| 2017 | 2018 | ||||||

| Price: | 18.70 | EPS | 1.85 | 1.95 | |||

| Shares Out. (in M): | 472 | P/E | 10.1 | 9.6 | |||

| Market Cap (in $M): | 8,826 | P/FCF | 9.9 | 9.8 | |||

| Net Debt (in $M): | 2,718 | EBIT | 1,116 | 1,130 | |||

| TEV (in $M): | 11,544 | TEV/EBIT | 10.3 | 10.2 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- Spin-Off

- Potential Acquisition Target

- accelerating growth

- Value trap

- Short squeeze

- WESTERN UNION CO WU S 03/18/2016

- Western Union Company WU 04/13/2015

- WESTERN UNION CO WU 02/25/2014

- WESTERN UNION CO WU S 08/29/2013

- WESTERN UNION CO WU S 06/06/2013

- WESTERN UNION CO WU S 11/13/2012

- WESTERN UNION CO WU 09/15/2011

- Western Union WU 07/12/2007

- Western Union WU wi 09/22/2006

- BETA

- First Data FDC 02/19/2006

- UNICREDIT SPA UCG IM 02/02/2023

- Chemours CC 03/06/2019

Description

Summary

Western Union has been written up 9 times on VIC (5 times as a long, 4 times as a short). WU is the dud of the spinoff category. The stock hasn’t worked in 11 years, and still trades at ~$19 which is where it traded post its spin from First Data in late 2006 (while the S&P 500 is up +80%). WU’s underperformance is even more pronounced when considering that it shrunk its fully diluted shares by 37% since its spin. The only return shareholders received was from the dividend which went from $0.04/year in 2007 to $0.70/year today (3.7% yield). WU’s flat stock chart had 2 phases: the first 6 years were about multiple compression, while the last 5 years were about flattish EPS.

With the stock trading at just 11x 2017 EPS guidance and with a 12 day short position (addressed later), two recent developments suggest WU’s “lost decade” is approaching its end. (1) Western Union’s rapidly-growing digital money transfer business (westernunion.com, or WU.com), could single-handedly lift EPS growth to 10%-13% by 2020. WU.com, which accounted for 8% of revenues in 2016 will grow to 15% of revenues by 2020. With +20% sustainable revenue growth, WU.com will contribute 300 bps to WU’s overall revenue growth in 2020. WU needs mid-single-digit revenue growth to experience margin expansion, which means that the remaining businesses (“RemainCo,” composed of Retail C2C, C2B and B2B) need to deliver just 1%-2% revenue growth, collectively. These businesses have delivered this level of growth for the past 2 years in constant currency, but FX headwinds have made them appear like declining businesses. If FX swings to a neutral, WU would achieve 5% revenue and 10%-13% EPS growth by 2020 (recent USD weakness is a positive development). If FX swings to a tailwind, 2020 EPS growth could exceed this projection. (2) Two recent takeovers allow for a sum-of-the-parts valuation on WU and suggest the stock is substantially undervalued. Applying discounted valuations to the precedent transactions, I get a conservative intrinsic value estimate of $33 at the end of 2020, for 72% upside, or a 3.5-year IRR of 20% including the dividend. I also believe WU is ripe for an LBO as PE recently raised record amounts and WU is a rare cheap stock with an accelerating growth profile in a fully-priced market.

Business Description

Western Union operates three different global money transfer businesses: C2C, C2B and B2B. I will focus on the C2C business because it accounts for 92% of earnings. The C2B business (6% of earnings) is a bill payment service where WU facilitates consumer payments to utilities, auto finance companies, mortgage servicers and government agencies. WU got into the B2B business through the 2011 acquisition of Travelex Global Business Payments for $976 million. B2B (2% of earnings) facilitates cross-border payment and FX solutions for small and medium-sized businesses.

Consumer-to-Consumer (C2C, 79% of 2016 revenues, 92% of op. income, 23% operating margin)

WU facilitates individual money transfers from one consumer to another. Western Union operates an asset-light transaction processing business which partners with local agents who own the brick-and-mortar locations where consumers go to initiate/receive a transaction. WU’s ~500,000 retail agents locations around the world include post offices, banks, financial services institutions, major retail stores, drug stores, convenience stores and foreign exchange agents. The typical customers of WU’s retail C2C business are international migrants (people who leave their home country for better economic opportunities in another country). The World Bank expects the international migrant population to soon surpass 250 million (~3% of the world’s population), reaching an all-time high, as people search for economic opportunity outside of their birth country. WU’s rapidly growing digital money transfer business (WU.com) is included in the C2C segment, and in 2016 made up 8% of the segment’s revenues. While WU.com historically had lower margins than the retail C2C business, WU.com recently achieved scale and its incremental margins are now equal to those of retail C2C. From here forward, growth is growth. C2C revenues are composed of transaction fees (73%), foreign exchange fees (26%) and other revenues (1%). The average principal amount sent in this business is ~$300 per transaction. WU is the #1 global provider in both its retail and digital C2C money transfer businesses. In 2016, the Company transferred $80 billion, with $72.5 billion (91%) being high-margin cross-border transfers and $7.5 billion (9%) being lower-margin intra-country transfers.

Western Union Is a Virtually Impossible-to-Replicate Global Asset

WU is the world’s largest money transfer provider, operating in over 200 countries through ~500,000 C2C retail agent locations. WU transfers money across 16,000 corridors (a corridor is a country-to-country pairing, such as from the U.S. to Mexico) and completes ~2.5 million transactions each day between its three businesses (C2C, C2B and B2B). Western Union benefits from an unmatched 91% brand awareness globally. WU’s business is a complex one, requiring 204 regulatory licenses around the world and necessitating the Company to spend 3.5%-4% of revenues on compliance annually (~$200 million per year; more than 20% of its workforce is dedicated to compliance). In recent years, stricter compliance requirements aimed at improving the industry’s anti-money laundering, anti-terrorism and anti-fraud initiatives have raised barriers to entry and contributed to a couple of small competitors’ exiting the business. WU’s compliance spend should give it a long-term competitive advantage. In the past 5 years, as WU significantly increased its compliance spend, the dollar value of reported fraud in WU’s C2C transactions compared with the total value of C2C transactions has declined by more than 60%. WU spends ~4% of revenues on marketing annually to maintain its unmatched brand awareness. The Company also engages in certain acts of goodwill which differentiate it in the marketplace. For example, after the 2015 earthquake in Nepal, WU temporarily waived its fees on money transfers into the country and experienced an immediate doubling of transactions into Nepal.

In 2016, Western Union had 12.6% market share of the $575 billion (principal) C2C cross-border money transfer market. However, WU’s market share is far greater when looking more closely at its true end market. About 55% of global remittances are sent through the banking system, leaving ~45% (or $259 billion in principal) sent through retail/digital C2C channels. So WU has ~28% global share of the retail/digital cross-border C2C money transfer market. In certain corridors which have less competition, WU’s market share can approach 50%-70%. MoneyGram (MGI), the #2 C2C competitor, has ~11% global market share on this basis, and Euronet (#3; ticker: EEFT) has another ~6%. In short, the top 3 retail/digital C2C money transfer providers control ~45% of the global market. There are no other global players, and the remainder of the industry consists of regional competitors (such as UAE Exchange in the United Arab Emirates, which is both a competitor and a WU/MGI agent; the company has plans to IPO on the London Stock Exchange in the near future) and single-corridor specialists. WU’s pricing in retail C2C is, on average, 15% higher than that of its competition, underscoring its competitive advantages and the strength of its brand. As the following table illustrates, WU generates almost 2x the C2C money transfer revenue of MoneyGram and Euronet combined and, due to its industry-leading margins, earns 5x their combined EBIT.

Top 3 C2C Money Transfer Providers, 2016 Data

I estimate that WU’s C2C profits account for 51% of the retail/digital C2C industry’s profits. My estimate is based on applying the average of MGI’s EBIT margin (6.6%) and EEFT’s margin (12.7%), or 9.6%, to the remaining 55% of the market not held by the top 3 players. I believe this is being generous, as the rest of the industry has far less scale and brand awareness, and must compete on price. In short, 51% most likely understates WU’s profit share. Western Union’s dominance of its industry’s profitability is almost as strong as that of Apple (AAPL). In 2016, Apple accounted for 14.5% of global smartphone units, but due to its premium pricing and industry-leading margins, Apple captured 79% of the industry’s profits. The main contributor to such a winner-takes-almost-all phenomenon in business is unmatched brand strength which allows for premium pricing.

WU.com is a Valuable Hidden Asset

WU.com allows customers to send money to a recipient’s bank account (almost 3 billion bank accounts worldwide can receive a WU.com transfers) or to one of WU’s ~500,000 retail agent locations around the world. The sender can fund the payment through a credit card, debit card, bank account or ApplePay. WU.com’s fees are different depending on the send/receive combination. For example, it is more expensive to send money to a retail location than to a bank account, as WU must pay the agent a commission. In addition, funding the payment with a credit card is more expensive than funding it with a bank account. A typical WU.com customer might be a 25-year-old with a job in London, sending money to family in rural India. WU.com customers generally send money to support family members, as gifts, and/or for emergencies.

Top 5 Digital Money Transfer Providers

The vast majority of WU.com’s transaction volume is incremental business to Western Union, and not a result of cannibalization. Over 80% of WU.com customers are new to Western Union, as measured by the fact that they did not make a retail C2C transaction through WU in the past 2 years. In addition, WU.com is appealing to a different demographic. The digital customer base is more affluent, more banked and more tech-savvy than WU’s retail C2C customers. Millennials make up over 46% of the digital customer base and represent 58% of WU.com transactions initiated on a mobile phone. WU’s mobile app has been downloaded by more than 3 million people worldwide. Mobile customers are the most valuable, as they make the most frequent transfers, due to the ease and convenience of using a mobile app.

WU.com currently offers digital money transfer capabilities in 41 send countries to the 200 receive countries where Western Union’s retail C2C business has a presence. Management’s long-term goal is for the digital business to cover 200 send and 200 receive countries, matching the coverage of the retail C2C business. WU.com is on track to exceed $400 million in revenues this year and account for ~10% of the C2C segment’s revenues (up from 8% in 2016). Moreover, since 16 of WU.com’s 41 send countries went live in just the past 2 years, WU.com’s current revenue run-rate does not reflect full penetration of its existing geographies. With another 159 send countries left to go live (albeit smaller countries) and aided by Western Union’s 91% brand awareness, it is not hard to see WU.com growing into a multiple of its current size. WU.com experienced 25% constant currency revenue growth in 1H:2017, and 24% in 2016. If WU.com can sustain its current rate of growth, its revenues will double roughly every 3 years.

Self-cannibalization at WU is not a valid concern, as retail and digital are two very different channels. Retail customers are largely un- or under-banked, non-tech-savvy and low-income, whereas digital customers are banked, tech-savvy and more affluent. The most likely scenario over the next 5 years is that WU’s retail C2C business remains flattish at ~$4 billion in revenues or grows modestly (it is difficult to grow a business that has almost 30% market share of a mature end market) while WU.com grows toward a $1 billion annual revenue business.

WU.com Revenues

WU.com also markets its platform as a white-label product, called WU Connect, that other online businesses can plug into to offer digital money transfers to their customers. So far, Facebook, Viber and WeChat have partnered with WU Connect, giving their users the option to send money without leaving their respective websites/apps. This relatively new business for WU has not generated a meaningful amount of transaction volume, and WU management believes that the social media/messaging channel is not one through which many people will ultimately want to send money. Nonetheless, WU Connect is a forward-looking innovation, protecting WU.com’s moat, and highlighting Western Union’s first-to-market leadership in any potential new channels.

MoneyGram’s Takeover Puts a Value of a Global Retail C2C Money Transfer Business

The recent bidding war for MoneyGram underscores the attractiveness of a global money transfer business (MGI shares traded at ~$6.50 in October 2016, Ant Financial offered to buy the company for $13.25 in January 2017, Euronet bid $15.20 in March, and Ant Financial raised its bid to $18.00 in April). As the world’s #2 retail C2C money transfer provider, with ~5% global market share (~11% of retail/digital), MoneyGram holds a solid position as a “value” option for consumers and consistently prices below Western Union’s pricing umbrella. Despite its stable market position and decent brand, MoneyGram is not in the same league as Western Union with respect to business quality. WU’s competitive advantages over MGI include having (1) ~2.5x MGI’s market share and more than triple its revenues, (2) a +1,000 bp advantage with respect to EBITDA and FCF margin, (3) a far superior brand, and (4) no exposure to Wal-Mart versus 18% exposure for MGI.

Western Union vs. MoneyGram

In its 2016 10-K, MoneyGram disclosed that it generated $194 million in digital revenues (representing 12.5% of the revenues of its Global Funds Transfer segment). However, MGI’s digital revenues include moneygram.com, mobile solutions, account deposit and kiosk-based services. I view the former two businesses as true digital businesses, and the latter two as extensions of the retail C2C business. MGI does not disclose the revenue split among these businesses, but I suspect the kiosk-based business represents a substantial portion of digital revenues since MGI rolled out this offering long before its digital and mobile offerings. I believe MGI’s revenues from true digital businesses are a small fraction of WU.com’s $345 million in revenues in 2016.

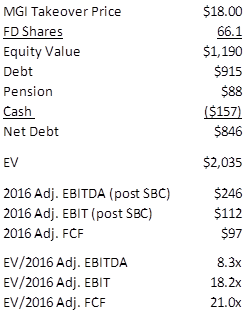

MoneyGram’s takeover valued it at 8.3x EV/LTM EBITDA, in line with WU’s current public market valuation. However, given MGI’s comparatively poor FCF conversion (39% FCF/EBITDA vs. 64% for WU, and 5.9% FCF/revenues vs. 16.2% for WU), I believe EV/FCF is a better metric for valuing both companies. MGI’s takeover value equates to 21x EV/FCF, while WU currently trades at 15x EV/FCF. Applying MGI’s takeover multiple to WU’s 2016 FCF results in a private market value for WU of almost $34, or +80% above the current share price, and implies an EV/EBITDA multiple of 13.5x. While such upside to PMV for WU may appear aggressive, MGI is being taken over at an ~170% premium to its share price of several months ago. In addition, 13.5x EBITDA does not appear as an excessive takeover valuation for a dominant, hard-to-replicate global asset like WU, which controls +50% its industry’s profitability.

MoneyGram Takeover Valuation

PayPal’s Acquisition of Xoom Puts a Value on a Digital Money Transfer Business

In November 2015, PayPal completed the acquisition of Xoom Corporation, the #2 digital money transfer provider. Xoom was founded in 2001 in San Francisco and was backed by VC firms including Sequoia Capital. The company went public in February 2013 at $16.00 and was acquired 2½ years later for $25.00, or an equity value of just under $1 billion. At the time of the acquisition, Xoom was entirely a U.S. send business (it offered digital money transfer service in the U.S. only) with just 37 receive countries. Xoom’s CEO, John Kunze, stated that the motivating factor behind the deal was PayPal’s global presence, as the acquirer’s know-how and relationships with banks around the world would help Xoom grow more rapidly. According to Xoom’s website, today, its service has been expanded to 63 receive countries under PayPal.

Xoom achieved an impressive valuation in its takeover: 4.8x EV/LTM revenues and 65x EV/LTM adjusted EBITDA. In using the Xoom deal as a precedent transaction for WU.com’s valuation, I’d note a few differences: (1) in 2015, WU.com’s revenues were almost 70% greater than Xoom’s (which should translate into higher margins for WU.com as scale is crucial for a money transfer business), (2) WU.com was growing faster than Xoom at the time of Xoom’s takeover (in the 9 months ending September 2015, WU.com’s revenues grew by 20% while Xoom’s grew by 15%), (3) WU.com already benefits from Western Union’s global presence, while Xoom had to sell to PayPal to facilitate its global expansion, and (4) WU.com is presently offered in 41 send countries and offers 200 receive countries on its way to 200/200. Xoom is presently offered in 1 send country (the U.S.) and offers 63 receive countries. I do not believe that Xoom will ultimately achieve WU.com’s targeted level of global coverage.

Xoom Corporation Takeover Valuation

The Bear Case

Western Union remains heavily shorted (short interest stands at ~14% of the float, and 12 days to cover) even after the bidding war for #2 competitor MoneyGram drove MGI shares up by ~170% in a matter of months. WU’s bear case states that digital money transfer providers will disintermediate WU’s high-margin, ~$4 billion-in-revenue retail C2C business. The bear case further states that the world is moving toward a cashless society in which more and more people will have smartphones and fewer people will need to walk into a retail money transfer location and pay WU’s high fees (WU’s C2C transaction + FX fees in 2016 averaged ~5.5% of principal) to transfer money overseas. As a result, WU will see a decline in transaction volume, pricing, or both. Short sellers see the digital money transfer industry as a collective Amazon.com and Western Union’s retail C2C business as a slowly dying brick-and-mortar retailer.

Many fintech startups have gained VC funding to go after the large opportunity in the $575 billion (in cross-border principal) global remittance market. Some of these startups have grown rapidly, but they have largely gained share from the banking industry, which controls ~55% of the global money transfer market, and have gained very little share from WU. Customers of digital money transfer providers are wealthier, more banked and more tech-savvy than WU’s international migrant customer base in retail C2C. I believe confusion, as well as inaccurate media coverage, has led some investors to erroneously conclude that digital money transfer is taking market share from WU.

For example, TransferWise, a UK-based startup, made a splash in 2014 when it attracted investment capital from Sir Richard Branson, founder of Virgin Group and a serial disrupter. TransferWise offers low fees because it doesn’t actually transfer money: it acts like a matchmaker for people looking to send cash overseas. When a customer in the U.S. wants to transfer funds to, say, India, TransferWise receives the money in the United States in USD and looks for a customer in India who is looking to transfer rupees to the U.S. Since no bank ever gets involved and money doesn’t actually cross national borders, TransferWise is able to charge very low fees (just 1% transaction fees for U.S. customers, as well as better deals on FX). TransferWise has grown rapidly and currently has a revenue run-rate of ~$120 million annually. However, TransferWise is primarily gaining share from banks. In order to use TransferWise, both the sender and receiver need a bank account (a rare occurrence in a typical Western Union retail C2C transfer). In addition, TransferWise takes one business day to pay out to the recipient, which is quicker than a bank transfer but much slower than WU’s “money in minutes” global standard. I see little overlap between TransferWise and WU’s end markets; instead, I see misguided opinions about the former disrupting the latter. Exhibit A is a Yahoo! Finance article on TransferWise that begins with the following claim: “Look out, Western Union. A new startup is making it easier—and a lot cheaper—for Americans to send and receive money overseas and it’s attracted funding from big name investors like venture capitalist Peter Thiel and Virgin Group founder Sir Richard Branson.” However, in a recent video interview with Yahoo! Finance, TransferWise’s CEO, Taavet Hinrikus, set the record straight on his competition: “But really if we think about competition, competition for us is banks. It’s the Citibanks of the world; it’s the HSBCs of the world. When we ask our customers ‘how did you do international payments before you learned about TransferWise?’ it’s about the banks, and then a little bit about Western Union.” (This quote accurately reflects what Hinrikus said in the video interview, but the article misquotes him as saying, “If you ask our customers how they used to send money to another country, it was their bank or Western Union.”)

I see two large holes in the bear case. First, it erroneously assumes that digital money transfer providers are targeting WU’s un- or under-banked, non–tech-savvy and low-income international migrant customer base (which is like saying that American Express is targeting Wal-Mart’s customers with its charge cards). In reality, digital money transfer growth is coming largely at the expense of the banking industry, which charges the highest fees for money transfer. But with money transfer fees representing a tiny fraction of revenues for banks, it is hard to see this erosion taking place. A World Bank study of 365 corridors found that the average cross-border money transfer fee (transaction + FX) to be 10.99% for banks, compared to 6.23% for money transfer operators (“MTO”, such as WU and MGI) in 2Q:2017 (see the following chart). Mobile operators, such as WU.com, charged the lowest rates, at 3.29%. The global average fee (among banks, MTOs, post offices and mobile operators) was 7.32%. As stated above, Based on data that Western Union’s overall (transaction + FX) fee was ~5.5% in 2016, which is a blend of its (higher) retail and (lower) digital pricing. I my personal view WU’s fees seem fair for its ability to deliver “money in minutes” across the globe (banks typically take a couple of business days to transfer money.) Second, the bear case ignores the fact that Western Union has built the world’s largest and widest-reaching digital money transfer business (WU.com), with almost 2x the revenues of its next largest competitor. WU.com is the biggest disrupter of bank-based money transfer, and there is little evidence that WU.com is cannibalizing WU’s retail C2C business which is primarily a cash-to-cash business. In addition, industry pricing has been stable for the past couple of years.

Average Money Transfer Fee by Industry, Q2 2017

Average Money Transfer Fee By Industry, Past 9 Years

Note: MTO = Money Transfer Operator. The above data covers 48 send countries and 105 receive countries, for a total of 365 corridors.

Source: World Bank

Regarding the view that cash will disappear and all payments will be digital, cash still remains the #1 form of payment in the U.S. Cash accounted for 32% of U.S. consumer transaction in 2015, albeit down from 40% in 2012, while debit and credit cards made up 27% and 21%, respectively. Moreover, cash represents a larger percent of payments in the rest of the world. I don’t believe in absolutes. While cash will continue to decline as a form of payment globally, I don’t think it will entirely go away in the next 50 years. With mobile phones, there is no need for landline phones, yet most people still have a landline in the office. In emerging markets, landlines in the home are still common. WU is a global company and it’s often important for investors in developed markets to bear in mind that much of the world looks like we did 20 years ago.

The Approaching End of WU’s Intercompany Working Capital Program Is Not a Major Concern

Through a creative (and legal) intercompany working capital program, WU has been able to access all of its global FCF and has been returning nearly all of its global FCF to shareholders through dividends and share buybacks in recent years. However, this process is not indefinite, and WU’s ability to return ~100% of FCF to shareholders will be impacted in the medium term.

Since all of WU’s debt is in the U.S., WU’s U.S. FCF is nil after interest and corporate expenses. From its ~$1 billion in annual CFFO, the Company repatriates ~$250 million annually, largely from high-tax jurisdictions so that repatriation taxes are minimized. To access the rest of its CFFO (~$750 million annually) without paying repatriation taxes, WU makes use of intercompany working capital programs. Rising intercompany accounts payables balances essentially allow WU to create an untaxed source of cash as long as the balance keeps growing. For example, if a B2B client wants to send $1 million from the United States to Argentina, instead of transferring the money immediately, WU receives the $1 million in the U.S. and has its Argentine subsidiary pay the equivalent amount in Argentine pesos (less fees) to the recipient. An intercompany payable of ~$1 million is then created between the U.S. and Argentine subsidiaries, which is paid off ~30 days later. However, within those 30 days, new transfers from the U.S. to Argentina are handled in the same manner, and the total payables balance rises. WU applies such programs globally. As long as the overall payables balance (the amount the U.S. subsidiary owes the various foreign subsidiaries) increases, an untaxed source of cash is created in the U.S., equal to the dollar-amount growth in the intercompany payable each year. This is no different than a company stretching out payables to its suppliers and creating a source of cash.

WU began this program in its C2C business. Recently, when the C2C intercompany payables balance reached a peak and stopped growing, WU extended the program to its B2B business, giving the program a longer life. But at an investment conference in late 2016, CFO Raj Agrawal stated, “We have another 2-3 years on the intercompany working capital programs.” By the end of 2019, I believe that WU will not be able to continue growing its intercompany payables balance. The Company discloses data about this program annually in the “Parent Company Only” financial statements at the back of its 10-Ks. While other small items are captured in the following line items as well, for the most part they reflect the effect of the program. “Payable to subsidiaries, net” largely captures the overall intercompany payables balance, which grew from $99 million at the end of 2011 to ~$3 billion at the end of 2016. “Advances from/(to), net” mostly captures the change in that payables balance. As the following table shows, WU significantly ramped up the program in 2014-2016, creating a cumulative (untaxed) source of cash of ~$2.6 billion in the U.S.

WU Intercompany Working Capital Program

Many global companies utilize intercompany working capital programs, but since WU is a remittance business, its program has a much larger impact, as it is able to create intercompany payables with principal balances while other businesses can only utilize revenues. Since the principal that WU transfers around the world is a multiple of the revenues it generates in transaction and FX fees, the company benefits from a multiplier effect on its program compared to non-remittance businesses.

The approaching peak of WU’s intercompany payables balance (likely to be reached by the end of 2019) is not the end of the world for WU. WU has several options to compensate: (1) WU could repatriate more foreign FCF to the U.S., but this would result in a higher tax rate and less after-tax FCF available in the U.S. than achieved through its working capital program. (2) The Company could close on an acquisition of a remittance business with substantial U.S. outbound volume, allowing it to extend the working capital program to the acquired company and continue growing the overall payables balance (for a finite period). The 2011 acquisition of Travelex Global Business Payments got WU into the B2B business and allowed it to extend the intercompany working capital program to B2B once it had peaked in C2C. (3) WU could also take on increasing debt and continue returning large amounts of capital to shareholders. Management has stated that it would reevaluate the Company’s investment-grade credit rating in the event the working capital program came to an end. WU is underleveraged at just 2x net debt/EBITDA. WU could easily support up to 3.5x leverage, giving it an incremental ~$2 billion in debt capacity, or ~22% of its market cap, for share repurchases. With WU buying back ~$500 million annually in recent years, $2 billion in incremental debt capacity would allow it to continue its current pace of share buybacks for another 4 years. (4) Potential corporate tax reform may allow U.S. companies to repatriate foreign FCF at favorable tax rates going forward.

In a worst-case scenario, WU’s dividend would not be impacted, but WU would have less FCF available for share repurchases than it does today (~$500 million annually). I don’t expect this to impact WU’s valuation, as most U.S.-based multinationals do not access all of their global FCF (Apple and Oracle, for example, compensate for their rising overseas cash balances by taking on debt in the U.S., in line with overseas FCF, to fund share repurchases). I haven’t observed much of a valuation discount for U.S.-based multinationals with large amounts of cash trapped overseas versus largely domestic companies.

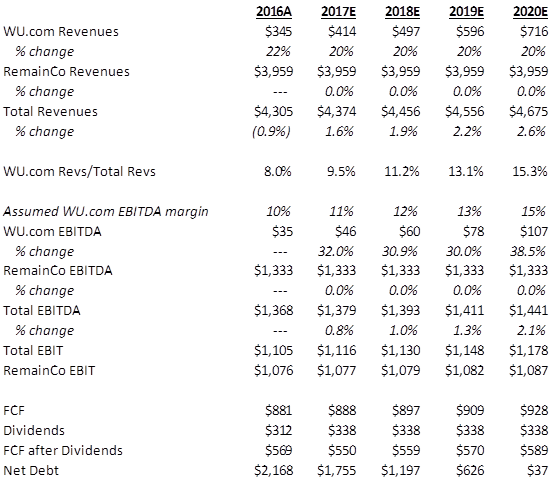

By 2020, WU Should Deliver 10%-13% EPS Growth, Driven by WU.com

WU.com’s rapid growth, combined with its increasing share of WU’s revenues, is having an ever-growing impact on WU’s revenue growth. I’ve assumed 20% revenue growth for WU.com going forward. By 2020, WU.com’s revenues will account for 15% of WU’s overall revenues (up from 8% in 2016). With 20% revenue growth, WU.com alone will contribute 300 bps to WU’s overall revenue growth in 2020. This is a substantial positive for a business that has experienced flattish revenues for the past 5 years. More important, CFO Raj Agrawal recently stated that WU needs mid-single-digit top-line growth to experience margin expansion. If WU’s RemainCo businesses can collectively grow revenues by just 1%-2% annually, WU would experience operating leverage and therefore accelerating EPS growth. This scenario is not difficult to attain; in fact, FX is masking the fact that RemainCo delivered 1.1% and 2.8% constant currency revenue growth in 2016 and 2015, respectively. With the potential for ~5% revenue growth in 2020 and beyond (driven by WU.com), WU could sustain 10%-13% EPS growth, depending on the amount of share buybacks it is able to engage in after its intercompany working capital program peaks. Under this scenario, WU should trade at a substantially higher valuation than its current 11x P/E and 8.3x EV/EBITDA, which reflects its short-term outlook for flattish EPS growth. All WU needs is for FX to become a neutral factor. If FX swings to a tailwind, WU could deliver 13%-20% EPS growth in 2020. In addition to being fundamentally undervalued, WU is a low-risk way to profit from USD weakness.

Recent News

Over the past 2 years, WU has endured a string of macro headwinds. Unprecedented USD strength in 2015 and 2016 not only haircut WU’s revenue and EPS growth but also created the appearance that WU is a declining business. C2C principal transferred appeared to decline in both 2015 and 2016 (see the following table), but it is important to keep in mind that principal transferred is measured in USD and the apparent weakness reflects lower values as measured in USD. These apparent declines give the shorts (false) evidence of digital disintermediation.

WU C2C Principal Transferred ($ billions)

More recently (3Q:2016 to 2Q:2017), WU was further impacted by the delayed effects of lower crude oil prices. Sharply reduced infrastructure spending in Saudi Arabia and the UAE resulted in a decline in the largely Indian migrant workforce in those countries and thus lowered remittances by that population to family members back home. In addition, India’s demonetization in late 2016 (~85% of the country’s banknotes were demonetized in an attempt to curb corruption and black market transactions) further pressured remittances into that country. All told, WU’s Middle East, Africa, and South Asia region (“MEASA,” which accounted for 17% of C2C revenues) exhibited a 13% revenue decline in 1Q:2017 (down 10% in constant currency). However, when removing this geography as well as WU.com and its 28% constant currency revenue growth (accounting for 9% of revenues), WU’s remaining retail C2C business (accounting for 74% of retail C2C revenues) exhibited 1.2% constant currency revenue growth in 1Q:2017. Aside from transitory macro headwinds, WU’s retail C2C business appears healthy and is exhibiting no signs of disintermediation.

In January 2017, WU reached a joint settlement with the U.S. Department of Justice and Federal Trade Commission relating to the Company’s oversight of certain agents from 2004 to 2012 and whether its anti-fraud and anti-money laundering controls adequately prevented misconduct by those agents. This year, WU will pay $601 million to settle the investigation, as well as an additional $100 million to settle an IRS tax dispute from 2011. As a result, the Company will generate about $200 million in CFFO this year, well below its historic rate of ~$1 billion in annual CFFO. However, WU will not reduce its historic pace of share repurchase (~$500 million annually), as it has raised debt in 1Q:2017 to fund the settlements (taking net debt/EBITDA to 2.0x from 1.6x). WU always appears under-leveraged and it now seems that management was preparing the balance sheet to absorb a sizable settlement. WU recently increased its share repurchase authorization by $1.2 billion, to $1.5 billion (16% of its current market cap), and management stated that the buyback would be completed roughly evenly over the next 3 years. WU also increased its dividend by 9% in February 2017 to $0.70 annually (3.7% yield).

2Q:2017 Marked a Turning Point

WU’s last quarter revealed the first green shoots of the company’s accelerating growth story. Adjusted EPS came in at $0.50, substantially ahead of the $0.42 consensus and 13% better than a year ago. This was a big improvement from the flattish EPS WU has been delivering for years. The largest source of the strength was lower expenses (more on this below). Management raised 2017 guidance to $1.70-$1.80 (previously $1.63-$1.75). Midpoint guidance, which is flat with 2016 EPS of $1.75, appears very conservative. 1H:2017 EPS of $0.86 was up 6% vs. a year ago. For full-year 2017 EPS to come in flat with 2016, 2H:2017 EPS has to be down 5%. This is highly unlikely given that (1) 2H:2016 EPS was depressed due to weakness in oil-related markets and India’s demonetization, 2) WU has continued shrinking its share count (down 4% yr/yr in 2Q:2017), and 3) H2:2016 EPS was 16% higher than H1:2016, even with weakness in the Middle East and India. A similar seasonal pattern this year will result in 2017 EPS of $1.85. The stock trades at 10x.

After disappointing shareholders for some time, it seems that management is low-balling guidance (2017 original guidance called for down EPS). In addition, due to the unprecedented revenue headwinds WU faced in the last couple of years, management became very focused on what it can control: expenses and customer satisfaction. Through a new program called WU Way, WU is implementing lean management techniques, consolidating IT, automating certain compliance processes, has taken severance actions, has negotiated lower commissions with its agents and is focused on improving customer retention. The end result should be that WU operates more efficiently and with a lower customer lapse rate. WU’s recent deal with BP Australia, where it offers 24hr service at 300 BP gas stations across Australia, will be expanded to other countries. The added convenience of 24hr cash money transfer capability should allow WU to gain some share and/or improve retention.

In 2H:2017, WU begins to lap the weakness it experienced in oil-related geographies and due to India’s demonetization. Recent USD weakness also bodes well. All told, a break-out scenario is brewing where WU is cutting costs aggressively, macro headwinds will soon be lapped, and WU continues to shrink its share count (down 4% yr/yr in 2Q). Trading at 11x 2017 EPS guidance (more realistically, 10x), with just 16% of the sell-side having a Buy rating (48% are at Hold, and 36% at Underweight/Sell) and a large, misguided short position (12 days), WU’s accelerating growth profile could set up a rapid upward revaluation of its shares.

An LBO attempt by PE is also possible as the bidding war for MoneyGram likely drew attention to the industry, and WU sticks out like a sore thumb. WU shareholders are frustrated. After 11 years of the stock going nowhere, many would likely give the company away for a 15%-20% premium. All PE would need to do is own WU for 3 years, deleverage the balance sheet, potentially divest the C2B and/or B2B businesses, and bring it back public in 2020 as a growth stock with WU.com driving the growth. If I worked in PE, I’d be working 24/7 to set up this deal (it would require a consortium of funds given the +$11B EV). But since I don’t, shareholders should vote against a potential LBO that tries to steal the company.

Projections

To estimate WU’s intrinsic value I’ve made more conservative projections than in the scenario described earlier (10%-13% EPS growth in 2020) to account for potential additional macro headwinds. I’ve assumed that all of WU’s growth comes from WU.com, and projected 20% revenue growth out to 2020, a deceleration from 25% constant currency growth in H1:2017. I’ve assumed WU.com will experience modest margin improvement (natural for a scalable business), from an estimated 10% EBITDA margin in 2016 to 15% in 2020. For the RemainCo businesses (Retail C2C, C2B and B2B), I conservatively assumed flat revenues and EBITDA out to 2020. I’ve also assumed that the dividend remains constant at $0.70, and that WU simply pays down debt with its post-dividend FCF. At the end of 2020, WU is essentially debt-free.

Financial Projections

Intrinsic Value

I valued WU.com at 3.5x revenues, a discount to Xoom’s takeover multiple of 4.8x revenues. By the end of 2020, WU.com will account for 28% of WU’s then EV, up from 11% in 2016. When stripping out the value of WU.com, Western Union’s RemainCo businesses have an implied valuation of just 4.9x EV/EBITDA, 6.0x EV/EBIT and 7.5x EV/FCF at the end of 2020, a large discount to MoneyGram’s takeover valuation (8.3x, 18.2x and 21x, respectively).

Implied Valuation of RemainCo with WU.com Valued at 3.5x Revenues

In estimating WU’s intrinsic value at the end of 2020 I applied a 10x EV/EBITDA multiple to RemainCo, which equates to 12.3x EV/EBIT and 15x EV/FCF (a discount to MGI’s 18.2x EV/EBIT and 21x EV/FCF takeover valuation). At 3.5x revenues, WU.com’s implied EV/EBITDA multiple is 23x, a substantial discount to Xoom’s 65x in its takeover. All told, WU’s sum-of-the-parts equates to an overall valuation of 11x EV/EBITDA, 13.4x EV/EBIT and 17x EV/FCF at the end of 2020.

Intrinsic Value at the end of 2020

I get a conservative fair value of almost $33 at the end of 2020, offering upside of 75%, or a 3.5-year IRR of 21% including the dividend (3.7% yield). WU currently trades near the high end of its historic dividend yield range. WU’s peak dividend yield of 3.95% was set in late 2012 after a 33% plunge in the stock due to the company reporting that C2C pricing reductions would be necessary in certain corridors to remain competitive. WU’s current dividend yield suggests an almost similar level of concern despite the fact that pricing has been stable for the past 3 years.

WU Dividend Yield

Risks

-

Although to date, there is little evidence of WU.com and other digital money transfer providers’ cannibalizing WU’s retail C2C business, cannibalization could pick up speed in the future if digital money transfer technology somehow penetrates the international migrant population more deeply.

-

Despite WU’s industry-leading compliance efforts, there is always the risk that terrorist, money laundering or fraud activity could become an issue and temporarily tarnish WU’s brand.

-

Anti-immigration sentiment could lead to possible limits on immigration in certain countries, negatively impacting WU’s traditional customer base.

-

WU’s intercompany working capital program will peak by late 2019, and the Company might not be able to fully replace this source of cash, resulting in a reduction in FCF available for share repurchase.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

- (While I dislike this kind of language) WU will "beat and raise" in H2:17.

- EPS growth will accelerate to 10%-13% sustainable growth by 2020 (conservatively) after a few years of flattish growth. WU is priced for perpetual flattish growth.

- WU makes for an attractive LBO candidate.

| show sort by |