| 2022 | 2023 | ||||||

| Price: | 15.64 | EPS | NA | NA | |||

| Shares Out. (in M): | 18 | P/E | NA | NA | |||

| Market Cap (in $M): | 288 | P/FCF | NA | NA | |||

| Net Debt (in $M): | -28 | EBIT | 0 | 0 | |||

| TEV (in $M): | 260 | TEV/EBIT | NA | NA | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- None found

- BETA

- ADT INC ADT 09/15/2022

- PICO HOLDINGS INC PICO 05/11/2013

- LINCOLN ELECTRIC HLDGS INC LECO S 10/02/2022

- PICO HOLDINGS INC PICO 01/13/2011

- PICO HOLDINGS INC PICO 02/04/2014

- LAYNE CHRISTENSEN CO LAYN 08/18/2015

- D.R. Horton DHI 03/31/2023

- TEXAS PACIFIC LAND TRUST TPL 05/09/2019

- Walter Industries WLT 12/19/2005

- PICO HOLDINGS INC PICO 05/05/2015

Description

|

From: |

|

|

Date: |

May 2022 |

|

Subject: |

STRATEGY – BUY Vidler Water Resources (NYSE:VWTR) BELOW $16.00 |

Summary

On April 13, 2022, Vidler Water Resources, Inc. (Nasdaq:VWTR, "Vidler" or the "Company") and D.R. Horton, Inc. (NYSE:DHI), the U.S.' largest homebuilder, announced that the two companies entered into an all-cash merger agreement to which D.R. Horton would acquire Vidler for $15.75 per share (the "Offer"), representing a 19% premium to the 90-day volume-weighted average share price and a 39% premium to Vidler's book value of equity. We believe it is a terrible buyout for VWTR shareholders and an excellent outcome for DR Horton if the deal is consummated.

We recommend reading AltaRocks' write-up on Vidler's (fka PICO Holdings, Inc.) historical and asset basics [here]. We were initially planning our memo to update AltaRock since not much had changed since. In the last year, management has given the market extensive insight into the valuation of its assets. We had finished doing a complete asset analysis on Vidler's underlying properties and were preparing to post our findings and views on VIC just as the merger was announced. We decided to wait and observe what unfolded. In light of the most recent [14D-9], we believe the assets are worth far more than shareholders will be receiving.

Interestingly, no new bids have come out to challenge. The Company's many failed attempts to sell itself since its business/management restructuring in 2016 suggest the drought in proposals. In fact, according to the 14D, an "exhaustive" sell-side approach was followed. Nevertheless, we estimate the value of the stock to be at least 50 percent undervalued at $15.75. Our analysis suggests a fair market value of closer to $30-$40 per share, and DHI offering anything less than $25.00 per share should not be accepted by shareholders. We would be surprised if many shareholders tender at these prices. The deal price is now below where the stock was trading before the deal was even announced.

Our analysis is not far off from management’s projections. However, several questions arise: (i) what is the right discount rate; (ii) what amount of unpermitted and additional water rights exist from legal challenges; (iii) Fish Springs infrastructure value is hard to pin down (investments needed, third-party use, etc.); (iv) where are other assets (e.g., solar leases, grazing rights, etc.); (v) interest and mortgage rates are rising, but Reno’s growth (and in other VWTR areas) could be unaffected, while DHI’s investor calls suggest positive development growth over the next two years in these key areas which suggest water right monetization; lastly, (vi) it is unclear why the deal is not structured for VWTR to sell the assets to DHI and fully utilize the NOLs, then issue a dividend.

We were buyers of the stock at $12, and we are still buyers at $15.75. We believe it should get interesting as shareholders in the market realize the loss in value D.R. Horton is offering for these unique assets as the tender offer will either succeed or fail in the next week. We will try to keep this memo brief, given the deal’s timing.

Note: This idea is not for those untrained in mergers speculation, but there is enough evidence to show why it might make sense for long-term value investors to participate in purchasing the stock and NOT tendering their shares for the current offer on the table. Our original memo can be found HERE.

SITUATION UPDATE

Brief Company History

In 1996, the Company was formed as PICO Holdings, Inc., through the reverse merger of two insurance company investment arms and their attempt to recreate a Berkshire Hathaway investment model. By 2015, the project had failed, and investors soured on the Company’s poor investment acumen and operating stewardship, all while management compensation increased and the stock price decreased (see Exhibit 1). In 2016, a shareholder battle (led by today’s largest shareholders: Amundi Asset Management, Bandera Partners, and First Foundation Advisors) cleaned up the board and put in place a liquidation of the business. With only the water rights business left, in 2021, the Company changed its name to Vidler Water Resources, Inc. During the restructuring, due to the peculiar nature of the water assets and the size of their value, the board appointed and kept long-time PICO employees Dorothy A. Timian-Palmer (CEO) and Maxim C.W. Webb as senior management (Executive Chairman and CFO) to oversee the Company’s run-off efforts. The former and latter receive ~$600k and $500k per year in annual cash compensation. Senior management does not have significant control of the shares (see Exhibit 2) but would be compensated with ~$1.5 million for Ms. Timian-Palmer and ~$2.5 million for Mr. Webb if the DHI deal is completed.

|

Exhibit 1: VWTR Price / Volume |

Exhibit 2: Ownership Summary |

|

|

|

|

|

|

Source: Company Filings, RWR Estimates |

Source: Company Filings, RWR Estimates |

DHI Transaction Background

Vidler provides sustainable potable water resources to fast-growing communities that are lack or are running short of available water resources. It monetizes and further develops existing water rights, water storage credits, and alternative energy sites it owns in Arizona, Colorado, Nevada, and New Mexico (see Exhibit 3). A water right is the legal right to divert water and put it to beneficial use. Water rights are real property rights that can be bought and sold and are commonly measured in acre-feet ("AF"), which is a measure of the volume of water required to cover an area of one acre to a depth of one foot and is equal to 325,850 gallons (1.2 million liters) of water. Almost all of the Company's inventory of water rights are groundwater rights (i.e., water pumped from underground aquifers or basins) located in and governed by the state of Nevada.

|

Exhibit 3: Vidler Current Water Right Projects Summary |

|

|

Source: Company Filings 2Q 2021. |

Theoretically, water rights assets should not exist, but for the strange fact that the Southwest is an interesting fusion of rapid expansion, special political business incentives (tax, etc.), and a highly arid climate with high population growth demanding water needs. This should suggest that water rights pricing should not be as sensitive to broader market conditions. The development of water assets requires significant capital, expertise, and time. A complete project takes 5 to 20 years from acquisition, development, permitting, and sale. New housing and commercial and industrial developments require an assured or sustainable water supply (e.g., in Arizona, access to water supplies for at least 100 years is required) before a permit for the development will be issued. Once water assets are permitted and developed, they are sold to real estate developers (such as DHI), alternative energy facilities, or other commercial and industrial users who must secure rights to an assured or sustainable supply of water to receive permits for their continued projects. Water rights are also sold to water utilities, municipalities, or other government agencies for their specific needs, including to support population and economic growth.

Over the last two years, management has disclosed abundantly rich detail surrounding all of the water rights it owns in the desert states of NV, AZ, CO, and NM. Interestingly, prices for water rights appear to have increased or stayed at above historical levels for the last 20 years through the housing market crash.

|

Exhibit 4: Vidler Current and Historical Water Asset Pricing (Acre-Ft) Analysis |

|

|

|

Source: Company Filings. RWR analysis. |

|

Exhibit 5: DH Horton Southwest Asset Footprint (within the circle) |

|

|

|

Source: Company Filings. |

We went back 25 years and evaluated the Company’s historical water right sales to validate management’s current Vidler’s net asset value assessment. We have summarized our average historical and current estimated water rights prices for each Vidler property in Exhibit 4. A link to our full analysis can be found [HERE].

We understand DHI might be the ideal acquirer for Vidler, as it would bring down anticipated land development costs (i.e., the purchase of these water rights, and pre-development) for its fourth-largest Southwest division (see Exhibit 5). Locking in certain water rights at below-market pricing would help DHI mitigate rising water rights costs and potentially allow them to also sell these rights to competitors and other entities.

|

Exhibit 6: DHI Homebuilding Regions (104 Markets) |

Exhibit 7: DHI Homebuilding Revenue by Region |

|

|

|

|

|

Source: Company Filings. |

Source: Company Filings. |

It was no surprise that the large volume and run-up in the stock before the announcement was likely the deal leaking out. However, what we had not anticipated was that this Offer Price might stand, given the lack of new bidders (so far) and the volatility in the market to trigger the 50% the deal needs to be accepted. We decided that it might be in the best interest of this community and the broader community to share our views on valuation, at the very least as a “discussion” on proper valuation considerations for Vidler. We believe that shareholders are transferring a tremendous amount of value to DHI, who could afford to pay significantly more than $15.75 ($6B in cash generated from homebuilding, with ~$320 million in annual dividends), at least above $25 per share. Interestingly, most of the Company’s largest shareholders have been long-term holders of this stock since before the 2017 restructuring. Potential deal fatigue and an attractive IRR at $15.75 during that time might have influenced and pressured this deal through. The board’s agreements in the 14D suggest this behavior since some of their arguments run opposite to what they share with the public. We believe that only enough new shareholders might put some reasoning into the situation.

The tender offer also points to a rushed process: (i) the timing on when was it announced; (ii) the initial time frame pre any extension; (iii) the relatively manageable breakup fee; (iv) the lack of a shareholder vote; and (v) only a 50% requirement for minimum tender condition (SC TO-T 1). For sophisticated investors, is availing of the appraisal rights option for mergers worth pursuing? It might be something to consider.

|

Exhibit 8: DHI Share and Rankings in Largest U.S. Housing Markets (2Q 2022) |

|

|

|

Source: Company Filings. |

Water-Rights Valuation "Discussion"

Before the Offer, we were anticipating significant interest in the Company, pursuant to the release of the 10-k, from various parties ranging from special situation funds (we had even contemplated it), home builders, real estate developers, and even companies with predictable asset sales that might utilize the Company’s large NOLs. Since 2017, the Company has executed well for shareholders by issuing a special dividend (tax-free) of $5 per share (~$116 million), buying back $51.2 million (4.9 million shares), and opening disclosing the value of its water assets to the public. Effectively, it has issued a “for sale” sign to the market in bright neon lights. Using management’s open disclosures, we calculated that over the last several months, the stock had been trading at the value of its largest asset, the Fish Springs Ranch pipeline and infrastructure (see Exhibit 9) at $230 million (even before the consideration of the $218 million in project cost recoup in the form of preferred capital), while dismissing the value of its other water assets, solar leasing projects, grazing ranch land, and NOLs.

The aggregate Fish Springs value is challenging to determine. Things to consider: How much is the pipeline worth without the attached water rights? Is the whole package worth 1+1 or do we need to include the pipeline costs to get the $39K per AF value? What other rights or use cases could the pipeline have over time? The bear case would be the total Fish Springs package is worth the $39K per AF (or some premium) and then we could subtract the necessary cost recovery. Nevertheless, the value of this property is quite strong.

|

Exhibit 9: Vidler's Largest Assets: Fish Springs Ranch & Carson-Lyon Intertie Projects |

|

|

|

Source: Company Filings. |

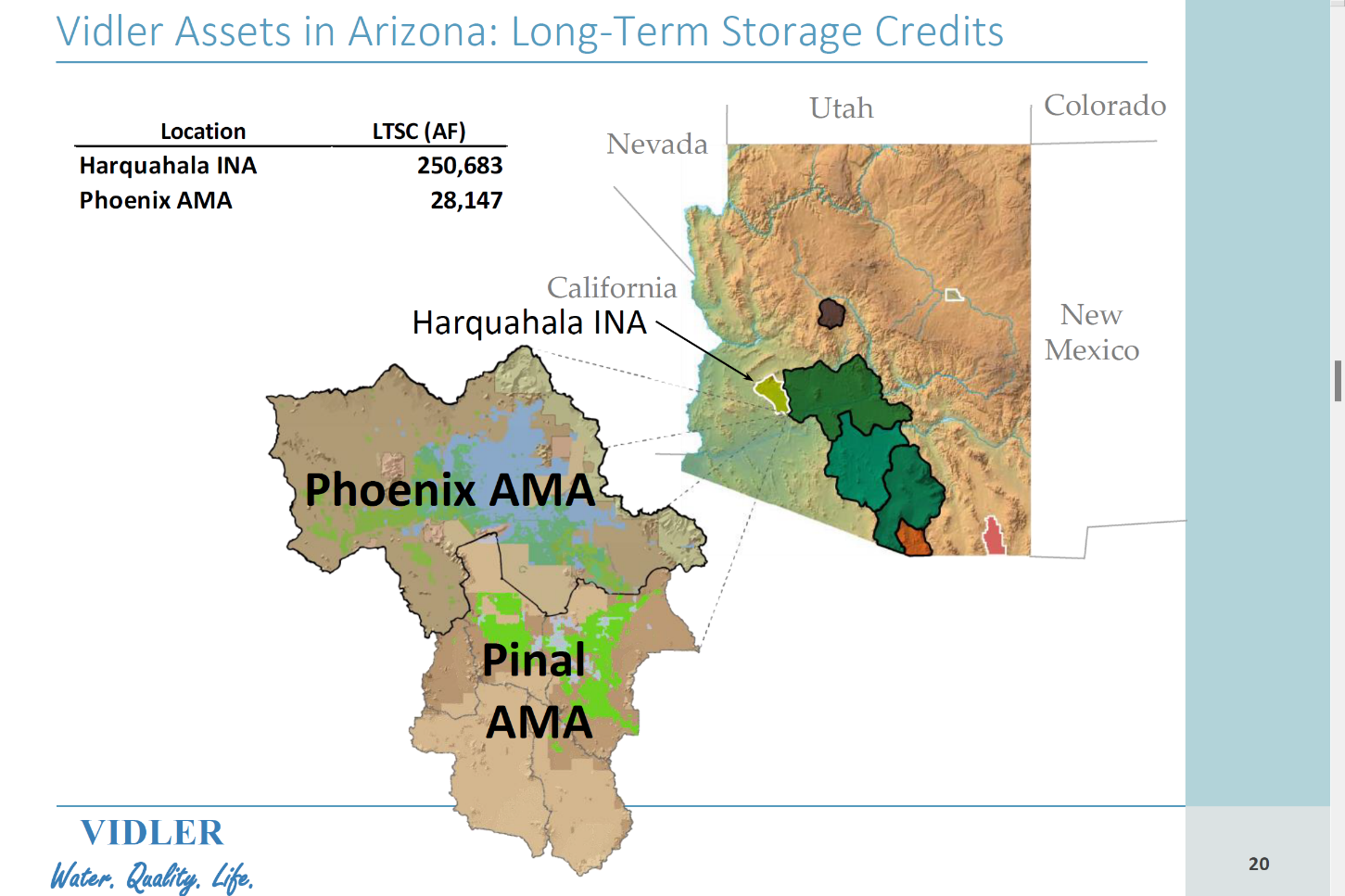

The Company is “actively marketing” all its Long-Term Storage Credits (“LTSC”) in both the Phoenix Active Management Area (“AMA”) and in its Harquahala storage facility (see Exhibit 10). It is in discussions with numerous parties who require water supplies for their projects’ development. The Company is currently asking for an open $450 per LTSC. We estimate that this is probably the lowest price for these assets. In fact, in 2021, the Company had a very significant sale of 55,000 LTSC that generated $22 million, which the Company has yet to return to shareholders. These assets are an essential component in providing an assured water supply for commercial, industrial, and residential growth in Arizona at present. In fact, according to the latest earnings press release, “this has never been so apparent as the ‘mega-drought’ continues in the Western U.S., which exacerbates the difficulty of providing sustainable water supplies for the region’s growth” (see Exhibit 11).

Using management's estimate of the floor pricing of $450 per LTSC, we have calculated the value of Vidler's Arizona assets to be closer to ~$100 million.

In 1998, Lincoln County Water District and Vidler (“Lincoln/Vidler”) entered into a water delivery “Teaming Agreement” to locate and develop water resources in Lincoln County, Nevada. Under their agreement, proceeds from sales of water are shared equally ONLY AFTER Vidler is reimbursed for the expenses incurred in developing water resources in Lincoln County. Effectively, it is a way for Vidler to claw back the percentage ownership of their split above 50/50. Based on historical sales, Vidler’s effective “split” appears to lie closer to 45/65 (Lincoln/Vidler). Vidler has filed applications for more than 100,000 AF of water rights with the intention of supplying water for residential, commercial, and industrial use, as contemplated by the County’s approved master plan. We believe that this is the only known new source of water for Lincoln County. Vidler anticipates that up to 40,000 AF of water rights will ultimately be permitted from these applications, and put to use for projects in Lincoln County. In February 2005, under the Lincoln County Land Act, more than 13,300 acres of federal land in southern Lincoln County near the fast-growing City of Mesquite was offered for sale. According to press reports at that time, the eight parcels offered were sold to various developers (see Exhibit 12).

|

Exhibit 10: Vidler's Arizona Assets: Vidler (Harquahala) Recharge Facility & Phoenix AMA Storage |

|

|

|

Source: Company Filings. |

|

Exhibit 11: 2022 Colorado River Drought Projections – It Might Only Get Worse |

|

|

|

|

|

Source: The Central Arizona Project . Based on the Jan. 1, 2022 projected level of Lake Mead at 1065.85 feet above sea level, the U.S. Secretary of the Interior has declared the first-ever Tier 1 shortage for Colorado River operations in 2022. |

|

In 1998, Lincoln/Vidler filed for 14,000 acre-feet of water rights for industrial use from the Tule Desert Groundwater Basin. In November 2002, the Nevada State Engineer granted an application for 2,100 acre-feet of water rights and ruled that another 7,244 acre-feet would be granted. Historical pricing over the last 15 years has put water rights at around $7,500 per acre-foot, with its most recent pending sale at $7,000 per acre-foot. Some of these purchases appear to have had annual price increases of up to 10%. Pricing these parcels of potential water rights, conservatively at $7,000 per acre-foot we estimate the value of the Company’s Lincoln/Vidler assets at ~$73 million. Including its other Southern Nevada assets of Sandy Valley and Muddy River, we estimate its total water asset value to be ~$76 million.

|

Exhibit 12: Vidler's Southern Nevada Assets: Lincoln County- Vidler Teaming Agreement (except areas 8 & 9) |

|

|

|

Source: Company Filings. |

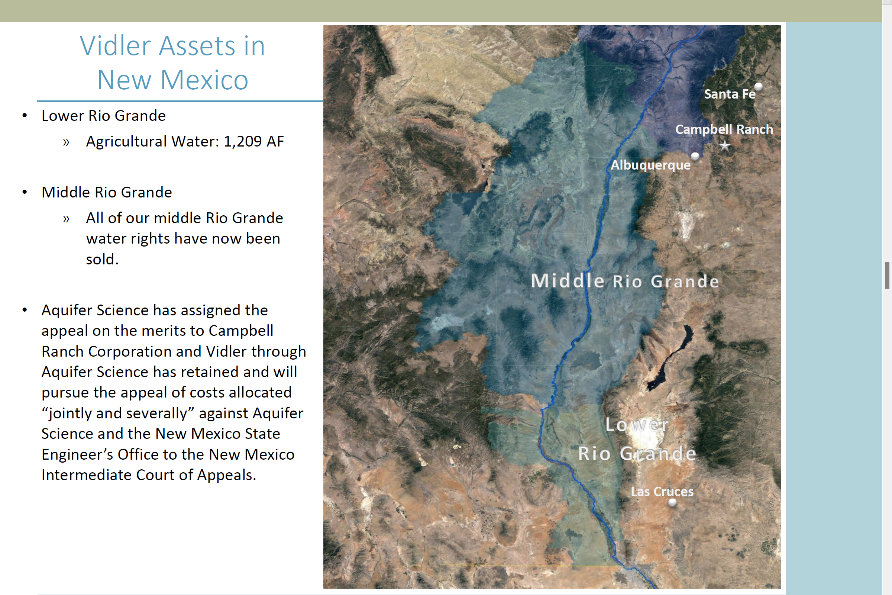

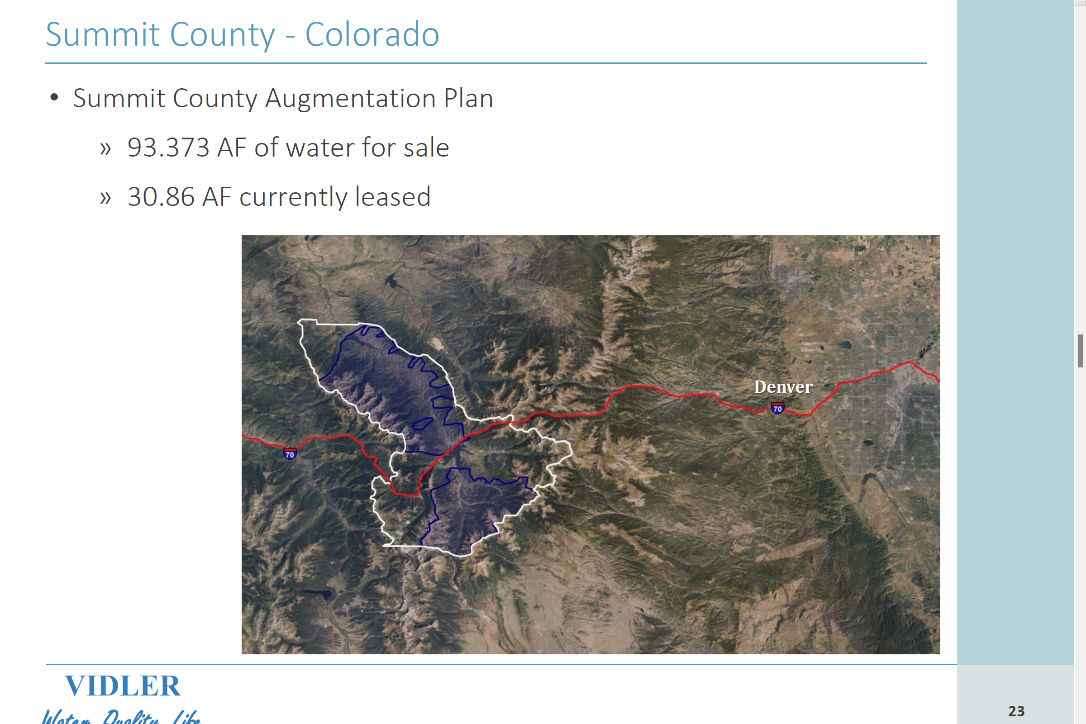

Vidler's last water assets are in New Mexico and Colorado (see Exhibit 13 and Exhibit 14). Using conservative historical pricing of $14k per AF for NM and $44k per AF for CO we value these assets ~$9 million.

|

Exhibit 13: Vidler New Mexico Assets |

Exhibit 14: Summit County – CO Assets |

|

|

|

|

|

|

Source: Company Filings. |

Source: Company Filings. |

The Company has stated several times that it would repurpose some of its lands for solar use, where possible. While solar panels can be used in multiple locations, areas with low cloud coverage and large amounts of solar energy are best for solar panels, particularly in arid climates (see Exhibit 15). Many of the climates where Vidler’s water rights exist are ideal for solar farming. The Company has repurposed some of its lands in Northern and Southern Nevada and Arizona for such projects. In the next year or so, it should have three full solar lease projects online with long-term lease rates of $400-$500 per acre. Using a 15% discount rate on 30-year lease payments, we estimate the value of these assets to be ~$11 million.

|

Exhibit 15: U.S. Solar Irradiance |

|

|

|

Source: EIA and NREL. |

Finally, the Company has other assets in land, preferred capital recovery assets, and NOLs. We value these assets at ~$280 million. With no debt and adding $28 million in cash, we value Vidler's entire assets/equity at around ~$700 million (see Exhibit 16). Even using a deep discount to account for the timing of sale realizations, we cannot see how DHI's offer of ~$290 million is feasible for investors unless there is something else at hand.

|

Exhibit 16: Vidler Asset Valuation Work-up Analysis |

|

|

|

Source: Company filings, RWR estimates. |

Using a 15% discount rate, we quickly calculate the value of the business to be closer to $26.00 per share (see Exhibit 17). We believe we have used a lot of conservative assumptions, and a change to any of them would increase the Company's value for this exercise. We recognize the analysis is not that simple, but a price of $15.75 per share does not seem fair to investors.

|

Exhibit 17: Vidler Fair Market Valuation |

|

|

|

Source: RWR analysis. |

Insulated Water Asset Value

After management’s last shareholder presentation in 2021, we anticipated that it would only be a matter of time before the market properly pieced together the value of the water assets. Despite the Company’s open disclosure on market pricing of water rights, we very much appreciate the illiquidity and timing uncertainty in asset sales. However, these water assets should not get less valuable over time, particularly in the face of rapid population growth in the past twenty years, reducing sustainable water supplies and exacerbating the region’s general water scarcity. We had planned to share a lot of data that demonstrates that Vidler serves some of the fastest and strongest growing regions in the U.S. and that these regions are water strapped. However, management has substantiated these facts through various presentations over the last two years. We find it interesting that the board accepted the offer because they feared a lack of growth in the region due to rising interest and mortgage rates, changes in regulatory laws, and its ability to execute timely water sales.

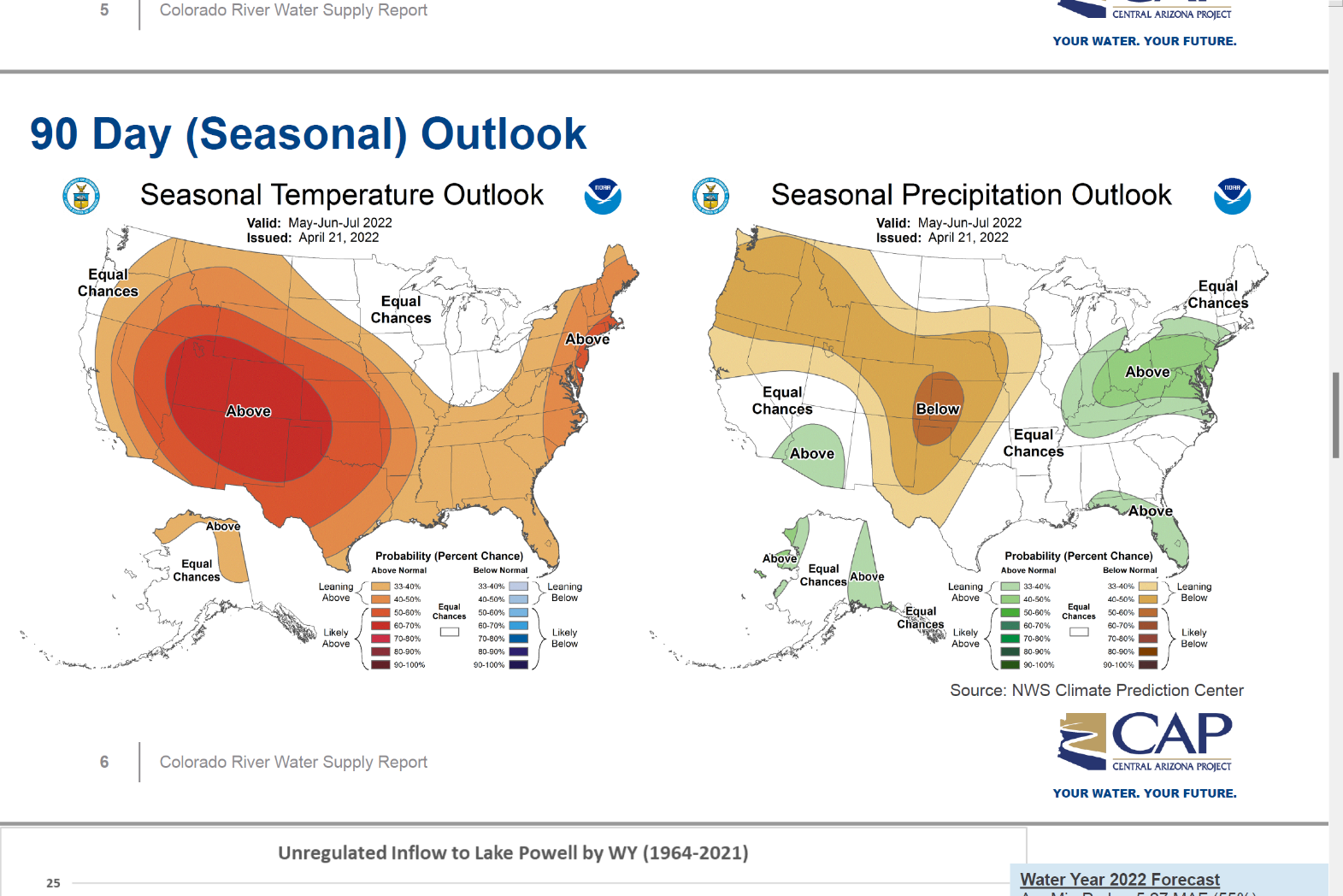

There is enough data to prove that these water assets' value and timely realization are undeniable. Water needs in Vidler’s key environments are necessary for new development, and the existing population as the drought and consumption outpace existing supply (see Exhibit 18). Employers such as Tesla, Apple, Google, Amazon, Blockchain LLC, Switch, and Panasonic have provided thousands of new jobs in Reno. Reno's market conditions demonstrate a propensity to increase due to an overwhelming increase in business start-ups spurred on by Nevada's tax-friendly status with businesses and labor availability from local college graduates. Fearing a correction in the overall housing market is one thing, but Vidler is still in the top growth markets in the country, with an existing population having less and less water every year, even if new homes slow down.

Overall, we argue that Vidler should be considered a pro-inflation hedge asset, whereby the assets should continue to grow in value each year at some GDP+ level.

|

Exhibit 18: U.S. 90-Day 2022 Seasonal Outlook – It Might Only Get Worse |

|

|

|

Source: NWS Climate Prediction Center. |

Management and Board Level Fatigue

The Company has planned to liquidate all its remaining assets (i.e., share buybacks, transparent water sales, price disclosures, etc.). Dorothy Timian-Palmer has extensive background and experience in the development of water assets but has little voting influence. On the other hand, Maxim Webb started with the original investment group in 1996 that formed PICO. He has held various executive management positions and witnessed Vidler’s life cycle. He, too, has little voting influence. The Company’s top shareholders were the catalyst to the Company’s operational restructuring in 2017 and are still calling the shots (see Exhibit 19). A read of some of the shareholder proxy exchanges from 2016-2017 suggests that this group would have been quite satisfied if all of the assets, including water rights, had been sold immediately. The 14D confirms this thinking. From 2017 to 2021, the Company approached 290 suitors, including private equity funds, publicly traded entities, infrastructure investors, endowments and other institutions, and family offices. Management met with representatives from multiple potential bidders. Bank of America Securities Investment Bank ran the sale-side process for the most recent solicitations. We can only imagine that the last five years of this process have been exhausting for management, and it interfered with management’s ability to focus on water asset sales.

|

Exhibit 19: Vidler Major Shareholder Table |

|

|

|

Source: Company, SEC filings, S&P, and Bloomberg. |

Furthermore, we speculate that Vidler’s top shareholders identified in Exhibit 19 most likely have a basis in the stock anywhere between $8.00 to $10.00 per share. Considering all of the Company’s favorable return of capital actions plus the current Offer Price would mean a good IRR for most of them, despite the volatility in the stock over that period. Waiting for management to execute water sales might not be an option for them.

After examining the Company’s latest projections in the 14D, we conclude that either management has historically embellished the value of the assets and their capabilities or their views on these topics have changed dramatically in the last two months. We have our suspicion. We find it odd that management left out several assets from its cash projections, added cash projections for assets it had not discussed in years, was unclear on the discount rate, and used new terminology to discuss water assets (e.g., management used “S&C” to define Stage Coach & Silver Springs, although it had never used or described this phrasing in any filings). We are unsure if this was done unintentionally, so we decided to bridge historical asset-pricing-based disclosures for valuation (see Exhibit 16) with this new cash-flow-based disclosure found in the 14D. Our analysis can be found in Exhibit 20. We admit that it is difficult to align the analysis, but it was clear that the discount rate and missing assets were material to the final analysis. It would be helpful if management could disclose the underlying $/AF prices used to calculate their cash flows because these cash flows are piecemeal sales of the water assets over time. We attempted to calculate the average $/AF sales prices implied by management’s cash flows. We found that many implied $/AF prices were inconsistent with what was represented to the market as far back as their June 2021 presentation.

Company Valuation

The Fish Springs infrastructure is their most significant and visible asset. Yet, it is still hard to pin down, but we believe it should be worth at least the preferred value (i.e., their cost basis) portion of the project, or $216 million (~$12.00 per share). Effectively, the stock traded around that level when DHI made the Offer.

Based on management's cash projections, the company should receive DHI’s cash offer in less than four years. Interestingly, the Arizona storage rights are far more liquid and could be sold quicker and frontload most of the expected cash flows. Another interesting observation is the overhead costs of ~$4.8 million per year. It appears to be made up entirely of compensation. It also seems excessive for a Company in run-off, but management would make more staying on as a public company than under DHI even if it were to come down. We tried to re-engineer management’s assessment that the Offer price is the fair value for the Company by using a conservative 15% discount rate. Using their historical $/AF price methodology, we assumed the same discount rate but added other “missed” assets and got to a price of closer to $26.00 per share (see Exhibit 21). Our complete analysis can be found [HERE].

|

Exhibit 20: Comparison of Management's Pricing-Based vs. Expected Cash Flow Valuation |

|

|

|

Source: Company Filings and RWR estimates. |

|

Exhibit 21: Normalized Equity Valuation |

|

|

Source: Company filings, RWR estimates. |

Catalysts

Unfortunately, the resolution to this deal should be resolved within the next week.

Recommendation

We believe that DHI is the best candidate to take on these assets; however, the current Offer price leaves investors scratching their heads. We believe that a sufficient number of shareholders not tendering may force DHI to increase the Offer price. $26.00 per share seems to be a fair price for new investors in the stock and still provides a very cheap asset for DHI. We recommend purchasing the stock and not tendering at current levels. Regardless, buying back shares with sale proceeds seems more accretive to remaining shareholders at current stock price levels. Finally, we are still curious why the deal is not structured for VWTR to sell the assets to DHI and fully utilize the NOLs, then issue one large dividend, thereby avoiding Section 382. Otherwise, the current deal gives little value to the NOLs.

Risks to the Investment

The lack of new bidders (so far) and the volatility in the market might make this tender offer get the 50% it needs to be ratified.

Additional Unanswered Questions for Management

-

What is the right discount rate?

-

What amount of unpermitted and/or additional water rights exist from legal challenges;

-

Fish Springs infrastructure value is hard to pin down (investments needed, third-party use, etc.), please help?

-

Where are other assets (e.g., solar leases, grazing rights, etc);

-

Interest and mortgage rates are rising, but Reno's growth (and in other VWTR areas) could be unaffected, while DHI’s investor calls suggest positive development growth over the next two years in these key areas which suggest water right monetization?

-

It is unclear why the deal is not structured for VWTR to sell the assets to DHI and fully utilize the NOLs, then issue a dividend, why?

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

The resolution to this deal should be resolved within the next week.

| show sort by |