recover that service in our price, and that's really where it's coming from. It's less so, I'm afraid, in the UK for mix. There is a little bit for mix, but I think, predominantly, in the UK, this is coming from more disciplined pricing.

· “With respect to passing price increase on, we've still got a lot of domestic purchases in the UK. As the majority of our purchases are domestic, we do this particularly in Soak, which is our B2C channel in the UK. That is all priced in U.S. dollars. And those input price increases will have to be passed on because we will have to do that and the competition will have to do that as well… So, will we recover at all? I don't know at the moment, but we will certainly expect, A, to give that to our vendors and make sure that they're not being predatory, if that's the right word, in setting their prices; and, B, making sure that we recover them appropriately because otherwise the relative benefit of imported products will reduce and we'll have to source more products in the UK, which should be fine.”

Bunnings:

· Sales for the first quarter4 were in line with expectations at £320 million ($554 million). The first quarter marked the fifth, sixth and seventh months of ownership of the Homebase business and trading continued to be steady. There is a strong focus within the business on continuing to transition core ranges across to home improvement and garden products. Pleasing progress is being made with this work. Mr Gillam said the implementation of new pricing, marketing and operational strategies within Homebase is achieving results in line with plans. On a like-for-like trading basis across the first quarter, customer participation, as measured by transactions, increased by 8.4 per cent. “Good progress is also being made across all elements of the acquisition agenda,” Mr Gillam said.

· Closed 2 centers

· Bunnings UK essentially at zero profitability today

SIG:

· Thank you, Leslie. Good morning, everyone. You will no doubt have read the statement we released this morning, so I'll keep this brief. Following a slowing of activity around the time of the EU Referendum, trading conditions in the UK have continued to soften and competition has intensified. In particular, we've been impacted by delays to some projects in the commercial sector, and seen subdued demand for technical insulation. The UK RMI market also remains challenging.

· Furthermore, our offsite construction business has been temporarily affected by the commissioning of new machinery, which has taken longer than originally anticipated. This has led to the deferral of some projects into 2017. As a result, like-for-like sales in the UK and Ireland declined by 1.1% in the July to October period. In response to these challenging conditions, we've accelerated our supply chain and procurement programs and undertaken a further review of our UK branch network and cost structure. This will provide us with annualized net savings of approximately £10 million and are in addition to the previously disclosed targets. So, we're now targeting at least £20 million of savings in 2017.

· In terms of improving trends into October, we're not seeing that, quite frankly. If that's what our peers are seeing, we're not seeing that. We've had a very disappointing October both in terms of the sales development and also gross margin development. So, October was, as I say, a very disappointing month for us.

Grafton:

· Reported 1.2% LFL growth in merchant from July through October in UK, down from 3.3% in the first half.

· “After an encouraging start in Q1, market conditions in the UK merchanting business grew progressively more challenging in Q2”[18]

Appendix:

1. Construction as % of GDP:

2. RMI Growth vs US Home equity

[1] Company states ~20% lower distribution costs than peers

[2] See company description for images

[3] 40% of products are sourced overseas, or 28% of revenues. 5% price increase will result in COGs inflating 1.4% if there is no price pass through (or .70% if for half year). Our conversations suggest around 25% of cost can be passed through quickly, and a portion of the remaining 75% can be reduced through sourcing/supplier power negotiations.

[4] In 2013/2014, the UK government gave huge incentives that basically covered efficient boiler upgrades. Boilers, which can last 20 years, were all retired early given that it was almost free to do so. This pulled forward massive demand, but which now has “reset” the replacement cycle

[5] One of the many reasons the entire sector has sold off

[6] https://www.retail-week.com/stores/property/travis-perkins-takes-on-screwfix-as-it-eyes-100-further-toolstation-stores/5077739.article

[7] Quote from management: “I think, it's a great question regarding kitchens versus bathrooms. But the route to market is very different and the category is extremely different. We're enjoying good growth in kitchens both through Wickes and through Benchmarx. We've worked really hard on our supply chain, and we've undertaken a project in the last 12 months to improve our bathroom performance as well. I think where you'll have a more narrow supply base in kitchens you have a very wide supply base in bathrooms. And it has attracted a lot of attention online as well…. But in my mind, kitchens are easier for customers or businesses to access the range. It's easy to buy online. There are fewer products in it. And the cost of delivery of bathrooms is not dissimilar from the cost of delivery of kitchens and unfortunately, kitchen is often 3, 4 times the value of a bathroom delivery“

[8] 2015 annual report

[9] Canaccord Genuity December 2015

[10] Credit Suisse

[11] Travis Perkins investor presentation

[12] This remark from a former employee fits TPK’s description that St. Gobain hasn’t been investing in Jewson for the last 3-5 years.

[13] http://www.travisperkinsplc.co.uk/~/media/Files/T/Travis-Perkins/reports-and-presentations/property-investor-event-presentation.pdf

[14] Part of a 5 year upgrade

[15] TPK IR

[16] Our conversations also indicate how heavily intensive relationships matter in this industry, hence the need to disrupt buying patterns at a generational change level.

[17] This initiative started in 2010-2014 as an eco-friendly scheme. Government gave very good/free incentives for homes to change their boilers to more energy efficient ones. 7 years after the beginning of the scheme, capacity continues to be too high. Bathroom vs heaters are 50/50 in revenue, but 95/5 in profitability

[18] http://www.graftonplc.com/~/media/Files/G/Grafton/result-centre/2016/2016-half-year-results-presentation.pdf. Company still still set to open 9 more Selco stores (to 51 by June ’17)

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

Time

| show sort by |