| 2020 | 2021 | ||||||

| Price: | 14.00 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 55 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 760 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 350 | EBIT | 0 | 0 | |||

| TEV (in $M): | 1,110 | TEV/EBIT | 0 | 0 | |||

| Borrow Cost: | General Collateral | ||||||

Sign up for free guest access to view investment idea with a 45 days delay.

Description

FORMATTED PDF:

https://www.dropbox.com/s/nhj77ha2a9yn50w/WNC%20VIC%20Write-Up%20v3.pdf?dl=0

Preface We believe shorting trailer manufacturer Wabash (WNC) offers an exceptional risk/reward, with ~50% downside in a generous base case scenario, with risk skewed meaningfully worse. Furthermore, we expect an imminent rerating, as we believe the key elements of our thesis will become increasingly clear when the company reports Q4 earnings in several weeks, and is reluctantly compelled to report its backlog, update investors on the concluding order season, and provide initial color on the earnings implications of the return to normal. Our 2020 and 2021 EBITDA estimates, which we believe to be generous (further described below), imply >35% EBITDA misses. Compounded with meaningful financial leverage on a cyclical business, we envision significant equity value impairment.

WNC operates in the commoditized and viciously cyclical trailer manufacturing business, characterized by bullwhip supply/demand imbalances and acute operating leverage. Recent years, driven by the perfect tailwinds of temporary and/or cyclical factors, have been a steroid-fueled super-cycle, with WNC generating ROIC’s multiples of historical levels. A plethora of data points – some readily available and others more research-intensive (such as auction data we have aggregated) – all point in the same direction: the end market has already begun to unwind. While investors generally understand that the trailer cycle is coming off a cyclical high, we believe that most market participants are: (1) grossly underestimating the earnings implications of a return to normal demand levels (not to mention the far more likely case of a cyclical downturn!), (2) unaware that industry capacity has increased dramatically in recent years, & (3) completely overlooking WNC’s significant and accelerating market share losses (share losses of orders in the most recent quarters appears staggering, yet has gone unnoticed due to the data aggregation, calculations, and estimates required).

Short interest approached 10-year lows several months ago, which combined with sparse sell-side coverage, has led to lack of scrutiny and notable real-time inefficiency in the security. Some of our favorite shorts, such as with WTRH and CINE LN last year, occur when the thesis has already begun to play out, yet is being ignored because it has yet to show up in the headline reported financials. We believe that is the case with WNC: we are observing rather than predicting many aspects of our thesis.

N.B.: All references to our base case are based on our assumptions for mid-cycle / normalized earnings. In reality, intuition, recent data, and historical precedent would suggest a downcycle will occur.

Key Thesis Points

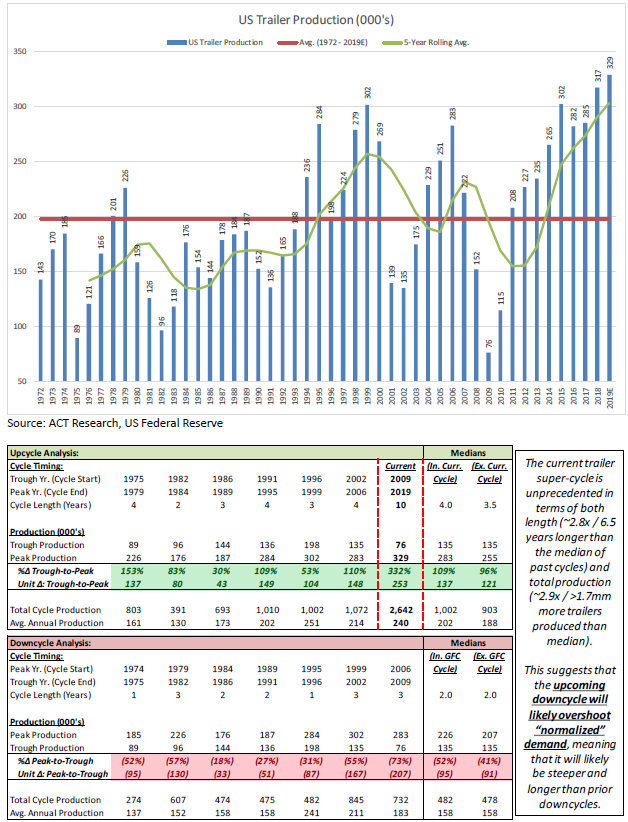

1. Industry Dynamics: The trailer industry is a highly-cyclical, commoditized industry that is coming off a multi-year super-cycle. Framing the industry properly is paramount, as we believe sellside and investor anchoring to recent upcycle years is core to the inefficiency.

a. Long-term industry data provides compelling evidence that trailer volumes are highly cyclical.

b. The trucker customer base is highly fragmented with cyclical profitability of its own.

i. Truckers over-order during good times and pullback during tough times.

c. High fixed costs + narrow margins = high operating leverage and earnings volatility at cycle peaks / troughs.

i. Leads to intense price competition during periods of low utilization to fill capacity.

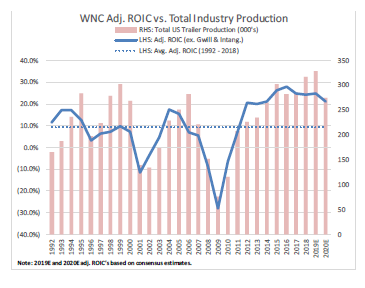

d. Through the cycle, WNC’s ROIC’s are mid to high single digits but have been ~25% in recent years.

i. The industry trends resulting in this over-earning have already turned but have yet to be reflected in WNC’s financials given the lag between orders and reported numbers.

2. Demand: Following several years of well-above replacement cycle demand and production, industry orders have turned, and forward indicators suggest this will continue.

a. We estimate that replacement demand for all trailers is ~230k (~195k for dry van, refrigerated (“reefer”), and platforms).

i. Avg. total US trailer production since 1975: ~200k annually. ii. Avg. dry vans, reefers, and platforms production (WNC’s core trailers) since 1975: ~165k annually.

b. The last five years have been a super-cycle for trailers.

i. Avg. production from 2014 – 2018 → all trailers ~300k (~250k for dry van, reefer, and platforms).

ii. 2019 will set the production record at ~330k trailers (40% - 45% above our replacement demand).

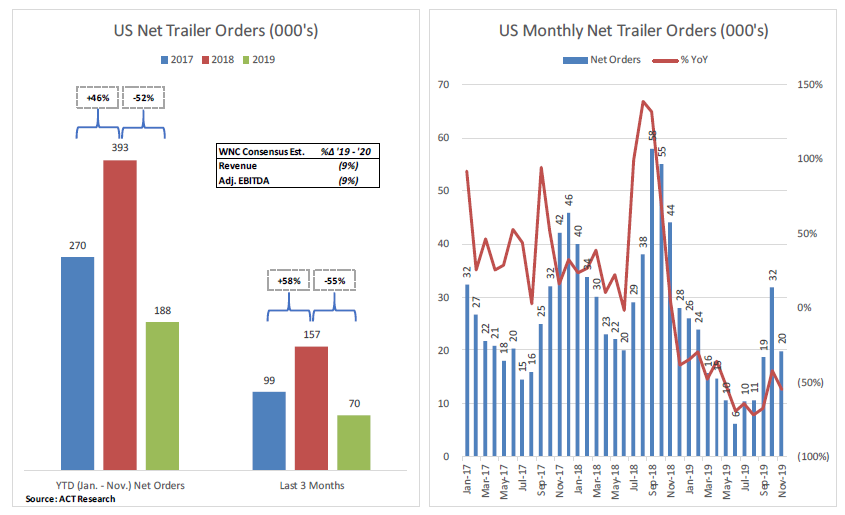

c. Freight market has been rolling over → truckers are placing fewer orders and cancellations have increased.

i. YTD net orders have declined ~52% YoY and LTM net orders are ~215k (-50% YoY).

ii. Order cancellations have averaged ~3.8k per month in 2019 vs. ~1.3k average from 2000 – 2017.

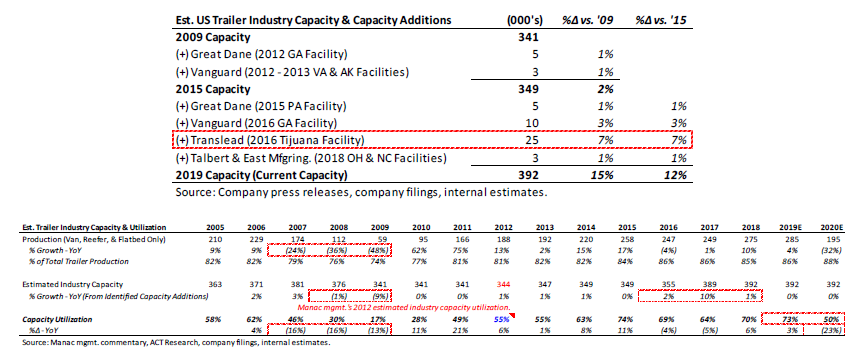

3. Supply: OEMs didn’t bring on capacity for years following the Global Financial Crisis (“GFC”). That all changed in ‘16 - ‘19, when WNC’s competitors built a record amount of capacity, which has increased the downcycle risks materially.

a. We believe industry utilization is poised to fall faster than ever before as demand retreats.

i. OEMs are notoriously slow at adjusting capacity (it’s costly).

b. Industry executives and experts are concerned about excess capacity and price wars.

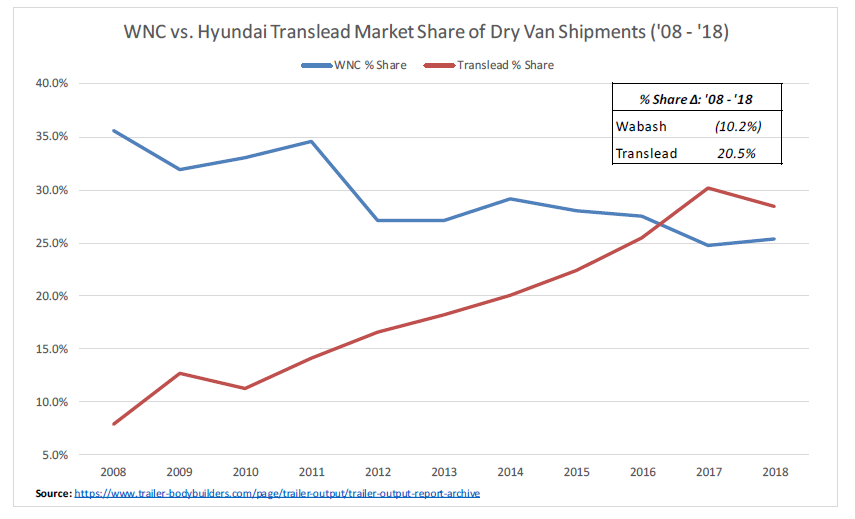

4. Market Share Losses: Current demand super-cycle has masked WNC’s structural share loss to Hyundai Translead, who has led the capacity additions. This share loss will become brutally apparent during the next downcycle.

a. Hyundai has added more capacity than anyone and has been aggressively taking share from WNC for years.

b. A discerning analysis of WNC’s reported backlog highlights that this share shift has likely accelerating in recent quarters, but appears to have been entirely overlooked by market participants.

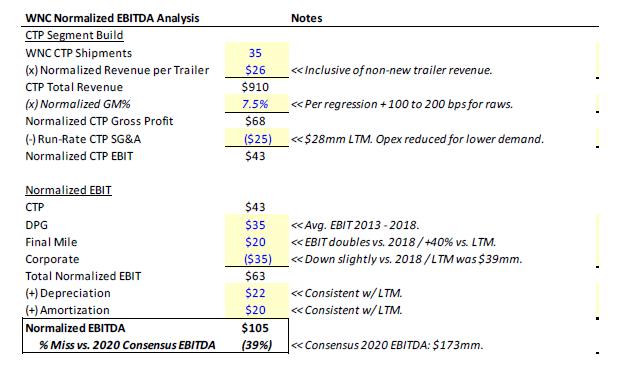

5. Capacity Utilization (Demand + Supply): Our analysis of expected capacity utilization suggests WNC can generate ~$105mm of “mid-cycle” EBITDA, which is ~40% below consensus expectations.

a. To get to capacity utilization, we simply combine new supply (already fully baked) and mid-cycle demand (generous given the consistent trend of volumes overshooting).

b. Our logarithmic regression of capacity utilization and gross margins has a correlation >80%.

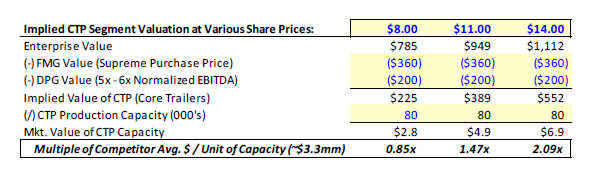

6. Current Valuation: At ~$14.00 today, we believe that WNC’s valuation is at odds with the current trailer cycle, as WNC is trading at a large premium to replacement cost and its historical multiple.

a. WNC is trading at ~2.3x its tangible invested capital, despite significant industry over-capacity and lower cost supply having come online.

i. We estimate WNC’s core trailer business is being valued at ~$6.9k per unit of capacity, while competitors have recently added new, more efficient capacity for ~$3.3k per unit.

b. WNC valuation relative to its historical multiples also appears stretched.

i. WNC’s 7-yr. avg. EBITDA multiple is ~6x; it is trading at ~10x our normalized EBITDA estimate. CapEx is a material, recurring cash drag.

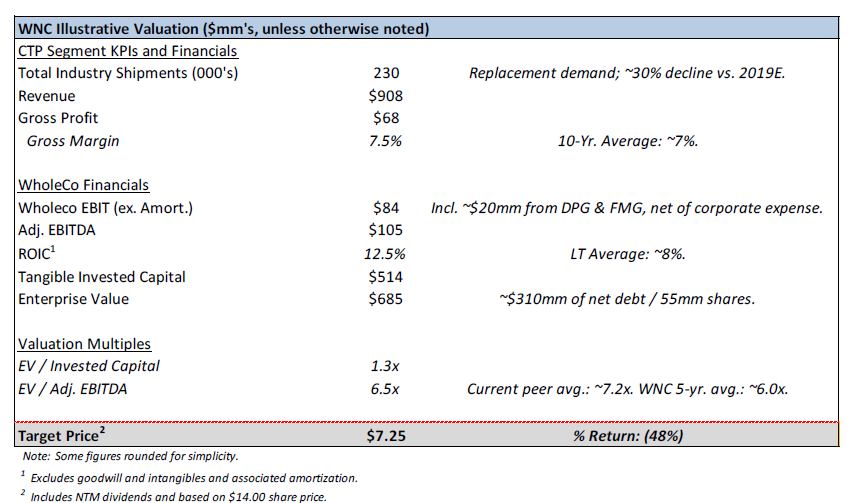

7. Price Target: Based on mid-cycle EBITDA, which we believe is generous given that trailer cycles historically overshoot “normalized demand” to downside (and upside), we believe WNC is worth $7.25 (~50% downside).

Company Background: Since its founding in 1985, Wabash National has grown into one of the US’ largest manufacturers of dry van, refrigerated, platform, tank, and other specialty trailers and industrial products. Today, WNC is the only US-listed trailer manufacturer and reports three segments – Commercial Trailer Products (“CTP”), Diversified Product Group (“DPG”), and the Final Mile Group (“FMG”).

CTP Segment The CTP segment is WNC’s largest segment, accounting for ~66% of LTM revenue, ~56% of LTM gross profit, and ~76% LTM EBIT. This is WNC’s core business and profit center, and therefore the focus of this report. CTP designs, manufactures, and sells dry vans (~79% of segment revenue), reefers (~11%), and platform trailers (~7%), as well as aftermarket parts and used trailers (~3%) from four manufacturing facilities located KY, AR, IN, & MN. Based on historical mgmt. commentary, these facilities have a max production capacity of 80k trailers annually.

WNC sells most of its trailers direct to carriers (~2/3rd) and the rest through its network of independent dealers. CTP’s core customers are large carriers (truckload, LTL, leasing companies, private fleets, etc.), especially for direct sales, while the independent dealer network targets medium and small carriers.

WNC holds leading market positions in its core trailer products. As of 2018, WNC was the #2 dry van manufacturer with 25% share, behind Hyundai Translead (~28% share). WNC was also the #3 reefer manufacturer with ~10% share, behind Utility (~53%) and Great Dane (~17%) and the #2 platform trailer manufacturer with 11% share behind Fontaine (~25%).

DPG Segment DPG is WNC’s second largest segment, representing ~17% of LTM revenue, ~25% of LTM gross profit, and ~17% of LTM EBIT. This segment manufactures tank trailers (58% of segment revenue), process systems (23%), and composites (19%) from its seven US and two international (UK & Mexico) manufacturing facilities.

WNC is the market leader in tank trailers, which are steel and aluminum trailers used to transport chemicals, foods, and dairy. Process systems are vertical tanks and equipment for the food, dairy, and pharmaceutical industries. Composites are WNC’s “DuraPlate” panels, which are used in truck trailers and truck bodies.

WNC sells these products directly to end customers, other OEMs, and to its own CTP segment. DPG’s key end markets consist of chemicals (~25% of segment revenue), food / dairy / beverage (~25%), parts / other (~20%), general freight (18%), O&G / refined fuels (7%) and pharma (~6%). Historically, the US oil patch has driven the chemicals business.

WNC built up the DPG segment mostly through its acquisition of Walker Group (tank trailers + process systems) for $360mm in 2012 and Beall Corp (tank trailers) for ~$15mm in 2013. WNC acquired these businesses to diversify its operations away from its core CTP business. However, these acquisitions have failed to live up to expectations, as WNC bought these businesses at the peak of the O&G cycle (2013 EBIT: ~$60mm →2018 EBIT: $22mm). While hyped as game changing and diversifying transactions by mgmt., they have failed to deliver. It’s important to remember these value- destructive deals when considering WNC’s more recent acquisition of Supreme Industries (more below).

FMG Segment FMG is WNC’s smallest segment (18% of sales / 19% of GP, 8% of EBIT) and was formed after the acquisition of Supreme Industries (ticker: STS) in late Q3 2017 for ~$360mm. The FMG segment designs and manufactures dry van and reefer truck bodies (the exterior of a box truck) at its six manufacturing facilities across the US.

FMG’s revenue primarily comes from dry van truck bodies (~82% of segment revenue) followed by reefer bodies (~13%), and van upfitting parts and services (~5%). By end markets (truck classes), ~40% of segment revenue comes from Class 6, ~26% from Class 2 - 3’s, ~25% from Class 4 - 5’s, and the rest (~9%) comes from Class 7 - 8’s. WNC expects truck bodies and cargo van upfitting market to grow MSD% driven primarily by e-commerce and final mile delivery services growth.

WNC holds the #2 position for truck bodies with high-teens share (Morgan Olson’s has 45% share).

Mgmt. viewed Supreme as highly strategic for its scale in medium and light-duty truck bodies and its ability to reduce WNC’s dependence on the Class 8 dry vans and reefers. As such, WNC paid a full price (~14x LTM EBITDA / ~8x LTM EBITDA including the $20mm of run-rate 2021 synergies) for Supreme.

Like the Walker & Beall deals (DPG), WNC bought Supreme at peak cyclical profitability. Standalone Supreme generated ~$25mm of LTM EBITDA at the time of the deal while the FMG segment (incl. WNC’s small legacy truck body business) generated ~$17mm of LTM EBITDA, despite mgmt.’s promises of synergies. Additionally, analyzing Supreme’s historical financials reveals that truck body manufacturing not only is cyclical (not surprising as Class 1 - 8 trucks are cyclical), but also failed to produce meaningful cash flow. For example, from 2012 – 2016 Supreme generated only ~$8mm of average annual FCF.

Key Thesis Points 1) The trailer industry is a highly-cyclical, commoditized industry that is coming off a multi-year super-cycle.

We want to highlight a very simple truth about the trailer industry – that it is highly cyclical and commoditized. Framing the industry properly is a key source of inefficiency to the short because we believe that the sellside and investors are anchoring to recent upcycle years and have overlooked the very rich long-term historical trailer data.

As the LT data shows, the trailer industry – like many capital goods industries – is highly cyclical, characterized by boom and bust delivery cycles. This is a function of its fragmented core customer base (truckers), whose profits are also highly cyclical profits. When profits are high, truckers over-order tractors and trailers to defer taxes. This usually leads to excess

capacity and depressed trucker profitability, causing truckers to slash capex and/or partially or fully liquidate their fleets (dampens demand for new trailers). In 2018 historically high trucker profitability and Trump tax incentives (designed in a manner to accelerate capex), exacerbated this “normal” cycle and pulled forward a significant amount of trailer demand into 2018 and 2019.

While not as sizeable of an investment as a new tractor (~$115k), a new dry van trailer (~$25k) is still a large purchase, when trucker profitability is depressed. Furthermore, truckers will buy a new tractor over a trailer in bad times because new tractors usually provide better ROIs. It also costs less to extend the life of a trailer by 1 - 2 years (no engine).

The trailer industry is not only cyclical, but also highly competitive, as trailers are largely undifferentiated across OEMs. As with most capital goods manufacturers, trailer OEMs have a high degree of fixed-costs and operating leverage, which exacerbates earnings volatility in demand peaks and troughs. Cyclical demand, high fixed costs, and undifferentiated products supplied by a fragmented OEM base results in intense price competition in downcycles, as OEMs cut price to cover fixed costs and drive utilization. In addition to the historical data, numerous conversations with industry executives point to the extreme price competition in industry downcycles.

Due to these factors, WNC historically generated ~HSD% ROICs (adjusted to exclude goodwill /

intangibles, acquisition amortization, & one-time charges) through the cycle. However, the recent perfect storm of positive developments – historically strong truck profitability and Trump tax cuts – have driven WNC’s ROICs to 25%. As we will detail shortly, the super-cycle reversing in realtime, which we believe will return WNC’s ROIC to LT averages (and likely overshoot to the downside) as demand reverts to replacement levels and price competition returns for the first time in years. To further highlight the cyclicality of WNC’s CTP segment, we point you to its historical financials. We think that the super-cycle has led investors to overlook WNC’s not only current over-earning vs. history, but also substantial losses in down-cycles, which is key given the trajectory of the trailer cycle and WNC’s leverage ($354mm of net debt).

2) Demand: Following several years of well-above replacement cycle demand and production, industry orders have turned, and forward indicators suggest this softness will continue.

Since 1975 total US trailer production has averaged ~200k annually with dry vans, reefers, and platforms (WNC’s core) accounting for ~165k. Due to conservatism and to account for population growth and other factors, we estimate current replacement demand to be higher than the LT average. Therefore, we estimate total US trailer replacement demand is ~230k (+15% above LT avg.) with dry vans, reefers, and platforms accounting for ~195k (+18% above LT avg.).

As we have said, the trailer industry has been experiencing a super-cycle in recent years. In the last 5 years, production has averaged to ~305k, and 2019 will set the production record at ~330k trailers (>40% above estimated replacement demand). As the freight market has entered recession in 2019, trailer orders have fallen precipitously with net orders YTD and LTM declining >50% YoY. ACT Research has also noted that there are elevated inventories at OEMs and dealers. Despite these clear forward indicators, consensus assumes a modest decline (HSD%) in WNC’s 2020 topline and EBITDA.

There is a plethora of other forward indicators that suggest trailer demand will continue to be soft, including the following (note: we include further detail on some of these in the appendix):

• Spot rates – the key driver of trucking profitability – are down sharply YoY.

o YTD dry van, reefer, and flatbed spot rates are down -15% to -20% YoY.

o Significant capacity additions (class 8 trucks) and a slowing US economy (esp. manufacturing) have resulted in excess freight capacity, which is expected to continue pressuring trucking rates well into 2020.

• Public truckers have communicated to investors that capex will be down sharply YoY.

o Consensus expects capex for 22 public truckers to decline >10% YoY in 2020 and another 5% in 2021.

o Public truckers have already been shrinking their trailer fleets in Q2 and Q3 and many have specifically said that they expect trailer purchases to be down YoY in 2020.

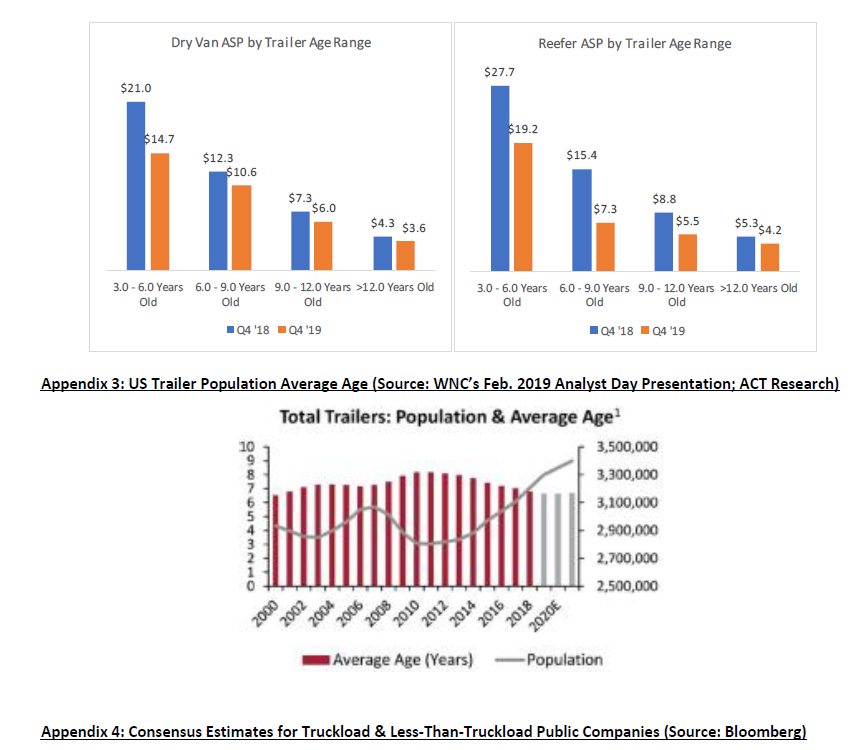

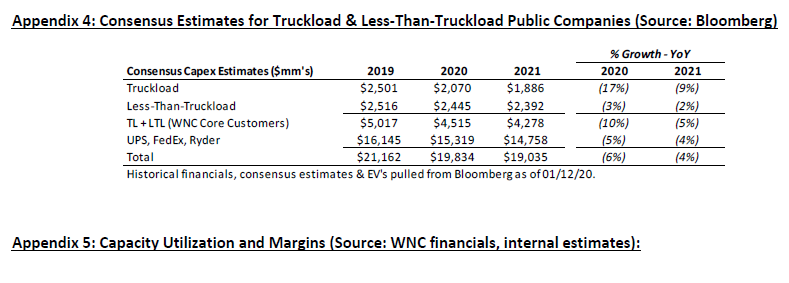

• The average age of the trailer population is at all-time lows (data to 2000), indicating limited need for replacement.

o In early ‘19, ACT estimated the avg. US trailer would be ~6 years old by YE ‘19 vs. the LT avg. of ~7 years.

▪ Based on ~300k deliveries. Actual ‘19 deliveries will be ~330k implying an even younger avg. age.

o The last time the US trailer population was this young was 2000 (~6.5 years), which followed 4-years of above replacement level production (average of 273k trailers per year).

▪ In 2001 trailers production fell sharply and production only averaged 173k per year from ‘01 - ‘04.

• 2019 trucker bankruptcies are up ~3x YoY.

o There have been several large bankruptcies (Celadon – 3k drivers, New England Motor Freight – 1.5k drivers, Falcon – 585 drivers, Stevens Tankers – 575 drivers) and many more medium and smaller BKs.

o Bankruptcies directly reduce trailer demand (no orders if not operating / no funds) and indirectly, as the bankrupt carriers sell their used trucks and trailers (including the auction market).

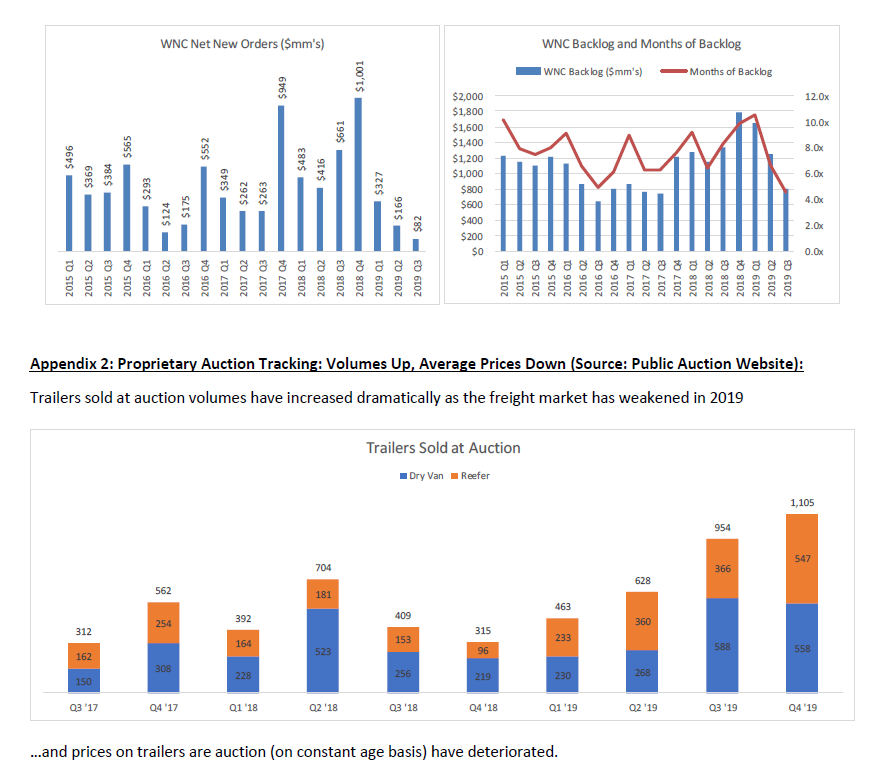

• Our proprietary trailer auction data indicates that trailer volumes are up and used prices are down.

o Dry van and reefer volumes are up significantly, while ASPs on constant age trailers are down.

o Importantly, as the channel of last resort for disposing assets due to auction fees, elevated auction volumes and soft realized prices at auctions suggest that there is excess trailer supply in the market.

As a result of these large capacity additions and our expectation that industry volumes retreat to or below replacement demand in 2020 (30% - 35% decline vs. ‘19), we project industry capacity utilization will fall from ~73% (2nd highest ever) to ~50% (average from ‘10 - ‘13). Furthermore, this would represent an even larger YoY decline (>20%) in industry utilization than 2009 (13% decline). At least one trailer executive has publicly said that he is concerned:

“The trailer industry needs to adjust down in capacity to some degree to get it to where the demand meets the capacity. How that happens is what still needs to play out...an adjustment could come in [Q1] because there are slots without orders to fill them. If production capacity isn’t reined in, then lines will continue to build trailers simply to add inventory.” - David Giesen, Stoughton VP of Sales

Importantly, capacity is unlikely to exit the market because it is costly and difficult to do so given the upfront investment and high human capital requirements (don’t want to fire employees you may need in the future, especially in a tight labor market). This means that industry utilization is unlikely to be buoyed by capacity exiting the market:

“Adding production capacity isn’t a short-term decision; reducing capacity, likewise, isn’t a short-term decision. Capacity may be there, but you may be running the line at the rate lower than you anticipated.” – Frank Maly Director of Commercial Vehicle Transportation Analysis at ACT

(Source for above quotes: https://www.ttnews.com/articles/november-trailer-orders-weaken-leaving-excess-production-capacity)

At these low levels of utilization not seen in years, we expect trailer OEMs to reduce price to maintain volumes to cover their fixed costs. In fact, we believe that OEMs may already be enticing customers with better deals to “keep the lights on,” which may be propping up industry order stats. Industry contacts have suggested that Translead’s #1 priority is keeping volumes high at the Tijuana plant, and that they can be aggressive on price to ensure that given their cost advantage.

It’s Important to note just how detrimental price cuts would be to WNC. For example, a $25k trailer with a 10% gross margin generates ~$2.5k in gross profit. All else equal, a 2.5% price reduction ($625) would cut gross profit on that trailer by 25% and result in a 7.7% gross margin (~230 bps of GM% compression). Clearly the impact on operating profit would be much worse.

4) Market Share Losses: Current demand super-cycle has masked WNC’s structural share loss to Hyundai, which is accelerating and will become brutally apparent in the upcoming downcycle.

As the graph shows, WNC has persistently lost market share to Hyundai over the last decade, as Hyundai has built two new Mexican facilities. Production cost advantages (both facilities in Mexico / more modern than WNC’s) has allowed Hyundai to produce a comparable product to WNC’s at a lower cost, which it has shared with customers via lower prices.

This long-term share loss cannot be described as anything but structural, but market participants have overlooked this fact due to the recent trailer super-cycle. Furthermore, while bulls might counter this point with WNC ‘18 share gain vs. Hyundai, industry experts believe this was likely due to supply chain constraints, which was have since likely been fixed. As industry volumes retreat in ‘20 and Hyundai isn’t restricted by supply chain issues, we expect the LT trend to reemerge, and likely even accelerate, with WNC ceding significant share to Hyundai, who will look to aggressively protect volumes.

We are already observing the share loss in 2019 in two ways:

1) YTD deliveries & Q4 guidance: WNC has lost share of ‘19 deliveries, as its YTD unit sold (CTP + DPG) are down -5% YoY while YTD total industry production is up +10% YoY, which implies that WNC has lost ~265 bps of share YTD. This YTD share loss does NOT appear to be timing related, as WNC lowered the midpoint of Q4 deliveries guide by ~9% vs. the prior implied Q4 guide. This updated guidance shows delivery share losses accelerating into Q4 for WNC. Additionally, in an attempt to put lipstick on the pig, mgmt. said on the Q3 ’19 call that they had not seen the same level of cancellations as the industry when asked about lowering guidance. We believe them (somewhat)! Because what they are really saying is that that WNC has lost share of gross orders (more on this in point 2 below table).

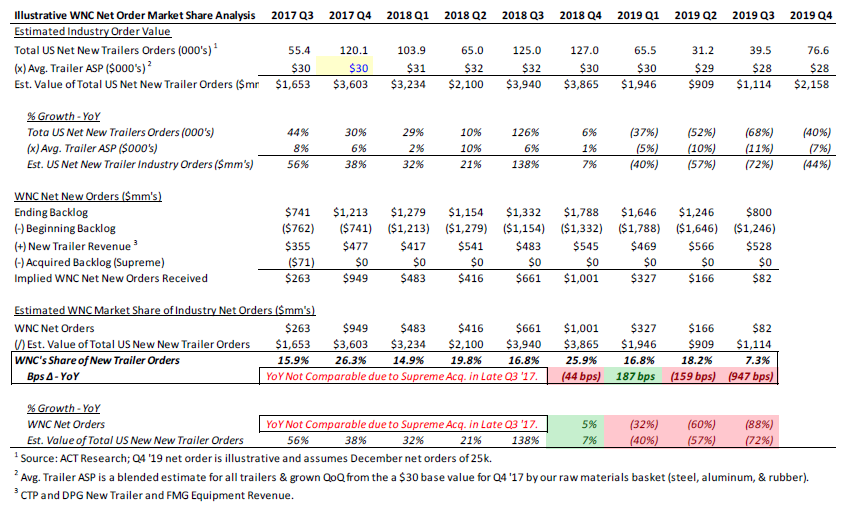

2) YTD net orders: A discerning backlog analysis shows that WNC’s net orders have massively lagged industry net orders, especially in Q2 & Q3, suggesting that WNC will lose further market share of deliveries in Q4 and into 2020.

a. Analysis summary: Imply WNC’s net orders from its backlog & compare the YoY change in WNC’s net orders to industry net orders and our estimate of industry net order value to determine net order market share. b. Key takeaways of this analysis (see table below for math):

i. The rough math suggests that WNC’s share of net new trailer orders may have fallen to ~7% in Q3 ’19 vs. ~20% shipments share in ‘18.

ii. Q3 ’19 was WNC’s worst quarterly net order intake figure looking back to Q1 ’15.

iii. The -88% decline in net orders is especially bad considering that the FMG segment (10% - 15% of total backlog) is likely experiencing backlog growth.

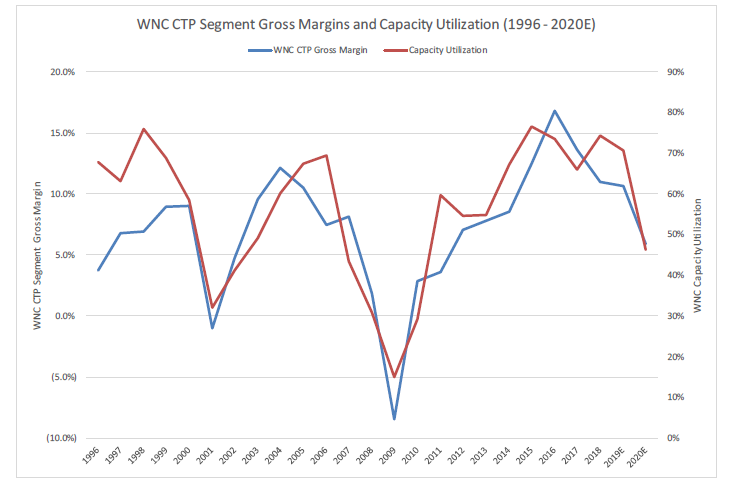

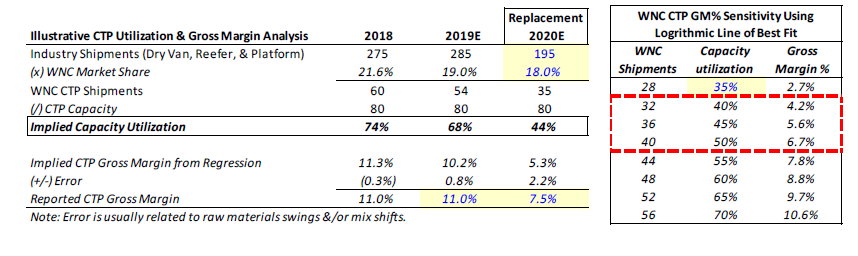

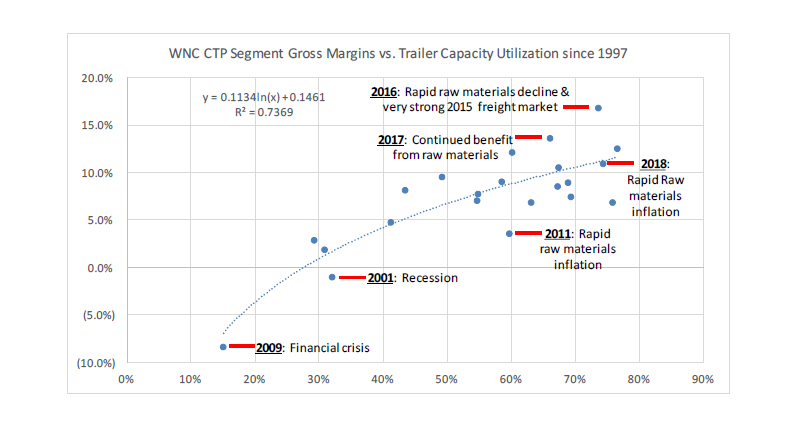

5) Capacity Utilization (Demand + Supply): An analysis of WNC’s CTP segment capacity utilization implies that WNC can generate ~$105mm of “mid-cycle” EBITDA, while consensus expects $173mm and $191mm of EBITDA in 2020 and 2021, respectively, making our normalized EBITDA estimate 40% - 45% below consensus.

As a manufacturer with a high degree of fixed costs (facilities + labor), there is a strong relationship between CTP gross margins and capacity utilization, which we define as trailer shipments divided by capacity. We have scrubbed WNC’s financials to the late ‘90’s to understand this relationship (~80% correlation) and have used a regression to illustratively predict CTP gross margins at different shipment levels. (2020 in graph below is our estimate for utilization and gross margins.)

Below is the quick build for how we arrive at our CTP gross margin estimate and some details on our assumptions.

• We expect shipments to revert to replacement level in 2020 and 2021 and for WNC to cede share to Hyundai.

• Our regression suggests that gross margins will be just over 5%; however, we think this is likely a bit too low given that H1 ‘20 gross margins will temporarily benefit from raw material tailwinds (steel / aluminum down in 2019).

Using a few other high-level assumptions (detailed in the table below), we arrive at our “normalized” / “mid-cycle” EBITDA estimates of ~$105mm, which we use as our 2020 and 2021 base case given the direction of the trailer cycle.

6) Valuation: At ~$14.00 today, we believe that WNC’s valuation is at odds with the current trailer cycle, as WNC is trading at a large premium to replacement cost and its historical multiple (~6x EBITDA).

Given the commoditized nature of WNC’s business, replacement cost is a relevant valuation metric. With a current EV of ~$1.1bn vs. ~$480mm of tangible invested capital, WNC is trading at 2.3x tangible invested capital. This seems like an excessive premium given (1) the direction of the trailer cycle and (2) WNC’s continued share losses.

We also compare what WNC’s share price implies for the value of CTP’s capacity vs. competitor capacity additions. In aggregate Hyundai, Vanguard, and Great Dane spent $132mm to add ~40k in annual production capacity since 2015. This equates to ~$3.3k per unit of new capacity. As the table below illustrates, WNC’s current share price implies that the market is valuing WNC’s trailer capacity at ~$6.9k per unit even though this capacity is 10 – 20 years old.

7) Valuation: We believe WNC is worth ~$7.25 in a generous base case (~50% downside).

A return to normalized demand + greater industry supply → lower volumes, utilization rates, & price pressure. This will cause WNC’s ROIC and margins to normalize back to, and likely below, LT averages. Below is our price target derivation:

We believe that bulls may point to lower raw materials in ‘19 as an offset to trailer volume softness. However, while raw materials are clearly down YoY, we disagree on WNC’s ability to realize the benefits from lower raw materials based on:

1) It was abundantly clear in our conversations with OEMs, suppliers & customers that all parties know about raws.

a. Customers felt squeezed on prices as raw materials inflated in 2019, and view that the pendulum has swung in their favor as it relates to pricing negotiations.

2) Even OEMs admitted to us that 2020 won’t be like 2015 - 2016 (last time they benefitted from raw materials deflation) was because backlogs had reached an all-time high.

a. OEMs didn’t have to pass on raw materials savings because there weren’t enough production slots, evidenced by the industry backlog-to-build ratio ballooning to all-time high of >10 months.

i. Note: Hyundai’s Tijuana plant didn’t open until the very end of 2016, which is part of the reason why there weren’t enough slots in 2015 – 2016. That plant is now open but took several years to ramp.

b. Today, the industry backlog has reportedly shrunk to ~4 months (below LT average of 5 – 6 months).

i. There are simply too many slots available for OEMs to hold firm on price. 3) When capacity utilization was low, WNC struggled to pass on raw materials inflation. The reverse should hold true.

a. In ‘11 WNC’s CTP shipments doubled YoY from 23k to 48k, but gross margins only improved 80 bps (2.8% → 3.6%) b/c of higher component and raw materials costs that WNC was “unable to pass along” to customers.

i. This should not be surprising given that industry utilization was only ~50% (our expected mid-cycle industry utilization). At 50%, there are too many slots available for OEMs to hold firm on price. 4) Even if WNC benefits from raw materials in 2020, we believe that benefit will be limited and dissipate quickly.

Appendix 1: WNC Backlog and Net Order Analysis (Our estimates):

Catalyst

- Q4 2019 earnings

- December, January, and February industry order data

| 1 show sort by |