| 2017 | 2018 | ||||||

| Price: | 3.42 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 108 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 379 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 348 | EBIT | 0 | 0 | |||

| TEV (in $M): | 727 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- eDreams ODIGEO EDR SM 12/22/2022

- eDreams ODIGEO EDR SM 10/20/2021

- BETA

- Wadell Reed WDR 04/08/2020

- BOOKING HOLDINGS INC BKNG 01/17/2020

- BOOKING HOLDINGS INC BKNG 10/07/2018

- HOUSTON WIRE & CABLE CO HWCC 02/14/2018

- ALPHABET INC GOOGL S 06/29/2022

- PUBMATIC INC PUBM 04/29/2022

- EXPEDIA GROUP INC EXPE 03/30/2019

- I3 VERTICALS INC IIIV 12/08/2021

Description

Summary

eDreams ODIGEO, S.A. (EDR SM / BME:EDR), (“eDreams”, “the Company”) is the market-leading online travel agency (“OTA”) focused in Europe. The Company is a broken IPO from 2014 whose public equity has been left for dead while the business has improved materially on numerous fronts with the help of a new management team. The sell-side isn’t fully tuned into the changes that have taken place, while investors remain gun shy after being burned post-IPO. Credit markets signal immense confidence in the business at a 2.2% YTW on the bonds, yet the equity trades at a high-teens yield on a growing FCF stream.

While the Company has been considered “cheap” for some time, over the past three weeks there have been three material events that have de-risked the business and provided a more visible line of sight to value realization. The Company (1) settled its longstanding suit with Ryanair, (2) raised both 2018 and 2020 Adj. EBITDA guidance, and (3) announced the hiring of Morgan Stanley to review strategic options. Despite rallying ~40% on this news, eDreams still trades at less than 7x EBITDA compared to other OTAs Expedia, Priceline, Ctrip, TripAdvisor, and WebJet that all trade in the high-teens or higher multiples.

Further, the OTA space has been fraught with M&A activity over the past 4 years, with numerous transactions have gone off in the range of 10-20x EBITDA.

Assuming that the Company is taken out at just 9x management’s 2018 Adj. EBITDA guide, shares would trade to €6.31 per share, or 85% upside. Given conversations with management, a sale seems likely in the next 12 months.

Though seeing a high probability of a sale well above the current price given numerous potential suitors, if a sale should not go through, downside is protected through an undemanding valuation, continued business improvements, FCF generation, and debt paydown that will accrue to the equity.

Note low float of ~250,000 shares traded daily at €3.42 per share implies €855,000 in value traded daily.

Company Overview

eDreams ODIGEO was created via the merger of eDreams with Go Voyages and Opodo in 2011, facilitated by PE firm Permira Advisers. eDreams is the largest online travel agency (OTA) focused in Europe. The Company served over 17mln customers in 2015, operates in 44 countries, and is growing market share as the industry is highly fragmented across a variety of regional players. The Company holds five brands: eDreams, GO Voyages, Opodo, Travellink, and Liligo. These were each acquired in line with the original IPO’s intention of rolling up the European OTA industry. Though each was individually managed rather haphazardly, new management has substantially consolidated the bank ends of each of the platforms.

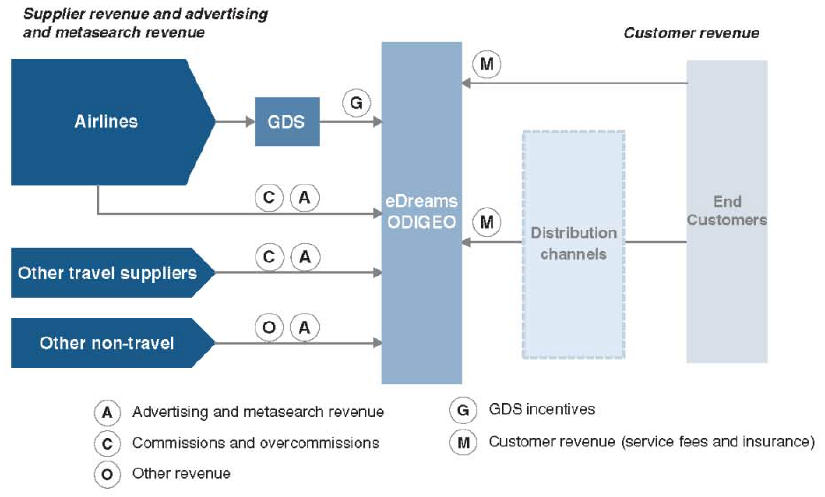

Of OTAs, there are two models: merchant and agency. eDreams is an agency model in that it generates commissions via the sale of flights and hotels. Expedia is an example of the merchant model, in which OTAs purchase flights and hotels in bulk at a discount and hope to re-sell them to customers at a higher margin.

The Company earns revenue primarily from customer fees (79% total; 50% on flights and 29% on hotels, trips, and cars), secondarily from suppliers (14% via airlines and GDSs) and a growing portion from advertising and the meta-search business (7%).

Customer revenue is earned through service fees, mark-ups, insurance revenue, and other fees. The Company charges an average take rate of 9% relative to peers at 6-9%. In the US, flights get 2-3% due to the concentration of the industry, while US hotels gather anywhere from 15-30%. eDreams’s take rate results from a combination of best-in-class technology and scale, which simply offer more value to customers, as well as the fragmented European air travel market. Further, the Company has been amassing customer data, which allows it to price more effectively on an individual customer basis based on previous bookings. Every time the customer comes back to the platform, eDreams obtains more information which feeds this loop.

On a $100 booking, the Company saves customers on average ~$40, of which the Company takes $9. Based on average round-trip ticket values, eDreams saves €134 per customer, per trip.

Supplier revenue is linked to volumes, and is earned through commissions and over-commissions based on year-end targets being met. The Company currently has agreements in place with over 100 airlines out of about 450 in Europe, while payments from GDS’s (Amadeus, Sabre, Travelport) for bookings mediated by eDreams, and commissions from white-label partners. Management noted to us that some of their incremental confidence contributing to the increased 2020 EBITDA guide was in renegotiated and new contracts on the supplier side.

The company is increasingly becoming a full-service OTA, shifting from its historical focus on flights to include hotels and car rentals (consisting the “revenue diversification ratio”). The Company serves four “principle areas” / geographies which form two segments: Core and Expansion.

Business Segments

Flight (79% of 2017 revenue)

The Flight segment sells flights through every major airline in Europe. In some scenarios (supplier revenue), eDreams has agreements in place with airlines to earn commissions on booked flights. In most scenarios, the fees are charged directly to the customer.

Non-flight (21% of 2017 revenue)

Non-flight revenues include hotels and car rentals, as well as the advertising and metasearch businesses. Liligo is the metasearch business, which is best explained by CEO Dunne,

"The success story, which is Liligo, our metasearch business. Liligo is an acquisition that is working well, that is expanding geographically and into multi-modal. Multi-modal is the concept of within one set of search results combining different forms of transportation such as bus, car sharing, train and flight. Liligo is the leader in France and is present in 11 countries and expanding. In total, our advertising and metasearch business is growing by 37% year-on-year."

Ownership

Private equity owners Premira Advisors and Ardian own a combined 48% of the shares outstanding. The next largest holder HG Vora owns 4.94%. Institutions own just 13.4%, with HG Vora being the only hedge fund owner per CapIQ.

Investment Thesis

eDreams is a market leader in the online travel agency industry in Europe. The business is asset-light with scale advantages and network effects.

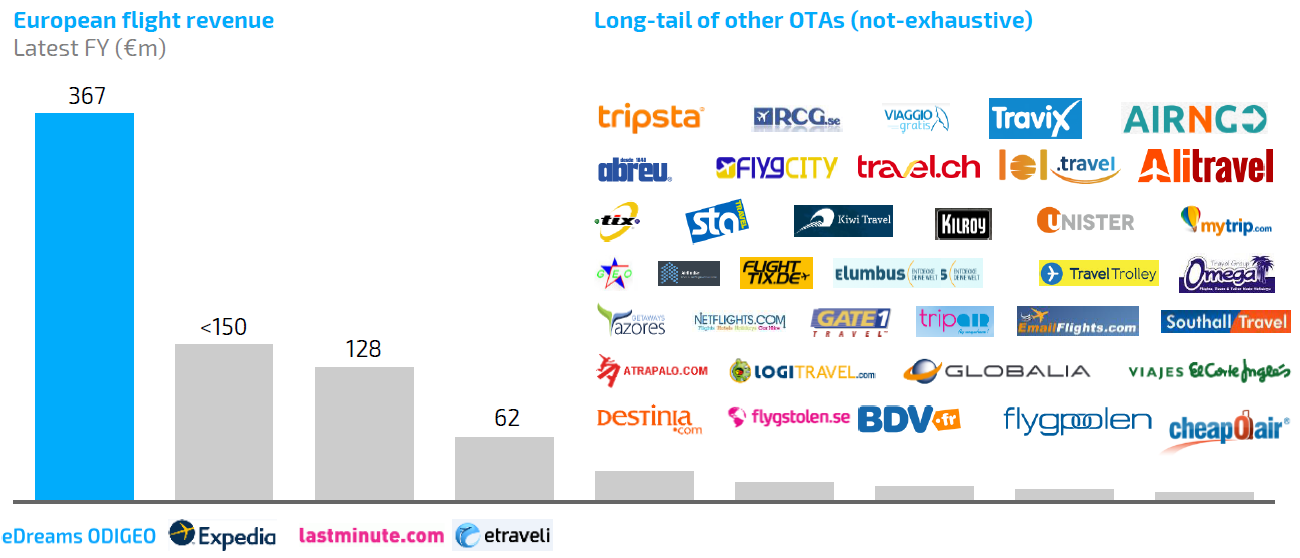

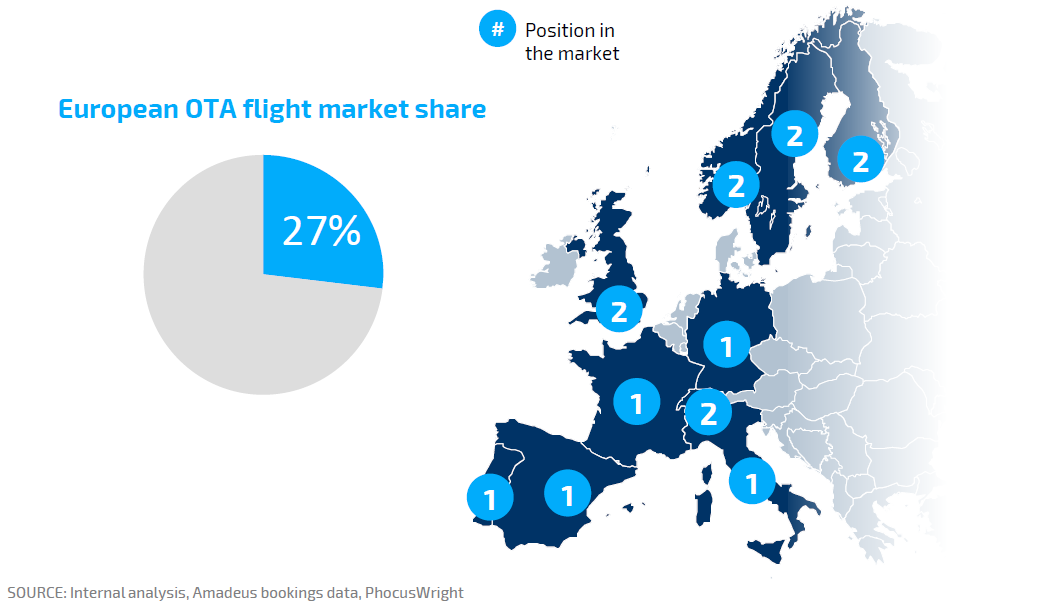

The Company has #1 or #2 positions in all European markets, and a 27% share overall. eDreams' Europe flight revenue was €367mln in 2016 relative to Expedia's €150mln.

There is a flywheel effect in that the Company's scale leads to more bookings, leading to higher margins, which allows for more investments to be made in technology and marketing, hence bettering the brand and bringing more customers, driving further scale leadership. This leadership can be seen as eDreams currently employs over 400 engineers vs. an average of ~30 across other regional European players.

While eDreams competes against EXPE, PCLN, and LMN, the Company is still gaining share at the expense of these smaller players. Examples of these include: Bravofly, Lastminute, Gotogate, Unister, Travix, and Travelgenio. This share gain is due to the underlying strength of the Company’s tech. These other OTAs are startup-like in nature with a constant need for capital (VC dollars).

European industry dynamics are unlike those in the US, leading investors to be wary of the value-add that the business provides.

While US-based OTAs focus on the hotel business which brings higher profitability, eDreams is focused on the low-margin flight business. Investors mistakenly believe that this is a salient factor in the valuation of the business. However, the European industry structure with respect to flights is much different than in the US. In the US, the top four airlines control ~75% of seats flown, while in Europe, this figure is just 29%. In the US, 80% of flights are domestic, while in Europe, 80% are international.

eDreams offers flights from ~450 airlines. This means that there are a variety of different options for customers, many of which they may or may not actually be aware of; eDreams provides value by connecting customers with these available options. In Europe, it's not as simple as simply pulling up Google Flights where one can see predominantly all options in United, Delta, American, (and Southwest) on one page. CEO Dana Dunne provided an example on the Q3 2016 conference call,

“So just one simple small example would be Pegasus, right. A very, very credible, very important airline that flies to Turkey but most people wouldn't know that, people sitting in London they would want to fly to Istanbul, necessarily wouldn't know of Pegasus at all. So again the competitive landscape is very different structurally. And so therefore, structurally for us, we continue to provide real value to customers for it. That's why we invest in our platforms, we invest in features and functionality, we invest in things that set us apart from the airlines and provide real values that customers want to come to us as opposed to going any place else. And particularly again in European context, where we're a very strong brand, customers do really benefit from that and like that.”

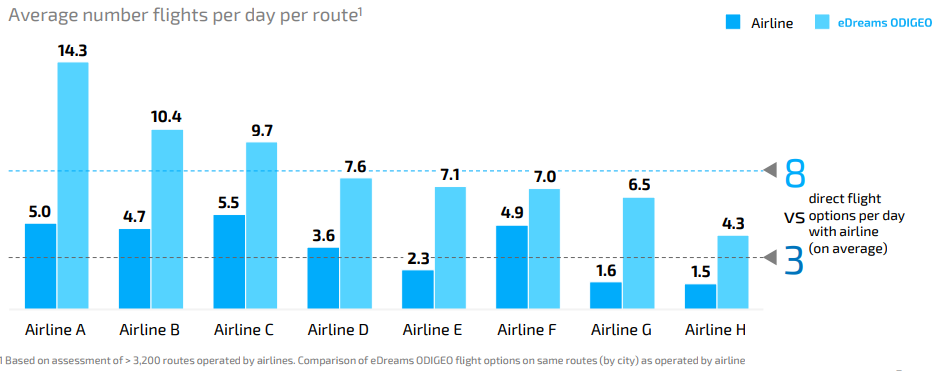

As shown below, eDreams offers more than 2x the options on average, than what is provided by direct. Thus, despite the LCCs’ push to direct, eDreams still provides value. Though not disclosed, our channel checks suggest that multi-legged flights are a significant portion of bookings. eDreams provides tremendous value here as the platform can piece together legs from multiple airlines that the customer is otherwise unable to discover via direct booking. eDreams then saves time via a singular booking process.

Investors may also be unduly worried over airline consolidation as a threat to this industry structure. However, even if the top 5 airlines in Europe purchased the next 6th through 10th largest airlines, the aforementioned 29% figure would expand by just 7% to 36% of seats flown. Though the Company no longer discloses, an older presentation cited the top 2 airlines at 11% of bookings (likely Lufthansa and Ryanair), with a long tail below. Our conversations with management indicate that the concentration remains roughly the same today, with no single airline representing over 10% of bookings or revenues.

Prior management missteps and questionable business practices caused the stock to rightly fall from highs. However, new management is in place and has been righting the ship.

Missteps – Google Algorithm:

eDreams was founded by Javier Perez-Tenessa in 2000, and in April 2014, the Company went public at €10.25 per share. Just two months later in June 2014, the Company stated that 2015 EBITDA would be “difficult to discern” due to changes to Google’s search algorithm and rising competition. Shares fell 36% to €5.65. The impact to 2015 EBITDA was €36mln (28% of total Adj. EBITDA). The CMO at Google discovered a loophole wherein the Company was obtaining AdWords for far below market rates; Google changed the algo without eDreams's knowledge and the Company's margins were destroyed. However, the Company's relationship with Google has improved meaningfully, and the risk of algo changes being detrimental to the business are negligible. The Company is partnered with Google's beta testing, which should aid in ensuring a mutually beneficial relationship. At least once or twice a year, both management teams meet in California. eDreams initiated that relationship in February 2015. Per the Q2 2017 call,

“Just quite frankly, the team had not -- Prior to the new management change, we've not been out there as a company to Google before. Since we've made the change kind of been -- let's say February 2015, our teams have been [ph]out multiple times, I as a CEO have been out three times already, all right. We're building a much closer relationship, because they still are a meaningful partner nonetheless. And we are actually now in beta programs of Google, whereas two years ago, we had never been in a beta program whatsoever, we now are in beta programs. Beta programs are like 15-20 companies worldwide Google chooses to do things.”

The company was once heavily reliant on Google for customer acquisition, as are the other OTAs, but have reduced their reliance considerably. In Q3 2016, the company generated 33% of bookings from Google, while in February 2017, the Company disclosed that they had reduced this figure by 33% to just 22%. Again, the dynamic is similar with respect to the multitude of travel options available; it’s not as easy as simply comparing Delta, United, American, and Southwest. Per Dunne on the Q2 2017 call,

"Look, at the end of day, the customer wants the lowest price, that just tells you the lowest price what Google is offering you. The lowest price can absolutely be found in other places on average, for example, if you go to airline.com, right, the major airlines in Europe to their website airline.com for the same trip, or you come to us on average, you will save €140 return for one passenger."

Missteps – Iberia / British Airways:

In October 2014, the Company’s stock fell 59% in a single day after Iberia Airlines and British Airways said it would no longer market its tickets with eDreams, stating that the Company was, “not fulfilling its obligation to transparently report total ticket prices to clients from the start of the booking process.” The fares were restored to the site three days later.

This came about as the Company's strategy was to lure the customer via advertising low fares initially, then disclosing the fees at the very end of the booking process. Our commentary on the revised strategy is expanded upon in the "Phase I" section below.

Missteps – Ryanair / deceptive AdWords:

In December 2015, Ryanair sued both eDreams and Google for misleading advertising, stating that it has received “numerous complaints from Ryanair customers who were deceived into buying on the eDreams website when they thought they were booking on Ryanair.com.” In speaking with management and former employees, we found that the Company was essentially placing AdWords bids for “Cheap [airline name] flights” (Ryanair included) instead of simply “eDreams” or “cheap flights to Barcelona” for example. The magnitude of this sort of spend was ~80% of total AdWords spend. This was not only deceptive but unsustainable and highly vulnerable to potential algo changes. Conversations also indicated that this policy was largely a result of the former CIO and Head of Marketing who was replaced in early 2015. The policy went with him; currently ~20% of AdWords are airline-specific.

The court ruled against eDreams in November 2016, ordering the Company to display the final price of flights at the beginning of the booking process, including all surcharges. Further, it found that eDreams was overcharging customers on payment fees, and directed the Company to provide a payment option without a charge. Notably, the Company had no agreement with Ryanair in place; all the revenue generated from this practice was via fees charged to customers rather than a booking fee from Ryanair.

As noted, Ryanair settled with Google and eDreams in October 2017. All parties are keeping the conditions of the settlement confidential. Note that prior to the settlement, eDreams was permitted to and has been selling Ryanair flights on its sites.

New management and board member changes has led to refreshed culture:

Founder and former CEO Perez-Tenessa’s strength was in playing all the roles, but this method led to tremendous micromanagement as the Company grew; it’s easy to do with 25 engineers but much more difficult with a team of 2,000. Employees were no longer engaged and often buried relevant information.

Perez-Tenessa was replaced, as Dana Dunne was appointed CEO in January 2015, previously serving as president and Group COO in the Company since 2012, Chief Commercial Officer at EasyJet from 2009 to 2011, and CEO and Head of AOL Europe. Dana was brought in by the PE investors as a likely successor, and though he was with the Company through the missteps, conversations with former employees indicate the dynamic was one of Dana often “biting his tongue” and biding his time.

Further, Dana brought the former CCO from Air Berlin with him to eDreams to work on the supplier side. Philip Wolf was appointed non-executive chairman. Wolf has a variety of experience in the travel industry, most notably founding travel research company Phocuswright and serving as CEO of Travelmation. Skift said that he, “defined online travel for a whole industry.” In March 2015, James Hare, co-founder of the company, resigned from the Board. In July 2015, Amanda Wills and David Elizaga Corrales were appointed as Independent and Executive Directors, respectively. This extends past the c-suite as well; per the Q3 2016 call,

"We recently hired people from eBay, Amazon and a number of other companies. And in addition, our new Head of User Experience was previously in eBay -- Sorry in Amazon as well. In order to improve relationships with Airlines, we brought a new Chief Supply Officer from Air Berlin. And in marketing, we have brought in a number of people, two of the most recent were previously at Expedia and Cheapflights."

The Company has since become far more agile as under Dunne, lower level employees were also empowered to right the ship. Product development teams were shifted as the pre-purchase, post-purchase, and marketing teams began working together rather than being siloed. Currently, there are 5 to 7 people per team working 24/7 on a single product. Changes are released daily and are much more iterative. Per an employee, “the product owner role has grown dramatically … The Company would go weeks without a release previously and then pile too many code changes into one release.” This led to more disruptions than anything value additive. Per Dunne’s presentation at South Summit, product delivery times have come down over 70% in the last 12 months, with a 2-3x increase in the number of A/B tests running.

What was previously a death spiral in terms of talent has become a virtuous cycle that attracts talented engineers and developers.

With missteps now firmly in the past, new management is moving forward, executing the business plan, and guiding expectations higher, but the Street is slow to recognize the full impact.

Phase I – stabilize and transform the business (FY15-16):

In October 2015, the Company completed the rollout of the OneFront platform, which both (1) consolidated the backend of each site while (2) providing a better front-facing user experience. One reason for this change was customer complaints regarding fees that weren’t disclosed up front. The new platform is entirely transparent, which is highly valued by customers.

As of Q3 2016,

"Our web Help Centre is now live in 13 websites including all core markets. In addition, a new contact centre platform has been deployed and is now live in all of our locations. As a result, we have improved significantly the handling of our customers reducing by 20%, the contact rate of service calls and e-mails. In fact, we've reduced our e-mail backlog by 81% and improved responses to customer queries by 11%. Now the majority of our e-mails are answered within 24 hours."

And in the Q4 call, the Company gave an update;

“Overall, these initiatives have led to an 8% rise in customer service availability at eDreams, and an 8% increase in customer satisfaction as well, and a 11% improvement in how promptly we respond to customer enquiries. And at the same time as all this, our service cost per booking has fallen by 10%."

Increased transparency has been brought to all areas of the business, most importantly in the customer booking process, resulting in a considerably better experience; up-front disclosure is now being provided to customers with respect to pricing throughout the booking process.

"53% of people abandon the purchase process at the point, where they're shown the final price, due to the fact that the price looks higher than what they thought they were getting. Customer perception has significantly improved, and we now have the top TrustPilot scores and top rating for our mobile apps."

The Company's strategy was to advertise low fares on Google, click-based advertising, banner ads, etc. but these fares would exclude fees. Further, customers would go through the entire booking process being shown this same rate, only seeing the true cost, including fees, when the time for payment came. As noted, 53% of customers would abandon the booking at that point alone -- even after having entered in traveler(s) information, credit card information, etc. Further, of those who would book, their booking was primarily a function of the sunk costs and the incremental time to re-book on a different platform overwhelming the customers' growing sense that they had been duped. This fostered resentment against the Company and a low repeat booking rate.

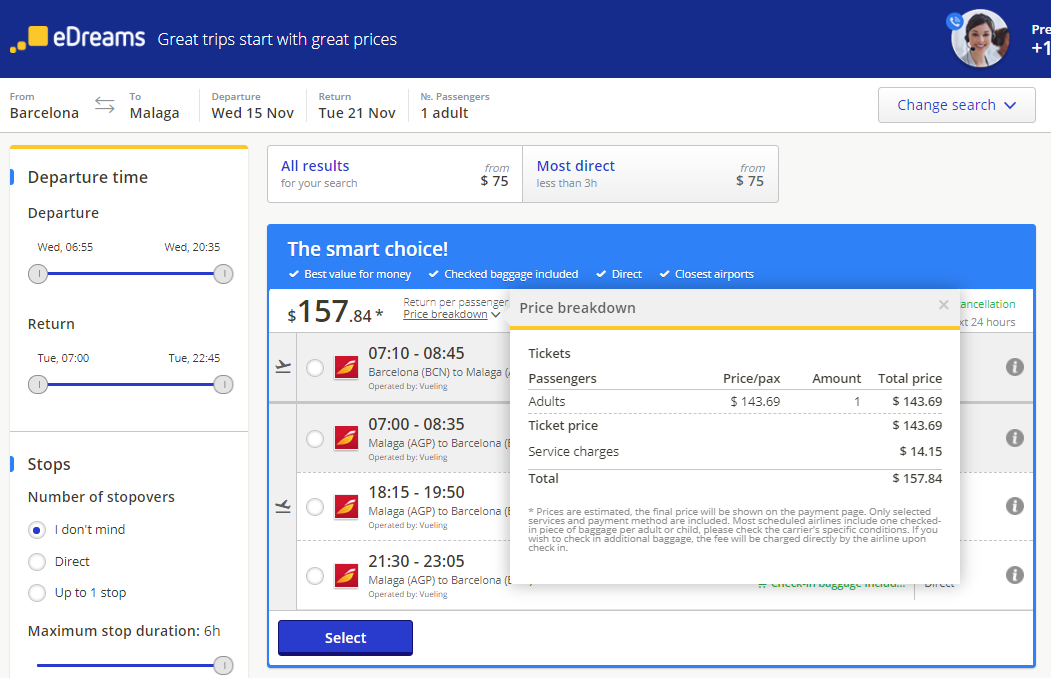

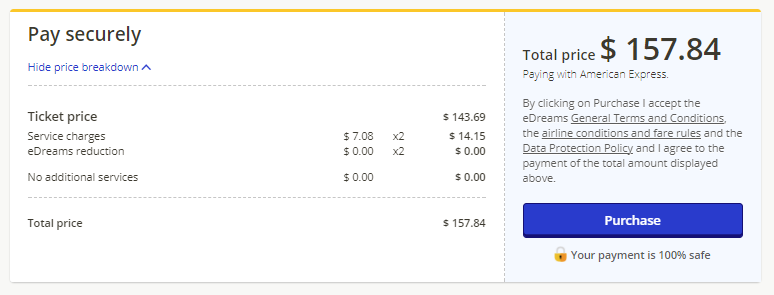

A simple visit to the site(s) will show that this is now the case. See the screenshots below displaying a flight from Barcelona to Malaga. At each point in the process, the true final price is disclosed, including a fee breakdown.

Search landing:

Final booking:

The Company has been working alongside various EU regulators as it rolls out more transparent pricing across its footprint. There are a few factors at play here: (1) given previous missteps, management is hesitant to make large changes all at once, (2) this is happening in the public markets, where “we’ve still got to meet guidance,” and (3) upstart competitors across Europe are utilizing the same techniques. Thus, the Company is working with regulators to “move the curve along” such that the Company can become more transparent while also not losing ground to competition.

As it currently stands, the transformation is complete at over 50% of the Company’s footprint and as of the US investor day in August, expect to be completed within the next 18-24 months. Management expects to give an update on this front on the Q2 2018 call in late November.

The success or failure of this revised strategy should be judged on the basis of (1) the number of inbounds and (2) the resulting conversion of those inbounds. As the Company has grown bookings for 10 straight quarters, the results are fair and ought to validate the current management team's strength and the shifting culture relative to history.

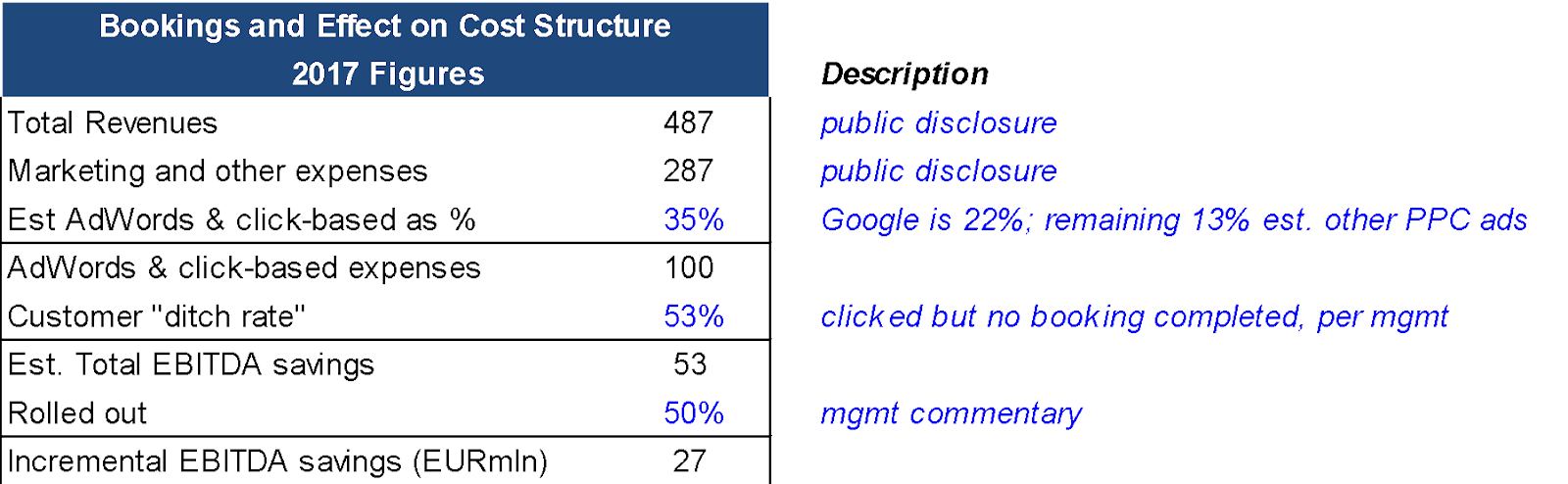

Further, this strategy has, and will continue to have, a tremendous positive effect on the cost structure, which we believe to be underappreciated by investors. Consider that "marketing and other operating expenses" ran €287mln in FY 2017, relative to €487mln in revenue. The Company spends on the higher end of OTA peers as a % of revenues. It’s our belief that simply bringing more discipline to the spend will result in noticeably improved margins.

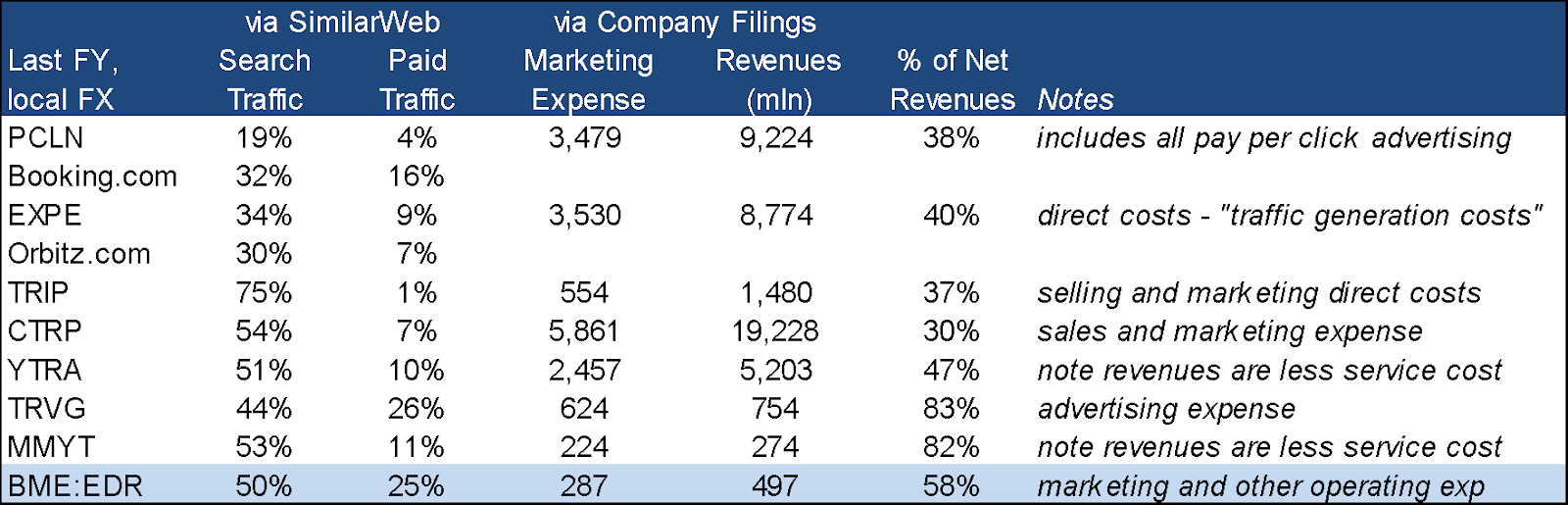

As AdWords now drives 22% of bookings (in line with 25% traffic quoted via SimilarWeb), we believe we conservatively assume that Google and other click-based advertising consists of 35% of these costs. These include banner ads and other pay-per-click advertising methods through which eDreams has been generating high priced, but low conversion leads.

eDreams was still previously paying a fee for each of these "leads" while only 47% of them ended up booking with the Company. If we assume that all of these customers who were drawn in with the low fee and then "ditched" upon seeing the final price instead are led to never click on the ad in the first place, then eDreams is no longer paying for those leads. As the Company has been working through this conversion process and is only ~50% rolled-out across the footprint, this has yet to fully show in headline results. As shown below, we estimate that this could drive incremental cost savings of €27mln per year. Given a 2018E FCF to equity of €69mln, this is a substantial figure.

This bring us into the mobile platform and flight updates, which has also improved significantly. As of Q4 2016,

"I would like to update you on a new eDreams mobile initiative. This is in fact one of the leading services in the world. It's a free service that notifies customers of travel updates such as gate announcements, baggage belt location via our app and thus enhancing the customer journey and making as easy for them as possible. This service is already tracking more than 90,000 flights per day and covers over 90% of passenger flights worldwide."

In November 2015 and November 2016, eDreams was named the best flight-booking website at the British Travel Awards. This is somewhat more than an ad hoc award; it is notable that the methodology for the award is completely in the hands of customers and the number of voters is well over 200,000, “ultimately it is the travelling public who decide the winners by voting for the travel companies they consider the best in the business.”

Mobile bookings represented just 15% of flight bookings in 2014, yet were 30% of bookings in 2017. Though over half of these mobile customers book using a web browser, mobile remains highly attractive from both an initial and ongoing acquisition cost perspective, as booking directly through the app avoids the use of AdWords or other click-based advertising. Incremental CAC on the app is zero, while the Company boasts a 40% repeat booking rate.

The Company offers a single sign-on such that one can save a trip on mobile and book through a desktop if preferable. Generally, lower-priced tickets are on mobile and higher-priced are booked on a desktop. eDreams has been selectively running promotions such as $20 off the first booking when booked through the app. eDreams has ~40 people working on mobile right now, and the Company's iOS app has improved from a 2.5-star rating to a 4.4-star rating today.

Phase II – accelerate transformation to build stronger customer-centric business (now; FY16-17)

Given the Company’s history, new management has sought to provide increased transparency with investors. It is now doing so by offering 5 key performance indicators (KPIs). We expect execution on these KPIs and further disclosures to act as catalysts.

1. Revenue diversification ratio: seeks to inform investors as to the breakdown of revenues by source. “Diversification revenues” are earned via commissions on dynamic packages (tours), cars, and hotels, relative to flights. This also includes add-ons such as trip insurance, which isn’t as widely offered among European airlines. This has expanded to 31% of total revenues as of Q1 2018.

2. Product diversification ratio: Represents the number of additional products sold as a percentage of total bookings. These products primarily include insurance, seats, bags, and dynamic packages. This figure has risen to 46% in Q1 2018 vs. 42% in 2017.

3. Acquisition cost per booking index: Represents customer acquisition cost. Q4 2015 acted as the baseline, which dropped to 78 in Q1 2018 and has been ~flat over the past three quarters.

4. Repeat booking: Represents the share of customers that have booked with eDreams in the past year. This has risen to 48% in Q1 2018.

5. Share of mobile bookings: Represents the share of bookings that are done through a mobile device. This has risen from 26% in Q1 2017 to 32% in Q1 2018.

Phase III – leverage market leadership with sustainable revenue model (FY18-20)

Phase III is expands upon the foundations built in Phase II by, “having a more diversified product portfolio and leveraging in full our large customer base, by consolidating the one-stop shop to the launch of new products, a growth platform that takes advantage of strongly favorable market trends and a significantly diversified business portfolio." Essentially, Phase III looks to continue to diversify the business away from the less sustainable areas in the past, specifically with respect to reliance on Google paid and straight fees to customers relative to other revenues. Phase III has begun in FY 2018.

The Company is significantly de-risking its financial leverage profile, which should continue to accrue to equity shareholders. European investors in particular are generally hesitant to invest in highly levered companies.

In September 2016, the Company received B and B2 credit ratings from S&P and Moody’s, with a stable outlook. This allowed the refinancing of the Company’s 2018 and 2019 notes outstanding in October 2016. The Company issued €435mln of 2021 notes, which allow for repurchases of up to 10% of principal per year. These 2021 notes have a coupon of 8.5%, but currently trade at a YTW of ~2.2%. Further, the covenant leverage cap was extended from 5.5x to 6.0x (net debt to LTM adjusted EBITDA) and the revolver was expanded to €147mln from €130mln.

Net leverage is down from 4.3x in December 2015 to 3.1x as of June 2017. Management’s public commentary shows a clear commitment to increased debt pay down., and the Company told us that they "plan to pay down as much debt as possible over the next 5 years."

Investor day, November 2016,

"We will continue to monitor the financial markets for future repurchase of our debt and to continue deleveraging."

Q3 2017 call, February 28, 2017,

"And we've said that with the excess cash flow that we generate on a yearly basis, we will continue with our strategy to manage the gross debt down and apply portions of our cash to reduce leverage."

The Company most recently redeemed €10mln of its 8.5% senior notes in September 2017. Management's intention is to go below 3.0x EBITDA which will improve business stability, but also as they see the leverage profile as the biggest "bottleneck" to a more robust valuation to the equity (in addition to a low float).

The Company is currently under-earning on their fixed cost base; incremental margins on top line growth should drive margin and free cash expansion.

G&A costs have been elevated as the company invests in alternative means that have gone to reducing reliance on Google paid (AdWords) as a lead source. These include affiliates, CRM, SEO, print campaigns, TV campaigns, YouTube, and digital. The Company invested significantly in digital, with “a significant push” from mid-2016 to mid-2017. Though this has weighed on short-term results, the long-run health of the Company is much stronger for it. Further, the Company's investment in mobile will prove to structurally reduce customer acquisition costs, as customers become loyal to the brand and specifically, the apps.

The Company is growing (organically) non-flight revenues at a faster rate than flight revenues, the former carrying a higher margin. From 2015 to 2016, lower margin flight revenue grew 5.5% while non-flight revenue, though consisting of just 20% of revenues, grew 9.6%. Further, in January 2017, the Company purchased Barcelona-based budgetplaces.com for a "mid-single digit figure in the millions of Euro." The site focuses on hotels rather than eDreams’s current flight focus, and processes 55,000 room nights per month at over 1,000 destinations worldwide. Though we don't estimate this will in itself be a tremendous growth factor, it is indicative of management's commitment to improving the business in this way.

From a strategic standpoint, eDreams is a collection of high quality assets that would be highly valuable to a potential acquirer.

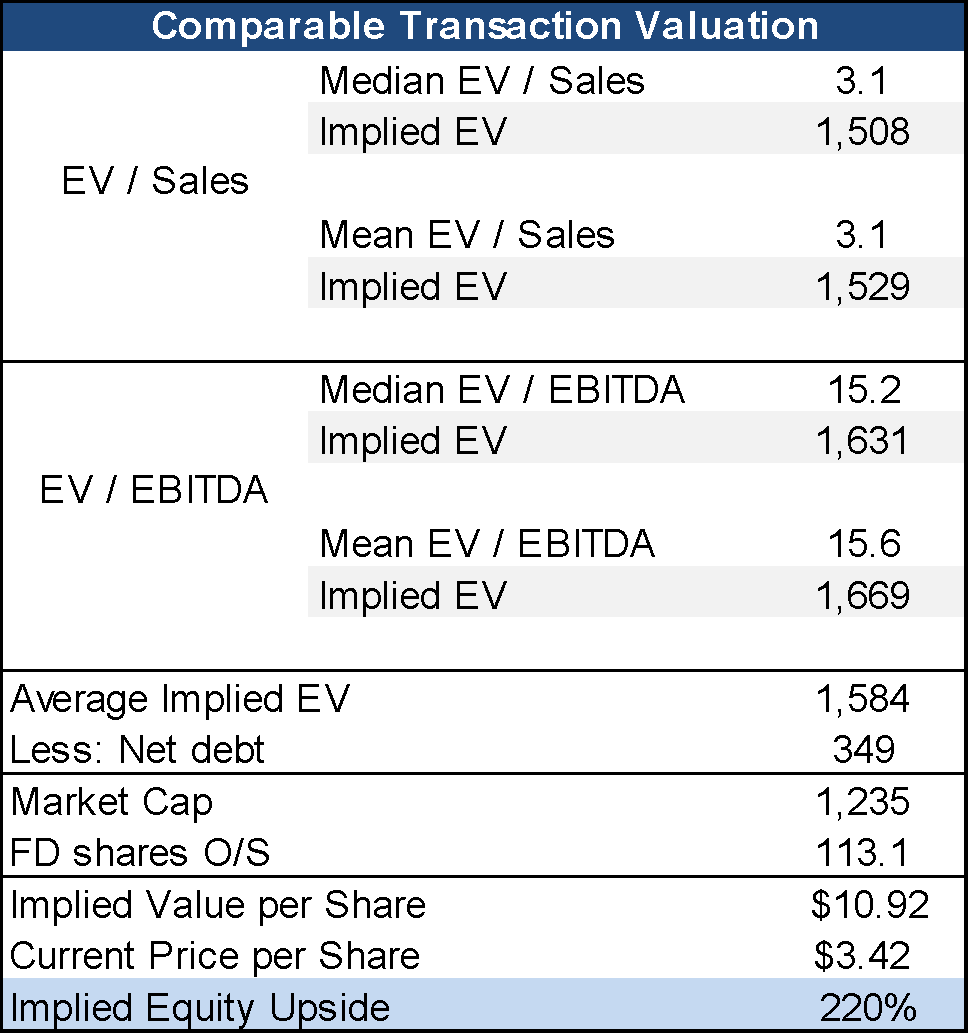

eDreams trades at ~7x EBITDA and ~1.4x revenue relative to peers who trade substantially higher on both metrics. Thus, a combination would be highly accretive to a potential acquirer, even before a consideration of cost synergies. There are numerous precedent transactions over the past several years in the space; applying median / mean deal multiples would result in over 200% upside to the equity.

eDreams has €274mln in NOLs that are worth ~€74.5mln per the Company’s given tax rates, though 50.3mln of these are unrecognized on the balance sheet. While international carryforwards never expire and the US carryforwards are good for the next 20 years, we estimate that the company can monetize essentially all of these carryforwards within the next 5 years. On a present value basis, this equates to €0.44 per share, or 13% of the current market capitalization. Further, this will aid in delivering the balance sheet and returning capital to shareholders on a rapid basis.

With the recent announcement of strategic alts, we believe Morgan Stanley would have no trouble finding a buyer at the current price.

See our M&A Event Upside Scenario and NOL valuation in the Valuation section below.

Valuation

Base Case

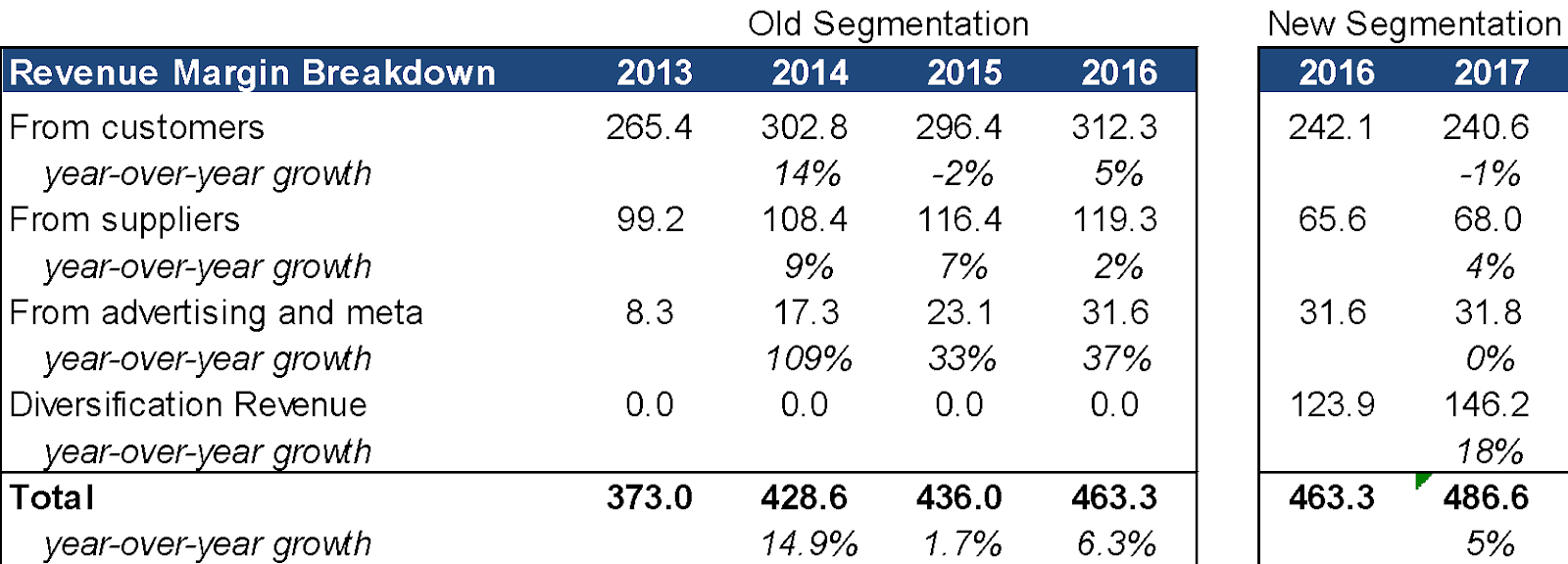

In the base case scenario, we assume meager top line growth of 3.0% through 2021. Revenue margin grew 15.0% in 2014, 1.7% in 2015, 6.3% in 2016, and 5.0% in 2017. Growth will be driven by an increasing number of bookings, and while revenue per booking will most likely continue to decline, this should be offset by increased diversification revenues, meta, and advertising.

Increased EBITDA will be driven by a slight increase in gross margin, though not especially material to our valuation. TripAdvisor and Priceline boast gross margins of 95% and 96%, respectively. More so, decreases in G&A (advertising) will drive margin expansion. In 2012 and 2013, the business spent 44.1% and 47.3% of sales on G&A, respectively, while in 2016, that figure was 64.6%. Capex should taper off as the business transition is completed and eDreams returns to a more capital-light model typical of OTAs.

At a 9x terminal year EBITDA of $114mln, we come to a €4.73 value per share. This implies a 2.0% perpetuity growth rate on FCF or an EV to Sales ratio of 1.70x.

Downside Case

The downside case portrays a scenario in which revenues meet the low end of expectations for 2018, with revenues falling by 3% in each year relative to consensus expectations of growth of 5.7% and 3.7%, respectively. Further, we see no gross margin expansion, and only slight EBITDA margin expansion due to decreased G&A costs. We also factor working capital as a cash flow headwind, and capex levels remaining elevated throughout the forecast period, resulting in worsening cash flow conversion.

We believe that in this scenario, equity downside would be capped by the extremely low resulting EV / Revenue multiple, which would be attractive to an acquirer. At 7x EBITDA or an implied 1.25x Sales, downside is 33%.

Upside Case – M&A Event

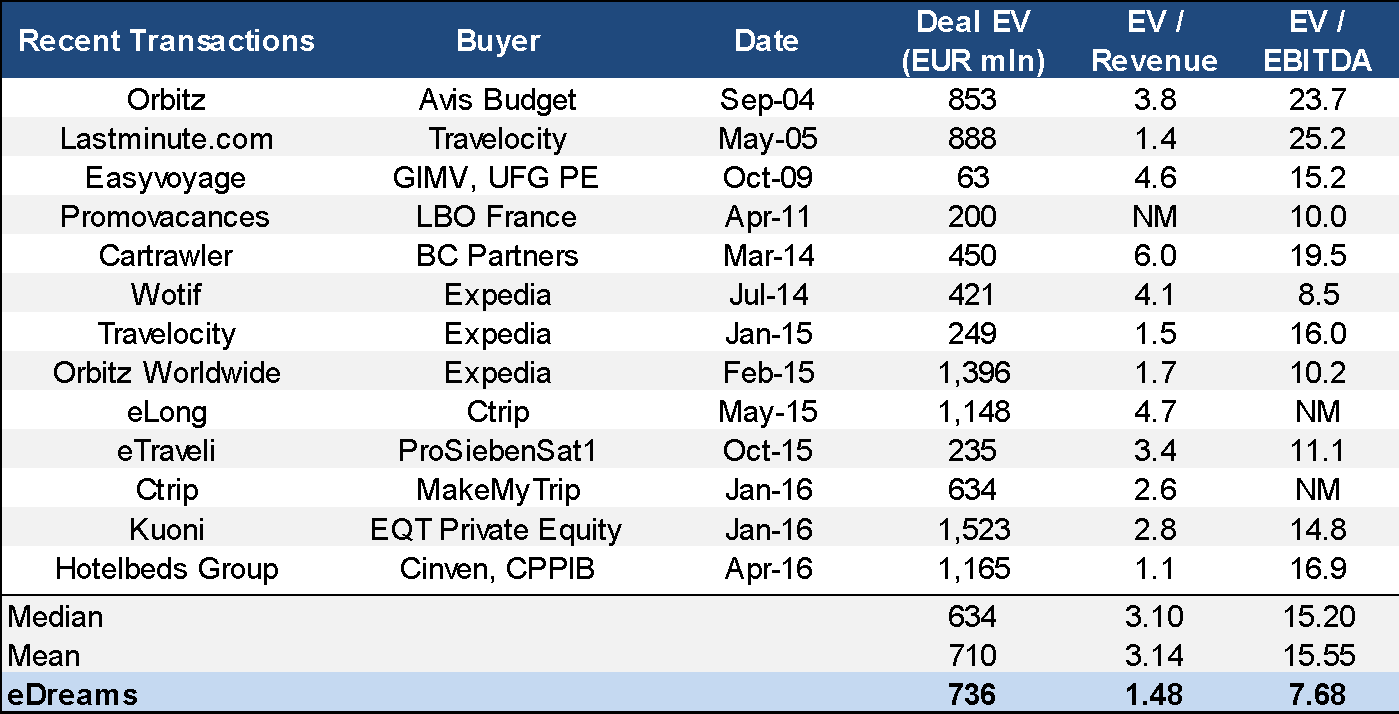

M&A in the OTA space has accelerated over the past 36 months. Comparable transactions are shown below.

Two key features of these deals that dispel the bear thesis are that they include (1) flight-focused OTAs and Hotel-focused OTAs, and (2) companies that generate similar levels of revenue, EBITDA, and that were consummated at comparable enterprise values. The median / mean EV to Revenue multiple was 3.10x / 3.14x and the median / median EV to EBITDA multiple was 15.2x / 15.6x. eDreams Currently trades at ~1.5x revenue and 6.9x EBITDA.

With Permira, Ardian, and HG Vora holding over 50% of shares outstanding, they would be inclined to support a bid for the business that would allow a swift exit. Ardian's AXA LBO Fund IV has exited every other portfolio company except for eDreams. As the Fund is a 2008 vintage and it is irregular for European PE shops to distribute shares to LP's, we believe they could seek a liquidity event and this is most likely a factor behind the strategic alts announcement.

Potential acquirers include Expedia, Priceline, Ctrip, TripAdvisor, Trivago, Google, Sabre, Travelport, Amadeus, and AirBnb, to name several. The Company could also be a PE target; note that management indicated the Company received interest from potential investors.

Per Skift in December of 2016 (at which point the Company traded at €3.15 per share),

"Based on eDreams Odigeo’s 2017 outlook of $481 million in revenue, Airbnb might be able to acquire the company for $1.9 to $2.8 billion or so."

Apparently, the Skift analyst was unware of the Company’s current valuation, but even at the low end this valuation represents multiples of the current share price. Though we don’t anticipate such a high multiple, it is indicative of the embedded value being currently unrecognized in the public markets that could be soon recognized through the strategic alts process.

Also note that sell-side analysts have surprisingly varied price targets on the stock. For example, Jefferies had a hold with a €1.75 price target based on "peer group P/E and PEG with a discount of 20%."

These examples again serve to demonstrate that eDreams has been orphaned by the sell-side community since the IPO blow-up, and the magnitude of changes that have occurred hasn’t been followed closely, if at all, thus leading to the price / value dislocation.

As a kicker, the Company holds tax loss carryforwards off the balance sheet which we estimate are worth €0.30 to €0.50 per share on a present value basis.

Risks & Mitigants

No deal consummated, deal consummated at a bad price, weak IRR if timeline is dragged out.

Regardless of a deal, the Company remains cheap as evidenced by a high-teens FCF yield while debt paydown should accrue to equity as a pseudo public LBO.

Conversations with management indicate that a process has been in the works for perhaps a few months. Management and the board seem frustrated by the lack of reaction in the public equity despite fundamental improvements. PE owners wouldn’t hesitate to accept a deal.

Disintermediation: metasearch and direct book

A fragmented flight industry increases the value proposition of OTAs relative to direct booking.

eDreams has a rapidly growing metasearch business that can be scaled profitably, though management maintains the position that OTAs are the better business to be in.

eDreams counts Google as a beta partner; the Company is one of just a handful who can do so.

European travel cycle, terrorism disruptions

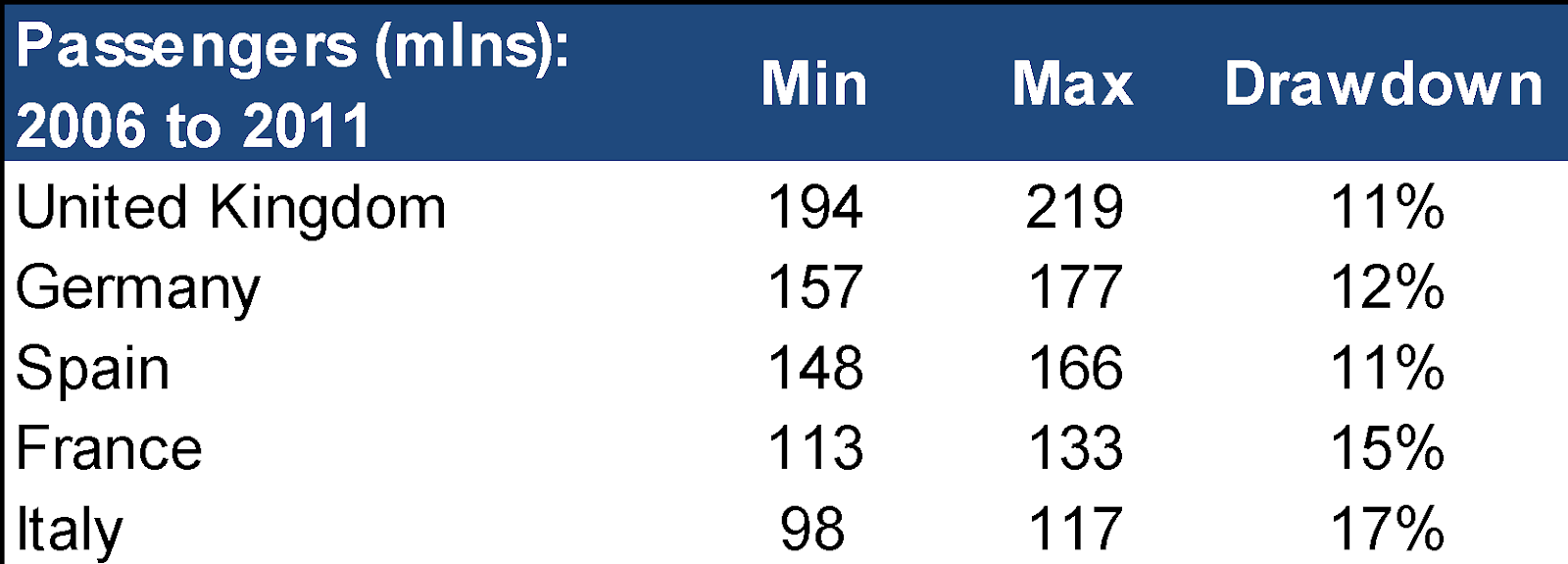

Through the GFC, passengers in top 5 European markets drew down in the teens.

In this scenario, the Company will be able to maintain positive free cash flow through the cycle as variable costs (Click-based ads, AdWords) come down with top line.

As eDreams is the largest player in the European space, a prolonged downturn should adversely affect competitors to a much greater extent. As a variety of these smaller competitors are less well capitalized and/or have weaker cost structures, the Company should be able to take share at an accelerated rate through the cycle.

Private equity owners selling

The more likely outcome, if they wanted to force an exit, would be to sell the entire business, which would most likely demand a substantially higher price than today.

Poor capital allocation

With a new management team and board members in place, the focus is on right-sizing and re-aligning the current business rather than growing via M&A as was Perez-Tenessa’s original intent. Dunne has demonstrated prudence thus far and we see no reason for this changing.

Financial leverage

The credit markets have demonstrated confidence as the 2021 bonds trade at a YTW of 2.2% on an 8.5% coupon.

The company believes they can pay down ~€40mln per year going forward. The Company most recently (September 2017) redeemed €10mln of its 8.5% notes.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

strategic alts

FCF growth + deleveraging

| show sort by |